Detecting long-range dependence in non-stationary time series

Abstract

An important problem in time series analysis is the discrimination between non-stationarity and long-range dependence. Most of the literature considers the problem of testing specific parametric hypotheses of non-stationarity (such as a change in the mean) against long-range dependent stationary alternatives. In this paper we suggest a simple approach, which can be used to test the null-hypothesis of a general non-stationary short-memory against the alternative of a non-stationary long-memory process. The test procedure works in the spectral domain and uses a sequence of approximating tvFARIMA models to estimate the time varying long-range dependence parameter. We prove uniform consistency of this estimate and asymptotic normality of an averaged version. These results yield a simple test (based on the quantiles of the standard normal distribution), and it is demonstrated in a simulation study that - despite of its semi-parametric nature - the new test outperforms the currently available methods, which are constructed to discriminate between specific parametric hypotheses of non-stationarity short- and stationarity long-range dependence.

AMS subject classification: 62M10, 62M15, 62G10

Keywords and phrases: spectral density, long-memory, non-stationary processes, goodness-of-fit tests, empirical spectral measure, integrated periodogram, locally stationary process, approximating models

1 Introduction

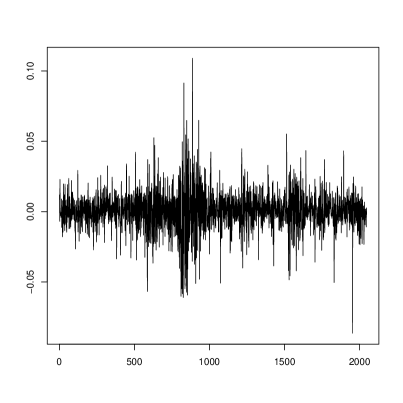

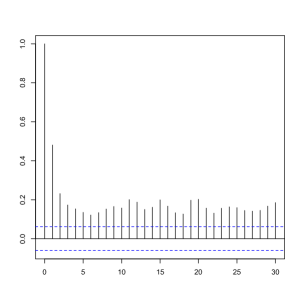

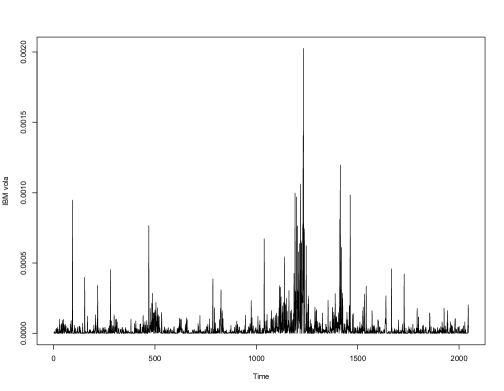

Many time series [like asset volatility or regional temperatures] exhibit a slow decay in the sample autocorrelation function and simple stationary short-memory models can not be used to analyze this type of data. A typical example is displayed in Figure 1, which shows log-returns of the IBM stock between July th and August th , with estimated autocovariance function of the squared returns .

In this example the assumption of stationarity with a summable sequence of autocovariances, say , is hard to justify for the volatility process. Long-range dependent processes have been introduced as an attractive alternative to model features of this type using an autocovariance function with the property

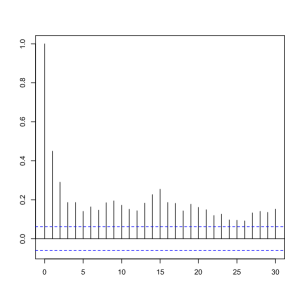

as , where denotes a “long memory” parameter. Statistical models (and corresponding theory) for long-range dependent processes are very well developed [see book1 or book2 for recent surveys] and have found applications in numerous fields [see breicrali, anwendung2 or anwendung3 for such an approach in the framework of asset volatility, video traffic and wind power modeling]. However, it was pointed out by several authors that the observation of “long memory” features in the sample autocovariance function can be as well explained by non stationarity [see mikosch2004 or motivation2 among many others]. This is clearly demonstrated in Figure 2, which shows the sample autocovariances of the squared returns from a fit of the (non-stationary) model for the returns [here is an i.i.d. sequence and is piecewise-constant, cf. starica2005 or fryzlewicz2006 for more details], and from a stationary FARIMA()-fit for the squared ones . Both models are able to explain the observed effect of ’long-range dependence’ for the volatility process. So, in summary, the same effect can be explained by two completely different modeling approaches.

For this reason several authors have pointed out the importance to distinguish between long-memory and non-stationarity [see starica2005, motivation1 or motivation2 to mention only a few]. However, there exists a surprisingly small number of statistical procedures which address problems of this type. To the best of our knowledge, kuensch1986 is the first reference investigating the existence of “long memory” if non-stationarities appear in the time series. In this article a procedure to discriminate between a long-range dependent model and a process with a monotone mean functional and weakly dependent innovations is derived. Later on, heydedai developed a method for distinguishing between long-memory and small trends. sibbertsen2009 tested the null hypothesis of a constant long-memory parameter against a break in the long-memory parameter. Furthermore, horvarth2006, baekpipi and Yau2012 investigated CUSUM and likelihood ratio tests to discriminate between the null hypothesis of no long-range and weak dependence with one change point in the mean.

Although the procedures proposed in these articles are technically mature and work rather well in suitable situations, they are, however, only designed to discriminate between long-range dependence and a very specific change in the first-order structure, like one structural break and two stationary segments of the series. This is rather restrictive, since the expectation might change in a different way than assumed [there could be, for example, continuous changes or multiple breaks instead of a single one] and the second-order structure could be time-varying as well. However, if these or more general non-stationarities occur, the discrimination techniques, which have been proposed in the literature so far, usually fail, and a procedure which is working under less restrictive assumptions is still missing.

The objective of this paper is to fill this gap and to develop a test for the null hypothesis of no long-range dependence in a framework which is flexible enough to deal with different types of

non-stationarity

in both the first and second-order structure. The general model is introduced in Section 2.

Our approach uses an estimate of a (possibly time varying) long-range dependence parameter, which

is derived by a sequence of approximating tvFARIMA models with a slightly enlarged parameter space.

This statistic estimates a functional which vanishes if and only if the null hypothesis of a short-memory locally stationary process is satisfied.

The method is based on some non-intuitive features of averages of

unconstrained estimators in models with a constrained parameter space, which become

clear from the rather technical proofs given in Section 7. In order to make

these phenomena also visible to readers which are less familiar with the technical machinery used

for the asymptotic analysis of non-stationary long range dependent processes we provide in Section 3 a motivation of our approach in the context of the classical

nonparametric regression model with repeated observations.

In Section 4 we return to the locally stationary long range dependent time series model and

prove consistency and asymptotic normality of a corresponding test statistic under the null hypothesis of no long-range dependence.

As a consequence we obtain a nonparametric test, which is based on the quantiles of the standard normal distribution and therefore very easy to implement. The finite sample properties of the new test are investigated in Section 5, which also provides a comparison with the competing procedures with a focus on non-stationarities. We demonstrate the superiority of the new method and also illustrate its application in two data examples.

2 Locally stationary long-range dependent processes

In order to develop a test for the presence of long-range dependence which can deal with different kinds of non-stationarity, a set-up is required which includes short-memory processes with a rather general time-varying first and second order structure and a reasonable long-range dependent extension. For this purpose, we consider a triangular scheme of locally stationary long-memory processes, which have an MA() representation of the form

| (2.1) |

where

| (2.2) |

is a “smooth” function and are independent standard normal distributed random variables. The assumption of a normal distribution for the innovations is made to simplify the technical arguments in the proofs of our results [see Section 7] and can be replaced by the existence of moments of all order of the random variables - see Remark 4.8 for more details. Note also that the random variables have been standardized to have variance . Alternatively, one could normalize by and allow for an additional parameter in the variance. For the coefficients and the function in the expansion (2.1) we make the following additional assumptions.

Assumption 2.1.

Let denote a sequence of stochastic processes which have an MA() representation of the form (2.1) satisfying (2.2), where is twice continuously differentiable. Furthermore, we assume that the following conditions are satisfied:

-

1)

There exist twice continuously differentiable functions () such that the conditions

(2.3) (2.4) are satisfied uniformly with respect to as , where and Moreover, the functions , in (2.4) are twice continuously differentiable.

- 2)

-

3)

There exists a constant , which is independent of and , such that for the conditions

(2.8) are satisfied for all .

Similar locally stationary long-range dependent models have been investigated by beran2009, palole2010 and vonsachs2011 and wuzhou2014. It is also worthwhile to mention that in general (2.4) does not imply (2.6) and (2.7) and vice versa conditions (2.6) and (2.7) do not imply (2.4). Therefore, none of the conditions (2.4), (2.6) or (2.7) can be omitted in Assumption 2.1. Note also hat in contrast to the standard framework of local stationarity introduced by dahlhaus1997 and extended to the long-memory case in palole2010, condition (2.3) is much weaker. For example, in contrast to these references the assumptions made here include tvFARIMA()-models as well [see Theorem 2.2 in prevet2012]. Moreover, we mention again that the assumption of Gaussianity is only imposed to simplify the technical arguments in the proofs of our main results - see Remark 4.8 for more details. The very specific form of the function in (2.7) implies that the process can be locally approximated by a FARIMA() process in the sense of (2.3). More precisely, we obtain with

| (2.9) |

() the relation

between the approximating functions and the time-varying AR-parameters [see the proof of Lemma 3.2 in koktaqqu for more details]. The relation (2.9) can be used to calculate the coefficients from the functions , i.e.

In order to further visualize some properties of these kinds of locally stationary long-memory models we introduce for every fixed the stationary process

One can show that condition (2.4) implies the existence of bounded functions such that the approximations

| (2.10) |

and

| (2.11) |

hold [see palole2010 for details].

Consequently, the autocovariances are not absolutely summable if the function in (2.4) is not vanishing, and in this case the time varying spectral density has a pole at for any for which is positive.

Note that in general

the statements (2.10) and (2.11) are not equivalent [see yong1974 for a discussion of this problem in the stationary case].

In the framework of these long-range dependent locally stationary processes we now investigate the null hypothesis that the time-varying “long memory” parameter vanishes for all , i.e. there is no long-range dependence in the locally stationary process . The alternative is defined by the property that the function is nonnegative on the interval and positive on a subset of positive Lebesgue measure. Since the function is continuous and non-negative we obtain that the hypotheses

| (2.12) |

are equivalent to

| (2.13) |

where the quantity is defined by

| (2.14) |

In Section 4 we will develop a nonparametric estimator of the function and the integral . Roughly speaking, the sample size is decomposed into blocks with length (i.e. ), where is some positive integer. We define the corresponding midpoints in both the time and rescaled time domain by , , respectively, and calculate an estimator of the long range dependence parameter at the point on each of the blocks (for the exact definition of the estimator see Section 4). The test statistic is then obtained as

| (2.15) |

and could be considered as a Riemann sum of the integral , which approximates the integral in (2.14).

Remark 2.2.

(some boundary issues)

Note that for each the local long range dependence parameter is a boundary point of the parameter

space defined by the two hypotheses in (2.12). However, we will not use this property for the construction of the estimates

of the quantities , which are aggregated in the statistic (2.15).

For this purpose we consider a sequence of approximating

tvFARIMA models, where the parameter converges to infinity as the sample size increases

and the corresponding long range

dependence parameters are allowed to vary in intervals of the form , where .

and are positive sequences converging to .

We will prove in Theorem 4.3 below

that this provides a uniformly consistent estimate of the function and that

an average of these statistics provides a consistent and asymptotically normal distributed estimate of the integral (see Theorem 4.5 and

Theorem 4.6 below).

As a consequence we obtain a consistent level- test for the presence of long-range dependence in non-stationary time series by rejecting the null hypothesis for large values of the estimator of .

On a first glance these

properties are surprising because we use unconstrained (i.e. potentially negative) estimators of the long range dependence parameters in the approximating tvFARIMA models to estimate the non-negative function , but the statements become clear

from the rather technical arguments given in the proofs of Section 7.

The situation is similar to the problem of testing the hypothesis versus for the mean of a

sample of i.i.d. random variables . A test which rejects , whenever (here is an estimator of the variance and the -quantile of the standard normal distribution) has asymptotic level and is consistent. Moreover,

in Section 3 we consider an example of testing for a positive signal in a nonparametric regression model and

demonstrate that the aggregation of local statistics of the type might have substantial advantages compared

to the aggregation of local estimators of the from , which reflect the constraint in its definition.

3 Testing for a positive nonparametric signal

In this section we provide some heuristic explanation for the phenomenon described in the previous paragraph, which is also available to readers which are less familiar with the technical machinery used for the asymptotic analysis of non-stationary long range dependent processes. We will also demonstrate that there are situations where more powerful tests can be obtained by ignoring particular constraints in the estimation procedure. This situation occurs in particular if different estimators are aggregated as described in (2.15).

For this purpose we consider the problem of testing the hypothesis of a vanishing regression function against the alternative that the regression function is positive on the interval in the common nonparametric regression model

Here are i.i.d. standard normal distributed (centered) random variables (this assumption is in fact not necessary but makes some of the following arguments much simpler), and is a smooth non-negative Lipschitz continuous function on the interval . We are interested in testing the hypothesis

| (3.1) |

Note that the alternative could also be considered on the set of all non-negative functions which are positive on a subset of positive Lebesgue measure, say . As this generalization does not change any of the subsequent arguments (only integrals of the form and sums of the form have to be replaced by and (here denotes the Lebesgue measure of the set ) we restrict ourselves to the case for the sake of transparency.

3.1 Tests based on unconstrained estimators: The idea used in Section 4 below for testing hypotheses of this type translates in the nonparametric regression model to the following procedure. We first define (unconstrained) estimators for the values , that is (), and then consider the average

Note that is a sum of independent identically distributed random variables with variance Consequently, using a central limit theorem for triangular arrays, shows that as . Moreover, since is Lipschitz continuous, this implies

whenever . Thus a consistent and asymptotic level test for the hypothesis (3.1) is obtained by rejecting the null hypothesis , whenever

| (3.2) |

where is the -quantile of the standard normal distribution.

3.2 Tests based on constrained estimators: Alternatively, and - on a first glance - more reasonable strategy is to use a constrained estimator which addresses the boundary condition . This gives

as estimator for , and we obtain with the notation the representation

| (3.3) |

where , Note that , which yields

| (3.4) |

This term is of order (exponentially in and independent of , provided that on ). Note also that

This gives for the variance of the random variable

Ljapunoff’s central limit theorem now shows that where and

This implies (observing the Lipschitz continuity of the regression function and )

Note that the statistic is asymptotically normal distributed, although we average constrained estimators. Under the null hypothesis things are simplifying. In particular we obtain and a test based on rejects the null hypothesis , whenever

| (3.5) |

This test has asymptotic level and is consistent. We conclude this section mentioning once again that the assumption of i.i.d. standard normal distributed errors was made to minimize the technical arguments. All statements remain true for arbitrary centered errors which have moments of order . This observation is a simple consequence of the central limit theorem, and in the following finite sample comparison we actually use non-normal error distributions.

3.3 A comparison of the two tests: The use of different estimators for the quantities yields to the different tests (3.2) and (3.5) the hypotheses in (3.1). Both test statistics have an asymptotic normal distribution under the null hypothesis and the alternative. A finite sample comparison is given in Table 1 where we report simulation results for the functions

| (3.6) | |||||

| (3.7) | |||||

| (3.8) |

The sample sizes are and and we use simulation runs to estimate the rejection probabilities of the tests (3.2) and (3.5). For the distribution of the errors distribution we use a distribution, in order to demonstrate that the previous findings do not depend on the assumption of normal distributed errors. We observe that the test (3.2) based on the statistic (which uses the unconstrained estimators of the regression function) outperforms the method (3.5) which uses the constrained estimators.

| model | (3.6) | (3.7) | (3.8) | (3.6) | (3.7) | (3.8) | ||||||

| level | ||||||||||||

| test (3.2) | 0.052 | 0.103 | 0.634 | 0.764 | 0.918 | 0.966 | 0.056 | 0.109 | 0.999 | 1.000 | 1.000 | 1.000 |

| test (3.5) | 0.070 | 0.118 | 0.576 | 0.684 | 0.873 | 0.926 | 0.065 | 0.112 | 0.997 | 0.998 | 1.000 | 1.000 |

We can also give a “theoretical” argument for the advantages of the unconstrained approach. Note that for a positive function the power of test (3.2) is approximately given by

| (3.9) |

where denotes the distribution function of the standard normal distribution. This formula is remarkably precise. For example, if we obtain for the power of the test (3.2) , while the result of the simulation is . Similarly, the power of the test (3.5) is approximately given by

| (3.10) |

where the term is defined by

Now, note that and that of exponential order (uniformly) if for all

as Consequently, the term will be negative for reasonable large . It actually

diverges to , but at a lower rate as the dominating term in (3.10), which converges to .

This means that the test (3.2) based on unconstrained estimation is more powerful than the test (3.5), which uses constrained estimation.

A similar argument for the superiority of the test (3.2) based on the unconstrained estimators of the regression function

can be given for local alternatives of the form , where is a Lipschitz continuous function.

More precisely, the asymptotic power of the tests (3.2) and (3.5) is given by

and

respectively. As , it follows that the unconstrained test (3.2) also outperforms the test (3.5) under local alternatives. Exemplarily, we display in Table 2 the power of the two tests under the local alternatives

4 Testing short- versus long-memory

In order to estimate the integral we use a sequence of semi-parametric models approximating the processes with time varying spectral density (2.6) and proceed in several steps. First we choose an increasing sequence , which diverges ’slowly’ to infinity as the sample size grows, and fit a tvFARIMA(,,0) model to the data. To be precise, we consider a locally stationary long-memory model with time varying spectral density defined by

| (4.1) |

where

and is a vector valued function. We emphasize again that depends on the sample size and refer to Assumption 4.1 for the precise condtions regarding its growth rate. We then estimate the function by a localized Whittle-estimator, that is

| (4.2) |

where

| (4.3) |

denotes the (local) Whittle likelihood [see optimallength or dahlpolo2009] and for each the parameter space is a compact set which will be specified in Assumption 4.1. In (4.2) and (4.3) the quantity

| (4.4) |

denotes the mean-corrected local periodogram, is an even window-length which is ’small’ compared to

and is an asymptotically unbiased estimator of the mean function ,

see dahlhaus1997. Here and throughout this paper we use the convention

for . We finally obtain an estimator for the time-varying long-memory parameter by taking the first component of the dimensional vector defined in (4.2). We emphasize that the tvFARIMA models are only used to define the estimator

as the solution of the optimization problem (4.2).

It will be demonstrated in Theorem 4.3

below that - provided that the “true” underlying process can be approximated by tvFARIMA models -

this approach results in a uniformly consistent estimator of the time-varying long-memory parameter.

For this purpose we define as the dimensional vector containing

the long memory parameter and the first AR-parameter functions of the approximating process defined by the representation (2.6) and (2.7). Here and

throughout this paper, denotes the element in the position (1,1) and the spectral norm of the matrix , respectively.

We state the following technical assumptions.

Assumption 4.1.

Let be a sequence converging to infinity for increasing sample size and let and denote positive sequences in the interval such that

For each and define , where the constant is the same as in Assumption 2.1. For each is a compact set with a finite number (independent of ) of connected components with positive Lebesgue measure. Let denote the space of all four times continuously differentiable functions with for all . If and are distinct elements of , we assume that the set has positive Lebesgue measure. We assume that the following conditions hold for each :

-

(i)

The functions in (4.1) are bounded from below by a positive constant (which is independent of ) and are four times continuously differentiable with respect to and , where all partial derivates of up to the order four are bounded with a constant independent of .

-

(ii)

For each the parameter exists and is uniquely determined, where

Moreover, for each the vectors and are interior points of .

-

(iii)

Define

(4.5) [here denotes the derivative with respect to the parameter-vector ], then the matrix is non-singular for every , , and

(4.6) as . Furthermore, condition (4.18) is also satisfied if the function is replaced by any sequence such that . For such a sequence we additionally assume that the condition

is satisfied as .

-

(iv)

Let be compact and

In order do illustrate the construction of the sets in Assumption 4.1, consider exemplarily the case where for some the polynomial with the coefficients from (2.7) is bounded away from zero inside the disc (uniformly with respect to ). In this case the sets can be chosen as the intersection of the set with the set

Here the set is defined by

the constants are chosen such that and such that the sequence is an inner point of the set .

Assumption (i) and (ii) are rather standard in a semi-parametric locally stationary time series model [see for example optimallength or dahlpolo2009

among others]. Note that the number of parameters grows with increasing sample size in order to obtain a consistent estimate of the function in model (2.5).

The restriction on the spectral norm in part (iv) was verified for a large number of long-range dependent models

by kokozkarate [see equation (4.4) in this reference]. Note that these assumptions solely depend on the ”true” underlying model.

On the other hand, an important step of our approach is the approximation

of the spectral density in (2.6) by the truncated analogue

and the following assumption guarantees that the corresponding approximation error converges to with reasonable rate. As a consequence it provides a link between the growth rate of and as the sample size increases.

Assumption 4.2.

Suppose that , and

| (4.7) |

for some as .

Note that

| (4.8) |

and an application of Lemma 2.4 in kreisspappol2011 to the second factor (corresponding to the ”short memory” part) shows that condition (4.7) with implies

As a consequence Assumption 4.1 (iii) is rather intuitive, because the parametric model (4.1) can be considered as an approximation of the “true” model defined in terms of the time varying spectral density (2.5). We finally note that condition (4.7) is satisfied for a large number of tvFARIMA() models, because it can be shown by similar arguments as in the proof of Theorem 2.2 in prevet2012 that the coefficients are geometrically decaying. This yields for some resulting in a logarithmic growth rate for , which is in line with the findings of kokozkarate. Similarly, one can include processes whose AR coefficients decay such that is satisfied for some . In this case needs to grow at some specific polynomial rate.

Our first main result states a uniform convergence rate for the difference between and its true counterpart . As a consequence it implies that the estimator obtained in the approximating models is uniformly consistent for the (time varying) long-range dependence parameter of the locally stationary process.

Theorem 4.3.

Remark 4.4.

It follows from the proof of Theorem 4.10 below that there exists an estimator with

for every . Under the addional assumption

| (4.11) |

for some a logarithmic rate for the dimension of the tvFARIMA models can be used such that assumption (4.9) is satisfied [for a broad class of models, where the stronger condition (4.11) is in fact satisfied, we refer to the discussion following (4.8)].

In order to obtain an estimator of the quantity in (2.14) we assume without loss of generality that the sample size can be decomposed into blocks with length (i.e. ), where is some positive integer. We define the corresponding midpoints in both the time and rescaled time domain by , , respectively, and calculate on each of the blocks as described in the previous paragraph. The test statistic is then obtained as

| (4.12) |

The following two results specify the asymptotic behaviour of the statistic under the null hypothesis and alternative.

Theorem 4.5.

Assume that the null hypothesis (of no long-range dependence) is true. Let Assumptions 2.1, 4.1 and 4.2 be satisfied, define and suppose that the estimator of the mean function satisfies

| (4.13) | |||||

| (4.14) |

where is the constant in Assumption 4.2 satisfying . Moreover, if the conditions

hold as , then we have

| (4.15) |

Note that is an average of the estimates of the long-range dependence parameter in the approximating tvFARIMA model. By Assumption 4.1 the point is an interior point of the canonical projection of the parameter space onto the first component, which motivates the asymptotic normality obtained in Theorem 4.5. More precisely, we show in Section 7 that the leading term in the stochastic expansion of is given by

where denotes the first element of the dimensional vector . Asymptotic normality follows because the individual terms in this sum are asymptotically independent (see Section 7 for details and Section 3 for a similar result in a simplified model).

Theorem 4.6.

Remark 4.7.

(more transparent conditions) If assumption (4.11) is satisfied, more transparent conditions for Theorem 4.3, 4.5 and 4.6 can be given. To be precise assume that (4.11) holds for some and choose

for some . If , then it follows by straightforward but tedious calculations that Theorem 4.3, 4.5 and 4.6 hold for with any satisfying (note that this conditions provides a further restriction for the choice of the constant ). Similarly, if the results hold, whenever .

Remark 4.8.

(the non-Gaussian case)

It is worthwhile to mention that in most of articles cited in this paper the assumption of Gaussianity for the innovation process in (2.1) is required. In the present case this assumption is not necessary and is only imposed here to simplify technical arguments in the proof of Theorem 7.1. This observation is a consequence of method of proof used in Section 7. In fact, asymptotic normality is established by the method of moments showing that all cumulants of the statistic under consideration converge to those of a normal distribution. In the definition of all cumulants one needs the existence of all moments of (which is obviously true in the Gaussian case).

The main simplification under the assumption of Gaussianity consists in the fact that one does not have to work with partitions including cumulants of any possible order. The extension to non Gaussian innovations does not change the main argument in the proofs, but the calculations become

substantially more complicated, and the details are omitted for the sake of brevity.

As a consequence all results of this section remain true as long as the innovations are independent with all moments existing, mean zero and for some twice continuously differentiable function .

To be more precise, in order to address for non-Gaussian innovations

the variance in Theorem 7.1 (which is one of the main ingredients for the proofs in Section 7) has to be replaced by

where is defined in (7.5) and denotes the fourth cumulant of the innovations, i.e. for all . In the proof of Theorem 4.5 we apply this result with . Consequently, we obtain that in the non-Gaussian case the asymptotic normality in Theorem 4.5 holds, where the matrix has to be replaced by

| (4.17) |

Thus, under the null hypothesis it follows that

| (4.18) |

Remark 4.9.

(the final test) Note that the first term in (4.17) can be consistently estimated by

This gives as an estimator for the statistic

where and are obtained by calculating the empirical second and fourth moment , of the residuals

and setting , . Since , an asymptotic level -test is obtained from (4.18) by rejecting the null hypothesis (2.13), whenever

| (4.19) |

where denotes the -quantile of the standard normal distribution (in the Gaussian case can be replaced by ). It then follows from Remark 4.8 and Theorem 4.6 that for any estimator of the mean function satisfying (4.13), (4.14) and (4.16), the test, which rejects whenever (4.19) is satisfied, is a consistent level- test for the null hypothesis stated in (2.13). The finite sample properties of this resulting test are investigated in Section 5.

A popular estimate of the mean function is given by the the local-window estimator

| (4.20) |

where is a window-length which does not necessarily coincide with the corresponding parameter in the calculation of the local periodogram. Note that also is an asymptotically unbiased estimator for if and . The final result of this section shows that this estimator satisfies the assumptions of Theorem 4.5 and 4.6 if grows at a ’slightly’ faster rate than . This means, it can be used in the asymptotic level test defined by (4.19).

Theorem 4.10.

- a)

- b)

Remark 4.11.

(parametric models) Analogues of Theorem 4.5 and 4.6 can be obtained in a parametric framework. To be precise, assume that the approximating processes has a time varying spectral density of the form (4.1), where is fixed and known. In this case it is not necessary that the dimension is increasing with the sample size and Assumption 4.1(iii) and 4.2 are not required. All other stated assumptions are rather standard in this framework of a semi-parametric locally stationary time series model [see for example optimallength or dahlpolo2009 among others]. With these modifications Theorem 4.5 and 4.6 remain valid and as a consequence we obtain an alternative test to the likelihood ratio test proposed in Yau2012, which operates in the spectral domain and can be used for more general null hypotheses as considered by these authors.

Remark 4.12.

(local alternatives) Theorem 4.5 remains valid under local alternatives converging to the null hypothesis at a rate . To be precise let where is a twice continuously differentiable function such that . Then it follows by similar arguments as given in the proof of Theorem 4.5, that

(note that due to Assumption 4.1(iv) and that does not depend on the long-memory parameter function ). This indicates that (asymptotically) the power of the test (4.19) is increasing with , which can also be observed in the simulation study presented in the following Section.

Remark 4.13.

(some technical comments) The (uniform) smoothness conditions stated in Assumption 2.1 are commonly made in the literature [see for example palole2010] and are also required in the present context to obtain the uniform consistency of the estimator for the function . However, it is worthwhile to mention that the asymptotic properties of the proposed test can also be derived under weaker assumptions. To be more precise, Theorem 4.5 remains valid if the conditions on the function and its derivatives stated in Assumption 2.1 are replaced by

for all and .

Here denotes a function such that for all . The proof of this statement can be performed by

similar arguments as given in the proof of Theorem 4.5 with additional technical arguments for the more delicate

estimates of the error terms.

Moreover, we conjecture that, the conditions can be further weakened such that the function

is only integrable up to a specific order. A detailed verification of such a statement, however, is an open problem and far beyond the scope of

the present paper.

5 Finite sample properties

The application of the test (4.19) requires the choice of several parameters. Based on an extensive numerical investigation we recommend the following rules. For the choice of the parameter in the local window estimate of the mean function [for a precise definition see (4.20)] we use . Because the procedure is based on a sequence of approximating tvFARIMA-processes the choice of the order is essential, and we suggest the AIC criterion for this purpose, that is

| (5.1) |

where , and is the estimated spectral density of a stationary FARIMA process and is the mean-corrected periodogram given by

Note that we choose the same order for each of the blocks. An alternative choice is to use tvFARIMA models of different order for each block. In our numerical experiments we investigated both methods and we observed substantial advantages for the rule (the results of this comparison are not displayed for the sake of brevity). Because this approach also has additional computational advantages we recommend to choose the same approximating tvFARIMA(k,d,0) model for all blocks. Finally, the performance of the test depends on the choice of , and this dependency will be carefully investigated in the following discussion.

5.1 Simulation of level and power

All results presented in this section are based on simulation runs, and we begin with an investigation of the approximation of the nominal level of the test (4.19) considering three examples. The first example is given by a location model with a tvAR(1)-process, that is

| (5.2) |

where

| (5.3) |

The innovations in (5.3) are either i.i.d. standard normal or i.i.d. chi-square distributed normalized such that , i.e. . Two cases are investigated for the mean function representing a smooth change and abrupt change in the mean effect, i.e.

| (5.4) | |||||

| (5.7) |

The mean function (5.7) is not smooth and used to investigate the impact of a violation of the assumptions in the procedure. Our third example consists of a tvMA(1)-process given by

| (5.8) |

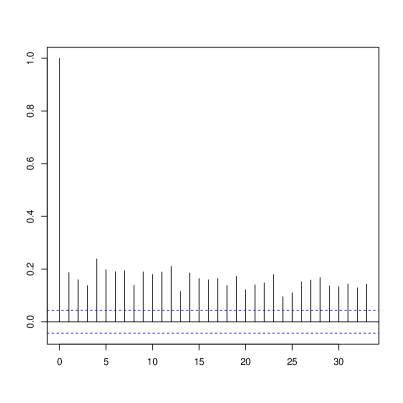

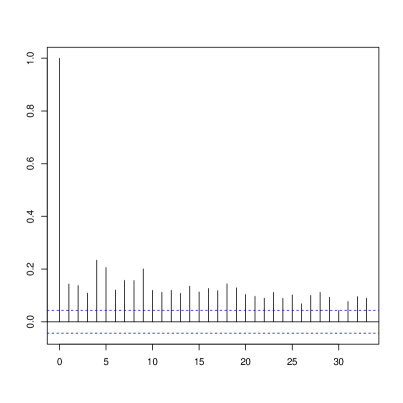

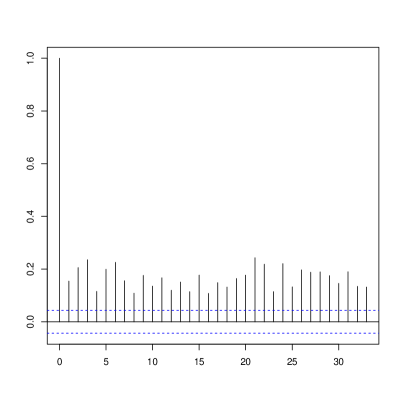

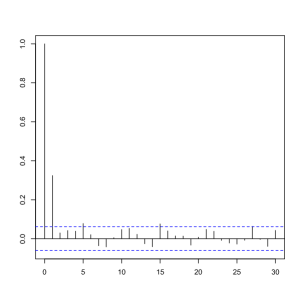

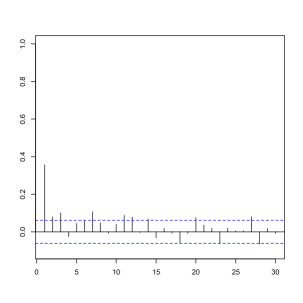

where is again a sequence of i.i.d. normal or chi-square distributed random variables normalized to have mean 0 and variance 1. Figure 3 and 4 show the sample autocovariance and the sample partial autocovariance functions of 1024 observations generated by the models (5.4), (5.7) and (5.8), respectively, from which it is clearly visible that the mean functions in (5.4) and (5.7) are causing a long-memory type behaviour. In Table 3, we show for these models the simulated level of the test (4.19) for various choices of . We observe in model (5.2) and (5.8) a reasonable approximation of the nominal level whenever and the sample size is larger or equal than . Here the results are similar for normal and chi-square distributed innovations. On the other hand in model (5.2) with mean function (5.7) the assumptions of the asymptotic theory are violated and the situation is different. For moderate sample sizes the specification yields to an overestimation of the nominal level. Moreover, the approximation of the nominal level becomes worse with increasing sample size. We conjecture that the performance of the test could be improved by using estimators addressing the problem of jumps in the mean function.

In order to investigate the power of the test (4.19) and to compare it with the competing procedures proposed by horvarth2006, baekpipi and Yau2012, we simulated data from a tvFARIMA(-process

| (5.9) |

and a tvFARIMA(-process

| (5.10) |

where is the backshift operator that is . In both cases the long-memory function is given by . Because all competing procedures are designed to detect stationary long-range dependent alternatives, we also simulated data from a stationary FARIMA(1,,1)-process

| (5.11) |

The corresponding results for the new test (4.19) and its competitors are presented in Table 4-7. In Table 4 and 5 we show the simulated power in model (5.9) for (standardized) normal and chi-square distributed innovations. We do not observe substantial differences in the power of the new test under different distributional assumptions and for this reason Table 7 and 7 only contain results for normal distributed innovations. In the first column the rejection probabilities of the new test are displayed and we observe a reasonable power in all models under consideration. Interestingly, the differences in power between the tvFARIMA( and the tvFARIMA(-model are rather small (see second column in Table 4 and 7). The results in Table 7 show a loss in power, which corresponds to intuition because the “average” long-memory effect in model (5.11) is 0.1, while it is in model (5.9) and (5.10) [see also Remark 4.12 and the discussion at the end of this section].

In order to compare the new test with existing approaches we next investigate the performance of the procedures proposed by horvarth2006, baekpipi and Yau2012, which are designed for a

test of the null hypothesis ”the process has the short memory property

with a structural break in the mean” against the alternative ”the process is stationary and has the long memory property”.

The third columns of Table 4-7 show the power of the test in baekpipi, which also operates in the spectral domain.

These authors estimate

the change in the mean with a break point estimator and remove

this mean effect (which is responsible for the observed local stationarity) from the time series. Then they calculated the local Whittle estimator introduced by rob95 for the self similarity parameter and reject the null hypothesis for large value of this estimate.

Note that the calculation of the local Whittle estimator requires the specification of the number of “low frequencies” and we used as baekpipi suggested in their simulation study.

We observe that the new test (4.19) yields larger power than the procedure of baekpipi in nearly all cases under consideration. This improvement becomes more substantial with increasing sample size.

Next we study the performance of the procedure proposed by horvarth2006 in models (5.9)-(5.11). These authors use a CUSUM statistic to construct an estimator, say , for a (possible) change point in a time series.

Then two CUSUM statistics are computed for the first elements of the time series and the remaining ones, respectively.

The test statistic is given by the maximum of those two.

For the choice of the bandwidth function we use as suggested by these authors in

Section 3 of their article. The results are depicted in the fourth columns of Table 4-7 and demonstrate that this test is not able to detect long-range dependence in both the stationary and locally stationary case. These findings coincide with the results of baekpipi who also remarked that the test in horvarth2006 has very low power against long-range dependence alternatives.

The method proposed by Yau2012 consists of a parametric

likelihood ratio test assuming two (not necessarily equal) ARMA models before and after

the breakpoint of the mean function. Their method requires a specification of the order of these two models and

we used ARMA-models under the null hypothesis and a FARIMA model under the alternative hypothesis.

The corresponding results for this test are depicted in the fifth columns of Table 4-7 corresponding to non-stationary and stationary

long-range dependent alternatives, respectively. We observe that in these cases the new test (4.19) outperforms

the test proposed in Yau2012 if the sample size is larger than and that both tests have similar power for sample size (see the fifth column of Table 4 and 7). On the other hand, in the case of the long-range dependent stationary alternative (5.11) the test of Yau2012 yields slightly better rejection probabilities than the new test (4.19) for smaller sample sizes while we observe advantages of the proposed test in this paper for sample sizes and . These results are remarkable, because the test of Yau2012 is especially designed to detect stationary alternatives of FARIMA() type, but the new semi-parametric test still yields an improvement in many cases.

Finally, as it was pointed out by a reviewer, it is also of interest to systematically investigate the power of the test (4.19) as a function of the quantity . The arguments in Remark 4.12 indicate that the power is increasing with , and we will now investigate if these properties can also be observed in finite samples. For this purpose we simulated data from the tvFARIMA(0,d,1)-process in (5.10) with different choices for the long-memory function :

| (5.12) | |||||

| (5.16) | |||||

| (5.17) |

For the functions and the quantity is given by while for and . The corresponding results are shown in Table 8. We mainly discuss the case (because it yields to the best approximation of the nominal level) and mention that the interpretation of the results for other choice of is very similar. For a fixed we do not observe substantial differences between the functions and in the case , while the function yields to a larger power. This observation can be explained by the fact that the integral in (2.14) is approximated by a Riemann sum at points . Consider exemplarily the case (which is recommended, because it yields to a good approximation of the nominal level). While for the function all estimates roughly yield the same contribution of size , we observe that for the function two points (namely and ) yield a contribution of size and the other points yield the value . Nevertheless the total contribution in this case is , while it is only for . This explains the improvement in power observed for the function . We expect that these advantages vanish asymptotically, because the approximation of by its Riemann sum becomes more accurate with increasing . Finally, a comparison of columns 1-3 (corresponding to the case with columns 4-5 in Table 8 (corresponding to the case ) shows that the monotonicity of the power as a function of the integral can also be observed in samples of realistic size.

| (5.2), (5.4) | (5.2),(5.7) | (5.8) | (5.2), (5.4) | (5.2),(5.7) | (5.8) | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 256 | 64 | 4 | .090 | .128 | .094 | .145 | .085 | .122 | .094 | .142 | .100 | .162 | 084 | .118 |

| 256 | 32 | 8 | .151 | .228 | .165 | .255 | .182 | .261 | .218 | .319 | .249 | .335 | .187 | .258 |

| 512 | 128 | 4 | .061 | .095 | .070 | .114 | .069 | .099 | .066 | .100 | .062 | .098 | .068 | .090 |

| 512 | 64 | 8 | .089 | .130 | .089 | .126 | .081 | .107 | .086 | .144 | .102 | .140 | .074 | .118 |

| 1024 | 256 | 4 | .046 | .072 | .077 | .119 | .069 | .106 | .042 | .076 | .080 | .126 | .080 | .114 |

| 1024 | 128 | 8 | .059 | .087 | .061 | .088 | .064 | .093 | .058 | .082 | .090 | .124 | .066 | .106 |

| 2048 | 512 | 4 | .048 | .090 | .094 | .148 | .074 | .122 | .048 | .078 | .116 | .154 | .086 | .116 |

| 2048 | 256 | 8 | .026 | .034 | .026 | .058 | .062 | .084 | .020 | .026 | .040 | .068 | .046 | .074 |

| 4096 | 1024 | 4 | .056 | .094 | .164 | .248 | .076 | .112 | .052 | .098 | .196 | .264 | .085 | .127 |

| 4096 | 512 | 8 | .014 | .030 | .026 | .056 | .060 | .080 | .026 | .044 | .046 | .062 | .058 | .090 |

| (4.19) | Baek/Pipiras | Berkes et. al | Yau/Davis | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 256 | 64 | 4 | 0.288 | 0.354 | 0.248 | 0.330 | 0.037 | 0.080 | 0.250 | 0.306 |

| 256 | 32 | 8 | 0.290 | 0.436 | ||||||

| 512 | 128 | 4 | 0.530 | 0.590 | 0.356 | 0.468 | 0.006 | 0.041 | 0.182 | 0.226 |

| 512 | 64 | 8 | 0.348 | 0.458 | ||||||

| 1024 | 256 | 4 | 0.746 | 0.770 | 0.562 | 0.656 | 0.026 | 0.102 | 0.204 | 0.267 |

| 1024 | 128 | 8 | 0.412 | 0.512 | ||||||

| 2048 | 512 | 4 | 0.882 | 0.900 | 0.724 | 0.816 | 0.152 | 0.222 | 0.376 | 0.452 |

| 2048 | 256 | 8 | 0.625 | 0.683 | ||||||

| 4096 | 1024 | 4 | 0.974 | 0.978 | 0.892 | 0.928 | 0.318 | 0.460 | 0.740 | 0.782 |

| 4096 | 512 | 8 | 0.892 | 0.910 | ||||||

| (4.19) | Baek/Pipiras | Berkes et. al | Yau/Davis | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 256 | 64 | 4 | 0.340 | 0.436 | 0.244 | 0.343 | 0.034 | 0.082 | 0.262 | 0.335 |

| 256 | 32 | 8 | 0.373 | 0.492 | ||||||

| 512 | 128 | 4 | 0.550 | 0.600 | 0.434 | 0.510 | 0.005 | 0.021 | 0.228 | 0.276 |

| 512 | 64 | 8 | 0.362 | 0.476 | ||||||

| 1024 | 256 | 4 | 0.714 | 0.756 | 0.527 | 0.641 | 0.047 | 0.130 | 0.197 | 0.240 |

| 1024 | 128 | 8 | 0.446 | 0.522 | ||||||

| 2048 | 512 | 4 | 0.910 | 0.926 | 0.721 | 0.805 | 0.143 | 0.244 | 0.263 | 0.334 |

| 2048 | 256 | 8 | 0.634 | 0.708 | ||||||

| 4096 | 1024 | 4 | 0.974 | 0.976 | 0.889 | 0.938 | 0.311 | 0.408 | 0.713 | 0.741 |

| 4096 | 512 | 8 | 0.923 | 0.938 | ||||||

| (4.19) | Baek/Pipiras | Berkes et. al | Yau/Davis | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 256 | 64 | 4 | 0.260 | 0.330 | 0.230 | 0.322 | 0.039 | 0.088 | 0.296 | 0.366 |

| 256 | 32 | 8 | 0.276 | 0.394 | ||||||

| 512 | 128 | 4 | 0.528 | 0.590 | 0.342 | 0.456 | 0.010 | 0.036 | 0.268 | 0.322 |

| 512 | 64 | 8 | 0.314 | 0.414 | ||||||

| 1024 | 256 | 4 | 0.774 | 0.796 | 0.546 | 0.656 | 0.024 | 0.086 | 0.228 | 0.292 |

| 1024 | 128 | 8 | 0.414 | 0.492 | ||||||

| 2048 | 512 | 4 | 0.900 | 0.913 | 0.758 | 0.820 | 0.168 | 0.268 | 0.320 | 0.404 |

| 2048 | 256 | 8 | 0.608 | 0.665 | ||||||

| 4096 | 1024 | 4 | 0.994 | 0.996 | 0.900 | 0.940 | 0.332 | 0.444 | 0.649 | 0.697 |

| 4096 | 512 | 8 | 0.982 | 0.990 | ||||||

| (4.19) | Baek/Pipiras | Berkes et. al | Yau/Davis | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 256 | 64 | 4 | 0.094 | 0.136 | 0.087 | 0.149 | 0.045 | 0.093 | 0.178 | 0.210 |

| 256 | 32 | 8 | 0.138 | 0.216 | ||||||

| 512 | 128 | 4 | 0.146 | 0.196 | 0.119 | 0.177 | 0.022 | 0.055 | 0.140 | 0.176 |

| 512 | 64 | 8 | 0.138 | 0.214 | ||||||

| 1024 | 256 | 4 | 0.328 | 0.406 | 0.127 | 0.197 | 0.018 | 0.079 | 0.152 | 0.206 |

| 1024 | 128 | 8 | 0.152 | 0.218 | ||||||

| 2048 | 512 | 4 | 0.646 | 0.710 | 0.174 | 0.266 | 0.052 | 0.116 | 0.374 | 0.470 |

| 2048 | 256 | 8 | 0.312 | 0.388 | ||||||

| 4096 | 1024 | 4 | 0.854 | 0.888 | 0.232 | 0.466 | 0.064 | 0.162 | 0.736 | 0.792 |

| 4096 | 512 | 8 | 0.716 | 0.742 | ||||||

| 256 | 64 | 4 | 0.118 | 0.174 | 0.118 | 0.168 | 0.146 | 0.222 | 0.374 | 0.450 | 0.356 | 0.432 |

| 256 | 32 | 8 | 0.184 | 0.270 | 0.167 | 0.241 | 0.183 | 0.261 | 0.359 | 0.452 | 0.335 | 0.464 |

| 512 | 128 | 4 | 0.198 | 0.272 | 0.216 | 0.296 | 0.350 | 0.412 | 0.592 | 0.638 | 0.622 | 0.662 |

| 512 | 64 | 8 | 0.092 | 0.146 | 0.134 | 0.188 | 0.104 | 0.188 | 0.372 | 0.490 | 0.400 | 0.518 |

| 1024 | 256 | 4 | 0.430 | 0.504 | 0.402 | 0.504 | 0.648 | 0.716 | 0.792 | 0.808 | 0.776 | 0.808 |

| 1024 | 128 | 8 | 0.160 | 0.226 | 0.136 | 0.200 | 0.230 | 0.290 | 0.506 | 0.608 | 0.500 | 0.586 |

| 2048 | 512 | 4 | 0.746 | 0.790 | 0.804 | 0.844 | 0.868 | 0.880 | 0.876 | 0.892 | 0.912 | 0.932 |

| 2048 | 256 | 8 | 0.434 | 0.492 | 0.454 | 0.510 | 0.534 | 0.578 | 0.670 | 0.754 | 0.678 | 0.744 |

| 4096 | 1024 | 4 | 0.932 | 0.940 | 0.930 | 0.940 | 0.943 | 0.953 | 0.982 | 0.985 | 0.992 | 0.992 |

| 4096 | 512 | 8 | 0.914 | 0.922 | 0.910 | 0.918 | 0.910 | 0.925 | 0.967 | 0.978 | 0.895 | 0.923 |

Remark 5.1.

It is well known that fitting tvFAR or tvFARIMA to tvAR or tvARMA models yields to confounded estimates of the AR/MA coefficients and the long-memory parameter. As a consequence the approximation of the nominal level becomes less accurate if the AR polynomial has roots close to the unit disc. For example, motivated by a comment of a reviewer, we have conducted a further simulation study investigating a tvAR(1) model. These results are not depicted for the sake of brevity but they clearly show that the approximation of the nominal level of the new test is not accurate if the AR coefficients vary in the interval . In this case the level is overestimated, and the test (4.19) decides too often for a long-memory process.

5.2 Simulation of prediction error

In this subsection we investigate the question what one loses by fitting a short-range dependent non-stationary model to data that is truly non-stationary and long-range dependent. For this purpose we simulate data from the tvFARIMA()-process in (5.10) with long-memory functions and in (5.12) and (5.17), respectively. We separately fit a tvARMA(1,1) model and a tvFARIMA(1,d,1) model to the data and use the state space framework in palolefer2013 in order to predict future values and then compare the prediction errors of these two fitted models. To be more precise we consider the sample size with block length (resulting in blocks) and use the local Whittle estimator from Section 4 to estimate on each block the locally varying AR and MA coefficients for the tvARMA(1,1) model and the AR, MA and long-memory parameters for the tvFARIMA() model. With these time-varying coefficients we use the Kalman filter equations in palolefer2013 and calculate and -step predictors with each of these two models. The prediction error is calculated by sum of squared residuals

In Table 9 we display the median and median absolute deviation of the prediction errors obtained in simulation runs. We observe that the predictions, which take the long memory property into account are substantially more accurate.

| model (5.10) with | model (5.10) with | |||||||

| tvARMA(1,1) | tvFARIMA(1,d,1) | tvARMA(1,1) | tvFARIMA(1,d,1) | |||||

| -step prediction | med | dev | med | dev | med | dev | med | dev |

| 5 | 19.1 | 52.4 | 4.8 | 3.6 | 12.3 | 42.3 | 4.5 | 3.3 |

| 10 | 25.2 | 56.5 | 10.7 | 5.0 | 18.1 | 44.0 | 10.1 | 4.7 |

| 25 | 43.2 | 54.6 | 25.4 | 7.8 | 36.5 | 40.1 | 26.3 | 10.8 |

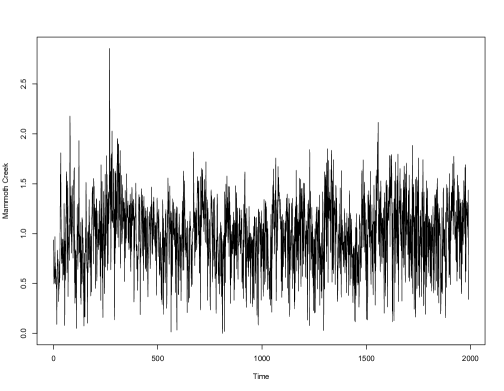

5.3 Data examples

Testing: As an illustration we apply the new test to two different datasets, where in both examples the mean function has been estimated as described in Section 4. As pointed out in the previous section the quality of predictions can be improved, if long range dependence

is present in non stationary data and considered in the predictions. For this reason the test proposed in this paper can be useful to obtain more accurate forcasts.

The first data set contains annual pinus longaeva tree ring width measurements at Mammoth Creek, Utah, from 0 A.D. to 1989 A.D. while the second data set contains 2048 squared log-returns of the IBM stock between July th and August th which was already discussed in the introduction. Both time series are depicted in Figure 5, and in the case of the tree ring data our test statistic equals 17.8 for and yields a p-value . This implies that the null hypothesis of a non-stationary short-memory model has to be rejected for this dataset, which coincides with the results of the tests in baekpipi and Yau2012. Their test statistics have the values 3.49 and 9.37 and p-values of and corresponding to the local Whittle and likelihood ratio approach, respectively. The CUSUM procedure of horvarth2006 yields a value of for the test statistic and does not reject the null hypothesis at even nominal level. This result

is possibly due to the low power of this test as remarked in Section 5.1.

In the situation of the squared log-returns of the IBM stock, the assumption of Gaussianity is too restrictive and we therefore apply the more general test described in Remark 4.8. The values of the test statistic are and for and , respectively, yielding that the p-value is smaller than for both choices of the segmentation. This means that the assumption of no long-range dependence is clearly rejected. If we apply the likelihood ratio test of Yau2012 to this dataset, we obtain a value for the statistic of which is then compared with the quantiles of the standard normal distribution. This yields also to a rejection of the null hypothesis. On the other hand, the CUSUM procedure of horvarth2006 only rejects the null hypothesis of no long-range dependence at a but not at a level. This observation is, however, not surprising given the low power of this test in the finite sample situations presented in the previous section. The test of baekpipi rejects the null hypothesis with a p-value , yielding the same result as our approach and the one of Yau2012.

Prediction: The result of the test (4.19) has important consequences for the subsequent data analysis as it advices the statistician to use short memory or long memory (non-stationary) models. In the final part of this section we demonstrate how the information of the test can be employed to obtain superior forecasting results in the two datasets analyzed in the previous paragraph. For this purpose, we divide both datasets into two parts. One part contains the first observations of the corresponding dataset while the second part contains the remaining data points. The new testing procedure (4.19) proposed in this paper is applied to the first part of the data, and - depending on the result of the test - forecasts are performed using either a tvFARIMA(1,d,1) or a ARMA(1,1) with the window of size in the localized Whittle estimator [see also Section 5.2]. In order to compare the forecasting performance of the short- with the long-memory model, we define the prediction error on the second part of each dataset by

and denote with and the prediction error for the short- and long-memory approach respectively. The expression

then serves as a measure for the comparison. It is smaller than one if the long-range dependence approach yields superior predictions, while it is larger than one in the other case. As in the previous paragraph (where we applied the test to the total sample), an application of the test (4.19) to the first observations of the Mammoth Creek and the IBM dataset yields -values much smaller than one percent in both cases. Consequently one would perform data analysis on the basis of a non-stationary long range dependent model. The advantages of this approach are clearly visible in Table 10 where we depict the ratio of the prediction error from a short and long range dependent model. We observe that the long-range dependence approach, in fact, yields substantially smaller prediction errors. In all cases the prediction error from the long-range dependent model is less than one third of the corresponding error from the short-memory model (for both datasets and all considered values of ). This demonstrates that the difference in forecasting performance is huge and highlights the importance of powerful tests to discriminate between long- and short-range dependence.

| dataset | |||

|---|---|---|---|

| Mammoth Creek Data | |||

| IBM Data | |||

6 Conclusions

In this paper we have developed a test for weak against strong (long-range) dependence for non-stationarity

time series. Our approach is based on an average of unconstrained Whittle-likelihood estimates

of the (nonnegative) local long-range dependence

parameter from a sequence of approximating time varying FARIMA models [see equation (4.12) for its definition]. It is demonstrated that

a standardized version of this average is asymptotically normal distributed, which

provides a very simple asymptotic level and consistent

test for discriminating between short and long range dependence of a non-stationary time series.

As an alternative to the statistic in (4.12) one could form an average of constrained Whittle-likelihood estimates, say . Constrained

parameter estimation has found considerable attention

in the literature [see for example chernoff1954 or andrews1999 among many others], but - to our best knowledge - it has not been considered so far

in locally stationary processes. The “classical” results indicate that for a fixed

value the asymptotic distribution of

is given by a function of a multivariate

normal distribution (in the simplest case a half normal type distribution). However, we expect that - due to averaging - the (standardized) statistic

is still asymptotically normal distributed. An interesting direction for future

research is the development of an asymptotic theory for constrained estimators in locally stationary (long memory) processes

and to use it for a rigorous investigation of the asymptotic properties of the statistic . Moreover, the results of Section

3 for the nonparametric regression model with independent errors indicate some advantages of unconstrained

over unconstrained averages, and it will be of interest to investigate if the superiority of over

can also be observed for the testing problem considered in this paper.

It is also notable that this paper has its focus on discriminating between short and standard long-range dependence,

which corresponds to a pole of the local spectral density at frequency . However, it was pointed out by several authors

[see for example arteche2000; hidalgo2004; reisen2006 among others] that - due to strong cyclic components -

strong dependency can also occur as a pole in the spectral density at any other frequency (reflecting strong seasonal long range dependence).

In this case the analogue of the model (2.6) is given by

| (6.1) |

where denotes the unknown pole [see hidalgo2004], and a further interesting direction of future research

is the construction of tests for the hypothesis (2.12) in the more general model (6.1).

We finally note that several authors have analyzed financial data under

linearity assumptions as made in equation (2.1) [see mikosch2004, motivation1 or motivation2

among others]. On the other hand it is also argued in the literature that this assumption

might not be reasonable in some cases. Long range dependent processes have

mainly been investigated in models with linear representations. A nonlinear (nonparametric) extension does not seem to be obvious

as indicated by the results of grusur2014, who proposed a linear representation with random coefficients.

Therefore, an interesting problem for future research is to investigate if the methodology

suggested in this paper is also valid for processes with nonlinear representations.

Acknowledgements. This work has been supported in part by the Collaborative Research Center “Statistical modeling of nonlinear dynamic processes” (SFB 823, Teilprojekt A1, C1) of the German Research Foundation (DFG). We would also like to thank Tobias Kley and Kevin Kokot for computational assistance, Lutz Dümbgen for some helpful discussions about Section 3 and Wilfredo Palma for some constructive discussion on the subject and for making the R-Code in palolefer2013 available to us.

7 Appendix: Proofs

7.1 Preliminary results

We begin stating two results, which will be the main tools in the asymptotic analysis of the proposed estimators and the test statistic. For this purpose, we let denote a function which (might) depend on the the sample size and define

where is the analogue of the local periodogram (4.4) where the estimator has been replaced by the “true” mean function .

Theorem 7.1.

-

a)

Let Assumption 2.1 be fulfilled and assume that is symmetric in , twice continuously differentiable with uniformly bounded partial derivatives such that for all , ,

(7.1) (7.2) (7.3) where are constants and is a given function. Then we have

(7.4) (7.5) where

-

b)

Suppose the assumptions of part a) hold with , and additionally

Then we have

Proof: In order to prove part a) Theorem 7.1 we define , , and obtain

where

Note that and compromise the error arising in the approximation of by and by , respectively. In order to establish the claim (7.4), we prove the following statements:

| (7.6) | |||||

| (7.7) | |||||

| (7.8) |

Proof of (7.6): Due to the independence of the random variables , we only need to consider terms fulfilling (this means because of ) which in turn implies . Therefore

where

Using (2.4), (7.1) and Lemma 8.2 in the online supplement, we obtain

where we used the fact that terms corresponding to or are of smaller or the same order (we will use this property frequently from now on without further mentioning it). We set and obtain from Lemma 8.1a) in the online supplement that

By proceeding analogously we obtain that which proves the assertion in (7.6).

Proof of (7.7): Without loss of generality we only consider the first summand

in (the second term is treated exactly in the same way). A Taylor expansion and similar arguments as in the proof of (7.6) yield

where

and . Using (2.4), (2.8), (7.1), Lemma 8.2 it follows

where we used Lemma 8.1(c) in the online supplement for the last step.

Finally, (2.4), (2.8), (7.1), Lemma 8.2 in the online supplement and the same arguments as above, show that the term is of order .

Proof of (7.8): By employing (2.3) and the same arguments as above it can be shown that is of order .

In the next step we prove the asymptotic representation for the variance in (7.5). We obtain

where we used assumption (2.3) and similar arguments as given in the proof of (7.4). Because of the Gaussianity of the innovations we obtain

This implies that the calculation of the (dominating part of the) variance splits into two sums, say and . In the following discussion we will show that both terms converge to the same limit, that is

For the sake of brevity we restrict ourselves to the case . Because of the independence of the innovations , we obtain that the conditions and must hold, which, because of , directly implies and . Thus, the term can be written as

Since , we get from the condition that, if are fixed, there are at most two possible values for such that the corresponding term does not vanish. It follows from Lemma 8.3 (i)–(iii) in the online supplement that there appears an error of order if we drop the condition and assume that the variable runs from to . Therefore, up to an error of order , the term is equal to

where

We show

| (7.9) | |||||

which then concludes the proof of (7.5). For this purpose we begin with an investigation of the term for which the terms in the sum vanish if . Moreover, the following facts are correct:

-

I.

The variable runs from to since and .

-

II.

We can drop the condition by making an error of order [this follows from Lemma 8.3(iv) in the online supplement].

-

III.

There appears an error of order if we omit the sum with [we prove this in Lemma 8.3(v) in the online supplement].

-

IV.

We can afterwards omit the condition since it is and [note that, because of III., we assume from now on].

-

V.

We can then drop the condition since and .

Thus, using the representation of in (2.5), the term can be written as (up to an error of order )

where

With Parseval’s identity, we get

while Lemma 8.2 in the online supplement yields (up to a constant) the inequalities

which proves (7.9). We now consider the term

where

Here corresponds to the sum over all and vanishes by Parseval’s identity. stands for the resulting error term which is of order because of Lemma 8.3 (vi) in the online supplement.

Part b) follows with par a) if we show

| (7.10) |

For a proof of this statement where we proceed (with a slight modification) analogously to the proof of Theorem 6.1 c) in prevet2012. Note that these authors work with functions such that

| (7.11) |

while for the integrated case. The authors then derive the exact same order as in (7.10) with the only difference that and . In our situation, assumption (7.1) and Lemma 8.2 in the online supplement imply

| (7.12) |

and we can therefore proceed completely analogously to the proof of Theorem 6.1 c) in prevet2012 but using (7.12) instead of (7.11). The details are omitted for the sake of brevity.

For the formulation of the next result we define the set

and state the following result.

Theorem 7.2.

Suppose Assumption 2.1 and 4.2 are fulfilled, and is the constant of Assumption 4.2. Let denote a class of functions consisting of elements, which are twice continuously differentiable with uniformly bounded partial derivates with respect to and satisfy (7.1)–(7.3) with , where the constant does not depend on , . Furthermore, we assume that for all the condition holds, where are fixed and denotes a sequence satisfying . Then

Proof: We define as the set of functions which we obtain by multiplying all elements with , that is for some and , and consider

It follows from Theorem 2.1 in unifeconometrica that the assertion of Theorem 7.2 is a consequence of the statements:

-

(i)

For every we have

(7.13) -

(ii)

For every we have

(7.14)

In order to prove part (i) we use the same arguments as given in the proof of (7.4) and (7.5) and obtain

which yields (7.13) observing the growth conditions on and . For the proof of part (ii) we note that it follows by similar arguments as given in the proof of Theorem 6.1 d) of prevet2012 that there exists a positive constant such that the inequlality

holds for all even and all , where

for a constant which is sufficiently large such that

By an application of Markov’s inequality and a straightforward but cumbersome calculation [see the proof of Lemma 2.3 in dahlhaus1988 for more details] this yields

for all . The statement (7.14) then follows with the extension of the classical chaining argument as described in dahlhaus1988 if we show that the corresponding covering integral of with respect to the semi-metric is finite. More precisely, the covering number of with respect to is equal to one for and bounded by for some constant for [see Chapter VII.2. of pollard for a definition of covering numbers]. This implies that the covering integral is up to a constant bounded by . The assertion follows by the assumptions on and .

7.2 Proof of Theorem 4.3

Introducing the notation

we obtain with the same arguments as given in the proof of Theorem 3.6 in dahlhaus1997

for some constant and is defined by . By proceeding as in the proof of Theorem 7.2 one verifies

and (4.9) yields

| (7.15) |

and analogously we get

| (7.16) |

For each let denote the Whittle-estimator defined in (4.2). Then Theorem 7.2 and similar arguments as in the proof of Theorem 3.2 in dahlhaus1997 yield

| (7.17) |

We will now derive a refinement of this statement. By an application of the mean value theorem, there exist vectors , , satisfying such that

and the first term on the left-hand side vanishes due to (7.17). This yields

where denotes the difference between and , which is of order by (7.16). It follows from

and Theorem 7.2 that so it remains to show

7.3 Proof of Theorem 4.5 and Theorem 4.6

We will show in Section 7.3.1 that under the null hypothesis the estimate

| (7.18) |

is valid, while Theorem 4.3 and (4.16) imply

| (7.19) |

under the alternative . As in the proof of Theorem 4.3 there exist vectors , , satisfying such that

holds because of Assumption 4.1 (ii) and (7.18) (under ) or (7.19) (under ). By rearranging and summing over every block, it follows that

| (7.20) |

where

is defined in (4.5) and the terms are given by

We obtain for the first summand in (7.20)

and with the notation , it is easy to see that Assumption 4.1 (i)–(iv) imply the conditions of Theorem 7.1 b) with . Moreover, observing the definition of and in Theorem 7.1 and 4.5, (4.18) yields . Consequently, under the assumptions of Theorem 4.5 it follows (observing (4) and the growth conditions on , )

Since is the first element of the vector , Theorem 4.5 is a consequence of the fact [this can be proved by a second order Taylor expansion] if we are able to show that

Analogously, Theorem 4.6 follows from (7.4) and (7.5) if the estimates

can be established. It can be shown analogously to the proof of Theorem 3.6 in dahlhaus1997, that, under assumptions (4.13) – (4.14), both terms and are of order , while, under assumption (4.16), the order is [see the proof of (7.23) and (7.15), respectively, for more details]. Therefore it only remains to consider the quantities and . For this purpose note that

| (7.21) | |||||

| (7.22) | |||||

where we used the notation . For the term we obtain with the well-known inequality

By the mean value theorem there exist vectors such that

where for every . Therefore, we obtain

where, in the last inequality, we have used the fact that the second and third term in (7.22) are bounded by a constant [this follows directly from Assumption 4.1]. Before we investigate the order of this expression, we derive a similar bound for the term . Observing (7.21) we obtain

If we show

it follows with Assumption 4.1 (iv) in combination with (7.18) (under ) and (7.19) (under ) that the terms and are of order (under ) and (under ). These two claims, however are a direct consequence of Theorem 7.2 and (4).

7.3.1 Proof of (7.18)

With the same arguments as in the proof of Theorem 3.6 in dahlhaus1997 we obtain

where

and denotes a positive constant. By proceeding as in the proof of Theorem 7.2 one obtains

which implies (observing the assumptions (4.13) and (4.14))

| (7.23) |

under . Analogously we obtain

| (7.24) | |||||

under the null hypothesis. By using (7.23) and (7.24) instead of (7.15) and (7.16), assertion (7.18) follows by the same arguments as given in the proof of Theorem 4.3.

7.4 Proof of Theorem 4.10

A second order Taylor expansion yields

| (7.25) |

For the cumulants of order

are bounded by

where we used the independence of the innovations, (2.3) and (2.4) and the last inequality follows by replacing the sums by its corresponding approximating integrals and holds for some positive constant (which is independent of and may vary in the following arguments). This yields that estimates its true counterpart at a pointwise rate of and we now continue by showing stochastic equicontinuity. The expansion (7.25) and the bound for the -th cumulant () of yield for all and every , from which we get

[see the proof of Lemma 2.3 in dahlhaus1988 for more details]. By considering the order of the bias (7.25) this yields

as in the proof of Theorem 7.2. Consequently (4.13) [under the conditions of part a)] and (4.16) [under the conditions of part b)] follow. So it remains to show (4.14) in the case . For this purpose we define

and from (7.25) we obtain . A simple calculation reveals (where the estimate is independent of ) and with the Gaussianity of the innovations we get for . This yields, as above,

for every , and completes the proof of Theorem 4.10.

8 Online supplement: Auxiliary results

Finally, we state some lemmas which were employed in the above proofs.

Lemma 8.1.

Suppose it is . Then there exists a constant such that the following holds:

-

a)

If and , then

(7.1) -

b)

If and , then it follows for

(7.2) -

c)

If and , then

Proof: The proof can be found in senpreudet2013.

Lemma 8.2.

For every , let be a symmetric and twice continuously differentiable function such that for some as (where the constant in the term is independent of ). Then, for , we have

uniformly in .

Proof: The assertion follows from Lemma 4 and Lemma 5 in foxtaqqu1986.

Lemma 8.3.

If Assumption 2.1 holds, then

-

(i)

-

(ii)

-

(iii)

-

(iv)

-

(v)

-

(vi)

Proof: Without loss of generality we restrict ourselves to a proof of part (i) and (v) and note that all other claims are proven by using the same arguments.

Proof of (i): We use (2.4), (7.1) and Lemma 8.2 to bound the term in (i) (up to a constant) through

If the variables and are fixed, it follows with the constraint that there are at most two possible values for such that the resulting term is non vanishing. We now discuss for which combinations of and the above expression is maximized and then restrict ourselves to the resulting pair .

If and are given, the variables can only be chosen such that and are fulfilled. Therefore, the possible values of the fractions are the same for any combination of and . Consequently, in order to maximize the term above we need to maximize , which is achieved by the choice [since then can be jointly taken as small as possible due to the constraints and ]. Hence we can bound that above expression (up to a constant) by

By setting and this term can be written as

Proof of (v): By setting

we can write the term in (v) as

and by integrating over this is the same as

By (7.1) and Lemma 8.2 this sum can be bounded by

As in the proof of (i) we can argue that there are at most two possible values for if and are chosen and that the expression is maximized for . Therefore we can bound the above expression up to a constant through

By setting the claim follows with (7.2).