Multivariate correlation analysis plays an important role in

various fields such as statistics, economics, and big data

analytics. In this paper, we propose a pair of measures, the

unsigned correlation

coefficient (UCC) and the unsigned incorrelation coefficient (UIC), to

measure the strength of correlation and incorrelation (lack of correlation)

among multiple variables. The absolute value of Pearson’s correlation coefficient is a special case of

UCC for two variables. Some important properties of UCC and UIC show that the proposed UCC and UIC are a pair of effective

measures for multivariate correlation. We also take the unsigned tri-variate correlation coefficient as an example to visually

display the effectiveness of the proposed UCC, and the geometrical explanation of UIC is also discussed.

All the properties and the figures of UCC and UIC show that the proposed UCC and UIC are the general measures of correlation for multiple variables.

Correlation analysis is a statistical subject which studies

linear relationship and the “strength” of linear relationship among

variables. It has been widely applied not only in statistics but

also in almost all fields of science [1].

The research on quantitative method of correlation is one of the main research strategies for

correlation analysis, in which the strength of correlation

among variables is measured by a correlation measurement. Pearson’s correlation coefficient is

a well-known bivariate correlation measurement.

For vectors and , let and be the means of the elements in and , respectively, let and be the variances of the elements in and , respectively, and let be the covariance between and . If is not zero, we call ‘a non-zero-variance vector’. Then for two non-zero-variance variables

and , Pearson’s correlation coefficient between them is defined as

(1)

where is the angle between the zero-mean variables of and . In this paper, we call the variable the zero-mean variable of , where is the vector with all ones. Pearson’s

correlation coefficient and its absolute

value can be used to measure the strength of

correlation between and . Let

be the angle between the zero-mean variables of and without considering

their directions, we have

and

The linear relation of the variables and then

can be completely determined by the angle . If

, and are linear

dependent; If , and are

perpendicular to each other and have the minimum correlation.

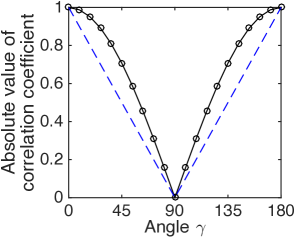

Figure 1: The curve of the absolute value of Pearson’s correlation

coefficient against the angle between two zero-mean

variables.

It shows the curve of against the angle within the intervals

in Figure 1, from which we can see that the absolute value of Pearson’s correlation coefficient is a good

bivariate correlation measurement for two reasons. Firstly, the curve of against the angle is always kept the opposite trend of change of the angle . Secondly, the strength of correlation measured by the absolute value of Pearson’s correlation coefficient (the black curve in Figure 1) is close to the strength of correlation measured by the angle (the blue dotted segments in Figure 1).

Pearson’s correlation coefficient can only describe the correlation

relationship between two variables. Lots of

applications, such as data dimensionality reduction, subset selection, and sparse regression, need a correlation measurement to

measure the strength of correlation among multiple variables.

These applications usually select several variables from a number of

variables to make the selected variables have the minimum

correlation while maintaining enough information.

The development of information technology and big data analytics further

increases the importance of multivariate correlation

analysis. Unfortunately, there is no compact formulation to define and measure correlation for multiple variables. People have to estimate the strength of multivariate correlation by the indirect methods such as the partial correlation and the coefficient of determination. However, for most systems, such as physical, sociological, and economic systems, it is more important to discover associations among more than two variables.

In this paper, an unsigned correlation coefficient (UCC) and an unsigned

incorrelation coefficient (UIC) are proposed.

The proposed UCC and UIC can be used to measure the strength of

multivariate correlation and linear irrelevance. Many

properties of them are introduced in the paper. For example, both

the proposed UCC and UIC belong to an interval [0,1]; The sum of the

squared UCC and the squared UIC of a group of variables is always 1; The

value of UCC for multiple non-zero-variance variables

achieves the maximum value 1 if and only if these variables are

linear dependent, and achieves the minimum value 0 if and only if

these variables are perpendicular to each other; The value of UCC

for a group of variables is not less than the value of UCC for part of them; If

the number of variables is the same as their dimension, their UIC

then equals to the absolute value of the determinant of the square

matrix whose row or column vectors are the standardized vectors of

these variables.

We also show that the value of UIC for multivate variables is the volume of the parallelotope formed by the standardized vectors of them. Then we visually display that the strength of correlation of three variables measured by the unsigned tri-variate correlation coefficient is very close to the strength of correlation measured by a spatial angle .

All the properties and the figures of UCC and UIC show that the proposed UCC and UIC are the general measures of correlation for multiple variables.

2. INNER PRODUCT-DETERMINANT EQUATION

If two non-zero-variance variables and are linear dependent, we have . Garnett had proved that if three non-zero-variance variables , , and are linear dependent, then [3].

For two variables and , we use to measure the strength of correlation between them. According to the above discussion, we analyze the relation of the strength of correlation among , , and with the value of .

According to Garnett’s conclusion, if and only if variables

, , and on the same plane. Moreover, it is obviously that if and only if variables

, , and are perpendicular to each

other. The two important properties of show that may be a proper measurement to measure the strength of correlation among three variables.

We denote by the standardized vector of

the non-zero-variance vector :

If and are the standardized

vectors of and , respectively, Pearson’s

correlation coefficient between and is then

the inner product between and , and can also be expressed by the inner product of and , the inner product of and , and the inner product of and .

Here we focus on an identical relation between inner

product and a determinant group, which we call the inner

product-determinant equation (IPD equation).

For -dimensional variables , , ,

and , , , , , , we denote

where .

According to Cauchy-Binet formula [4], we have the following

lemma:

Lemma 1 For -dimensional variables ,

, , and , , , , if

is the inner product matrix of these variables,

then we have

(2)

where .

Proof: According to Cauchy-Binet formula, for the matrixes

and

, we have

Because , this lemma is true.

We denote by the circular inner product

(3)

For a group of variables, all the permutations of them which can generate

the same inner product or circular inner product are regarded as the

same inner-product-permutation, then the inner product-determinant

equation can be rewritten as following:

Inner product-Determinant Equation For

-dimensional variables , , , and

, , the inner-product-determinant equation is

(4)

where runs through the list of all partitions of

, with only

consider the inner-product-permutation, and the subsets in each

partition are divided into three classes: If one subset only

contains one variable, then this subset belongs to the first class

, and the self-inner product of the variable appears in the

formula of the partition; If one subset contains two different variables, then

this subset belongs to the second class , and the square of

mutual inner product between the two variables appears in the

formula of the partition; The others belong to the third class

, and the circular inner product for each subset in

appears in the formula of the partition; The number of subsets in a

partition and are and , respectively.

Proof: In fact, each partition in the inner

product-determinant equation is corresponding to one item in the

expansion of the determinant of the inner product matrix. By

considering the inversion number and the symmetry of inner product

matrix, the above equation can be easily obtained.

If the number of subsets in each and are and , respectively, then

. Moreover, the subsets in are

not the standard sets because the inner-product-permutation is

involved.

The inner product-determinant equation has a set-partition-based

form, which is similar to the joint cumulant equation

[5, 6].

For three -dimensional variables , , and

, , there are 6 cases of inner products in total,

and they are , ,

, , ,

and . From Lemma 1, the IPD equation for three

variables can be obtained as following:

Corollary 1 For three -dimensional variables

, , and , , the inner

product-determinant equation is as following:

(5)

where .

Similarly, IPD equation for two variables is listed below.

Corollary 2 For two -dimensional variables

and , , the inner product-determinant

equation is

(6)

where .

3. CORRELATION MEASURES FOR MULTIPLE VARIABLES

According to Corollary 1, if , , and

are the standardized vectors of ,

, and , respectively, we have

(7)

Similarly, the square of Pearson’s correlation coefficient between

and can be obtained from Corollary 2:

(8)

Inspired by the above formulas of and

, we define the multivariate correlation

measurement as following:

Definition 1 For -dimensional non-zero-variance

variables , , , , , if is the standardized vector of

, , then the unsigned correlation

coefficient among

, , , and is defined as

(9)

where

and .

The sign of mutual direction for two variables can be judged by

whether the angle between the zero-mean variables of them is larger than . However, there is

no the mutual direction for multiple variables. Therefore, the

correlation measurement for multiple variables in this paper is defined as an unsigned value, the rationality of which is also discussed in Section 3 in this paper.

According to Definition 1, for two non-zero-variance

variables and , . Then we can see that the sum of the squares of the

determinant group is a coupling part of the proposed

UCC. We define the coupling part as the square of the unsigned

incorrelation coefficient (UIC), which can be used to measure linear

irrelevance among variables:

Definition 2 For -dimensional non-zero-variance

variables , , , , , if is the standardized vector of

, , the unsigned incorrelation

coefficient (UIC) among , , , and is

defined as

(10)

where and .

A lemma exists for UIC as following:

Lemma 2 For -dimensional variables ,

, , , , , if is the standardized vector of ,

, we have

(11)

where ,

, , , ,

, and is the number of

elements which are larger than in the set .

Proof: Let ,

, , , ,

, , and , , , ,

, , , , .

The first part can be rewritten as

and the second part can be rewritten as

Hence, we have

and can be expressed as

The proposed unsigned correlation coefficient and unsigned

incorrelation coefficient have some important properties,

several of which are discussed below.

Property 3.1

and are both the

symmetric functions of , , ,

.

Property 3.2 If and are

UCC and UIC for non-zero-variance variables

, , , , respectively,

and and

are

UCC and UIC for , , ,

, respectively, then

Property 3.2 can be directly obtained from Lemma 2. It shows that

the value of UCC for some variables is not less than the value of UCC for

part of the variables.

Property 3.3

Proof: According to Definition 2 we have . From Property 3.2, , . Because , we have .

Property 3.4 if and only if variables ,

and are linear dependent.

Proof:

Sufficiency: If , and

are linear dependent, , for all cases of , .

Necessity: We denote by the th column vector of

the matrix [, , ], .

Presume that exist to make rank,

then and

. Hence, the

presume is incorrect. We have rank if . Because the row rank equals to the column

rank of the same matrix, we have

For four variables , and

, let be Pearson’s

correlation coefficient between the variables and

, . Then , and are linear dependent if and only if

(12)

which is also kept the same with Garnett’s results [3].

Property 3.5 if and only if variables ,

and are perpendicular to each other.

Proof:

According to Properties 3.2 and 3.3, we can obtain

Hence, for arbitrary , we have

and .

Property 3.6 If variables

and are not linear dependent,

then gets the biggest

value 1 if and only if variable lies on the hyperplane

spanned by and ,

and gets the smallest

value if and only

if is perpendicular to the hyperplane spanned by

and .

Proof: The first half is true according to Property 3.4. Now we

prove the second part.

According to Lemma 2, we have

Denote the determinant as

Then we have

The first part of the above equation is a formula of the inner

product. The second part can be simplified as

Hence,

Then gets the

minimum value if

and only if

(13)

holds for all possible and .

Because variables

are not linear dependent, , }

exists to make the rank of equal to

. Then is an invertible matrix and

its adjoint matrix is also an invertible matrix. Each row of the

adjoint matrix of is just the linear

coefficients of one equation in the above equation. Finally, we

obtain .

According to Lemma 1 and Definition 2, if the number of variables is

the same as their dimension, we have the following corollary, which

gives a new explanation of determinant from the view of multivariate

correlation.

Corollary 3 For -dimensional non-zero-variance variables , and ,

if is the standardized vector of ,

, and , then we have

(14)

This corollary gives a new explanation of determinant that if the

row or column vectors of a matrix are all standardized, then the

absolute value of the determinant of the matrix depicts the linear

irrelevance of these standardized vectors.

Corollary 3 prompts us to consider the sign of the proposed UCC and

UIC. If UIC is defined by the determinant of when the

number of variables is the same as their dimension, the value of

UIC will have a positive or negative sign for a group of variables.

However, because the sign of the determinant of varies

with the order of these variable appeared in the matrix ,

it is meaningless to take time to decide which sign is better.

Moreover, the absolute value of correlation coefficient is more appropriate to measure the

strength of correlation.

Lastly, if the variables in the inner product matrix are

all standardized vectors, the inner product matrix is then transformed into

the correlation matrix. Correlation matrix is also a widely used

tool in various fields. For -dimensional non-zero-variance

variables , , , , , if is Pearson’s correlation

coefficient between and ,

, the correlation matrix of these

variables is as following:

in which the diagonal elements are all 1.

Then we have the following Multivariate correlation Theorem

from Lemma 1, Definition 1 and Definition 2:

Multivariate Correlation Theorem If

and

are the unsigned correlation coefficient and the unsigned incorrelation coefficient for -dimensional

non-zero-variance variables , ,

, and , respectively, then

(15)

Then according to the inner product-determinant equation, we have the UIC equation as following:

UIC Equation For

-dimensional non-zero-variance variables , , , and

, ,

(16)

where is the circular correlation coefficient, and , , , , and are kept the same meanings as that in the inner product-determinant equation in which the inner products are replaced by correlation coefficients.

4. VISUALIZATION ANALYSIS

Here we take the unsigned tri-variate correlation

coefficient as an example to visually display the proposed UCC and discuss its effectiveness.

4.1 Visualization of the Proposed

UCC

Figure 2: Some surfaces of the unsigned correlation

coefficient against the angles and with the other

angle fixed as , , , and ,

respectively.

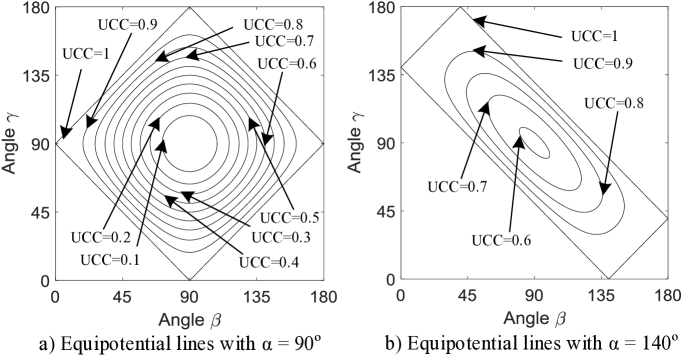

Figure 3: Some equipotential lines with different unsigned correlation coefficients

for three variables with fixed the angle and , respectively.

As shown in Fig. 1, we can easily show the effectiveness of Pearson’s correlation coefficient by a 2D graph. For UCC with more variables, it is impossible to visually display the relation among UCC and these spatial angles in a 2D or 3D graph. However, if one angle is fixed, then the relation of the other two

angles and , and the value of UCC among three variables can be visually display in a 3D graph. Four such

graphs are shown in Figure 2 with different fixed angles

, , , and ,

respectively. From Figure 2 we can see that these surfaces

have the similar structure but different depth, curvature, and top

rectangles.

4.2 Contour Line and Geometrical

Explanation of UIC

From Figure 2 we can see that a myriad of contour lines exist in

the surfaces. A simple example is that if the

pairwise angles for three variables , , and

are , , and , respectively, and the

pairwise angles for three variables , , and

are , , and , respectively, then the

three variables , , and and another three variables , , and

have the same value of UCC. Some equipotential lines for three variables

with the fixed angle equal to and are shown

in Figure 3.

In fact, the linear relation for multiple variables is closely tied

with the parallelotope in multi-dimensional space. For example, the

linear space structured by independent variables is the

-dimensional linear space, and the vector sum of the

variables is the diagonal of the parallelogram formed by these

variables in this -dimensional space.

Barth had proposed that the determinant of a Gram matrix is the

square of the volume of the parallelotope formed by the variables

[9], and the correlation matrix is a special Gram matrix.

According to Section 3 in this paper, the square of the proposed

unsigned incorrelation coefficient is the determinant of correlation

matrix. Hence, we have the following corollarys:

Corollary 4 If is the unsigned incorrelation coefficient among multiple

variables , , , , then

is the volume of

the parallelotope formed by the vectors ,

, , , where is the

standardized vector of .

Corollary 5 For spatial angles , the unsigned incorrelation coefficient is the

volume of the parallelotope formed by the unit vectors whose

pairwise angles are , , and ,

respectively.

According to Corollary 5, the equipotential lines on the UCC surface is

the equal-volume line for different spatial angles.

4.3 Effectiveness of the Proposed

UCC

Figure 4: A case of , and . , and are the angles between and

, between and , and between

and , respectively. .

Points C0 is the projection point of C on the plane spanned by and . COC0.

In Section 3, some important properties have shown that the proposed UCC and UIC are effective measures for correlation of multivariate variables. Here we visually verify the effectiveness of UCC for three variables.

The effective of Pearson’s correlation coefficient has been visually displayed in Figure 1, from which we can see that the strength of correlation measured by correlation coefficient is very close to the strength of correlation measured by the angle . In subsection 4.1, several 3D figures of the unsigned tri-variate correlation

coefficient with a fixed angle are provided, the effectiveness of which will be discussed here.

In fact, we can take this case of the unsigned tri-variate correlation

coefficient with a fixed

as that and are fixed and can be any vectors starting from O. Then the strength of correlation among , , and can be measured by the angle between and OC0, in which C0 is the projection point of C on the plane spanned by and .

We select three points A, B, and C on , and , respectively, to make . Let UCC and UIC among , and be and , respectively. According to Corollary 4 and Corollary 5, the volume of the parallelotope formed by , and their other nine parallel line segments is . Hence, we have

(17)

then

(18)

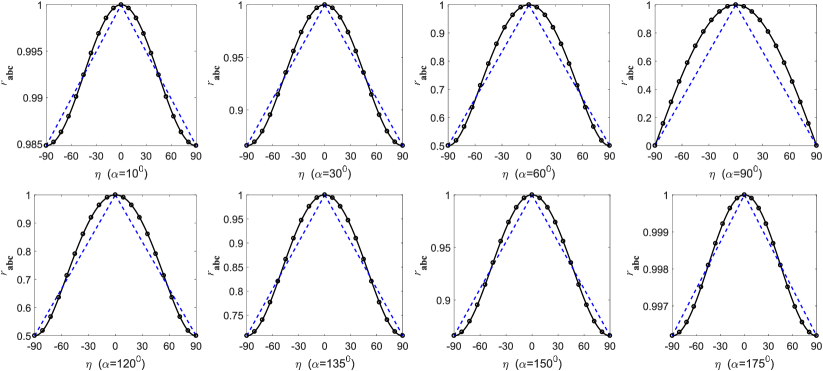

Then the curves of the unsigned tri-variate correlation

coefficient against the angle are depicted in Figure 5, from which we can see that the strength of correlation among , and measured by the unsigned tri-variate correlation coefficient (the black curves in Figure 5) is very close to the strength of correlation measured by the angle (the blue dotted segments in Figure 5).

Figure 5: The curves of the unsigned tri-variate correlation

coefficient against the angle . The angle is fixed with different values, and is COC0 in Figure 4.

5. CONCLUSION

References

[1]

Stigler, S. M. (1989), “Francis Galton’s Account of the Invention

of Correlation,” Statistical Science, 4, 73–79.

[2]

Dragomir, S. S. (1999), “A Generalization of Grüss’s Inequality

in Inner Product Spaces and Applications,” Journal of Mathematical Analysis and Applications, 237, 74–82.

[3]

Garnett, J. C. M. (1919), “On Certain Independent Factors in Mental

Measurements,” Proceedings of the Royal Society of London,

Series A, 96, 91–111.

[4]

Zeng, J. (1993), “A Bijective Proof of Muir’s Identity and the

Cauchy-Binet Formula,” Linear Algebra and its Applications,

184, 79–82.

[5]

Leonov, V. P. and Shiryaev, A. N. (1959), “On a Method of

Calculation of Semi-Invariants,” Theory of Probability &

its applications, 4, 319–329.

[6]

Hasebe, T. and Saigo, H. (2011), “Joint Cumulants for Natural

Independence,” Electronic Communications in Probability,

16, 491–506.

[7]

Wang, J. and Zheng, N. (2013), “A Novel Fractal Image Compression

Scheme With Block Classification and Sorting Based on Pearson’s

Correlation Coefficient,” IEEE Transactions on Image

Processing, 22, 3690–3702.

[8]

Kutner, M. H., Nachtsheim, C. J., Neter, J., and Li, W. (2005),

“Applied Linear Statistical Models,” 5th edition, New York:

McGraw-Hill.

[9]

Barth, N. (1999), “The Gramian and k-Volume in n-Space: Some

Classical Results in Linear Algebra,” Journal of Young

Investigators, 2.