Information and optimal investment

in defaultable assets

Giulia Di Nunno

Giulia Di Nunno: Center of Mathematics for Applications, University of Oslo,

PO Box 1053 Blindern, N-0316 Oslo, Norway, and, Norwegian School of Economics and Business Administration, Helleveien 30, N-5045 Bergen, Norway.

and Steffen Sjursen

Steffen Sjursen: Center of Mathematics for Applications, University of Oslo, PO Box 1053 Blindern, N-0316 Oslo, Norway

giulian@math.uio.no, s.a.sjursen@cma.uio.nohttp://folk.uio.no/giulian/

Abstract.

We study optimal investment in an asset subject to risk of default for investors that rely on different levels of information. The price dynamics can include noises both from a Wiener process and a Poisson random measure with infinite activity. The default events are modeled via a counting process in line with large part of the literature in credit risk. In order to deal with both cases of inside and partial information we consider the framework of the anticipating calculus of forward integration. This does not require a priori assumptions typical of the framework of enlargement of filtrations. We find necessary and sufficent conditions for the existence of a locally maximizing portfolio of the expected utility at terminal time. We consider a large class of utility functions. In addition we show that the existence of the solution implies the semi-martingale property of the noises driving the stock. Some discussion on unicity of the maxima is included.

The research leading to these results has received funding from the

European Research Council under the European Community’s Seventh Framework

Programme (FP7/2007-2013) / ERC grant agreement no [228087]

1. Introduction: The model, the optimization problem, the streams of information

Occasionally, we observe that unexpected events wipe out shareholder values. We will generically call all these events default events.

Inspired by default risk literature, we consider a model for stocks where there is a varying risk of instantaneous loss in the stock value.

Of particular interest here is when the default events are dependent on the noises driving the stock or when the investor has insider information. In these cases mathematical questions arise as to whether the driving noises are still (semi)-martingales and the relevant stochastic integrals can be interpreted in the Itô sense. Since this is not a priori certain, we choose to investigate this issue using forward integration in the modeling of stock prices. With this we do not need a priori assumptions or restrictions on the information available to the investor and we will be able to use a unique framework for all the situations of interest.

Our main result is a sufficent and necessary criteria for an optimal investment strategy maximizing the expected utility of the final portfolio value, for a portfolio involving the defaultable asset. We remark that this result also holds for optimization problems with partial or delayed information.

Furthermore we show that the existence of an optimal strategy yields the semi-martingale property of the noises. This would usually be assumed a priori if working in the framework of enlargement of filtrations see for instance [4, 9, 11, 21, 19, 18].

The defaultable stock is modeled with three random noises, a Wiener process , a Poisson random measure and a pure jump process . The occurence of defaults or catastrophic events is modelled by . The intensity of , as viewed by the investor, is stochastic and can either depend on current and future knowledge of and or be independent of the two.

Our model market on the time horizon () consists of a (non-defaultable) bond serving as numéraire with dynamics:

(1.1)

and a defaultable asset with price dynamics:

(1.2)

Here , , is a standard Wiener process and , , is a Poisson random measure, independent of and with . We denote .

Moreover , is a càdlàg counting process, with

We remark that is not necessarily independent of and . Being a process of finite variation the corresponding integral is intended path-wise. On the other side, the indicates forward integration. The forward integral extends the Itô integral but does not require the integrand to be adapted to a specific filtration, see Section 2 for details.

The random processes considered live in a complete probability space . In the sequel the following -augmented filtrations appear

•

where

,

•

where

,

•

where

is a right continuous filtration that represents the information available to the investor at time .

We assume that the coefficients , , , and are càglàd

stochastic processes and is a càglàd random field, in the sense that is càglàd -a.e. (-a.e.). Here , , and are measurable with respect to while is -measurable. The choice of the forward integral in (1.2) allows us to drop the usual requirements of adaptedness of the coefficients to the given information. Naturally, in the case of adaptedness (1.2) could be expressed in terms of Itô integration (see Section 2).

The Borel measure on is -finite and satisfies . For modeling purposes would be taken to be negative though it is not a necessary condition for the optimization problem.

We denote as the -predictable intensity of , i.e. the -predictable random measure such that

for all -predictable processes . In addition, we assume that and do not jump at the same time, i.e.

compact such that

(1.3)

We set forward integrable with respect to , and forward integrable with respect to and

(1.4)

To have well defined and non-negative at all times, we assume

(1.5)

(1.6)

Using an adequate version of the Itô formula (Theorem 2.6), we see that the solution of (1.2) is

(1.7)

and it is easy to argue that this solution is unique. This can be achieved using similar arguments as in [27, Theorem 37] though adapted to forward integration.

The investor’s optimization problem is to divide his money between the asset and the bond in order to achieve the maximum expected utility of the portfolio value at the end of the period allowed. The investor bases his decisions on the information available to him represented by the filtration .

The investor’s wealth , , is given by:

(1.8)

with initial value . The process , , represents the fraction of wealth invested in .

Note that is a -adapted stochastic process.

We aim for generality in how the optimization scheme ends. In particular we are interested in the two different scenarios:

(1)

It is no longer possible to invest in the asset after the first jump of . In this case, the jump of signifies default or another catastrophic event. See, e.g. [6, 7, 11].

(2)

It is possible to invest in the asset even after several “default” events. The jumps of signify the occurence of these “default” events. and the dynamics of can possibly change. See, e.g. [21, 26].

To describe both the above scenarios, we assume that the it is longer possible to invest in after a -stopping time . For the period all the investor’s wealth is invested in the bond. The stopping time must satisfy , meaning that the optimization problem terminates in any case when the time horizon is reached, and , meaning that the optimization problem ends if there is no value in the asset .

By application of the Itô formula, we can see that the (unique) solution of (1.8), for a given admissible (see Definition 3.1), is:

(1.9)

and set .

In summary we study the optimal portfolio problem

(1.10)

of an investor having as information flow at disposal and as utility function. Here represents the set of admissible portfolios (see Definition 3.1).

The optimization scheme itself Theorem 3.3 and the related Theorem 4.2 are an extension of the results in [2, 12] to include a form of default risk.

We refer to [29, 30] for the treatment of the forward integral with respect to the Wiener process, and to [12] for the case of integration with respect to the compensated Poisson random measure. The forward integral is an extension of the Itô integral, but does not require the adaptedness of the integrands to the integral filtration.

Applications of this type of integration to optimization problems and the justification of the use of these integrals from the modeling point of view have been studied. See, e.g. [2, 13, 10, 22]. We also refer to [14] for a unified presentation of the topics.

Related to our optimization problem is the optimization of investments under uncertain time-horizons, as done in [6, 11].

In [6], optimization ends at a stopping time related to the noise in stock price.

In [11] both optimal consumption and investment are treated. Typically the problems are solved using some variants of Hamilton-Jacobi-Bellman (HJB) equations.

Our approach differs from these works for several reasons.

First we focus on different streams of information for the investor, second we consider that the loss in the case of default depends on the position in the risky asset. Moreover, our approach is different in framework and we do not use HJB type solutions.

In [25] we find a study of a problem similar to ours. The approach is however entirely different as in this case backward stochastic differential equations are involved.

Moreover we allow for a more general information structure and we consider a

Lévy type of noise in the price dynamics.

Our work has some similarities to [1], where an optimization problem is considered when the stock dynamics include a jump component with an unknown intensity modeled by a continous time Markov chain. But the filtering techniques therein may be less suited to default modeling since default is a jump happening only once. The methodology presented there relies on HJB equations and differs from ours.

Bielecki and coauthors consider various forms of optimal investments in, e.g. [4], [5] and [3], looking at optimality and hedging when there is a number of instruments, some of which are subject to default.

However, their main focus is on the use of defaultable instruments for hedging purposes and the evaluation on whether to invest in defaultable bonds. In the same line is the study in [16].

As announced, in this paper we adopt the framework of anticipating stochastic calculus, specifically forward integration to tackle the optimization problem (1.10). Moreover, we consider the problem for various choices of investor’s information flow .

To the best of our knowledge it is the first time that the framework of forward integration is applied in optimization problems in presence of default.

In this paper we provide a characterization for the existence of locally optimal controls in a great generality both in the choice of utility function and in the amount of information available. Considerations on the meaning of locality and some examples are also provided. These topics are presented in Section 3. The key results of forward integration is summarized in Section 2. In Section 4 we reinterpret the results of section 3 in the context of semimartingale-integration.

2. Mathematical framework: Forward Integrals

Forward integrals were introduced by Russo and Valois in the articles [29] and [30] for continuous processes and in [12] for pure jump Lévy process, see also [14] for a systematic presentation.

The forward integral is a type of stochastic anticipating integration that does not require assumptions of adaptedness or predictability to some filtration related to the integrator. Moreover, it is also an extension of the Itô integral in the sense that when the appropiate predictability is in place the two integrals coincide. This makes the forward integral especially suited for studying portfolio optimization problems under insider or partial information, where different filtrations are considered. See for, e.g. [2, 12] and [14].

We follow the idea of [22] and consider the forward integral with respect to the Wiener processes as a limit in . This would also imply forward integrability in the sense of Russo and Valois, [29, 30, 31], who consider the same limit in probability.

Definition 2.1.

We say that the stochastic process , is forward integrable over the interval with respect to W if there exists a process , such that

In this case we write

and call the forward integral of with respect to W on .

Lemma 2.2 shows that the forward integral is an extension of the Itô integral.

Lemma 2.2.

Let } be a given filtration. Suppose that

(1)

W is a semimartingale with respect to the filtration ,

(2)

is -predictable and the Itô integral exists (in ),

Elementary processes are forward integrable, and have a natural interpretation as Riemann-like sums. Suppose the stochastic process , ,, is elementary, meaning that it has the form

(2.1)

where the are bounded random variables and . Then is forward integrable, see [28, Remark 1], and

(2.2)

However, it is not obvious that one can approximate a general forward integrable function by elementary functions and in this way obtain also an approximation to the integral.

Example 2.3.

Let . Then any is forward integrable. But

(2.3)

So even though is bounded, the forward integral with respect to can have arbitrarily large expectations. This would not happen with Itô integrals as it is a result of having infinite total variation and using anticipating information.

To prove (2.3), let be elementary functions of the form

Additionally we can remark that letting , we would get that pointwise and is bounded by the forward integrable function , thus proving that the dominated convergence theorem does not hold for forward integrals with respect to Brownian motions.

Characterizing when integrals are finite or limits do not explode is non-trivial, and from the remark above we see that the boundedness of the integrand is not enough. Thus we have to be careful, even though a sequence of forward integrable functions converge in some suitable space, the corresponding forward integrals over these functions may not converge at all. See also the discussion in [27, Section 1.8].

Definition 2.4.

The forward integral

with respect to the Poisson random measure of a càglàd random field , , , , is defined as

if the limit exists in . Here, is an increasing sequence of compact sets with such that .

Also in this case the forward integral is an extension of the Itô integral [14, Remark 15.2]:

Remark 2.5.

Let be a given filtration such that

(1)

The process , is a semimartingale with respect to .

(2)

The random field , is -predictable.

(3)

The integral exists as a classical Itô integral.

Then is forward integrable and we have

2.1. The Itô formula for forward integrals

An Itô formula for forward type integrals when the integrator is continuous was developed in [30, 31]. An Itô formula for forward integrals with Poisson random measures is found in [12], both the results are also summarized in [14]. In this paper we need a more general version that include processes of finite variation to guarantee the existence of solutions of (1.8) and (1.2). The proof can be seen as a continuation of the one presented in [14, Theorem 8.12], thus we only sketch the additional part.

Theorem 2.6.

Let

where

•

is a stochastic process satisfying

•

is forward integrable with respect to .

•

and are forward integrable with respect to and satisfies

•

is a càdlàg pure jump process of finite variation, with and

compact such that

(2.4)

for all compact.

Here and .

Assume and let . Then

Remark 2.7.

Condition (2.4) is for instance fulfilled if and are independent.

Proof.

Let

where is as in Definition 2.4. We denote , the times of the jumps of . By condition (2.4) we can uniquely (-a.s.) divide the sequence by the jumps of either or as and . We formally set .

Then

with

and

(2.5)

For the elements of the sum in we use [14, Theorem 8.12]:

Adding , and together and letting the result follows.

∎

3. Optimization problem: local maxima

Now we are ready to tackle directly our stated optimization problem (1.10). First we give a description of the set of the investor’s admissible portfolios.

Definition 3.1.

The set of admissible portfolios consists of stochastic processes , such that

i)

is càglàd and -adapted,

ii)

for every , there exists such that for all t,

(3.1)

and

(3.2)

iii)

and

iv)

is càglàd and forward integrable with respect to W,

v)

, and are càglàd and forward integrable with respect to .

The subset of consists of all admissible portfolios that are representable as elementary integrands- see (2.1).

In particular we note that condition i) ensures that the portfolio choices correspond to the investors knowledge and that condition 3.2 ensures that the investor never reaches zero wealth from the jumps of or . In addition 3.2 means that fractions of the form are bounded, which is implicitly used in some forthcoming equations.

Note that if

where is a bounded -measurable random variable, then as long as (3.1) and (3.2) are satisfied.

As announced we are interested in the problem

(3.3)

(We recall that is the value of the investor’s wealth at and the definition of is in (1.8)).

We will search for solutions to (3.3) that are optimal in the sense that they cannot be improved by small perturbations.

Definition 3.2.

We say that the stochastic process is a local maximum for the problem (3.3) if

(3.4)

for all bounded and for some that may depend on .

We say that is a weak local maximum for (3.3) if (3.4) is true for all .

From the terminology point of view, when we say that a property holds under , we mean that the property holds under the measure with respect to the filtration . Moreover, we say that a stochastic process has the martingale property under if

for all . We stress that does not need to be a -martingale despite having the martingale property under . In fact no statement is given about being adapted to .

Following the techniques in [2, 13], we consider pertubations of stochastic controls to find necessary and sometimes sufficient criteria to characterize local maximums. We will need the following assumption for a differentiable utility function .

Assumption . We say that assumption holds for if

i)

,

ii)

, with ,

iii)

For all with bounded, there exists that may depend on such that the family

(3.5)

is uniformly integrable, where

(3.6)

Assumption depends strongly on the utility function . Condition i) is related to the optimization problem (3.3) and ii) is used in the definition of (3.8).

Condition iii), uniform integrability, is the minimal condition for taking limits under the integral sign.

It is unfortunate in that it stems from mathematical rather than modeling necessities, but we cannot do without it.

There is a good discussion in when uniform integrability conditions like Assumption is fulfilled in [14, section 16.5]. The conclusions from [14, section 16.5] can be transferred to our model.

Theorem 3.3.

Suppose the utility function is increasing and differentiable, and holds.

i)

If is a local maximum for (3.3), then the process , , has the martingale property under . Where is defined as

(3.7)

and the measure is defined by , with

(3.8)

ii)

Suppose the mappings

(3.9)

are concave for all controls and . If has the martingale property under then is a weak local maximum for (3.3)

iii)

Suppose is -adapted and the conditions in 3.9 are satisfied. If is a -martingale then is a local maximum for (3.3).

Proof.

Part 3.8 If is a local maximum, then for all bounded we have

(3.10)

Here assumption is used, see for instance [15, Appendix A]. With some calculations we obtain

(3.11)

We now let , where is a -measurable bounded random variable. We can put outside the forward integrals, see for instance [14, Lemma 8.7] and [14, Remark 15.3] to get

(3.12)

Hence we conclude that

with and defined as in (3.8) and (3.7) respectively. Since , we can define a new probability measure on by

(3.13)

We thus have that if is a local maximum, has the martingale property under .

Part 3.9.

Suppose has the martingale property under . Then, for ,

or, equivalently, that for all bounded -measurable random variables we have

Taking linear combinations we get that

(3.14)

for any . Since the mapping is concave on then is a weak local maximum.

Part iii). The conditions of 3.9 are satisfied so (3.14) holds for all . Let , be bounded, and , , be a sequence of elementary stochastic processes such converges pointwise in and uniformly in to .

Since is adapted and has the martingale property, it is a local martingale and

By assumption , the random variable is -integrable so that

(3.15)

Since the mapping is concave, from the computations in part 3.8 we see that (3.15) can only be zero if is a local maximum.

∎

With the introduction of the forthcoming assumption we can detail additional results on the convavity of (3.9) and the uniqueness of local maximums.

Assumption : The utility function is twice differentiable, strictly increasing and concave. For , we assume that for all bounded, there exists a , that may depend on , such that the family

is uniformly integrable where is defined in (3.6) and

(3.16)

Since it is reasonable to assume that the coefficients , and are not zero on the same time intervals, then for and .

Lemma 3.4 will give us a sufficient condition for the concavity of (3.9) in Theorem 3.3.

Lemma 3.4.

Suppose and hold with , bounded, and that the utility function satisfies

(3.17)

Then for the mappings (3.9), , , , are concave for all bounded controls .

Proof.

By assumptions and the following equations hold true:

(3.18)

Thanks to (3.17) and the observation that for all , both summands are negative and the mapping (3.9) is locally concave.

∎

Remark 3.5.

Examples of utility functions satisfying (3.17) are the power utility when , and logarithmic utility , while the exponential utility, , does not.

Remark 3.6.

Condition (3.17) can also be discussed in terms of the Arrow Pratt measure of relative risk aversion. This measure is defined by

so an equivalent way of stating condition (3.17) would be to require the .

We can use a concavity argument from the derivatives to get some form of uniqueness. A similar argument occurs in [22], where it is proven that local maximums are unique in the case of logarithmic utility under some restriciton on admissible controls. In our case we have the following result:

Theorem 3.7.

Suppose is a convex set in such that all are bounded. If for all assumptions , with , bounded, and (3.17) is satisfied, then there can at most be one local maximum in .

Proof.

Suppose are two local maximums. Let . Since A is convex, we have for . We note that

Indeed and hold for as it is an element of . In particular we can apply Lemma 3.4 to conclude that

is strictly monotone for .

We show that there cannot exist two local maximums by contradiction. Consider

(3.19)

since , and is a local maximum. On the other hand, we also have that is a local maximum, hence

Consequently is strictly monotone and zero at two different points, which is absurd.

∎

3.1. Some examples with logarithmic utility

We concentrate on the logarithmic utility to reduce computation and highlight some interesting aspects of the analysis. Note that if then in (3.8). By application of Theorem 3.3 the following equation plays a crucial role:

(3.20)

Example 3.8.

Assume that is independent of and and that all the coefficients are -adapted, as in classical market modeling. Further we assume that , for some positive stochastic process .

We consider the case of an investor having access to an information flow with , for all . We call this a case of partial information. The expectation of the forward integrals in (3.20) are zero in this setup, so the equation can be written

Dividing by and letting , we find that the locally optimal in this case must satisfy

(3.21)

For illustration, assume . Then (3.21) yields a polynomial equation in of degree 2:

Example 3.9.

Assume that and that contains no anticipating information on . In this case we say that the investor has full information. If and the coefficients , , , are adapted to , equation (3.21) reduces to

(3.22)

If we assume , the explicit solution of (3.22) is given by

(3.23)

where we used (3.1) to exclude one of the two solutions of the quadratic eqauation.

Remark that equation (3.22) gives us Merton ratio when .

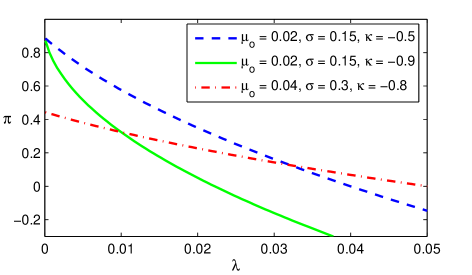

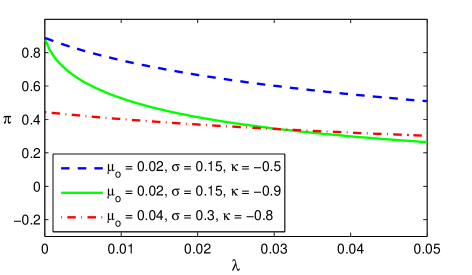

(a)Default risk not compensated by higher drift

(b)Default risk compensated by higher drift

Figure 1. Optimal investment as a function of .

Two explicit examples with full information can be found in the figures. In Figure 1a the stock price is modeled as

(3.24)

with , fixed, and . We see that with higher default risk the agent invests less and the asset is also shorted when the overall return becomes negative at the point .

The assumptions in (3.25) are similar to (3.24). But with the term in the drift, the expected return of the asset is invariant to the value of . So the agent invests less due to risk aversion and not due to changes in the asset returns.

Next we explicitly detail how after-default and/or multiple defaults are easily treated in our framework.

Example 3.10.

Here we discuss a model with default time . After default the asset has a recovery process with different dynamics than before default. We assume that it is possible to invest both before and after default and set . Set and

where . Here and are the coefficients of the noises of the asset dynamics pre-default and and the coefficients after default while and are the drift coefficients before and after default respectively.

In the case of full information as above, , the optimization scheme seperates into pre-default and after default. The optimal portfolio satisfies:

The cases of anticipating information, i.e. , are more subtle than partial or full information, with various approaches being possible depending on the specific conditions. The main challenge with anticipating information is to evaluate the terms and in (3.20).

One possible way to compute the expectations of the forward integrals above is to exploit Malliavin calculus, see [14, Chapter 8 and Chapter 15] for the theoretical framework. However we must stress that this general approach cannot always be taken here. In fact the application of Malliavin calculus requires that the integrands are measurable with respect to , which is not, in general, the case when considering default risk.

See also [13] on how the integral can be evaluated using predictable compensators of the measure with respect to and [2, 23, 22] for other examples on the integral in insider models without default risk.

Hereafter we show an example where the process contains anticipating information on the jumps of . In this example the process , , is martingale under but not under . While we claim no particular market model related to this, we show how the suggested framework enables solutions for optimization problems with anticipating information. In particular the process generalizes the optimization problem not only because of it’s precense, but also because it adds knowledge on the other noises driving . Nevertheless a solution is obtained from Theorem 3.3.

Example 3.11.

Assume , i.e. the Poisson random measure is actually where is a Poisson process with intensity . Define , , and . Thus is independent of but is dependent on . Note that contains anticipating information with respect to since implies . Set .

Our ad hoc interpretation is that too many bad events (represented by ) in a limited time span () will cause the firm to default (with a loss and the asset is no longer tradeable ).

We assume , , , and are constants. Starting from (3.20)

Computing the predictable compensators of and (sketched below), and dividing by we find that the optimal is a solution of

To compute the -predictable compensators of and we investigate the intensities (see, e.g. [8, Section 3.2]) on the set

The -predictable compensators of and are then given by and . We consider the case of , the computations for are similar. First note that

Recall that implies and that implies . For ,

We have

and

Thus

Similarly we find

4. On the driving processes as semi-martingales

The results of Theorem 3.3 take a more specific form when is -adapted. This will be our standing assumption throughout the section, implying that for all and that the integrands and are -adapted.

Theorem 4.1.

Suppose that is -adapted and that for assumption holds.

i)

If is a local maximum, then , , is a martingale under .

ii)

If is a local maximum, then the stochastic process

is a martingale under . Here, we have set

Assume that the mapping is concave for all bounded controls . Then we also have the converse conclusions

iii)

If is a martingale under , then is a local maximum.

Part iv) is again an application of the Girsanov theorem.

∎

The existence of a local maximum also has other implications.

Theorem 4.2.

If a local maximum exists, is -adapted and holds, then and , , are semi-martingales under .

Proof.

Assume a local maximum exists. By Theorem 3.3 this implies that is a -martingale. Define

where is the -predictable compensator of . Note that is a -martingale and thus is also a -martingale. We can (uniquely) decompose into a continuous martingale and pure jump martingale [17, Theorem 1.4.18] which we denote by and respectively. By the definition of it follows that we can write

where

and is such that

(4.1)

The right hand side of (4.1) have a finite expectation by the assumptions (1.4) and Definition 3.1 so that and are processes of finite variation.

As in Theorem 4.1, is a -martingale. We note that is absolutely continouos with respect to Lebesgue by the Kunita-Watanabe-inequality (see for instance [27, Theorem 25]) since the quadratic variation of is absolutely continouos with respect to Lebesgue. Thus the quadratic variation of is , making a -Brownian motion. Hence has the semi-martingale decomposition

where is a -Brownian motion.

Similarly,

(4.2)

is a -martingale. We have that

is a -adapted process of finite variation and thus a semi-martingale (recall that is of finite variation [27, p. 67]). Since also and are semi-martingales we must have that

is a semi-martingale by (4.2). Since the is bounded away from zero (recall Definition 3.1) we must also have that is a semi-martingale.

∎

Finally we do an analysis on the jumps of .

Theorem 4.3.

Assume that a local maximum exists, , is -adapted and Assumption holds. Then the jumps of are totally inaccessible stopping times (for the filtration ) and the -predictable compensators of is absolutely continuous with respect to Lebesgue.

Proof.

With the above assumptions, is a -martingale by Theorem 3.3.

Denote

for . Remark that is a martingale. Since is discontinuous, must be the sum of the predictable compensator of and a martingale. Hence, since is continuous the compensator of is continuous. It immediately follows that the jump times of are totally inaccesible (see, e.g. [20, Corollary 22.18]). ∎

References

[1]N. Bäuerle and U. Rieder, Portfolio optimization with jumps and

unobservable intensity process, Mathematical Finance, 17 (2007),

pp. 205–224.

[2]F. Biagini and B. Øksendal, A general stochastic calculus

approach to insider trading, Applied Mathematics Optimization, 52 (2005),

pp. 167–181.

[3]T. Bielecki and I. Jang, Portfolio optimization with a defaultable

security, Asia-Pacific Financial Markets, 13 (2006), pp. 113–127.

[4]T. Bielecki, M. Jeanblanc, and M. Rutkowski, Hedging of Defaultable

Claims.

Paris-Princeton Lectures on Mathematical Finance, 2004.

[5], PDE approach to

valuation and hedging of credit derivatives, Quantitative Finance, 5

(2007), pp. 257–270.

[6]C. Blanchet-Scalliet, N. E. Karoui, M. Jeanblanc, and L. Martellini, Optimal investment decisions when time-horizon is uncertain, Journal of

Mathematical Economics, 44 (2008), pp. 1100–1113.

[7]B. Bouchard and H. Pham, Wealth-path dependent utility maximization

in incomplete markets, Finance and Stochastics, 8 (2004), pp. 579–603.

10.1007/s00780-004-0125-8.

[8]P. Brémaud, Point Processes and Queues - Martingale dynamics,

Springer, 1981.

[9]D. Coculescu, M. Jeanblanc, and A. Nikeghbali, Default times,

no-arbitrage conditions and changes of probability measures, Finance and

Stochastics, 16 (2012), pp. 513–535.

[10]D. David, Y. Y. Okur, et al., Optimal consumption and portfolio for

an insider in a market with jumps, Communications on Stochastic Analysis, 3

(2009), pp. 101–117.

[11]L. Delong, Optimal investment and consumption in the present of

default in a financial market driven by a Lévy process, Annales

Universitatis Mariae Curie-Sklodowska, LX (2006).

[12]G. Di Nunno, T. Meyer-Brandis, B. Øksendal, and F. Proske, Malliavin calculus and anticipative Itô formulae for Lévy processes,

Infinite Dimensional Analysis, Quantum Probability and Related Topics, 8

(2005), pp. 235–258.

[13], Optimal portfolio

for an insider in a market driven by Lévy processes, Quantitative

Finance, 6 (2006), pp. 83–94.

[14]G. Di Nunno, B. Øksendal, and F. Proske, Malliavin Calculus

for Lévy Processes with Applications to Finance, Springer, 2009.

[15]R. Dudley, Uniform Central Limit Theorems, Cambridge University

Press, 1999.

[16]Y. Hou and X. Jin, Optimal investment with default risk.

FAME Research Paper No. 46, 2002.

[17]J. Jacod and A. N. Shiryaev, Limit Theorems for Stochastic

Processes, Springer, 2003.

[18]M. Jeanblanc and Y. Le Cam, Immersion property and credit risk

modelling, in Optimality and Risk - Modern Trends in Mathematical Finance,

Springer Berlin Heidelberg, 2010, pp. 99–132.

[19]M. Jeanblanc, M. Yor, M. Chesney, M. Jeanblanc, M. Yor, and M. Chesney,

Default risk: An enlargement of filtration approach, in Mathematical

Methods for Financial Markets, Springer Finance, Springer London, 2009,

pp. 407–456.

[20]O. Kallenberg, Foundations of Modern Probability, Springer, 1997.

[21]N. E. Karoui, M. Jeanblanc, and Y. Jiao, What happens after a

default: The conditional density approach, Stochastic Processes and their

Applications, 120 (2010), pp. 1011 – 1032.

[22]A. Kohatsu-Higa and A. Sulem, Utility maximization in an insider

influenced market, Mathematical Finance, 16 (2006), pp. 153–179.

[23]J. A. León, R. Navarro, and D. Nualart, An anticipating calculus

approach to the utility maximization of an insider, Mathematical Finance, 13

(2003), pp. 171–185.

[24]F. C. Leone, L. S. Nelson, and R. B. Nottingham, The Folded Normal

Distribution, Technometrics, 3 (1961).

[25]T. Lim and M.-C. Quenez, Exponential utility maximization in an

incomplete market with defaults, Electronic Journal of Probability, 16

(2011), pp. 1434–1464.

[26]H. Pham, Stochastic control under progressive enlargement of

filtrations and applications to multiple defaults risk management,

Stochastic Processes and their Applications, 120 (2010), pp. 1795–1820.

[27]P. Protter, Stochastic Integration and Differential Equations,

Springer, 2005.

Version 2.1.

[28]F. Russo and P. Vallois, Elements of stochastic calculus via

regularization, in Séminaire de Probabilités XL, C. Donati-Martin,

M. Émery, A. Rouault, and C. Stricker, eds., vol. 1899 of Lecture Notes

in Mathematics, Springer Berlin Heidelberg, 2007, pp. 147–185.

[29]F. Russo and P. Valois, Forward, backward and symmetric stochastic

integration, Probability Theory and Related Fields, 97 (1993),

pp. 403–421.

[30], The generalized

covariation process and Itô formula, Stochastic Processes and their

Applications, 59 (1995), pp. 81–104.

[31], Stochastic calculus

with respect to continous finite quadratic variation processes, Stochastics

and Stochastics Reports, 70 (2000), pp. 1–40.