Pointwise Convergence of the Lloyd algorithm in higher dimension

Abstract

We establish the pointwise convergence of the iterative Lloyd algorithm, also known as -means algorithm, when the quadratic quantization error of the starting grid (with size ) is lower than the minimal quantization error with respect to the input distribution is lower at level . Such a protocol is known as the splitting method and allows for convergence even when the input distribution has an unbounded support. We also show under very light assumption that the resulting limiting grid still has full size . These results are obtained without continuity assumption on the input distribution. A variant of the procedure taking advantage of the asymptotic of the optimal quantizer radius is proposed which always guarantees the boundedness of the iterated grids.

Keywords: Lloyd algorithm ; -means algorithm ; centroidal Voronoi Tessellation ; optimal vector quantization ; stationary quantizers ; splitting method ; radius of a quantizer.

1 Introduction

A Centroidal Voronoi Tessellation (CVT) with respect to a probability (or mass) distribution is a Voronoi tessellation of a set of (generating) points in (centers of mass) such that each generating point is the centroid of its corresponding Voronoi region with respect to this density function. This definition can be extended to more general probability measures, typically those assigning no mass to hyperplanes to avoid ambiguity on the boundaries of the Voronoi regions. CVTs enjoy very natural optimization properties, especially in connection with vector quantization (see further on) which makes them very popular in various scientific and engineering applications including art design, astronomy, clustering, geometric modeling, image and data analysis, resource optimization, quadrature design, sensor networks, and numerical solution of partial differential equations.

For modern applications of the CVT concept in large-scale scientific and engineering problems, it is important to develop robust and efficient algorithms for constructing CVTs in various settings. Historically, a number of algorithms have been studied and widely used. However, the pioneering contribution is undoubtedly the procedure first developed in the 1960s at Bell Laboratories by S. Lloyd. It remains so far, in its randomized form, one of the most popular methods due to its effectiveness and simplicity.

Let us begin with a more detailed description of the CVT. First assume that the probability distribution, say , on , has a support included in a closed convex set with non empty interior denoted of . Also, note that, up to a reduction of the dimension , one may always assume that has a nonempty interior.

A Voronoi diagram (or partition) of refers to a Borel partition of induced by a set of given generating points or Generators (the notation also refers to the application to numerics where the set of generators is also called a grid). For every , the Voronoi region (or cell) satisfies

where denotes the canonical Euclidean norm on . Then

so that the have convex interiors and closures. The family of closures is also known as Voronoi tessellation of induced by and the , are called tessels). Furthermore they have a polyhedral structure, in particular their boundaries are contained in where is the median hyperplane of and . Of course, a notion of Voronoi regions can be defined with respect to any norm on but the above (polyhedral) convexity properties fail (see [7], chapter 1) for non Euclidean norms.

We will often assume that is strongly continuous in the sense that it assigns no mass to hyperplanes (so is the case if is absolutely continuous where is a probability density function defined on whose support is contained in ). Then the boundaries of the Voronoi regions are -negligible so that we can define in a unique way the centroids , of the Voronoi regions by setting

| (1.1) |

Note that, owing to the convexity of the Voronoi cells and the finiteness of the measure , one has (closure in ) for every . From a more probabilistic point of view, if denotes an -valued random vector with distribution , then (with an obvious convention when )

This naturally leads to the definition of a CVT which is but a Voronoi tessellation whose generators are the centroids of their respective Voronoi regions. With the notation given above, the Lloyd algorithm for constructing CVTs can be described more precisely by the following procedure.

The paradigm of Lloyd’s algorithm is to consider the definition of CVT as a fixed point equality for the so-called Lloyd map defined on the set of -valued grids with at most values by (1.1),

As mentioned above, since the Voronoi tessels are convex and is probability distribution.

Note that, furthermore, if or if is contain,ious (assigns no mass to hyperplanes) then, a supporting hyperplane argument shows that (interior in ) for every (see further on Lemma 2.2, see also [7], p.22). In particular, and have the same size .

The Lloyd algorithm is simply the formal fixed point search procedure for the Lloyd map starting from a given grid of full size

Algorithm 1 (Lloyd’s algorithm for computing CVTs):

Inputs:

-

•

, the domain of interest;

-

•

a probability distribution supported by ;

-

•

, the initial set of generators.

Pseudo-script:

Formally, at the th iteration, one has to proceed as follows:

-

1.

Construct the Voronoi tessellation of with the grid of generators .

-

2.

Compute the -centroids of as the new grid of generators .

Repeat the iteration above until some stopping criterion is met to provide a grid of generators as close as possible of a -centroid.

end.

In -dimension, Kieffer has proved in [9] that is contracting if has a -concave density over a compact interval so that only one -centroid with points exists for such distribution and the above procedure converges exponentially fast toward it. See also, more recently a convergence result in [4].

In practice, these two steps become intractable in higher dimension by analytic or even deterministic approximation methods, say when or (see however the website QHull: www.qhull.org). So this theoretical procedure has to be replaced for numerical purpose by a randomized version in which:

– Step 1 is replaced by a systematic nearest neighbour search of simulated random -distributed vectors.

– Step 2 is replaced by a Monte Carlo estimation of both terms of the ratio which define the Lloyd map.

In the community of data analysis, note that when is the empirical measure of a -valued data set , it is still possible to define and compute the Lloyd map (using appropriate conventions like random allocation of points lying on the boundary of (closed) Voronoi tessels). In such a case the Lloyd procedure is known as the Forgy algorithm or the batch--means procedure. When the data set is so huge that a uniform sampling (of size ) of the dataset is necessary at each iteration, the procedure is known as the -means procedure.

In this paper we will focus on the converging properties of the theoretical (or batch in the data-mining community) Lloyd procedure, prior to any randomization or approximation, although we are aware that in higher dimension for continuous distributions , it is a pseudo-algorithm. So far we have presented the Lloyd procedure in an intrinsic manner. In fact Lloyd’s algorithm is deeply connected with the theory of Optimal Vector Quantization of probability distribution. This connection turns out to provide very powerful tools to investigate its convergence properties. It is also a major field of application when trying to compute with a sharp accuracy optimal quantizers of simulatable distribution arising in the design of numerical schemes for solving nonlinear problems (optimal stopping problems, (possibly Reflected) Backward Stochastic Differential Equations, Stochastic Control, etc, see [1, 16]).

Quantization is a way to discretize the path space of a random phenomenon: a random vector in finite dimension (but also stochastic process in infinite dimension viewed as a random variable taking values in its path space which we will not investigate in this paper). We consider here a random vector defined on a probability space taking its values in equipped with its Borel -field .

It is convenient for what follows to introduce a few notions and results about vector quantization and its (mean quadratic) optimization. It makes a connection between CVTs and stochastic optimization, gives a rigorous meaning to the notion of “goodness” of a CVT. Optimal vector quantization goes back to the early 1950’s in the Bell laboratories and have been developed for the optimization of signal transmission.

Let be a square integrable random vector ( ) or equivalently . Assume that its distribution is included in (defined as above). The terminology -quantizer (or a quantizer at level ) is assigned to any -valued subset with cardinality . When used in a numerical framework, it is also known as quantization grid.

The cardinality of is . In numerical applications, is also called a (quantization) grid. It is the set of genrators of its (borel) Voroni regions . Then can discretize in pointwise way by where : is a Borel function. Then we get

so that the best pointwise approximation of is provided by considering any (Borel) nearest neighbour projection associated with the Voronoi tessellation by setting

It is clear that such a projection is in one-to-one correspondence with the Voronoi partitions (or diagrams) of induced by . These projections only differ on the boundaries of the Voronoi cells so that, as soon as is strongly contoinuous, these neratest neighbour projections are all - equal. We define a Voronoi -quantization of (or at level ) by setting for every ,

Thus for all ,

| (1.2) |

We will call a Voronoi -quantization of or, in short, a quantization of .

The mean quadratic quantization error is then defined by

where is the norm in . The distribution of as a random vector is given by the -tuple . This distribution clearly depends on the choice of the Voronoi partition.

We naturally wonder whether it is possible to design some optimally fitted grids to a given distribution i.e. which induces the lowest possible mean quadratic quantization error among all grids of size at most . This optimization problem, known as the optimal quantization problem at level , reads as follows:

By introducing the energy function or distortion value function

the optimization problem also reads

since the value of at an -tuple only depends on its value grid of size at most of the -tuple (in particular is a symmetric function). We will make occasionally the abuse of notation consisting in denoting instead of .

One proves (see [2, 7, 12]) that there always exists at least one optimal -point grid with cardinal such that . If the support of has at least elements ( because it is infinite), then has full size . Furthermore, ; this last claim strongly relies on the Euclidean feature of the norm on : if , then the projection of the elements of on the closed (nonempty) convex strictly reduces the mean quadratic quantization error (see [12, 7, 10]). Note that this existence result does not require to be strongly continuous. In fact, even if has an atomic component, it is shown in [7] (see Theorem 4.2, p.38) that .

Furthermore, the function is differentiable on at every -tuple such that , and and its gradient is given by

| (1.3) |

where denotes any Voronoi diagram of (or with, once again, an obvious abuse of notation). In particular, if is an optimal quadratic quantizer, one shows (see [7], Theorem 4.2 p.38) that even if assigns mass to (at most countably many) hyperplanes. As a consequence,

where stands for the Lloyd map related to the distribution of the random vector . The equivalence is a straightforward consequence of (1.3)). Hence any optimal quantizer induces a CVT for the distribution of . In reference to the fact that such an -quantizer is a zero of a gradient, this property is also known as stationarity for the -tuple itself.

Unfortunately, the converse is not true since may have many local minima, various types of saddle points (and a “pin” behaviour on affine manifolds induced by clusters of stuck components). This phenomenon becomes more and more intense as grows. However, it makes a strong connection between search for optimal quantizers and Lloyd’s algorithm as described above. And there is no doubt that what practitioners are interested in are the optimal quantizers rather than any “saddle” stationary quantizers. One can also derive a stochastic gradient algorithm from the representation of as an expectation of a computable function of the quantizer and the random vector . This second approach leads to a stochastic optimization procedure, a stochastic gradient descent to be more precise, known as the Competitive learning vector Quantization algorithm () which has also been extensively investigated (see among others [12]).

The paper is organized as follows: in Section 2 we establish the convergence of the Lloyd procedure at level under some natural assumptions on the probability distribution (at least for numerical probability purpose) but assuming that the starting quantizer (or generators) induces a lower quantization error than the lowest quantization error at level . In Section 3, we propose a modified Lloyd’s procedure, inspired by recent results on the asymptotics of the “radius” of optimal quantizers at level as , to overcome partially this constraint on the starting grid.

Notations: denotes the support of the Borel probability measure on . denotes the Lebesgue measure on .

denotes the canonical inner product on . , , denotes the canonical Euclidean ball centered at with radius .

denotes the cardinality of set .

2 Convergence analysis of Lloyd’s algorithm with unbounded inputs

2.1 The main result

Owing to both simplicity and efficiency of of practical implementations of Lloyd’s algorithm in various fields of applications, it is important to study its convergence as it has been carried out, at least partially, in [12] for its “counterpart” in the world of Stochastic Approximation, the recursive stochastic gradient descent attached to the above gradient of the distortion function . This procedure is also known as (for Competitive Learning Vector Quantization algorithm). In fact, as concerns the convergence properties of Lloyd’s algorithm, many investigations have already been carried out . Thus, as mentioned in the introduction, true convergence for -concave densities has been established in [9] whereas global “weak” convergence has been proved in a one dimensional setting (see [4]). However, there are not many general mathematical results on the convergence analysis for distributions on multi-dimensional spaces, especially when the support of the distribution of interest is not bounded.

It is convenient to rewrite the iterations of the Lloyd algorithm in a more probabilistic form, using quantization formalism (with a generic notation for the grids: , ). Let . For every ,

with the following degeneracy convention:

if then .

We need now to formalize in a more precise way what can be a consistent connection between the sequence of iterated grids in the Lloyd procedure and the -tuples that can be associated to their values.

Definition 2.1.

Let be a sequence of iterates of the Lloyd procedure where . A sequence of -tuples is a consistent representation of the sequence if

-

(i)

,

-

(ii)

For every integer and every , is the centroid of the cell of

(still with the above degeneracy convention).

There are clearly consistent representations of a sequence of Lloyd iterates, corresponding to the possible numbering of . But then this numbering is frozen as increases. It is also clear that roundedness, convergence (in ) of such consistent representations does not depend on the selected representation. So is true for a possible limit of such sequences since will not depend on the selected representation. However on may have in case of an asymptotic merging of some of the components of the representation. One checks that under the assumptions we make ( continuous, or convex support or splitting assumption on ) no merging occurs at finite range.

Throughout the paper will always denote a consistent representation of the sequence of iterates . These remark lead naturally to the following definition

Definition 2.2 (Convergence of iterated grids).

We will say that (converges) as if there exists a constant representation converging in toward such that .

Several specific results established in what follows are known in the literature, but we chose to provide all proofs for self-completeness of the paper and reader’s convenience.

Let us first recall a basic fact which is at the origin of the efficiency of the Lloyd algorithm.

Lemma 2.1.

The iteration of Lloyd’s algorithm makes the quantization error decrease.

Furthermore, as long as with positive -probability. Conversely, if - for an integer , then - for every .

Proof: By its very definition, is the best approximation of among the -measurable functions, including itself. Thus

| (2.4) |

with equality if and only if . Note that, if so is the case, since . On the other hand, by (1.2), is the best approximation of among all -valued random vectors since

and if , this inequality holds as an equality.

This seminal property of Lloyd’s algorithm is striking not only by its simplicity. It is also at the origin of its success. Morally speaking, it suggests a convergence toward a stationary – and hopefully optimal or at least locally optimal – quantizer of the distribution of . In fact, things are less straightforward, at least from a theoretical point of view since this property provides absolutely no information on the boundedness of the sequence of grids generated by the procedure, although it is a crucial property the way toward convergence.

The main result of this paper is the following theorem.

Theorem 2.1.

Let be a square integrable random vector with a distribution having a convex support assigning no mass to hyperplanes. Let with size . Then, all the iterates have full size and are -valued.

If the sequence is bounded (or equivalently kits consistent representations ), then

and there exists and a connected component of such that

In particular, if is locally finite ( is reduced to finitely many points on each compact set), then .

Splitting method: If furthermore , then the sequence is always - bounded and .

Remarks. The result in claim does not depend on the original numbering of on the selected order (among ) selected to define and the then the sequence . In particular in case of true convergence of the sequence , all its permutations do converge as well toward the corresponding permutations of so that one can, by an abuse of notion write that . A direct approach based on a formal notion of set convergence is also possible but would be of no help in practice.

Nothing ensures that the limiting grid is optimal or even a local minimum. We refer to the Appendix for a brief discussion and an closed formula for the Hessian of .

The first claim of this theorem relies on a boundedness assumption for the sequence . This condition is of course satisfied if the support of the distribution of is compactly supported and (closed convex hull of the support of ) since we assume that : then, for every , so will be the case for as emphasized in the description of the procedure.

Claim emphasizes that, by an appropriate choice of (the quadratic quantization error) may imply the boundedness of the whole sequence of iterates . This approach known by practitioners as the splitting method is investigated in the next subsection.

We will prove this theorem step by step, establishing intermediary results, often under less stringent assumptions than the above theorem, which may have their own interest.

2.2 Possibly unbounded inputs: the splitting method

In practical computations, if one aims at computing (hopefully) optimal quantization grids (or ) of on a wide range of levels (see the website www.quantize.maths-fi.com), the so-called splitting method appears as an extremely efficient “level-by-level” procedure. The principle is to compute the grids in a telescopic manner based on their size : assume we have access to an optimal grid of size . Imagine we add to this grid an -valued component sampled randomly from the distribution of (or any -supported distribution). Doing so, we make up a grid which has for sure a lower quadratic mean quantization error than any grid with points. This grid of size is likely to lie in the attracting basin of the optimal quadratic quantizer (or ) at level . This is often observed in practice and, even if not optimal, it provides at least very good quantizers. Its main the trade-off is that it requires a systematic, hence heavily time consuming, simulation. Many variants or potential improvements can be implemented (like adding an optimal quantizer of size at each new initialization to directly obtain (hopefully) optimal quantizers of size (see [13]).

Splitting Assumption (on the starting grid): Let be such that card (where ). Let be an optimal grid of size for and let . The Lloyd algorithm is initialized as follows:

| (2.5) |

One natural way to generate the additional element is in practice to simulate randomly a copy of (in fact one can also simulate a copy of a random vector whose distribution is equivalent to that of , see the remark below).

Remark. If has a density , it is more efficient to simulate according to the distribution whose probability density is proportional to (one checks that this function is integrable if for an , see [7]). The reason is that the resulting distribution provides the best random -quantizers of for every in the following sense: the asymptotic minimization problem

has as a solution ( denotes here independence).

If the Splitting Assumption on the initialization of the procedure is satisfied, the grids of the iterations in the Lloyd algorithm share an interesting property (which implies their global boundedness). The arguments developed in the proof below are close to those used in the proof of the existence of an optimal quantizer at level (see [12, 7]).

Proposition 2.1.

Assume the Splitting Assumption (2.5).

The quantization error induced by the grid defined by (2.5) is strictly smaller than ( that of the optimal -quantizer ) so that and

The sequence of iterated grids is bounded in there exists a compact set such that

All the limiting values of the sequence of consistent representations have pairwise distinct components ( the the sequence of grids has asymptotically full size full size ).

Proof: The (squared) quadratic means quantization error (or “distortion value”) induced by satisfies:

where , . Let . For every ,

Consequently, on the event , we have

whereas we always have that . On the other hand we know that so that which implies in turn that

One concludes by noting that Lloyd’s algorithm makes the sequence of (squared) quadratic quantization error induced by the iterated grids non-increasing.

Suppose that there exists a subsequence and a component such that as . Then, by re-extracting finitely many subsequences, we can split the set into two disjoint non empty subsets and and find a subsequence (still denoted for convenience) such that

and

It is clear that

Therefore, it follows from Fatou’s Lemma that

Finally since contains at least . On the other hand, we know from that , so that we get the following contradictory inequality

Consequently is empty which completes the proof.

The proof is similar to that of the above item . Assume . If there exists two components and converging to . Then, owing to Fatou’s Lemma

which yields a contradiction.

2.3 Convergence of the Lloyd procedure under a boundedness assumption

From now on, our aim is to investigate the structure of the set of limiting grids of the sequence the set of grids such that there exists a subsequence for which .

The two lemmas and the proposition below establish several properties of the iterated grids which are the basic “bricks” of the proof of Claim of Theorem 2.1.

Lemma 2.2.

Let be a closed convex set of with non-empty interior and let be a Borel probability distribution such that and . Furthermore assume that, either satisfies , or assigns no mass to hyperplanes. Then the function defined on by

is continuous, strictly convex and atteins its unique minimum at .

Proof. Elementary computations show that

so that .

Now assume . There exists a supporting hyperplane to at defined by , . For every , so that

so that - -. This leads to a contradiction with the assumptions made on .

Lemma 2.3.

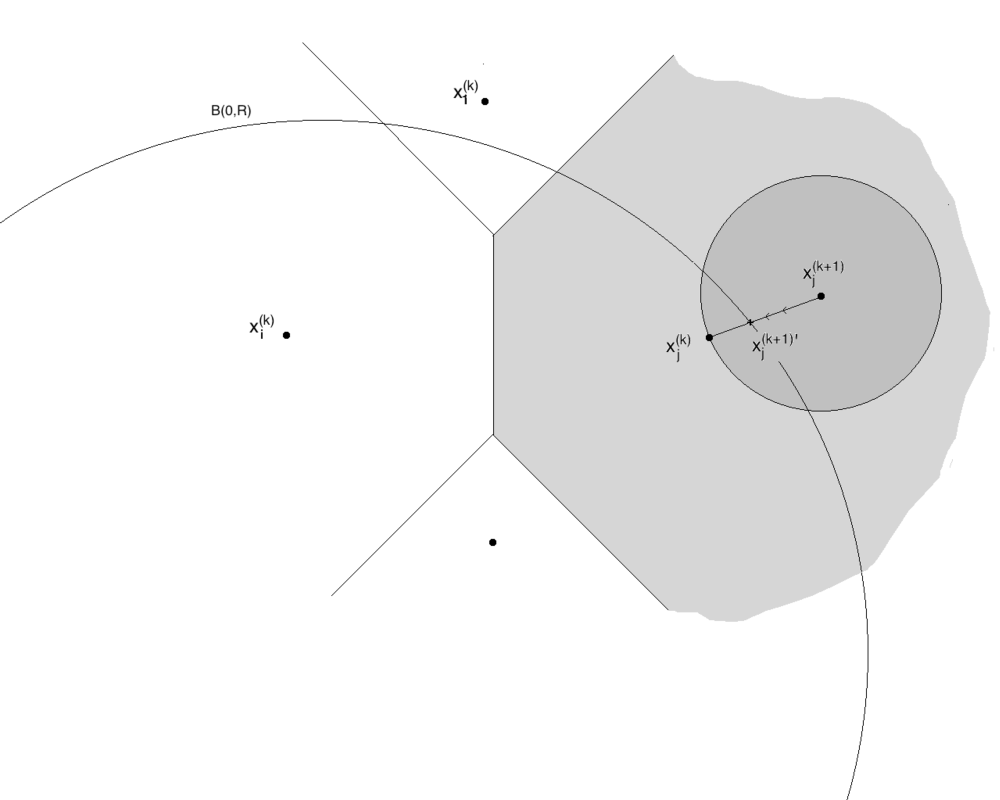

Assume that a subsequence as and that the boundary of the Voronoi tessellation of are -negligible. Let . Then

Proof of Lemma 2.3: By definition,

We know from what precedes that, since , if , the functions

Our assumption on implies that these convergences hold -. We conclude by Lebesgue’s dominated convergence theorem that for every

Therefore, with our convention for the index such that (if any), we get by applying the above convergence to and

Proposition 2.2 (Grid convergence I).

Assume that is a -valued grid and that the iterates of the Lloyd algorithm are bounded.

Assume that assigns no mass to hyperplanes and ( is convex). If the sequence of iterations of the Lloyd procedure is bounded ( because is itself bounded) then

no components of the grids get asymptotically stuck as goes to infinity.

Assume . Let be a limiting grid of . If the boundary of the Voronoi cells of are -negligible , then the grid is stationary it is a fixed point of the Lloyd map or equivalently that (any of) its induced Voronoi tessellation(s) is a CVT. Moreover if , then

If the distribution of assigns no mass to hyperplanes, then as .

If the distribution of has a convex support , then the consistent representations of satisfy

In particular, as . Hence, the set of (consistent representations of) limiting grids of is a (compact) connected subset of .

Remarks. In the literature the convergence of the gradient of the iterated grids as established in is sometimes known as “weak convergence” of the Lloyd procedure.

Lemma 2.2 improves a result obtained in [5] which show that component do not asymptotically merge in Lloyd’s procedure even when the Splitting Assumption is not satisfied. In [5], the distribution is supposed to be absolutely continuous with a density a continuous , everywhere strictly positive on its support. Our method of proof allows for relaxing this absolute continuity assumption.

Proof of Proposition 2.2: For every , , we define the median hyperplane of and by

We define together the affine form

which satisfies on and . Moreover, note that and that

The sequence of iterated grids being bounded by assumption, we may assume without loss of generality, up to an extraction ,

and

Set for every

Hence, for every , is a closed polyhedral convex set containing . It also contains since owing to the stationarity property. Then, for every ,

since uniformly on compact sets toward (simple convergence of affine forms in finite dimension implies locally uniform convergence).

Assume there exists such that is not reduces to contains at least two indices.

It is clear that

The above nonempty open set has non zero -mass since . Hence, there exists two indices such that and . First note that and but both quantities being opposite since they are equal to which means that

Since these sets are polyhedral and assigns no mass to hyperplanes, and . Then one checks that

so that, still using that assigns no mass to the boundaries of these polyhedral convex sets, we get

Set . It follows form (2.7) that

Letting go to infinity implies that

since is a converging sequence. Hence , , which in turn implies that .

One shows likewise, still taking advantage of the -negligibility of the boundaries of the polyhedral sets , that

Passing to the limit in the stationary equation satisfies by , , finally implies that

But, owing to Lemma 2.2 (see also [7], p.22), this implies that , . This yields a contradiction to the fact that both are equal .

Let . Then belong to the interior of one of the tessels , say . Hence, is strictly smaller than . Consequently, there exists an such that for all ,

or equivalently . Thus, for every ,

This clearly implies that -, as since . To carry on the proof, we need the following lemma.

If we set in Lemma 2.3, then

Moreover, the sequence being -uniformly integrable since , the above convergence also holds in .

Now, since and is -valued, we derive from Lemma 2.1 that

Since we know that -, it follows from from Fatou’s Lemma that

On the other hand, we derive from the convergence in that

so that

which in turn implies by the very definition of conditional expectation as an orthogonal projection on that

First we note that, for any grid , Schwarz’s Inequality implies

so that the sequence is bounded. Now, as assigns no mass to the boundary of any Voronoi tessellations, we derive from what precedes that any limiting grid of is stationary . It is clear by an extraction procedure that is the only limiting value for the bounded sequence which consequently converges toward .

The set of limiting grids of the sequence is compact by construction. Its connectedness will classically follow from

(see [15]).

It is clear from item that is a compact whose intersection with the closed set . Hence, stands at a positive distance of this set or, equivalently, there exists , such that

As a consequence, every Voronoi cell satisfies

where denotes the open ball with center and radius . Since is a (closed) convex set and , then for every . As a consequence, which in turn implies that the function is (strictly) positive on the compact set , so that we can define

| (2.6) |

which implies in particular that

On the other hand so that, finally,

Comments. The restrictions on the possible limiting grids in Theorem 2.1 do not imply uniqueness in general in higher dimensions: the symmetry properties shared by the distribution itself already induces multiple limiting grids as emphasized by the case of the multivariate normal distribution . In fact, for an orthogonal matrix that is ( stands for the transpose of ) and any optimal grid ,

For distribution with less symmetries like with , one can reasonably hope that at least local uniqueness of stationary grids (CVT) holds true. One way to check that is to establish that the Hessian is invertible at each stationary grid . A closed form is available for this Hessian (see [6]).

Proof of Theorem 2.1: The preliminary claim follows by induction from the structural stationary properties of the iterates and Lemma 2.2.

Combining the results obtained in the above proposition and the convergence toward a non-negative real number completes the proof.

3 A bounded variant of Lloyd’s procedure based on spatial estimation of the optimal quantizers

So far our results are based on the hypothesis that we initialize the Lloyd algorithm using a grid of size whose induced quadratic quantization error is lower than the minimal quantization error achievable with a grid of size at most . This is clearly the key point to ensure that the iterates of the procedure remain bounded. From a practical point of view, this choice for the initial grid is not very realistic, in particular if we are processing a “splitting method”: nothing ensures, even if the Lloyd procedure converges at a level , that the limiting grid will be optimal with the consequence that the initialization at level “below” becomes impossible.

However, we know from theoretical results on optimal vector quantization where the optimal quantizers are located a priori.

3.1 A priori bounds for optimal quantizers

The following proposition can be found in [7].

Proposition 3.1.

Let . Let . There exists such that

An upper bound satisfies the following conditions:

-

(i)

such that and ,

-

(ii)

.

If we specify , then the set will be the set of grids corresponding to optimal -quantizers, and will be an upper bound of the optimal -quantizers.

3.2 A variant of Lloyd’s algorithm

Since we know that all optimal -quantizers are constrained in a bounded domain (depending on in a more or less controlled way), a natural idea is to constrain the exploration of the Lloyd iterates inside it to take advantage of this information.

We can fix an area that we are sure that the optimal quantizer have its grids in it. Once an iteration of the algorithm includes some points that go beyond the area, we will be sure that it is not the optimal grid. So we can do something to pull the points back into the area while keeping the error non-increasing.

To this end, we now compute the difference made on the second phase of the Lloyd iteration in condition that we pick a point other than the mass center point. If we take instead of for a certain , the resulting difference in the th Voronoi region created by the second phase will be:

This shows that if we pick a point which lies at the same distance to as , then the above difference becomes zero. The idea is then to choose the point inside the prescribed domain if is outside. It is always possible, by keeping still (although this is probably not the optimal way to proceed).

With this idea we present a modified version of Lloyd’s algorithm, which does not need the Splitting Assumption, to be run successfully. We set a that all optimal quantizers are in the ball . The algorithm is as follows (assuming that is centered for convenience):

Algorithm 2 (Modified Lloyd’s algorithm):

Inputs:

-

•

, the domain of interest (with close to ) hopefully.

-

•

a simulatable probability distribution (with a convex support ) and assigning no mass to hyperplanes.

-

•

, the initial set of generators (starting grid).

Pseudo-script:

At the th iteration:

-

1.

Compute the position of , the mass centroid of . If there is an index such that lies outside (and for every such point), replace the current value by a point defined by (other choices are possible like choosing it randomly on .

-

2.

If every point lies in the ball , then take these mass centroids of as the new set of generators ,

-

3.

Construct the Voronoi tessellation of with the grid of generators .

Repeat the above iteration until a stopping criterion is met. And the output is the CVT with generators in .

end.

In this new version we modify Phase I (2.4) of the Lloyd procedure in such a way that the quadratic approximation error still decreases. The second phase being unchanged, so this modified Lloyd algorithm is still energy descending and furthermore it lives in the ball . The trade-off is that with the fixed at the beginning of the algorithm, we loose the (theoretical) possibility that the iterated sequence cruises very far during the iterations to finally come back with a lower energy. Therefore the energy level of the new limit points will be higher than setting . We also see that the larger the radius we take, the lower limit energy level we can get.

Another trade-off of the modified procedure is that it does not guarantee Lemma 3 because we do not use the Splitting Assumption. In this case we cannot prove the non-degeneracy of the limit grid by this global energy reasoning. However, we can now rely on Proposition 2.2 to ensure that no merging occurs.

Provisional remarks. One verifies on numerical implementation of Lloyd algorithm, that the main default that slows down the procedure is more the freezing of one component of the grid which is“ too far from the core” of the support of the distribution than the explosion of the grid with components going to infinity. but in some sense these seeming radically different behavior are the two sides of the same coin and the above procedure is an efficient way to prevent these parasitic effects. Though, in practice we proceed in a less formal way: using the theoretical estimates on the radius of the distribution allows for an adequate choice of the initial grid as confirmed by various numerical experiments carried in [18].

References

- [1] V. Bally and G. Pagès (2003): A quantization algorithm for solving multi-dimensional discrete-time optimal stopping problems. Bernoulli, 9(6):1003-1049.

- [2] J. A. Cuesta, C. Matrán (1988): The strong law of large numbers for k-means and best possible nets of Banach valued random variables. Probab. Theory Related Fields, 78(4):523-534.

- [3] Q. Du, V. Faber and M. Gunzburger (1999): Centroidal Voronoi tessellations: Applications and algorithms, SIAM Review, 41:637-676.

- [4] Q. Du, M. Emelianenko and L. Ju (2006): Convergence of the Lloyd algorithm for computing centroidal Voronoi tessellations, SIAM Journal on Numerical Analysis, 44:102-119.

- [5] M. Emelianenko, L. Ju and A. Rand (2008): Nondegeneracy and Weak Global Convergence of the Lloyd Algorithm in , SIAM Journal on Numerical Analysis, 46(3):1423 - 1441.

- [6] J.C. Fort and G. Pagès (1995): On the a.s. convergence of the Kohonen algorithm with a general neighborhood function. Ann. Appl. Probab. 5(4):1177-1216.

- [7] S. Graf and H. Luschgy (2000): Foundations of Quantization for Probability Distributions. Lecture Notes in Mathematics 1730, Berlin: Springer.

- [8] S. Junglen (2011): Quantization Balls and Asymptotics of Quantization Radii for Probability Distributions with Radial Exponential Tails, EJP, 16:283-295.

- [9] J.C. Kieffer (1982): Exponential rate of convergence for Lloyd’s method I, IEEE Trans. on Inform. Theory, Special issue on quantization, 28(2):205-210.

- [10] S. Graf, H. Luschgy and G. Pagès (2012): The local quantization behaviour of absolutely continuous probabilities. Annals of Probability, 40(4):1795-1828, 2012

- [11] D. G. Luenberger and Y. Ye (2008): Linear and Nonlinear Programming, 3rd ed. Springer.

- [12] G. Pagès (1998): A space vector quantization method for numerical integration, J. Computational and Applied Mathematics, 89, 1-38 (Extended version of “Voronoi Tessellation, space quantization algorithms and numerical integration” (1993), in: M. Verleysen (Ed.), Proceedings of the ESANN’ 93, Bruxelles, Quorum Editions, 221-228).

- [13] G. Pagès and J.. Printems (2003): Optimal quadratic quantization for numerics: the Gaussian case, Monte Carlo Methods & Applications Journal, 9(2):135-166.

- [14] G. Pagès and A. Sagna (2008): Asymptotics of the maximal radius of an -optimal sequence of quantizers, Bernoulli 18(1):360-389.

- [15] M.D. Ašić and D.D. Adamović (1970): Limit points of sequences in metric spaces, The American Mathematical Monthly, 77(6): 613-616.

- [16] G. Pagès, H. Pham and J. Printems (2004): Optimal quantization methods and applications to numerical problems in finance, in Handbook on Numerical Methods in Finance (S. Rachev, ed.), Birkhauser, Boston, 253-298.

- [17] D. Pollard (1982): A central limit theorem for -means clustering, Ann. Probab., 10, 919-926.

- [18] A. Sagna (2008): Méthodes de quantification optimale avec applications à la finance, PhD thesis, UPMC.

4 Appendix: Numerical detection of the nature of a limiting grid

We provide here a formula for the Hessian of the distortion value function when the distribution of is absolutely continuous with density function . From such a formula it is possible, at least numerically in low dimensions, to detect the status of a stationary grid/quantizer in terms of stability: local minimum, saddle point, etc.

As a first step we need a Lemma which provides a formula for the differentiation of integrals overs teasels of the Voronoi partition of an -tuple .

Lemma 4.1.

Let . Set for every with pairwise distinct components,

where denotes the Lebesque measure on . Then is continuously differentiable on the open set of -tuples with pairwise distinct components and

where denotes the Lebesque measure on the median hyperplane of and and . Furthermore,

We refer to [6] or [17] for a proof. This leads to the announced general result concerning the Hessian of the distortion function . We set for every , and ( denotes the Kronecker symbol).

Proposition 4.1.

Let with continuous. Then, for every , ,

and

This formula is used in [6] to show the instability of “square”, ”hyper”-rectangular stationary grids for the uniform distribution over the unit hypercube for Kohonen’s Self-Organizing Maps (). When the neighborhood function of the is degenerated (no true neighbor) the amounts to the and its equilibrium points are those of the Lloyd procedure, with the same (un-)stability properties. These quantities also appear in the asymptotic variance of the established in [17].