Nonparametric Identification in Panels using Quantiles ††thanks: We thank the editor Qi Li, two anonymous referees, participants at Demand

Estimation and Modelling Conference, and Arthur Lewbel for comments. We

gratefully acknowledge research support from the NSF.

Victor Chernozhukov, Ivan Fernandez-Val, Stefan Hoderlein,

Hajo Holzmann, Whitney Newey

Abstract

This paper considers identification and estimation of ceteris paribus

effects of continuous regressors in nonseparable panel models with time

homogeneity. The effects of interest are derivatives of the average and

quantile structural functions of the model. We find that these derivatives

are identified with two time periods for “stayers”, i.e. for individuals

with the same regressor values in two time periods. We show that the

identification results carry over to models that allow location and scale

time effects. We propose nonparametric series methods and a weighted

bootstrap scheme to estimate and make inference on the identified effects.

The bootstrap proposed allows uniform inference for function-valued

parameters such as quantile effects uniformly over a region of

quantile indices and/or regressor values. An empirical application to Engel curve estimation with panel data

illustrates the results.

Keywords: Panel data, nonseparable model, average effect, quantile

effect, Engel curve

1 Identification for Panel Regression

A frequent object of interest is the ceteris paribus effect of on

when observed is an individual choice variable partly determined by

preferences or technology. Panel data holds out the hope of controlling for

individual preferences or technology by using multiple observations for a

single economic agent. This hope is particularly difficult to realize with

discrete or other nonseparable models and/or multidimensional individual

effects. These models are, by nature, not additively separable in unobserved

individual effects, making them challenging to identify and estimate.

A fundamental idea for using panel data to identify the ceteris paribus

effect of on is to use changes in over time. In order for

changes over time in to correspond to ceteris paribus effects, the

distribution of variables other than must not vary over time. This

restriction is like “time being randomly

assigned” or ”time is an instrument.” In this paper we

consider identification via such time homogeneity conditions. They are also

the basis of many previous panel results, including Chamberlain (1982),

Manski (1987), and Honore (1992). Recently time homogeneity has been used as

the basis for identification and estimation of nonseparable models by

Chernozhukov, Fernandez-Val, Hahn, Newey (2013), Evdokimov (2010), Graham

and Powell (2012), and Hoderlein and White (2012). Because economic data

often exhibits drift over time, we also allow for some time effects, while

maintaining underlying time homogeneity conditions.

In this paper we give identification and estimation results for quantile

effects with time homogeneity and continuous regressors. The effects of

interest are derivatives of quantile structural functions of the model. We

find that these derivatives are identified with two time periods for

“stayers”, i.e. conditional on being equal in two time

periods. Time homogeneity is too strong for many econometric applications

where time trends are evident in the data. We weaken homogeneity by allowing

for location and scale time effects. Allowing for such time effects makes

identification and estimation more complicated but more widely applicable.

We also give analogous results for conditional mean effects under weaker

identification conditions than previously.

Quantile identification under time homogeneity is based on differences of

quantiles. It is also interesting to consider whether quantiles of

differences can help identify effects of interest. We do not find that time

homogeneity alone can lead to identification from quantiles of differences.

We do give quantile difference identification results that restrict the

distribution of individual effects conditional on , similarly to

Chamberlain (1980), Altonji and Matzkin (2005), and Bester and Hansen

(2009). In our opinion these added restrictions make quantiles of

differences less appealing. We therefore focus for the rest of the paper,

including the application, on differences of quantiles.

To illustrate we provide an application to Engel curve estimation. The Engel

curve describes how demand changes with expenditure. We use data from the

2007 and 2009 waves of the Panel Study of Income Dynamics (PSID).

Endogeneity in the estimation of Engel curves arises because the decision to

consume a commodity may occur simultaneously with the allocation of income

between consumption and savings. In contrast with the previous cross

sectional literature, we do not rely on a two-stage budgeting argument that

justifies the use of labor income as an instrument for expenditure. Instead,

we assume that the Engel curve relationships are time homogeneous up to

location and scale time effects, which leads to identification of structural

effects from panel data.

An alternative approach to identification in panel data is to impose

restrictions on the conditional distribution of the individual effect given . This approach leads to nonparametric generalizations of Chamberlain’s

(1980) correlated random effects model. As shown by Chamberlain (1984),

Altonji and Matzkin (2005), Bester and Hansen (2009), and others, this kind

of condition leads to identification of various effects. In particular,

Altonji and Matzkin (2005) show identification of an average derivative

conditional on the regressor equal to a specific value, an effect they call

the local average response (LAR). In this paper we take a different

approach, preferring to impose time homogeneity rather than restrict the

relationship between observed regressors and unobserved individual effects.

We refer to Hsiao (2003) for a broader perspective of panel data models.

Section 2 describes the model and gives an average derivative result.

Section 3 gives the quantile identification result that follows from time

homogeneity. Section 4 considers how quantiles of differences can be used to

identify the effect of on . Section 5 explains how we allow for time

effects. Estimation and inference are briefly discussed in Section 6, and

the empirical example is given in Section 7. The Appendix contains the

proofs of the main results.

2 The Model and Conditional Mean Effects

The data consist of observations on and , for a dependent variable and

a vector of regressors . Throughout we assume that the observations , , are independent and identically distributed. The nonparametric

models we consider satisfy

Assumption 1.

There is a function and vectors of random

variables and such that

We focus in this paper on the two time period case, , though it is

straightforward to extend the results to many time periods. The vector consists of time invariant individual effects that often represent

individual heterogeneity. The vector represents period specific

disturbances. Altonji and Matzkin (2005) considered models satisfying

Assumption 1. As discussed in Chernozhukov et. al. (2013), the invariance of

over time in this Assumption does not actually impose any time

homogeneity. If there are no restrictions on then could be one

of the components of allowing the function to vary over time in a

completely general way. The next condition together with Assumption 1

imposes time homogeneity on the model.

Assumption 2.

for all

This is a static, or ”strictly exogenous” time homogeneity condition, where

all leads and lags of the regressor are included in the conditioning

variable It requires that the conditional

distribution of given and does not

depend on but does allow for dependence of over time. This

assumption rules out dynamic models where lagged values of are

included in

Setting , an equivalent

condition is

Thus, the time invariant has no distinct role in this model. As

further discussed in Chernozhukov et. al. (2013), this seems a basic

condition that helps panel data provide information about the effect of

on It is like the time period being ”randomly assigned” or ”time is an

instrument,” with the distribution of factors other than not varying

over time, so that changes in over time can help identify the effect of on .

Although they seem useful for nonlinear models, the time homogeneity

conditions are strong. In particular they do not allow for

heteroskedasticity over time, which is often thought to be important in

applications. We partially address this problem below by allowing for

location and scale time effects.

For notational convenience we shall drop the subscript and let in

the following. Our focus in this paper is on the case where the regressors are continuously distributed. We will be interested in

several effects of on . For we let . We

will let or denote a possible value of the regressor vector and a

possible value of . Let denote the vector of partial

derivatives of w.r.t. the coordinates of . One effect we consider

is a conditional expectation of the derivative given by

This is the object considered in Hoderlein and White (2012) and is similar

to the local average response considered in Altonji and Matzkin (2005). It

gives the local marginal effect for individuals with regressor value in

both periods. This effect is related to the conditional average structural

function (CASF):

through

under the conditions that permit interchanging the derivative and

expectation.

The other effects we consider are similar to this effect except that we also

condition on certain values of . One of these is given by

where is the conditional quantile of given This is a quantile derivative effect,

similar to the local average structural derivative in Hoderlein and Mammen

(2007). It gives the local marginal effect for individuals with regressor

value in both periods and at the quantile . This effect is

also related to the conditional quantile structural function (CQSF), , that gives the -quantile of conditional on through

We also consider linking quantiles of arbitrary linear combinations of the

dependent variables and to conditional expectations of the

form

These are dependent variable conditioned average effects. One intended

direction is to compare the derivative of the quantiles of the differences to the differences of the derivative of the quantiles of

and in terms of objects they identify. In what follows we carry out the comparison.

To set the stage for the quantile results we first discuss mean

identification. We first give an explanation of identification of the mean

effect and then give a precise result with regularity conditions.

Consider the identified conditional mean

Together these conditional expectations are a nonparametric version of

Chamberlain’s (1982) multivariate regression model for panel data.

Derivatives of them can be combined to identify the conditional mean effect.

Let denote the conditional density of given that does not depend on by

Assumption 2. Assume that and are differentiable in and

respectively and that differentiation under the integral is permitted. For we let and , , denote the vector of partial derivatives

w.r.t. the coordinates of . Then for ,

where the first term is the conditional mean effect of interest and the

second term is the analog to Chamberlain’s (1982) heterogeneity bias.

Subtracting and using Assumption 2 gives

(2.1)

Evaluating at we find

that

(2.2)

where

It also follows similarly that

(2.3)

Thus, the conditional mean effect is identified from the derivative of the

conditional expectation of the difference with respect to the leading time

period for individuals where is the same in both periods. We note

here that this means the conditional mean effect is overidentified.

Introducting time effects, as we do below, will lead to exact

identification. Thus, testing for the presence of time effects is one way of

testing this overidentifying restriction.

The importance of conditioning on the event can be seen from

equation (2.1), where setting eliminates

heterogeneity bias. Thus, one can think of the conditioning on

as a device to eliminate the heterogenity bias in nonseparable models under

time stationarity. In contrast, if were additively separable

with the heterogeneity bias would be zero for all not necessarily equal to because . Hence the derivative effect of interest would be for each value of and one

could estimate that derivative more precisely by averaging over its first

argument. Also, one could test for whether the model is additively separable

by testing whether varies with its first

argument, though it is beyond the scope of this paper to analyze such tests.

Conditioning on does restrict the set over which the

structural derivative is averaged but this can correspond to an interesting

set of individuals. For example, in the Engel curve application we give

is total expenditure so the restriction corresponds to

individuals whose total expenditure was the same in the two time periods.

This seems mostly likely to occur for middle aged individuals, which is an

interesting though special group to focus on.

Altonji and Matzkin (2005) are able to identify derivative effects without

conditioning on but they also restrict the distribution of conditional on We do not impose such type of

assumptions but instead require time stationarity of the distribution of conditional on . The different assumptions make it

hard to compare results. We prefer to focus on time stationarity in this

paper, where we do not yet know whether it is possible to identify

interesting effects for continuous regressors without imposing

Graham and Powell (2012) consider a linear model with individual specific

coefficients where in the scalar case. In this case

Here we find that average slope for the stayer subpopulation with is identified. Graham and Powell (2012) use linearity of in to identify the average slope

over the whole population using the movers with . We

identify an average slope over a smaller population for a fully nonlinear,

nonparametric specification .

The following result makes the previous derivation precise, including

conditions for differentiating under integrals.

Theorem 1.

Suppose that Assumptions 1 and 2 are satisfied, , and that (where ) resp. the

conditional density of given are

continuously differentiable in resp. for fixed .

Given , suppose that for some ,

This result has slightly weaker conditions than that of Hoderlein and White

(2012). Here we drop their assumption that is independent of

conditional on . The result given here allows for to be

correlated with as long as the marginal distribution of conditional on does not vary with We maintain

these weaker conditions as we consider identification of quantile effects in

the next Section.

3 Conditional Quantile Effects

Turning now to the identification of the quantile effects given above, let denote the conditional

quantile of conditional on . It will be the solution to

The pair

is a quantile analog of Chamberlain’s (1982) multivariate regression for

panel data. We can identify a quantile analog of the Hoderlein and White

(2012) average derivative effect. We first describe how these multivariate

panel quantiles can be used to identify an average derivative effect, then

give a precise interpretation of the effect. This description helps explain

the source of identification as well as the precise nature of the identified

effect.

To describe how identification works, differentiate both sides of the

previous identity with respect to , treat the derivative of an

indicator function as a dirac delta, and assume the order of differentiation

and integration can be interchanged. This calculation gives

Let and note that

Solving for we find that,

Note that at , and by time

homogeneity. Then differencing the conditional quantile derivatives gives

(3.1)

where the last term does not depend on due to time homogeneity. The

equation (3.1) is a panel version of the Hoderlein and

Mammen (2007) identification result. It is interesting to note that, unlike

in the mean case, differences of derivatives of quantiles generally differ

from derivatives of quantiles of differences. Below we will consider

identification from derivatives of quantiles of differences.

To make the above derivation precise we need to formulate conditions that

allow differentiation under the integral. The following regularity condition

is one approach to this, in particular for the dirac delta argument given

above.

Assumption 3.

We can write for

scalar , such that is continuously

differentiable in and and there is with and

everywhere. For the corresponding representation of the random vector , is continuously distributed given with conditional pdf that

is bounded and continuous in and , the conditional pdf of given ,

is continuous in . Moreover, given

there is a such that

(3.2)

The boundedness conditions on the derivatives of could further

be weakened at the expense of much more complicated notation and conditions.

For fixed let denote

the conditional pdf of given The following

lemma shows differentiability of with respect to and for given , and computes the derivatives.

Lemma 1.

If Assumption 3 is satisfied

then for fixed , is differentiable in and with derivatives

continuous in , and given by

where .

With this result in hand we can now make precise the quantile effect

sketched above.

Theorem 2.

If Assumptions 1 - 3 are satisfied, is continuously

differentiable in ,

(3.3)

and the conditional density of given is positive on

the interior of its support then for all exists and is continuously differentiable such that (3.1) holds true.

To illustrate the previous result, consider the familiar linear model with

additive heterogeneity where Let denote the

linear -quantile regression on a

quantile version of the panel multivariate regression of Chamberlain (1982).

Under time homogeneity

where and do not depend on . Taking

derivatives and differencing over time, for

Here the result holds for sequences with

because the heterogeneity is additive.

4 Quantiles of Transformations of the Dependent Variables

In this section we answer the question whether we can relate quantiles of

the first difference of the dependent variable to causal effects. In fact,

the same arguments and assumptions that are used for first differences can

also be employed for arbitrary functions of the dependent variables which

map the -vector of dependent variables (in our case

for simplicity ) into a scalar “index”. However, as it

turns out, if we restrict ourselves to using only two time periods of the

covariates , we have to strengthen the assumptions significantly to

make statements about causal effects. This is related to the fact that we do

not have an auxiliary equation at our disposal that allows us to correct for

the heterogeneity bias that arose from the correlation of and

To be more specific about the assumptions: While still considering the model

specified in Assumption 1, instead of time homogeneity

assumption 2, in this section we shall use independence

assumptions.

Assumption 4.

1.

2.

is independent of

The first part of this assumption states that the transitory error component

is independent of covariates, given the persistent fixed effect, which is a

notion of strict exogeneity. The second part of this assumption is more

restrictive as it rules out the case where is arbitrarily correlated

with the process. This is a special case of the sufficient statistic

type assumptions in Altonji and Matzkin (2005). Assumption 2

does not restrict the relationship between and and allows for

and to be correlated, but it is not formally nested within Assumption 4. To see this, consider the example of the panel

multivariate quantile regression in the additive linear model of Section 3. Without time homogeneity,

Assumption 2 imposes time homogeneity on the coefficients,

i.e., and whereas Assumption 4 imposes the

exclusion restrictions and but

lets vary with . In our view these exclusion

restrictions are stronger than time homogeneity in most economic

applications.

To adopt a similar framework as above, we rewrite

and note that the independence and strict exogeneity assumptions imply that:

Thus, the conditional distribution of given does not depend on , proving conditional independence.

∎

As already mentioned above, we consider now quantiles of differences and

other transformations of the dependent variables. To this end, let be an arbitrary (differentiable) function and note that

(4.1)

so that for , we have that . Denote

by the conditional quantile of

given , so that

For convenience, we first formulate and prove a result along the lines of

Hoderlein and Mammen (2007) for a general model of the form

(4.2)

in terms of regularity assumptions similar to Assumption 3, and then specialize it to (4.1).

Assumption 5.

Suppose that in the model (4.2),

we can write for scalar ,

such that is

continuously differentiable in and . Moreover, for fixed

there is a (possibly depending on ) with and for all

and . For the corresponding representation of the random

vector , is absolutely continuously distributed

given with conditional pdf that is bounded

and continuous in and the conditional distribution of given

is absolutely continuous with pdf .

These assumptions are by and large regularity conditions, akin to those

employed in Hoderlein and Mammen (2007), e.g., differentiability conditions.

They do not restrict the model significantly, and we therefore do not

discuss them at length. Together with the independence condition, they allow

us to establish an extension to the Hoderlein and Mammen (2007) result:

Proposition 1.

Suppose that in the model (4.2), is conditionally independent of given ,

that Assumption 5 is satisfied and that the conditional

pdf of given and is positive in the interior of its

support. Then for every , the conditional quantile of given , exists and is

continuously differentiable with

(4.3)

We now specialize this general result to the setup of this paper, and

discuss it below in this specialized setup. To this end, we modify the

regularity conditions accordingly:

Assumption 6.

Suppose that in the model (4.2), is continuously partially differentiable in

with for all for some . Further, assume that we can write for scalar , such that is continuously differentiable in and and such that

there is a with and for all . For the corresponding

representation of the random vector , is absolutely

continuously distributed given with conditional pdf

that is bounded and continuous in and the conditional distribution of given is absolutely continuous.

These preliminaries lead to the expected corollary:

Corollary 3.

Suppose that in (4.1), Assumptions 1, 4 and 6 are satisfied, and that

the conditional density of given is

positive in the interior of its support. Then (4.3)

holds true.

This result is very similar in spirit to the results in the previous

section, again an LAR for a subpopulation (or a derivative for an ASF) is

identified. The advantage, however, is now that we can look at

subpopulations that are characterized by arbitrary combinations of

and . If we confine ourselves to linear combinations, i.e., we can consider conditioning on arbitrary weights

. Since we can vary freely, this means that

we can use the entire joint distribution in the sense of the Cramer-Wold

device, by looking at any linear combination, and hence use multivariate

information through repeated use of one regular regression quantiles. It

allows to construct subpopulations where we put different weights on the

outcome in different periods. For instance, if is schooling, and

is labor income in different periods, we may think of as some

long run or average income. And when computing this long run income, we

could either discount future income stronger or emphasize it more when

characterizing the subpopulations, depending on the intention of the

researcher. Of course, one should always remember that the strength in

statements we can make always comes at the expense of the structure we

impose on the dependence between and

This result covers important special cases:

1.

The difference: . Then is the conditional quantile of the difference,

and

2.

: Here , so that

This is similar in spirit to Altonji and Matzkin (2005), just replacing

means by quantiles.

Note that the first special case answers one of the questions posed in the

introduction: should we consider the difference of the quantiles or the

quantiles of the differences, when talking about causal effects in panels.

In terms of the strength of the assumptions, the verdict has to be clearly

differences of quantiles. However, two remarks are in order: First, it also

happens to be the case that under the additional structure on the dependence

the quantiles of the difference yield a new effect that we could not have

obtained through differences in quantiles. In particular, for targeted

policy measures it may be sensible to use subpopulations that are defined

by, e.g., first differences . More precisely, since individuals

are often assumed to exhibit a pronounced loss aversion, i.e., they are more

much sensitive towards a negative change in their status than a positive, it

is conceivable that a policy maker would be much more interested in the

subpopulation for which the effect is negative. Similarly,

measures that focus on the subpopulation exhibiting large values of may be of interest, as high variance of over time may not be a

desirable feature for an individual.

Second, with more time periods we could weaken the restrictive independence

assumptions. In particular, if three periods are available and only effects

on supopulations defined by, say, first differences between two periods are

of interest, we may allow for more correlation between the unobservables and

the process, and use the third period to perform an analogous

correction as in the previous section. Since this involves a simple

combination of arguments, we do not elaborate on this further, and we still

want to point to the difference in assumptions in the two periods case.

5 Time Effects

The time homogeneity assumption is a strong one that often seems not to hold

in applications. In this section we consider one way to weaken it, by

allowing for additive location effects and multiplicative scale effects.

Allowing for such time effects leads to effects of interest being exactly

identified, unlike the overidentification we found in Sections 2 and 3.

We allow for time effects by replacing Assumption 1 with the following

condition.

Assumption 7.

There are functions and and

a vector of random variables such that

The time effects and are not separately identifiable from

without location and scale normalizations because

for , and .

In this model the effects of interest vary with time. We consider the

time-averaged conditional mean effect:

and the time-averaged conditional quantile effect:

where and is the

conditional quantile of given

The conditional mean effect is related to the time-averaged CASF:

through

under the conditions that permit interchanging the derivative and

expectation. Similarly, the conditional quantile effect is related to the

time-averaged CQSF, , that gives the -quantile of conditional on , through

Let and

Theorem 4.

Suppose that Assumptions 2 and 7 are satisfied,

and are

continuously differentiable in and the conditional density of

given is

continuously differentiable in . Given , suppose that

for some ,

Then, and

This theorem shows that the time effects are identified up to location and

scale normalizations. For example, if we set and then and . The identification of the conditional

mean effect does not require any normalization. Note that we now have just

one equation for identifying the conditional mean effect.

We find a similar result for quantiles.

Theorem 5.

Suppose that Assumptions 2 , 3 , and 7 are satisfied, and are continuously differentiable in and is continuously differentiable in ,

(5.1)

and the conditional density of given is positive on

the interior of its support. Then for all exists and is continuously differentiable at such that

and for any and such that .

As in Theorem 4, the time effects are identified up to

location and scale normalizations, whereas the conditional quantile effects

are identified without any normalization. Here, however, instead of

conditional mean and variance restrictions, we use quantile restrictions to

identify the time effects up to the normalizations. These effects are over

identified by many possible quantiles and . For example, for and

the scale is identified by a ratio of conditional interdecile ranges across

time and the location is identified by a difference of conditional medians

across time.

We note that Graham and Powell (2012) allowed for random time effects in

location and slope rather than location and scale effects that could depend

on .

6 Estimation and inference

The conditional mean and quantile effects of interest are identified by

special cases of the functionals:

and

respectively, where and are known smooth functions,

is a region of regressor values of interest, and is a region

of regressor values and quantiles of interest. We consider the estimators of

and based on the plug-in rule:

and

where , , and are nonparametric series estimators of , , and .

To describe the series estimators, let denote a vector of approximating functions, such as tensor products of

univariate polynomial or spline series terms of the components of , and let . Then,

where denotes any generalized inverse inverse of the matrix ;

is a series version of the (kernel) conditional variance estimator of Fan

and Yao (1998); and where is the Koenker and

Bassett (1978) quantile regression estimator

Following Praestgaard and Wellner (1993), Hahn (1995), and

Chamberlain and Imbens (2003), we use weighted bootstrap for inference.111See also Ma and Kosorok (2005)

and Chen and Pouzo (2009, 2013) for other applications of weighted

bootstrap; we are grateful to a referee for pointing out the latter

references. To describe this method, let be an i.i.d. sequence of nonnegative random variables

from a distribution with mean and variance equal to one (e.g., the standard

exponential distribution), independent of the data. The weighted bootstrap

uses the components of as random sampling weights in

the construction of the bootstrap version of the series estimators. Thus,

the bootstrap versions of and

are

and

where

is the bootstrap version of

is the bootstrap version of and is the bootstrap

version of , with

Belloni, Chernozhukov, Chetverikov, and Kato (2013) and Chernozhukov, Lee,

and Rosen (2013) developed functional distributional theory and bootstrap

consistency for series estimators of functionals of the conditional mean

function, and Belloni, Chernozhukov, and Fernandez-Val (2011) developed

similar theory for series estimators of functionals of the conditional

quantile function. We can use these results to construct analytical or

bootstrap confidence bands for the effects that have uniform asymptotic

coverage over regressor values and quantiles. For example, the end-point

functions of a confidence band for have the form

(6.1)

where and are consistent

estimators of the asymptotic variance function of and the quantile of the

Kolmogorov-Smirnov maximal -statistic

The following algorithm describes how to obtain uniform bands for quantile

effects using weighted bootstrap:

Algorithm 1(Uniform inference).

(i) Draw as i.i.d. realizations of

for conditional on the data. (ii) Compute a bootstrap

estimate of such as the bootstrap standard deviation: for ,

where ; or the bootstrap interquartile range of

rescaled with the normal distribution: for , where is the -sample

quantile of . (3) Compute

realizations of the bootstrap version of the maximal t-statistic for (iii) Form a -confidence band for using (6.1) setting to the -sample

quantile of . ∎

The validity of Algorithm 1 follows from the results in

Belloni, Chernozhukov, and Fernandez-Val (2011) and the delta method. We can

construct uniform bands for the conditional mean effects with a similar

algorithm replacing by , adjusting all the steps

accordingly, and relying on the results of Belloni, Chernozhukov,

Chetverikov, and Kato (2013) and Chernozhukov, Lee, and Rosen (2013).

7 Engel Curves in Panel Data

In this section, we illustrate the results with an empirical application on

estimation of Engel curves with panel data. The Engel curve relationship

describes how a household’s demand for a commodity changes as the

household’s expenditure increases. Lewbel (2006) provides a recent survey of

the extensive literature on Engel curve estimation. We use data from the

2007 and 2009 waves of the Panel Study of Income Dynamics (PSID). Since

2005, the PSID gathers information on household expenditure for different

categories of commodities. The PSID does not collect information on total

expenditure. We construct the total expenditure on nondurable goods and

services by adding all the expenses in housing, utilities, phone, child

care, food at home, food out from home, car, transportation, schooling,

clothing, leisure, and health. We exclude expenses in mortgage, home

insurance, car insurance, and health insurance because these categories have

many missing values. Our sample contains households formed by couples

without children, where the head of the household was 20 to 65 year-old in

2009, and that provided information about all the relevant categories of

expenditure in 2007 and 2009. We focus on the commodities food at home and

leisure for comparability with recent studies (e.g., Blundell, Chen, and

Kristensen (2007), Chen and Pouzo (2009, 2013), and Imbens and Newey

(2009)). The expenditure share on a commodity is constructed by dividing the

expenditure in this commodity by the total expenditure in nondurable goods

and services.

Endogeneity in the estimation of Engel curves arises because the decision to

consume a commodity may occur simultaneously with the allocation of income

between consumption and savings. In contrast with the previous cross

sectional literature, we do not rely on a two-stage budgeting argument that

justifies the use of labor income as an instrument for expenditure. Instead,

we assume that the Engel curve relationships are time homogeneous up to

location and scale time effects, and rely on the availability of panel data.

Specifically, we estimate

where is the observed share of total expenditure on food at home or

leisure, is the logarithm of total expenditure in dollars of 2005, and are location and scale time effects, is a

vector of unobserved household heterogeneity that satisfies time homogeneity

and captures both differences in preferences and idiosyncratic household

shocks, corresponds to 2007, and corresponds to 2009.222To deflate total expenditure, we use a price index for personal consumption

expenditures in nondurable goods constructed from Tables 2.4.4 and 2.4.5 of

the Bureau of Economic Analysis. The inclusion of time effects might be

important to account for temporal changes in preferences and relative prices

across commodities. For example, the price index of nondurable goods

increased by between 2007 and 2009, whereas the price indexes for food

and leisure increased by and during the same period.333Source: Tables 2.4.4.U and 2.4.5 of Bureau of Economic Analysis. We allow

these time effects to vary with total expenditure, what gives flexibility to

the model. This model does put some restrictions on interactions between

prices and heterogeneity, implying that price changes only shift the

location and scale of the distribution of demand.

Table 1 reports descriptive statistics for the variables

used in the analysis. Both total expenditure and expenditure shares display

within and between household variation, with means and standard deviations

that remain stable between 2007 and 2009. The low percentage of within

variation in expenditure indicates that there might be a substantial number

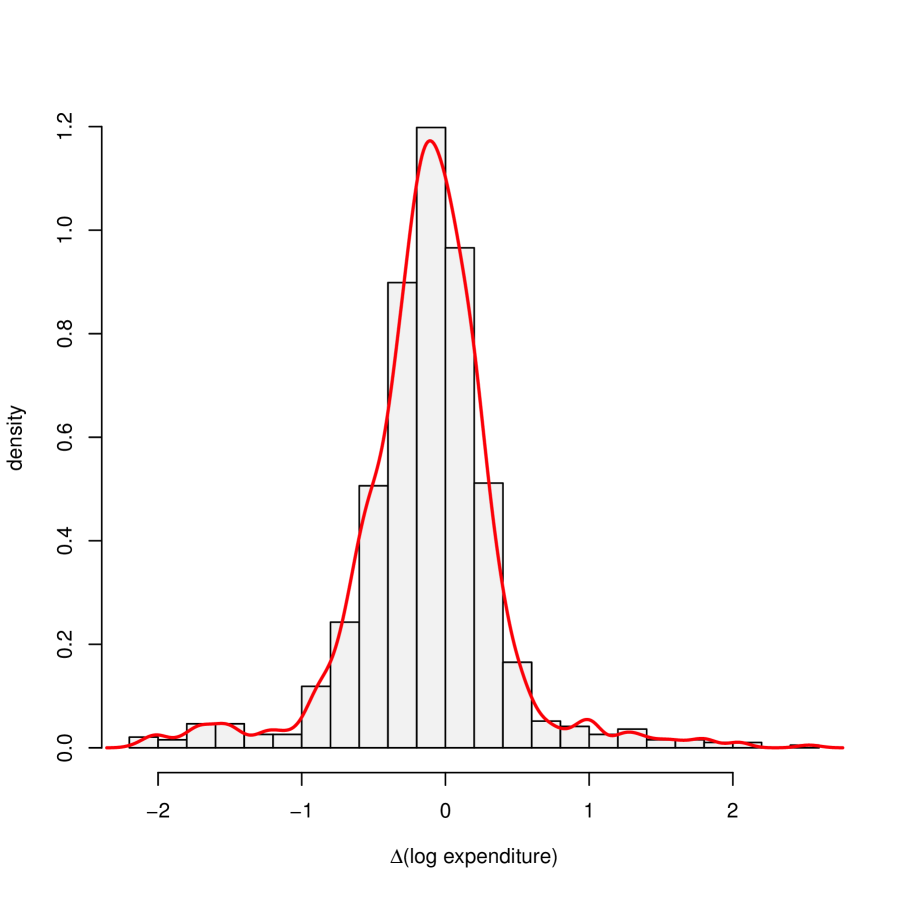

of households with zero or little change in expenditure across years. Figure 1 plots histogram and kernel estimates of the density of the

change in expenditure between 2007 and 2009. The kernel estimates are

obtained using a Gaussian kernel with Silverman’s rule of thumb for the

bandwidth. The estimates confirm that there is a high density of households

with zero change in expenditure. Our methods will identify mean and quantile

effects for these households with .

Table 1: Descriptive Statistics

Pooled sample

2007 sample

2009 sample

Variable

Mean

Std. Dev.

Within (%)

Mean

Std.

Dev.

Mean

Std. Dev.

Log expenditure

10.13

0.56

21

10.19

0.57

10.07

0.55

Food share

0.19

0.10

28

0.19

0.10

0.20

0.10

Leisure Share

0.10

0.10

26

0.10

0.09

0.10

0.10

Note: the source of the data is the PSID.

The number of observations is 968 observations for each year.

We estimate the location time effects, scale time effects, conditional mean

effects, and conditional quantile effects using sample analogs of the

expressions in Theorems 4 and 5. In

particular, we estimate the conditional expectation, variance, and quantile

functions by the nonparametric series methods described in Section 6. We consider two different specifications for the series

basis in all the estimators: a quadratic orthogonal polynomial and a cubic

B-spline with three knots at the minimum, median and maximum of total

log-expenditure in the data set. Both specifications are additively

separable in the total log-expenditures of 2007 and 2009.444We select these specifications by under smoothing with respect to the

specification selected by cross validation applied to the estimators of the

conditional expectation function.

We also compute cross sectional estimates that do not account for

endogeneity. They are obtained by averaging the nonparametric series

estimates in 2007 and 2009 that use the same specification of series basis

as the panel estimates but only condition on contemporaneous expenditure.

For inference, we construct 90% confidence bands around the estimates by

weighted bootstrap with exponential weights and 499 repetitions. These bands

are uniform in that they cover the entire function of interest with 90%

probability asymptotically.

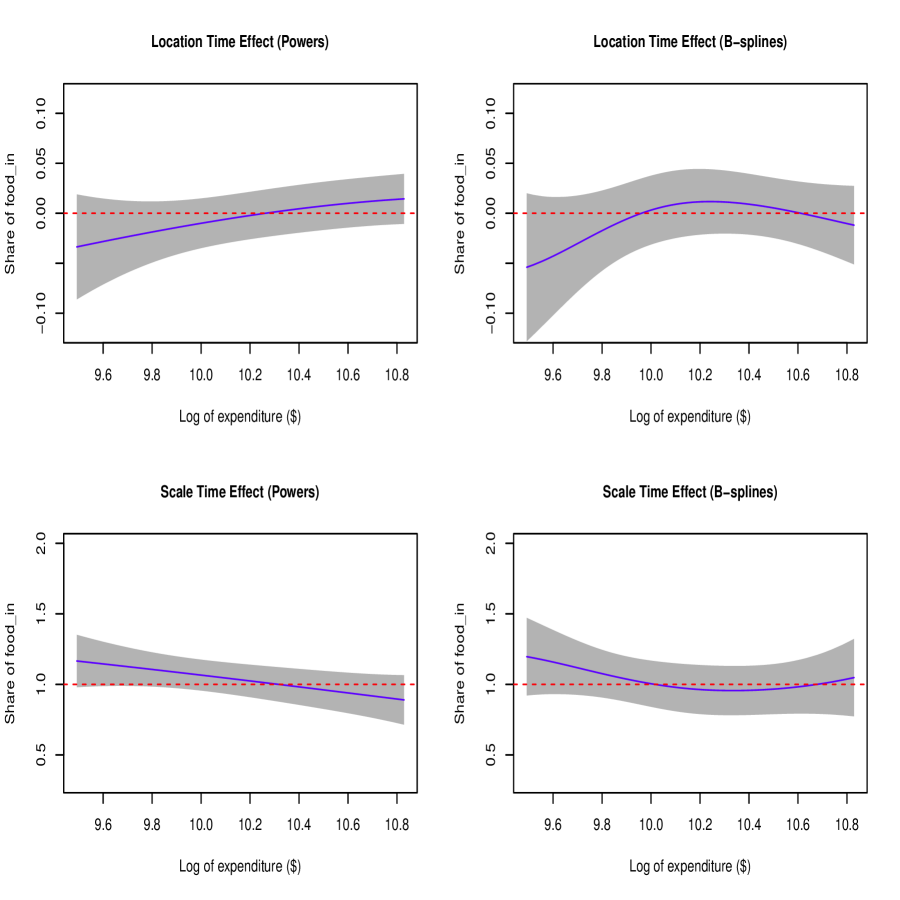

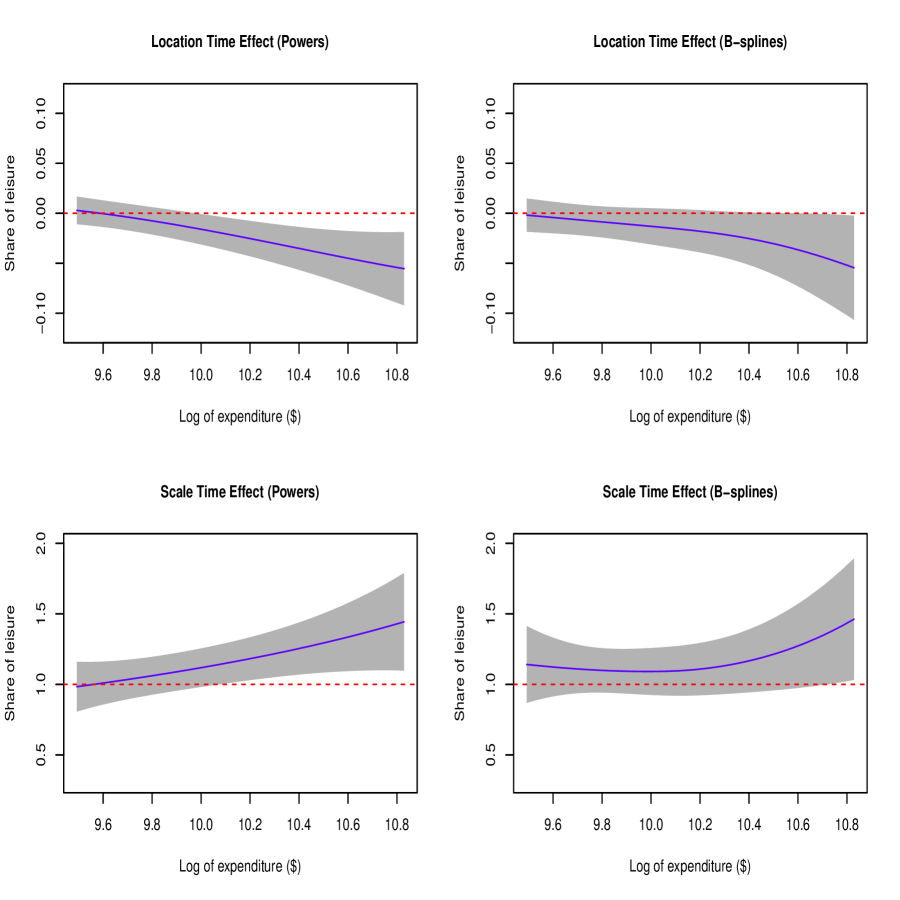

Figures 2 and 3 show the

estimates and confidence bands for the time effects functions:

based on Theorem 5 with and , where is the interval of values between the 0.10

and 0.90 sample quantiles of log-total expenditure. We find that we cannot

reject the hypothesis that there are no location and scale time effects for

food at home, whereas we find significant evidence of time effects for

leisure with both series specifications. In results not reported, we find

similar estimates and confidence bands for the time effects functions based

on conditional means and variances using Theorem 4.

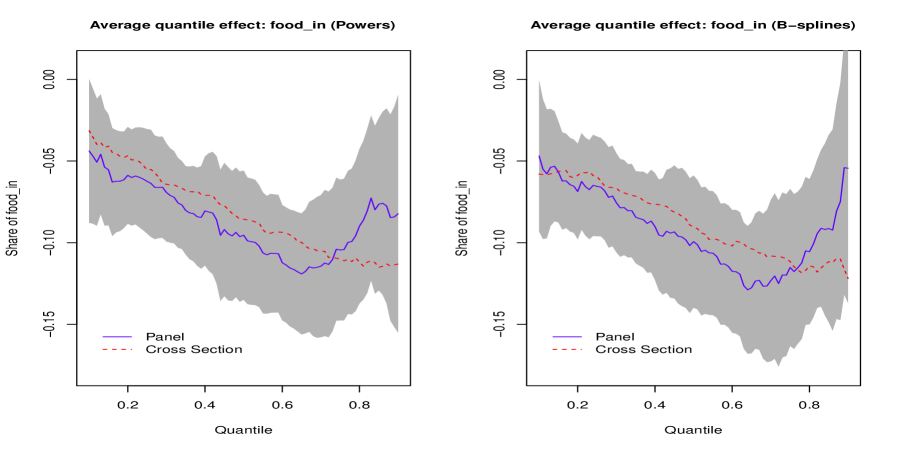

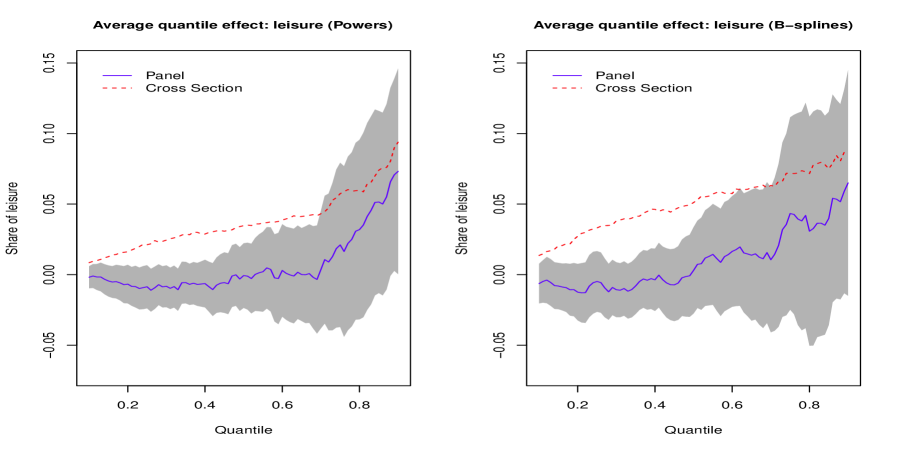

Figure 4 plots the estimates and confidence bands for the

time-averaged conditional quantile effects or CQSF derivates integrated over

the values of :

for where is the empirical measure of

log-expenditure, and Here we find heterogeneity

in the Engel curve relationship across the distribution. The pattern of the

effect is increasing with the quantile index for both food at home and

leisure, although the estimates are not sufficiently precise to distinguish

these patterns from sampling noise. The cross sectional estimates plotted in

dashed lines lie outside the confidence band for leisure, indicating

significant evidence of endogeneity. We do not find such evidence for food

at home.

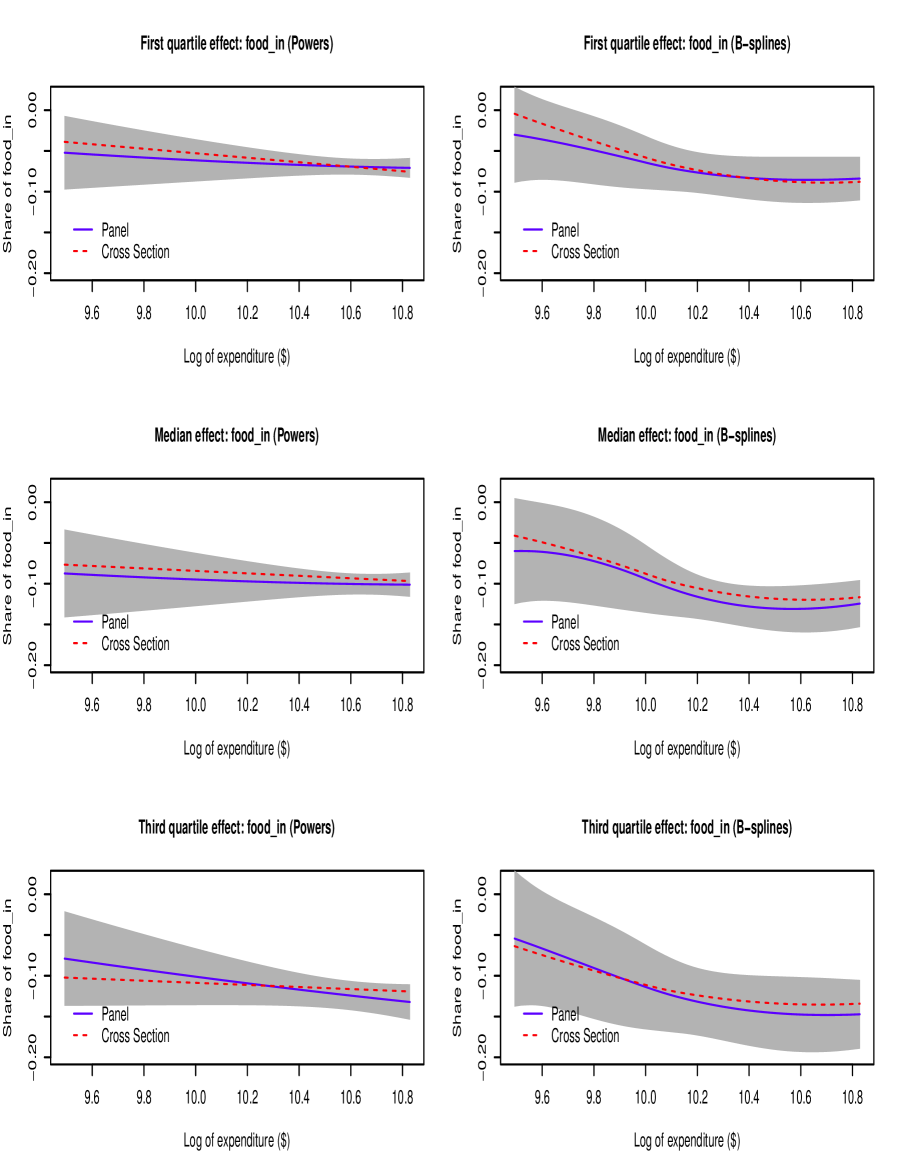

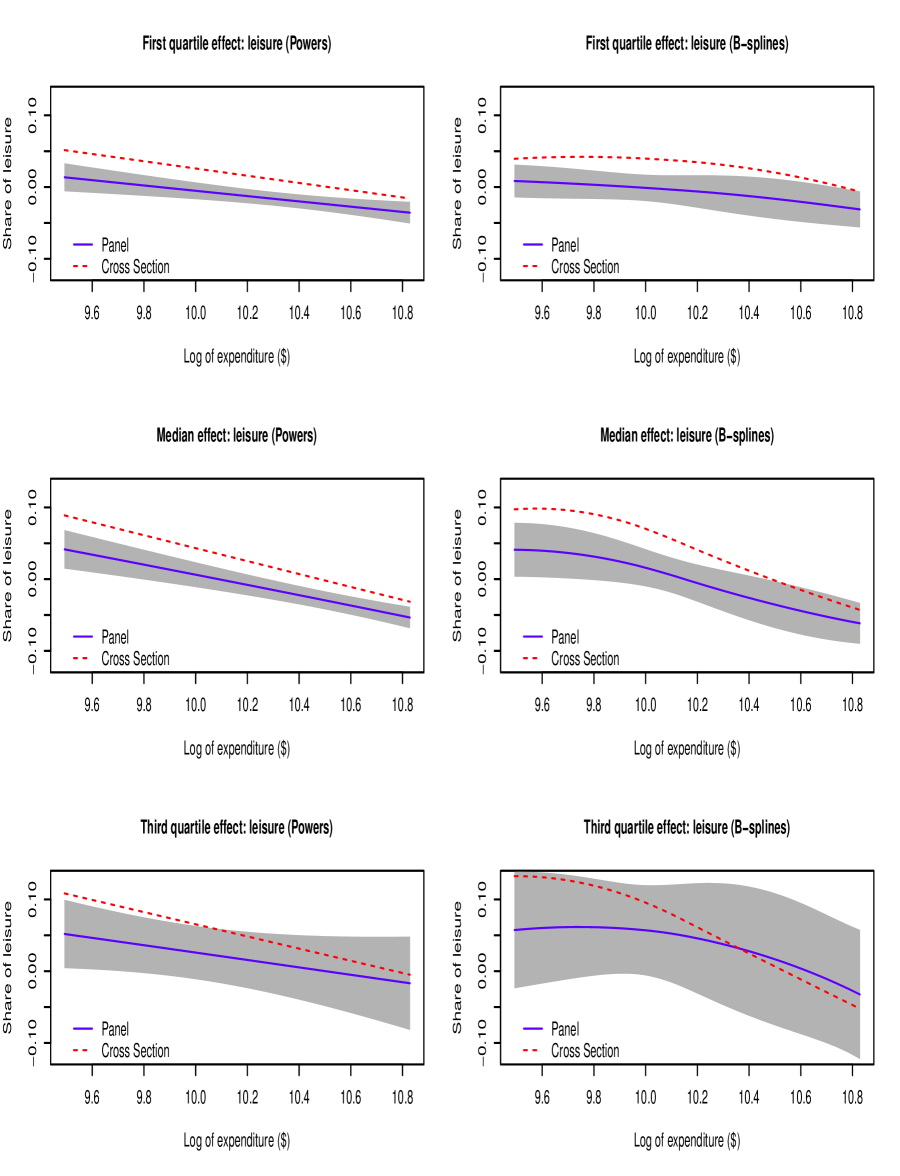

In figures 5 and 6, we show that

the panel estimates of the CQSF as a function of expenditure are decreasing

for food at home and increasing for leisure at low values of expenditure.

Imbens and Newey (2009) and Chen and Pouzo (2009, 2013) found similar

patterns in their estimates of the QSF and the quantile Engel curves,

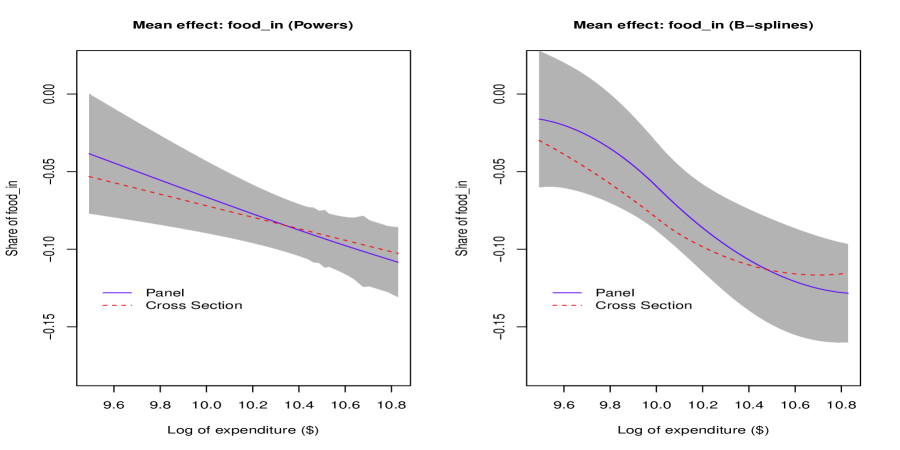

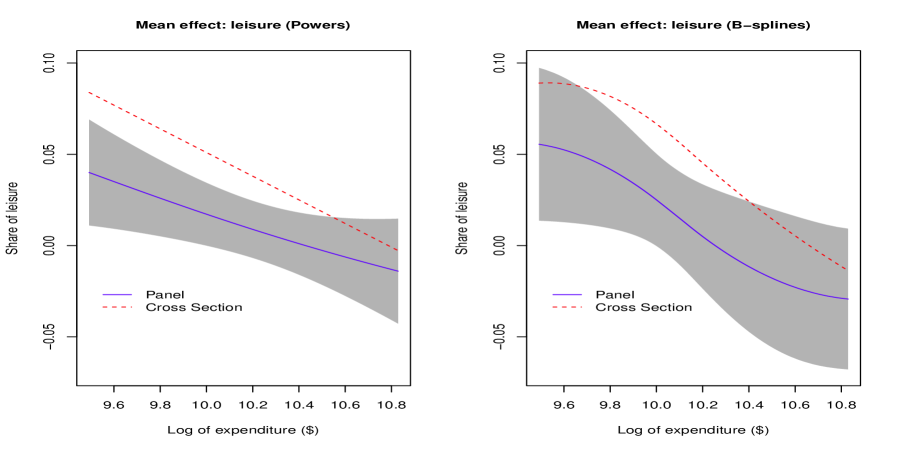

respectively. Figure 7 plots the estimates and confidence bands

for the time-averaged conditional mean effects or CASF derivatives:

We also again evidence of endogeneity for leisure in the mean effects, but

not for food at home. As in Blundell, Chen and Kristensen (2007), the

conditional ASF is decreasing in expenditure for food at home, whereas it is

increasing for leisure. We find that the curve is convex for food at home

and concave for leisure. Note, however, that we should interpret the shape

of our panel estimates with caution because they formally correspond to

multiple conditional QSFs and ASFs as the conditioning set

changes with along the curve.

Overall, the empirical results show that our panel estimates of the Engel

curves are similar to previous cross sectional estimates based on IV methods

to deal with endogeneity. Thus, the Engel curve relationship is decreasing

for food at home and increasing for leisure. Moreover, we find evidence of

the presence of time effects and endogeneity for leisure, but not for food

at home. These finding are consistent with consumer preferences where food

at home is a necessity good with little effect on the marginal allocation of

income between consumption and savings. Leisure, on the other hand, is a

superior good that affects the marginal allocation of income between

consumption and savings. The Engel curve relationship is stable over time

for food at home, whereas it is sensitive to changes over time in

preferences and relative prices for leisure.

It follows from the differentiability of and

and the dominance condition that

is continuously differentiable in in a neighborhood of , and that the order of differentiation and integration can be interchanged.

Furthermore, by the structure of the model and Assumption 2, for ,

Therefore, is continuously differentiable in in a neighborhood of , and for ,

(A.1)

where . Subtracting and using ,

Evaluating at gives

(2.2), and (2.3) follows similarly by

considering , using (A.1) and evaluating at . ∎

Let Then by the fundamental theorem of calculus, is differentiable in with derivative that is continuous in and .

Consider

(B.1)

By the inverse and implicit function theorems, is

continuously differentiable in and with

Then by Assumption 3 both

and are continuous in and and

bounded. Therefore,

(B.2)

are both bounded and continuous in and where the

last equality in each equation follows by a standard change of variables

argument. From the boundedness assumptions on and on

in Assumption 3, it follows that is partially differentiable in and

with partial derivatives continuous in , which can

be computed by differentiating under the integral in (B.1).

In order to establish the expressions in the lemma, insert (B.2) into the partial derivatives of (B.1)

w.r.t. and , and note that . The first expression is then immediate. For the

second, note that given (for a fixed ), , so that

Let

and let . From Lemma 1 it follows that is differentiable in and with partial derivatives

continuous in .

From (3.3), it follows that is also

differentiable in with

which is continuous in . Thus, is

continuously differentiable in , and the derivative w.r.t. is strictly positive (see the expression in Lemma 1). From the implicit function theorem, there is a unique solution , , to

which is differentiable with partial derivatives

where is the partial derivative

w.r.t. the components of in , . Evaluating at ,

subtracting and plugging in the expressions for the derivatives from Lemma 1 yields (3.1). ∎

by the form of the model and the conditional independence assumption. Below

we show that from Assumption 5, is

continuously partially differentiable with derivatives

(D.1)

From the positivity of the conditional density of given and

the implicit function theorem, the conditional quantile

given by exists and is

differentiable in with derivative

It remains to prove (D.1), which is analogous to Lemma 1. Let , so that is differentiable in with derivative that is

continuous in . Consider

(D.2)

By the inverse and implicit function theorems, is

continuously differentiable in and with

Then by Assumption 5 both and are

continuous in and and bounded. Therefore,

(D.3)

are both bounded and continuous in and where the

last equality in each equation follows by a change of variables argument

together with conditional independence of and given .

From the boundedness assumptions on and on in

Assumption 5, it follows that is partially

differentiable with continuous partial derivatives which can be computed by

differentiating under the integral in (D.2). Now insert (D.3) into (D.2) and note that by

conditional independence. The first expression is then immediate. For the

second, note that given (for a fixed ), , so that

The proof of the third result is similar to the proof of Theorem 1 replacing by . In particular, is continuously differentiable, , in a neighborhood

of and for

Let

and let where .

The first result follows by a similar argument to the proof of Theorem 2. In particular, by Lemma 1 and (5.1), is

continuously differentiable with derivatives

Thus, is continuously

differentiable with positive derivative with respect to . By the implicit

function theorem, there is a unique solution

to

which is differentiable with partial derivatives

where is the partial

derivative w.r.t. the components of in , .

Evaluating at , and plugging in the expressions for the

derivatives yields

where we use that by invariance of quantiles to monotone transformations, and

by a change of variables. Subtracting and using Assumption 2

and

The result then follows by averaging the previous expressions, using and that does not depend on

by Assumption 2.

The second and third results follow from Assumption 2 by

direct calculation because

∎

References

[1]Altonji, J., and R. Matzkin (2005): “Cross Section and Panel Data Estimators for Nonseparable Models with

Endogenous Regressors”, Econometrica 73,

1053-1102.

[2]Belloni, A., Chernozhukov, V., Chetverikov, D., and K.

Kato (2013), “On the Asymptotic Theory for Least Squares

Series: Pointwise and Uniform Results,” arXiv:1212:0442.

[3]Belloni, A., Chernozhukov, V., and I. Fernandez-Val

(2011), “Conditional quantile processes based on series or

many regressors,” arXiv:1105.6154.

[4]Bester, A.C., and C. Hansen (2009), “Identification of Marginal Effects in a Nonparametric Correlated Random

Effects Model,” Journal of Business & Economic Statistics 27(2),

pp. 235–250.

[5]Browning, M. and J. Carro (2007), “Heterogeneity and

Microeconometrics Modeling,” in Blundell, R., W.K. Newey, T. Persson

(eds.), Advances in Theory and Econometrics, Vol. 3, Cambridge:

Cambridge University Press.

[6]Blundell, R., Chen, X., and

D. Kristensen (2007) “Semi-nonparametric IV Estimation

of Shape-Invariant Engel Curves.” Econometrica

75(6). pp. 1613-1669.

[7]Chamberlain, G. (1980), “Analysis of Covariance with

Qualitative Data,” Review of Economic Studies, 47, pp. 225–238.

[8]Chamberlain, G. (1982), “Multivariate

Regression Models for Panel Data,” Journal of

Econometrics, 18, 5–46.

[9]Chamberlain, G. (1984), “Panel

Data,” in Z. Griliches and M. Intriligator eds

Handbook of Econometrics. Amsterdam: North-Holland.

[10]Chamberlain, G., and G. W. Imbens (2003), “Nonparametric applications of

Bayesian inference,” Journal of Business & Economic Statistics 21,

12–18.

[11]Chen, X., and Pouzo, D. (2009) “Efficient Estimation of Semiparametric Conditional Moment Models with

Possibly Nonsmooth Residuals,” Journal of

Econometrics, 152(1), 46-60.

[12]Chen, X., and Pouzo, D. (2013) “Sieve

Quasi Likelihood Ratio Inference on Semi/nonparametric Conditional Moment

Models,” Cowles Foundation Discussion Paper 1897.

[13]Chernozhukov, V., Fernandez-Val, I., Hahn, J., and W. K.

Newey (2013), “Average and Quantile Effects in

Nonseparable Panel Models,” Econometrica, 81(2),

pp. 535–580.

[14]Chernozhukov, V., Lee, S., and A.M. Rosen (2013),

“Intersection bounds: estimation and

inference,” Econometrica, 81 (2), pp. 667–737.

[15]Evdokimov, K. (2010), “Identification and Estimation of

a Nonparametric Panel Data Model with Unobserved Heterogeneity,”

unpublished manuscript, Princeton University.

[16]Fan, J. and Q. Yao (1998), “Efficient

estimation of conditional variance functions in stochastic

regression,” Biometrika, 85, pp. 645–660.

[17]Graham, B.W. and J.L. Powell (2012), “Identification and Estimation of Average Partial Effects in “Irregular”

Correlated Random Coefficient Panel Data Models,” Econometrica 80 (5), pp. 2105–2152.

[18]Hahn, J. (1995), “Bootstrapping quantile regression estimators,”Econometric Theory 11, 105–121.

[19]Hoderlein, S., and E. Mammen (2007): “Identification of Marginal Effects in Nonseparable Models without

Monotonicity,” Econometrica, 75, 1513 - 1519.

[20]Hoderlein, S. and H. White, (2012), ‘Nonparametric

identi cation in nonseparable panel data models with generalized fixed

effects’, Journal of Econometrics 168, 300-314.

[21]Honore, B.E. (1992): ”Trimmed Lad and Least Squares

Estimation of Truncated and Censored Regression Models with Fixed Effects,”

Econometrica 60, 533-565

[22]Hsiao, C. (2003), Analysis of panel data.

Second edition. Econometric Society Monographs, 34. Cambridge University

Press, Cambridge.

[23]Imbens, G. and W.K. Newey (2009), ”Identification and

Estimation of Triangular Simultaneous Equations Models Without Additivity,”

Econometrica 77, 1481-1512.

[24]Koenker R. and G. Bassett, (1978): “Regression

Quantiles,” Econometrica 46, pp. 33–50.

[25]Lewbel, A. (2006) “Entry

for the New Palgrave Dictionary of Economics, 2nd Edition.” Boston College. .

[26]Ma, S., and Kosorok, M. (2005): “Robust Semiparametric M-Estimation and the Weighted

Bootstrap,”Journal of Multivariate Analysis,

96(1), 190-217.

[27]Manski, C. (1987): “Semiparametric

Analysis of Random Effects Linear Models From Binary Response

Data,” Econometrica 55, 357-362.

[28]Praestgaard, J., and J. A. Wellner. (1993) “Exchangeably weighted

bootstraps of the general empirical process,” The Annals of

Probability, 2053–2086.

Figure 1: Density of the change in log-expenditure between 2007 and 2009.Figure 2: Location and scale time effects for food at home share: estimates from conditional quantiles.Figure 3: Location and scale time effects for leisure share: estimates from conditional quantiles.

Figure 4: Average conditional quantile effects of log total expenditure.Figure 5: Conditional quartile effects of log total expenditure on food at home share.Figure 6: Conditional quartile effects of log total expenditure on leisure share.

Figure 7: Conditional mean effects of log total expenditure.