Event conditional correlation

Abstract

Entries of datasets are often collected only if an event occurred: taking a survey, enrolling in an experiment and so forth. However, such partial samples bias classical correlation estimators. Here we show how to correct for such sampling effects through two complementary estimators of event conditional correlation: the correlation of two random variables conditional on a given event. First, we provide under minimal assumptions proof of consistency and asymptotic normality for the proposed estimators. Then, through synthetic examples, we show that these estimators behave well in small-sample and yield powerful methodologies for non-linear regression as well as dependence testing. Finally, by using the two estimators in tandem, we explore counterfactual dependence regimes in a financial dataset. By so doing we show that the contagion which took place during the 2007–2011 financial crisis cannot be explained solely by increased financial risk.

keywords:

[class=MSC]keywords:

1 Introduction

We provide methods to estimate and compare correlation estimates based on partial samples. We do so by deriving under minimal assumptions the properties of a new dependence parameter we introduce: event conditional correlation.

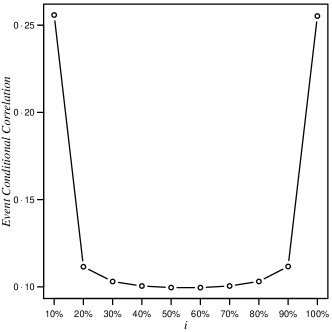

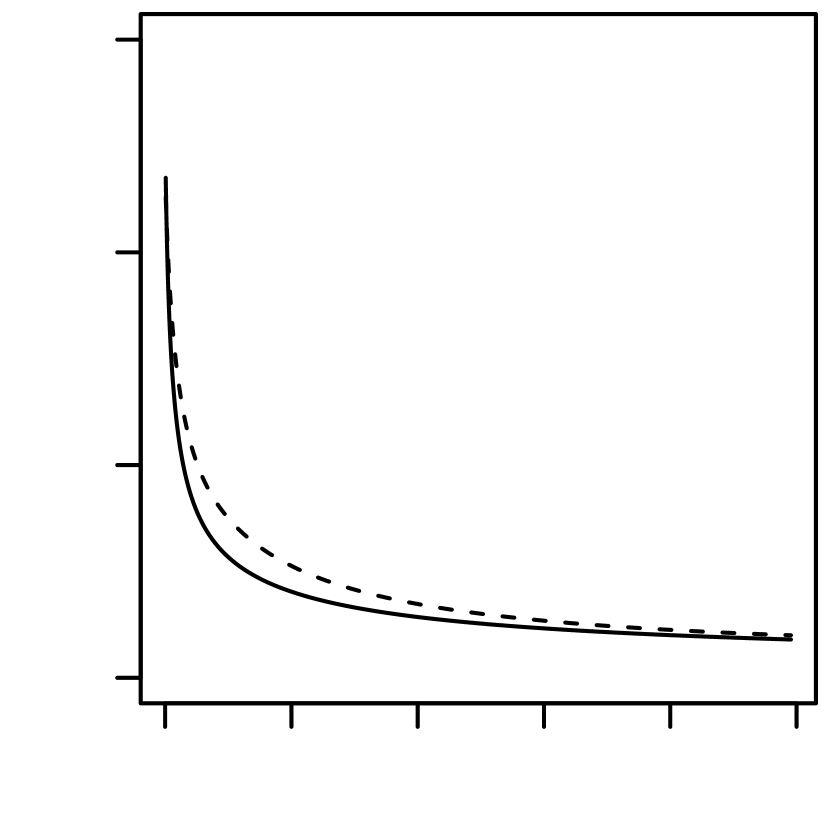

We define event conditional correlation as the correlation of two variables and conditionally to an event and denote it . Event conditional correlation is the natural correlation parameter when working with partial samples. Consider the case where one is able to measure only if a third random variable is large enough, say larger than a threshold . One classical example Akemann et al. (1983) is knowing the grades of students (the variables and ), only if these students had high enough scores in high school (the variable ) to enter university. In this setting, naively using the ordinary least squares estimator of correlation on the available sample produces an estimate of . Such an estimate can be sensibly different from , the classical or unconditional correlation parameter. We provide a quantified example in Fig 1a where is a trivariate Gaussian vector.

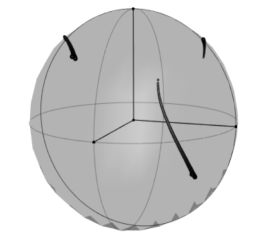

A more complex version of this problem has become central in finance since the 2007–2011 crisis. Let and be two assets returns, and be the overall volatility of the market. So as to quantify the risk a financial institution would face during a crisis, one must estimate , for a crisis volatility threshold potentially larger than all observed Campbell et al. (2008); Forbes and Rigobon (2002); Preis et al. (2012). As Fig 1a shows, can be markedly larger than even when is a Gaussian vector. Furthermore, Fig 1b, shows that in higher dimensions, conditioning by non-trivially affects the eigenvectors of the covariance matrix. It follows that efficient estimators of are needed by banks: to properly determine how much fund to set aside in provision of a crisis Kalkbrener and Packham (2015), and to efficiently allocate assets during a crisis Kenett et al. (2015).

We present two estimators that address under minimal assumptions these problems. First, in Theorem 1, we propose an admissible estimator of for any such that . Second, in Theorem 2, we present an estimator of relying on a sample where for all realizations an event is verified (henceforth referred to as an -sample). Using both estimators allows to estimate given a -sample, this for any two events and with non zero probabilities of occurring.

These results describe a highly counter-intuitive and non-trivial phenomena. As shown in Figs 1a and 1b, event conditional correlation has a strikingly far from linear behavior even in the Gaussian case. This underlines how non-linear linear dependence can be. As the analysis will show, it is the homogeneous nature of correlation that allows to transport estimates under one condition to another. However, the scale at which it is observed under a given condition is driven by the conditional variances of the variables under .

The proposed estimators can directly be used to complement many statistical approaches, either to address sampling problems or to extend them to non-linear cases. We present three examples: the first focuses on a non-linear regression method that uses event conditional correlation (Section 5.1); the second considers the power of event conditional correlation to test for independence while relying on a partial sample (Section 5.2); the third contrasts the realized and counterfactual topologies of a financial market across risk regimes (Section 5.3.) We conclude on the implications of Theorems 1 and 2 on the robustness to sampling of the leading eigenvectors of covariance matrices.

2 Relations with other dependence parameters

Here we discuss how event conditional correlation generalizes many partial dependence parameters. We derive the properties of event conditional correlation starting from Section 3.

We begin by formally defining . For two real valued random variables and defined on the probability space and assuming to be in and such that , event conditional correlation verifies:

Practically, as in the examples above, we will access though a third random variable defined on the same probability space as and . Then, will take the form , for a subset of the support of .

Event conditional correlation belongs to the class of conditional dependence parameters. All such parameters are built by considering the dependence between two variables and while controlling for the behavior of a third variable . We will see that using events allows us to replicate most such controls.

The simplest way of controlling is to fix it at some value . This is how conditional correlation, which we will write , is built. The relationship between and can be formalized by considering a sequence of events tending to and such that for all . If such a sequence exists, then . Fixing at a given value is also how conditional copulas are built Acar, Craiu and Yao (2013); Ghahramani, Póczos and Schneider (2012); Gijbels, Omelka and Veraverbeke (2012). However, the drawback of fixing , is that unless both conditional correlation and conditional copulas are only identifiable under parametric assumptions. On the other hand, we can always estimate event conditional correlation non-parametrically. Many other dependence parameters are built as the expectation over of a conditional dependence parameter defined for a fixed ; e.g., liquid association Li (2002), incomplete Lancaster interaction Sejdinovic, Gretton and Bergsma (2013), partial martingale difference correlation Park, Shao and Yao (2015) and conditional information Póczos and Schneider (2012). While taking the expectation makes it possible to use non-parametric methods in these cases, the obtained parameters lose their informational content regarding the local variations of the dependence.

An other way of controlling is to push it into one of its tails. Such conditional dependence parameter take the form of limit event conditional correlation: . This type of dependence parameter is explored further in Akemann et al. (1984). Importantly, the case leads to the tail dependence parameter.

The influence of over can also be controlled by removing its linear effects on and . This leads to partial correlation—that we denote . There also exists a direct relation between and . We formalize it below in (2).

Thus, is a bridge between partial, conditional and tail correlations. Furthermore, it can be used to describe when all or some of these parameters match in the neighborhood of a given . This part of our work completes the discussion started in Lawrance (1976) and continued more recently in Baba, Shibata and Sibuya (2004); Baba and Sibuya (2005). However, there are no direct connections between event conditional correlation and correlation distance as introduced in Székely, Rizzo and Bakirov (2007). Correlation distance and related dependence parameters aim to generalize correlation to test for dependence between random vectors. On the other hand, event conditional correlation aims to describe in more details the dependence between two scalar variables. Nonetheless, we show in Section 5.2 that event conditional correlation can detect dependence when more complex measures do not, while in Section 6 we discuss the consequences of Theorem 1 and 2 on the structure of conditional covariance matrices.

3 New event conditional correlation estimator

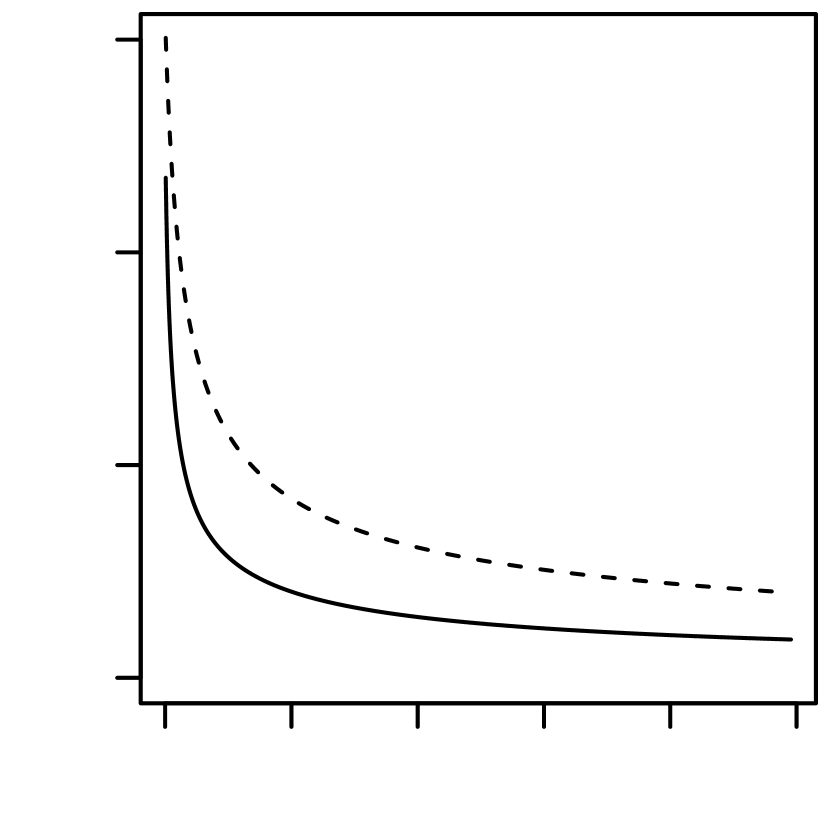

In this section we present an admissible estimator of event conditional correlation that uses all the available sample rather than the subsample where the condition is verified, as is common practice. We will proceed in two steps, first introducing the hypotheses and notation, before presenting the general result along with a small-sample study (see Fig 2).

Definition 1.

Let and be two centered real valued univariate random variables with finite second moments. Let and be two real valued random vectors of the same dimension, possibly containing (or equal) to or , both having second moments. Finally assume to be and -measurable and of non-zero probability of occurring; i.e., there exists and such that and .

We use classical notation: -s are the correlations and -s are the covariance matrices of the variables in index (we use -s for the standard deviation in the univariate case), finally -s are regression parameters and -s are the regression residuals. For instance for a centered scalar random variable we have:

with the classical ordinary least squares regression parameter, equal to .

Assumption 1.

We define here the two assumptions and :

These assumptions should be seen as minimal since is necessary according to Baba, Shibata and Sibuya (2004), and if , is automatically verified. Meeting can be attained by adding the sufficient number of covariates in and , something that was not possible before our contribution. Finally, if remains falsified, the bias induced in the following estimators can be controlled by , making them still of interest in cases where this value is small.

Theorem 1.

Under and , we have that:

| (1) |

with for all

Proof.

To be found in Appendix Appendix. ∎

To obtain a better intuition of the result, we simplify the problem and assume that the variables are scaled and such that , with univariate. Then (1) becomes

| (2) |

with . This form shows that is driven by the conditional variance, and more precisely by , the normalized shift in conditional variance between inside and outside of . In the limit case where , we recover the recursive equation to compute partial correlation , allowing us to relate the two dependence parameters.

Normal(0,): (02,04,06,1)

Normal(0,): (06,07,08,1e3)

Student-: (04,05,06,5)

Student-: (02,03,04,30)

Normal(0,): (02,06,06,10)

Normal(0,): (02,03,04,1)

Finally, (2) recovers the results of Boyer, Gibson and Loretan (1997); Avouyi-Dovi, Guégan and Ladoucette (2002); Forbes and Rigobon (2002); Kalkbrener and Packham (2015), connecting our result with theirs. However, because all these works focus on risk measures in finance, they make field specific assumptions on the nature of the condition and on the distribution of , while we work under minimal assumptions.

We now draw from Theorem 1 a new estimator of . In the following we denote using hat estimators: for instance is an estimator of .

Corollary 1.

Under , and the assuming that , , , , , , and are -consistent, asymptotically normal estimators, we have that

| (3) |

is a -consistent, asymptotically normal, estimator of .

Proof.

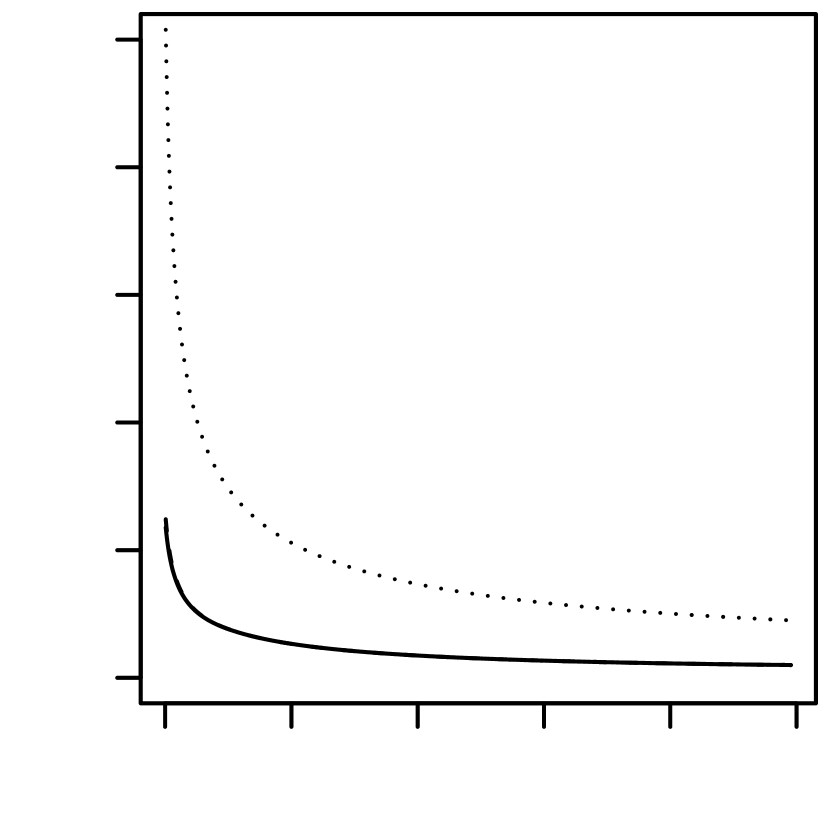

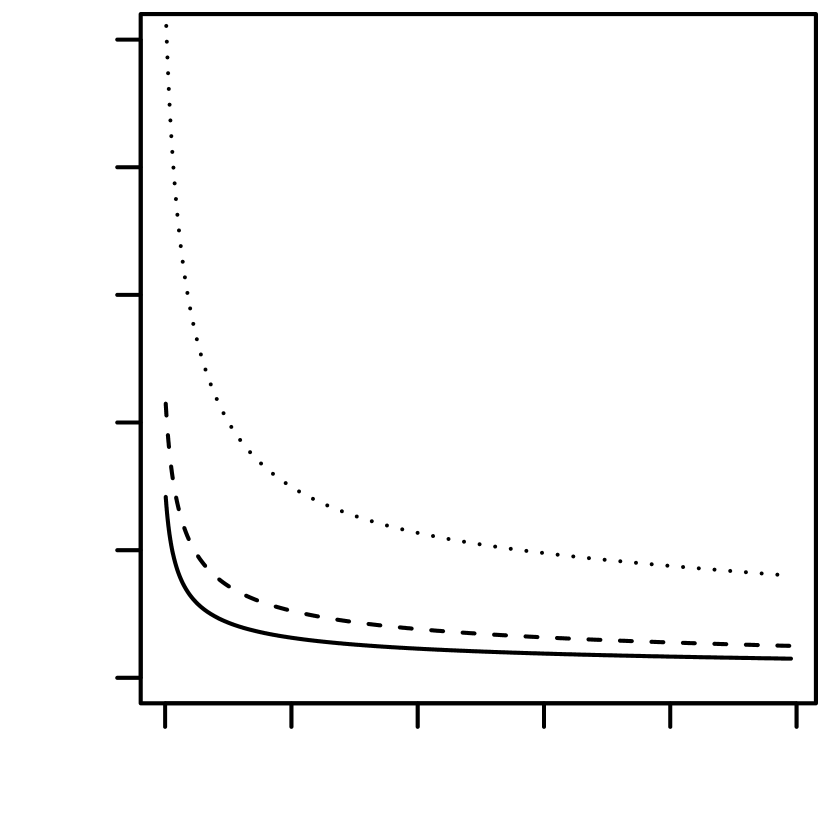

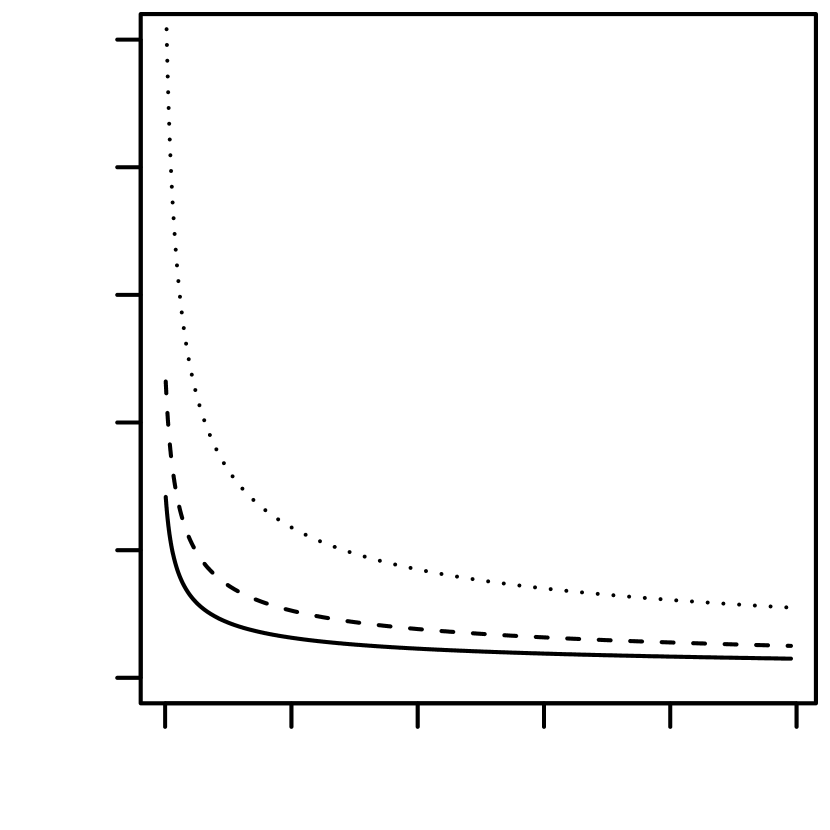

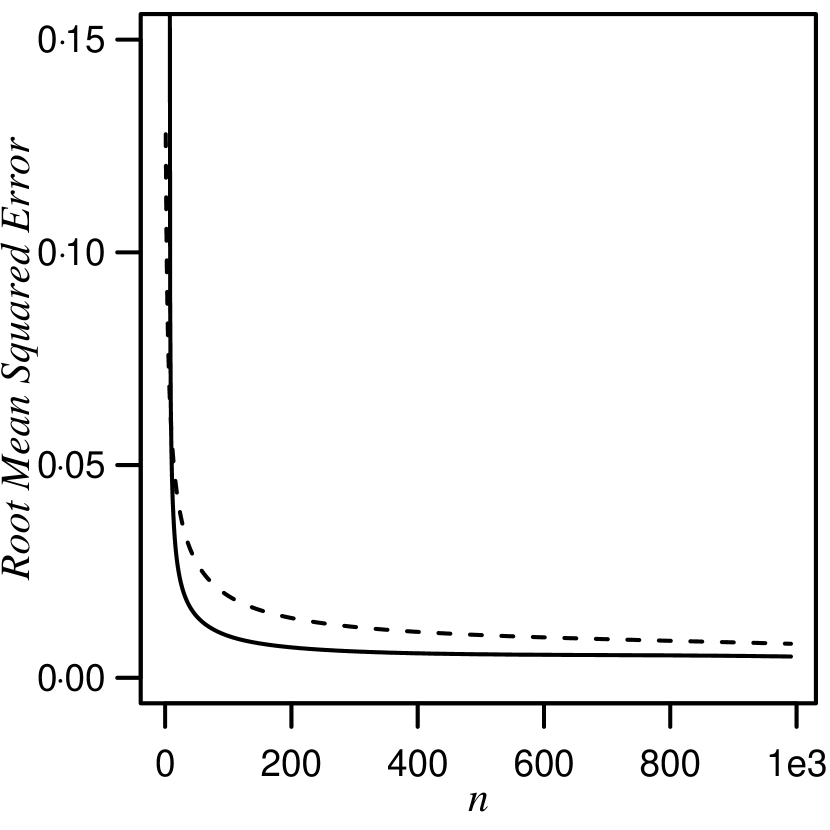

The result is a direct application of Theorem 1 and the delta method. We detail the proof in Appendix Variance. Figure 2 shows a small-sample study corroborating this result. To obtain an -consistent estimator of the variances—the -s—we estimate the joint distribution of using the whole sample and infer from that estimate the conditional covariance matrices. In all six cases our estimator almost realizes the Cramér-Rao bound: on average it only adds a 004 error in correlation estimates compared to the Cramér-Rao case. ∎

It is of interest to tell whether two event conditional correlation estimates are significantly different or not. To this end we must produce confidence intervals for our estimator. Since Corollary 1 is derived through the delta method, the variance stabilizing transformation, or inverse delta method, should be used Fisher (1915); Hotelling (1953). However, this method is not applicable here as it cannot be computed in closed form van der Vaart (1998). Nevertheless, resampling methods can be used, which we recommend.

4 Implied unconditional correlation estimator

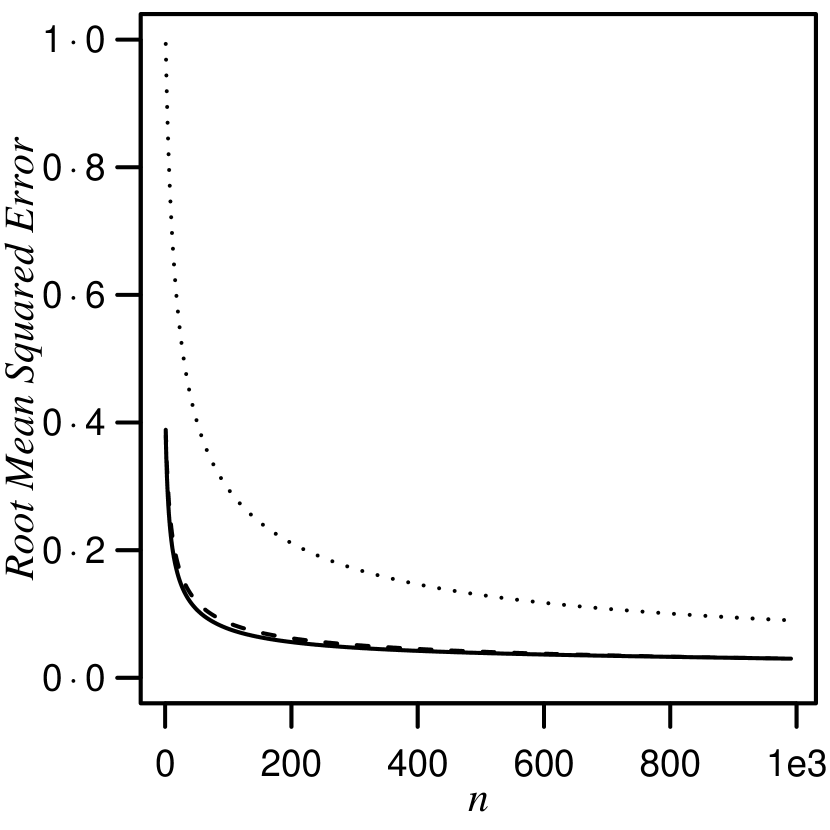

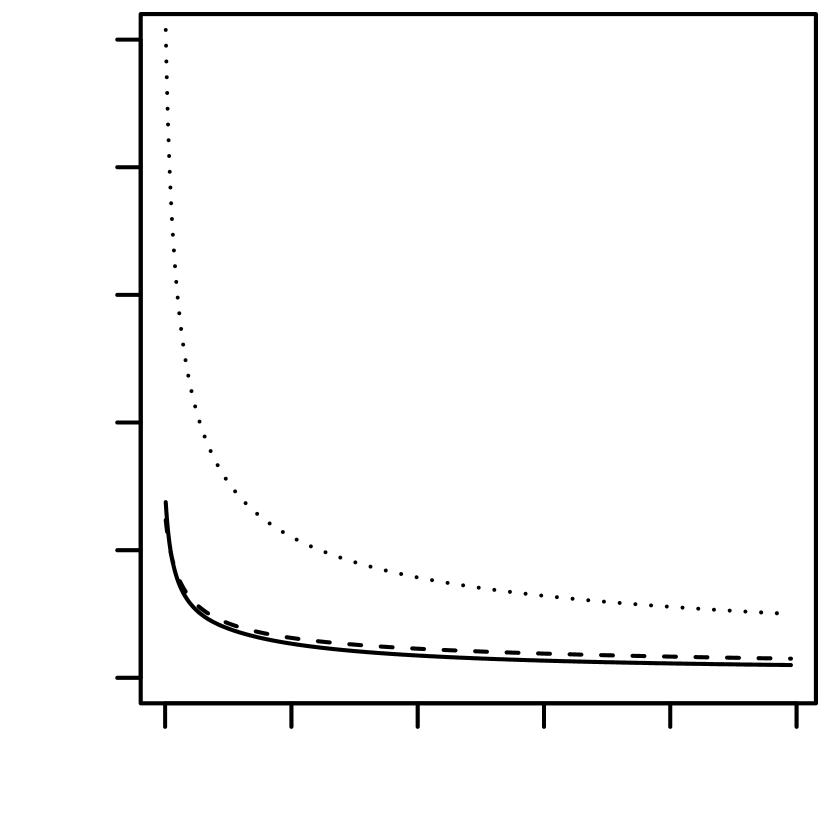

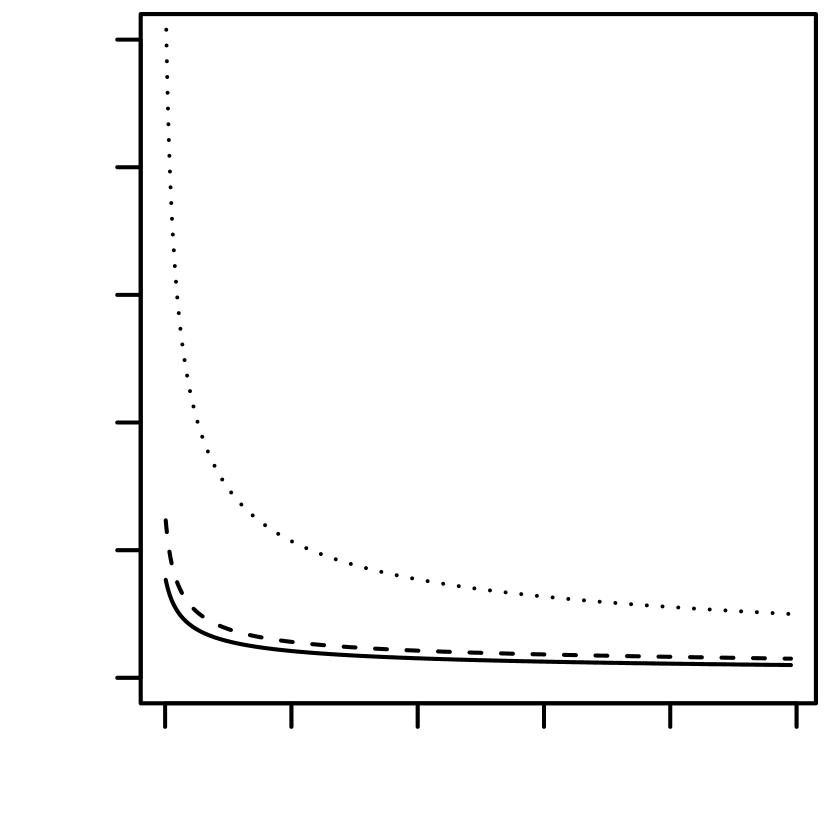

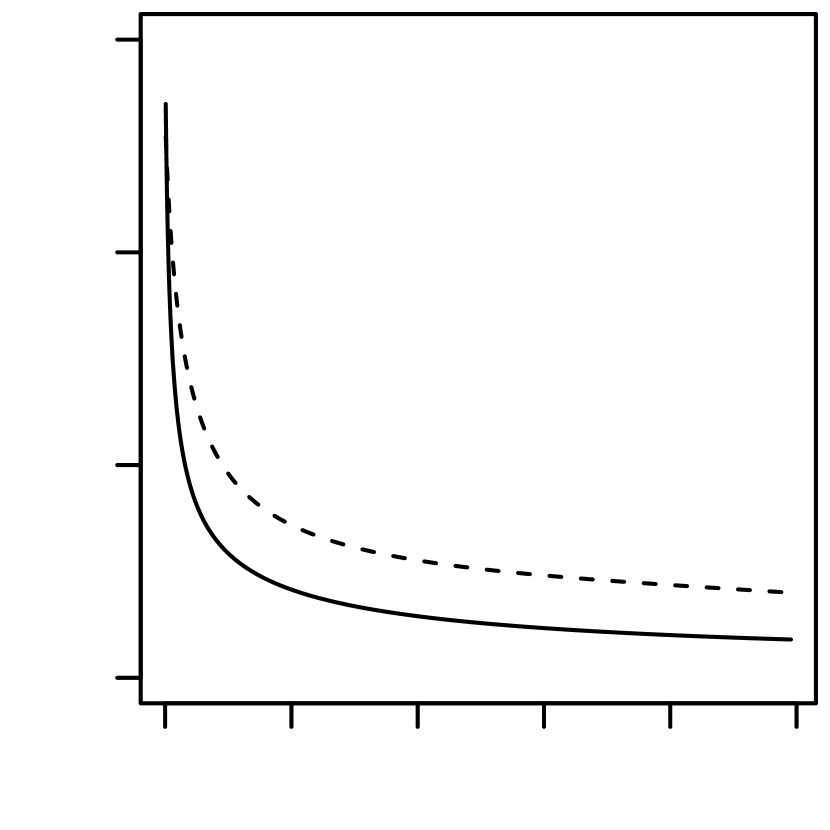

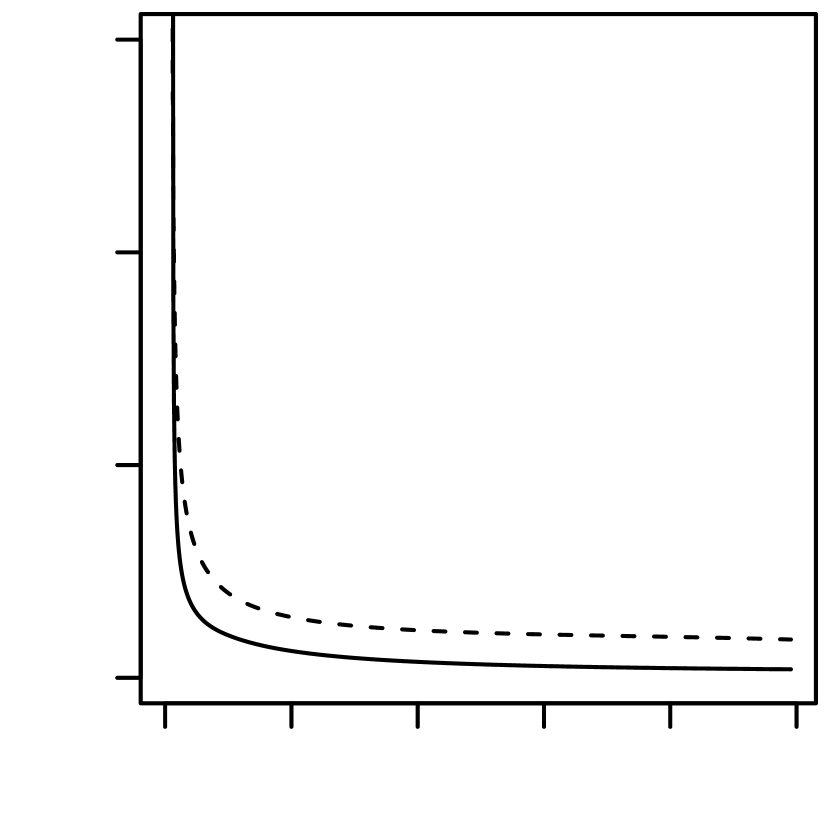

In this section we present an estimator of unconditional correlation based on an -sample (a sample where is verified for all observations.) The formulation of this estimator is not intuitive, but as detailed below it is in fact driven by the same adjustment for conditional variance shift as (1). We are not aware of any other estimator to compare our result with, but in Fig 3 we present a small-sample study where our estimator almost realizes the Cramér-Rao bound: On average it only adds a 002 relative error in correlation estimates compared to the Cramér-Rao case.

Theorem 2.

Assuming , we have that

| (4) |

with for all and

Proof.

Equation 4 does not make the link between conditional variance and event conditional correlation explicit. Rewriting it in the simplified case of (2), shows that it is in fact based on exactly the same transformation as that in (1): with , we have

In fact, in that specific setting, for any event and with , we have

Normal(0,): (02,04,06,1)

Normal(0,): (06,07,08,1e3)

Student-: (04,05,06,5)

Student-: (02,03,04,30)

Normal(0,): (02,06,06,10)

Normal(0,): (02,03,04,1)

From Theorem 2 we naturally obtain an estimator of the unconditional correlation:

Corollary 2.

With a -sample, under , and the additional assumption that , , , , and are -consistent, asymptotically normal estimators, using (4) yields a -consistent, asymptotically normal estimators of .

Proof.

The result is a direct consequence of Theorem 2 and the delta method. A proof is presented in Appendix Variance and small sample simulations are presented in Fig 3. To obtain -consistent estimators of the conditional covariances, the -s, we use maximum likelihood with a truncated distribution on and infer from the estimate the corresponding covariance. ∎

5 Examples

We now use the tools developed in Theorems 1 and 2 to address three problems: non-linear regression, dependence testing, and financial dependence structure. In the first two examples we use synthetic datasets, and in the last one we will consider the NASDAQ-100 index within and without the recent financial crisis.

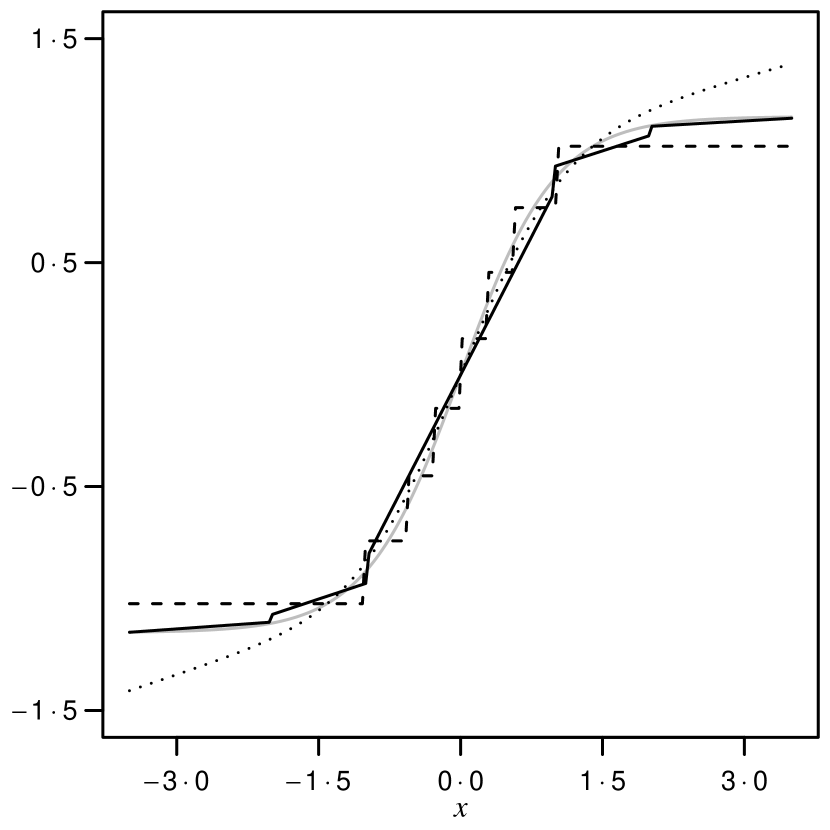

5.1 Piecewise affine functional regression

We compare three regression methodologies: generalized additive regression Hastie and Tibshirani (1986), tree regression Breiman (1984), and a new regression methodology we introduce that uses event conditional correlation. The synthetic dataset used consists in 1e4 realizations of two variables and such that is equal to , with a centered Gaussian noise.

The regression estimate that uses event conditional correlation is obtained in three steps and builds on the concept of segmented regression Liu, Wu and Zidek (1997). First, we break the support of into several disjoint intervals of the same size, say the . Then, using Corollary 1, for each we estimate the correlation between and conditionally on being in and obtain the corresponding regression slope . The final estimate is the piecewise affine function built using the regression slopes:

| (5) |

where is the empirical mean of conditionally on being in .

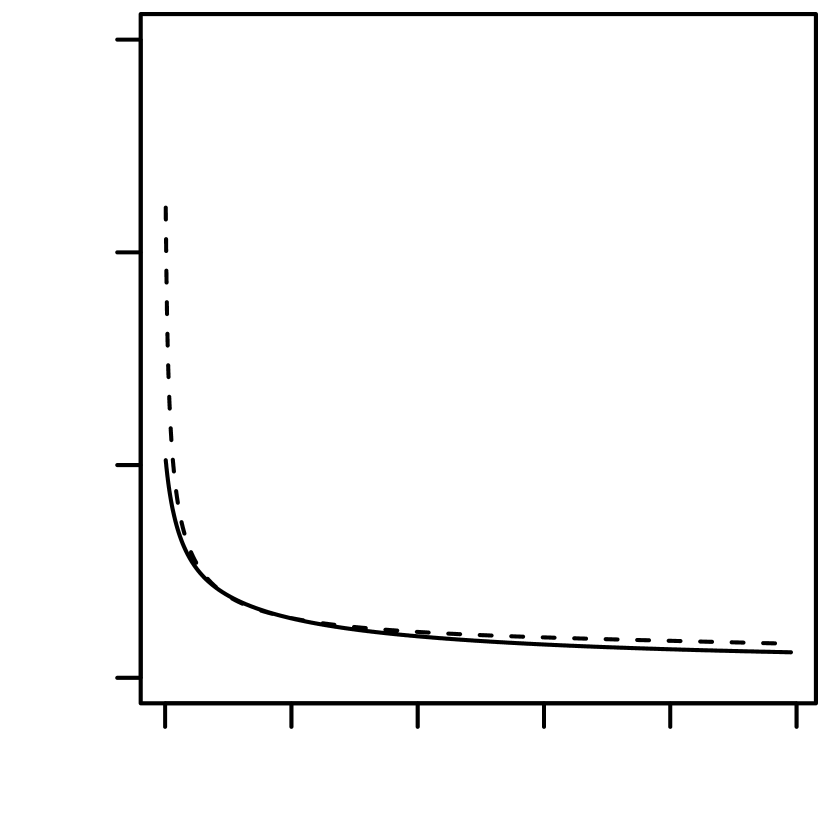

We present the obtained estimates in Fig 4 and observe that all three methods perform comparably well. However, we note that the estimate produced using conditional correlation is the only one to capture the tail of . This leads to a better root mean squared error (0051 compared to 012 and 0081 for generalized additive regression and tree regression respectively).

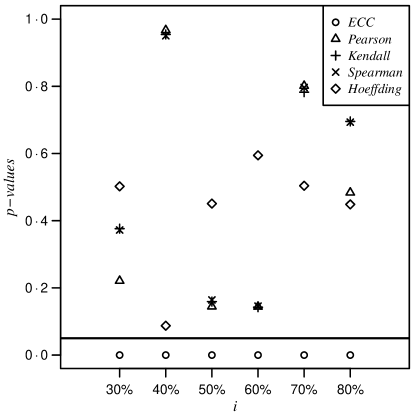

5.2 Test for bivariate dependence

We compare five bivariate tests for dependence between and given a -sample. We find that event conditional correlation outperforms all the other methods in the considered synthetic examples.

The tests considered are as follows. The first four test for a dependence parameter being equal to zero. The considered parameters are: i) the implied unconditional correlation estimated using Corollary 2 assuming that the unconditional variance of the covariate is 1, ii) the Pearson, iii) Spearman, and iv) Kendall dependence parameters. The last considered test is the Hoeffding test, which is the univariate case of correlation distance Székely, Rizzo and Bakirov (2007).

The total synthetic dataset consists of 5e3 realizations of , a trivariate Gaussian vector so that all entries have unit variance and that 025 and 050. We then apply the five considered tests to the -samples of where takes the same form as in Figure 1a:

for 01,02,,1. Then, each -sample consists of 5e2 realizations.

Only the test based on our results succeeds in detecting the dependence between and (see Fig 5). Because of the sampling constraint, the co-movement of and are limited, making classical tests unable to detect the dependence. The estimator of Corollary 2 allows to magnify this dependence, and hence detect it.

5.3 Financial dependence network

We now turn to one of the original objectives of our study of event conditional correlation: financial assets dependence. One prominent question since the contribution of Forbes and Rigobon (2002) is the following: Do crises alter the dependence structure of financial assets? By exhibiting a special case of Theorem 1, Forbes and Rigobon (2002) argued that it does not. This result raised a long and involved controversy that we do not review here.

Our new results allows us to consider the same problem in a more general setting: i) we can use varied covariates to describe the shift in dependence structure, whereas Forbes and Rigobon (2002) considered dependence at the bivariate level, of the form for some threshold ; ii) we can use the correlation structure as a whole, instead of considering each correlation parameters independently. We will do so for the NASDAQ-100, a widely traded financial index representing more than 15% of US equity market (nasdaqtrader.com, May 2015).

5.3.1 Dataset

We consider the daily closing quotes between 2007-07-23 and 2015-06-30 of all the NASDAQ-100 components at the last date, totaling 2e3 trading days. We only kept the components that were already listed on the first date of the dataset, keeping 94 out of 100111All quotes were obtained using the quantmod package Ryan (2015).. For each component, we extract the normalized residuals of the log-returns222We do so using a auto regressive model for the log returns (AR model), and model residuals with the generalized auto-regressive conditional heteroskedasticity model (GARCH model). We use the fGarch package Wuertz et al. (2013) to jointly estimate these models.. We call the matrix containing all the obtained normalized residuals.

The covariate we use is the CBOE-NASDAQ-100 volatility index over the same period; we call it . This index describes at each date the level of risk of the NASDAQ-100. To obtain a precise description of the dependence, we will use , , and the lag of these three quantities333We selected these lags and powers using classical analysis of variance methods.. We call the full matrix of regressors.

5.3.2 Correcting the correlations

We define two regimes: the crisis regime, where is in it’s higher quartile, and the complementary, the stable regime. Changing from the higher quartile to an other threshold does not substantially affect the results.

Using each subsample independently, we can estimate the correlation matrices of inside and outside of the crisis regime. If we do so, we find that more than 97% of correlation coefficients are significantly different across regimes444We use resampling methods and the -test. In this case, and throughout the remainder of this analysis, we use Bonferroni correction and 01% significance levels..

Using Theorem 2, we can correct for the bias induced by sampling: We use both sample independently to produce estimate of the unconditional correlations, the correction being made using as covariate. After correction, we find that less than 83% of the correlations are significantly different.

Thus, as in Forbes and Rigobon (2002), we observe that ignoring subsampling inflates the apparent shift in dependence structure across regimes. However, as opposed to Forbes and Rigobon (2002), there remains an important shift between regimes. Using Theorem 1 will allow us to describe this shift in dependence structure.

5.3.3 Describing the contagion

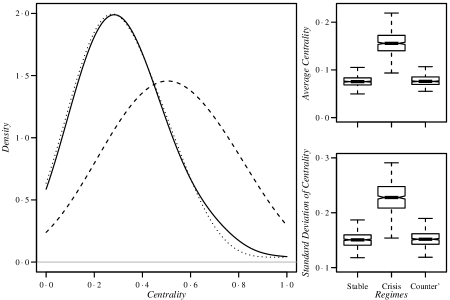

We now consider the network linking the components of the NASDAQ-100. Considering this network allows to describe dependence as a whole and does not require multiple testing. The nodes of the network are the components of the NASDAQ-100. The weight of the edge between two nodes is the partial correlation between the two components: the correlation after removing linear effects from all the other components.

We first compare the networks linking NASDAQ-100 components within and without the crisis regime, this is done while correcting for sampling using Theorem 2. To compare these networks we will use the nodes’ centrality scores. (These quantities describe the importance of each node in the network in terms of how likely a random walk over the network is to visit that node Newman (2010).) More precisely, we will compare the sample average and standard deviation of the centrality scores of all nodes in the network555These moments are tied to the first eigenvector of the covariance matrix of Newman (2010). Thus, by continuity arguments and using the Delta method, these moment estimates are expected to be asymptotically normal. We used the Shapiro-Normality-Test and failed to reject that the bootstrap distribution is normal in all cases..

We find that both the sample averages and standard deviations of centrality show marked upward shifts between the stable and crisis regimes (see Fig 6.) Further, since the network estimates are already corrected for sampling and the level of risk, the observed shifts must be caused by some other phenomena.

We explore this idea by evaluating the average and standard deviation of centrality in a counterfactual network. To build the counterfactual network, we use the realization from the stable regime along with Theorems 1 and 2 to produce an estimate of the network we would observe if the variance of was increased by . In Fig 6 we set and observe that the counterfactual network does not replicate the centrality distribution observed during the crisis regime. Other values of do not affect this observation.

To conclude, we showed that: i) the observed change in dependence structure between the stable and crisis regimes must be caused by contagion and that ii) the structure observed during the crisis regime cannot be replicated by stressing the dependence structure of the stable regime. Interestingly, between the stable and crisis regimes, the network is moving from a state where most nodes have small centrality (except a select few), to a state where centrality is on average higher, but otherwise much more spread out. Then, although a few leading components may drive the behavior of the NASDAQ during the stable regime, this does not appear to be the case during the crisis regime. We expect that this effect, beyond the increase in variance, makes the market much harder to predict as it presents no clear leading variable.

6 Discussion

Our results show that what drives correlation variations across events is the shift in conditional variances across events. It follows that by estimating the conditional variance shift, or by assuming a given value for it, we can estimate and compare correlation conditionally to any events using any partial sample. This is done while making no assumption on the dependence occurring between and . The only requirement of the method is to possess covariates able to describe the said dependence across conditions (the .) Furthermore, the proposed estimators are consistent, asymptotically normal and display good small sample properties (see Figs 2 and 3.)

These results have direct methodological applications. We provide three examples: one for non-linear regression, one for dependence testing, and one for financial networks. Event conditional correlation based approaches prove more powerful than comparable methods in the first two examples. In the last example, we characterized the occurrence of contagion (structural shift in the dependence structure) during the 2007–2011 financial crisis. Furthermore, we qualitatively described the uncovered crisis regime using counterfactuals.

Importantly, our last example exhibits a hidden consequence of Theorems 1 and 2: that the leading eigenvalues and eigenvectors of covariance matrices are robust to partial samples. To see this, consider a random vectors and a covariate . A direct consequence of Theorem 1 is that is of rank at most . Then, for small , the effect of conditioning by is very limited on the eigenvalues and eigenvectors of the sample covariance matrix. However, if the dimensions of and are comparable, the effects cannot be neglected. We provide an example of this later point in dimension 3 in Fig 1b.

An interesting final case to consider is when the dimension of goes to infinity Gao et al. (2015). Because of its lower dimensionality, will be much less affected than by this high dimensional setting. We conjecture that in this setting spectral methods become asymptotically frail to conditioning, even when the dimension of remains fixed.

Appendix

Proof of Theorem 1.

We will proceed in two steps: first we will compute the covariance of and knowing and then proceed to compute the variance of and knowing . In the following we will put as index to operators used conditionally to : for instance .

Covariance

Variance

| (9) | |||||

We make the simplification using . Let us now compute the variance of . To do so we use the fact that (9) is verified for any event such that and are verified. This is the case if , then the above equation writes:

so that:

| (10) |

| (11) |

The result for is obtained similarly.

Proof of Corollary 1.

For simplicity we will work here in the simplified case presented after Theorem 1, where the variables are normed, and is univariate. The result and the proof extends directly to the general setting of Corollary 1.

We call the vector composed of the parameters required to compute the : . We denote an estimator of that converges at rate as in the statement of Corollary 1 and the asymptotic covariance matrix of .

Let be the map defined by:

The map is such that . We denote the gradient of :

Then under our assumptions we have that is an asymptotically normal estimator of converging at the same rate , and of asymptotic variance as a direct application of the Delta Method, see (van der Vaart, 1998, p. 30) (with the same notation). ∎

Proof of Theorem 2.

We start from 1:

| (12) |

We then replace and by their value. To this en we introduce and , the vectors of correlation between and against and respectively, so that

From (12) we now recover

| (13) |

It follows that it is sufficient to obtain the result to show that and are equal to and respectively. To do so we use Theorem 1 to evaluate and obtain (as in the simplified case presented after the said theorem):

which concludes the proof. ∎

Proof of Corollary 2.

In the same fashion as for Corollary 2 we will consider here only the simplified framework where and with univariate. The result and the proof extends to the multivariate setting. Then the proof is the same as that of Corollary 2 using with the exact same function . ∎

References

- Acar, Craiu and Yao (2013) {barticle}[author] \bauthor\bsnmAcar, \bfnmE. F.\binitsE. F., \bauthor\bsnmCraiu, \bfnmR. V.\binitsR. V. and \bauthor\bsnmYao, \bfnmF.\binitsF. (\byear2013). \btitleStatistical testing of covariate effects in conditional copula models. \bjournalElectron. J. Statist. \bvolume7 \bpages2822–2850. \bdoi10.1214/13-EJS866 \endbibitem

- Adler et al. (2014) {bmanual}[author] \bauthor\bsnmAdler, \bfnmD.\binitsD., \bauthor\bsnmMurdoch, \bfnmD.\binitsD., \bauthor\bsnmNenadic, \bfnmO.\binitsO., \bauthor\bsnmUrbanek, \bfnmS.\binitsS., \bauthor\bsnmChen, \bfnmM.\binitsM., \bauthor\bsnmGebhardt, \bfnmA.\binitsA., \bauthor\bsnmBolker, \bfnmB.\binitsB., \bauthor\bsnmCsardi, \bfnmG.\binitsG., \bauthor\bsnmStrzelecki, \bfnmA.\binitsA. and \bauthor\bsnmSenger, \bfnmA.\binitsA. (\byear2014). \btitlergl: 3D visualization device system (OpenGL) \bnoteR package version 0.93.996. \endbibitem

- Akemann et al. (1983) {barticle}[author] \bauthor\bsnmAkemann, \bfnmC. A.\binitsC. A., \bauthor\bsnmBruckner, \bfnmA. M.\binitsA. M., \bauthor\bsnmRobertson, \bfnmJ. B.\binitsJ. B., \bauthor\bsnmSimons, \bfnmS.\binitsS. and \bauthor\bsnmWeiss, \bfnmM. L.\binitsM. L. (\byear1983). \btitleConditional correlation phenomena with applications to university admission strategies. \bjournalJournal of Educational and Behavioral Statistics \bvolume8 \bpages5–44. \endbibitem

- Akemann et al. (1984) {barticle}[author] \bauthor\bsnmAkemann, \bfnmC. A.\binitsC. A., \bauthor\bsnmBruckner, \bfnmA. M.\binitsA. M., \bauthor\bsnmRobertson, \bfnmJ. B.\binitsJ. B., \bauthor\bsnmSimons, \bfnmS.\binitsS. and \bauthor\bsnmWeiss, \bfnmM. L.\binitsM. L. (\byear1984). \btitleAsymptotic conditional correlation coefficients for truncated data. \bjournalJ. Math. Anal. Appl. \bvolume99 \bpages350–434. \endbibitem

- Avouyi-Dovi, Guégan and Ladoucette (2002) {barticle}[author] \bauthor\bsnmAvouyi-Dovi, \bfnmS\binitsS., \bauthor\bsnmGuégan, \bfnmD\binitsD. and \bauthor\bsnmLadoucette, \bfnmS\binitsS. (\byear2002). \btitleWhat is the best approach to measure the interdependence between different markets ? \bjournalBanque de France Notes d’études et de Recherche \bvolume95. \endbibitem

- Baba, Shibata and Sibuya (2004) {barticle}[author] \bauthor\bsnmBaba, \bfnmKunihiro\binitsK., \bauthor\bsnmShibata, \bfnmRitei\binitsR. and \bauthor\bsnmSibuya, \bfnmMasaaki\binitsM. (\byear2004). \btitlePartial correlation and conditional correlation as measures of conditional independence. \bjournalAust. N. Z. J. Stat. \bvolume46 \bpages657–664. \bdoi10.1111/j.1467-842X.2004.00360.x. \bmrnumber2115961 (2005k:62153) \endbibitem

- Baba and Sibuya (2005) {barticle}[author] \bauthor\bsnmBaba, \bfnmK.\binitsK. and \bauthor\bsnmSibuya, \bfnmM.\binitsM. (\byear2005). \btitleEquivalence of partial and conditional correlation coefficients. \bjournalJ. Japan Statist. Soc. \bvolume35 \bpages1–19. \endbibitem

- Boyer, Gibson and Loretan (1997) {btechreport}[author] \bauthor\bsnmBoyer, \bfnmB. H.\binitsB. H., \bauthor\bsnmGibson, \bfnmM. S.\binitsM. S. and \bauthor\bsnmLoretan, \bfnmM.\binitsM. (\byear1997). \btitlePitfalls in tests for changes in correlations \btypeTechnical Report No. \bnumber597, \binstitutionBoard of Governors of the Federal Reserve System (U.S.). \endbibitem

- Breiman (1984) {bbook}[author] \bauthor\bsnmBreiman, \bfnmLeo\binitsL. (\byear1984). \btitleClassification and Regression Trees. \bpublisherChapman & Hall, \baddressNew York. \endbibitem

- Campbell et al. (2008) {barticle}[author] \bauthor\bsnmCampbell, \bfnmR. A. J.\binitsR. A. J., \bauthor\bsnmForbes, \bfnmC. S.\binitsC. S., \bauthor\bsnmKoedijk, \bfnmK. G.\binitsK. G. and \bauthor\bsnmKofman, \bfnmP.\binitsP. (\byear2008). \btitleIncreasing correlations or just fat tails? \bjournalJ. Empirical Finance \bvolume15 \bpages287–309. \endbibitem

- Fisher (1915) {barticle}[author] \bauthor\bsnmFisher, \bfnmR. A.\binitsR. A. (\byear1915). \btitleFrequency distribution of the values of the correlation coefficient in samples from an indefinitely large population. \bjournalBiometrika \bvolume10 \bpages507–521. \endbibitem

- Forbes and Rigobon (2002) {barticle}[author] \bauthor\bsnmForbes, \bfnmK. J.\binitsK. J. and \bauthor\bsnmRigobon, \bfnmR.\binitsR. (\byear2002). \btitleNo contagion, only interdependence: measuring stock market comovements. \bjournalJ. Finance \bvolume57 \bpages2223–2261. \endbibitem

- Gao et al. (2015) {barticle}[author] \bauthor\bsnmGao, \bfnmC.\binitsC., \bauthor\bsnmMa, \bfnmZ.\binitsZ., \bauthor\bsnmRen, \bfnmZ.\binitsZ. and \bauthor\bsnmZhou, \bfnmH. H.\binitsH. H. (\byear2015). \btitleMinimax estimation in sparse canonical correlation analysis. \bjournalAnn. Statist. \bvolume43 \bpages2168–2197. \endbibitem

- Ghahramani, Póczos and Schneider (2012) {binproceedings}[author] \bauthor\bsnmGhahramani, \bfnmZ.\binitsZ., \bauthor\bsnmPóczos, \bfnmB.\binitsB. and \bauthor\bsnmSchneider, \bfnmJ. G.\binitsJ. G. (\byear2012). \btitleCopula-based kernel dependency measures. In \bbooktitleProceedings of the 29th International Conference on Machine Learning (ICML-12) (\beditor\bfnmJ.\binitsJ. \bsnmLangford and \beditor\bfnmJ.\binitsJ. \bsnmPineau, eds.) \bpages775–782. \bpublisherACM, \baddressNew York, NY, USA. \endbibitem

- Gijbels, Omelka and Veraverbeke (2012) {barticle}[author] \bauthor\bsnmGijbels, \bfnmI.\binitsI., \bauthor\bsnmOmelka, \bfnmM.\binitsM. and \bauthor\bsnmVeraverbeke, \bfnmN.\binitsN. (\byear2012). \btitleMultivariate and functional covariates and conditional copulas. \bjournalElectron. J. Statist. \bvolume6 \bpages1273–1306. \bdoi10.1214/12-EJS712. \bmrnumber2988448 \endbibitem

- Hastie (2013) {bmanual}[author] \bauthor\bsnmHastie, \bfnmT.\binitsT. (\byear2013). \btitlegam: Generalized Additive Models \bnoteR package version 1.09. \endbibitem

- Hastie and Tibshirani (1986) {barticle}[author] \bauthor\bsnmHastie, \bfnmTrevor\binitsT. and \bauthor\bsnmTibshirani, \bfnmRobert\binitsR. (\byear1986). \btitleGeneralized additive models. \bjournalStatist. Sci. \bvolume1 \bpages297–318. \bnoteWith discussion. \bmrnumber858512 \endbibitem

- Hotelling (1953) {barticle}[author] \bauthor\bsnmHotelling, \bfnmHarold\binitsH. (\byear1953). \btitleNew light on the correlation coefficient and its transforms. \bjournalJ. Roy. Statist. Soc. Ser. B. \bvolume15 \bpages193–225; discussion, 225–232. \bmrnumber0060794 (15,728d) \endbibitem

- Kalkbrener and Packham (2015) {barticle}[author] \bauthor\bsnmKalkbrener, \bfnmM.\binitsM. and \bauthor\bsnmPackham, \bfnmN.\binitsN. (\byear2015). \btitleCorrelation under stress in normal variance mixture models. \bjournalMath. Finance \bvolume25. \endbibitem

- Kenett et al. (2015) {barticle}[author] \bauthor\bsnmKenett, \bfnmD. Y.\binitsD. Y., \bauthor\bsnmHuang, \bfnmX.\binitsX., \bauthor\bsnmVodenska, \bfnmI.\binitsI., \bauthor\bsnmHavlin, \bfnmS.\binitsS. and \bauthor\bsnmEugene Stanley, \bfnmH.\binitsH. (\byear2015). \btitlePartial correlation analysis: Applications for financial markets. \bjournalQuant. Finance \bvolume14 \bpages569–578. \endbibitem

- Lawrance (1976) {barticle}[author] \bauthor\bsnmLawrance, \bfnmA. J.\binitsA. J. (\byear1976). \btitleOn conditional and partial correlation. \bjournalAmer. Statist. \bvolume30 \bpages146–149. \endbibitem

- Li (2002) {barticle}[author] \bauthor\bsnmLi, \bfnmK-C\binitsK.-C. (\byear2002). \btitleGenome-wide coexpression dynamics: Theory and application. \bjournalProc. Natl. Acad. Sci. USA \bvolume99 \bpages16875–16880. \endbibitem

- Liu, Wu and Zidek (1997) {barticle}[author] \bauthor\bsnmLiu, \bfnmJ.\binitsJ., \bauthor\bsnmWu, \bfnmS.\binitsS. and \bauthor\bsnmZidek, \bfnmJ. V\binitsJ. V. (\byear1997). \btitleOn segmented multivariate regression. \bjournalStat. Sinica \bvolume7 \bpages497–525. \bmrnumber1466692 (99b:62063) \endbibitem

- Newman (2010) {bbook}[author] \bauthor\bsnmNewman, \bfnmM. E. J.\binitsM. E. J. (\byear2010). \btitleNetworks: An Introduction. \bpublisherOxford University Press, \baddressOxford. \endbibitem

- Park, Shao and Yao (2015) {barticle}[author] \bauthor\bsnmPark, \bfnmT.\binitsT., \bauthor\bsnmShao, \bfnmX.\binitsX. and \bauthor\bsnmYao, \bfnmS.\binitsS. (\byear2015). \btitlePartial martingale difference correlation. \bjournalElectron. J. Statist. \bvolume9 \bpages1492–1517. \endbibitem

- Póczos and Schneider (2012) {binproceedings}[author] \bauthor\bsnmPóczos, \bfnmB.\binitsB. and \bauthor\bsnmSchneider, \bfnmJ. G.\binitsJ. G. (\byear2012). \btitleNonparametric estimation of conditional information and divergences. In \bbooktitleProceedings of the Fifteenth International Conference on Artificial Intelligence and Statistics (AISTATS-12) (\beditor\bfnmN. D.\binitsN. D. \bsnmLawrence and \beditor\bfnmM. A.\binitsM. A. \bsnmGirolami, eds.) \bvolume22 \bpages914–923. \endbibitem

- Preis et al. (2012) {barticle}[author] \bauthor\bsnmPreis, \bfnmT.\binitsT., \bauthor\bsnmKenett, \bfnmD. Y.\binitsD. Y., \bauthor\bsnmStanley, \bfnmH. E.\binitsH. E., \bauthor\bsnmHelbing, \bfnmD.\binitsD. and \bauthor\bsnmBen-Jacob, \bfnmE.\binitsE. (\byear2012). \btitleQuantifying the behavior of stock correlations under market stress. \bjournalSci. Rep. \bvolume2 \bpages752. \endbibitem

- R Core Team (2013) {bmanual}[author] \bauthor\bsnmR Core Team, (\byear2013). \btitleR: A Language and Environment for Statistical Computing, \baddressVienna, Austria. \endbibitem

- Ripley (2014) {bmanual}[author] \bauthor\bsnmRipley, \bfnmB.\binitsB. (\byear2014). \btitletree: Classification and regression trees \bnoteR package version 1.0-35. \endbibitem

- Ryan (2015) {bmanual}[author] \bauthor\bsnmRyan, \bfnmJ. A.\binitsJ. A. (\byear2015). \btitlequantmod: Quantitative Financial Modeling Framework \bnoteR package version 0.4-4. \endbibitem

- Sejdinovic, Gretton and Bergsma (2013) {bincollection}[author] \bauthor\bsnmSejdinovic, \bfnmD.\binitsD., \bauthor\bsnmGretton, \bfnmA.\binitsA. and \bauthor\bsnmBergsma, \bfnmW.\binitsW. (\byear2013). \btitleA kernel test for three-variable interactions. In \bbooktitleNIPS 26 (\beditor\bfnmC. J. C.\binitsC. J. C. \bsnmBurges, \beditor\bfnmL.\binitsL. \bsnmBottou, \beditor\bfnmM.\binitsM. \bsnmWelling, \beditor\bfnmGhahramani\binitsG. \bsnmZ. and \beditor\bfnmK. Q.\binitsK. Q. \bsnmWeinberger, eds.) \bpages1124–1132. \bpublisherCurran Associates, Inc. \endbibitem

- Székely, Rizzo and Bakirov (2007) {barticle}[author] \bauthor\bsnmSzékely, \bfnmG. J.\binitsG. J., \bauthor\bsnmRizzo, \bfnmM. L.\binitsM. L. and \bauthor\bsnmBakirov, \bfnmN. K.\binitsN. K. (\byear2007). \btitleMeasuring and testing dependence by correlation of distances. \bjournalAnn. Statist. \bvolume35 \bpages2769–2794. \endbibitem

- van der Vaart (1998) {bbook}[author] \bauthor\bparticlevan der \bsnmVaart, \bfnmA. W.\binitsA. W. (\byear1998). \btitleAsymptotic statistics. \bseriesCambridge Series in Statistical and Probabilistic Mathematics \bvolume3. \bpublisherCambridge University Press, \baddressCambridge. \bmrnumber1652247 (2000c:62003) \endbibitem

- Wuertz et al. (2013) {bmanual}[author] \bauthor\bsnmWuertz, \bfnmD.\binitsD., \bauthor\bsnmChalabi, \bfnmY\binitsY., \bauthor\bsnmMiklovic, \bfnmM.\binitsM., \bauthor\bsnmBoudt, \bfnmC.\binitsC. and \bauthor\bsnmChausse, \bfnmP.\binitsP. (\byear2013). \btitlefGarch: Rmetrics - Autoregressive Conditional Heteroskedastic Modelling \bnoteR package version 3010.82. \endbibitem