École polytechnique,

91128 Palaiseau, France.

22email: Michel.Fliess@polytechnique.edu 33institutetext: Cédric Join 44institutetext: Non-A – INRIA & CRAN (CNRS, UMR 7039),

Université de Lorraine,

BP 239,

54506 Vandoeuvre-lès-Nancy, France.

44email: cedric.join@univ-lorraine.fr 55institutetext: M.F. & C.J. 66institutetext: AL.I.E.N. (ALgèbre pour Identification & Estimation Numériques) S.A.S.,

24-30 rue Lionnois, BP 60120, 54003 Nancy, France.

66email: {michel.fliess, cedric.join}@alien-sas.com

Systematic and multifactor risk models revisited

Abstract

Systematic and multifactor risk models are revisited via methods which were already successfully developed in signal processing and in automatic control. The results, which bypass the usual criticisms on those risk modeling, are illustrated by several successful computer experiments.

1 Introduction

Systematic, or market, risk is one of the most studied risk models not only in financial engineering, but also in actuarial sciences, in business and corporate management, and in several other domains. It is associated to the beta () coefficient, which is familiar in the investment industry since Sharpe’s capital asset pricing model (CAPM) sharpe1 . The pitfalls and shortcomings of have been detailed by a number of excellent authors.111The literature questioning the validity of the beta coefficient is huge and well summarized in several textbooks (see, e.g., bodie ). A recent and remarkable paper by Tofallis tofa has been most helpful in this study. Replacing moreover time-invariant linear regressions by time-varying and/or nonlinear ones does not seem to improve this situation.222See, e.g., adrian ; ter , and the references therein. The model-free standpoint advocated in beta and douai alleviates several of the known deficiencies but unfortunately cannot be extended to multifactor risk models which became also popular after Ross’ arbitrage pricing theory (APT) ross . In order to encompass the univariate and multivariate cases, we propose here a unified definition, with the same advantages, namely a clear-cut mathematical foundation, which

-

•

bypasses clumsy statistical and/or financial assumptions,

-

•

leads to efficient computations.

Our approach is based on the following ingredients:

- •

-

•

Classic mathematical tools like the Wronski determinants ince .

-

•

We employ recent estimation and identification techniques333The use of advanced theory stemming from signal analysis is not new in finance. See, e.g., gen . sira1 ; sira2 , which are stemming from control theory and signal processing where they have been utilized quite successfully.444See, e.g., bruit ; shannon ; abrupt ; diag ; nl ; mexico ; mboup1 ; mboup2 ; trap1 ; trap2 ; trap3 ; ushi , and the references therein.

From a more practical standpoint, our main result is the derivation of two independent coefficients, the first one for the comparison between returns and the second one for the comparison between volatilities. It implies among other consequences that the importance of the popular coefficient might vanish.

Our paper is organized as follows. After a short review of the Cartier-Perrin theorem, Section 2 details the new mathematical definitions of the coefficients and , and of alone. Section 3 develops the comparison with the classical settings. Computer illustrations are provided in Section 4.

Future publications will be exploiting the above advances in at least three directions:

-

1.

The extension of Section 3.3 to skewness and kurtosis should be straightforward. Our understanding, which would not rely exclusively any more on “Gaussianism”, of the respective behaviors of various assets might therefore be quite enhanced.

- 2.

- 3.

2 Theoretical background

2.1 A short review on time series via nonstandard analysis

Take the time interval and introduce as often in nonstandard analysis the infinitesimal sampling

where , , is infinitesimal, i.e., “very small”.555See, e.g., diener1 ; diener2 for basics in nonstandard analysis. A time series is a function .

The Lebesgue measure on is the function defined on by . The measure of any interval , , is its length . The integral over of the time series is the sum

is said to be -integrable if, and only if, for any interval the integral is limited, i.e. not infinitely large, and, if is infinitesimal, also infinitesimal.

is -continuous at if, and only if, when .666 means that is infinitesimal. is said to be almost continuous if, and only if, it is -continuous on , where is a rare subset.777The set is said to be rare cartier if, for any standard real number , there exists an internal set such that . is Lebesgue integrable if, and only if, it is -integrable and almost continuous.

A time series is said to be quickly fluctuating, or oscillating, if, and only if, it is -integrable and is infinitesimal for any quadrable subset.888A set is quadrable cartier if its boundary is rare.

2.2 Multivariate factors

Arithmetical average

Assume that is -integrable. Take a quadrable set such that is appreciable, i.e., non-infinitesimal. The arithmetical average of on , which is written , is defined by

It follows at once from Equation (1) that the difference between and is infinitesimal, i.e.,

In practice, is a time interval , with an appreciable length . Set, if ,

| (2) |

Introduce

| (3) |

It corresponds via the classic Cauchy formula to an iterated integral of order (see, e.g., folland ). Note that .

2.3 Alpha and betas

Take -integrable time series . Assume, without any loss of generality, that their values at any is bounded by a given limited number. Set

, , , are not yet uniquely determined.

Define the time series , . Its arithmetical average is always . Equation (3) yields

Introduce the Wronskian-like determinant (see, e.g., ince )

| (4) |

are said to be -W-independent on if, and only if, is appreciable.

Introduce the matrix

| (5) |

Assume that are -W-independent on . Then the matrix (5) is of rank . The Cramer rule yields limited values for , , …, in Equation (2.3):

…

Remark 2

Replacing in Equation (2.3) the arithmetic averages by the original time series yields

where is infinitesimal.

2.4 Betas alone

Let us drop . Equation (2.3) becomes

| (6) |

Determinant (4) is replaced by

are said to be W-independent on if, and only if, is appreciable. Matrix (5) is replaced by the matrix

Assume that are W-independent on . Then is of rank . Limited values for , are again given by the Cramer rule. Although we do not give again the formulae, it goes without saying that these numerical values are in general different from those derived in Sect. 2.3. We do not repeat also Remark 2.

Remark 3

If and ,

| (7) |

3 Comments

3.1 The model-free standpoint

The length of the time window may be chosen quite short, i.e., of a size compatible with what is needed for calculating the trends in fes . Updating the various factors is achieved by letting slide this time window. Let us emphasize that the linearity of the local models (2.3) and (6), which are valid only during a short time interval, does not imply therefore a global time-invariant linearity as assumed in the CAPM and APT settings. This model-free standpoint has already been proved to be quite efficient in control theory.101010See ijc13 . Many successful concrete engineering applications may be found in the references.

3.2 Reverse formula

Take for simplicity’s sake in Equation (2.3). Then

yields, if ,

The same reverse formula would have also been derived from the linear algebra of Section 2.4.

Now, we restrict ourselves for simplicity’s sake to a CAPM-like equation

| (8) |

where

-

•

and are the values at time of some returns,

-

•

is a zero-mean stochastic processes,

-

•

and are constant.

As pointed out in tofa , the classic least square techniques utilized with Equation (8) do not lead to the most natural reverse formula.

3.3 Volatility

Today’s situation

Consider again Equation (8). This global linear time-invariant equation leads to usual systematic, or market, risk calculation, i.e, to

| (9) |

where should be “small” if there is a “good” diversification. It explains

-

1.

why increasing also increases the risk,

-

2.

the importance of generating a “good” in Equation (8).

If, as emphasized in tofa , Equation (8) does not hold, i.e., there is no global linear time-invariant relationship, Equation (9) is then erroneous. The whole “philosophy” which was built in order to justify the utilization of the CAPM and of its extensions like the APT (see, e.g., bodie ) might therefore break down.111111See also the harsh quotations and comments in bernstein .

A remedy

We start by reviewing the definitions of (co)variances and volatility given in douai ; agadir . Take two -integrable time series , such that their squares and the squares of and are also -integrable. Then the following property is obvious: , , , , are all -integrable. Assume moreover that and are differentiable in the following sense: there exist two Lebesgue integrable time series , such that, , with the possible exception of a limited number of values of , , . Integrating by parts shows that the products and are quickly fluctuating.

Remark 6

Let us emphasize that the product is not necessarily quickly fluctuating.

The following definitions are natural:

-

1.

The covariance of two time series and is

-

2.

The variance of the time series is

-

3.

The volatility of is the corresponding standard deviation

(10)

The definition of volatility given by Equation (10) associates to a time series another time series , which is called the volatility time series. Take now time series , , …, , which satisfy the above assumptions on integrability and differentiability. We may repeat for the time series , , …, the same calculations as in Sections 2.3 and 2.4. It yields new relations between those volatilities.

Remark 7

Take as in the CAPM setting. We now have two time-varying betas for comparing the two assets:

- 1.

- 2.

4 Some computer experiments

4.1 Monovariate

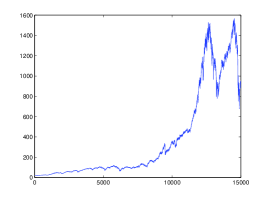

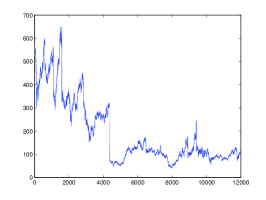

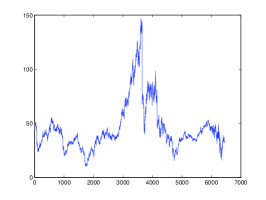

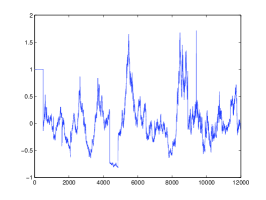

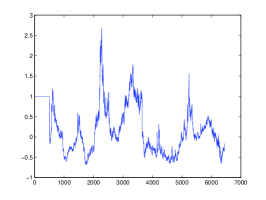

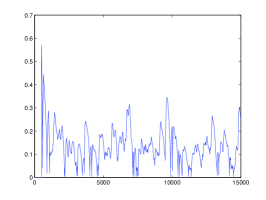

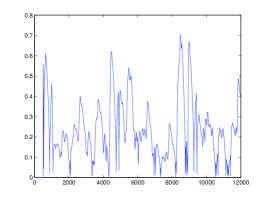

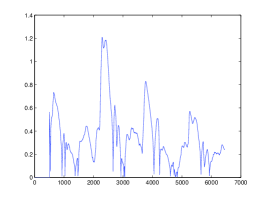

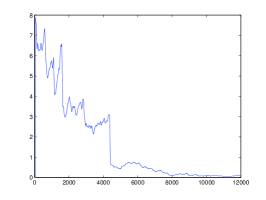

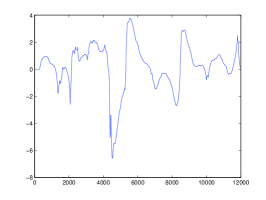

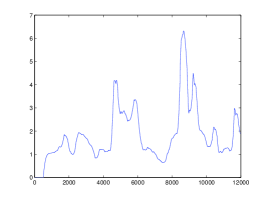

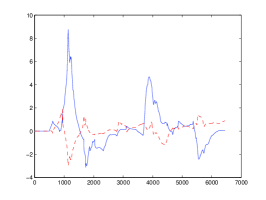

Figures 1-(a), 1-(b), 1-(c) exhibit the daily time series behaviors of the the S&P 500 and of the two following assets:

-

1.

IBM from 1962-01-02 until 2009-07-21 (11776 days),

-

2.

JPMORGAN CHASE (JPM) from 1983-12-30 until 2009-07-21 (6267 days).

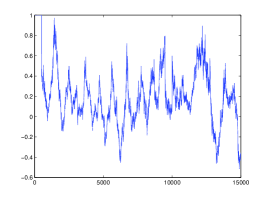

The corresponding returns are given in Figures 2-(a), 2-(b), 2-(c) and their volatilities in Figures 3-(a), 3-(b), 3-(c). We took for the length of the sliding windows.

Compare, as in Section 2.4, i.e., without , those various assets.

4.2 Bivariate

A bivariate extension is provided by a rather academic example where we want to “explain” the S&P 500 via IBM and JPM. Set therefore

where (resp. , ) is the return of S&P 500 (resp. IBM, JPM). According to Section 2.4 we have to invert the determinant of the matrix

Several sizes for the sliding windows are utilized in parallel in order, if , to pick up the size where is the greatest. Figure 4-(d) exhibits quite convincing results.

References

- (1) Adrian, T., Franzoni, F.: Learning about beta: Time-varying factor loadings, expected returns, and the conditional CAPM. J. Empirical Finance, vol. 16, pp. 537-556, 2009.

- (2) Béchu, T., Bertrand, E., Nebenzahl, J.: L’analyse technique ( éd.). Economica, 2008.

- (3) Bernstein, P.L.: Capital Ideas Evolving. Wiley, 2007.

- (4) Bodie, Z., Kane, A., Marcus, A.J.: Investments (7th ed.). McGraw-Hill, 2008.

- (5) Cartier, P., Perrin, Y.: Integration over finite sets. In F. & M. Diener (Eds): Nonstandard Analysis in Practice, pp. 195-204. Springer, 1995.

- (6) Diener, F., Diener, M.: Tutorial. In F. & M. Diener (Eds): Nonstandard Analysis in Practice, pp. 1-21. Springer, 1995.

- (7) Diener, F., Reeb, G.: Analyse non standard. Hermann, 1989.

- (8) Fliess, M.: Analyse non standard du bruit. C.R. Acad. Sci. Paris Ser. I, vol. 342, pp. 797-802, 2006.

-

(9)

Fliess, M.:

Critique du rapport signal à bruit en communications numériques. ARIMA,

vol. 9, pp. 419-429, 2008 (available at

http//hal.archives-ouvertes.fr/inria-00311719/en/). -

(10)

Fliess, M., Join, C.:

A mathematical proof of the existence of trends

in financial time series. In A. El Jai, L. Afifi, E. Zerrik (Eds):

Systems Theory: Modeling, Analysis and Control, , pp.

43-62. Presses Universitaires de Perpignan, 2009 (available at

http//hal.archives-ouvertes.fr/inria-00352834/en/). -

(11)

Fliess, M., Join, C.:

Systematic risk analysis:

first steps towards a new definition of beta. COGIS, Paris,

2009 (available at

http//hal.archives-ouvertes.fr/inria-00425077/en/). -

(12)

Fliess, M., Join, C.:

Preliminary remarks on option pricing and dynamic hedging. 1st Internat. Conf. Syst. Comput. Sci. , Villeneuve-d’Ascq, 2012 (available at

http//hal.archives-ouvertes.fr/hal-00705373/en). -

(13)

Fliess, M., Join, C.

Model-free control.

Internat. J. Control, vol. 86, pp. 2228-2252, 2013 (available at

http://hal.archives-ouvertes.fr/hal-00828135/en/). -

(14)

Fliess, M., Join, C., Hatt, F.:

Volatility made observable at last. 3es J. Identif. Modélisation Expérimentale,

Douai, 2011 (available at

http//hal.archives-ouvertes.fr/hal-00562488/en/). - (15) Fliess, M., Join, C., Hatt, F.: A-t-on vraiment besoin de modèles probabilistes en ingénierie financière? Conf. médit. ingénierie sûre systèmes complexes, Agadir, 2011 (available at http//hal.archives-ouvertes.fr/hal-00585152/en/).

- (16) Fliess, M., Join, C., Mboup, M.: Algebraic change-point detection. Applicable Algebra Engin. Communic. Comput., vol. 21, pp. 131-143, 2010.

- (17) Fliess, M., Join, C., Sira-Ramírez, H.: Residual generation for linear fault diagnosis: an algebraic setting with examples. Internat. J. Control, vol. 77, pp. 1223-1242, 2004.

-

(18)

Fliess, M., Join, C., Sira-Ramírez, H.:

Non-linear estimation is easy. Int. J. Model. Identif.

Control, vol. 4, pp. 12-27, 2008 (available at

http://hal.archives-ouvertes.fr/inria-00158855/en/). -

(19)

Fliess, M., Mboup, M., Mounier, H., Sira-Ramírez, H.:

Questioning some paradigms of signal processing via concrete examples. In H.

Sira-Ramírez, G. Silva-Navarro (Eds.): Algebraic Methods in

Flatness, Signal Processing and State Estimation, pp. 1-21,

Editiorial Lagares, 2003 (available at

http://hal.archives-ouvertes.fr/inria-00001059/en/). - (20) Fliess, M., Sira-Ramírez, H.: An algebraic framework for linear identification. ESAIM Control Optimiz. Calc. Variat., vol. 9, pp. 151–168, 2003.

- (21) Fliess, M., Sira-Ramírez, H.: Closed-loop parametric identification for continuous-time linear systems via new algebraic techniques. In H. Garnier, L. Wang (Eds): Identification of Continuous-time Models from Sampled Data, pp. 362-391. Springer, 2008.

- (22) Folland, G.B.: Advanced Calculus, Prentice Hall, 2002.

- (23) Gençay, R., Selçuk, F., Whitcher, B.: An Introduction to Wavelets and Other Filtering Methods in Finance and Economics. Academic Press, 2002.

- (24) Ince, E.L.: Ordinary Differential Equations. Longmans-Green, 1926.

- (25) Kirkpatrick, C.D., Dahlquist, J.R.: Technical Analysis: The Complete Resource for Financial Market Technicians (2nd ed.). FT Press, 2010.

- (26) Lobry, C., Sari, T.: Nonstandard analysis and representation of reality. Internat. J. Control, vol. 81, pp. 517-534, 2008.

- (27) Mboup, M.: Parameter estimation for signals described by differential equations. Applicable Analysis, vol. 88, pp. 29-52, 2009.

- (28) Mboup, M., Join, C., Fliess, M.: Numerical differentiation with annihilators in noisy environment. Numer. Algor., vol. 50, pp. 439-467, 2009.

- (29) Ross, S.: The arbitrage theory of capital asset pricing. J. Economic Theory, vol. 13, pp. 341-360, 1976.

- (30) Sharpe, W.F.: Capital asset prices: A theory of market equilibrium under conditions of risk. J. Finance, vol. 19, pp. 425-442, 1964.

- (31) Teräsvirta, T.: Forecasting economic variables with nonlinear models. In G. Elliott, C.W.J. Granger, A. Timmermann (Eds): Handbook of Economic Forecasting, vol. 1, pp. 413-457. North-Holland, 2006.

- (32) Tofallis, C.: Investment volatility: A critique of standard beta estimation and a simple way forward. Europ. J. Operat. Res., vol. 187, pp. 1358-1367, 2008.

- (33) Trapero, J.R., Sira-Ramírez, H., Feliu Battle, V.: An algebraic frequency estimator for a biased and noisy sinusoidal signal. Signal Processing, vol. 87, pp. 1188-1201, 2007.

- (34) Trapero, J.R., Sira-Ramírez, H., Feliu Battle, V.: A fast on-line frequency estimator of lightly damped vibrations in flexible structures. J. Sound Vibration, vol. 307 pp. 365-378, 2007.

- (35) Trapero, J.R., Sira-Ramírez, H., Feliu Battle, V.: On the algebraic identification of the frequencies, amplitudes and phases of two sinusoidal signals from their noisy sums. Internat. J. Control, vol. 81, pp. 505-516, 2008.

-

(36)

Ushirobira, R., Perruquetti, W., Mboup, M., Fliess, M.:

Algebraic parameter estimation of a biased sinusoidal waveform

signal from noisy data. 16th IFAC Symp. System

Identif., Brussels, 2012 (available at

http//hal.archives-ouvertes.fr/hal-00685067/en/).