A family of density expansions for Lévy-type processes

Abstract

We consider a defaultable asset whose risk-neutral pricing dynamics are described by an exponential Lévy-type martingale subject to default. This class of models allows for local volatility, local default intensity, and a locally dependent Lévy measure. Generalizing and extending the novel adjoint expansion technique of Pagliarani, Pascucci, and Riga (2013), we derive a family of asymptotic expansions for the transition density of the underlying as well as for European-style option prices and defaultable bond prices. For the density expansion, we also provide error bounds for the truncated asymptotic series. Our method is numerically efficient; approximate transition densities and European option prices are computed via Fourier transforms; approximate bond prices are computed as finite series. Additionally, as in Pagliarani et al. (2013), for models with Gaussian-type jumps, approximate option prices can be computed in closed form. Sample Mathematica code is provided.

To the memory of our dear friend and esteemed colleague Peter Laurence.

Keywords: Local volatility; Lévy-type process; Asymptotic expansion; Pseudo-differential calculus; Defaultable asset

1 Introduction and literature review

A local volatility model is a model in which the volatility of an asset is a function of time and the present level of . That is, . Among local volatility models, perhaps the most well-known is the constant elasticity of variance (CEV) model of Cox (1975). One advantage of local volatility models is that transition densities of the underlying – as well as European option prices – are often available in closed-form as infinite series of special functions (see Linetsky (2007) and references therein). Another advantage of local volatility models is that, for models whose transition density is not available in closed form, accurate density and option price approximations are readily available (see, Pagliarani and Pascucci (2011), for example). Finally, Dupire (1994) shows that one can always find a local volatility function that fits the market’s implied volatility surface exactly. Thus, local volatility models are quite flexible.

Despite the above advantages, local volatility models do suffer some shortcomings. Most notably, local volatility models do not allow for the underlying to experience jumps, the need for which is well-documented in literature (see Eraker (2004) and references therein). Recently, there has been much interest in combining local volatility models and models with jumps. Andersen and Andreasen (2000), for example, discuss extensions of the implied diffusion approach of Dupire (1994) to asset processes with Poisson jumps (i.e., jumps with finite activity). And Benhamou, Gobet, and Miri (2009) derive analytically tractable option pricing approximations for models that include local volatility and a Poisson jump process. Their approach relies on asymptotic expansions around small diffusion and small jump frequency/size limits. More recently, Pagliarani, Pascucci, and Riga (2013) consider general local volatility models with independent Lévy jumps (possibly infinite activity). Unlike, Benhamou et al. (2009), Pagliarani et al. (2013) make no small jump intensity/size assumption. Rather the authors construct an approximated solution by expanding the local volatility function as a power series. While all of the methods described in this paragraph allow for local volatility and independent jumps, none of these methods allow for state-dependent jumps.

Stochastic jump-intensity was recently identified as an important feature of equity models (see Christoffersen, Jacobs, and Ornthanalai (2009)). A locally dependent Lévy measure allows for this possibility. Recently, two different approaches have been taken to modeling assets with locally-dependent jump measures. Mendoza-Arriaga, Carr, and Linetsky (2010) time-change a local volatility model with a Lévy subordinator. In addition to admitting exact option-pricing formulas, the subordination technique results in a locally-dependent Lévy measure. Jacquier and Lorig (2013) considers another class of models that allow for state-dependent jumps. The author builds a Lévy-type processes with local volatility, local default intensity, and a local Lévy measure by considering state-dependent perturbations around a constant coefficient Lévy process. In addition to pricing formula, the author provides an exact expansion for the induced implied volatility surface.

In this paper, we consider scalar Lévy-type processes with regular coefficients, which naturally include all the models mentioned above. Generalizing and extending the methods of Pagliarani et al. (2013), we derive a family of asymptotic expansions for the transition densities of these processes, as well as for European-style derivative prices and defaultable bond prices. The key contributions of this manuscript are as follows: {itemize*}

We allow for a locally-dependent Lévy measure and local default intensity, whereas Pagliarani et al. (2013) consider a locally independent Lévy measure and do not allow for the possibility of default. A state-dependent Lévy measure is an important feature because it allows for incorporating local dependence into infinite activity Lévy models that have no diffusion component, such as Variance Gamma (Madan, Carr, and Chang (1998)) and CGMY/Kobol (Boyarchenko and Levendorskii (2002); Carr, Geman, Madan, and Yor (2002)).

Unlike Benhamou et al. (2009), we make no small diffusion or small jump size/intensity assumption. Our formulae are valid for any Lévy type process with smooth and bounded coefficients, independent of the relative size of the coefficients.

Whereas Pagliarani et al. (2013) expand the local volatility and drift functions as a Taylor series about an arbitrary point, i.e. , in order to achieve their approximation result, we expand the local volatility, drift, killing rate and Lévy measure in an arbitrary basis, i.e. . This is advantageous because the Taylor series typically converges only locally, whereas other choices of the basis functions may provide global convergence in suitable functional spaces.

Using techniques from pseudo-differential calculus, we provide explicit formulae for the Fourier transform of every term in the transition density and option-pricing expansions. In the case of state dependent Gaussian jumps the respective inverse Fourier transforms can be explicitly computed, thus providing closed form approximations for densities and prices. In the general case, the density and pricing approximations can be computed quickly and easily as inverse Fourier transforms. Additionally, when considering defaultable bonds, approximate prices are computed as a finite sum; no numerical integration is required even in the general case.

For models with Gaussian-type jumps, we provide pointwise error estimates for transition densities. Thus, we extend the previous results of Pagliarani et al. (2013) where only the purely diffusive case is considered. Additionally, our error estimates allow for jumps with locally dependent mean, variance and intensity. Thus, for models with Gaussian-type jumps, our results also extend the results of Benhamou et al. (2009), where only the case of a constant Lévy measure is considered.

The rest of this paper proceeds as follows. In Section, 2 we introduce a general class of exponential Lévy-type models with locally-dependent volatility, default intensity and Lévy measure. We also describe our modeling assumptions. Next, in Section 3, we introduce the European option-pricing problem and derive a partial integro-differential equation (PIDE) for the price of an option. In Section 4 we derive a formal asymptotic expansion (in fact, a family of asymptotic expansions) for the function that solves the option pricing PIDE (Theorem 1). Next, in Section 5, we provide rigorous error estimates for our asymptotic expansion for models with Gaussian-type jumps (Theorem 2). Lastly, in Section 6, we provide numerical examples that illustrate the effectiveness and versatility of our methods. Technical proofs are provided in the Appendix. Some concluding remarks are given in Section 7.

We mention specifically that the arguments needed to provide rigorous error estimates for our asymptotic expansions are quite extensive. As such, in this manuscript, we provide only an outline of the proof of Theorem 2. The full proof of Theorem 2, as well as further numerical examples, can be found in a companion paper Lorig, Pagliarani, and Pascucci (2013).

2 General Lévy-type exponential martingales

For simplicity, we assume a frictionless market, no arbitrage, zero interest rates and no dividends. Our results can easily be extended to include locally dependent interest rates and dividends. We take, as given, an equivalent martingale measure , chosen by the market on a complete filtered probability space satisfying the usual hypothesis of completeness and right continuity. The filtration represents the history of the market. All stochastic processes defined below live on this probability space and all expectations are taken with respect to . We consider a defaultable asset whose risk-neutral dynamics are given by

| (1) |

Here, is a Lévy-type process with local drift function , local volatility function and state-dependent Lévy measure . We shall denote by the filtration generated by . The random variable has an exponential distribution and is independent of . Note that , which represents the default time of , is constructed here trough the so-called canonical construction (see Bielecki and Rutkowski (2001)), and is the first arrival time of a doubly stochastic Poisson process with local intensity function . This way of modeling default is also considered in a local volatility setting in Carr and Linetsky (2006); Linetsky (2006), and for exponential Lévy models in Capponi et al. (2013).

We assume that the coefficients are measurable in and suitably smooth in to ensure the existence of a solution to (1) (see Oksendal and Sulem (2005), Theorem 1.19). We also assume the following boundedness condition which is rather standard in the financial applications: there exists a Lévy measure

| (2) |

such that

| (3) |

Since is not -measurable we introduce the filtration in order to keep track of the event . The filtration of a market observer, then, is . In the absence of arbitrage, must be an -martingale. Thus, the drift is fixed by , and in order to satisfy the martingale condition111 We provide a derivation of the martingale condition in Section 3 Remark 1 below.

| (4) |

We remark that the existence of the density of is not strictly necessary in our analysis. Indeed, since our formulae are carried out in Fourier space, we provide approximations of the characteristic function of and all of our computations are still formally correct even when dealing with distributions that are not absolutely continuous with respect to the Lebesgue measure.

3 Option pricing

We consider a European derivative expiring at time with payoff and we denote by its no-arbitrage price. For convenience, we introduce

| (5) |

Proposition 1.

The price is given by

| (6) |

The proof can be found in Section 2.2 of Linetsky (2006). Because our notation differs from that of Linetsky (2006), and because a short proof is possible by using the results of Jeanblanc, Yor, and Chesney (2009), for the reader’s convenience, we provide a derivation of Proposition 1 here.

Proof.

Using risk-neutral pricing, the value of the derivative at time is given by the conditional expectation of the option payoff

| (7) | ||||

| (8) | ||||

| (9) | ||||

| (10) | ||||

| (11) |

where we have used Corollary 7.3.4.2 from Jeanblanc, Yor, and Chesney (2009) to write

| (12) |

∎

Remark 1.

From (6) one sees that, in order to compute the price of an option, we must evaluate functions of the form222Note: we can accommodate stochastic interest rates and dividends of the form and by simply making the change: and .

| (14) |

By a direct application of the Feynman-Kac representation theorem, see for instance (Pascucci, 2011, Theorem 14.50), the classical solution of the following Cauchy problem,

| (15) |

when it exists, is equal to the function in (14), where

| (16) | ||||

| (17) |

is the characteristic operator of the SDE (1). In order to shorten the notation, in the sequel we will suppress the explicit dependence on in by referring to it just as .

Sufficient conditions for the existence and uniqueness of solutions of second order elliptic integro-differential equations are given in Theorem II.3.1 of Garroni and Menaldi (1992). We denote by the fundamental solution of the operator , which is defined as the solution of with . Note that represents also the transition density of 333Here with we denote the process .

| (18) |

Note also that is not a probability density since (due to the possibility that ) we have

| (19) |

Given the existence of the fundamental solution of , we have that for any that is integrable with respect to the density , the Cauchy problem (15) has a classical solution that can be represented as

| (20) |

Remark 2.

If is the generator of a scalar Markov process and contains , the Schwartz space of rapidly decaying functions on , then must have the following form:

| (21) |

where , , is a Lévy measure for every and (see Hoh (1998), Proposition 2.10). If one enforces on the drift and integrability conditions (3) and (4), which are needed to ensure that is a martingale, and allow setting , then the operators (17) and (21) coincide (in the time-homogeneous case). Thus, the class of models we consider in this paper encompasses all non-negative scalar Markov martingales that satisfy the regularity and boundedness conditions of Section 2.

Remark 3.

In what follows we shall systematically make use of the language of pseudo-differential calculus. More precisely, let us denote by

| (22) |

the so-called oscillating exponential function. Then can be characterized by its action on oscillating exponential functions. Indeed, we have

| (23) |

where

| (24) | ||||

| (25) |

is called the symbol of . Noting that

| (26) |

for any analytic function , we have

| (27) |

Then can be represented as

| (28) |

| (29) | ||||

| (30) |

If coefficients are independent of , then we have the usual characterization of as a multiplication by operator in the Fourier space:

where and denote the (direct) Fourier and inverse Fourier transform operators respectively:

| (31) |

Moreover, if the coefficients are independent of both and , then is the generator of a Lévy process and is the characteristic exponent of :

| (32) |

4 Density and option price expansions (a formal description)

Our goal is to construct an approximate solution of Cauchy problem (15). We assume that the symbol of admits an expansion of the form

| (33) |

where is of the form

| (34) | ||||

| (35) |

and is some expansion basis with being an analytic function for each , and (see Examples 1, 2 and 3 below). Note that is the symbol of an operator

| (36) |

so that

| (37) |

Thus, formally the generator can be written as follows

| (38) |

Note that is the generator of a time-dependent Lévy-type process . In the time-independent case is a Lévy process and is its characteristic exponent.

Example 1 (Taylor series expansion).

Pagliarani, Pascucci, and Riga (2013) approximate the drift and diffusion coefficients of as a power series about an arbitrary point . In our more general setting, this corresponds to setting and expanding the diffusion and killing coefficients and , as well as the Lévy measure as follows:

| (39) |

In this case, (33) and (38) become (respectively)

| (40) |

where, for all , the symbol is given by (35) with coefficients given by (39). The choice of is somewhat arbitrary. However, a convenient choice that seems to work well in most applications is to choose near , the current level of . Hereafter, to simplify notation, when discussing implementation of the Taylor-series expansion, we suppress the -dependence: , and .

Example 2 (Two-point Taylor series expansion).

Suppose is an analytic function with domain and . Then the two-point Taylor series of is given by

| (41) |

where

| (42) |

For the derivation of this result we refer the reader to Estes and Lancaster (1972); Lopez and Temme (2002). Note truncating the two-point Taylor series expansion (41) at results in an expansion which of which is of order ).

The advantage of using a two-point Taylor series is that, by considering the first derivatives of a function at two points and , one can achieve a more accurate approximation of over a wider range of values than if one were to approximate using derivatives at a single point (i.e., the usual Taylor series approximation).

If we associate expansion (41) with an expansion of the form then , which is affine in . Thus, the terms in the two-point Taylor series expansion would not be a suitable basis in (33) since . However, one can always introduce a constant and define a function

| so that | (43) |

Then, one can express as

| (44) |

where the are as given in (42) with . If we associate expansion (44) with an expansion of the form , then we see that and one can choose . Thus, as written in (44), the terms of the two-point Taylor series can be used as a suitable basis in (33).

Consider the following case: suppose , and are of the form

| (45) |

so that with

| (46) | ||||

| (47) |

It is certainly plausible that the symbol of would have such a form since, from a modeling perspective, it makes sense that default intensity, volatility and jump-intensity would be proportional. Indeed, the Jump-to-default CEV model (JDCEV) of Carr and Linetsky (2006); Carr and Madan (2010) has a similar restriction on the form of the drift, volatility and killing coefficients.

Now, under the dynamics of (45), observe that and can be written as in (33) and (38) respectively with and

| (48) |

As above (capital “C”) are given by (42) with and

| (49) |

As in example 1, the choice of , and is somewhat arbitrary. But, a choice that seems to work well is to set and where is a constant and . It is also a good idea to check that, for a given choice of and , the two-point Taylor series expansion provides a good approximation of in the region of interest.

Note we assumed the form (45) only for sake of simplicity. Indeed, the general case can be accommodated by suitably extending expansion (33) to the more general form

| (50) |

where for are related to the diffusion, jump and default symbols respectively. For brevity, however, we omit the details of the general case.

Example 3 (Non-local approximation in weighted -spaces).

Suppose is a fixed orthonormal basis in some (possibly weighted) space and that for all . Then we can represent in the form (33) where now the are given by

| (51) |

A typical example would be to choose Hermite polynomials centered at as basis functions, which (as normalized below) are orthonormal under a Gaussian weighting

| (52) |

In this case, we have

| (53) |

Once again, the choice of is arbitrary. But, it is logical to choose near , the present level of the underlying . Note that, in the case of an orthonormal basis, differentiability of the coefficients is not required. This is a significant advantage over the Taylor and two-point Taylor basis functions considered in Examples 1 and 2, which do require differentiability of the coefficients.

Now, returning to Cauchy problem (15), we suppose that can be written as follows

| (54) |

Following Pagliarani et al. (2013), we insert expansions (38) and (54) into Cauchy problem (15) and find

| (55) | ||||||

| (56) |

We are now in a position to find the explicit expression for , the Fourier transform of in (55)-(56).

Theorem 1.

Proof.

See Appendix A. ∎

Remark 4.

To compute survival probabilities over the interval , one assumes a payoff function . Note that the Fourier transform of a constant is simply a Dirac delta function: . Thus, when computing survival probabilities, (possibly defaultable) bond prices and credit spreads, no numerical integration is required. Rather, one simply uses the following identity

| (59) |

to compute inverse Fourier transforms.

Remark 5.

Assuming , one recovers using

| (60) |

As previously mentioned, to obtain the FK transition densities one simply sets . In this case, becomes .

When the coefficients are time-homogeneous, then the results of Theorem 1 simplify considerably, as we show in the following corollary.

Corollary 1 (Time-homogeneous case).

Suppose that has time-homogeneous dynamics with the local variance, default intensity and Lévy measure given by , and respectively. Then the symbol is independent of . Define

| (61) |

Then, for we have

| (62) |

where

| (63) | ||||||

| (64) | ||||||

Proof.

The proof is an algebraic computation. For brevity, we omit the details. ∎

Example 4.

Consider the Taylor density expansion of Example 1. That is, . Then, in the time-homogeneous case, we find that and are given explicitly by

| (65) | ||||

| (66) | ||||

| (67) | ||||

| (68) | ||||

| (69) | ||||

| (70) | ||||

| (71) |

Higher order terms are quite long. However, they can be computed quickly and explicitly using the Mathematica code provided in Appendix B. The code in the Appendix can be easily modified for use with other basis functions.

Remark 6.

As in Pagliarani et al. (2013), when considering models with Gaussian-type jumps, i.e., models with a state-dependent Lévy measure of the form (76) below, all terms in the expansion for the transition density become explicit. Likewise, for models with Gaussian-type jumps, all terms in the expansion for the price of an option are also explicit, assuming the payoff is integrable against Gaussian functions.

Remark 7.

Many common payoff functions (e.g. calls and puts) are not integrable: . Such payoffs may sometimes be accommodated using generalized Fourier transforms. Assume

| (72) |

Assume also that is analytic as a function of . Then the formulas appearing in Theorem 1 and Corollary 1 are valid and integration in (60) is with respect to (i.e., ). For example, the payoff of a European call option with payoff function has a generalized Fourier transform

| (73) |

In any practical scenario, one can only compute a finite number of terms in (54). Thus, we define , the th order approximation of by

| (74) |

The function (which we use for time-homogeneous cases) and the approximate FK transition density are defined in an analogous fashion.

5 Pointwise error bounds for Gaussian models

In this section we state some pointwise error estimates for , the th order approximation of the FK density of with as in (17). Throughout this Section, we assume Gaussian-type jumps with -dependent mean, variance and jump intensities. Furthermore, we work specifically with the Taylor series expansion of Example 1. That is, we use basis functions .

Theorem 2.

Assume that

| (75) |

for some positive constants and , and that

| (76) |

with

| (77) |

Moreover assume that and their -derivatives are bounded and Lipschitz continuous in , and uniformly bounded with respect to . Let in (39). Then, for , we have444Here , where denotes the sup-norm on . Note that if are constants.

| (78) |

for any and , where

| (79) |

Here, the function is the fundamental solution of the constant coefficients jump-diffusion operator

| (80) |

where is a suitably large constant, and is defined as

| (81) |

and where is the convolution operator acting as

| (82) |

Proof.

Remark 8.

The functions take the following form

| (83) |

and therefore can be explicitly written as

| (84) |

By Remark 8, it follows that, when and , the asymptotic behaviour as of the sum in (83) depends only on the term. Consequently, we have as tends to . On the other hand, for , , and thus also , tends to a positive constant as goes to . It is then clear by (78) that, with fixed, the asymptotic behavior of the error, when tends to , changes from to depending on whether the Lévy measure is locally-dependent or not.

Theorem 2 extends the previous results in Pagliarani et al. (2013) where only the purely diffusive case (i.e ) is considered. In that case an estimate analogous to (78) holds with

Theorem 2 shows that for jump processes, increasing the order of the expansion for greater than one, theoretically does not give any gain in the rate of convergence of the asymptotic expansion as ; this is due to the fact that the expansion is based on a local (Taylor) approximation while the PIDE contains a non-local part. This estimate is in accord with the results in Benhamou et al. (2009) where only the case of constant Lévy measure is considered. Thus Theorem 2 extends the latter results to state dependent Gaussian jumps using a completely different technique. Extensive numerical tests showed that the first order approximation gives extremely accurate results and the precision seems to be further improved by considering higher order approximations.

Corollary 2.

Under the assumptions of Theorem 2, we have the following estimate for the error on the approximate prices:

| (85) |

for any and .

Some possible extensions of these asymptotic error bounds to general Lévy measures are possible, though they are certainly not straightforward. Indeed, the proof of Theorem 2 is based on some pointwise uniform estimates for the fundamental solution of the constant coefficient operator, i.e. the transition density of a compound Poisson process with Gaussian jumps. When considering other Lévy measures these estimates would be difficult to carry out, especially in the case of jumps with infinite activity, but they might be obtained in some suitable normed functional space. This might lead to error bounds for short maturities, which are expressed in terms of a suitable norm, as opposed to uniform pointwise bounds.

Remark 9.

Since, in general, it is hard to derive the truncation error bound, the reader may wonder how to determine the number of terms to include in the asymptotic expansion. Though we provide a general expression for the -th term, realistically, only the fourth order term can be computed. That said, in practice, three terms provide an approximation which is accurate enough for most applications (i.e., the resulting approximation error is smaller than the bid-ask spread typically quoted on the market). Since, only requires a single Fourier integration, there is no numerical advantage for choosing smaller . As such, for financial applications we suggest using or .

6 Examples

In this section, in order to illustrate the versatility of our asymptotic expansion, we apply our approximation technique to a variety of different Lévy-type models. We consider both finite and infinite activity Lévy-type measures and models with and without a diffusion component. We study not only option prices, but also implied volatilities. In each setting, if the exact or approximate option price has been computed by a method other than our own, we compare this to the option price obtained by our approximation. For cases where the exact or approximate option price is not analytically available, we use Monte Carlo methods to verify the accuracy of our method.

Note that, some of the examples considered below do not satisfy the conditions listed in Section 2. In particular, we will consider coefficients that are not bounded. Nevertheless, the formal results of Section 4 work well in the examples considered.

6.1 CEV-like Lévy-type processes

We consider a Lévy-type process of the form (1) with CEV-like volatility and jump-intensity. Specifically, the -price dynamics are given by

| (86) |

where is a Lévy measure. When , this model reduces to the CEV model of Cox (1975). Note that, with , the volatility and jump-intensity increase as , which is consistent with the leverage effect (i.e., a decrease in the value of the underlying is often accompanied by an increase in volatility/jump intensity). This characterization will yield a negative skew in the induced implied volatility surface. As the class of models described by (86) is of the form (45) with , this class naturally lends itself to the two-point Taylor series approximation of Example 2. Thus, for certain numerical examples in this Section, we use basis functions given by (48). In this case we choose expansion points and in a symmetric interval around and in (43) we choose . For other numerical examples, we use the (usual) one-point Taylor series expansion . In this cases, we choose .

We will consider two different characterizations of :

| Gaussian: | (87) | ||||

| Variance-Gamma: | (88) | ||||

| (89) |

Note that the Gaussian measure is an example of a finite-activity Lévy measure (i.e., ), whereas the Variance-Gamma measure, due to Madan et al. (1998), is an infinite-activity Lévy measure (i.e., ). As far as the authors of this paper are aware, there is no closed-form expression for option prices (or the transition density) in the setting of (86), regardless of the choice of . As such, we will compare our pricing approximation to prices of options computed via standard Monte Carlo methods.

Remark 10.

555We would like to thank an anonymous referee for bringing the issue of boundary conditions to our attention.Note, the CEV model typically includes an absorbing boundary condition at . A more rigorous way to deal with degenerate dynamics, as in the CEV model, would be to approximate the solution of the Cauchy problem related to the process (as apposed to ). One would then equip the Cauchy problem with suitable Dirichlet conditions on the boundary , and work directly in the variable as opposed to the log-price on . Indeed, this is the approach followed by Hagan and Woodward (1999) who approximate the true density by a Gaussian density through a heat kernel expansion: note that the supports of and are and respectively. In order to take into account of the boundary behavior of the true density , an improved approximation could be achieved by using the Green function of the heat operator for instead of the Gaussian kernel: this will be object of further research in a forthcoming paper.

We would also like to remark explicitly that our methodology is very general and works with different choices for the leading operator of the expansion, such as the constant-coefficient PIDEs we consider in the case of jumps. Nevertheless, in the present paper, when purely diffusive models are considered, we always take the heat operator as the leading term of our expansion. The main reasons are that (i) the heat kernel is convenient for its computational simplicity and (ii) the heat kernel allows for the possibility of passing directly from a Black-Scholes-type price expansion to an implied vol expansion.

6.1.1 Gaussian Lévy Measure

In our first numerical experiment, we consider the case of Gaussian jumps. That is, is given by (87). We fix the following parameters

| (90) |

Using Corollary 1, we compute the approximate prices and of a series of European puts over a range of strikes and with times to maturity (we add the parameter to the arguments of to emphasize the dependence of on the strike price ). To compute , we use the we the usual one-point Taylor series expansion (Example 1). We also compute the price of each put by Monte Carlo simulation. For the Monte Carlo simulation, we use a standard Euler scheme with a time-step of years, and we simulate sample paths. We denote by the price of a put obtained by Monte Carlo simulation. As prices are often quoted in implied volatilities, we convert prices to implied volatilities by inverting the Black-Scholes formula numerically. That is, for a given put price , we find such that

| (91) |

where is the Black-Scholes price of the put as computed assuming a Black-Scholes volatility of . For convenience, we introduce the notation

| (92) |

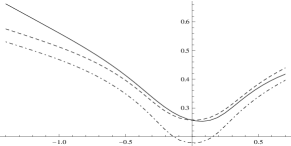

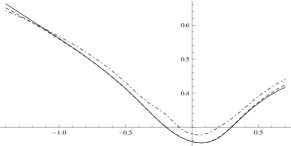

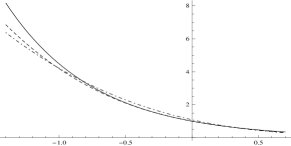

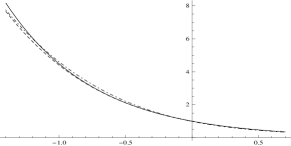

to indicate the implied volatility induced by option price . The results of our numerical experiments are plotted in Figure 1. We observe that agrees almost exactly with . The computed prices and their induced implied volatilities , as well as 95% confidence intervals resulting from the Monte Carlo simulations can be found in Table 1.

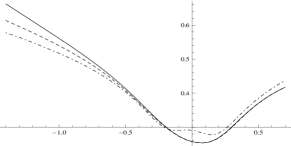

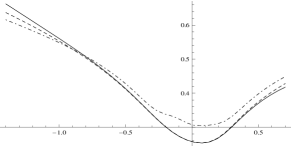

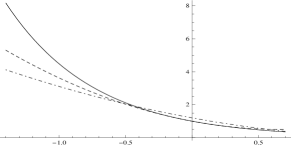

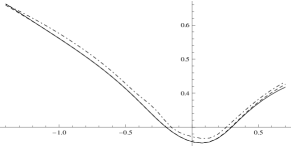

Comparing one-point Taylor and Hermite expansions

As choosing different basis functions results in distinct option-pricing approximations, one might wonder: which choice of basis functions provides the most accurate approximation of option prices and implied volatilities? We investigate this question in Figure 2. In the left column, using the parameters in (90), we plot , , where is computed using both the one-point Taylor series basis functions (Example 1) and the Hermite polynomial basis functions (Example 3). We also plot , the implied volatility obtained by Monte Carlo simulation. For comparison, in the right column, we plot the function as well as and where

| (93) |

From Figure 2, we observe that, for every , the Taylor series expansion provides a better approximation of the function (at least locally) than does the Hermite polynomial expansion . In turn, the implied volatilities resulting from the Taylor series basis functions more accurately approximate than do the implied volatilities resulting from the Hermite basis functions. The implied volatilities resulting from the two-point Taylor series price approximation (not shown in the Figure for clarity), are nearly indistinguishable implied volatilities induced by the (usual) one-point Taylor series price approximation.

Computational speed, accuracy and robustness

In order for a method of obtaining approximate option prices to be useful to practitioners, the method must be fast, accurate and work over a wide range of model parameters. In order to test the speed, accuracy and robustness of our method, we select model parameters at random from uniform distributions within the following ranges

| (94) |

Using the obtained parameters, we then compute approximate option prices and record computation times over a fixed range of strikes using our third order one-point Taylor expansion (Example 1). As the exact price of a call option is not available, we also compute option prices by Monte Carlo simulation. The results are displayed in Tables 2 and 3. The tables show that our third order price approximation consistently falls within the 95% confidence interval obtained from the Monte Carlo simulation. Moreover, using a 2.4 GHz laptop computer, an approximate call price can be computed in only seconds. This is only four to five times larger than the amount of time it takes to compute a similar option price using standard Fourier methods in an exponential Lévy setting.

6.1.2 Variance Gamma Lévy Measure

In our second numerical experiment, we consider the case of Variance Gamma jumps. That is, given by (88). We fix the following parameters:

| (95) |

Note that, by letting , we have set the diffusion component of to zero: . Thus, is a pure-jump Lévy-type process. Using Corollary 1, we compute the approximate prices and of a series of European puts over a range of strikes and with maturities . To compute , , we use the two-point Taylor series expansion (Example 2). We also compute the put prices by Monte Carlo simulation. For the Monte Carlo simulation, we use a time-step of years and we simulate sample paths. At each time-step, we update using the following algorithm

| (96) | ||||||

| (97) |

where is a Gamma-distributed random variable with shape parameter and scale parameter . Note that this is equivalent to considering a VG-type process with state-dependent parameters

| (98) |

These state-dependent parameters result in state-independent (i.e., remain constant). Once again, since implied volatilities rather than prices are the quantity of primary interest, we convert prices to implied volatilities by inverting the Black-Scholes formula numerically. The results are plotted in Figure 3. We observe that agrees almost exactly with . Values for , the associated implied volatilities and the 95% confidence intervals resulting from the Monte Carlo simulation can be found in table 4.

7 Conclusion

In this paper, we consider an asset whose risk-neutral dynamics are described by an exponential Lévy-type martingale subject to default. This class includes nearly all non-negative Markov processes. In this very general setting, we provide a family of approximations – one for each choice of the basis functions (i.e. Taylor, two-point Taylor, basis, etc.) – for (i) the transition density of the underlying (ii) European-style option prices and their sensitivities and (iii) defaultable bond prices and their credit spreads. For the transition densities, and thus for option and bond prices as well, we establish the accuracy of our asymptotic expansion.

Thanks

The authors would like to extend their thanks to an anonymous referee, whose comments and suggestions helped to improve this paper.

Appendix A Proof of Theorem 1

By hypothesis , and thus, by standard Fourier transform properties we the following relation holds:

| (99) |

We now Fourier transform equation (56). At the left-hand side we have

| (100) |

Next, for the right-hand side of (56) we get

| (101) | ||||

| (102) | ||||

| (by (99)) | ||||

| (103) | ||||

Thus, we have the following ODEs (in ) for

| (104) | ||||||

| (105) |

One can easily verify (e.g., by substitution) that the solutions of (104) and (105) are given by (57) and (58) respectively.

Appendix B Mathematica code

The following Mathematica code can be used to generate the automatically for Taylor series basis functions: . We have

| (106) | ||||

| (107) | ||||

| (108) | ||||

| (109) | ||||

| (110) | ||||

| (111) | ||||

| (112) | ||||

| (113) | ||||

| (114) | ||||

The function is now computed explicitly by typing and pressing Shift+Enter. Note that the function can depend on a parameter (e.g., -strike) through the Fourier transform of the payoff function . To compute using other basis functions, one simply has to replace the first line in the code. For example, for Hermite polynomial basis functions, one re-writes the top line as

| (115) |

where is the Mathematica command for the -th Hermite polynomial (note that Mathematica does not normalize the Hermite polynomials as we do in equation (52)).

Appendix C Sketch of the Proof of Theorem 2

Proof.

For sake of simplicity we only provide a sketch of the proof for the case , and . For the complete and detailed proof we refer to the companion paper Lorig et al. (2013).

The main idea of the proof is to use our expansion as a parametrix. That is, our expansion will be the starting point of the classical iterative method introduced by Levi (1907) to construct the fundamental solution . Specifically, as in Pagliarani et al. (2013), we take as a parametrix our -th order approximation with basis functions and with . By analogy with the classical approach (see, for instance, Friedman (1964) and Di Francesco and Pascucci (2005), Pascucci (2011) for the purely diffusive case, or Garroni and Menaldi (1992) for the integro-differential case), we have

| (116) |

where is determined by imposing the condition

Equivalently, we have

and therefore by iteration

| (117) |

where

| (118) | ||||

| (119) |

The proof of Theorem 2, then, is based on some pointwise bounds for each term in (117). These bounds, summarized in the next two propositions, can be combined with formula (116) to obtain the estimate for .

Proposition 2.

There exists a positive constant , only dependent on and , such that

| (120) |

for any and with .

Proposition 3.

There exists a positive constant , only dependent on and ,, such that

| (121) |

for any , and with .

The proofs of Proposition 2 and Proposition 3 are rather technical and are based on several global pointwise estimates for the fundamental solution of a constant coefficient integro-differential operator of the form (80), along with the semigroup property

| (122) |

We refer to Lorig et al. (2013) for detailed proofs.

References

- Andersen and Andreasen (2000) Andersen, L. and J. Andreasen (2000). Jump-diffusion processes: Volatility smile fitting and numerical methods for option pricing. Review of Derivatives Research 4(3), 231–262.

- Benhamou et al. (2009) Benhamou, E., E. Gobet, and M. Miri (2009). Smart expansion and fast calibration for jump diffusions. Finance and Stochastics 13(4), 563–589.

- Bielecki and Rutkowski (2001) Bielecki, T. and M. Rutkowski (2001). Credit Risk: Modelling, Valuation and Hedging. Springer.

- Boyarchenko and Levendorskii (2002) Boyarchenko, S. and S. Levendorskii (2002). Non-Gaussian Merton-Black-Scholes Theory. World Scientific.

- Capponi et al. (2013) Capponi, A., S. Pagliarani, and T. Vargiolu (2013). Pricing vulnerable claims in a Lévy driven model. preprint SSRN.

- Carr et al. (2002) Carr, P., H. Geman, D. Madan, and M. Yor (2002). The fine structure of asset returns: An empirical investigation. The Journal of Business 75(2), 305–333.

- Carr and Linetsky (2006) Carr, P. and V. Linetsky (2006). A jump to default extended CEV model: An application of Bessel processes. Finance and Stochastics 10(3), 303–330.

- Carr and Madan (2010) Carr, P. and D. B. Madan (2010). Local volatility enhanced by a jump to default. SIAM J. Financial Math. 1, 2–15.

- Christoffersen et al. (2009) Christoffersen, P., K. Jacobs, and Ornthanalai (2009). Exploring Time-Varying Jump Intensities: Evidence from S&P500 Returns and Options. CIRANO.

- Cox (1975) Cox, J. (1975). Notes on option pricing I: Constant elasticity of diffusions. Unpublished draft, Stanford University. A revised version of the paper was published by the Journal of Portfolio Management in 1996.

- Di Francesco and Pascucci (2005) Di Francesco, M. and A. Pascucci (2005). On a class of degenerate parabolic equations of Kolmogorov type. AMRX Appl. Math. Res. Express 3, 77–116.

- Dupire (1994) Dupire, B. (1994). Pricing with a smile. Risk 7(1), 18–20.

- Eraker (2004) Eraker, B. (2004). Do stock prices and volatility jump? Reconciling evidence from spot and option prices. The Journal of Finance 59(3), 1367–1404.

- Estes and Lancaster (1972) Estes, R. H. and E. R. Lancaster (1972). Some generalized power series inversions. SIAM J. Numer. Anal. 9, 241–247.

- Friedman (1964) Friedman, A. (1964). Partial differential equations of parabolic type. Englewood Cliffs, N.J.: Prentice-Hall Inc.

- Garroni and Menaldi (1992) Garroni, M. G. and J.-L. Menaldi (1992). Green functions for second order parabolic integro-differential problems, Volume 275 of Pitman Research Notes in Mathematics Series. Harlow: Longman Scientific & Technical.

- Hagan and Woodward (1999) Hagan, P. and D. Woodward (1999). Equivalent Black volatilities. Applied Mathematical Finance 6(3), 147–157.

- Hoh (1998) Hoh, W. (1998). Pseudo differential operators generating Markov processes. Habilitations-schrift, Universität Bielefeld.

- Jacquier and Lorig (2013) Jacquier, A. and M. Lorig (2013). The smile of certain Lévy-type models. ArXiv preprint arXiv:1207.1630.

- Jeanblanc et al. (2009) Jeanblanc, M., M. Yor, and M. Chesney (2009). Mathematical methods for financial markets. Springer Verlag.

- Levi (1907) Levi, E. E. (1907). Sulle equazioni lineari totalmente ellittiche alle derivate parziali. Rend. Circ. Mat. Palermo 24, 275–317.

- Linetsky (2006) Linetsky, V. (2006). Pricing equity derivatives subject to bankruptcy. Mathematical Finance 16(2), 255–282.

- Linetsky (2007) Linetsky, V. (2007). Chapter 6 Spectral methods in derivatives pricing. In J. R. Birge and V. Linetsky (Eds.), Financial Engineering, Volume 15 of Handbooks in Operations Research and Management Science, pp. 223 – 299. Elsevier.

- Lopez and Temme (2002) Lopez, J. L. and N. M. Temme (2002). Two-point Taylor expansions of analytic functions. Studies in Applied Mathematics 109(4), 297–311.

- Lorig et al. (2013) Lorig, M., S. Pagliarani, and A. Pascucci (2013). Pricing approximations and error estimates for local Lévy-type models with default. ArXiv preprint arXiv:1304.1849.

- Madan et al. (1998) Madan, D., P. Carr, and E. Chang (1998). The variance gamma process and option pricing. European Finance Review 2(1), 79–105.

- Mendoza-Arriaga et al. (2010) Mendoza-Arriaga, R., P. Carr, and V. Linetsky (2010). Time-changed markov processes in unified credit-equity modeling. Mathematical Finance 20, 527–569.

- Oksendal and Sulem (2005) Oksendal, B. and A. Sulem (2005). Applied stochastic control of jump diffusions. Springer Verlag.

- Pagliarani and Pascucci (2011) Pagliarani, S. and A. Pascucci (2011). Analytical approximation of the transition density in a local volatility model. Central European Journal of Mathematics 10(1), 250–270.

- Pagliarani et al. (2013) Pagliarani, S., A. Pascucci, and C. Riga (2013). Adjoint expansions in local Lévy models. SIAM J. Finan. Math. 4(1), 265–296.

- Pascucci (2011) Pascucci, A. (2011). PDE and martingale methods in option pricing. Bocconi&Springer Series. New York: Springer-Verlag.

|

|

|

|

| MC-95% c.i. | IV MC-95% c.i. | ||||

|---|---|---|---|---|---|

| -0.6931 | 0.0006 | 0.0006 - 0.0007 | 0.5864 | 0.5856 - 0.5901 | |

| -0.4185 | 0.0024 | 0.0024 - 0.0025 | 0.4563 | 0.4553 - 0.4583 | |

| 0.2500 | -0.1438 | 0.0111 | 0.0110 - 0.0112 | 0.2875 | 0.2865 - 0.2883 |

| 0.1308 | 0.1511 | 0.1508 - 0.1513 | 0.2595 | 0.2573 - 0.2608 | |

| 0.4055 | 0.5028 | 0.5024 - 0.5030 | 0.4238 | 0.4152 - 0.4288 | |

| -1.2040 | 0.0009 | 0.0009 - 0.0010 | 0.5115 | 0.5176 - 0.5210 | |

| -0.7297 | 0.0046 | 0.0047 - 0.0048 | 0.4174 | 0.4178 - 0.4199 | |

| 1.0000 | -0.2554 | 0.0314 | 0.0313 - 0.0316 | 0.3109 | 0.3102 - 0.3117 |

| 0.2189 | 0.2781 | 0.2775 - 0.2784 | 0.2638 | 0.2620 - 0.2649 | |

| 0.6931 | 1.0034 | 1.0030 - 1.0041 | 0.3358 | 0.3296 - 0.3459 | |

| -1.3863 | 0.0074 | 0.0081 - 0.0083 | 0.4758 | 0.4851 - 0.4870 | |

| -0.8664 | 0.0224 | 0.0224 - 0.0227 | 0.4031 | 0.4029 - 0.4045 | |

| 3.0000 | -0.3466 | 0.0776 | 0.0773 - 0.0779 | 0.3280 | 0.3274 - 0.3288 |

| 0.1733 | 0.3097 | 0.3094 - 0.3107 | 0.2690 | 0.2685 - 0.2703 | |

| 0.6931 | 1.0155 | 1.0150 - 1.0169 | 0.2558 | 0.2540 - 0.2604 | |

| -1.6094 | 0.0160 | 0.0164 - 0.0166 | 0.5082 | 0.5111 - 0.5128 | |

| -0.9324 | 0.0439 | 0.0436 - 0.0440 | 0.4118 | 0.4107 - 0.4121 | |

| 5.0000 | -0.2554 | 0.1504 | 0.1497 - 0.1507 | 0.3203 | 0.3194 - 0.3208 |

| 0.4216 | 0.6139 | 0.6123 - 0.6142 | 0.2521 | 0.2500 - 0.2524 | |

| 1.0986 | 2.0050 | 2.0032 - 2.0057 | 0.2297 | 0.2163 - 0.2342 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

years

Parameters

MC-95% c.i.

IV MC-95% c.i.

-0.6000

0.4552

0.4552 - 0.4553

0.6849

0.6836 - 0.6869

-0.3500

0.3123

0.3122 - 0.3124

0.6230

0.6217 - 0.6242

-0.1000

0.1621

0.1618 - 0.1623

0.5704

0.5687 - 0.5714

0.1500

0.0496

0.0492 - 0.0500

0.5240

0.5222 - 0.5266

0.4000

0.0059

0.0057 - 0.0067

0.4821

0.4787 - 0.4950

-0.6000

0.4566

0.4566 - 0.4567

0.7257

0.7239 - 0.7271

-0.3500

0.3137

0.3136 - 0.3139

0.6391

0.6378 - 0.6405

-0.1000

0.1431

0.1429 - 0.1434

0.4615

0.4602 - 0.4630

0.1500

0.0032

0.0030 - 0.0037

0.2013

0.1970 - 0.2073

0.4000

0.0000

0.0000 - 0.0000

0.2510

0.2567 - 0.2616

-0.6000

0.4621

0.4619 - 0.4621

0.8462

0.8439 - 0.8478

-0.3500

0.3190

0.3189 - 0.3192

0.6949

0.6933 - 0.6968

-0.1000

0.1578

0.1575 - 0.1581

0.5457

0.5444 - 0.5476

0.1500

0.0451

0.0448 - 0.0456

0.4990

0.4974 - 0.5021

0.4000

0.0155

0.0152 - 0.0162

0.6006

0.5981 - 0.6080

-0.6000

0.4592

0.4591 - 0.4593

0.7871

0.7857 - 0.7900

-0.3500

0.3100

0.3099 - 0.3102

0.5965

0.5950 - 0.5986

-0.1000

0.1341

0.1338 - 0.1343

0.4083

0.4069 - 0.4096

0.1500

0.0306

0.0302 - 0.0309

0.4149

0.4126 - 0.4168

0.4000

0.0176

0.0171 - 0.0179

0.6213

0.6171 - 0.6244

years

Parameters

MC-95% c.i.

IV MC-95% c.i.

-1.0000

0.6487

0.6486 - 0.6488

0.7306

0.7294 - 0.7319

-0.6000

0.5001

0.5000 - 0.5004

0.6719

0.6711 - 0.6734

-0.2000

0.3220

0.3216 - 0.3224

0.6167

0.6157 - 0.6182

0.2000

0.1512

0.1507 - 0.1520

0.5649

0.5636 - 0.5671

0.6000

0.0413

0.0408 - 0.0428

0.5166

0.5145 - 0.5219

-1.0000

0.6556

0.6555 - 0.6561

0.8022

0.8014 - 0.8075

-0.6000

0.5012

0.5011 - 0.5018

0.6779

0.6772 - 0.6809

-0.2000

0.3052

0.3051 - 0.3060

0.5655

0.5651 - 0.5678

0.2000

0.1188

0.1184 - 0.1198

0.4832

0.4822 - 0.4858

0.6000

0.0299

0.0296 - 0.0315

0.4708

0.4694 - 0.4772

-1.0000

0.6679

0.6677 - 0.6681

0.9122

0.9108 - 0.9140

-0.6000

0.5237

0.5236 - 0.5243

0.7916

0.7913 - 0.7943

-0.2000

0.3436

0.3431 - 0.3441

0.6830

0.6814 - 0.6845

0.2000

0.1592

0.1581 - 0.1596

0.5851

0.5823 - 0.5862

0.6000

0.0373

0.0358 - 0.0379

0.5009

0.4949 - 0.5033

-1.0000

0.6323

0.6323 - 0.6324

0.36740

0.3680 - 0.3708

-0.6000

0.4554

0.4553 - 0.4554

0.34493

0.3442 - 0.3456

-0.2000

0.2283

0.2281 - 0.2284

0.32159

0.3208 - 0.3221

0.2000

0.0495

0.0491 - 0.0500

0.29930

0.2980 - 0.3006

0.6000

0.0021

0.0015 - 0.0027

0.27807

0.2655 - 0.2888

|

|

| MC-95% c.i. | IV MC-95% c.i. | ||||

|---|---|---|---|---|---|

| -0.6931 | 0.0014 | 0.0014 - 0.0015 | 0.4631 | 0.4624 - 0.4652 | |

| -0.4185 | 0.0070 | 0.0070 - 0.0071 | 0.4000 | 0.3995 - 0.4014 | |

| 0.5000 | -0.1438 | 0.0363 | 0.0362 - 0.0365 | 0.3336 | 0.3331 - 0.3346 |

| 0.1308 | 0.1702 | 0.1697 - 0.1704 | 0.2727 | 0.2707 - 0.2736 | |

| 0.4055 | 0.5011 | 0.5004 - 0.5012 | 0.2615 | 0.2291 - 0.2646 | |

| -0.9163 | 0.0028 | 0.0027 - 0.0028 | 0.4687 | 0.4678 - 0.4702 | |

| -0.5697 | 0.0109 | 0.0109 - 0.0110 | 0.4057 | 0.4050 - 0.4068 | |

| 1.0000 | -0.2231 | 0.0473 | 0.0472 - 0.0476 | 0.3434 | 0.3428 - 0.3444 |

| 0.1234 | 0.1970 | 0.1965 - 0.1974 | 0.2836 | 0.2825 - 0.2847 | |

| 0.4700 | 0.6033 | 0.6025 - 0.6037 | 0.2452 | 0.2355 - 0.2506 |