Monte Carlo Simulation for Lasso-Type Problems

by Estimator Augmentation

Abstract

Regularized linear regression under the penalty, such as the Lasso, has been shown to be effective in variable selection and sparse modeling. The sampling distribution of an -penalized estimator is hard to determine as the estimator is defined by an optimization problem that in general can only be solved numerically and many of its components may be exactly zero. Let be the subgradient of the norm of the coefficient vector evaluated at . We find that the joint sampling distribution of and , together called an augmented estimator, is much more tractable and has a closed-form density under a normal error distribution in both low-dimensional () and high-dimensional () settings. Given and the error variance , one may employ standard Monte Carlo methods, such as Markov chain Monte Carlo and importance sampling, to draw samples from the distribution of the augmented estimator and calculate expectations with respect to the sampling distribution of . We develop a few concrete Monte Carlo algorithms and demonstrate with numerical examples that our approach may offer huge advantages and great flexibility in studying sampling distributions in -penalized linear regression. We also establish nonasymptotic bounds on the difference between the true sampling distribution of and its estimator obtained by plugging in estimated parameters, which justifies the validity of Monte Carlo simulation from an estimated sampling distribution even when .

Key words: Confidence interval, importance sampling, Lasso, Markov chain Monte Carlo, p-value, sampling distribution, sparse linear model.

1 Introduction

Consider the linear regression model,

| (1.1) |

where is an -vector, an design matrix, the vector of coefficients, and i.i.d. random errors with mean zero and variance . Recently, -penalized estimation methods (Tibshirani 1996; Chen et al. 1999) have been widely used to find sparse estimates of the coefficient vector. Given positive weights , , and a tuning parameter , an -penalized estimator is defined by minimizing the following penalized loss function,

| (1.2) |

By different ways of choosing , the estimator corresponds to the Lasso (Tibshirani 1996), the adaptive Lasso (Zou 2006), and the one-step linear local approximation (LLA) estimator (Zou and Li 2008) among others. We call such an estimator a Lasso-type estimator.

In many applications of -penalized regression, it is desired to quantify the uncertainty in the estimates. However, except for very special cases, the sampling distribution of a Lasso-type estimator is complicated and difficult to approximate. Closed-form approximations to the covariance matrices of the estimators in Tibshirani (1996), Fan and Li (2001), and Zou (2006) are unsatisfactory, as they all give zero variance for a zero component of the estimators and thus fail to quantify the uncertainty in variable selection. Theoretical results on finite-sample distributions and confidence sets of some Lasso-type estimators have been developed (Pötscher and Schneider 2009, 2010) but only under orthogonal designs, which clearly limits general applications of these results. The bootstrap can be used to approximate the sampling distribution of a Lasso-type estimator, in which numerical optimization is needed to minimize (1.2) for every bootstrap sample. Although there are efficient algorithms, such as the Lars (Efron et al. 2004), the homotopy algorithm (Osborne et al. 2000), and coordinate descent (Friedman et al. 2007; Wu and Lange 2008), to solve this optimization problem, it is still time-consuming to apply these algorithms hundreds or even thousands of times in bootstrap sampling. As pointed out by Knight and Fu (2000) and Chatterjee and Lahiri (2010), the bootstrap may not be consistent for estimating the sampling distribution of the Lasso under certain circumstances. To overcome this difficulty, a modified bootstrap (Chatterjee and Lahiri 2011) and a perturbation resampling approach (Minnier et al. 2011) have been proposed, both justified under a fixed- asymptotic framework. Zhang and Zhang (2014) have developed methods for constructing confidence intervals for individual coefficients and their linear combinations in high-dimensional () regression with sufficient conditions for the asymptotic normality of the proposed estimators. There are several recent articles on significance test and confidence region construction for sparse high-dimensional linear models (Javanmard and Montanari 2013a, b; Lockhart et al. 2014; van de Geer et al. 2013), all based on asymptotic distributions for various functions of the Lasso. On the other hand, knowledge on sampling distributions is also useful for distribution-based model selection with penalization, as demonstrated by stability selection (Meinshausen and Bühlmann 2010) and the Bolasso (Bach 2008).

A possible alternative to the bootstrap or resampling is to simulate from a sampling distribution by Monte Carlo methods, such as Markov chain Monte Carlo (MCMC). An obvious obstacle to using these methods for a Lasso-type estimator is that its sampling distribution does not have a closed-form density. In this article, we study the joint distribution of a Lasso-type estimator and the subgradient of evaluated at . Interestingly, this joint distribution has a density that can be calculated explicitly assuming a normal error distribution, regardless of the relative size between and . Thus, one can develop Monte Carlo algorithms to draw samples from this joint distribution and estimate various expectations of interest with respect to the sampling distribution of , which is simply a marginal distribution. This approach offers great flexibility in studying the sampling distribution of a Lasso-type estimator. For instance, one may use importance sampling (IS) to accurately estimate a tail probability (small p-value) with respect to the sampling distribution under a null hypothesis, which can be orders of magnitude more efficient than any method directly targeting at the sampling distribution. Another potential advantage of this approach is that, at each iteration, an MCMC algorithm only evaluates a closed-form density, which is much faster than minimizing (1.2) numerically as used in the bootstrap. Furthermore, our method can be interpreted as an MCMC algorithm targeting at a multivariate normal distribution with locally reparameterized moves and hence is expected to be computationally tractable.

The remaining part of this article is organized as follows. After a high-level description of the basic idea, Section 2 derives the density of the joint distribution of and in the low-dimensional setting with , and Section 3 develops MCMC algorithms for this setting. The density in the high-dimensional setting with is derived in Section 4. In Section 5, we construct applications of the high-dimensional result in p-value calculation for Lasso-type inference by IS. Numerical examples are provided in Sections 3 and 5 to demonstrate the efficiency of the Monte Carlo algorithms. Section 6 provides theoretical justifications for simulation from an estimated sampling distribution of the Lasso by establishing its consistency as . Section 7 includes generalizations to random designs, a connection to model selection consistency, and a Bayesian interpretation of the sampling distribution. The article concludes with a brief discussion and some remarks. Technical proofs are relegated to Section 8.

Notations for vectors and matrices are defined here. All vectors are regarded as column vectors. Let and be two index sets. For vectors and , we define , , and . For a matrix , write its columns as , . Then extracts the columns in , the submatrix extracts the rows in and the columns in , and extracts the rows in . Furthermore, and are understood as and , respectively. We denote the row space, the null space, and the rank of by , , and , respectively. Denote by the diagonal matrix with as the diagonal elements, and by the block diagonal matrix with and as the diagonal blocks, where the submatrices and may be of different sizes and may not be square. For a square matrix , extracts the diagonal elements. Denote by the identity matrix.

2 Estimator augmentation

2.1 The basic idea

Let . A minimizer of (1.2) is given by the Karush-Kuhn-Tucker (KKT) condition

| (2.1) |

where is the subgradient of the function evaluated at the solution . Therefore,

| (2.2) |

for . Hereafter, we may simply call the subgradient if the meaning is clear from context. Lemma 1 reviews a few basic facts about the uniqueness of and .

Lemma 1.

For any , and , every minimizer of (1.2) gives the same fitted value and the same subgradient . Moreover, if the columns of are in general position, then is unique for any and .

Proof.

We regard and together as the solution to Equation (2.1). Lemma 1 establishes that is unique for any assuming the columns of are in general position (for a technical definition see Tibshirani 2013), regardless of the sizes of and . We call the vector the augmented estimator in an -penalized regression problem. The augmented estimator will play a central role in our study of the sampling distribution of .

Let , where is the Gram matrix. By definition, . Rewrite the KKT condition as

| (2.3) |

which shows that is a function of . On the other hand, determines only through , which implies that is unique for any as long as it is unique for any . Therefore, under the assumptions for the uniqueness of , is a bijection between and . For a fixed , the only source of randomness in the linear model (1.1) is the noise vector , which determines the distribution of . With the bijection between and , one may derive the joint distribution of , which has a closed-form density under a normal error distribution. Then we develop Monte Carlo algorithms to sample from this joint distribution and obtain the sampling distribution of . This is the key idea of this article, which works for both the low-dimensional setting () and the high-dimensional setting (). Although the basic strategy is the same, the technical details are slightly more complicated for the high-dimensional setting. For the sake of understanding, we first focus on the low-dimensional case in the remaining part of Section 2 and Section 3, and then generalize the results to the high-dimensional setting in Section 4.

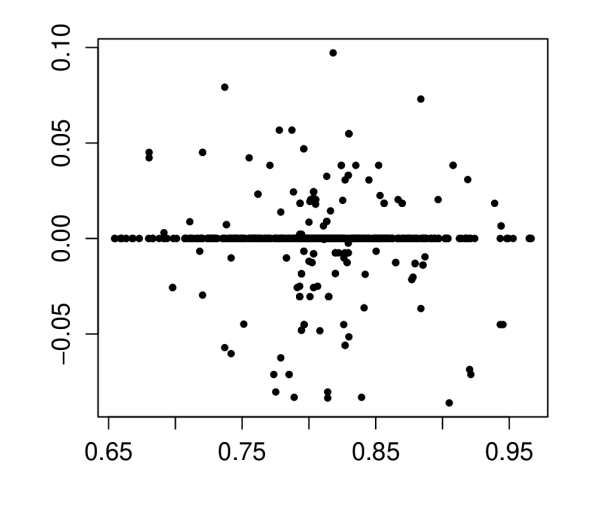

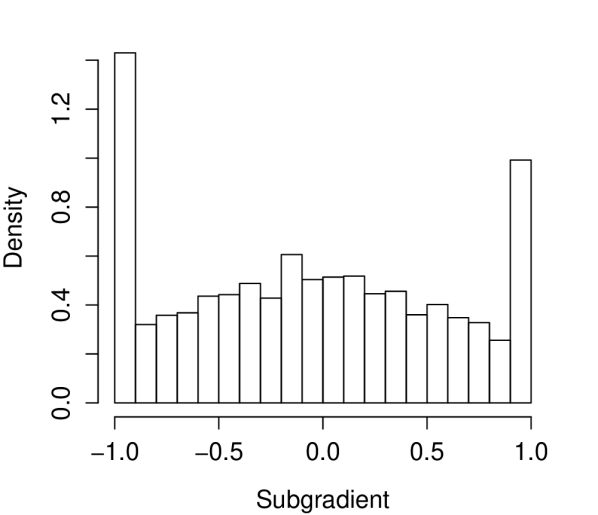

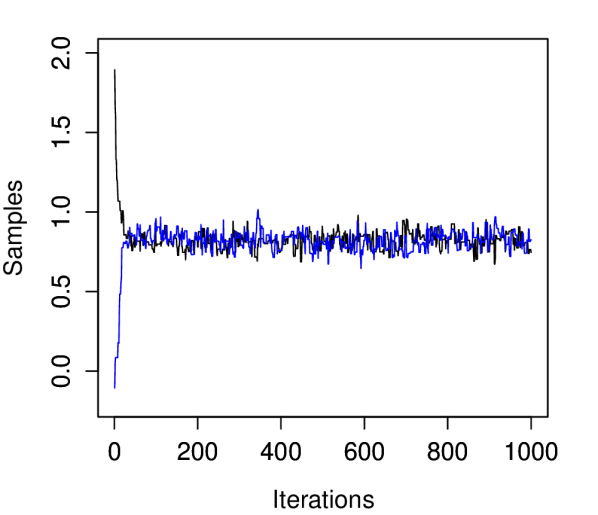

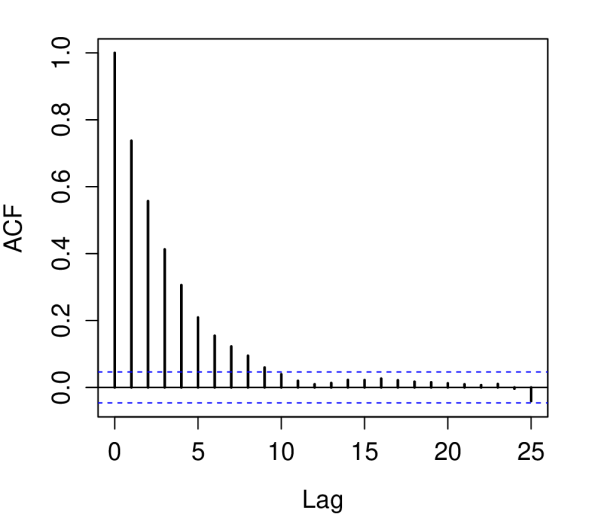

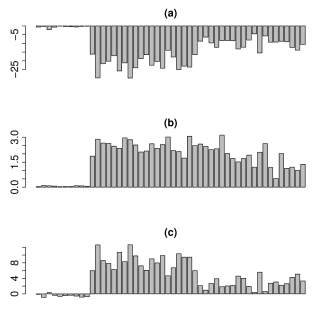

Before going through all the technical details, we take a glimpse of the utility of this work in a couple concrete examples. Given a design matrix and a value of , our method gives a closed-form joint density for the Lasso-type estimator and the subgradient under assumed values of the true parameters (Theorems 1 and 2). Targeting at this density, we have developed MCMC algorithms, such as the Lasso sampler in Section 3.2, to draw samples from the joint distribution of . Such MCMC samples allow for approximation of marginal distributions for a Lasso-type estimator. Figure 1 demonstrates the results of the Lasso sampler applied on a simulated dataset with , and a normal error distribution. The scatter plot in Figure 1(a) confirms that indeed may have a positive probability to be exactly zero in its sampling distribution. Accordingly, the distribution of the subgradient in Figure 1(b) has a continuous density on and two point masses on . The fast mixing and low autocorrelation shown in the figure are surprisingly satisfactory for a simple MCMC algorithm in such a high-dimensional and complicated space (, see (2.4)). Exploiting the explicit form of the bijection , we achieve the goal of sampling from the joint distribution of via an MCMC algorithm essentially targeting at a multivariate normal distribution (Section 3.5). This approach does not need numerical optimization in any step, which makes it highly efficient compared to bootstrap or resampling-based methods. Another huge potential of our method is its ability to estimate tail probabilities, such as small p-values in a significance test (Section 5). Estimating tail probabilities is challenging for any simulation method. With a suitable proposal distribution, having an explicit density makes it possible to accurately estimate tail probabilities by importance weights. For example, our method can estimate a tail probability on the order of , with a coefficient of variation around 2, by simulating only 5,000 samples from a proposal distribution. This is absolutely impossible when bootstrapping the Lasso or simulating from the sampling distribution directly.

(a)

(b)

(c)

(d)

2.2 The bijection

In the low-dimensional setting, we assume that , which guarantees that the columns of are in general position.

Before writing down the bijection explicitly, we first examine the respective spaces for and . Under the assumption that , the row space of is simply , which is the space for . Let be the active set of and be the inactive set, i.e., the set of the zero components of . After removing the degeneracies among its components as given in (2.2), the vector can be equivalently represented by the triple . They are equivalent because from one can unambiguously recover , by setting and (2.2), and vice versa. It is more convenient and transparent to work with this equivalent representation. One sees immediately that lies in

| (2.4) |

where . Hereafter, we always understand as the equivalent representation of with and . Clearly, , where is the collection of all subsets of , and thus lives in the product space of and a finite discrete space.

Partition as and as . Then the KKT condition (2.3) can be rewritten,

| (2.9) | |||||

| (2.12) |

where is a matrix. Permuting the rows of , one sees that

| (2.13) |

if . Due to the equivalence between and , the map defined here is essentially the same as the one defined in (2.3).

Lemma 2.

If , then for any and , the mapping defined in (2.12) is a bijection that maps onto .

Proof.

For any , there is a unique solution to Equation (2.3) if , and thus, a unique such that . For any , maps it into . ∎

It is helpful for understanding the map to consider its inverse and its restriction to , where is a fixed subset of . For any , if , then the unique solution to Equation (2.9) is . Given a fixed , lives in the subspace

| (2.14) |

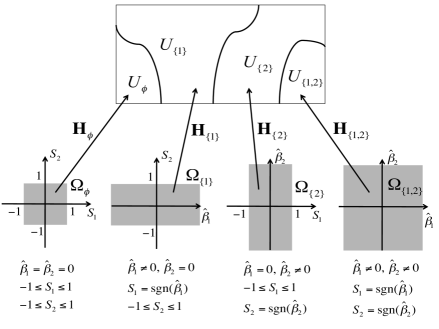

Let for and be the image of under the map . Now imagine we plug different into Equation (2.9) and solve for . Then the set is the collection of all possible solutions such that , the set is the collection of all that give these solutions, and is a bijection between the two sets. It is easy to see that , i.e., , for extending over all subsets of , form a partition of the space . The bijective nature of implies that also form a partition of , the space of . Figure 2 illustrates the bijection for and the space partitioning by . In this case, map the four subspaces for , each in a different , onto the space of which is another .

Remark 1.

The simple fact that maps every point in into is crucial to the derivation of the sampling distribution of in the low-dimensional setting. This means that every is the solution to Equation (2.9) for , and therefore one can simply find the probability density of at by the density of at . This is not the case when (Section 4).

2.3 The sampling distribution

Now we can use the bijection to find the distribution of from the distribution of . Let denote -dimensional Lebesgue measure.

Theorem 1.

Assume that and let be the probability density of with respect to . For , the joint distribution of is given by

| (2.15) | |||||

and the distribution of is a marginal distribution given by

| (2.16) |

Proof.

Remark 2.

Equation (2.15) gives the joint distribution of and effectively the joint distribution of . The density is defined with respect to the product of and counting measure on . Analogously, the sampling distribution of is given by the distribution of in (2.16). To be rigorous, (2.15) is derived by assuming that is an interior point of . Note that is not in the interior if and only if for some , and thus the Lebesgue measure of the union of these points is zero. Therefore, it will cause no problem at all to use as the density for all points in . The joint distribution of has at least two nice properties which make it much more tractable than the distribution of . First, the density does not involve multidimensional integral and has a closed-form expression that can be calculated explicitly if is given. Second, the continuous components always have the same dimension for any value of , while lives in whose dimension changes with . These two properties are critical to the development of MCMC to sample from . See Section 3.1 for more discussion. We explicitly include the dominating Lebesgue measure to clarify the dimension of a density.

Remark 3.

The distribution of in (2.16) is essentially defined for each . In many problems, one may be interested in the marginal distribution of such as for calculating p-values and constructing confidence intervals. To obtain such a marginal distribution, we need to sum over all possible active sets, which cannot be done analytically. Our strategy is to draw samples from the joint distribution of by a Monte Carlo method. Then from the Monte Carlo samples one can easily approximate any marginal distribution of interest, such as that of . This is exactly our motivation for estimator augmentation, which is in spirit similar to the use of auxiliary variables in the MCMC literature.

To further help our understanding of the density , consider a few conditional and marginal distributions derived from the joint distribution (2.15). First, the sampling distribution of the active set is given by

| (2.17) |

where is the subspace for defined in (2.14). In other words, is the probability of with respect to the joint distribution . Second, the conditional density of given (with respect to ) is

| (2.18) |

for . Using as an illustration, the joint density is defined over all four shaded areas in Figure 2, while a conditional density is defined on each one of them. To give a concrete probability calculation, for ,

which is an integral over the rectangle in (Figure 2). Clearly, this probability can be approximated by Monte Carlo integration if we have enough samples from .

Remark 4.

We emphasize that the weights and the tuning parameter are assumed to be fixed in Theorem 1. For the adaptive Lasso, one may choose based on an initial estimate . The distribution (2.15) is valid for the adaptive Lasso only if we ignore the randomness in and regard as constants during the repeated sampling procedure.

2.4 Normal errors

Denote by the -variate normal distribution with mean and covariance matrix , and by its probability density function. If the error and , then . In this case, the joint density (2.15) has a closed-form expression. Recall that and define

| (2.19) | |||||

| (2.20) |

Corollary 1.

If and , then the joint density of is

| (2.21) |

where and is an indicator function.

Proof.

Without the normal error assumption, Corollary 1 is still a good approximation when is large and is fixed, since assuming as .

Note that both the continuous components and the active set are arguments of the density (2.21). For different and , the normal density has different parameters. Given a particular and , let and

| (2.23) |

Then is the subset of corresponding to the event . For , the density is identical to , i.e.,

Intuitively, this is because restricted to and is simply an affine map [see (2.22)]. Consequently, the probability of with respect to is

| (2.24) |

and is the truncated on . For , if , and , the region is the left half of the in Figure 2 and the density restricted to this region is the same as the part of a bivariate normal density on the same region.

If and , the Lasso is equivalent to soft-thresholding the ordinary least-squares estimator . In this case, (2.19) and (2.20) have simpler forms:

By (2.24) we find, for example,

where the last equality is due to that . One sees that our result is consistent with that obtained directly from soft-thresholding each component of by .

2.5 Estimation

To apply Theorem 1 in practice, one needs to estimate and if they are not given. Suppose that is estimated by and is estimated by . Then, the corresponding estimate of the density is

| (2.27) |

Since and , estimating reduces to estimating when is normally distributed or when the sample size is large. A consistent estimator of can be constructed given a consistent estimator of . For example, when one may use

| (2.28) |

provided that is consistent for . If does not follow a normal distribution, one can apply other parametric or nonparametric methods to estimate . Here, we propose a bootstrap-based approach under the assumption that is elliptically symmetric. That is, is spherically symmetric: For , if then , where is the density of . Generate bootstrap samples, for , by resampling with replacement from , and calculate for each . Given , let for . The density of is then estimated by

| (2.29) |

for . The density for can be estimated by linear extrapolation of . Finally, set .

In general, estimating is difficult when is large. One may have to assume some parametric density for , which reduces the problem to the estimation of a few unknown parameters. Besides normality, one may assume that follows a multivariate distribution, which is motivated from a Bayesian perspective to be discussed in Section 7.3.

Sampling from or can be very useful for statistical inference based on a Lasso-type estimator. We may directly draw from given and use the conditional distribution to construct confidence regions around . Under some assumptions, the conditional distribution provides a valid approximation to the true sampling distribution of . We derive nonasymptotic error bounds for this approximation in Section 6 after the development of our method in the high-dimensional setting. If is specified in the null hypothesis in a significance test, then samples from can be used to calculate p-values. This aspect will be explored in Section 5.

3 MCMC algorithms

In this section, we develop MCMC algorithms to sample from given and (or ). Before that, we first introduce a direct sampling approach which includes the residual bootstrap method as a special case.

Routine 1 (Direct sampler).

Assume the error distribution is . For

-

(1)

draw and set ;

-

(2)

find the minimizer of (1.2) with in place of ;

-

(3)

if needed, calculate the subgradient vector .

This approach directly draws from its sampling distribution and requires a numerical optimization algorithm in step (2) for each sample. Moreover, step (1) will be complicated if we cannot draw independent samples from . If is drawn by resampling residuals, then Routine 1 is equivalent to the bootstrap method of Knight and Fu (2000).

As the density (2.15) has a closed-form expression given and , MCMC and IS can be applied to sample from and calculate expectations with respect to the distribution. These methods may offer much more flexible and efficient alternatives to the direct sampling approach, although the samples are either dependent or weighted. In what follows, we propose a few special designs targeting at different applications to exemplify the use of MCMC methods. Examples of IS will be given in Section 5 under the high-dimensional setting.

3.1 Reversibility

Our goal is to design a reversible Markov chain on the space , which is composed of a finite number of subspaces , each having the same dimension . Therefore, moves with an ordinary Metropolis-Hastings (MH) ratio are sufficient, which can be seen as follows. For any , let with components given by

| (3.1) |

i.e., and . Then our target distribution is . Suppose that is the current state and we have a proposal for a new state . In general, the proposal may only change some components of , say for , such that . Let be the density of this proposal with respect to and . The MH ratio in terms of probability measures is

| (3.2) | |||||

As , the dominating measures in (3.2) cancel out and the ratio reduces to a standard MH ratio involving only densities.

Now we see that our strategy of estimator augmentation plays two roles in MCMC sampling. First, plays the role of an auxiliary variable: The target distribution for has a closed-form density which allows one to design an MCMC algorithm, while the distribution of interest, that for , is a marginal distribution of without a closed-form density. Second, also plays the role of dimension matching so that the continuous components always have the same dimension in any subspace. This eliminates the need for reversible jump MCMC (Green 1995). On the contrary, if we were to sample (assuming a closed-form approximation to its density), moves between two subspaces of different dimensions would require reversible jumps, which are usually much harder to design.

3.2 The MH Lasso sampler

We develop an MH algorithm, called the MH Lasso sampler (MLS), with coordinate-wise update. That is, to sequentially update each , , while holding other components fixed. Suppose the current state is . We design four moves to propose a new state , which are grouped into two types according to whether or not. In the following proposals, if and otherwise.

Definition 1.

Proposals in the MLS for a given .

-

•

Parameter-update proposals: (P1) If , draw . (P2) If , draw . Set in both (P1) and (P2).

-

•

Model-update proposals: (P3) If , set and draw . (P4) If , set and draw .

The two parameter-update proposals, (P1) and (P2), are symmetric. They only change the value of and leave so that . From (2.15), one sees that the MH ratio is simply

which can be computed very efficiently, especially for a normal error distribution. The proposal (P3) removes a variable from the active set and (P4) adds a variable to the active set. Both propose moves between two subspaces. The two proposals are the reverse of each other and have a simple one-dimensional density. To be concrete, the MH ratio for proposal (P3) is

and analogously for proposal (P4). One needs to calculate the ratio between two determinants for these MH ratios,

| (3.3) |

by (2.13). As the two sets and differ by only one element, the ratio on the right-hand side can be calculated efficiently. When is large, we use the sweep operator to dynamically update (the inverse of ) and obtain the ratio. See Appendix for further details. In general, however, a model-update proposal is more time-consuming than a parameter-update proposal.

This computational efficiency consideration motivates the following scheme in the MLS which uses both types of proposals. Let be an integer between 1 and and be a vector with every .

Routine 2 (MLS).

Suppose the current state is .

-

(1)

Draw elements without replacement from with the probability of drawing proportional to for each . Let be the set of the elements.

-

(2)

For , sequentially update each and the active set by an MH step with a model-update proposal.

-

(3)

For , sequentially update each by an MH step with a parameter-update proposal.

After the above MH steps in an iteration, the state is updated to .

The MLS has three input parameters, , , and . Specification of these parameters that gives good empirical performance will be provided in the numerical examples (Section 3.6).

3.3 The Gibbs Lasso sampler

Let and . Conditional densities can be derived from the joint density , which allows for the development of a Gibbs sampler. However, as each conditional sampling step involves calculation of one-dimensional integrals and sampling from truncated distributions, the Gibbs sampler is more time-consuming and less efficient than the MLS for all examples on which we have tested these algorithms.

3.4 Conditioning on active set

Suppose that we have constructed a Lasso-type estimate from an observed dataset and the set of selected variables is , which defines an estimated model. One may want to study the sampling distribution of the estimator given the estimated model, i.e., . Confidence intervals of penalized estimators have been constructed by approximating this distribution via local expansion of the norm (Fan and Li 2001; Zou 2006). Since local approximation may not be accurate for a finite sample, Monte Carlo sampling from this conditional distribution may provide more accurate results. However, the direct sampling approach is not applicable in practice, because is often a rare event unless is very small. On the contrary, it is very efficient to draw samples by an MH algorithm from the conditional distribution

| (3.4) |

where , according to (2.18). The distribution of interest, , is a marginal distribution of (3.4). Since evaluation of this density does not involve calculation of determinants, each MH step is very fast.

Routine 3 (MLS given active set).

Given the current state , sequentially draw for each by an MH step with proposal (P1) and for each with proposal (P2) in one iteration.

3.5 Reparameterization view

To ease notation, write and for defined in (3.1). Suppose that are simulated by the MLS (Routine 2) and let . Since is a bijection, is a Markov chain that leaves invariant. Therefore, the MLS can be understood as an MH algorithm targeting at with moves designed under local reparameterization, for (2.14). The Jacobian of this reparameterization is . Under this view, the MH ratio for a proposal given the current is

which of course coincides with (3.2). Moreover, when such as in proposals (P1) and (P2), the Jacobian determinants cancel out as we are using the same reparameterization for both the proposal and the current state. Otherwise, the ratio of the Jacobian determinants accounts for the use of different reparameterizations. Clearly, if then .

This view provides an insight into the computational efficiency of the MLS. Under normal error assumption, is the density of a multivariate normal distribution, for which a simple MH algorithm is computationally tractable and can be quite efficient. We make a comparison with the direct sampler at a conceptual level. The direct sampler draws via a linear transformation of , which costs draws from a univariate normal distribution followed by a multiplication with a size matrix. After that, we find by numerical minimization due to the lack of a closed-form inverse of the mapping . The MLS draws () univariate proposals in one iteration, and does not need any numerical procedure to map back to the space of since the moves are by design in that space already. The mapping from to is simple and can be calculated analytically. This is fundamentally different from direct sampling which replies on a numerical procedure to find the image of each draw of under the mapping . The relatively time-consuming step in the MLS is calculating the ratio (3.3) when a model-update proposal is used, which can be done by at most sweeping a matrix on a single position (Appendix). Owing to sparsity, is usually much smaller than , which greatly speeds up this step. Since the target distribution in the space of has a nice unimodal density, the chain often converges fast and has low autocorrelation. Consequently, we expect to see efficiency gain over direct sampling for the same amount of computing time, which will be confirmed numerically in the next subsection.

As in the following routine, by a special initialization such that , the MLS can reach equilibrium in one step, which totally removes the need for burn-in iterations. This will make our method suitable for parallel computing. See Section 7.4 for a more detailed discussion. However, to demonstrate the efficiency of the MLS as an independent method, we did not use Routine 4 in the numerical results.

Routine 4.

Draw from the direct sampler and let be its equivalent representation. With as the initial state, generate for by an MCMC algorithm targeting at .

3.6 Numerical examples

We demonstrate with numerical examples the effectiveness of the above MCMC algorithms by comparing against the direct sampling approach. To this end, we simulated four datasets with different combinations of , , and (Table 1). The vector of true coefficients has 10 nonzero components, for and for . Each row of was generated independently from , where the diagonal and the off-diagonal elements of are 1 and , respectively. Given the design matrix , the response vector was drawn from .

| Dataset | A | B | C | D |

|---|---|---|---|---|

| 23 | 22 | 25 | 57 |

The weights (1.2) were set to 1 for all the following numerical results. The Lars package by Hastie and Efron was applied to find the solution path for each dataset. The value of was chosen by minimizing the criterion implemented in the package, which determined the estimated coefficients, , of a dataset. The number of selected variables, , for each dataset is given in Table 1. We considered two types of error distributions, the normal distribution and the elliptically symmetric distribution. Correspondingly, we calculated by (2.28) with or constructed by the approach in Section 2.5. For all the results, step (2) of the direct sampler (Routine 1) was implemented with the Lars package.

We first examined the performance of the MLS on sampling from the joint distribution (2.15) given and or . Let for , where is the standard error of and is the cumulative distribution function of . We set and , where serves as a baseline weight so that each variable has a reasonable chance to be selected for model-update proposals. See Routine 2 for notations. Under this setting, if the estimate is close to zero relative to , it will have a higher chance for model-update proposals. The used in the proposals (Definition 1) was set to . The MLS was applied to each dataset 10 times independently. Each run consisted of iterations with the first 500 as the burn-in period. In what follows, the sampler is abbreviated as MLSn and MLSe under the normal and the elliptically symmetric error distributions, respectively.

Figure 1(a) is the scatter plot of the samples of and , and illustrates that the distributions of some indeed have a point mass at zero. The histogram of the subgradient is shown in Figure 1(b) with two point masses on and otherwise continuous. Mixing of the MLS was fast, as demonstrated with two chains in Figure 1(c), where the initial values were chosen to be about 20 standard deviations away from each other. Figure 1(d) shows the fast decay of the autocorrelation among the samples of a , decreasing to below 0.05 in 10 to 15 iterations. The acceptance rate of the model-update proposals was generally between 0.2 and 0.4. For the parameter-update proposals, the acceptance rate was between 0.2 and 0.4 for (P1) and was higher than 0.6 for (P2), which is an independent proposal.

From the MCMC samples, we estimated the selection probability , the 2.5% and the 97.5% quantiles of , and the mean and the standard deviation of the conditional distribution for each . Since theoretical values are not available, we applied the direct sampling approach to simulate 5,000 independent samples for each dataset under the normal error distribution. These independent samples were used to estimate the above quantities as the ground truth. The MSEs across 10 independent runs of the MLS were calculated, and reported in Table 2 are the average MSEs over all for estimating the above five quantities. One clearly sees that all the estimates were very accurate. The MSE of the MLSe was greater than, but on the same order as, that of the MLSn for most estimates, which is expected due to the loss of efficiency without assuming a normal error distribution.

| Method | 2.5% | 97.5% | mean | SD | ||

|---|---|---|---|---|---|---|

| MLSn | ||||||

| A | MLSe | 1.29 | 1.20 | 1.19 | 0.97 | 1.38 |

| DSn | 1.11 | 2.28 | 2.45 | 2.23 | 2.53 | |

| MLSn | ||||||

| B | MLSe | 1.20 | 1.07 | 1.10 | 1.08 | 1.30 |

| DSn | 1.26 | 1.97 | 1.89 | 2.29 | 2.74 | |

| MLSn | ||||||

| C | MLSe | 1.55 | 2.09 | 1.78 | 1.03 | 2.46 |

| DSn | 0.47 | 1.18 | 1.33 | 1.24 | 1.39 | |

| MLSn | ||||||

| D | MLSe | 2.74 | 3.81 | 3.61 | 1.17 | 5.70 |

| DSn | 0.69 | 1.52 | 1.34 | 1.21 | 1.57 |

Note: For the MLSe and the DSn, reported is the ratio of MSE to that of the MLSn. The sweep operator was used in the MLS to calculate determinant ratios for dataset D.

We compared the efficiency of the MLS against the direct sampler (DSn) under the same amount of running time and under the same normal error distribution. The DSn generated around 500 samples in the same amount of time for 5,500 iterations of the MLSn. The ratio of the MSE of the DSn to that of the MLSn was calculated for each estimate (Table 2). For most estimates, the MLSn seems to be more efficient and may reduce the MSE by 10% to 60%. The improvement was more significant for datasets A and B where the sample size . For the other two datasets, the MLSn showed a higher MSE in estimating selection probabilities but was more accurate for all other estimates. Furthermore, if the error distribution is more complicated such that one cannot simulate samples independently from the distribution, the efficiency of the direct sampler may be even lower. These results clearly confirm the notion that the MLS can serve as an efficient alternative to the direct sampling method for simulating from the sampling distribution of a Lasso-type estimator.

Next, we implemented Routine 3 to sample from the conditional distribution of given the model selected according to the criterion, i.e., with given in Table 1. The same parameter setting as that in the previous example was used to run the MLSn and the MLSe. We estimated the 2.5% and the 97.5% quantiles, the mean, and the standard deviation of for . The model space is composed of models, and the probability of the model , , is practically zero for the datasets used here. Therefore, the direct sampling approach is not applicable. This shows the advantage and flexibility of the Monte Carlo algorithms. Since we cannot construct ground truth for this example, the accuracy of an estimate is measured by its variance across 10 independent runs of the MLS, averaging over (Table 3). The variance of every estimate was on the order of or smaller for datasets A, B and C and was on the order of or smaller for dataset D under both error models. This highlights the stability of the MLS in approximating sampling distributions across different runs. There were cases in which the variance of the MLSe was smaller. This does not necessarily suggest that the MLSe provided a more accurate estimate, as the loss of efficiency without the normal error assumption is likely to result in a higher bias.

| Method | 2.5% | 97.5% | mean | SD | |

|---|---|---|---|---|---|

| A | MLSn | ||||

| MLSe | 0.90 | 1.02 | 0.92 | 1.05 | |

| B | MLSn | ||||

| MLSe | 1.22 | 1.15 | 1.02 | 1.23 | |

| C | MLSn | ||||

| MLSe | 1.07 | 0.95 | 1.01 | 1.00 | |

| D | MLSn | ||||

| MLSe | 0.77 | 0.97 | 0.77 | 0.79 |

Note: Variance of the MLSe is reported as the ratio to that of the MLSn.

4 High-dimensional setting

Recent efforts have established theoretical properties of -penalized linear regression in high dimension with (Meinshausen and Bühlmann 2006; Zhao and Yu 2006; Zhang and Huang 2008; Bickel et al. 2009). Under this setting, we assume . Consequently, is an -dimensional subspace of and the Gram matrix has positive eigenvalues, denoted by , . The associated orthonormal eigenvectors , , form a basis for . Choose orthonormal vectors to form a basis for the null space of , , and let . Then and index the columns of that form respective bases for and .

Assumption 1.

Every columns of are linearly independent and every rows of are linearly independent.

The first part of this assumption is sufficient for the columns of being in general position, which guarantees that is unique for any and (Lemma 1). The second part will ease our derivation of the joint density of the augmented estimator. Note that Assumption 1 holds with probability one if the entries of are drawn from a continuous distribution on .

4.1 The bijection

Although is a -vector, by definition it always lies in . Therefore, and the -vector gives the coordinates of with respect to the basis . If follows a continuous distribution on , then has a proper density with respect to . For example, if , then with . Now plays the same role as does in the low-dimensional case. We will use the known distribution of to derive the distribution of the augmented estimator .

However, a technical difficulty is that when , the map defined in (2.12) is not a mapping from to as is not necessarily in for every . We thus need to remove those “illegal” points in so that the image of always lies in the row space of . This is achieved by imposing the constraint that

| (4.1) |

i.e., the image of must be orthogonal to . It is more convenient to use the equivalent definition of in (2.3), i.e.,

| (4.2) |

Because , constraint (4.1) is equivalent to

| (4.3) |

In words, the constraint is that the vector must lie in . Therefore, we have a more restricted space for the augmented estimator in the high-dimensional case,

| (4.4) |

Restricted to this space, is a bijection.

Lemma 3.

Proof.

Remark 5.

Now we represent the bijection in terms of its coordinates with respect to and equate it with :

| (4.5) |

4.2 Joint sampling distribution

The distribution for is completely given by the distribution of via the bijective map . The only task left is to determine the Jacobian of , taking into account the constraint (4.3). Left Multiplying by both sides of Equation (2.9), with the simple facts that and , gives

| (4.6) |

For any fixed value of , differentiating and both sides of the constraint (4.3) with respect to give, respectively,

| (4.7) | |||

| (4.8) |

Therefore, the constraint implies that is in .

Lemma 4.

If and Assumption 1 is satisfied, then the dimension of is .

Proof.

Let be an orthonormal basis for . Let be the coordinates of with respect to the basis , i.e., . Note that according to the above lemma. Then (4.7) becomes

| (4.11) | |||||

where , an matrix, is the Jacobian of the map . The dimension of is always for any . This confirms the notion in Remark 5 that the continuous components lie in an -dimensional subspace when is fixed.

Now we are ready to derive the density for in high dimension. For , for some and gives the infinitesimal volume at subject to constraint (4.4).

Theorem 2.

Assume that and Assumption 1 holds. Let be the probability density of with respect to . For , the joint distribution of is given by

| (4.12) | |||||

Particularly, if , then

| (4.13) |

Proof.

Remark 6.

The density does not depend on which orthonormal basis we choose for . If is another orthonormal basis, then , where is an orthogonal matrix and . Correspondingly,

and thus .

Remark 7.

One may unify Theorems 1 and 2 with the use of cumbersome notations, but the idea is simple. Note that and in (2.12) are connected by

If , the set reduces to the empty set and . Hence, the constraint (4.3) no long exists, the space is the same as , and is simply for any . Choosing leads to , which shows that the probability in (4.12) reduces to that in (2.15). In this case, , i.e., a column of gives the coordinates of the corresponding column of with respect to the basis .

In principle, one can develop MCMC algorithms to sample from the joint distribution (4.12). Development of such an algorithm is a little tedious because of the constraints in the definition of and the use of different bases in different subspaces. However, the explicit density given in Theorem 2 allows us to develop very efficient IS algorithms for approximating tail probabilities with respect to the sampling distribution of a Lasso-type estimator.

5 P-value calculation by IS

To simplify description, we focus on the high-dimensional setting with normal errors so that the distribution of interest is (4.13). For a fixed , the density , the bijection (4.5) and the matrix (4.11) are written as , , and , respectively, to explicitly indicate their dependency on different parameters. Suppose we are given a Lasso-type estimate for an observed dataset with a tuning parameter . Under the null model , we want to calculate the p-value of some test statistic constructed from the Lasso-type estimator for . Precisely, the desired p-value is

| (5.1) |

where and . Even if we can directly sample from , estimating will be extremely difficult when it is very small. With the closed-form density , we can use IS to solve this challenging problem.

5.1 Importance sampling

Our target distribution is and we propose to use as a trial distribution to estimate expectations with respect to the target distribution via IS. First, note that the trial and the target distributions have the same support as the constraint in (4.4) that defines the space only depends on . Thus, a sample from the trial distribution also satisfies the constraint for the target distribution. Second, one can easily simulate from the trail distribution by the direct sampler (Routine 1). Third, the importance weight for a sample from the trial distribution can be calculated efficiently. Let and note that . Using the fact that , the importance weight

| (5.2) | |||||

Essentially, for each sample, we only need to compute the image of the map and two sums of squares.

Routine 5.

Draw , , from the trial distribution by Routine 1. Then the IS estimate for the p-value is given by

| (5.3) |

The key is to choose the parameters and in the trial distribution so that we have a substantial fraction of samples for which . Next we discuss some guidance on tuning these parameters.

5.2 Tuning trial distributions

We illustrate our procedure for tuning the trial distribution assuming , i.e., the null hypothesis is . In this case, the problem is difficult when is close to one under the target distribution . In other words, is too big to obtain any nonzero estimate of the coefficients and consequently the p-value becomes a tail probability. Thus, one may want to choose the trial distribution under which there is a higher probability for nonzero . In general, we achieve this by choosing () and then tuning accordingly. When we increase , the variance of increases and thus will have a wider spread in . This will increase the variance of the augmented estimator . As illustrated in Figure 2, a larger variance in will lead to a more uniform distribution over different subspaces .

The following simple procedure is used to determine given , which works very well based on our empirical study.

Routine 6.

Draw from and calculate for . Then set to the first quartile of .

Setting in (2.1), we have

which shows that the calculated in Routine 6 is the minimum value of with which for . Therefore, under the trial distribution , is around 25% and there is a 75% of chance for to have some nonzero components. This often results in a good balance between the dominating region of the target distribution () and the region of interest for p-value calculation (5.1). For all numerical examples in this article, we choose and .

5.3 Multiple tests

Consider multiple linear models with the same set of predictors,

| (5.4) |

where , , and . After proper rescaling of and , we may assume that all are identical, i.e., . Suppose we are interested in testing against null hypotheses and , given Lasso-type estimates with for . There are p-values to calculate,

| (5.5) |

where for . This problem occurs in various genomics applications. To give an example, may be the expression level of gene and the expression levels of transcription factors across individuals. The transcription factors may potentially regulate the expression of a gene through the linear model (5.4). Rejection of indicates that gene is regulated by at least one of the transcription factors.

To estimate all , we only need to draw , , from one trial distribution , in which and is obtained by applying the same tuning procedure (Routine 6) once. Then we calculate the importance weights by (5.2) for all target distributions, , , and construct estimates for all by (5.3).

Remark 8.

Alternatively, one may apply the Lars algorithm in the direct sampler to draw from the sampling distribution of given and for all , as the Lars algorithm provides the whole solution path. The computing time of both methods is dominated by drawing samples and thus is comparable. However, when is small, the IS method will be orders of magnitude more efficient than direct sampling, and when is not too small, the accuracy of the two methods is on the same order. We will see this in the numerical examples. In addition, we do not have to use the Lars algorithm to draw from the trial distribution since there is no need to compute the solution path for importance sampling. One thus has the freedom to choose other algorithms, such as coordinate descent (Friedman et al. 2007; Wu and Lange 2008), which may be more efficient when both and are large.

5.4 Numerical examples

We first simulated two datasets to demonstrate the effectiveness in p-value calculation by the IS method for individual tests. Each row of was generated from , where the diagonal and the off-diagonal elements of are 1 and , respectively. Given the predictors , the response vector was drawn from . We set all weights . Table 4 reports the values of , , , and for the two datasets. We applied the Lars algorithm on the two datasets and chose as the first along the solution path such that the Lasso estimate gave the correct number of active coefficients (Table 4). It turned out that only included one true active coefficient for both datasets. Let be the active set of . We designed the following test statistics, , , and for , and aimed to calculate p-values under the null hypothesis and .

| Dataset | ||||||

|---|---|---|---|---|---|---|

| E | 5 | 10 | 1/4 | 1.65 | 0.60 | |

| F | 10 | 20 | 1/4 | 0.315 | 0.57 |

We chose and used Routine 6 to choose for the trial distributions. The values of for the two datasets are given in Table 4. When is sufficiently large for a dataset, the tuned by Routine 6 can be greater then (dataset F). The IS method (Routine 5) was applied with to estimate p-values for all the above tests. This estimation procedure was repeated 10 times independently to obtain the standard deviation of an estimated p-value. We quantify the efficiency of an estimated p-value, , by its coefficient of variation , where the standard deviation and the mean are calculated across multiple runs. Table 5 summarizes the results, where for dataset E and for dataset F. One sees that the IS estimates were very accurate: Even for a tail probability as small as , the coefficient of variation was less than or around 2. To benchmark the performance, we approximated the coefficient of variation of the estimate constructed by direct sampling from the target distribution, with . As reported in the table, for estimating an extremely small p-value, can be orders of magnitude greater than that of an IS estimate, and for a moderate p-value (around ), the two methods showed comparable performance.

| 2.37 | |||||

| E | 1.09 | ||||

| 1.81 | |||||

| 1.16 | |||||

| 0.30 | 11.5 | ||||

| 0.11 | 0.41 | ||||

| F | 0.38 | 1.87 | |||

| 0.12 | 0.14 | ||||

| 0.08 | 0.09 | ||||

| 0.31 | 2.04 |

Next, we simulated datasets to test our p-value calculation for the multiple testing problem. We used the design matrix in dataset F and . The response vector was drawn from , where the true coefficient vector is given in Table 6 for . For 10 datasets, and the null hypothesis is true. For 20 datasets, there are two large coefficients, which represents the case that the true model is sparse. The other 20 datasets mimic the scenario in which the true model has many relatively small coefficients. We chose as the first that gave two active coefficients along the solution path and used as the test statistic. Summaries of and for the 50 datasets are provided in Table 6 as well, from which we see that these datasets cover a wide range of and . We chose . As seen from Routine 6, for identical and , the tuning procedure is the same. Therefore, we simply set , the value we used for dataset F (Table 4).

| Dataset | range of | range of | |

|---|---|---|---|

| 1-10 | (0.16, 0.34) | (0.08, 0.23) | |

| 11-30 | (0.88, 1.31) | (0.27, 0.84) | |

| 31-50 | (0.70, 1.13) | (0.04, 0.51) |

We simulated samples from the trial distribution and estimated the p-values for all the 50 datasets. This procedure was repeated 10 times independently. The average over 10 runs of the estimated p-value, , is shown in Figure 3(a) for . As expected, most of the p-values for the first 10 datasets were not significant, while those for the other 40 datasets ranged from to , which confirms that is a reasonable test statistic. Again, we see that even for p-values on the order of , the coefficient of variation of an IS estimate was at most around 3 (Figure 3(b)). This provides huge gain in accuracy compared to direct sampling. Figure 3(c) plots for the 50 datasets, where was approximated in the same way as in the previous example. It is comforting to see that while the IS estimates showed huge improvement over the DS estimates in estimating a tail probability, they were only slightly worse than the DS estimates for an insignificant p-value. For the first 10 datasets, the coefficient of variation of was at most 7.9 times that of . For majority of the other 40 datasets, the ratio of over was between and .

6 Estimating sampling distributions

For a vector , denote its active set by . Let be the true coefficient vector and . Consider model (1.1) with and . The penalized loss in (1.2) is, up to an additive constant,

| (6.1) |

where , , and . Assuming has a unique minimizer,

| (6.2) |

where is the Lasso-type estimator that minimizes (1.2). Suppose that and are estimators of and , following their respective sampling distributions. Let

| (6.3) |

where and . For random vectors and , we use to denote the distribution of and to denote the conditional distribution of given . In general, is a random probability measure. The goal of this section is to derive nonasymptotic bounds on the difference between and , with all proofs relegated to Section 8. Our results provide theoretical justifications for any method that estimates the uncertainty in via simulation from . In particular, for estimator augmentation, we draw from an estimated sampling distribution whose density is given by (2.21) or (4.13) with and .

6.1 Relevant existing results

We compile relevant published results here. The following restricted eigenvalue (RE) assumption is a special case of the one used in Lounici et al. (2011), which extends the original definition in Bickel et al. (2009).

Assumption 2 (RE).

For some positive integer and a positive number , the following condition holds:

Lemma 5 is from Theorem 3.1 and its proof in Lounici et al. (2011), regarding the Lasso as a special case of the group Lasso (Yuan and Lin 2006) with the size of every group being one.

Lemma 5.

Consider the model (1.1) with and , , and let , . Suppose that all the diagonal elements of are and . Let , where , and Assumption RE be satisfied. Choose and

| (6.4) |

where . Then on the event , which happens with probability at least , for any minimizer of (1.2) we have

| (6.5) | ||||

| (6.6) |

where is the maximum eigenvalue of . If Assumption RE is satisfied, then on the same event,

| (6.7) |

As an immediate consequence of this lemma, the Lasso-type estimator has the screening property assuming a suitable beta-min condition.

Lemma 6.

Let the assumptions in Lemma 5 be satisfied. If , then on the event , for any . If , then on the same event,

6.2 Known variance

In this subsection we assume that the noise variance is known and fix in the definition of (6.3). We first regard as a fixed vector and find conditions which are sufficient for the distribution of to be close to that of . Then we construct an estimator that satisfies these conditions with high probability. Let

| (6.8) |

Lemma 7.

Assume that the columns of are in general position. Fix . Suppose that is a fixed vector in so that (i) for all and (ii) as defined in (6.8). Let and assume

| (6.9) |

Then we have

One possible way to construct that satisfies conditions (i) and (ii) in Lemma 7 is to threshold the Lasso-type estimator by a constant , i.e.,

| (6.10) |

Theorem 3.

Remark 9.

Depending on the estimator , the conditional probability is a random variable. The probability is with respect to the sampling distribution of . This theorem gives an explicit nonasymptotic bound (6.12) on the difference between the two probability measures, and , and justifies simulation from the estimated sampling distribution with .

Remark 10.

Consider the asymptotic implications of Theorem 3 by allowing as . Suppose that and stay bounded away from 0 and . For the Lasso, . Choose so that , i.e., the convergence rate of is . For any , there is so that . Let in Lemma 5 and assume that when . With a suitable choice of ,

Because , we have . Thus, the order of satisfies

| (6.13) |

Consequently, a sufficient condition for (6.11) is

| (6.14) |

with the order of in between. Theorem 3 then implies that (6.12) holds with probability at least as . Choosing arbitrarily close to zero, this demonstrates that

| (6.15) |

As may decay to zero at a rate slower than , Theorem 3 applies in the high-dimensional setting ().

6.3 Unknown variance

When is unknown, recall that and . Denote the components of by , . Define

| (6.16) |

whose distribution does not depend on and is identical to that of when is fixed to . Thus, results in Section 6.2 show that is close to . We will further bound the difference, , in this subsection. In other words, serves as an intermediate variable between and to help quantify the difference between their distributions.

Lemma 8.

Assume that the columns of are in general position. Let and be fixed such that with and

| (6.17) |

If Assumption RE is satisfied, then on the event ,

| (6.18) |

Based on (6.18), we can obtain an upper bound on via the restricted eigenvalues of . Define the minimum restricted eigenvalue of for an integer by

| (6.19) |

and let

which is twice the upper bound on in (6.5).

Theorem 4.

Remark 11.

Assume that with . Following the asymptotic framework in Remark 10, we can establish by the same reasoning that

| (6.23) |

Suppose that for and that is bounded from above by a constant (or at least does not diverge too fast). Then and is bounded from below by a positive constant. The upper bound in (6.22) becomes as (6.13) and . If , then (6.22) implies that

for any . Combing with (6.23) this shows that, with probability tending to one, converges weakly to for any fixed index set . If is estimated by the scaled Lasso (Sun and Zhang 2012), one may reach under certain conditions by their Theorem 2 and it is then sufficient to have . If is fixed, we only need and hence any consistent estimator of will be sufficient. In this case, (6.13) and with probability tending to one, converges weakly to .

The key assumptions on the underlying model are the RE assumption on the Gram matrix and beta-min and sparsity assumptions on the true coefficients , which are comparable to those in Lemma 5 and Lemma 6. There is an extra assumption that in Theorem 4, which is again imposed on the restricted eigenvalues of . If is drawn from a continuous distribution on , then with probability one for any . It should be noted that we do not assume the irrepresentable condition (Zhao and Yu 2006; Meinshausen and Bühlmann 2006; Zou 2006), which is much stronger than the assumptions on the restricted eigenvalues of .

We compare our results to residual bootstrap for approximating the sampling distribution of the Lasso. To be precise, a residual bootstrap is equivalent to Routine 1 with estimated by and drawn by resampling residuals. Assuming is fixed, Knight and Fu (2000) argue that the residual bootstrap may be consistent if is model selection consistent and Chatterjee and Lahiri (2011) establish such fixed-dimensional consistency when is constructed by thresholding the Lasso, in the same spirit as (6.10). As discussed above, Theorem 4 applied to a fixed is clearly in line with these previous works. However, our results are much more general by providing explicit nonasymptotic bounds that imply consistency when . More recently, Chatterjee and Lahiri (2013) have shown that the residual bootstrap is consistent for the adaptive Lasso (Zou 2006) when under a number of conditions. A fundamental difference is that the weights are specified by an initial -consistent estimator in their work and will not stay bounded as . Therefore, their results do not apply to the Lasso. On the contrary, the results in this section are derived assuming the weights are constants without being specified by any initial estimator. In addition, Chatterjee and Lahiri (2013) impose in their Theorem 5.1 that for some when , which disallows the decay of the magnitudes of nonzero coefficients as grows. This is considerably stronger than our assumption (6.14).

7 Generalizations and discussions

7.1 Random design

We generalize the Monte Carlo methods to a random design, assuming that is drawn from a distribution . The distribution of the augmented estimator , (2.15) and (4.12), becomes a conditional distribution given , written as and , respectively.

In the low-dimensional setting, we may generalize the MLS (Routine 2) to draw samples from and approximate the sampling distribution of . It may be difficult to assume or estimate a reliable density for , but it is sufficient for the development of an MH sampler under a random design (rdMLS) if we can draw from . As seen below, we do not need an explicit form of for computing the MH ratio (7.1) and thus may draw by the bootstrap.

Routine 7 (rdMLS).

Suppose the current sample is .

-

(1)

Draw from , and accept it as with probability

(7.1) otherwise, set .

-

(2)

Regarding as the target density, apply one iteration of the MLS (Routine 2) to obtain .

Generalization of the IS algorithm (Routine 5) is also straightforward. Draw from and draw from the trial distribution given . Calculate importance weights by (5.2) with , and apply the same estimation (5.3). Again, an explicit expression for is unnecessary. But bootstrap sampling from is not a choice for the high-dimensional setting, because a bootstrap sample from violates Assumption 1.

7.2 Model selection consistency

The distribution of the augmented estimator may help establish asymptotic properties of a Lasso-type estimator. Here, we demonstrate this point by studying the model selection consistency of the Lasso. Our goal is not to establish new asymptotic results, but to provide an intuitive and geometric understanding of the technical conditions in existing work. Recall that and are the respective active sets of and . Let and . Without loss of generality, assume and . We allow both and to grow with .

Definition 2 (sign consistency (Meinshausen and Yu 2009)).

We say that is sign consistent for if

| (7.2) |

If is unique, the size of its active set (Lemma 4), and thus is invertible from (2.13). Therefore, the definitions of and in (2.19) and (2.20) are also valid for any when . Rewrite the KKT condition (2.12) as

| (7.3) |

where . Fixing and in (7.3), we define a random vector

| (7.4) |

via an affine map of . Note that we always have and , regardless of the sizes of and . When , is semipositive definite, meaning that components of are linearly dependent of each other, since only lies in , a proper subspace of . Consequently, and . Simple calculation from (2.19) and (2.20) gives

| (7.9) | |||

| (7.12) |

where .

Lemma 9.

If the columns of are in general position and is i.i.d. with mean zero and variance , then for any and ,

| (7.13) |

where is defined by (2.23).

Proof.

Consequently, to establish sign consistency, we only need a set of sufficient conditions for : (C1) . (C2) for some . (C3) Let and be the components of and , respectively. As ,

| (7.14) |

where for and for .

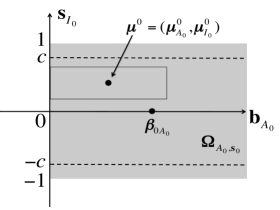

The first two conditions ensure that lies in the interior of . The third condition guarantees that always stays in a box centered at , and the box is contained in if (C1) and (C2) hold. These conditions have a simple and intuitive geometric interpretation illustrated in Figure 4.

Lemma 10.

Assume the columns of are in general position and is i.i.d. with mean zero and variance . If conditions (C1), (C2), and (C3) hold as , then is sign consistent for , regardless of the relative size between and .

Now we may recover some of the conditions for establishing consistency of the Lasso in the literature. In what follows, let in (7.9) and (7.12). Condition (C2) is the strong irrepresentable condition (Zhao and Yu 2006; Meinshausen and Bühlmann 2006; Zou 2006):

Assume that the minimum eigenvalue of is bounded from below by , which is equivalent to condition (6) in Zhao and Yu (2006). Condition (C1) holds if

| (7.15) |

This shows that some version of a beta-min condition is necessary to enforce a lower bound for . For example, we may assume that

| (7.16) |

for some positive constants and , which is the same as (8) in Zhao and Yu (2006). Then one needs to choose for (C1) to hold.

Let such that and . To establish condition (C3), assume that and is bounded from above. Then all are bounded and let be an upper bound of . Furthermore, follows a univariate normal distribution: For , and for , according to (7.12) with . By (7.15) and (7.16), for as , and

| (7.17) |

as long as and . Since for all ,

| (7.18) |

if and . Clearly, the above two inequalities imply (7.14). Therefore, must satisfy , which implies that . This is consistent with the beta-min condition in Meinshausen and Bühlmann (2006): . In summary, choosing such that , the Lasso can be consistent for model selection with and , both diverging with . For more general scaling of , see the work by Wainwright (2009).

7.3 Bayesian interpretation

It is well-known that the Lasso can be interpreted as the mode of the posterior distribution of under a Laplace prior. However, the posterior distribution itself is continuous on . If we draw from this posterior distribution, every component of will be nonzero with probability one. In this sense, sampling from this posterior distribution does not provide a direct solution to model selection, which seems unsatisfactory from a Bayesian perspective. Here, we discuss a different Bayesian interpretation of the Lasso-type estimator from a sampling distribution point of view.

Assume that and thus is invertible. Under the noninformative prior and the assumption that , the conditional and marginal posterior distributions of are

| (7.19) | |||||

| (7.20) |

where is given by (2.28) with and is the multivariate distribution with degrees of freedom, location , and scale matrix .

Following the decision theory framework, let be a decision regarding that incurs the loss

| (7.21) |

Since the covariance of is proportional to with respect to the posterior distribution (7.19) or (7.20), is essentially the squared Mahalanobis distance between and , plus a weighted norm of to encourage sparsity. Denote by the optimal decision that minimizes the loss for a given , i.e., . Let be the subgradient of at . The KKT condition for is

| (7.22) |

Since is a random vector in Bayesian inference, the distribution of determines the joint distribution of and via the above KKT condition. Represent by its equivalent form in the same way as for in Section 2.

The conditional posterior distribution (7.19) implies that . Thus, conditional on and , Equation (7.22) implies that

| (7.23) |

where . One sees that (7.23) is identical to the KKT condition (2.3) with in place of . Therefore, the conditional distribution , determined by (7.23), is identical to the estimated sampling distribution (2.27) under a normal error distribution with estimated by , i.e., . Furthermore, due to (7.20). By a similar reasoning, the conditional distribution is the same as if and if is estimated by the density of . This motivates our proposal to use as a parametric model for and estimate from data to construct . The above discussion also provides a Bayesian justification for sampling from .

Under this framework, we may define a point estimator by the decision that minimizes the posterior expectation of the loss ,

| (7.24) |

provided that the expectation exists. Although minimizes the posterior expected loss, its Bayes risk is not well-defined due to our use of an improper prior. To avoid any potential confusion, we call a posterior point estimator instead of a Bayes estimator. Taking subderivative of with respect to leads to the following equation to solve for the minimizer :

| (7.25) |

where is the subgradient of at . Under the noninformative prior, the posterior mean . In this case, and Equation (7.25) is identical to the KKT condition (2.1) for the Lasso-type estimator . Therefore, can be interpreted as the estimator (7.24) that minimizes the posterior expected loss.

Remark 13.

These results provide a Bayesian interpretation of the Lasso-type estimator and its sampling distribution. Assume a normal error distribution with a given and the noninformative prior. The posterior distribution of the optimal decision, , is identical to the sampling distribution of assuming is the true coefficient vector. Therefore, a posterior probability interval for , the optimal decision, constructed according to is the same as the confidence interval constructed according to with . Point estimation about also coincides between the Bayesian and the penalized least-squares methods (). Lastly, if we set in the loss (7.21), then the optimal decision is simply . In this special case, the aforementioned coincidences become the familiar correspondence between the posterior distribution (7.19) and the sampling distribution of and that between the posterior mean and .

It is worth mentioning that, in a loose sense, this Bayesian interpretation also applies when . In this case, the posterior distribution (7.19) does not exist, but is a well-defined normal distribution in . From KKT conditions (7.22) and (7.25), we see that the posterior point estimator and the posterior distribution only depend on . Therefore, they are well-defined and have the same coincidence with the Lasso-type estimator and its sampling distribution.

7.4 Bootstrap versus Monte Carlo

We have demonstrated that Monte Carlo sampling via estimator augmentation has substantial advantages in approximating tail probabilities and conditional distributions, say , over direct sampling (or bootstrap). The MH Lasso sampler also showed some improvement in efficiency when compared against direct sampling in the low-dimensional setting. Now we discuss some limitations of estimator augmentation relative to bootstrap.

The joint density of the augmented estimator is derived for a given , and thus does not take into account the randomness in when it is chosen via a data-dependent way, say via cross-validation. Denote by the Lasso-type estimator when , where is estimated from the data . We stress that the density in Theorem 1 or Theorem 2 does not apply to the sampling distribution of and it is only valid for with being fixed during the repeated sampling of . However, the direct sampler (or bootstrap in a similar way) can handle data-dependent by adding one additional step to determine after each draw of in Routine 1.

Bootstrap and the direct sampler can be parallelized. The importance sampling algorithm (Routine 5) can easily be parallelized as well, since it uses the direct sampler to generate proposals and calculates importance weights independently for each sample. An MCMC algorithm needs a certain number of burn-in iterations before the Markov chain reaches its stationary distribution. It seems that naively running multiple short chains in parallel may impair the overall efficiency due to the computational waist of multiple burn-in iterations. Initialized with one draw from the direct sampler, a Markov chain simulated by Routine 4, however, reaches its equilibrium at the first iteration and thus is suitable for parallel computing. Its efficiency relative to direct sampling when both are parallelized can be calculated as follows.

Suppose our goal is to estimate and assume that without loss of generality. Assume that the time to run one iteration of the direct sampler allows for running iterations of an MCMC algorithm. Suppose that we have access to computing nodes and the available computing time from each node allows for the simulation of samples from the direct sampler, where may be small. Thus, on a single node we can run MCMC iterations plus an initial draw from the direct sampler in the same amount of time. In other words, we can run Routine 4 for iterations to draw for . Note that this Markov chain reaches equilibrium from . Let and

for an integer . Then we have

Denote by the variance in estimating by the mean of an i.i.d. sample of size , and let

The efficiency of Routine 4 relative to direct sampling is

where we have assumed that for the last inequality. This assumption holds if is nondecreasing in . This derivation shows that Routine 4 will be more efficient than the direct sampler on each computing node if , which can be as small as 1 when . We have observed two decay patterns of the autocorrelation of the MLS in the simulation study in Section 3.6. For some components of , is always positive before it decays to zero, in which case is obviously nondecreasing. For other components, first decreases monotonely to zero and then shows small fluctuations around zero. In the second case, we empirically observed that is nondecreasing as well. The efficiency comparison in Table 2, with and both large, suggests that for most functions estimated there, for datasets A and B and for the other two datasets. Therefore, as long as we need to run a few iterations of the direct sampler on each node, parallelizing Routine 4 can bring computational gain. Of course, if the number of computing nodes is so large that only one draw is needed from each node, direct sampling or bootstrap will be a better choice.

7.5 Concluding remarks

Utilizing the density of an augmented estimator, this article develops MCMC and IS methods to approximate sampling distributions in -penalized linear regression. This approach is clearly different from existing methods based on resampling or asymptotic approximation. The numerical results have already demonstrated the substantial gain in efficiency and the great flexibility offered by this approach. These results are mostly for a proof of principle, and there is room for further development of more efficient Monte Carlo algorithms based on the densities derived in this article.

In principle, the idea of estimator augmentation can be applied to the use of concave penalties in linear regression (Frank and Friedman 1993; Fan and Li 2001; Friedman et al. 2008; Zhang 2010) for studying the sampling distribution. However, there are at least two additional technical difficulties for the high-dimensional setting. First, we need to find conditions for the uniqueness of a concave-penalized estimator in order to construct a bijection between and the augmented estimator. Second, the constraint in (4.4) will become nonlinear in general, even for a fixed , when a concave penalty is used, which means that the sample space is composed of a finite number of manifolds. Another future direction is to investigate theoretically and empirically the finite-sample performance in variable selection by the Lasso sampler which may take into account the uncertainty in parameter estimation in a coherent way.

8 Proofs

Let and throughout this section.

8.1 Proof of Theorem 3

Lemma 11.

Let be a random vector, , and be the truncation of to such that for . If , then

Proof.

For any , and thus

On the other hand,

Therefore, for any and the conclusion follows. ∎

Lemma 12.

Proof.

The assumptions on imply that and for all . By the definition of (6.1) it then suffices to show that

| (8.1) |

for all . By the definition of in (6.8), for

and therefore

where we have used (6.9) and that . Consequently, for we have

On the other hand, by (6.9) and , for and thus

Now (8.1) follows since for all . ∎

Proof of Lemma 7.

Define , which follows the same distribution as (6.2). This is because by fixing and has a unique minimizer for any if the columns of are in general position (Lemma 1). Consequently,

Let . According to Lemma 12, for all . As the unique minimizer of (6.3), implies that is also a local minimizer of . Since is convex in and has only a unique minimizer , we must have and . Furthermore, using the same argument in the other direction, one can show that implies , and thus is equivalent to . This completes the proof. ∎

Proof of Theorem 3.

Let be the event that satisfies conditions (i) and (ii) in Lemma 7 and . We first show that (6.12) holds on . Obviously, (6.9) holds because of (6.11). The argument in the proof of Lemma 7 implies that, on event ,

| (8.2) |

where the second equality is due to . Let and be the respective truncations of and to . Lemma 7 implies on event . A direct consequence is that on , for any and therefore,

8.2 Proof of Theorem 4

Lemma 13.

Let be any minimizer of for and . For any , we have

| (8.4) |