Uniform approximation of the Cox-Ingersoll-Ross process

Abstract

The Doss-Sussmann (DS) approach is used for uniform simulation of the Cox-Ingersoll-Ross (CIR) process. The DS formalism allows to express trajectories of the CIR process through solutions of some ordinary differential equation (ODE) depending on realizations of a Wiener process involved. By simulating the first-passage times of the increments of the Wiener process to the boundary of an interval and solving the ODE, we uniformly approximate the trajectories of the CIR process. In this respect special attention is payed to simulation of trajectories near zero. From a conceptual point of view the proposed method gives a better quality of approximation (from a path-wise point of view) than standard, or even exact simulation of the SDE at some discrete time grid.

AMS 2000 subject classification. Primary 65C30; secondary 60H35.

Keywords. Cox-Ingersoll-Ross process, Doss-Sussmann formalism, Bessel functions, confluent hypergeometric equation.

1 Introduction

The Cox-Ingersoll-Ross process is determined by the following stochastic differential equation (SDE)

| (1) |

where are positive constants, and is a scalar Brownian motion. Due to [6] this process has become very popular in financial mathematical applications. The CIR process is used in particular as volatility process in the Heston model [13]. It is known ([14], [15]) that for there exists a unique strong solution of (1) for all . The CIR process is positive in the case and nonnegative in the case Moreover, in the last case the origin is a reflecting boundary.

As a matter of fact, (1) does not satisfy the global Lipschitz assumption. The difficulties arising in a simulation method for (1) are connected with this fact and with the natural requirement of preserving nonnegative approximations. A lot of approximation methods for the CIR processes are proposed. For an extensive list of articles on this subject we refer to [3] and [7]. Besides [3] and [7] we also refer to [1, 2, 11, 12], where a number of discretization schemes for the CIR process can be found. Further we note that in [17] a weakly convergent fully implicit method is implemented for the Heston model. Exact simulation of (1) is considered in [5, 9] (see [3] as well).

In this paper, we consider uniform pathwise approximation of on an interval using the Doss-Sussmann transformation ([8], [20], [19]) which allows for expressing any trajectory of by the solution of some ordinary differential equation that depends on the realization of The approximation will be uniform in the sense that the path-wise error will be uniformly bounded, i.e.

| (2) |

where is fixed in advance. In fact, by simulating the first-passage times of the increments of the Wiener process to the boundary of an interval and solving this ODE, we approximately construct a generic trajectory of Such kind of simulation is more simple than the one proposed in [5] and moreover has the advantage of uniform nature. Let us consider the simulation of a standard Brownian motion on a fixed time grid

Although may be even exactly simulated at the grid points, the usual piecewise linear interpolation

is not uniform in the sense of (2). Put differently, for any (large) positive number there is always a positive probability (though possibly small) that

Therefore, for path dependent applications for instance, such a standard, even exact, simulation method may be not desirable and a uniform method preserving (2) may be preferred.

We note that the original DS results rely on a global Lipschitz assumption that is not fulfilled for (1). We therefore have introduced the DS formalism that yields a corresponding ODE which solutions are defined on random time intervals. If gets close to zero however, the ODE becomes intractable for numerical integration and so, for the parts of a trajectory that are close to zero, we are forced to use some other (not DS) approach. For such parts we here propose a different uniform simulation method. Another restriction is connected with the condition We note that the case is more general than the case that ensures positivity of and stress that in the literature virtually all convergence proofs for methods for numerical integration of (1) are based on the assumption We expect that the results here obtained for can be extended to the case where however in a highly nontrivial way. Therefore, the case will be considered in a subsequent work.

The next two sections are devoted to DS formalism in connection with (1) and to some auxiliary propositions. In Sections 4 and 5 we deal with the one-step approximation and the convergence of the proposed method, respectively. Section 6 is dedicated to the uniform construction of trajectories close to zero.

2 The Doss-Sussmann transformation

2.1 Due to the Doss-Sussmann approach ([8], [14], [19], [20]), the solution of (1) may be expressed in the form

| (3) |

where is some deterministic function and is the solution of some ordinary differential equation depending on the part of the realization of the Wiener process

Let us recall the Doss-Sussmann formalism according to [19], V.28. In [19] one consideres the Stratonovich SDE

| (4) |

The function is found from the equation

| (5) |

and is found from the ODE

| (6) |

It turns out that application of the DS formalism after the Lamperti transformation (see [7]) leads to more simple equations. The Lamperti transformation yields the following SDE with additive noise

| (7) | ||||

| (8) |

Let us seek the solution of (7) in the form

| (9) |

in accordance with (3)-(6). Because the Ito and Stratonovich forrms of equation (7) coincide, we have

The function is found from the equation

i.e.,

| (10) |

and is found from the ODE

| (11) |

From (9), (10), and solution of (11), we formally obtain the solution of (7):

| (12) |

Hence

| (13) |

2.2 Since the Doss-Sussmann results rely on a global Lipschitz assumption that is not fulfilled for (1), solution (13) has to be considered only formally. In this section we therefore give a direct proof of the following more precise result.

Proposition 1

3 Auxiliary propositions

3.1 Let us consider in view of (14) solutions of the ordinary differential equations

| (16) |

which are given by

| (17) |

In the case i.e., we have: if then as and if then as Further is a solution of (16).

In the case the solution under for any We note that the case is more general than the case (we recall that in the latter case ,).

In the case the solution is convexly decreasing under not too large . It attains zero at the moment given by

| (18) |

and

In what follows we deal with the case

| (19) |

3.2. Our next goal is to obtain estimates for solutions of the equation

| (20) |

(cf. (14) ) for a given continuous function

Lemma 2

Let Let be two solutions of (20) such that on for some with Then

| (21) |

Remark 3

It is known that for the Bessel process BESδ has the representation

where is standard Brownian Motion, a.s., and that in particular (See [18]; for the representation of BESδ is less simple and involves the concept of local time.) From this fact it is not difficult to show that for the solution of (7) may be represented as

Thus, with it holds that

for and that in particular is continuous and of bounded variation. From this it follows that (22) holds for when and is an arbitrary Brownian trajectory, and then inequality (21) in Lemma 2 goes through for

3.3 Now consider (20) for a continuous function satisfying

| (23) |

for some and Along with (16), (20) with (23), we further consider the equations

| (24) | ||||

| (25) |

Let us assume that and consider an to be specified below, that satisfies

| (26) |

The solutions of (16), (20) with (23), (24), and (25) are denoted by , and respectively, where is given by (17). By using (17) we derive straightforwardly that

| (27) | ||||

| (28) |

Note that and Due to the comparison theorem for ODEs (see, e.g., [10], Ch. 3), the inequality

which is fulfilled in view of (23) for then implies that

| (29) |

The same inequality holds for replaced by We thus get

| (30) |

Proposition 4

Proof. We estimate the difference It holds

| (32) |

where

Further,

| (33) |

Using the inequality for any and we get

whence

Therefore

From (33) we have that

and so due to (32) we get

Since for any and under (26), we obtain

Corollary 5

Under the assumptions of Proposition 4, we get by taking

where and only depend on the parameters of the CIR process under consideration and the time horizon

4 One-step approximation

Let us suppose that for is known exactly. In fact, may be considered as a realization of a certain stopping time. Consider on some interval with given by the ODE (cf. (14)),

| (34) | ||||

Assume that

| (35) |

Due to (15), the solution of (1) on is obtained via

| (36) |

Though equation (34) is (just) an ODE, it is not easy to solve it numerically in a straightforward way because of the non-smoothness of We are here going to construct an approximation of via Proposition 4. To this end we simulate the point by simulating as being the first-passage (stopping) time of the Wiener process to the boundary of the interval So, for and, moreover, the random variable which equals either or with probability is independent of the stopping time A method for simulating the stopping time is given in Subsection 4.1 below. Proposition 4 and Corollary 5 then yield,

| (37) | ||||

where is the solution of the problem

that is given by (17) with We so have,

where due to (37),

| (38) |

We next introduce the one-step approximation of on by

| (39) |

Since if and if the one-step approximation (39) for is given by

| (40) | |||

| (43) |

with being drawn from the distribution of

| (44) |

where is an independent standard Brownian motion. For details see Subsection 4.1 below. We so have the following theorem.

Theorem 6

For the one-step approximation due to the exact starting value we have the one step error

| (45) |

4.1 Simulation of and

For simulating we utilize the distribution function

where is the first-passage time of the Wiener process to the boundary of the interval A very accurate approximation of is the following one:

and it holds

(see for details [16], Ch. 5, Sect. 3 and Appendix A3 ). Now simulate a random variable uniformly distributed on Then compute which is distributed according to That is, we have to solve the equation for instance by Newton’s method or any other efficient solving routine. Next set

For simulating in (40) we observe that (44) is equivalent with

We next sample from the distribution function where is the known conditional distribution function (see [16], Ch. 5, Sect. 3)

| (46) |

and set The simulation of the last step looks rather complicated and may be computationally expensive. However it is possible to take for simply any value between and e.g. zero. This may enlarge the one-step error on the last step but does not influence the convergence order of the elaborated method. Indeed, if we set to be zero, for instance, on the last step, we get instead of (40), and

| (47) |

Remark 7

We have in any step the random number of steps before reaching say is finite with probability one, and For details see [16], Ch. 5, Lemma 1.5. In a heuristic sense this means that, if we have convergence of order we obtain accuracy for an (expected) number of steps similar to the standard Euler scheme.

5 Convergence theorem

In this section we develop a scheme that generates approximations where and are realizations of a sequence of stopping times, and show that the global error in approximation is in fact an aggregated sum of local errors, i.e.,

with provided that for and so

Let us now describe an algorithm for the solution of (1) on the interval in the case Suppose we are given and such that

For the initial step we use the one-step approximation according to the previous section and thus obtain (see (40) and (45))

where

| (48) |

Suppose that

We then go to the next step and consider the expression

| (49) |

where is the solution of the problem (see (34))

| (50) | ||||

Now, in contrast to the initial step, the value is unknown and we are forced to use instead. Therefore we introduce as the solution of the equation (50) with initial value From the previous step we have that Hence, due to Lemma 2,

| (51) |

Let be the first-passage time of the Wiener process to the boundary of the interval If then set else set In order to approximate for let us consider along with equation (50) the equation

Due to Proposition 3 and Corollary 5 it holds that

| (52) |

and so by (51) we have

| (53) |

We also have (see (49))

| (54) |

where

| (55) |

We so define the approximation

| (56) | ||||

| (57) |

and then set

| (58) | |||

| (61) |

cf. (40) and (44). We thus end up with a next approximation such that

| (62) |

From the above description it is obvious how to proceed analogously given a generic approximation sequence of approximations with that satisfies by assumption

| (63) | ||||

| (64) | ||||

Indeed, consider the expression

where is the solution of the problem

| (65) | ||||

for a to be determined. Since is unknown we consider as the solution of the equation (65) with initial value Due to (64) and Lemma 2 again, we have

In order to approximate for we consider the equation

| (66) |

By repeating the procedure (52)-(62) we arrive at

| (67) |

satisfying

| (68) |

with

| (69) | ||||

Remark 8

In principle it is possible to use the distribution function (see (46)) for constructing for However, we rather consider for the approximation

where (a) for is an arbitrary continuous function satisfying

and (b) for one may take As a result we get similar to (47) an insignificant increase of the error,

Let us consolidate the above procedure in a concise way.

5.1 Simulation algorithm

So, under the assumption (63) we obtain the estimate (68) (possibly enlarged with a term ). The next theorem shows that if a trajectory of under consideration is positive on then the algorithm is convergent on this trajectory. We recall that in the case almost all trajectories are positive, hence in this case the proposed method is almost surely convergent.

Theorem 9

Proof. Let us define

| (70) |

and let We then claim that for all

| (71) |

For we trivially have

Now suppose by induction that for Then due to (69) we have

because of (70). Thus, since it follows that This proves (71) and the convergence for

Remark 10

. In the case where trajectories will reach zero with positive probability, that is convergence on such trajectories is not guaranteed by Theorem 9. So it is important to develop some method for continuing the simulations in cases of very small One can propose different procedures, for instance, one can proceed with standard SDE approximation methods relying on some known scheme suitable for small (e.g. see [3]). However, the uniformity of the simulation would be destroyed in this way. We therefore propose in the next section a uniform simulation method that may be started in a value close to zero.

6 Simulation of trajectories near to zero

Henceforth we assume that Let us suppose that and consider conditions that guarantee that under Of course in the case this is trivially fulfilled, and we thus consider the case yielding

We so need

| (72) |

Since we are interested in properties of algorithms when we may further assume w.l.o.g. that i.e.

| (73) |

Under assumption (73), (72) is obviously fulfilled when If we need

which is fulfilled if

| (74) |

Note that (73) is equivalent with and so (74) is the condition we were looking for. Conversely, if then with positive probability. In view of the above considerations, one may carry out the algorithm of Subsection 5.1 as long as (74) is fulfilled. Let us say that was the last step where (74) was true. Then the aggregated error of due to the algorithm up to step may be estimated by (cf. (63) and (64)),

| (75) |

Let us recall that our primal goal is a scheme where almost surely and uniformly in In this respect, and in particular in the case where trajectories may attain zero with positive probability, it is not recommended to carry out scheme 5.1 all the way through until (74) is not satisfied anymore. Indeed, if the trajectory attains zero, the worst case almost sure error bound would then be when all would be close to hence of order That is, no convergence on such trajectories. We therefore propose to perform scheme 5.1 up to a (stopping) index defined by

| (76) |

where is a positive constant and is to be determined suitably. A pragmatic choice would be (see Remark 11). Due to (76) and (75) with replaced by we then have,

| (77) |

for some constant

Let us now fix a realization and consider two solutions of equation (1) starting at the moment from (known value) and (true but unknown value), denoted by and respectively, Let be the first time at which the solution of (1) attains the level hence

A construction of the distribution function of is worked out in Section 6.1. Let us now denote with (For simplicity and w.l.og. we assume that We then naturally set

The solutions and correspond to two solutions and of (20) with starting in and respectively. Due to Lemma 2, see Remark 3, and (77) it thus follows that

| (78) |

and in particular

In contrast to the previous steps we now specify the behavior of on by

| (79) |

which we actually do not know. However, we do know that and that is bounded on by Therefore, if we just take a straight line that connects the points and as an approximation for then By (78) and (79) we then also have

Thus, the accuracy of the approximation to for outside the band is of order and for inside the band of order But, at the boundary point the accuracy is of order again. Finally, the scheme may be continued from the state

with the algorithm of Subsection 5.1.

Remark 11

From the above construction it is clear that for in (76) the accuracy for outside the band and for inside the band are of the same order. However, an exponent would give a higher accuracy outside the band and at the exit points of the band while inside the band the accuracy is worse but uniformly bounded by

6.1 Simulation of

In order to carry out the above simulation method for trajectories near zero we have to find the distribution function of where is the first-passage time of the trajectory to the level For this it is more convenient to change notation and to write (1) in the form

| (80) |

where without loss of generality we take the initial time to be The function

is the solution of the first boundary value problem of parabolic type ([16], Ch. 5, Sect. 3)

| (81) |

with initial data

| (82) |

and boundary conditions

| (83) |

To get homogeneous boundary conditions we introduce The function then satisfies:

| (84) |

| (85) |

The problem (84)-(85) can be solved by the method of separation of variables. In this way the Sturm-Liouville problem for the confluent hypergeometric equation (the Kummer equation) arises . This problem is rather complicated however. Below we are going to solve an easier problem as a good approximation to (84)-(85). Along with (80), let us consider the equations

| (86) | ||||

| (87) |

with It is not difficult to prove the following inequalities

| (88) |

According to (88), we consider three boundary value problems: first (81)-(83) and next similar ones for the equations

| (89) |

From (88) it follows that

hence

where

As the band for a certain is narrow due to small enough the difference will be small and so we can consider the following problem

| (90) |

| (91) |

as a good approximation of (84)-(85). Henceforth we write By separation of variables we get as elementary independent solutions to (90), where

| (92) | |||

| (93) |

It can be verified straightforwardly that the solution of (93) can be obtained in terms of Bessel functions of the first kind (e.g. see [4]),

with

| (94) |

Since has to be bounded for we may take (regardless the sign of (!))

| (95) |

In our setting we have i.e.

The following derivation of a Fourier-Bessel series for is standard but included for convenience of the reader. Denote the positive zeros of by for example,

| (96) |

Then the (homogeneous) boundary condition yields

| (97) |

and we have

By the well-known orthogonality relation

we get by setting

Now set

| (98) |

For we have due to the initial condition

So for any

| (99) |

Further it holds that

by well-known identities for Bessel functions (e.g. see [4]), and (99) thus becomes

| (100) |

So, from (92) (95), (97), (100), and (98) we finally obtain

| (101) |

Example 13

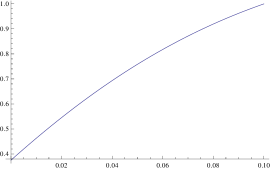

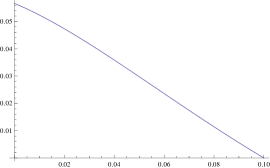

We now consider some numerical examples concerning in (101) and given by (101) due to (102). Note that actually in (101) the function only depends on and That is, depends on and the product Let us consider a CIR process with and let us take We then compare which is given by (101) for due to (94) (see Example 12), with given by (101) for due to (102). The results are depicted in Figure 1. The sums corresponding to (101) are computed with five terms (more terms did not give any improvement).

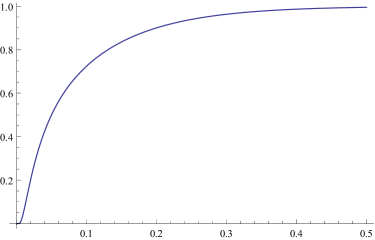

Normalization of

For practical applications it is useful to normalize (101) in the following way. Let us treat as essential but fixed parameter, introduce as new parameters

and consider the function

that is connected to (101) via

For simulation of we need to solve the equation

For this we set and solve the normalized equation and then take

Note that

We have plotted in Figure 2 the normalized function for

References

- [1] A. Alfonsi (2005). On the discretization schemes for the CIR (and Bessel squared) processes. Monte Carlo Methods Appl., v. 11, no. 4, 355-384.

- [2] A. Alfonsi (2010). High order discretization schemes for the CIR process: Application to affine term structure and Heston models. Math. Comput., v. 79 (269), 209-237.

- [3] L. Andersen (2008). Simple and efficient simulation of the Heston stochastic volatility model. J. of Compute Fin., v. 11, 1-42.

- [4] H. Bateman, A. Erdélyi (1953). Higher Transcendental Functions. MC Graw-Hill Book Company.

- [5] M. Broadie, Ö. Kaya (2006). Exact simulation of stochastic volatility and other affine jump diffusion processes. Oper. Res., v. 54, 217-231.

- [6] J. Cox, J. Ingersoll, S.A. Ross (1985). A theory of the term structure of interest rates. Econometrica, v. 53, no. 2, 385-407.

- [7] S. Dereich, A. Neuenkirch, L. Szpruch (2012). An Euler-type method for the strong approximation of the Cox-Ingersoll-Ross process. Proc. R. Soc. A 468, no. 2140, 1105–1115.

- [8] H. Doss (1977). Liens entre équations différentielles stochastiques et ordinaries. Ann. Inst. H. Poincaré Sect B (N.S.), v. 13, no. 2, 99-125.

- [9] P. Glasserman (2003). Monte Carlo Methods in Financial Engineering. Springer.

- [10] P. Hartman (1964). Ordinary Differential Equations. John Willey & Sons.

- [11] D.J. Higham, X. Mao (2005). Convergence of Monte Carlo simulations involving the mean-reverting square root process. J. Comp. Fin., v. 8, no. 3, 35-61.

- [12] D.J. Higham, X. Mao, A.M. Stuart (2002). Strong convergence of Euler-type methods for nonlinear stochastic differential equations. SIAM J. Numer. anal., v. 40, no. 3, 1041-1063.

- [13] S.L. Heston (1993). A closed-form solution for options with stochastic volatility with applications to bond and currency options. Review of Financial Studies, v. 6, no. 2, 327-343.

- [14] N. Ikeda, S. Watanabe (1981). Stochastic Differential Equations and Diffusion Processes. North-Holland/Kodansha.

- [15] I. Karatzas, S.E. Shreve (1991). Brownian Motion and Stochastic Calculus. Springer.

- [16] G.N. Milstein, M.V. Tretyakov (2004). Stochastic Numerics for Mathematical Physics. Springer.

- [17] G.N. Milstein, M.V. Tretyakov (2005). Numerical analysis of Monte Carlo evaluation of Greeks by finite differences. J. Comp. Fin., v. 8, no. 3, 1-33.

- [18] D. Revuz, M. Yor (1991). Continuous Maringales and Brownian Motion. Springer

- [19] L.C.G. Rogers, D. Williams (1987). Diffusions, Markov Processes, and Martingales, v. 2 : Ito Calculus. John Willey & Sons.

- [20] H.J. Sussmann (1978). On the gap between deterministic and stochastic ordinary differential equations. Annals of probability, v. 6, 19-41.