A Note on Sparse Least-squares Regression

Abstract

We compute a sparse solution to the classical least-squares problem where is an arbitrary matrix. We describe a novel algorithm for this sparse least-squares problem. The algorithm operates as follows: first, it selects columns from , and then solves a least-squares problem only with the selected columns. The column selection algorithm that we use is known to perform well for the well studied column subset selection problem. The contribution of this article is to show that it gives favorable results for sparse least-squares as well. Specifically, we prove that the solution vector obtained by our algorithm is close to the solution vector obtained via what is known as the “ SVD-truncated regularization approach”.

1 Introduction

Fix inputs and . We study least-squares regression: It is well known that the minimum norm solution vector can be found using the pseudo-inverse of : When is ill-conditioned, becomes unstable to perturbations and overfitting can become a serious problem. For example, when the smallest non-zero singular value of is close to zero, the largest singular value of can be extremely large and the solution vector obtained via a numerical algorithm is not the optimal, due to numerical instability issues. Practitioners deal with such situations using regularization.

Popular regularization techniques are the Lasso [8], the Tikhonov regularization [4], and the truncated SVD [6]. The lasso minimizes and Tikhonov regularization minimizes (in both cases is the regularization parameter). The truncated SVD minimizes where is a rank parameter and is the best rank- approximation to obtained via the SVD. So, the truncated SVD solution is Notice that these regularization methods impose parsimony on in different ways. A combinatorial approach to regularization is to explicitly impose the sparsity constraint on , requiring it to have few non-zero elements. We give a new deterministic algorithm which, for , computes an with at most non-zero entries such that

1.1 Preliminaries

The compact (or thin) Singular Value Decomposition (SVD) of a matrix of rank is

Here, and contain the left singular vectors of . Similarly, and contain the right singular vectors. The singular values of , which we denote as are contained in and . We use to denote the Moore-Penrose pseudo-inverse of with denoting the inverse of . Let and .

For , the SVD gives the best rank approximation to in both the spectral and the Frobenius norm: for , let ; then, for , . Also, , and . The Frobenius and the spectral norm of are defined as: ; and . Let and be matrices of appropriate dimensions; then, . This is a stronger version of the standard submultiplicativity property , which we will refer to as “spectral submultiplicativity”.

Given , the truncated rank- SVD regularized weights are

and note that

Finally, for , let where are standard basis vectors; is a sampling matrix because is a matrix whose columns are sampled (with possible repetition) from the columns of . Let be a diagonal rescaling matrix with positive entries; then, we define the sampled and rescaled columns from by : samples some columns from and then rescales them.

2 Results

Our sparse solver to minimize takes as input the sparsity parameter (i.e., the solution vector is allowed at most non-zero entries), and selects rescaled columns from (denoted by ). We then solve the least-squares problem to minimize . The result is a dense vector with dimensions. The sparse solution will be zero at indices corresponding to columns not selected in , and we use to compute the other entries of .

Theorem 1.

Let , , rank , and . Algorithm 1 runs in time and returns with at most non-zero entries such that:

This upper bound is “small” when is “effectively” low-rank, i.e., . Also, a trivial bound is (error when is the all-zeros vector), because .

In the heart of Algorithm 1 lies a method for selecting columns from (Algorithm 2), which was originally developed in [1] for column subset selection, where one selects columns from to minimize . Here, we adopt the same algorithm for least-squares.

The main tool used to prove Theorem 1 is a new “structural” result that may be of independent interest.

Lemma 2.

Fix , , rank , and sparsity . Let , where is the rank- SVD approximation to . Let and be any sampling and rescaling matrices with . Let be a matrix of sampled rescaled columns of and let (having at most non-zeros). Then,

The lemma says that if the sampling matrix satisfies a simple rank condition, then solving the regression on the sampled columns gives a sparse solution to the original problem with a performance guarantee.

2.1 Algorithm Description

Algorithm 1 selects columns from to form and the corresponding sparse vector . The core of Algorithm 1 is the subroutine DeterministicSampling, which is a method to simultaneously sample the columns of two matrices, while controlling their spectral and Frobenius norms. DeterministicSampling takes inputs and ; the matrix is orthonormal, . (In our application, and .) We view and as two sets of column vectors, and

Given and and the iterator define . For a symmetric matrix with eigenvalues and , define functions and where . Also, for a column , define At step , the algorithm selects any column for which and computes a weight such that ; Any in the interval is acceptable. (There is always at least one such index (see Lemma 8.1 in [1]).)

The running time is dominated by the search for a column which satisfies . To compute , one needs , and hence the eigenvalues of , and . This takes time once per iteration, for a total of . Then, for , we need to compute for every . This takes per iteration, for a total of . To compute , we need for which takes . So, in total, DeterministicSampling takes time, hence Algorithm 1 needs time.

DeterministicSampling uses a greedy procedure to sample columns of that satisfy the next Lemma.

2.2 Proofs

Proof of Theorem 1

Proof of Lemma 2

We will prove a more general result, and Lemma 2 will be a simple corollary. We first introduce a general matrix approximation problem and present an algorithm for this problem (Lemma 4). Lemma 2 is a corollary of Lemma 4.

Let be a matrix which we would like to approximate; let be the matrix which we will use to approximate . Specifically, we want a sparse approximation of from , which means that we would like to choose consisting of columns from such that is small. If , then, this is the column based matrix approximation problem, which has received much interest recently [2, 1]. The more general problem which we study here, with , takes on a surprisingly more difficult flavor. Our motivation is regression, but the problem could be of more general interest. We will approach the problem through the use of matrix factorizations. For , with , let where ; and, is the residual error. For fixed and , () is minimized when . Let , , and .

Lemma 4.

If , then,

Proof.

| (a) | |||

| (b) | |||

| (c) |

(a) follows by the optimality of ; (b) follows because and so ; (c) follows by the triangle inequality of matrix norms.

Lemma 4 is a general tool for the general matrix approximation problem. The bound has two terms which highlight some trade offs: the first term is the approximation of using ( is used in the factorization to approximate ); the second term is related to , the residual error in approximating . Ideally, one should choose and to simultaneously approximate with and have small residual error . In general, these are two competing goals, and a balance should be struck. Here, we focus on the Frobenius norm, and will consider only one extreme of this trade off, namely choosing the factorization to minimize . Specifically, since has rank , the best choice for which minimizes is . In this case, . Via the SVD, , and so . We apply Lemma 4, with , , and , obtaining the next corollary.

Corollary 5.

If , then,

Setting with and , we get Lemma 2.

3 Related work

A bound can be obtained using the Rank-Revealing QR (RRQR) factorization [3] which only applies to : a QR-like decomposition is used to select exactly columns of to obtain a sparse solution . Combining Eqn. (12) of [3] with Strong RRQR [5] one gets a bound We compare and and our bound is generally stronger and applies to any user specified .

Sparse Approximation Literature

The problem studied in this paper is NP-hard [7]. Sparse approximation has important applications and many approximation algorithms have been proposed. The proposed algorithms are typically either greedy or are based on convex optimization relaxations of the objective. We refer the reader to [9, 10, 11] and references therein for more details. In general, these results try to reconstruct to within an error using the sparsest possible solution . In our setting, we fix the sparsity as a constraint and compare our solution with the benchmark .

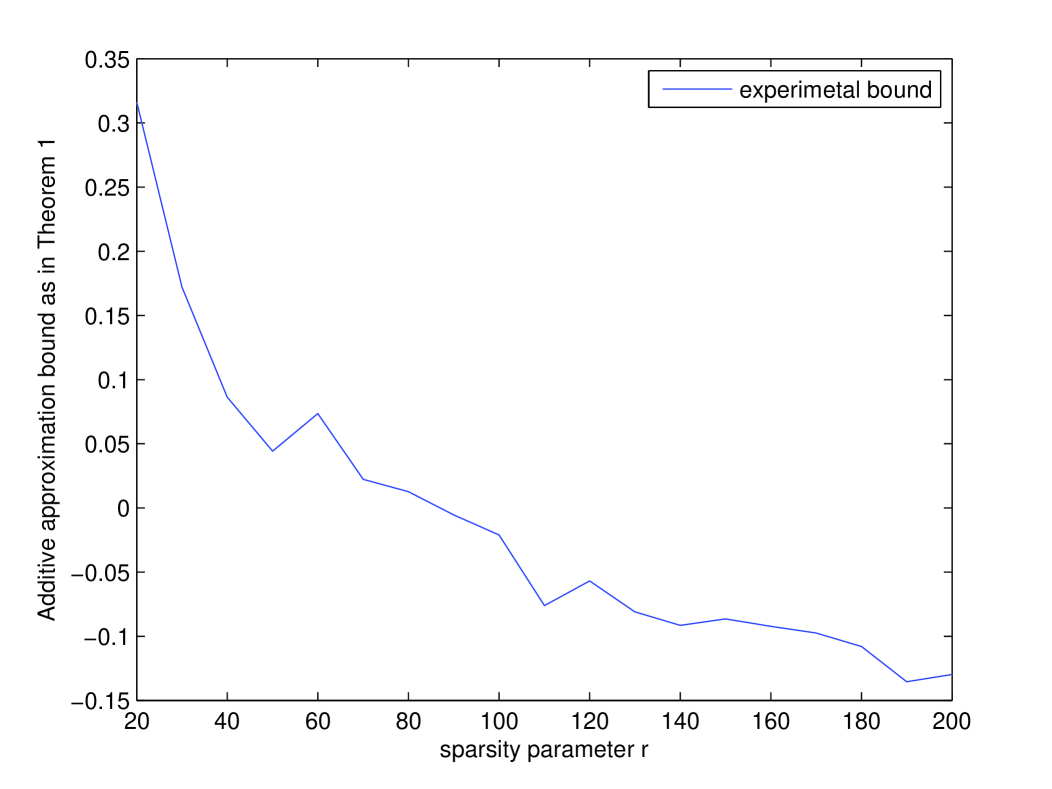

4 Numerical illustration

We implemented our algorithm in Matlab and tested it on a sparse approximation problem where and are and , respectively, with and . Each element of and are i.i.d. Gaussian random variables with zero mean and unit variance. We chose and experimented with different values of . Figure 1 shows the additive error . This experiment illustrates that the proposed algorithm computes a sparse solution vector with small approximation error. In this case, and , so the algorithm performs empirically better than what the worst-case bound of our main theorem predicts.

5 Concluding Remarks

We observe that our bound involves . This can be converted to a bound in terms of using . The better bound can be obtained by using a more expensive variant of Deterministic sampling in [1] that bounds the spectral norm of the sampled : .

Sparsity in our algorithm is enforced in an unsupervised way: the columns are selected obliviously to . An interesting open question is whether the use of different factorizations in Lemma 5, together with choosing the columns in a -dependent way can give an error bound in terms of the optimal error ?

Acknowledgements

Christos Boutsidis acknowledges the support from XDATA program of the Defense Advanced Research Projects Agency (DARPA), administered through Air Force Research Laboratory contract FA8750-12-C-0323. Malik Magdon-Ismail was partially supported by the Army Research Laboratory’s NS-CTA program under Cooperative Agreement Number W911NF-09-2-0053 and an NSF CDI grant NSF-IIS 1124827.

References

- [1] C. Boutsidis, P. Drineas, and M. Magdon-Ismail. Near-optimal column based matrix reconstruction. In Annual IEEE Symposium on Foundations of Computer Science (FOCS), 2011.

- [2] C. Boutsidis, M. W. Mahoney, and P. Drineas. An improved approximation algorithm for the column subset selection problem. In SODA, 2009.

- [3] T. F. Chan and P. C. Hansen. Some applications of the rank revealing QR factorization. SIAM Journal on Scientific and Statistical Computing, 13:727–741, 1992.

- [4] G.H. Golub, P.C. Hansen, and D. O’Leary. Tikhonov regularization and total least squares. SIAM Journal on Matrix Analysis and Applications, 21(1):185–194, 2000.

- [5] M. Gu and S. Eisenstat. Efficient algorithms for computing a strong rank-revealing QR factorization. SIAM Journal on Scientific Computing, 17:848–869, 1996.

- [6] P.C. Hansen. The truncated svd as a method for regularization. BIT Numerical Mathematics, 27(4):534–553, 1987.

- [7] B. Natarajan. Sparse approximate solutions to linear systems. SIAM Journal on Computing, 24(2):227 234, 1995.

- [8] R. Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society, pages 267–288, 1996.

- [9] J. Tropp. Greed is good: Algorithmic results for sparse approximation. Information Theory, IEEE Transactions on 50:10 (2004): 2231-2242.

- [10] J. Tropp, A. Gilbert, and M. Strauss. Algorithms for simultaneous sparse approximation. Part I: Greedy pursuit. Signal Processing 86.3 (2006): 572-588.

- [11] J. Tropp. Algorithms for simultaneous sparse approximation. Part II: Convex relaxation. Signal Processing 86.3 (2006): 589-602.