Projective stochastic equations and nonlinear long memory

Ieva Grublytė and Donatas Surgailis

(

Vilnius University)

Projective stochastic equations and nonlinear long memory

Ieva Grublytė and Donatas Surgailis

(

Vilnius University)

Abstract

A projective moving average is a Bernoulli shift written as

a backward martingale transform of the innovation

sequence. We introduce a new class of nonlinear stochastic equations for projective moving averages, termed projective equations,

involving a (nonlinear) kernel and a linear combination of projections of

on ”intermediate” lagged innovation subspaces with given coefficients . The class of

such equations include usual moving-average processes and the Volterra series of

the LARCH model. Solvability of projective equations is studied, including a

nested Volterra series representation of the solution . We show that under natural conditions on

, this solution exhibits covariance and distributional long memory, with

fractional Brownian motion as the limit of the corresponding partial sums process.

A discrete-time second-order stationary process is called long memory

if its covariance decays slowly with the lag in such a way that

its absolute series diverges: . In the converse case

when and the process

is said short memory. Long memory processes

have different properties from short memory (in particular, i.i.d.) processes.

Long memory processes have been found to arise in a variety of physical and social sciences. See, e.g.,

the monographs

Beran [2], Doukhan et al. [7], Giraitis et al. [13] and the references therein.

Probably, the most important model of long memory processes is the linear, or moving average process

(1.1)

where is a standardized i.i.d. sequence,

and the moving average coefficients ’s decay slowly so that . The last condition guarantees that the series in (1.1) converges in mean

square and satisfies . In the literature it is often

assumed that the coefficients regularly decay as

and hence

The parameter in (1.2) is called the long memory parameter of

. A particular case of linear processes

(1.1)-(1.2) is the parametric class ARFIMA, in which case

is the order of fractional integration. An important property

of the linear process in (1.1)-(1.2) is the fact that its (normalized) partial sums process

tends to a fractional Brownian motion ([4]), viz.,

(1.4)

where is the Hurst parameter, and denotes the

weak convergence of random processes in the Skorohod space .

On the other hand, the linear model (1.1) has its drawbacks and sometimes is not capable

of incorporating empirical features (“stylized facts”) of some observed time series. The

”stylized facts” may include typical asymmetries, clusterings, and other nonlinearities

which are often observed in financial data, together with long memory.

The present paper introduces a new class of nonlinear processes which generalize the linear model

in (1.1)-(1.2) and enjoy similar long memory properties to (1.3)

and (1.4). These processes are defined through solutions of the so-called

projective stochastic equations. Here, the term “projective” refers to the fact that these equations

contain linear combinations of projections, or conditional expectations, of ’s on lagged innovation subspaces which enter the equation in a nonlinear way.

Let us explain the main idea of our construction. We call a projective moving average a random process of the form

(1.5)

where is a sequence of standardized i.i.d. r.v.’s as in (1.1), is a deterministic constant

and are r.v.’s

depending only on

such that

(1.6)

where

are nonrandom functions satisfying

(1.7)

It follows easily that under condition (1.7) the series in (1.5) converges in mean square and define

a stationary process with zero mean and finite variance . The next question -

how to choose the “coefficients” (1.6) so that they depend on and behave like

(1.2) when ?

A particularly simple choice of the ’s to achieve the above goals is

(1.8)

where are as in (1.2), is a given deterministic kernel,

and is the projection of onto the subspace of generated

by the innovations (the conditional expectation).

The corresponding projective stochastic equation has the form

(1.9)

Notice that when then by a general property of a conditional expectation

and then if is continuous. This means that

the ’s in (1.8) feature both the long memory in (1.2) and the dependence on the “current” value through .

In particular, for , the behavior of in (1.8)

strongly depends on the sign of and

the trajectory of (1.9) appears very asymmetric (see

Fig. 3, top).

Let us briefly describe the remaining sections.

Sec. 2 contains basic definitions and properties of projective processes.

Sec. 3 introduces the notion of nested Volterra series which plays an important role for solving of

projective equations.

Sec. 4 introduces a general class of projective stochastic equations, (1.9) being a particular case.

We obtain sufficient conditions

of solvability of these equations, and a recurrent formula for computation of ”coefficients”

(Theorem 4.3). Sec. 5 and 6 present some examples and

simulated trajectories and histograms of projective equations.

It turns out that the LARCH model studied in [9] and

elsewhere is a particular case of projective equations corresponding

to linear kernel (Sec. 5). Some modifications of projective equations are discussed in Sec.7.

Sec. 8 deals with long memory properties of stationary solutions of stochastic projective equations.

We show that under some additional conditions these solutions have

long memory properties similar to (1.3)

and (1.4).

Finally, we remark that “nonlinear long memory” is a

general term and that other time series models different from ours

for such behavior

were proposed in the literature. Among them, probably the most studied

class are subordinated processes of the form , where

is a Gaussian or linear long memory process and is a nonlinear function.

See [23], [16] and [13] for a detailed discussion. A related class

of Gaussian subordinated stochastic volatility models is studied in [18]. [8] discuss a class

of long memory Bernoulli shifts.

[1] consider

fractionally integrated process with nonlinear autoregressive innovations.

A general invariance principle for fractionally integrated models with weakly dependent innovations satisfying

a projective dependence condition of [5]

is established in [21]. See also [25] and Remark 8.3 below.

We expect that the results of this paper can be extended in several directions, e.g.,

projective equations with initial condition, continuous time processes, random field set-up,

infinite variance processes.

For applications,

a major challenge is estimation of “parameters” of projective equations. We plan to study some

of these questions in the future.

2 Projective processes and their properties

Let be a sequence of i.i.d. r.v.’s with .

For any integers we denote

the sigma-algebra generated by ,

For ,

we define as the trivial sigma-algebra. Let

be the spaces of all square integrable r.v.’s measurable w.r.t. , respectively.

For any let

be the conditional expectation. Then is a bounded linear operator in ; moreover,

is a projection family satisfying

for any intervals .

From the definition of conditional expectation it follows that if are arbitrary measurable functions with

is a given interval and

is a product of independent r.v.’s, then for any interval

In particular, if then

(2.10)

Any r.v. can be expanded into orthogonal series

where

Note that is a backward martingale difference sequence and

Definition 2.1

A projective process

is a random sequence of the form

(2.11)

where are r.v.’s satisfying the following conditions (i) and (ii):

(i) is -measurable, is a

deterministic number;

(ii)

In other words, a projective process has the property that the projections form a backward martingale transform

w.r.t. the nondecreasing family of sigma-algebras, for each fixed. A consequence

of the last fact is the following moment inequality which is an easy consequence of

Rosenthal’s inequality ([14], p.24).

See also [13], Lemma 2.5.3.

Proposition 2.2

Let be a projective process in (2.11).

Assume that and

for some . Then . Moreover,

there exists a constant

depending on alone and such that

Definition 2.3

A projective

moving average is a projective process of (2.11) such that the mean is constant and

there exist a number and

nonrandom measurable functions such that

By definition, a projective moving average is a stationary Bernoulli shift ([6], p.21):

(2.12)

with mean and covariance

(2.13)

These facts together with the

ergodicity of Bernoulli shifts (implied by a general result in [22], Thm.3.5.8) are summarized in the following corollary.

Corollary 2.4

A projective moving average is a strictly stationary and ergodic

stationary process with finite variance and

covariance given in (2.13).

Remark 2.5

If the coefficients are nonrandom, a projective moving average is a linear process

Proposition 2.6

Let be a projective process of (2.11) and a deterministic

sequence, .

Then is a projective

process with and

coefficients .

Proof follows easily by the Cauchy-Schwarz inequality and is omitted.

Proposition 2.7

If is a projective process of (2.11), then for any

(2.14)

The representation (2.11) is unique: if

(2.11) and are two representations, with satisfying

conditions (i) and (ii) of Definition 2.1, then

Proof.

(2.14) is immediate by definition of projective process. From

(2.14) it follows that where is independent of . Relation

implies for all small enough.

Hence, implying

for any .

The following invariance principle is due to Dedecker and Merlevède ([5], Cor. 3), see also ([24], Thm. 3 (i)).

Proposition 2.8

Let be a projective moving average of (2.11) such that

and

(2.15)

where

Then

(2.16)

where is a standard Brownian motion and

3 Nested Volterra series

First we introduce some notation. Let be a set of integers which is bounded from above, i.e., .

Let

be a class of finite nonempty subsets .

Write for the cardinality of .

For any

the notation

means that and . In particular,

implies and . Note that is not a partial order in

since do not imply .

A set is said maximal if there is no such that

.

Let denote the class of all maximal elements of

Definition 3.1

Let and

be as above. Let

be a family of measurable functions

indexed by sets and such that

is a constant function for any maximal set .

A nested Volterra series is a sum

(3.17)

where the nested summation is taken over all sequences ,

with the convention

and for

In particular, when is the class of all subsets of ,

(3.17) can be rewritten as

(3.18)

where the last sum is taken over all such that

The following example clarifies the above definition and its relation to the usual Volterra series

([6], p.22).

Example 3.2

Let and be the class of all subsets

having points. Let be a family of

linear functions

Then

(3.19)

is the (usual) Volterra series of order . The series

in (3.19) converges in mean square if and only if

(3.20)

in which case .

Proposition 3.3

Let as in Example 3.2.

Assume that the system in Definition 3.1

satisfies

the following condition

(3.21)

where are real numbers satisfying

(3.22)

where the inner sums are taken over all sequences

with

and .

Then, the nested Volterra series

in (3.18) converges in mean square and satisfies

Moreover,

is a projective process with zero mean and coefficients

(3.23)

if , otherwise,

where the nested summation is defined as in (3.17).

Proof.

Clearly, the coefficients in (3.23) satisfy the measurability condition (i) of Definition

2.1. Condition (ii) for these coefficients

follows by recurrent application of (3.21):

Thus, is a well-defined projective process and

.

Remark 3.4

In the case of a usual Volterra series in (3.19), condition

(3.21) is satisfied with for

and the sums of (3.22) and of (3.20) coincide:

This fact confirms that condition

(3.22) for the convergence of nested Volterra series cannot be generally improved.

4 Projective stochastic equations

Let be some given measurable deterministic functions

depending on real variables and be some given constants. A projective stochastic equation has the form

(4.24)

Definition 4.1

By solution of (4.24) we mean a projective process

satisfying

Assume that that does not depend on

the functions in (4.24) depend only on and that

is a solution of (4.24).

Then is a projective moving average of (2.12) with and

defined recursively by

(4.25)

Moreover, such a solution is unique.

Proof.

From (4.24) and the uniqueness of (2.11) (Proposition 2.7) we have

where

For this yields as in (4.25). Similarly,

, where is defined in

(4.25). Assume by induction that

(4.26)

with defined in (4.25),

hold for any and some

; we need to show that (4.26) holds for , too. Using (4.26), (2.14) and

(4.25) we

obtain

This proves the induction step and hence the proposition, too, since

the uniqueness follows trivially.

Clearly, the choice of possible kernels in (4.24) is very large. In this paper

we focus on the following class of projective stochastic equations:

(4.27)

where are given arrays of real numbers, is a constant,

and is a measurable function

of a single variable . Two modifications of (4.27) are briefly discussed below, see

(7.49) and (7.52).

Particular cases of (4.27) are

(4.28)

and

(4.29)

corresponding to and

respectively.

Next, we study the solvability of projective equation (4.27).

We assume that

satisfies the following dominating bound: there exists a constant such that

(4.30)

Denote

(4.31)

The main result of this section is the following theorem.

according to (4.32). Therefore, is a well-defined projective moving-average.

The remaining statements about follow from Proposition 4.2.

(ii) Similarly to (4.34), (4.36) in the case we obtain

and hence . This proves (ii) and

Theorem 4.3, too.

In the case of equations (4.28) and (4.29),

condition (4.32) can be simplified, see below. Note that for ,

equations (4.33) admit a trivial solution since by (4.30), leading

to the constant process in (4.27).

Proposition 4.4

(i) Let

and . Then

is equivalent to and .

(ii) Let ,

and .

Then

is equivalent to and . Moreover,

Proof.

(i) By definition,

where Since entails ,

such that

. Hence,

Therefore, and imply . The converse implication is

obvious.

(ii) Follows by

Remark 4.5

It is not difficult to show that conditions on the ’s

in Proposition 4.4 (i) and (ii) are part of the following more general

condition: which also guarantees that

.

The following Proposition 4.6 obtains a sufficient condition for the existence

of higher moments of the solution of projective

equation (4.27). The proof of Proposition 4.6 is based on a recurrent

use of Rosenthal-type inequality of Proposition 2.2, which contains an absolute constant

depending only on . For , denote

(4.37)

where (recall) . Note

, hence coincides with (4.31).

Proposition 4.6

Assume conditions of Theorem 4.3 and

for some .

Then .

Proof.

The proof is similar to that of Theorem 4.3 (i).

By Proposition 2.2,

Using condition (4.30), Proposition 2.2 and inequality we obtain the following recurrent inequality:

Iterating the last inequality as in the proof of Theorem 4.3 we obtain

, with given in (4.37).

Finally, let us discuss the question when of (4.27) satisfies the weak

dependence condition in (2.15) for the invariance principle.

Proposition 4.7

Let satisfy the conditions of Theorem 4.3 and be defined

in (2.15). Then

(4.38)

In particular, if the quantity on the r.h.s. of (4.38) is finite, satisfies

the functional central limit theorem in (2.16).

1. Finitely dependent projective equations. Consider equation (4.27), where

for all and some . Since , the corresponding equation writes as

(5.39)

where the r.h.s. is -measurable. In particular, of (5.39) is an -dependent process.

We may ask if the above process can be represented as a moving-average of length w.r.t. to some i.i.d. innovations?

In other words,

if there exists an i.i.d. standardized sequence

and coefficients such that

(5.40)

To construct a negative counter-example to the above question,

consider the simple case of (5.39) with , , :

(5.41)

Assume that . Then . On the other hand, from

(5.40) with

we obtain implying that

is an i.i.d. sequence.

Let us show that the last conclusion contradicts the form of in (5.41) under general assumptions on and the distribution of

. Assume

that is symmetric, and is antisymmetric. Then

Assume, in addition, that is monotone nondecreasing on . Then , implying

. As a consequence,

(5.41) is not a moving average of length 2 in some standardized i.i.d. sequence.

2. Linear kernel . For linear kernel , the solution of (4.27) of Theorem 4.3

can be written explicitly as , where is a linear process and

for is a Volterra series of order , see ([6], p.22),

which are orthogonal in sense that .

Let be the subspace spanned by

products Clearly, the above Volterra series (corresponding to linear )

constitute a very special class of projective processes. For example, the process in

(5.41) cannot be expanded in such series unless is linear. To show the last fact, decompose (5.41) as

, where

and

is orthogonal to

hence .

3. The LARCH model.

The Linear ARCH (LARCH) model, introduced by Robinson [17], is defined by the equations

(5.42)

where is a standardized i.i.d. sequence, and the coefficients satisfy . The LARCH model was studied in [9], [10], [12]), [11],

[3] and other papers.

In financial modeling, are interpreted as (asset) returns and as volatilities.

Of particular interest is the case when the ’s in (5.42)

are proportional to

ARFIMA coefficients, in which case it is possible to rigorously prove long memory of the volatility and the

(squared) returns.

It is well-known ([11])

that a second order strictly stationary solution to (5.42) exists if and only if

(5.43)

in which case it can be represented by the convergent orthogonal Volterra series

Clearly, the last series is a particular case of the Volterra series of the previous example.

We conclude that under the condition (5.43),

the volatility process of the LARCH model satisfies the projective

equation (4.29) with linear function and . Note that

(5.43) coincides with the condition of Proposition 4.4 (ii) for the existence

of solution of (4.29).

From Proposition 4.6 the following new result about the existence of

higher order moments of the LARCH model is derived.

Corollary 5.1

Assume that

(5.44)

where and is the absolute constant from Proposition 2.2,

. Then

. Moreover,

(5.45)

Proof. Follows from Proposition 4.6 and the easy fact that for the LARCH model,

of (4.37) coincides with the r.h.s. of

(5.45).

Condition (5.44) can be compared with the sufficient condition for

in ([9], Lemma 3.1):

(5.46)

Although the best constant in the Rosenthal’s inequality is not known,

(5.44) seems much weaker than

(5.46), especially when is large. See, e.g. [15], where

it is shown that

where and

is a bounded measurable function with . If is a step function:

where is a partition of

into disjoint intervals , the process in (5.47) follows

different “moving-average regimes” in the regions exhibiting

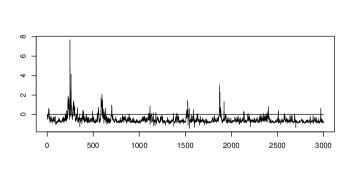

a “projective threshold effect”. See Fig. 1, where the left graph shows a trajectory

having a single threshold at and the right graph a trajectory with two threshold points at and .

Figure 1: Trajectories of solutions of (5.47), . Left: , right: .

6 Simulations

Solutions of projective equations can be

easily simulated using a truncated expansion

instead of infinite series in (1.5). We chose the truncation level equal to the sample size in

the subsequent simulations. The coefficients of projective equations

are computed very fast from recurrent formula (4.33) and simulated values

. The innovations were taken standard normal. For better comparisons,

we used the same sequence in all simulations.

Stationary solution of equation (4.29) was simulated for three different choices of and

two choices of coefficients . The first choice of coefficients is and

corresponds to a short memory process .

The second choice is with

corresponds to a long memory process with coefficients as in ARFIMA.

The value of

was chosen so that . The latter condition guarantees the existence

of a stationary solution of (4.29), see Proposition 4.4.

The simulated trajectories and (smoothed) histograms of marginal densities strongly depend on the kernel . We

used the following functions:

(6.48)

Clearly, in (6.48) satisfy (4.30) with and the Lipschitz condition

(8.56). Note that is bounded and supported in the compact interval while

are unbounded, the latter being bounded from below. Also

note that for and the choice of as above, the projective

process of (4.29) agrees with AR(.5) for and with ARFIMA for

in all three cases in (6.48)

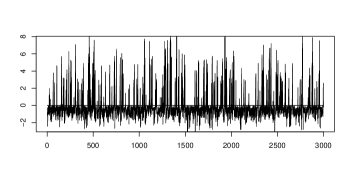

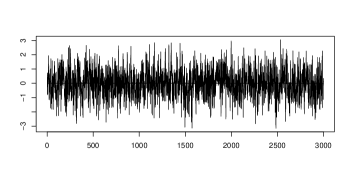

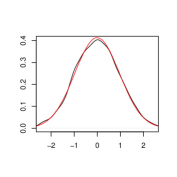

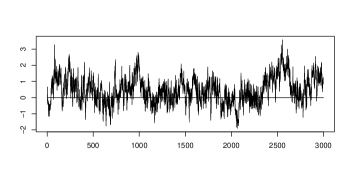

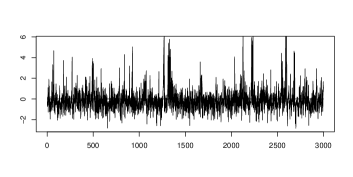

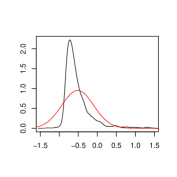

Figure 2: Trajectories and (smoothed) histograms of solutions of projective equation (4.29) with . Top: ,

bottom: .

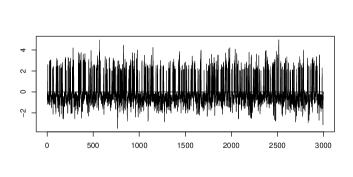

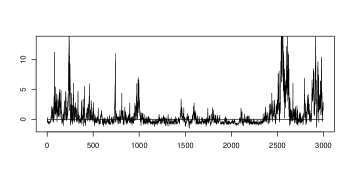

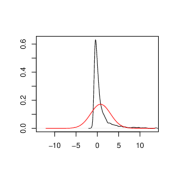

Figure 3: Trajectories and (smoothed) histograms of solutions of projective equation (4.29) with Top: , bottom:

.

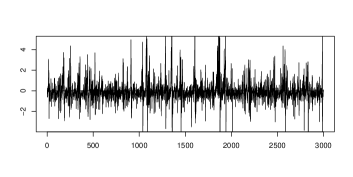

Figure 4: Trajectories and (smoothed) histograms of solutions of projective equation (4.29) with = the “triangle function” in

(6.48).

Top: , bottom:

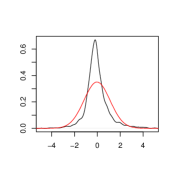

A general impression from our simulations is that in all cases of in (6.48), the coefficients account for the persistence

and for the clustering of the process. We observe that as ’s increase, the process becomes more asymmetric and its empirical

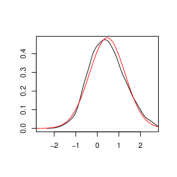

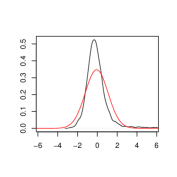

density diverges from the normal density (plotted in red in Figures 2-4

with parameters equal to the empirical mean and variance of the simulated series).

In the case of unbounded and long memory ARFIMA coefficients, the marginal distribution seems

strongly skewed to the left and having a very light left tail and a much heavier right tail. On the other hand,

in the case of geometric coefficients, the density for seems rather symmetric although heavy tailed. Case of

corresponding to

bounded seems to result in asymmetric distribution with light tails.

7 Modifications

Equation (4.27) can be modified in several ways. The first modification is

obtained by taking

the ’s “outside of ”:

(7.49)

where satisfy similar conditions as in (4.27). However, note that (4.30) implies

in which case (7.49) has a trivial solution . To avoid

the last eventuality, condition (4.30) must be changed.

Instead,

we shall assume that is a measurable function

satisfying

(7.50)

for some .

Denote

Proposition 7.1 can be proved similarly to Theorem 4.3 and its proof is omitted.

Then there exists a unique solution of (7.49), which is written as

a projective moving average of (2.11)

with coefficients recursively defined as

(ii) In the case of linear function , condition (7.51) is also necessary

for the existence of a solution of (7.49).

Remark 7.2

Let and . Then

Hence, and imply for any

; see the proof of Proposition 4.4.

Projective stochastic equations (4.27) and (7.49) can be further modified by

including projections of lagged variables.

Consider the following extension of (4.27):

(7.52)

where are the same as in (4.27) and the only new feature is that is replaced

by in the inner sum on the r.h.s. of the equation. This fact allows to study nonstationary solutions

of (7.52) with a given projective initial condition and the convergence

of to the equilibrium as ; however, we shall

not pursue this topic in the present paper.

The following proposition is a simple extension

of Theorem 4.3 and its proof is omitted.

Proposition 7.3

Let satisfy the conditions of Theorem 4.3, including

(4.30) and (4.32).

Then there exists a unique solution of (7.52), which is written as

a projective moving average of (2.11)

with coefficients recursively defined as and

Finally, consider a projective equation (4.24) with

and kernels depending on real variables,

where and

(7.53)

, where is a measurable function taking values in the interval .

More explicitly,

(7.54)

where . Note that when is constant,

(7.54)

is a stationary ARFIMA process. Time-varying fractionally integrated processes with

deterministic coefficients of the form

(7.53) were studied in [19], [20]. We expect that (7.54)

feature a “random” memory intensity depending on the values of the process. A rigorous study

of long memory properties of this model does not seem easy. On the other hand, solvability of

(7.54) can be established similarly to the previous cases (see below).

Proposition 7.4

Let be a measurable function taking values in and

such that , where .

Then there exists a unique stationary solution of (7.54), which is written as

a projective moving average of (2.11)

with coefficients recursively defined as and

Proof. Note that and . Therefore

the ’s in (7.55) satisfy

for any . The rest of the proof is analogous as the case

of Theorem 4.3.

8 Long memory

In this section we study long memory properties (the decay of covariance and partial sums’ limits) of

projective equations (4.27) and (7.49) in the case when the coefficients

’s decay slowly as

Theorem 8.1

Let be the solution

of projective equation (4.27) satisfying the conditions of Theorem 4.3 and .

Assume, in addition,

that is a Lipschitz function, viz., there exists a constant such that

(8.56)

and that there exist

and such that

(8.57)

and

(8.58)

Then, as

(8.59)

where and

is beta function. Moreover, as

(8.60)

where is a fractional Brownian motion with parameter and variance

and .

Proof.

Let us note that the statements (8.59) and (8.60) are well-known when

, in which case coincides

with the linear process . See, e.g.,

[13], Proposition 3.2.1 and Corollary 4.4.1.

The natural idea of the proof is to approximate by the linear process

. For , denote

To show (8.60), consider

By stationarity of , for any we have

see above, and therefore , implying

Therefore partial sums of and tend to the same limit , in the sense of weak convergence

of finite dimensional distributions. The tightness in follows from (8.59) and

the Kolmogorov criterion. Theorem 8.1 is proved.

A similar but somewhat different approximation by a linear process applies in the case of projective equations of

(7.49).

Let us discuss a special case of :

(8.61)

Note that for such ,

and the corresponding projective equation (7.49) with coincides

with (1.9). Recall that for bounded ’s as in (8.61), condition

(7.50) on together with guarantee

the existence

of the stationary solution (see Remark 7.2). We shall also need the following

additional condition:

(8.62)

Since , so (8.62) is satisfied

if is Lipschitz, but otherwise conditions (8.62) and (7.50) allow to be even

discontinuous.

Denote

Theorem 8.2

Let be the solution

of projective equation (7.49) with as in (8.61),

satisfying (7.50)

and

Proof.

Similarly as in the proof of the previous theorem,

let

, , . Relation (8.64) follows from

(8.66)

We have and

Decompose , where

and where

Here, see above, while

(8.67)

uniformly in , according to (8.62). Hence and from

(8.63)

it follows that

(8.68)

Accordingly, it suffices to prove (8.66) with replaced by . We have

where the “remainders” ,

and

can be estimated similarly to (8.67), leading to the asymptotics of (8.68) for

each of the three sums in the above decomposition of . This proves (8.64).

Let us prove (8.65). Consider the convergence of one-dimensional distributions for , viz.,

where we used the fact that and are independent. Here,

thanks to (8.62), we see that

uniformly in as

. The same is true for since

it is completely analogous to (8.67). This proves (8.72). Next,

with (8.71) in mind, split , where

where is a large number. By (8.72), for any we can find such that

and therefore

holds for all large enough, where in view

of (8.63).

On the other hand,

for any fixed. Then (8.70) follows, implying

the finite-dimensional convergence in (8.65). The tightness in (8.65) follows from (8.64) and

the Kolmogorov

criterion, similarly as in the proof of Theorem 8.1. Theorem 8.2 is proved.

Remark 8.3

Shao and Wu [21] discussed partial sums limits of fractionally integrated nonlinear processes

where is the backward shift, is the fractional differentiation operator,

and

is a causal Bernoulli shift:

(8.73)

in i.i.d. r.v.’s . The weak dependence condition

on (8.73), analogous to (2.15) and

guaranteeing the weak convergence of normalized partial sums of towards a fractional Brownian motion,

is written in terms of projections :

(8.74)

where and for ;

see ([21], Thm. 2.1), also [25], [24]. The above mentioned papers verify

(8.74) for several classes of Bernoulli shifts. It is of interest

to verify (8.74) for projective moving averages.

For of (1.5) and

,

is a well-defined projective

moving average with coefficients

see Proposition 2.6.

For concreteness, let as in Theorem 8.2 with

. We have

, where

(8.75)

where

and we used in the last equality.

Note that have the same sign and are not negligible in

(8.75). Therefore

we conjecture that and hence

for . The above argument suggests that projective

moving averages posses a different ”memory mechanism” from

fractionally integrated processes in [21].

9 Acknowledgements

This work was supported by a grant (No. MIP-063/2013) from the Research Council of Lithuania.

The authors also thank an anonymous referee for useful remarks.

References

[1] Baillie, T.R., Kapetanios, G., 2008. Nonlinear models for strongly dependent processes

with financial applications. J. Econometrics, 147, 60–71.

[2] Beran, J., 1994. Statistics for Long Memory Processes.

Monographs on Statistics and Applied Probability, vol. 61.

Chapman and Hall, New York.

[3] Berkes, I., Horváth, L., 2003. Asymptotic

results for long memory LARCH sequences. Ann.

Appl. Probab., 13, 641–668.

[4] Davydov, Y., 1970. The invariance principle for stationary

process. Theory Probab. Appl., 15, 145–180.

[5] Dedecker, J., Merlevède, F., 2003. The conditional central limit theorem

in Hilbert spaces. Stoch. Process. Appl., 108, 229–262.

[7] Doukhan, P., Oppenheim, G., Taqqu, M.S. (Eds.), 2003. Theory

and Applications of Long-Range Dependence. Birkhäuser, Boston.

[8] Doukhan, P., Lang, G., Surgailis, D., 2012. A class of Bernoulli

shifts with long memory: asymptotics of the partial sums process. Preprint.

[9] Giraitis, L., Robinson, P.M., Surgailis, D., 2000. A model for long memory conditional heteroskedasticity. Ann. Appl. Probab.,

10, 1002–1024.

[10] Giraitis, L., Leipus, R., Robinson, P.M., Surgailis, D., 2004. LARCH, leverage and long memory. J. Financial Econometrics,

2, 177-210.

[11] Giraitis, L., Surgailis, D., 2002. ARCH-type bilinear models with double long memory. Stoch. Process. Appl. 100,

275–300.

[12] Giraitis, L., Leipus, R., Surgailis, D., 2009. ARCH() models

and long memory properties. In: T.G. Andersen, R.A. Davis, J.-P. Kreiss, T. Mikosch (Eds.)

Handbook of Financial Time

Series, pp. 71–84. Springer-Verlag.

[13] Giraitis, L., Koul, H.L., Surgailis, D., 2012. Large Sample Inference

for Long Memory Processes. Imperial College Press, London.

[14] Hall, P., Heyde, C.C., 1980. Martingale Limit Theory and Applications.

Academic Press, New York.

[15] Hitchenko, P., 1990. Best constants in martingale version of

Rosenthal’s inequality. Ann. Probab. 18, 1656–1668.

[16] Ho, H.-C., Hsing, T., 1997. Limit theorems for functionals of moving

averages. Ann. Probab. 25, 1636–1669.

[17] Robinson, P.M., 1991. Testing for strong serial correlation and dynamic

conditional heteroskedasticity in multiple regression. J.

Econometrics, 47, 67–84.

[18] Robinson, P.M., 2001. The memory of stochastic volatility models.

J. Econometrics, 101, 195–218.

[19] Philippe, A., Surgailis, D., Viano, M.-C., 2006. Invariance principle

for a class of non stationary processes with long memory. C. R.

Acad. Sci. Paris Ser. 1 342, 269–274.

[20] Philippe, A., Surgailis, D., Viano, M.-C., 2008.

Time-varying fractionally integrated processes with nonstationary

long memory. Th. Probab. Appl. 52, 651-673.