A Distributed Approach for the Optimal Power Flow Problem Based on ADMM and Sequential Convex Approximations

Abstract

The optimal power flow (OPF) problem, which plays a central role in operating electrical networks is considered. The problem is nonconvex and is in fact NP hard. Therefore, designing efficient algorithms of practical relevance is crucial, though their global optimality is not guaranteed. Existing semi-definite programming relaxation based approaches are restricted to OPF problems where zero duality holds. In this paper, an efficient novel method to address the general nonconvex OPF problem is investigated. The proposed method is based on alternating direction method of multipliers combined with sequential convex approximations. The global OPF problem is decomposed into smaller problems associated to each bus of the network, the solutions of which are coordinated via a light communication protocol. Therefore, the proposed method is highly scalable. The convergence properties of the proposed algorithm are mathematically substantiated. Finally, the proposed algorithm is evaluated on a number of test examples, where the convergence properties of the proposed algorithm are numerically substantiated and the performance is compared with a global optimal method.

Index Terms:

Optimal power flow, distributed optimization, smart grid.I Introduction

The optimal power flow (OPF) problem in electrical networks determines optimally the amount of power to be generated at each generator. Moreover, it decides how to dispatch the power such that a global network-wide objective criterion is optimized, while ensuring that the power demand of each consumer is met and that the related laws of physics are held. Traditionally, the OPF problem has only been solved in transmission networks. However, the extensive information gathering of individual power consumption in the smart grid has made the problem relevant, not only in transmission networks, but also in distribution networks which deliver electricity to end users.

I-A Previous work

The problem was originally presented by Carpentier [1], and has been extensively studied since then and become of great importance in efficient operation of power systems [2]. The OPF problem is nonconvex due to quadratic relationship between the powers and the voltages and because of a lower bound on the voltage magnitudes. In fact, the problem is NP-hard, see [3]. Therefore, practical and general purpose algorithms must rely on some approximations or heuristics. We refer the reader to [2, 4] for a contemporary survey of OPF.

It is well known that the OPF problem is equivalently reformulated as a rank constrained problem [5]. As a result, classic convex approximation techniques are applied to handle nonconvexities of the rank constraint, which usually results in a semidefinite program [6] (SDP). SDP relaxations to OPF have gained a lot of attention recently, see [3, 7, 8, 9] and references therein. Authors in [3] show that SDP relaxation is equivalent to the dual problem of the original OPF. Moreover, sufficient conditions for zero duality and mechanisms to recover the primal solution by the dual problem are given. Thus, [3] identifies a class of OPF problems, where the global optimum is obtained efficiently by using convex tools. Some other classes of OPF problems, for which zero duality holds, are investigated in [7, 8, 9]. In particular, [7] derives zero duality results for networks that have tree topology where over satisfaction of loads is allowed. On the other hand, [8, 9] provide a graphically intuitive conditions for the zero duality gap for 2-bus networks, which are later generalized to tree topologies.

The references above suggest that the applicability of SDP approaches are limited to special network classes. Of course, SDP relaxations can always be used to compute a lower bound on the optimal value of the primal problem. However, in practice, what is crucial is a network operating point. In general, SDP relaxations fail to provide a network operating point (i.e., a feasible point) due to nonzero duality gap [10]. Another drawback of SDP based methods is that, even when zero duality holds, if the objective functions are non-quadratic, the dual machinery employed in constructing primal feasible solutions is not applied. Authors in [10, 11] explore limitations of SDP approaches and give practical examples where the sufficient conditions for zero duality does not hold.

Centralized methods for OPF problem, of course, exhibit a poor scalability. On the contrary, distributed and scalable OPF solution methods are less investigated, though they are highly desirable in the context of rapidly growing real world electrical networks. Unlike centralized methods, distributed OPF solution methods are also appealing in the context of privacy and security, because they do not entail collecting possibly sensitive problem data at a central node. In other words, when solving in a centralized manner the OPF problem in the smart grid, the power companies must rely on private information, such as the load profile of their costumers [12, 13], which might be of interest to a third party. For example, government agencies might inquire the information to profile criminal activity and insurance companies might be interested in buying the information to determine if an individual is viable for an insurance [14]. Therefore, gathering of private information at a centralized node has raised serious concerns about personal privacy, which in turn discourages the use of centralized approaches. Interestingly, the sparsity of most electrical networks brings out an appealing decomposition structure, and therefore it is worth investigating distributed methods for the OPF problem.

Distributed methods for the OPF problem are first studied in [15, 16, 17], where the transmission network is divided into regions and different decomposition methods, including auxiliary problem principle, predictor-corrector proximal multiplier method, and alternating direction method are explored to solve the problem distributively among these regions. The formulation is restricted to 2-region network decompositions and border variables cannot be shared among more than 2 regions. Another approach to decentralize the problem into regions is presented in [18, 19, 20] . The method is based on solving the Karush-Kuhn-Tucker (KKT) optimality conditions where a Newton procedure is adapted. The authors provide a sufficient condition for convergent which can be interpreted as a measurement of coupling between regions. However, when the condition is not satisfied they rely on the generalized minimal residual method to find the Newton direction, which involves a lot of communications between entities. Methods presented in [21] are limited to DC OPF.

More recent distributed algorithms are found in [22, 23, 24, 25, 26, 27, 28]. The decentralized methods in [22, 23, 24] capitalize on the SDP relaxation, which still has the drawbacks of being specific to special classes of networks and lack of flexibility with general objective functions. Another relaxation method is presented in [25], where instead of the original nonconvex constraint sets, the convex hull of those are used. However, the method can result in an infeasible point to the original unrelaxed problem, entailing local methods to help construct good local points. Other recent works consider distributed methods for optimal reactive power flow in distribution networks [26, 27]. Both papers first make approximations that yield a convex OPF problem and then distribute the computation by using dual decomposition [26] and ADMM [27]. The recent work in [28] employees ADMM to the general nonconvex OPF problem to devise a scalable algorithm. A major drawback of the method in [28] is that its convergence is very sensitive to the initialization. In fact, the authors of [28] always initialize their algorithm with a point which is close to the optimal solution. However, the optimal solution is not known a priori, limiting scope of the method.

Almost all the methods above can be classified as those which are general yet not scalable and those which are scalable yet not general. However, methods, which are simultaneously general and scalable are of crucial importance in theory, as well as in practice, and therefore deserve investigations.

I-B Our Contributions

The main contributions of this paper are as follows:

-

1.

We develop a distributed algorithm for the general nonconvex OPF problem. Our approach is not restricted to any special classes of networks, where zero duality holds. It also handles non-quadratic convex objective functions, unlike the SDP based distributed algorithms.

-

2.

We capitalize on alternating direction method of multipliers (ADMM) [29] to accomplish the distributed implementation (among electrical network buses) of the proposed algorithm with a little coordination of the neighboring entities. Thus, the proposed algorithm is highly scalable, which is favorable in practice.

-

3.

In the case of subproblems, we capitalize on sequential approximations, in order to gracefully manipulate the nonconvexity issues. The approach is adopted from an existing algorithm originally proposed in [30] in the context of centralized OPF problem.

-

4.

The convergent properties of the proposed algorithm are mathematically and numerically substantiated.

-

5.

A number of numerical examples are provided to evaluate the performance of the proposed algorithm.

I-C Organization and Notations

The paper is organized as follows. Section II describes the system model and problem formulation. The solution method is presented in Section III. In Section IV, we discuss some fundamental properties of the algorithm. Numerical results are provided in Section V. Finally, Section VI concludes the paper.

The imaginary unit is denote by , i.e., . Boldface lower case and upper case letters represent vectors and matrices, respectively, and calligraphic letters represent sets. The cardinality of is denoted by . len(x) denotes the length of . The set of real and complex -vectors are denoted by and , respectively, and the set of real and complex matrices are denoted by and . We denote the real and imaginary parts of the complex number by and , respectively. The set of nonnegative integers is denoted by , i.e., . The superscript stands for transpose. We use parentheses to construct column vectors from comma separated lists, e.g., . We denote the diagonal block matrix with on the diagonal by . The Hadamard product of the matrices and is denoted by . We denote by the -norm of the vector . We denote the gradient of the function in the point by .

II System model and Problem Formulation

Consider an electrical network with buses with denoting the set of buses and the set of flow lines. We let be the current injection and be the voltage at bus . Let and denote the complex power demand and the complex power generated by bus , respectively. Thus, the complex power injected to bus is given by .

For notational compactness, we let , , , , , , , , , , , and denote the vectors , , , , , , , , , , , and , respectively. We denote by the complex current and by the complex power transferred from bus to the rest of the network through the flow line . The admittance matrix of the network is given by

| (1) |

where is the admittance in the flow line , and is the admittance to ground at bus . We let and denote the real and imaginary parts of , respectively. In particular, and yielding .

II-A Centralized formulation

For fixed power demands, and , the goal of the OPF problem is to find the optimal way to tune the variables , , , , , , , , ensuring that the relationships among the variables are held and system limitations are respected. The objective function differs between applications. In this paper we consider the minimization of a convex cost function of real power generation. We denote by the cost of generating power at bus , where denotes the set of generator buses. The OPF problem can now be expressed as 111Formulation (2) is equivalent to the OPF formulation in [3], and one can easily switch between the two formulation by using simple transformations. We use formulation (2), because it is convenient, in terms of notations, when describing the contents in subsequent sections.

| min | (2a) | |||

| s. t. | (2b) | |||

| (2c) | ||||

| (2d) | ||||

| (2e) | ||||

| (2f) | ||||

| (2g) | ||||

| (2h) | ||||

| (2i) | ||||

| (2j) | ||||

| (2k) | ||||

| (2l) | ||||

where the variables are , , , , , , , , and , , , for . Here constraint (2b) is from that , (2c) is from that the conservation of power flow holds, (2d) is from that , (2e) is from that complex power is , and with and , and (2f) is from that and . Note that (2b)-(2f) correspond to the constraints imposed by the laws of physics associated with the electrical network. In addition, (2g)-(2l) correspond to the constraints imposed by operational limitations, where the lower bound problem data and the upper bound problem data determine the boundaries of the feasible regions of power, current, as well as voltages in the network. Note that if a bus is not a generator bus, then there is no power generation at that bus, and thus . Such situations can be easily modeled by letting

| (3) |

The constraints (2e), (2f), and (2l) are nonconvex, which in turn make problem (2) nonconvex. In fact, the problem is NP-hard [3]. Thus, it hinders efficient algorithms for achieving optimality. However, in the sequel, we design an efficient algorithm to address problem (2) in a decentralized manner.

II-B Distributed formulation

In this section, we derive an equivalent formulation of problem (2), where all the constraints except for a single consistency constraint are decoupled among the buses. In particular, the resulting formulation is in the form of general consensus problem [29, § 7.2], where fully decentralized implementation can be realized, without any coordination of a central authority. More generally, the proposed formulation can be easily adapted to accomplish decoupling among subsets of buses, each of which corresponds to buses located in a given area, e.g., multi-area OPF [15].

We start by identifying the coupling constraints of problem (2). From constraint (2b), note that the current injection of each bus is affected by the voltages of its neighbors and by its own voltage. Therefore, constraint (2b) introduces coupling between neighbors. To decouple constraint (2b), we let each bus maintain local copies of the neighbors’ voltages and then enforce them to agree by introducing consistency constraints.

To formally express the idea above, we first denote by the set of bus itself and its neighboring buses, i.e., . Copies of real and imaginary parts of the voltages corresponding to buses in is denoted by and , respectively. For notational convenience, we let and . We refer to and as real and imaginary net variables, respectively. Note that the copies of either the net variable or are shared among entities, which we call the degree of net variable or . The consistency constraints are given by

| (4) |

where is given by

| (5) |

Note that (4) ensures the agreement of the copies of the net variables and that, for any bus , either or is local in the sense that they depend only on neighbors.

The constraints (2b)-(2l) of problem (2) can be written by using local variables and . In particular, we can equivalently list them as follows:

| (6a) | ||||

| (6b) | ||||

| (6c) | ||||

| (6d) | ||||

| (6e) | ||||

| (6f) | ||||

| (6g) | ||||

| (6h) | ||||

| (6i) | ||||

| (6j) | ||||

| (6k) | ||||

where , , , , and , with the order kept preserved as in and . In addition, (or ) in constraint (6a) are obtained by first extracting the -th column of (respectively, ) and then extracting the rows corresponding to the buses in , where the order of the components are preserved as in and . In addition, and in constraint (6c) are given by

| (11) | ||||

| (16) |

Moreover, , and of constraints (6f)-(6k) are chosen in a straightforward manner [cf (2g)-(2l)].

Finally, for notational convenience, associated with each bus , we denote by

| (17) |

the local variables of bus , by the affine constraints (6a)-(6c), by the nonlinear equality constraint (6d), by the nonlinear equality constraint (6e), by the linear convex inequality constraints (6f), (6g), (6j), and by the nonlinear convex inequality constraints (6h) and (6i) as we will see next.222The functions and depend on , , , , , , and which are intentionally omitted for clarity and space reasons.

Now we can express the distributed formulation of problem (2) as

| min | (18a) | |||

| s. t. | ||||

| (18b) | ||||

| (18c) | ||||

| (18d) | ||||

| (18e) | ||||

| (18f) | ||||

where the variables are , , , , , , , , , , , , for and and . Note that (18f) establishes the consistency constraints [cf (4)], which affirms the consistency among neighbor voltages. The coupling in the original centralized formulation (2) has been subsumed in the consistency constraint (18f), which results in the form of general consensus problem [29, § 7.2], where decomposition methods can gracefully be applied.

III Distributed solution method

In this section, we present our distributed algorithm to the OPF problem (18). In particular, we use the ADMM method as basis for our algorithm development, where we have fast convergence properties, compared to the dual decomposition [29]. The use of ADMM method is promising in the sense that it works on many nonconvex problems as a good heuristic [29, § 9]. Once the solution method is established, we investigate the properties in Section IV.

III-A Outline of the algorithm

For notational simplicity, we let and denote and , respectively, for each . Moreover, we let denote . The ADMM essentially minimizes the augmented Lagrangian associated with the problem in an iterative manner. Particularized to our problem (18), The partial augmented Lagrangian with respect to the consistency constraints (18f) (i.e., ) is given by

| (19) |

where is dual variable associated with (18f) and is called the penalty parameter. Together with the separability of (19) among , steps of ADMM is formally expressed below.

Algorithm 1: ADMM for distributed OPF (ADMM-DOPF)

-

1.

Initialization: Set and initialize and .

-

2.

Private variable update: Set and . Each bus updates locally, where we let be the primal and dual (possibly) optimal variables achieved for the following problem:

min (20a) s. t. (20b) (20c) (20d) (20e) (20f) (20g) (20h) where the variables are , , , , , , , , , , , , and . We denote by the part of corresponding to .

-

3.

Net variable update: We let be the solution to the problem

(21) where the variable is .

-

4.

Dual variable update: Each bus updates its dual variable as

(22) -

5.

Stopping criterion: Set . If stopping criterion is not met go to step 2, otherwise stop and return .

The first step initializes the net and dual variables. In the second step each bus solves a nonconvex optimization problem in order to update its private variable (see Section III-B). In the third step the net variable is updated by solving the unconstrained quadratic optimization problem (21), which has a close form solution. The net variable update can be done in a distributed fashion with a light communication protocol (see Section III-D). The fourth step is the dual variable update, which can be done locally on each bus (see Section III-D). The fifth step is the stopping criterion. Natural stopping criterions include 1) running the ADMM-DOPF algorithm for a fixed number of iterations, 2) running the ADMM-DOPF algorithm till the decrement between the local- and net variables of each bus () is below a predefined threshold 3) running the ADMM-DOPF algorithm till the objective value decrement between two successive iterations is below a predefined threshold. In the sequel, we discuss in detail the algorithm steps (20)-(22).

III-B The subproblems: Private variable update

In this section, problem (20) is considered. Since Problem (20) is NP-hard, only exponentially complex global methods can guarantee its optimality. We capitalize on sequential convex approximations [31] to design an algorithm, which is efficient compared to global methods. Similar techniques are used in [30] for centralized OPF, which we use as basis for designing our subproblem algorithm.

We start by noting that constraints (20b), (20c), (20f), and (20g) are convex as opposed to constraints (20h), (20d), and (20e), which are clearly nonconvex. The idea is to approximate the nonconvex constraints.

In the case of (20h), we note that for any , the values of and represent a donut, see Fig. 1(a). In other words, the 2-dimensional set

is a donut, which is clearly nonconvex.

We approximate the nonconvex set by considering a convex subset of instead, which we denote by , see Fig. 1(b). To do this, we simply consider the hyperplane tangent to the inner circle of the donut at the point in Fig. 1(b). Specifically, given a point , is the intersection of and the halfspace

| (23) |

where

if and

if . In the case of nonlinear nonconvex constraints (20d) and (20e), we capitalized on the well known Taylor’s approximation. Specifically, given a point , we denote by the first order Taylor’s approximation of at . Similarly, we denote by the first order Taylor’s approximation of at . The approximation is refined in an iterative manner until a stopping criterion is satisfied.

It is worth noting that to construct the functions and one only needs the values of , where is the component of corresponding to . 333This follows directly from the definition of the first order Taylor approximation and equations (6a) and (6c).

By using the constraint approximations discussed above, we design a subroutine to perform step 2 of the ADMM-DOPF algorithm. The outline of this successive approximation algorithm is given as follows.

Algorithm 2: Subroutine for step 2 of the ADMM-DOPF

-

1.

Initialize: Given and from ADMM-DOPF th iteration. Set . For all , set and construct . Let and initialize .

-

2.

Solve the approximated subproblem:

min (24a) s. t. (24b) (24c) (24d) (24e) (24f) (24g) (24h) where the variables are , , , , , , , , , , , , and . The solution corresponding to the variable is denoted by and all the dual optimal variables are denoted by .

-

3.

Stopping criterion: If stopping criterion is not met, set , and go to step 2. Otherwise stop and return .

The initialization in the first step is done by setting , where is the component of corresponding to the variable . The rest of the vector is then initialized according to equations (6a)-(6e), which have a unique solution when is given. The second step involves solving a convex optimization problem and the third step is the stopping criterion. A natural stopping criterion is to run the algorithm till the decrement between two successive iterations is below a certain predefined threshold, i.e., for a given . However, since only depends on , the component related to , we use

| (25) |

where and are the components of and , respectively, corresponding to the variable and is a given threshold. Furthermore, we do not need to reach the minimum accuracy in every ADMM iteration, but only as the ADMM method progresses . Therefore, it might be practical to set an upper bound on the number of iterations, i.e

| (26) |

for some .

III-C On the use of quadratic programming (QP) solvers

Problem (24) can be efficiently solved by using general interior-point algorithms for convex problems. However, even higher efficiencies are achieved if problem (24) can be handled by specific interior-point algorithms. For example, if the objective function (24a) is quadratic, sophisticated QP solvers can be easily employed. See the appendix for the detail.

III-D Net variables and dual variable updates

Note that the net variable is the unique solution of the unconstrained convex quadratic optimization problem (21), and is given by

| (27) | ||||

| (28) | ||||

| (29) | ||||

| (30) |

where (27) follows trivially from the differentiation of the objective function of problem (21), (28) follows by invoking the optimality conditions for problem (21), i.e., , (29) follows from that , and (30) follows from that . From (30), it is not difficult to see that any net variable component update is equivalently obtained by averaging its copies maintained among the neighbor nodes. Such an averaging can be accomplished by using fully distributed algorithms such as gossiping [32]. Therefore, step 3 of ADMM-DOPF algorithm can be carried out in a fully distributed manner.

The dual variable update (22) can be carried out in a fully distributed manner, where every bus increment the current dual variables by a (scaled) discrepancy between current net variables and its own copies of those net variables.

IV Properties of the distributed solution method

Recall that the original problem (2) or equivalently problem (18) is nonconvex and NP-hard. Therefore, ADMM based approaches are not guaranteed to converge [29, § 9], though general convergence results are available for the convex case [29, § 3.2]. Nevertheless, in the sequel, we highlight some of the convergence properties of our proposed ADMM-DOPF algorithm. In particular, we first illustrate, by using an example, the possible scenarios that can be encountered by Algorithm 2, i.e., step 2 of the ADMM-DOPF algorithm. Then we capitalized on one of the scenario, which is empirically observed to be the most dominant, in order to characterize the solutions of the ADMM-DOPF algorithm.

IV-A Graphical illustration of Algorithm 2

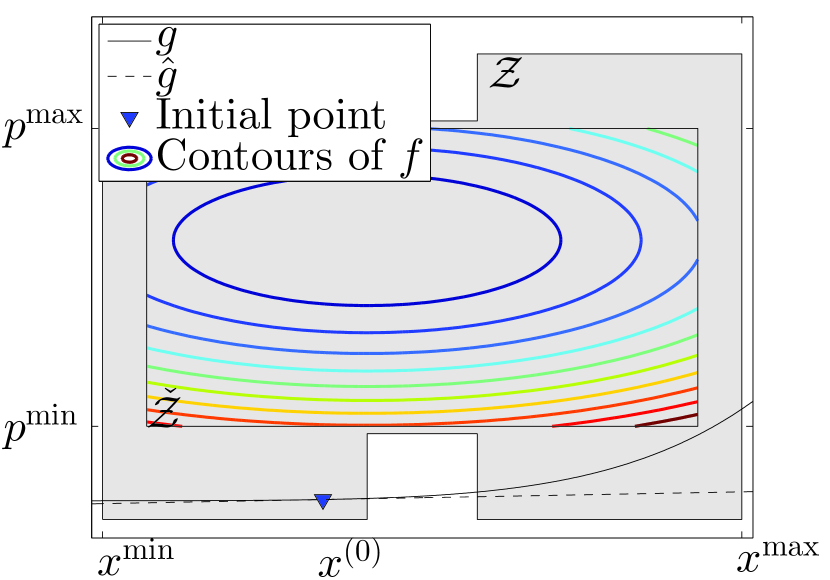

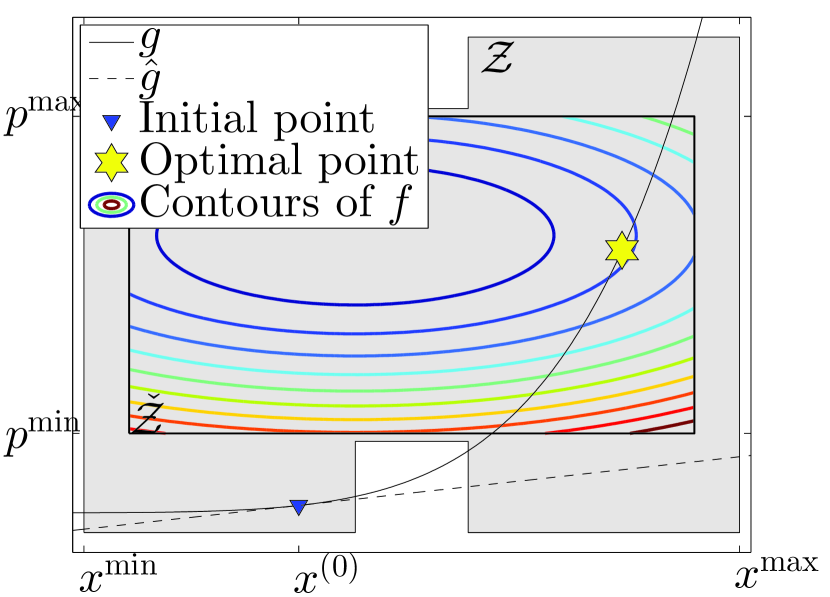

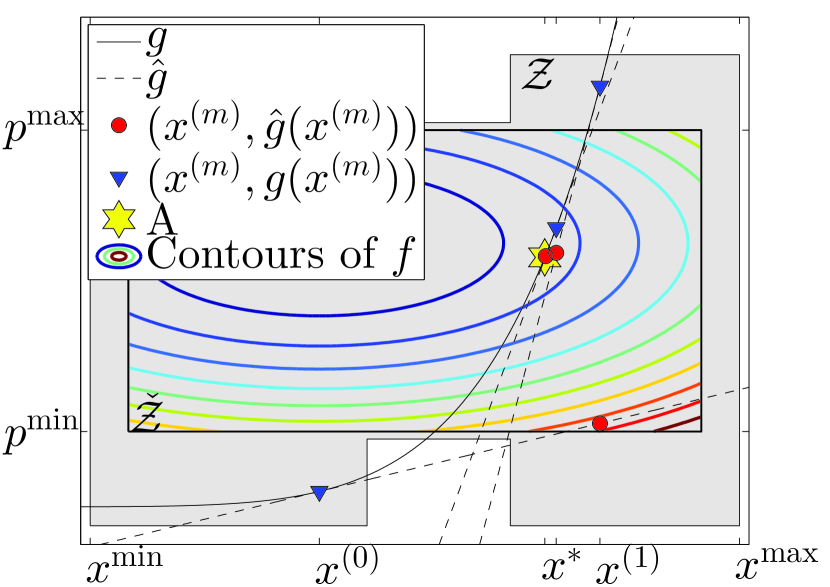

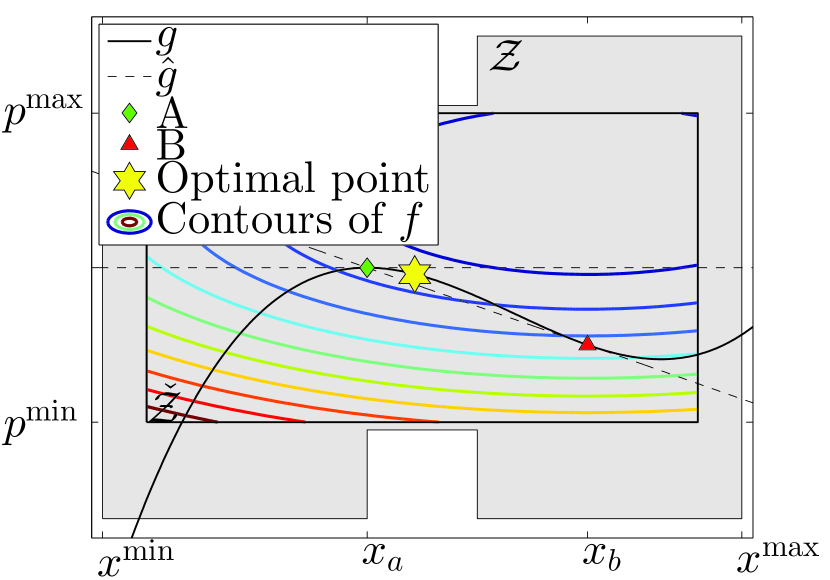

We start by focussing on the step 2, the main ingredient of ADMM-DOPF algorithm. To get insights into the subroutine (i.e., Algorithm 2) performed at step 2, we first rely on a simple graphical interpretation. Here instead of problem (20), we consider a small dimensional problem to built the essential ingredient of the analysis. In particular, we consider the convex objective function in the place of (20a). Moreover, instead of the nonconvex constraints (20d) and (20e) [cf (6d),(6e)], we consider the constraint

| (31) |

where is a nonconvex function, which resembles righthand side of (6d) and (6e). Finally, instead of the remaining constraints (20b), (20c), (20f), (20g), and (20h) of problem (20), we consider the constraint

| (32) |

where is not a convex set [cf (20h)]. Thus the smaller dimensional problem, which resembles subproblem (20) is given by

| (33) |

where the variables are and . Recall that Algorithm 2 approximates nonconvex functions in constraints (20d) and (20e) of problem (20) by using their first order Taylor’s approximations [see (24d),(24e)] and the nonconvex constraint (20h) by using a convex constraint [see (24h)]. Particularized to the smaller dimensional problem (33), the approximations pointed above equivalent to replace by its first order Taylor’s approximation and to approximate by some convex set , where . The result is the approximated subproblem given by

| (34) |

where the variables are and and represents the point at which the first order Taylor’s approximation is made.

Let us next examine the behavior of Algorithm 2 by considering, instead of problem (24), the representative smaller dimensional problem (34). Recall that the key idea of Algorithm 2 is to iteratively refine the first order Taylor’s approximations and [see step 2,3 of Algorithm 2], until a stopping criterion is satisfied. This behavior is analogously understood from problem (34), by iteratively refining the first order Taylor’s approximation of .

Fig. 2 illustrate sequential refinement of , where the shaded area represents the set , rectangular box represents the convex set , the solid curve represent function , dotted curves represents sequential approximations , and thick solid curves represents the contours of . Note that there are several interesting scenarios, which deserve attention to built intuitively the behavior of Algorithm 2, see Fig. 2(a)- 2(d).

Fig. 2(a) shows the first scenario, where an improper approximation of set makes the approximated problem (34) infeasible, irrespective of the choice of . In contrast, Fig. 2(b) depict a scenario, where an improper choice of the approximation point makes the approximated problem (34) infeasible. Fig. 2(c) shows a sequence of approximations, which eventually converges to a desired point ‘A’ that would have obtained without having the first order Taylor’s approximations on . Finally, Fig. 2(d) shows a scenario, where a sequence of approximations switch between two points ‘A’ and ‘B’, i.e., there is no convergence. Any other scenario can be constructed by combining cases from Fig. 2(a)- 2(d).

Analogously, the discussion above suggests that the approximation points [cf ] used when constructing and [cf ] and the approximations used in the set [cf ], can heavily influence the performance of Algorithm 2. Therefore, especially if the scenario 1 and 2 depicted in Fig. 2(a) and Fig. 2(b) occurs, during the algorithm iterations, they have to be avoided by changing the initializations. However, extensive numerical experiments show that there are specific choices of and can make Algorithm 2 often converge to a point as depicted in Fig. 2(c) and barely encounters the scenarios depicted in Fig. 2(a), Fig. 2(b), and Fig. 2(d) see Section V-A for details.

IV-B Optimality properties of Algorithm 2 solution

Results obtained in this section are based on the empirical observations (see § V) that scenario 3 depicted in Fig. 2(c) is more dominant compared to others. In particular, we make the following assumptions.

Assumption 1

For any , there exists , to which Algorithm 2 can converge. Specifically, there exists , where for all . In addition, for all , the components of , strictly satisfy the constraint (24h).

Under Assumption 1, the following assertion can be made:

Proposition 1

Suppose Assumption 1 holds. Then the output of Algorithm 2 satisfy Karush-Kuhn-Tucker (KKT) conditions for problem (20).

Proof:

See Appendix B-A. ∎

IV-C Optimality properties of ADMM-DOPF solution

As we already pointed out, there is no guarantee that the eventual output of ADMM-DOPF is optimal, or even feasible to the original problem (18), because the problem is NP-hard. However, Proposition 1, asserts that the eventual output of Algorithm 2 is a KKT point for problem (20) solved at step 2 of ADMM-DOPF. One can easily relate this result to characterize properties of of ADMM-DOPF output, as we will see later. However, the properties of the remaining output is still to be investigated. In this section, combined with the results of Proposition 1, we analyze the optimality properties of ADMM-DOPF output.

To quantify formally the optimality properties of ADMM-DOPF, we rely on the following definition:

Definition 1 ()-KKT optimality)

Consider the possibly nonconvex problem of the form

| (35) |

where is the objective function, are the associated inequality constraint functions, and are the equality constraint functions, and is the optimization variable. Moreover, let denote the dual variable associated with constraint , and denote the dual variable associated with constraint and , respectively. Then an arbitrary point is called )-KKT optimal, if

| (36) | ||||

| (37) | ||||

| (38) | ||||

| (39) | ||||

| (40) |

| (41) |

Note that (36)-(41) are closely related to the well known KKT optimality criterions, see [6, § 5.5.3]. It suggest that smaller the and , better the point to its local optimality. We use Definition 1 to formally analyze the optimality properties of ADMM-DOPF as discussed in the sequel.

Recall that, we have used to denote the vector of all the local primal variables in (17), to denote the vector of all net variables, to denote the dual variables associated with constraints (18b)-(18e), and finally to denote the dual variables associated with constraint (18f).

Let us assume that at the termination of ADMM-DOPF, the output corresponding to and is and , respectively. The output of ADMM-DOPF corresponding to and are simply the output of Algorithm 2 given by and . However, unlike in convex problems, in the case of problem (18), one cannot take as granted that the consistency constraint (18f) is satisfied (cf [29, § 3.2.1]). In particular, does not necessarily hold when , where and is the ADMM-DOPF iteration index. However, appropriate choice of the penalty parameter in the ADMM-DOPF algorithm usually allows finding outputs, where the consistency constraints are almost satisfied with a small error floor, which is negligible in real practical implementations as we will see empirically in § V. For latter use, let us quantify this error floor from , i.e.,

| (42) |

Now we can formally establish the optimality properties of ADMM-DOPF as follows:

Proposition 2

Given Assumption 1 holds, the output at the termination of ADMM-DOPF is -KKT optimal, where , is the penalty parameter used in the ADMM-DOPF iterations, and , are normalization factors.

Proof:

See appendix B-B. ∎

We note that deriving an analytical expression of by using problem (18) data is very difficult. However, we can numerically compute and given in Proposition 2 as

| (43) |

Extensive numerical experiences show that we usually have very small values for . For example, for all considered simulations with [see § V], we have on the order of (or smaller) and on the order of (or smaller) after 5000 ADMM-DOPF iterations.

V Numerical results

In this section we present numerical experiments to illustrate the proposed algorithm. We compare our algorithm with the branch and bound algorithm [11], centralized OPF solver provided by Matpower [33], and the SDP relaxation from [3]. In order to study the convergence properties of the algorithm we evaluate it on four examples that have a (non-zero) duality gap, see Table I, rows 1-4. These four examples come from [10, 11] and are obtained by making a small modification, see Table I, column 3. It is worth noting that the methods based on the SDP relaxation do not apply here due to nonzero duality gap [10]. Moreover, to study the scalability properties of the proposed algorithm, we also evaluate it on two larger examples, see Table I, rows 5-6. The exact specifications of considered examples, such as the objective functions and admittance matrices, are found in Table I and references therein.

| Original Problem | Modification | # G | # L | FL | |

| 3 | 3bus [10] | MVA | 3 | 3 | (2j) |

| 9 | Case9 [33] | MVAr, | 3 | 3 | None |

| , | |||||

| 14 | IEEE14 [34] | MVAr, | 5 | 11 | None |

| 30 | IEEE30 [34] | 6 | 21 | None | |

| 118 | IEEE118 [34] | None | 54 | 99 | None |

| 300 | IEEE300 [34] | None | 69 | 201 | None |

The units of real power, reactive power, apparent power, voltage magnitude, and the objective function values are MW, MVAr, MVA, p.u. (per unit) 444 The voltages base is 400 kV. , and $/hour, respectively. In all 6 problems the average power demand of the loads is in the range 10-100 MW and 1-10 MVAr, for the real and reactive powers, respectively.

The simulations were executed in a sequential computational environment, using matlab version 8.1.0.604 (R2013a) [35]. The convex problem (24) is solved with the convex solution method presented in Section III-C together with the built in matlab QP solver quadprog. As a stopping criterion for Algorithm 2 we use and , unless stated otherwise . For the ADMM method we use and as an initial point.

V-A Properties of Algorithm 2

In this subsection we investigate the convergence properties of Algorithm 2. In particular, we relate the convergence behavior of Algorithm 2 to the analysis in Sections IV-A and IV-B, where 4 scenarios, or possible outcomes, of Algorithm 2 [Fig. 2] were identified.

During the numerical evaluations, Algorithm 2 was executed 11060000 times. Scenarios 1 and 2 [Fig. 2(a) and 2(b), respectively], where the approximated subproblem is infeasible, occurred only 6 times (). These occurrences happened at one of the buses in the 300 bus example, during ADMM iterations 137-143. This suggests even if a particular bus fails to converge with Algorithm 2 in consecutive ADMM iterations, the bus can recover to find a solution in latter ADMM iterations.

To numerically study the occurrences of Scenarios 3 and 4, we run Algorithm 2 with 1) , 2) , and 3) . In all considered cases, we use [compare with (25)]. The following table summarizes how frequently the stopping criteria (26) of Algorithm 2 is met.

| max_iter | ||||

|---|---|---|---|---|

Note that the entries of Table II suggest an upper bounds on the frequencies of Senario 4. Therefore, Table II shows that the frequencies of the Scenario 4 is decreasing (or unchanged) as max_iter is increased. However the effects are marginal as indicated in the table, specially for . On the other hand, recall that , i.e., the decrement of voltages between two successive iterations is below [compare with (25)]. Such an infinitesimal accuracy in the stopping criteria (25) suggests the algorithm’s convergence, see Scenario 3, Fig. 2(c). For example, consider the case and in Table II. From the results, the frequency of termination of Algorithm 2 from the stopping criteria (25) (i.e., Scenario 3) become . Thus, from Proposition 1, it follows that when , of the cases Algorithm 2 converges to a point satisfying the KKT conditions. It is worth noting that for all the considered cases the convergence of the algorithm is in the range -. Results also suggest that the convergence properties of Algorithm 2 can be improved (see the case ) or remain intact (see the cases , , , , and ) at the expense of the increase in max_iter.

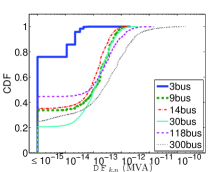

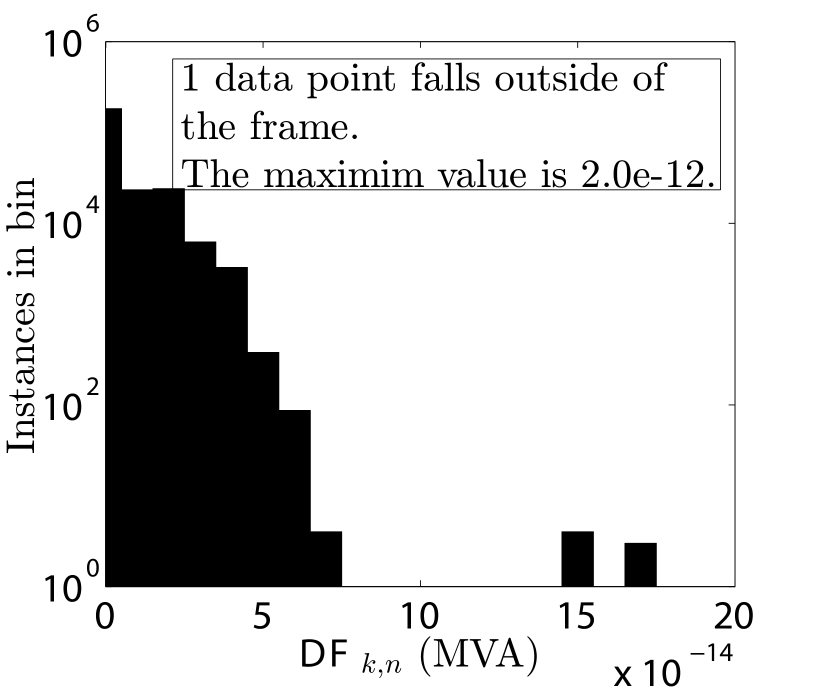

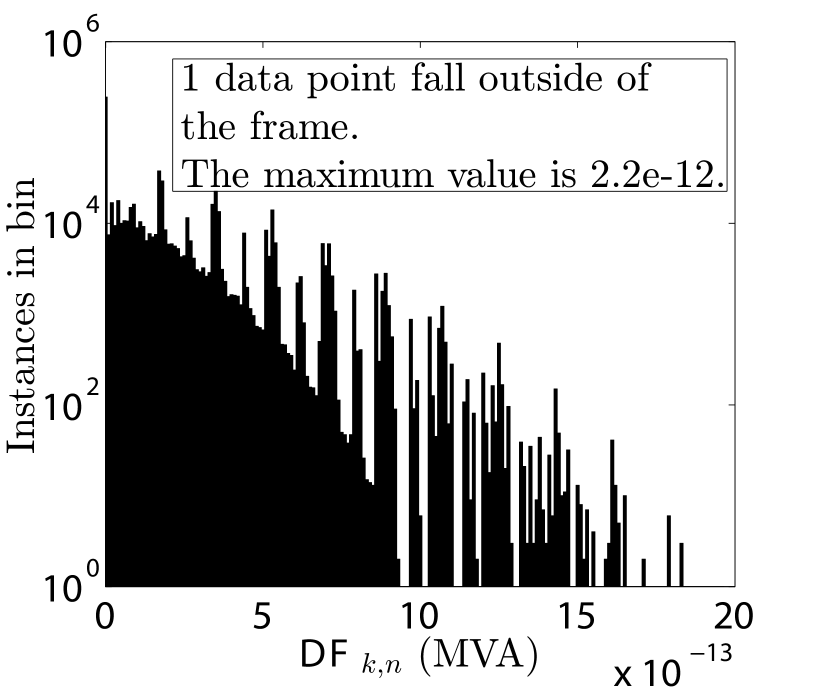

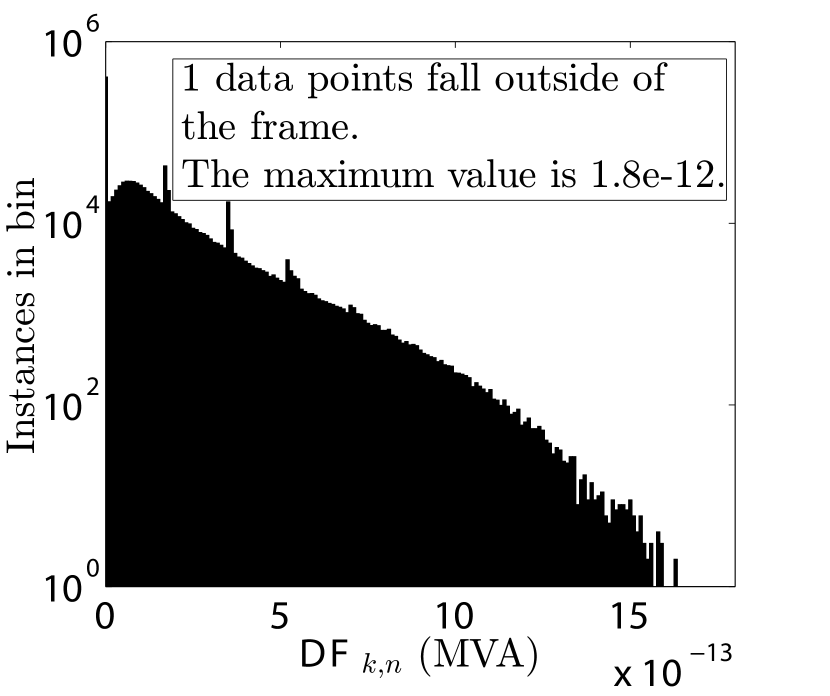

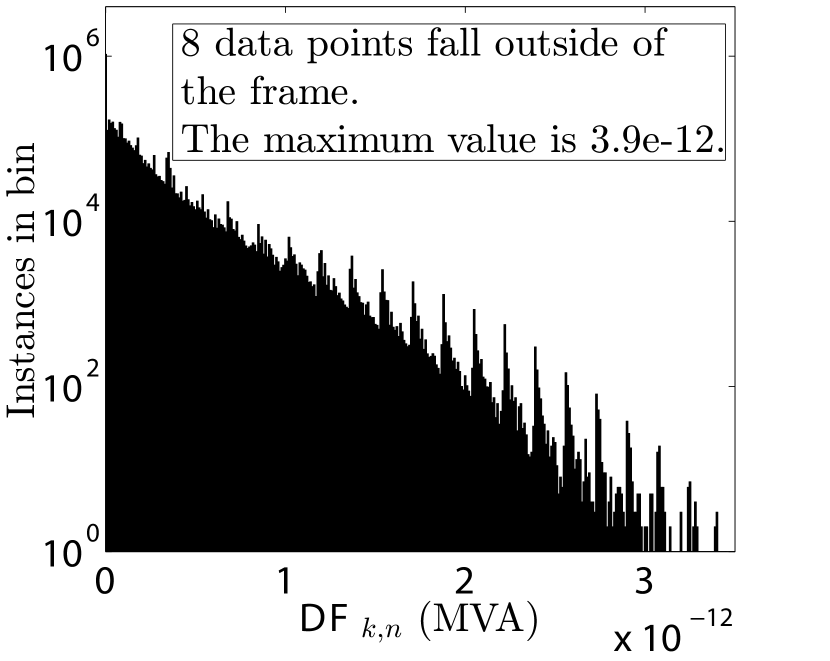

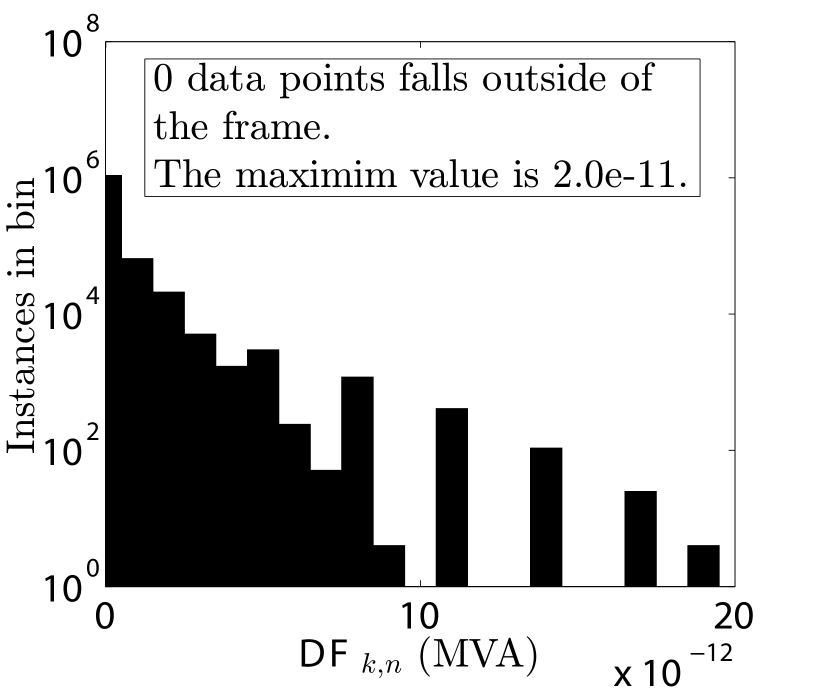

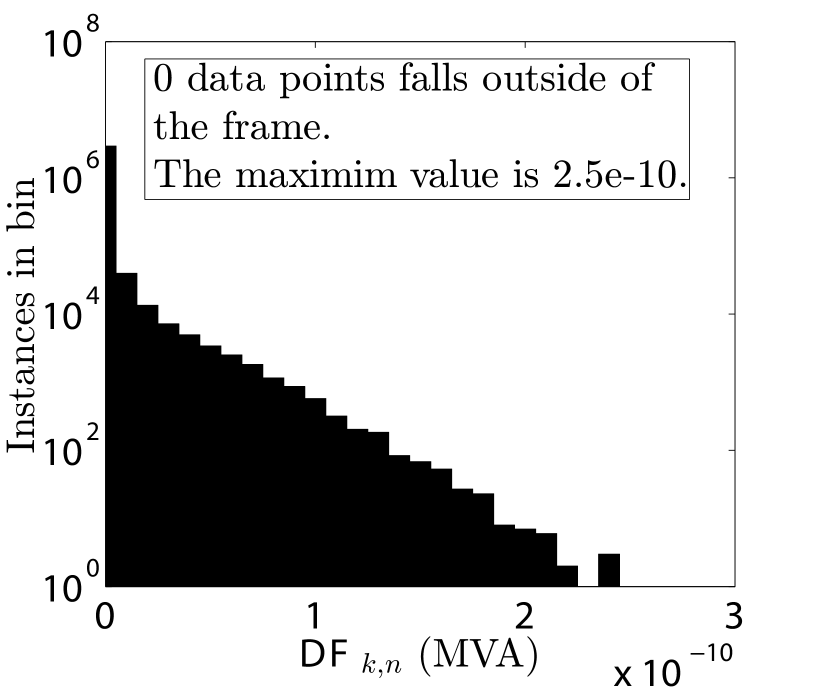

Note that the voltages returned by Algorithm 2 are always feasible to problem (20), i.e., satisfies (20h). However, the resulting power injections might be infeasible, [compare with (20c)-(20g)]. To measure the feasibility of the returned power injections of Algorithm 2, we define the following metric called the degree of feasibility (DF):

| (46) |

where and indicate the bus and ADMM iteration, respectively, is the returned power injection, and

| (47) |

The unit of measurement for is MVA. In order to provide a statistical description of for every execution of Algorithm 2, we consider an empirical cumulative distribution function (CDF) [Fig. 3] and a histogram [Fig. 4], for each example separately. These results suggest that Algorithm 2 returns a feasible solution with high accuracy in all cases, where the worst case accuracy is .

As a consequence of this promising behavior of Algorithm 2, we will proceed under Assumption 1.

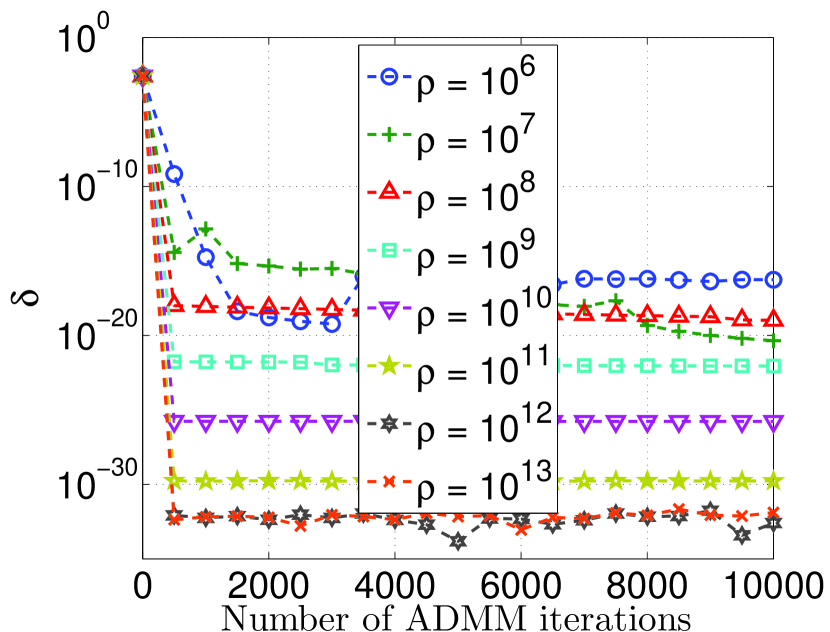

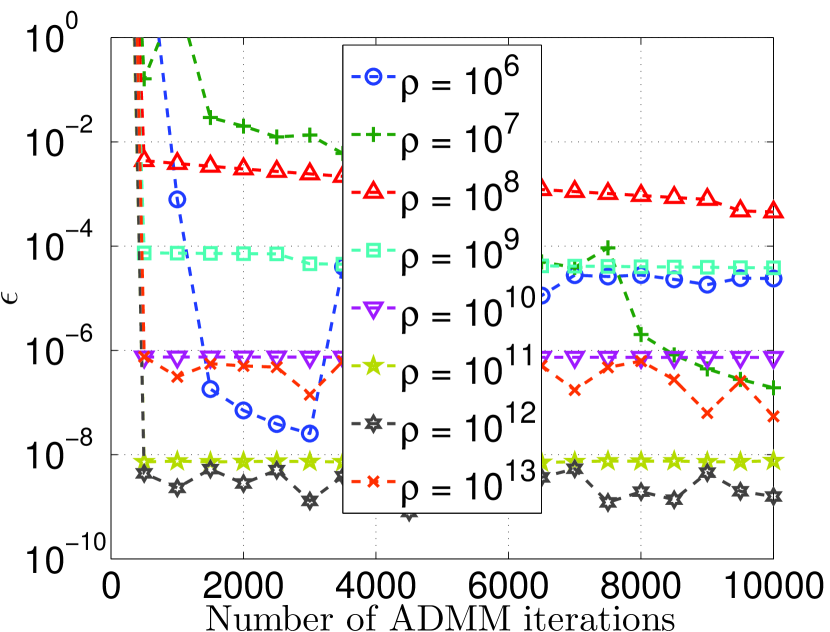

V-B Connection to Proposition 2

In this section we relate the numerical evaluations to Proposition 2. In particular, we inspect the behavior of [compare with (38) and (43)], and [compare with (41) and (43)] with respect to , which are defined in Section IV-C. The unit of measurements for is and the unit of can be interpreted as the square of the decrease/increase in $/hour with respect to a small perturbation in the variable .

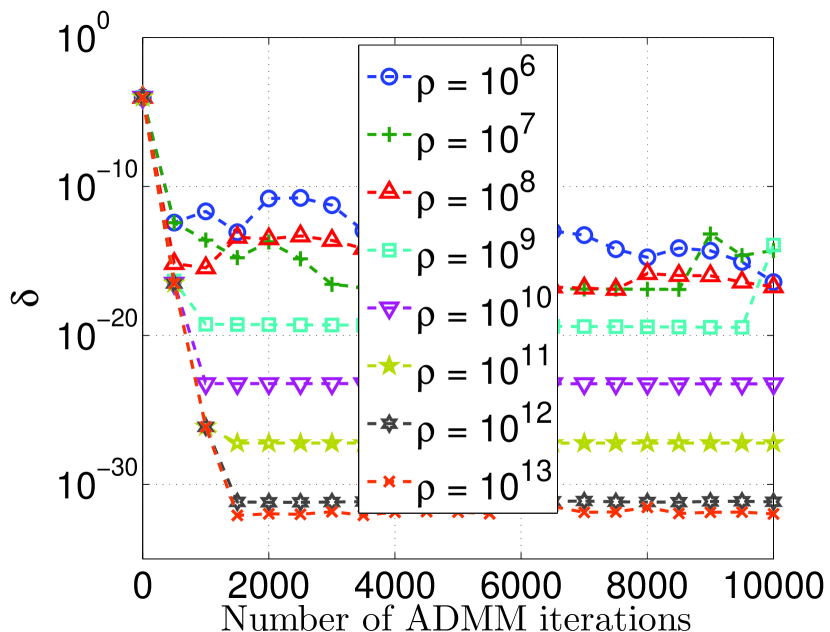

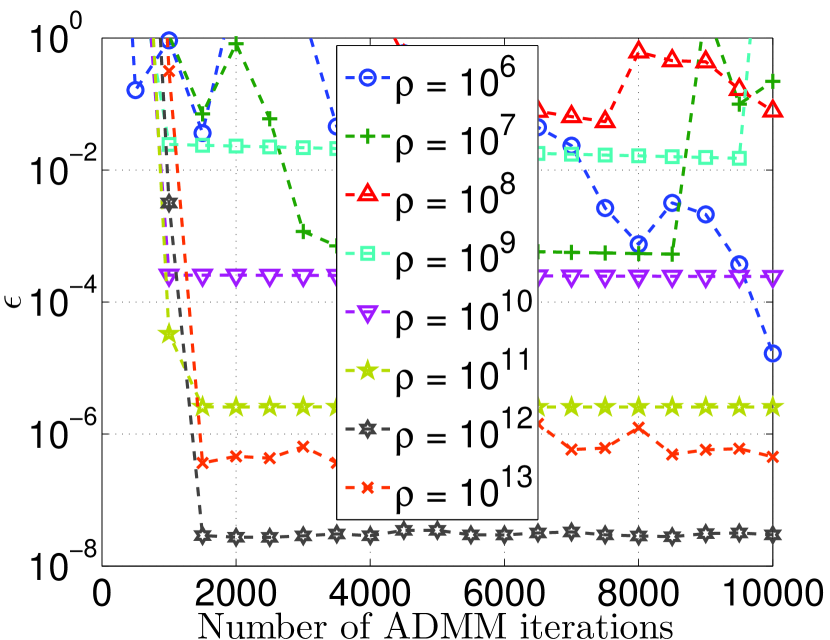

Fig. 5 depicts at every ADMM iterations, for .

In the bus example the results are almost identical for and, accordingly, we only include the results for . Since measures the inconsistency between the subproblems, the point returned by ADMM-DOPF can only be considered feasible when has reached acceptable accuracy, i.e., for some . We do not consider any particular threshold , since we are only interested in observing the convergence behavior. In this aspect, the result show a promising behavior, as has a decreasing trend in all cases. Furthermore, for the , , and bus examples, converges to a fixed error floor for the larger values of the penalty parameter . In particular, as increases, converges to a point closer to zero, which suggests a negative relationship between and . Thereby, indicating that increasing the penalty parameter enforces higher accuracy of consistency among the subproblems. On the contrary to the , , and bus examples, decreases slower when the penalty parameter increases in the case of the bus example. However, in the case of the bus example, is still decreasing after the last iteration considered when .

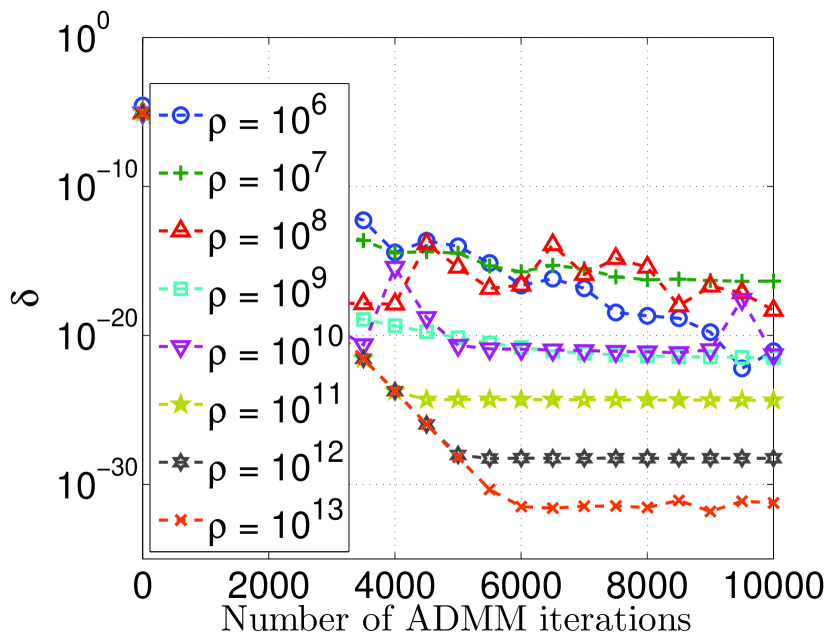

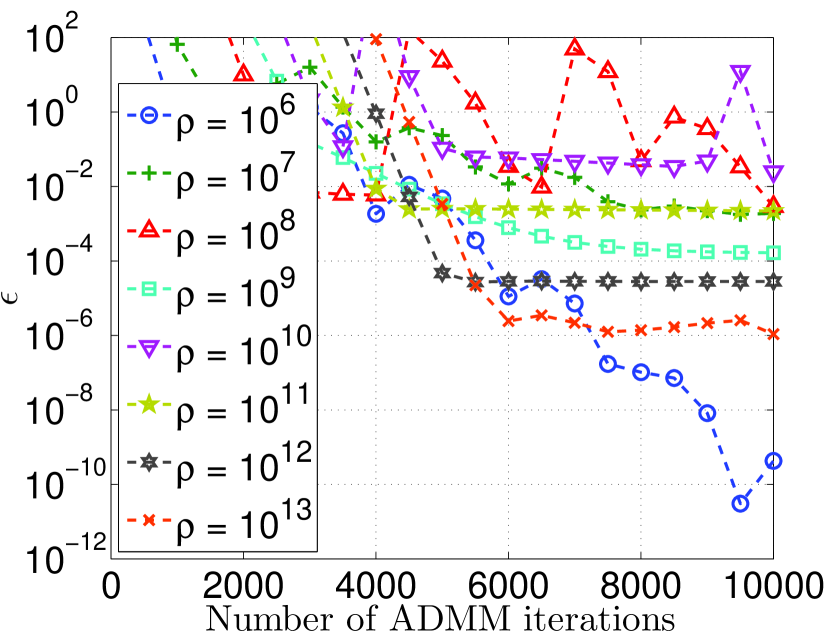

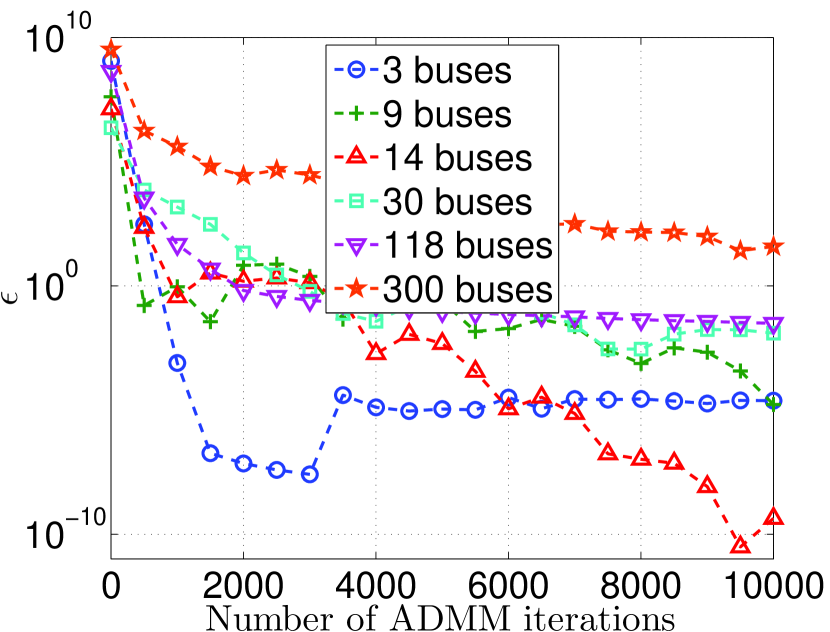

Fig. 6 depicts at every ’th ADMM iterations, for different ’s.

In contrast to , decreasing trend in is not necessary to obtain a feasible solution to the problem. However, under Assumption 1, as and go to zero, the algorithm converges to KKT optimal point. Therefore, the decreasing trend in , which is observed from the results, is desired. In the case of the , and bus reaches values between and in almost every case. However, in the bus example, only when does epsilon reach below .

V-C Convergence and scalability properties

By convention, the objective value of problem (18) is if the problem is infeasible and is given by (18a) if it is feasible. Therefore, when computing the objective function of the problem, one has to verify whether the constraints (18b)-(18f) are feasible or not. Based on Fig. 4, the feasibility of the subproblem variables including is on the order of in the worst case for every ADMM iteration [compare with (46)]. In other words, returned by Algorithm 2 in every ADMM iteration is feasible (with very high precision). Therefore, our proposed Algorithm 1, which includes Algorithm 2 as a subroutine, ensures the feasibility of constraints (18b) -(18e) (with very high precision). However, the feasibility of the remaining constraint (18f) has to be verified, in order to compute a sensible operating point. In the sequel, we numerically analyse the feasibility of the constraint (18f) together with the objective value computed by using (18a).

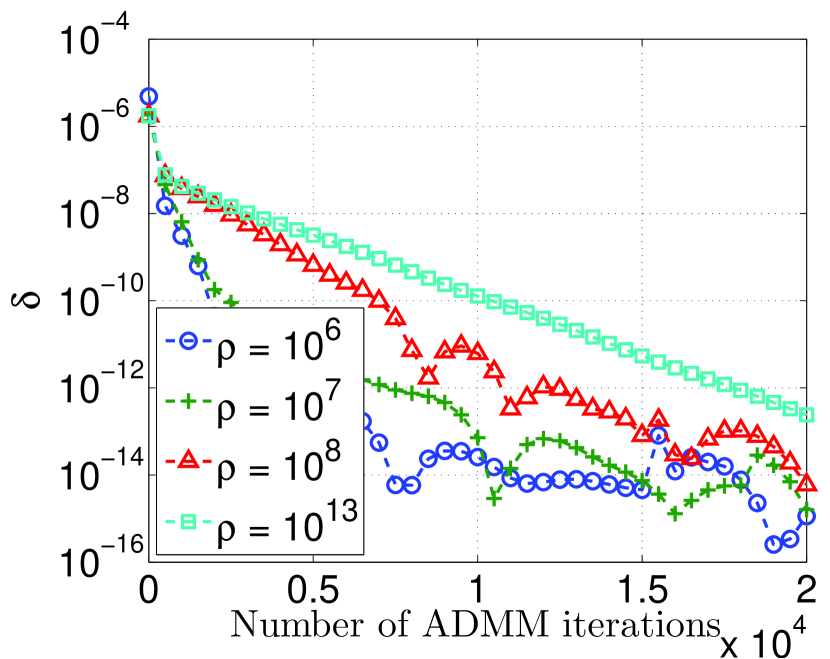

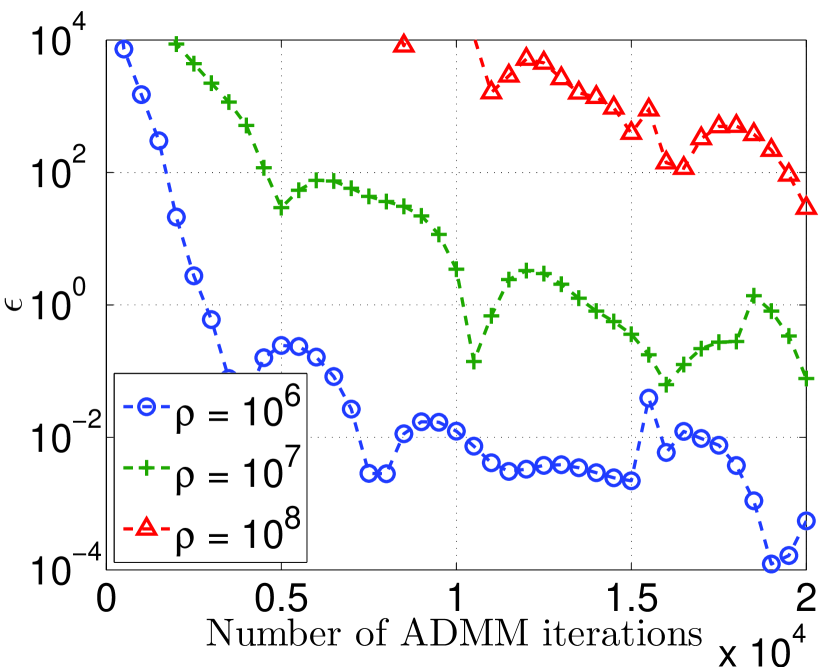

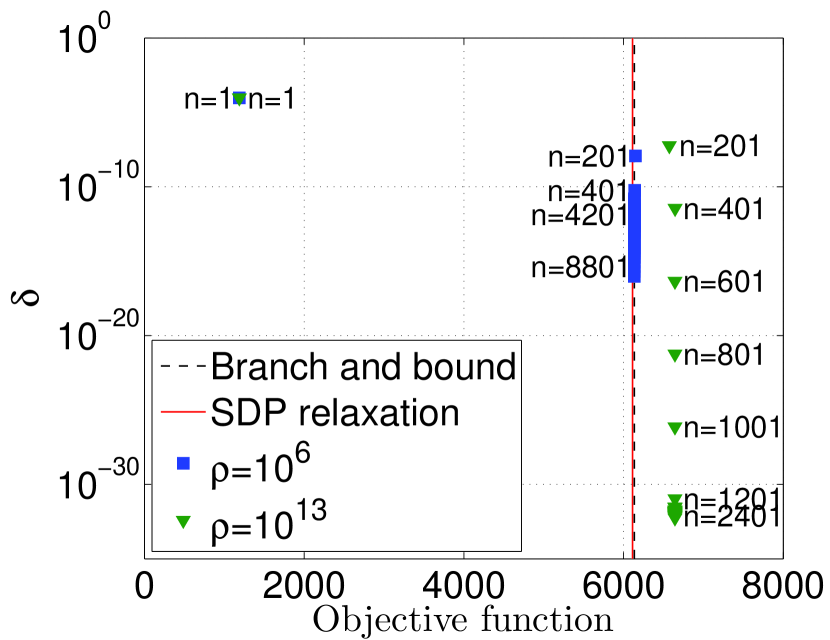

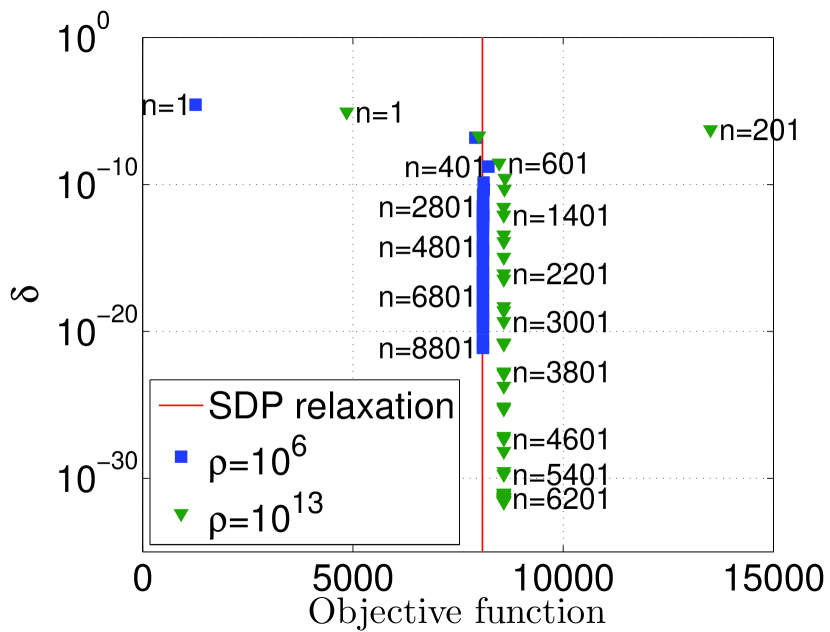

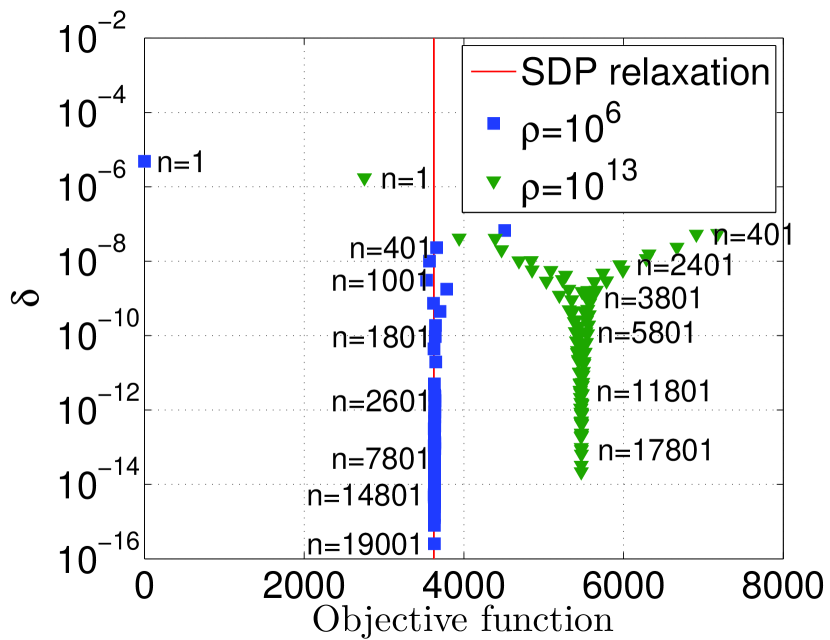

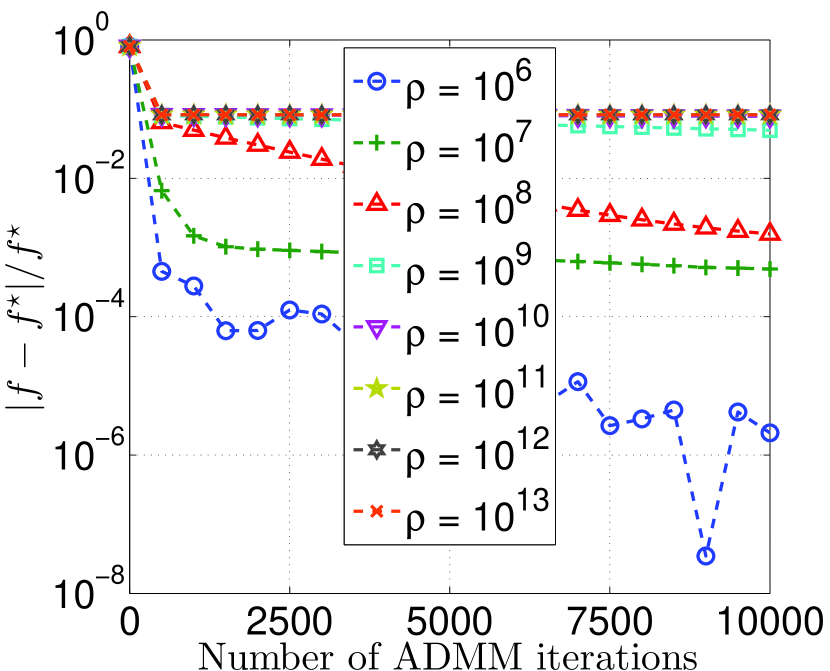

Fig. 7 shows the objective value versus , at every or ’ ADMM iterations.

In the case of the and bus examples we compare the objective value with the branch and bound algorithm from [11] where the relative tolerance, the difference between the best upper and lower bounds relative to the best upper bound, is . The upper bound is obtained from Matpower and the lower bound is obtained by using the matlab toolbox YALMIP [36] and the solver SEDUMI [37] to solve the dual of the SDP relaxation. In the case of the and bus examples, the branch and bound algorithm failed due to memory errors. In all cases we compare our results with the SDP relaxation from [3]. The results show that the algorithm converges to some objective value in relatively few iterations, which can even be optimal with an appropriate choice of . For example, for the considered cases yields almost optimal objective values. Moreover, as desired the consistency metric is driven towards zero as the number of ADMM iterations increases.

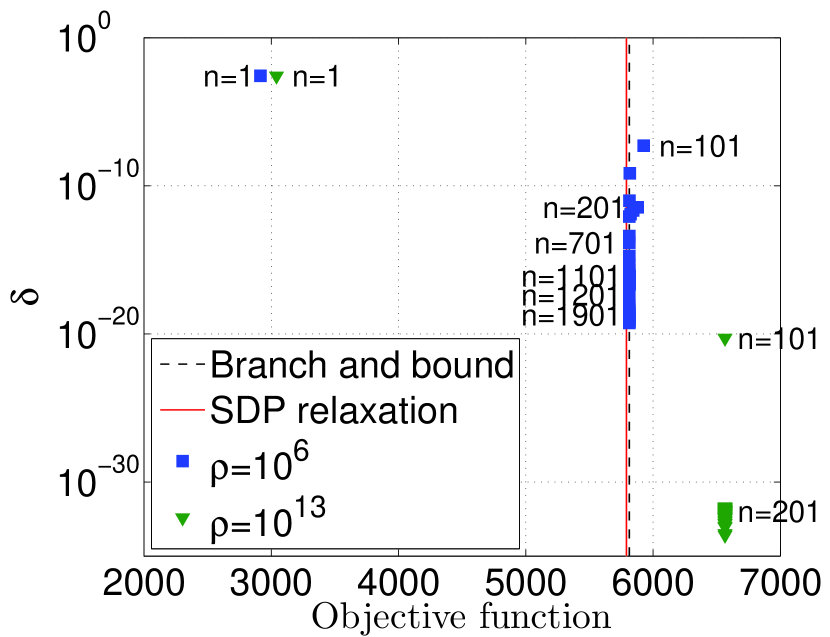

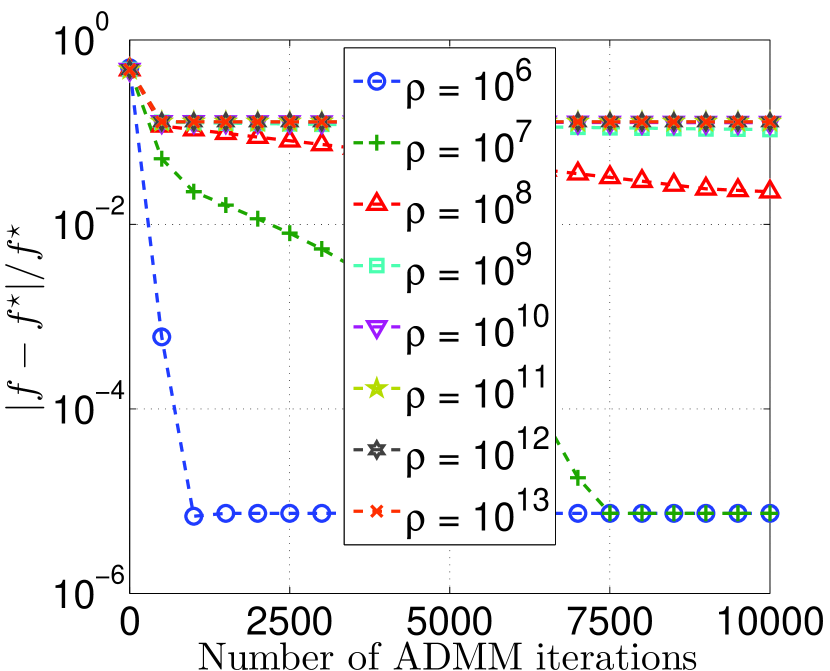

Fig. 8 depicts the relative objective function for the 3 and 9 bus examples. The results are consistent with thous presented in Fig. 7. For example, in the case of the relative objective function value is on the order of . Results suggest that a proper choice of is beneficial to achieve a good network operating point.

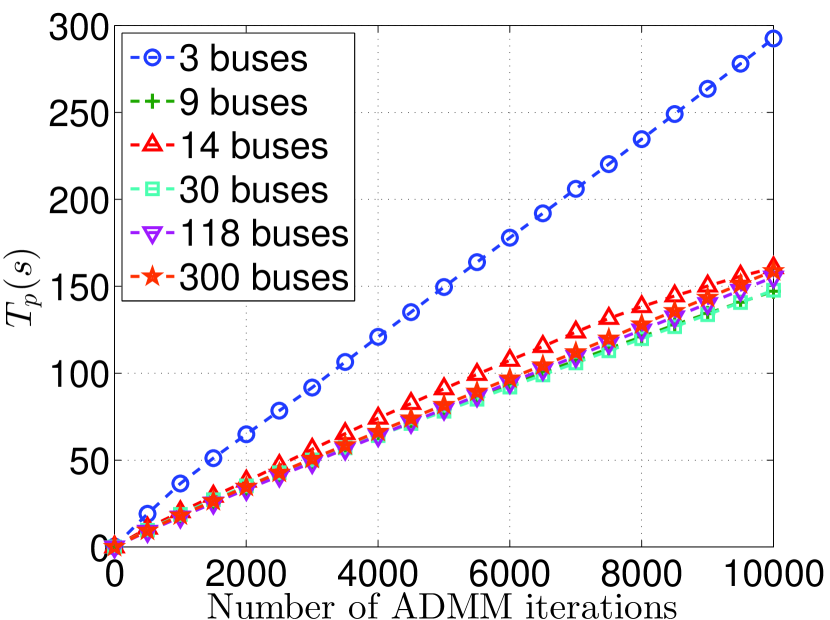

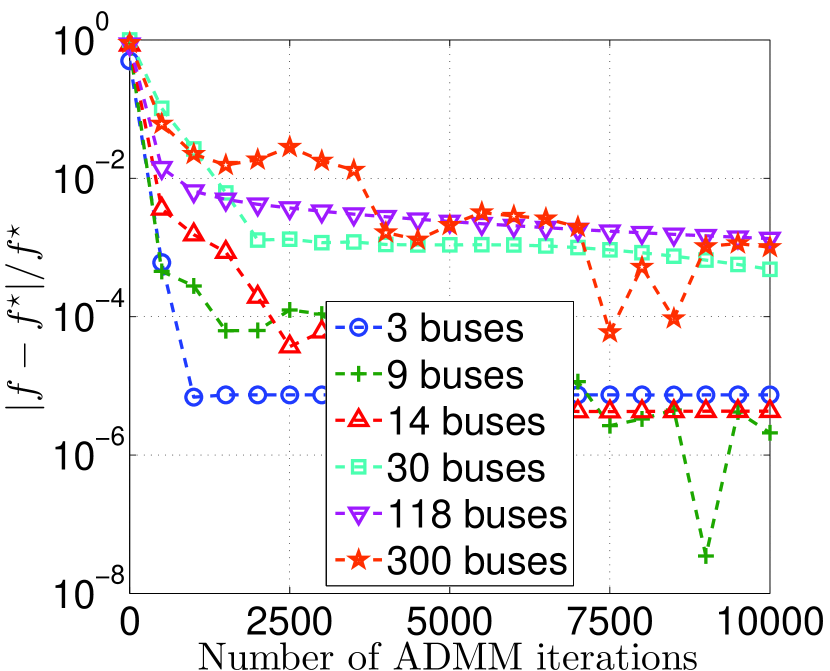

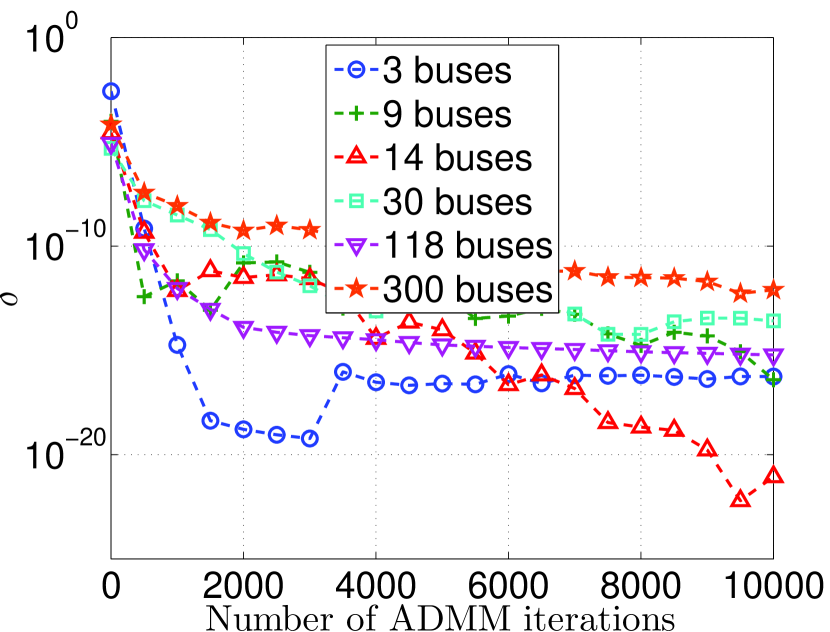

To study the scalability properties of the proposed algorithm, we compute the CPU time, relative objective value, , and of the algorithm for all the considered examples. In the case of , , , and bus examples, we choose and in the case of and bus examples we chose .

Fig. 9(a) shows the parallel running times versus ADMM iterations. In particular, we define , where is the sequential CPU time. The behavior of the plots in the case of , , , , and bus examples are very similar. In other words, the parallel running time is independent of the number of busses, indicating promising scalability of the proposed algorithm. Note that the bus example has to handle more variables per subproblem, compared with the other examples, see column 6 of Table I. This is clearly reflected in the plot of bus example, as an increase of the associated parallel running time .

Fig. 9(b) depicts the relative objective function, . In the case of , , , and bus examples the global optimum is found by branch and bound algorithm. However, in the case of and bus examples, branch and bound algorithm failed, and therefore the best known objective value found by Matpower was considered as . 555 Since the and bus examples have zero duality gap, the branch and bound algorithm worked efficiently. However, in the case of and bus examples, where there is nonzero duality gap, the branch and bound algorithm failed. Results show that for large and relatively large test examples (e.g., , , ) the relative objective function value is on the order of and is not affected by the network size. A similar independence of the performance is observed for very small test examples as well (e.g., , , ) with relative objective function values on the order of . The reduction of the relative objective function values of smaller networks compared with larger network examples are intuitively expected due to substantial size differences of those networks.

Fig. 9(c) and Fig. 9(d) depict and as a function of ADMM iterations. Results show that, irrespective of the number of buses, the metrics and are decreasing as desired. Results further suggest that those values are driven towards small values as ADMM iterations increase.

| Example | SDP | Branch & Bound | Matpower | ADMM-DOPF, n=3000 | ADMM-DOPF, n=10000 | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| obj | obj | obj | obj | obj | ||||||

| buses | 8 | 0.08 | 91.73 | 5812.6 | 292.54 | |||||

| buses | 0.08 | 49.19 | 6135.2 | 147.16 | ||||||

| buses | 0.1 | 56.12 | 8092.4 | 160.71 | ||||||

| buses | 0.12 | 51.53 | 3632.5 | 152.95 | ||||||

| buses | 0.2 | 48.62 | 129835.2 | 155.29 | ||||||

| buses | 0.42 | 51.19 | 720449.4 | 158.97 | ||||||

Table III shows the running time and the objective value obtained by different approaches. As benchmarks, we consider the centralized algorithms, SDP relaxation [3], branch and bound [11], and Matpower [33]. Table III shows that our proposed method yields network operating points, which are almost optimal, where the discrepancy with respect to the optimal is on the order of (respectively, ) or less with (respectively, ) ADMM iterations. Note that the running time of ADMM-DOPF is insensitive to the network size, see Fig. 9(a) for more details. However, even in small networks (e.g., case with , ), the running time of branch and bound algorithm can explode. This is expected because the worst case complexity of the branch and bound algorithm grows exponentially with the problem size. Results further suggest that the running time of the centralized algorithm SDP relaxation increases as the network size grows, unlike the proposed ADMM-DOPF. Note that the running time of ADMM-DOPF is large compared to the centralized Matpower. However, those values can further be reduced if ADMM-DOPF is deployed in a parallel computation environment, where every subproblem is handled at a dedicated set of resources, including processors, memory, among others. In addition to the centralized benchmarks, we also consider the decentralized one proposed in [28], which employs ADMM for general nonconvex OPF. However, the results of [28] are not documented in Table III, because for all the considered examples, the algorithm therein did not converge. This agrees with the numerical results of [28], where the authors mentioned that the convergence of their algorithm is more sensitive to the initial point in the case of mesh networks [28, p. 5], so does ADMM-DOPF. We note that their method converges if it is initialized close to the optimal solution. However, in practice, such an initialization point in unknown, thus limiting dramatically the applicability of the method in [28].

Finally, from all our numerical experiments discussed above, we note that the power losses in the flow lines are typically on the order of (or less) of the total power flow in the line. Because the losses are not negligible, approximations such as the linearization of power flow equations can be less applicable to compute better network operating points.

VI conclusions

We proposed a distributed algorithm for the optimal power flow (OPF), by decomposing the OPF problem among the buses that compose the electrical network. A light communication protocol among neighboring buses is needed during the algorithm, resulting in high scalability properties. The subproblems related to each bus capitalize on sequential convex approximations to gracefully manipulate the nonconvexity of the problem. We showed the convergence of subproblem solutions to a local optimum, under mild conditions. Furthermore, by using the local optimality results associated with the subproblems, we quantified the optimality of the overall algorithm. We evaluated the proposed algorithm on a number of test examples to demonstrate its convergence properties and to compare it with the global optimal method. In all considered cases the proposed algorithm achieved close to optimal solutions. Moreover, the proposed algorithm showed appealing scalability properties when tested on larger examples.

Appendix A On the use of quadratic programming QP solvers

Note that, not all the constraints of problem (24) are affine (or linear). In particular, constraints (24g) and (24h) are not affine. Therefore, QP solvers are not directly applied to solve the problem. However, if constraints (24g) and (24h) are approximated by using affine constraints, then QP is readily applied to the modified problem.

Let us start by considering the feasible regions defined by (24h), which accounts for , , see Fig. 1(b). Next, we approximate the nonlinear boundary of by affine functions as depicted in Fig. 1(c). We denote by the approximated polyhedral set. We can apply similar ideas to approximate the feasible regions specified by (24g) [cf (6h)-(6i)], where we use to denote the resulting affine function. Finally, the idea is to find the desired optimal solution of problem (24) by constructing a series of sets of the form and affine functions of the form that approximate the feasible set specified by (24g) and (24h) in an increasing precision. The QP based algorithm to solve problem (24) can be summarized as follows.

Algorithm 3: QP to solve Problem (24)

-

1.

Initialize: Given the initial approximated set and affine function . Let .

-

2.

Solve the QP:

min (48a) s. t. (48b) (48c) (48d) (48e) (48f) where the variables are , , , , , , , , , , , , and . The solution corresponding to the variable , are denoted by , , respectively and and all the dual optimal variables are denoted by .

-

3.

Stopping criterion: If and for all , stop and return . Otherwise, increase the precession of set and function by adding a hyper plane and an affine function, respectively, set and go to step 2.

The set is initialized in the first step by approximating the exterior boundary of the donut [Fig. 1(a)] by an equilateral octagon as shown in Fig. 1(c), and is initialized correspondingly. The second step simply involves solving a QP programming problem. The algorithm terminates in the third step if and for all . However, if we increase the precession of by adding a hyper plane on the exterior boundary of the donut , so that . In particular, we set where is the halfspace

| (49) |

where

if and

can be treated identically.

Appendix B Proofs

B-A Proof of Proposition 1

Proof:

Obviously, problem (24) is convex and in any iteration of Algorithm 2, [so is ] are primal and dual optimal, with zero duality gap. Thus, satisfies KKT conditions for problem (24) [6, § 5.5.3]. However, in order to show that satisfies KKT conditions for problem (20), we need to show 1) is primal feasible, 2) is dual feasible, 3) and satisfy complementary slackness conditions, and 4) derivative of the Lagrangian of problem (20) vanishes with and [6, § 5.5.3].

We start by noting that the original functions definitions and [see (20d) and (20e)] are characterized by using the basic form

| (50) |

where represents power, represent currents, represent voltages, and we have denoted compactly by . Let denote the first order Taylor’s approximation of at . That is, characterizes the basic form of the first order Taylor’s approximation of function definitions and , see (24d) and (24e). Therefore, without loss of generality, we make our assertions based on and together with the assumption , where plays the role of and plays the role of .

Let us next summarize some intermediate results, which will be useful later.

Lemma 1

Given the function definition of the form (50), and , we have 1) and 2) .

Proof:

see Appendix B-C. ∎

From Lemma 1 above, we conclude that

| (51) |

By relating the result (51) to our original problems (20) and (24), we can deduce that

| (52) |

and

| (53) |

where is used to represent component-wise differentiation of associated functions.

Now we can easily conclude that is primal feasible for problem (20). This follows from (52), the fact that constraints (20b), (20c), (20f), and (20g) are identical to (24b), (24c), (24f), and (24g), respectively, and that .

Dual feasibility of associated with constraints (24f) and (24g) affirms the dual feasibility of associated with identical constraints (20f) and (20g). In the case of constraint (24h), recall from (23) that is characterized by such that

| (54) |

Thus, dual feasibility of components associated with first (respectively second) constraint above ensures the dual feasibility of same components associated with (respectively ) of (20h). Thus, we conclude is dual feasible for problem (20).

From (52), the fact that constraints (20b), (20c), (20f), and (20g) are identical to (24b), (24c), (24f), and (24g), respectively, and that the components of , strictly satisfy the constraint (24h) [see Assumption 1], it follows that and satisfy complementary slackness conditions for problem (20). In addition, Assumption 1 together with complementary slackness condition ensure that the components of associated with constraints (24h) are identically zero.

Finally, recall that are optimal primal and dual variables for problem (24). Therefore, the derivative of the Lagrangian associated with problem (24) vanishes at , i.e., . This result combined with (53), the fact that constraints (20b), (20c), (20f), and (20g) are identical to (24b), (24c), (24f), and (24g), respectively, and the fact that the components of associated with constraints (24h) are identically zero, affirms that derivative of the Lagrangian associated with problem (20) vanishes at and , i.e.,

| (55) |

which concludes the proof. ∎

| (64) |

| (65) |

B-B Proof of Proposition 2

Proof:

Given Assumption 1 holds, Proposition 1, asserts that all constraints, but (18f) of problem (18) are primal feasible. Combined this with (42), it trivially follows that , where and [cf (38)]. To show that [cf (41)], let us consider the Lagrangian associated with problem (20). Note that is related to the Lagrangian of problem (20) as

Note the notation used when passing the parameters to , where we have highlighted the dependence of on [cf (20a)]. Let us now inspect the derivative of the Lagrangian , evaluated at . In particular, we have (64) [see top of this page], where is given in (65) [compare with (42)]. Here the first equality follows form standard derivation combined with Proposition 1, the second equality follows from (55) and by invoking the optimality conditions for problem (21), i.e., . From (64)-(65), we conclude that [cf (41)], where . Finally, conditions (36), (37), (39), and (40), associated with problem (18) follow from straightforward arguments, which concludes the proof. ∎

B-C Proof of Lemma 1

Let denote the Hessian of function . Note that is a matrix with constant entries and thus does not depend on . From the definition of the Taylor series expansion at we have

| (66) |

Moreover, differentiation of (66) yields

| (67) |

To show the case 1 of the proposition, we consider the following relations:

| (68) |

| (69) |

where (68) follows from (66) with and (69) follows from (68) and basics of linear algebra. By letting in (69), we conclude , since . Similarly, by using (67) and that and , we conclude .

References

- [1] J. Carpentier, “Contribution à l’étude du dispatching économique,” Bulletin Society Francaise Electricians, vol. 3, no. 8, pp. 431–447, 1962.

- [2] S. Frank, I. Steponavice, and S. Rebennack, “Optimal power flow: a bibliographic survey I,” Energy Systems, vol. 3, no. 3, pp. 221–258, Sept. 2012.

- [3] J. Lavaei and S. H. Low, “Zero duality gap in optimal power flow problem,” Power Systems, IEEE Transactions on, vol. 27, no. 1, pp. 92–107, 2012.

- [4] S. Frank, I. Steponavice, and S. Rebennack, “Optimal power flow: a bibliographic survey II,” Energy Systems, vol. 3, no. 3, pp. 259–289, Sept. 2012.

- [5] X. Bai, H. Wei, K. Fujisawa, and Y. Wang, “Semidefinite programming for optimal power flow problems,” International Journal of Electrical Power & Energy Systems, vol. 30, no. 6-7, pp. 383–392, July 2008.

- [6] S. Boyd and L. Vandenberghe, Convex Optimization, Cambridge University Press, New York, NY, USA, 2004.

- [7] S. Bose, D. Gayme, S. H. Low, and K. M. Chandy, “Optimal power flow over tree networks,” in Communication, Control, and Computing (Allerton), 2011 49th Annual Allerton Conference on, Monticello, IL, 2011.

- [8] B. Zhang and D. Tse, “Geometry of injection regions of power networks,” Power Systems, IEEE Transactions on, vol. 28, no. 2, pp. 788–797, 2013.

- [9] J. Lavaei, D. Tse, and Baosen Zhang, “Geometry of power flows and optimization in distribution networks,” Power Systems, IEEE Transactions on, vol. 29, no. 2, pp. 572–583, March 2014.

- [10] B. C. Lesieutre, D. K. Molzahn, A. R. Borden, and C. L. DeMarco, “Examining the limits of the application of semidefinite programming to power flow problems,” in Communication, Control, and Computing (Allerton), 2011 49th Annual Allerton Conference on, 2011, pp. 1492–1499.

- [11] A. Gopalakrishnan, A. U. Raghunathan, D. Nikovski, and L. T. Biegler, “Global optimization of optimal power flow using a branch and bound algorithm,” in Communication, Control, and Computing (Allerton), 2012 50th Annual Allerton Conference on, 2012, pp. 609–616.

- [12] E. L. Quinn, “Privacy and the New Energy Infrastructure,” Tech. Rep., Center for Energy and Environmental Security (CEES), University of Colorado, Feb 2009, [Online]. Available at SSRN: http://ssrn.com/abstract=1370731or%****␣paper_v25_sindri.bbl␣Line␣75␣****http://dx.doi.org/10.2139/ssrn.1370731.

- [13] A. Cavoukian, J. Polonetsky, and C. Wolf, “Smartprivacy for the smart grid: embedding privacy into the design of electricity conservation,” Identity in the Information Society, vol. 3, no. 2, pp. 275–294, 2010.

- [14] S. Salinas, M. Li, and P. Li, “Privacy-preserving energy theft detection in smart grids: A P2P computing approach,” Selected Areas in Communications, IEEE Journal on, vol. 31, no. 9, pp. 257–267, 2013.

- [15] B. H. Kim and R. Baldick, “Coarse-grained distributed optimal power flow,” Power Systems, IEEE Transactions on, vol. 12, no. 2, pp. 932–939, 1997.

- [16] R. Baldick, B. H. Kim, C. Chase, and Y Luo, “A fast distributed implementation of optimal power flow,” Power Systems, IEEE Transactions on, vol. 14, no. 3, pp. 858–864, 1999.

- [17] B. H. Kim and R. Baldick, “A comparison of distributed optimal power flow algorithms,” Power Systems, IEEE Transactions on, vol. 15, no. 2, pp. 599–604, 2000.

- [18] A. J. Conejo, F. J. Nogales, and F. J. Prieto, “A decomposition procedure based on approximate Newton directions,” Mathematical Programming, vol. 93, no. 3, pp. 495–515, 2002.

- [19] F. J. Nogales, F. J. Prieto, and A. J. Conejo, “A decomposition methodology applied to the multi-area optimal power flow problem,” Annals of Operations Research, vol. 120, no. 1-4, pp. 99–116, 2003.

- [20] G. Hug-Glanzmann and G. Andersson, “Decentralized optimal power flow control for overlapping areas in power systems,” Power Systems, IEEE Transactions on, vol. 24, no. 1, pp. 327–336, 2009.

- [21] A. G. Bakirtzis and P. N. Biskas, “A decentralized solution to the DC-OPF of interconnected power systems,” Power Systems, IEEE Transactions on, vol. 18, no. 3, pp. 1007–1013, 2003.

- [22] A. Y. S. Lam, B. Zhang, and D. Tse, “Distributed Algorithms for Optimal Power Flow Problem,” ArXiv e-prints, Sept. 2011.

- [23] E. Dall’Anese, Hao Zhu, and G.B. Giannakis, “Distributed optimal power flow for smart microgrids,” Smart Grid, IEEE Transactions on, vol. 4, no. 3, pp. 1464–1475, 2013.

- [24] B. Zhang, A. Y. S. Lam, A. Dominguez-Garcia, and D. Tse, “Optimal Distributed Voltage Regulation in Power Distribution Networks,” ArXiv e-prints, Apr. 2012, [Online]. Available: http://adsabs.harvard.edu/abs/2012arXiv1204.5226Z.

- [25] Matt Kraning, Eric Chu, Javad Lavaei, and Stephen Boyd, “Dynamic network energy management via proximal message passing,” Foundations and Trends® in Optimization, vol. 1, no. 2, pp. 73–126, 2014.

- [26] S. Bolognani, G. Cavraro, R. Carli, and S. Zampieri, “A distributed feedback control strategy for optimal reactive power flow with voltage constraints,” ArXiv e-prints, Mar. 2013.

- [27] P. Šulc, S. Backhaus, and M. Chertkov, “Optimal Distributed Control of Reactive Power via the Alternating Direction Method of Multipliers,” ArXiv e-prints, Oct. 2013.

- [28] A. X. Sun, D.T. Phan, and S. Ghosh, “Fully decentralized ac optimal power flow algorithms,” in Power and Energy Society General Meeting (PES), 2013 IEEE, July 2013, pp. 1–5.

- [29] S. Boyd, N. Parikh, E. Chu, B. Peleato, and J. Eckstein, “Distributed optimization and statistical learning via the alternating direction method of multipliers,” Foundations and Trends in Machine Learning, vol. 3, no. 1, pp. 1–122, Jan. 2011.

- [30] R. O’Neil, A. Castillo, and M. B. Cain, “The IV formulation and linear approximation of the AC optimal power flow problem,” 2012, [Online]. Available: http://www.ferc.gov/industries/electric/indus-act/market-planning/opf-papers/acopf-2-iv-linearization.pdf.

- [31] S. Boyd, “Sequential convex programming,” University Lecture, 2013, [Online]. Available: http://web.stanford.edu/class/ee364b/lectures/seq_slides.pdf.

- [32] S. Boyd, A. Ghosh, B. Prabhakar, and D. Shah, “Randomized gossip algorithms,” Information Theory, IEEE Transactions on, vol. 52, no. 6, pp. 2508–2530, 2006.

- [33] R. D. Zimmerman, C. E. Murillo-Sánchez, and R. J. Thomas, “Matpower: Steady-state operations, planning, and analysis tools for power systems research and education,” Power Systems, IEEE Transactions on, vol. 26, no. 1, pp. 12–19, 2011.

- [34] “Power systems test case archive,” [Online]. Available: http://www.ee.washington.edu/research/pstca/.

- [35] MATLAB, version 8.1.0.604 (R2013a), The MathWorks Inc., Natick, Massachusetts, 2013.

- [36] J. Löfberg, “Yalmip : A toolbox for modeling and optimization in MATLAB,” in Proceedings of the CACSD Conference, Taipei, Taiwan, 2004, [Online]. Available: http://users.isy.liu.se/johanl/yalmip.

- [37] J. F. Sturm, “Using SeDuMi 1.02, a MATLAB toolbox for optimization over symmetric cones,” Optimization Methods and Software, vol. 11–12, pp. 625–653, 1999, [Online]. Available: http://plato.asu.edu/ftp/usrguide.pdf.