Convex Optimal Uncertainty Quantification

Abstract

Optimal uncertainty quantification (OUQ) is a framework for numerical extreme-case analysis of stochastic systems with imperfect knowledge of the underlying probability distribution. This paper presents sufficient conditions under which an OUQ problem can be reformulated as a finite-dimensional convex optimization problem, for which efficient numerical solutions can be obtained. The sufficient conditions include that the objective function is piecewise concave and the constraints are piecewise convex. In particular, we show that piecewise concave objective functions may appear in applications where the objective is defined by the optimal value of a parameterized linear program.

Key words.

convex optimization, uncertainty quantification, duality theory

AMS subject classifications.

90C25, 90C46, 90C15, 60-08

1 Introduction

In many applications, given a cost function that depends on a random variable in , we would like to compute , where is the probability distribution of . If is known exactly, this amounts to a numerical integration problem. However, sometimes we only have access to partial information (e.g., moments) about that can be expressed in the following form:

| (1.1) |

where and are (real) vector-valued functions. Since the constraints appearing in (1.1) are used to specify the available information about , we will refer to these constraints as information constraints throughout the paper. Using only information constraints, it is generally impossible to compute the exact value of . Instead, we can only hope to obtain a lower or upper bound of .

Generally speaking, such bounds are unavailable in closed form except for several special cases, where the bound can be obtained from probability inequalities. To this end, this paper focuses on computing such bounds numerically by solving infinite-dimensional optimization problems over the set of probability distributions that satisfy the information constraints. We follow Owhadi et al. [20] and refer to this problem as optimal uncertainty quantification (OUQ) for convenience (note that the actual OUQ framework presented in [20] is more general and is capable of dealing with unknown functions in addition to unknown probability distributions). Formally, an example of OUQ problems is an optimization problem in the following form:

| (1.2) | |||||

| (1.3) | |||||

| (1.4) | |||||

| (1.5) | |||||

where is a random variable in , and is the probability distribution of . The function is real-valued. The functions and are (real) vector-valued. The inequality (1.3) is entry-wise. Formulas (1.3) and (1.4) correspond to information constraints on . For example, when and consist of powers of , it implies that information on the moments of is available. The set is the support of the distribution. For brevity, the phrase “almost surely” is dropped later in this paper. Note that the condition that is a probability distribution imposes the following implicit constraints:

| (1.6) |

Main result

Despite being infinite-dimensional, a large class of OUQ problems can be reduced to equivalent finite-dimensional optimization problems that have the same optimal value [20]. This reduction operates in several steps, in which the first one is a generalization of linear programming in spaces of measures [22, 23]. Although this reduction permits a numerical solution to OUQ problems, the resulting reduced problems may be highly constrained and non-convex.

The paper focuses on the first reduction step and presents sufficient conditions (Theorem 1.1) under which an OUQ problem can be reduced to a finite-dimensional convex optimization problem. Specifically, we require that the functions , , and satisfy the following conditions:

-

1.

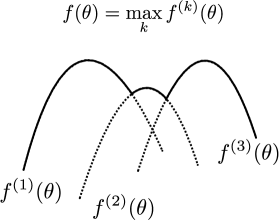

The function is piecewise concave, i.e., it can be written as

(1.7) where each function is concave.

-

2.

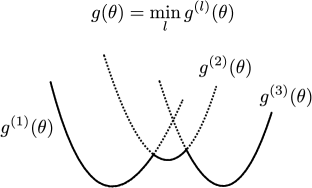

Each entry of the function is piecewise convex, i.e., each can be written as

(1.8) where each function is convex.

-

3.

The function is affine. Namely, it can be represented as

(1.9) for appropriate choices of and .

Figure 1 illustrates how piecewise concave and piecewise convex functions look like in dimension one. In general, these functions are neither concave nor convex. Later in section 4, we will give a number of useful examples of piecewise concave/convex functions in the context of OUQ applications.

The main result of the paper is that the OUQ problem (1.2) can be solved by considering an equivalent finite-dimensional convex optimization problem, given that conditions (1.7)–(1.9) are satisfied. For notational simplicity, we will only present the case where is defined from to (i.e., ):

| (1.10) |

The results can be easily generalized to the case of .

Theorem 1.1.

Theorem 1.1 provides sufficient conditions under which an OUQ problem can be solved in a tractable manner, as guaranteed by the convexity of the optimization problem (1.11). The proof of Theorem 1.1 will be given later in section 3. The paper is organized as follows. Section 2 gives a historical perspective of OUQ by reviewing related work and previous results on equivalent finite-dimensional reduction of OUQ problems. Section 3 presents the main result on convex reformulation of OUQ, which can be derived either from the primal or the dual form of the original OUQ problem. Section 4 gives several applications of the convex OUQ formulation. Section 5 provides numerical illustrations of the main theoretical result.

Remarks on the OUQ formulation

Problem (1.2) can also be written in a form without the equality constraint (1.4) and the support constraint (1.5). The equality constraint (1.4) can be eliminated by introducing the following inequality constraints:

The support constraint can be shown as equivalent to

| (1.15) |

where is the 0-1 indicator function:

In order to prove this, we note that

automatically holds due to the fact that is non-negative. Therefore, the condition (1.15) is equivalent to

which is equivalent to (1.5). However, we will still use the original form in problem (1.2) to distinguish these constraints from pure inequalities. In some cases, problem (1.2) is also called the (generalized) moment problem or problem of moments, since the information constraints (1.3) and (1.4) often consist of moments of the distribution or can be considered as generalized moments of the distribution.

2 Optimal uncertainty quantification

2.1 Historical perspective and related work

Among various convex formulations of OUQ, one important special case is when

| (2.1) |

where and is the 0-1 indicator function. Solution to the OUQ problem will yield a sharp bound of the probability under the given information constraints. This bound is also called Chebyshev-type bound or generalized Chebyshev bound. The earliest theoretical analysis of such bounds can be traced back to the pioneering work by Chebyshev and his student Markov (see Krein [14] for an account of the history of this subject along with his substantial contributions). We also refer to early work by Isii [10, 11, 12] and Marshall and Olkin [16].

As related in Owhadi and Scovel [19, section 2], OUQ starts from the same mindset and applies it to more complex problems that extend the base space to functions and measures. Instead of developing sophisticated mathematical solutions, OUQ develops optimization problems and reductions, so that their solution may be implemented on a computer, as in Bertsimas and Popescu’s [3] convex optimization approach to Chebyshev inequalities, and the decision analysis framework of Smith [24]. Interestingly, many inequalities in probability theory can be viewed as OUQ problems. One such example is Markov’s inequality, which has its origin in the following problem [14, Page 4] (according to Krein [14], although Chebyshev did solve this problem, it was his student Markov who supplied the proof in his thesis):

“Given: length, weight, position of the centroid and moment of inertia of a material rod with a density varying from point to point. It is required to find the most accurate limits for the weight of a certain segment of this rod.”

Although the statement of the problem assumes knowledge about both the first and second moments (centroid and moment of inertia), Markov has also obtained an inequality (known as Markov’s inequality) that is optimal with respect to the information contained in the first moment.

Example 2.1 (Markov’s inequality).

Suppose is a nonnegative univariate random variable whose probability distribution is unknown, but its mean is given. For any , Markov’s inequality [9, Page 311] gives a bound for as follows, regardless of the probability distribution of :

Substituting into the above inequality, we obtain

In the OUQ framework, the problem of obtaining a tight bound for becomes

In fact, it can be shown that the optimal value of the above problem is . Namely, Markov’s inequality produces a tight bound.

Recent works on convex optimization approach to Chebyshev inequalities (motivated by efficient numerical methods such as the interior-point method [18]) also include Lasserre [15], Popescu [21], and Vandenberghe et al. [26] for convex formulations for different classes of sets in (2.1) (e.g., ellipsoids, semi-algebraic sets). Compared to these formulations that only consider the case where can be expressed in the form of (2.1), our formulation extends the objective function to the more general class of piecewise concave functions as given in (1.7).

Besides indicator set functions (2.1), another class of functions that appear in convex formulations are functions that are both convex and piecewise affine:

| (2.2) |

where and are given constants. This form arises in applications such as stock investment [8] and logistics [2]. Since all affine functions are concave, we can define in (1.7), so that objective functions in the form of (2.2) become a special case of our formulation.

Besides the conditions on , there are convex formulations that incorporate information constraints in the form of moment constraints. Oftentimes these constraints are limited to the mean and covariance, such as in Delage and Ye [8]. For constraints on moments of arbitrary order, it is known that the feasibility of moment constraints can be represented as a linear matrix inequality on a Hankel matrix consisting of the given moments [5, Page 170]. The linear matrix inequality formulation allows OUQ problems to be cast as semidefinite programs, if the objective function is the 0-1 indicator function [21] or a linear combination of the moments [5, Page 170]. The same technique can also be extended to the case of complex moments and functions [6]. Compared to constraints on moments of arbitrary order, our formulation is restricted to inequality constraints on the moments of even order but can handle the broader class of piecewise concave objective functions.

To summarize, this paper shows that a convex reformulation of OUQ problems can be obtained for the broader class of piecewise concave objective functions , which contains both the 0-1 indicator function (2.1) and functions of the form (2.2) that are considered in previous formulations by others. The information constraints in the formulation are required to be inequalities containing piecewise convex functions, which extend the moment constraints in previous formulations at the expense of relaxing equality to inequality constraints.

2.2 Finite reduction of OUQ problems

The perhaps surprising fact is that an OUQ problem can always be reduced to an equivalent finite-dimensional optimization problem that yields the same optimal value. The following proposition is originally due to Rogosinski [22]. See also Shapiro [23] for an extension to conic linear programs and Owhadi et al. [20] for a more general result that allows other kinds of constraints.

Proposition 2.1 implies that the optimal value of any OUQ problem can always be achieved by a discrete probability distribution with finite support, whose number of Dirac masses depends on the information constraints. In the following, we give a simple example (reproduced from Owhadi et al. [20]) to illustrate this property.

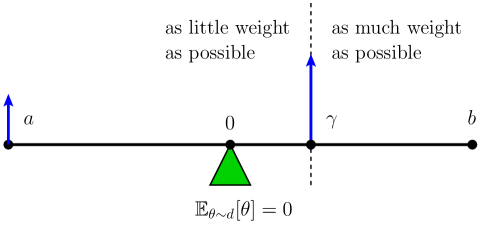

Example 2.2 (“Seesaw”, see also [20]).

The following example OUQ problem illustrates the fact that the optimal value of an OUQ problem can be achieved by a discrete distribution with finite support; it also shows the connection between the number of information constraints and the number of Dirac masses required in the (optimal) discrete distribution. Consider the following OUQ problem for a scalar random variable :

where , and are constants satisfying In order to maximize , we would want to assign as much probability as possible within . On the other hand, the condition requires that the probability within and that within must be identical. This condition is analogous to a seesaw pivoted at with two end points at and (Figure 2). It is not difficult to see that the best assignment is to put all the probability on the right side at (for least leverage) and all the probability on the left side at (for most leverage). This assignment implies that the optimal distribution can be achieved with a discrete distribution consisting of Dirac masses at and . Indeed, since there is only one scalar constraint, the total number of Dirac masses predicted by Proposition 2.1 is .

3 Convex optimal uncertainty quantification

We will now prove Theorem 1.1, the main result of this paper. Namely, under conditions (1.7)–(1.9), the OUQ problem (1.2) can be reformulated as a finite-dimensional convex optimization problem. We will prove Theorem 1.1 in two ways by considering the primal form and dual form of the OUQ problem, respectively.

3.1 Primal form

According to the finite reduction property, it suffices to use a finite number of Dirac masses to represent the optimal distribution. In particular, due to the special form of the objective function and constraints, these Dirac masses satisfy a useful property as given in the following lemma.

Lemma 3.1.

Proof.

We will prove the lemma by contradiction. From Proposition 2.1, we know that the optimal probability distribution can be achieved by a discrete distribution with finite support. By way of contradiction, assume that the optimal discrete distribution contains more than Dirac masses. Then, by an argument using the pigeonhole principle, the optimal discrete distribution must contain two Dirac masses located at and with probabilities and , respectively, such that both and achieve maximum at and minimum at for some and , i.e.,

Consider a new Dirac mass whose probability and location are given by

It can be verified that replacing the two previous Dirac masses and with this new Dirac mass will still yield a valid probability distribution (i.e., the probability masses sum up to 1). Moreover, the new distribution will give an objective that is no smaller than the previous one, since

| (3.1) |

where the second inequality is an application of Jensen’s inequality and last equality uses the fact that and achieve maximum at .

On the other hand, it can be shown that the new distribution will remain as a feasible solution. The equality constraint on remains feasible, because

The feasibility of the inequality constraint on can be proved by using a similar argument as in (3.1) by observing that evaluated under the new distribution will be no larger than that under the original distribution, because

Therefore, the two old Dirac masses can be replaced by the new single one without affecting optimality, from which the uniqueness of follows. ∎

The number of Dirac masses given by Lemma 3.1 depends only on and , and is independent from that given by the finite reduction property. By using Lemma 3.1, we can obtain an equivalent convex optimization problem for the original problem (1.2), as given in Theorem 1.1 presented in section 1. The proof of Theorem 1.1 is given as follows.

Proof.

(of Theorem 1.1) According to Lemma 3.1, we can optimize over a new set of Dirac masses whose probability weights and locations are (, ). The requirement that the set of Dirac masses forms a valid probability distribution imposes the constraints (1.12) and (1.13). Under the new set of Dirac masses, the objective function can be rewritten as

where the second equality uses the fact that achieves maximum at . Unless otherwise noted, the range of the summation over the indices and is given by and . As will be shown later, this step is critical, since is generally not concave, but is concave. Similarly, we have

The final form can be obtained by introducing new variables for all and and choosing to optimize over instead of . Each term in the sum in the objective function

is a perspective transform of a concave function and hence is concave [5, Page 39]. Therefore, the objective function is concave. Likewise, the term

is convex, and corresponding constraint (1.14) is also convex. All the other constraints are affine and do not affect convexity. In conclusion, the final optimization problem is a finite-dimensional convex problem and is equivalent to the original problem (1.2) due to Lemma 3.1. ∎

Remark.

The perspective transformation of , which appears in the objective function (1.11), maintains the convexity of . For certain forms of , the perspective transformation can be directly handled by numerical optimization software. For example, when (where is a positive semidefinite matrix) is a quadratic form, the perspective transformation becomes , which can be handled directly by the quad_over_lin() function included in CVX [7].

Meanwhile, there are a couple straightforward extensions to Theorem 1.1.

Multiple inequality constraints

Lemma 3.1 and Theorem 1.1 can be generalized to the case of based on a similar proof, except that the number of Dirac masses becomes . It can be shown that, among all Dirac masses, there is at most one Dirac mass that achieves maximum at and minimum at for any given indices and :

The corresponding convex optimization problem can be formed by following a similar procedure as in the proof of Theorem 1.1.

Support constraints

It is possible to impose certain types of constraints on the support without affecting convexity. Specifically, we can allow

| (3.2) |

where each is a convex set. In order to show that the corresponding OUQ problem remains convex, we use the fact that the support constraint (1.5) is equivalent to

| (3.3) |

as presented at the beginning of section 2. When satisfies (3.2), we have

| (3.4) |

which is piecewise convex.

If the support constraint (or equivalently (3.3)) is added to an OUQ problem where and satisfy (1.7) and (1.10), the number of Dirac masses becomes . Denote these Dirac masses as and (; ; ). Then inequality constraint (3.3) becomes

where the first term appears due to the constant in (3.4). Recall that for all and . Then we have

| (3.5) |

for all and . The fact implies that the actual number of Dirac masses needed in this case is .

In particular, when each is a convex polytope, the corresponding support constraint has a simpler form. It is known that any convex polytope can be represented as an intersection of affine halfspaces. Namely, each can be expressed as:

for certain constants and (cf. [4]). Then the support constraint (3.5) becomes affine constraints

for all and .

3.2 Dual form

The convex reformulation of OUQ that appears in Theorem 1.1 can also be derived from the Lagrange dual problem of (1.2). Derivation from the dual problem is particularly useful in distributionally robust stochastic programming, as studied by Delage and Ye [8], Mehrotra and Zhang [17]. First of all, the Lagrangian of problem (1.2) can be written as

The last two terms are due to the constraints (1.6). From the Lagrangian, the Lagrange dual can be derived as

By including the conditions on the Lagrange multipliers, i.e.,

we can obtain the the dual problem as

| (3.6) | |||||

| (3.7) | |||||

which is a linear program with an infinite number of constraints (also known as a semi-infinite linear program). Under standard constraint qualifications, as shown by Isii [10, 11, 12], strong duality holds so that we can solve the dual problem (3.6) to obtain the optimal value of problem (1.2). Analysis on strong duality can also be found in Karlin and Studden [13], Akhiezer and Krein [1], Smith [24], and Shapiro [23].

The inequality constraint (3.7) implies that the optimal solution must satisfy

which allows us to eliminate the inequality constraint (3.7) and rewrite problem (3.6) as

| (3.8) | |||||

As it turns out, Theorem 1.1 can also be proved from the dual form (3.8). Similar to section 3.1, we will only prove for the case of for notational convenience. First, we present the following lemma for later use in the proof.

Lemma 3.2.

Given a set of real-valued functions , the optimal value of the optimization problem

| (3.9) | |||||

is .

Proof.

Proof.

(of Theorem 1.1) For convenience, we define the objective function in (3.8) as

where is now reduced to a scalar in the case of . Recall that

Because , we have

and, by Lemma 3.2,

where (; ) need to satisfy and for all and . Similar to the previous proof in section 3.1, we introduce new variables , and rewrite as

Next, because is concave and is convex for all and , and is affine, if problem (3.8) is feasible, then the optimal solution is a saddle point of

Therefore, problem (3.8) achieves the same optimal value as the following problem, obtained by exchanging the order of maximization and minimization:

| (3.10) | |||||

Using the fact

we can further rewrite problem (3.10) as problem (1.11) in Theorem 1.1. ∎

Remark.

The dual form (3.8) is often used to derive a numerically favorable solution for distributionally robust stochastic programming, in which an optimization problem in the following form is being solved:

| (3.11) |

where the set is defined by the information constraints (1.3)–(1.5). Using the dual form (3.8), it can be seen that the distributionally robust stochastic programming problem (3.11) can be rewritten as

| (3.12) | |||||

If is convex in , then the objective function in (3.12) is a pointwise maximum of convex functions of , , and , and hence problem (3.12) is convex. In some cases (e.g., Delage and Ye [8], Mehrotra and Zhang [17]), the objective function in (3.12) can be rewritten using linear matrix inequalities to permit a more efficient numerical solution.

4 Applications

In this section, we illustrate the applications of the convex OUQ framework through a number of examples. In particular, we show that piecewise concave functions are expressive enough in modeling the objective function for several different applications.

4.1 Piecewise convex functions as information constraints

In the next, we list several examples of piecewise convex functions that can be used as information constraints.

Example 4.1 (Even-order moments).

Consider the case where the random variable is univariate and the function in the inequality constraint is given by (for some positive integer ). It can be verified that is convex, which is a special case of piecewise convex functions.

Example 4.2.

Consider for any convex set . The function can be used to specify the probability , since . The function can be rewritten as

where the function is defined as

| (4.1) |

for any . It can be verified that both and are convex in , and hence is piecewise convex.

4.2 Piecewise concave functions as objectives

We begin by two simple examples of piecewise concave functions that are used as objective functions in OUQ.

Example 4.3 (Convex and piecewise affine).

Example 4.4.

Consider for any convex set . The function can be used to specify the probability , since . The function can be rewritten as

where the the definition of follows from (4.1). It can be verified that both and are concave in , and hence is piecewise concave.

Aside from the two simple examples presented above, we present in the following a very important form of objective functions that is also piecewise concave.

Example 4.5 (Optimal value of parameterized linear programs).

This form of objective functions is defined by the optimal value of a parameterized linear program whose constraints contain nonlinear terms of the random variable . The following is the linear program under consideration:

| (4.2) | |||||

where , , , , and each component of the function is convex in .

For any fixed , denote the optimal value of problem (4.2) by . We assume that there exists a nonempty set such that problem (4.2) is feasible for all , i.e., for all . We will show that is piecewise concave on . Namely, can be expressed as

for some and concave functions . First, we consider the Lagrange dual problem of problem (4.2), which is given as follows:

| (4.3) | |||||

Since problem (4.2) is feasible, strong duality between problems (4.2) and (4.3) holds, so that is also the optimal value of problem (4.3). Notice that problem (4.3) is a linear program for any given . Since the optimal value of a linear program can always be achieved at a vertex of the constraint set, we can rewrite as

where is the set of vertices of the polytope

Since for all , and each component of is convex, we know that is concave, which implies that is piecewise concave.

In the following, we give two applications in which the objective function is defined through the optimal value of a linear program.

Revenue maximization with stochastic supplies

We start with a simple application that cannot be handled by previous convex formulations of OUQ. Consider a scenario where a merchant would like to estimate the expected revenue from selling (divisible) goods to potential customers, whereas the quantity of the goods follows an unknown probability distribution. We assume that the merchant can only choose to sell the goods exclusively to one of the customers. Each customer offers a different price, and the merchant tries to maximize the revenue by selling to the one who offers the best price. In addition, price from each customer drops as the quantity increases, which makes the revenue a nonlinear function of the quantity. This model can capture the situation in which the customer gradually loses interest in purchasing as the quantity increases. Eventually, a customer stops purchasing beyond a certain maximum quantity, at which point the merchant can no longer increase the revenue by selling to that customer.

We denote by the total quantity of goods. We denote by the corresponding revenue of selling quantity of goods to customer . In the following, we shall assume that is concave. Then, the maximum revenue of selling quantity of goods is given by

which is piecewise concave by definition. We can also write (as a function of ) as the optimal value of the following optimization problem:

| (4.4) | |||||

It can be verified that problem (4.4) has the same form as problem (4.2), which also implies that is piecewise concave.

DC optimal power flow with stochastic demands

Consider a power network modeled as a graph , where is the set of nodes, and is the set of edges. We assume that a subset of the nodes are capable of generating electric power to supply other loads in the network. The power generation at any node is denoted by . For convenience, we assume for all . We assume that the power demand at any node is stochastic, and the demand can be modeled by a function that depends on some random variable . As an example, the power demand that comes from the usage of air conditioning depends on the ambient temperature, which can be modeled as a random variable. Specifically, we can define as the vector of ambient temperatures at different nodes (corresponding to different geographical regions), so that depends on the temperature at node . We shall assume that the demand function is concave (in fact, also monotonic) in for all .

We consider a simplified DC power flow model of the network adopted from Stott et al. [25]. Denote by the power flow from node to node . The power flow is determined by the difference in the voltage angles of and as follows:

| (4.5) |

where is the susceptance of the transmission line between and . The amount of power flow is also limited by the transmission capacity of the line connecting nodes and :

| (4.6) |

The net supply at node is given by

| (4.7) |

We require that there should be enough net supply to satisfy the demand at any node , which implies

| (4.8) |

The goal of the DC optimal power flow problem is to minimize the total generation cost while respecting the constraints (4.5)–(4.8). We assume that the generation cost at node can be modeled by a convex and piecewise affine function:

where and are given constants. Then, the DC optimal power flow problem can be cast as an optimization problem as follows:

| (4.5)–(4.8). |

We can rewrite the above optimization problem as a linear program by introducing additional slack variables (also denoted by , in an abuse of notation):

| (4.9) | |||||

| (4.5)–(4.8) | |||||

It can be verified that problem (4.9) has the same form as problem (4.2), and hence its optimal value is a piecewise concave function of .

5 Numerical examples

This section demonstrates the numerical aspect of convex OUQ through two examples. The first example compares bounds obtained by asymmetric and incomplete information using convex OUQ and the algorithm introduced by Bertsimas and Popescu [3]. The second example follows from the application in revenue maximization (with stochastic supplies) given in section 4; in particular, it presents a scenario where convex OUQ is (up to the authors knowledge) the only applicable convex formulation, since previous formulations do not handle arbitrary piecewise concave objective functions.

Bound on the tail of Gaussian distributions

This example applies convex OUQ and the algorithm introduced by Bertsimas and Popescu [3] in order to compute an upper bound of (where is a given constant) in presence of incomplete and asymmetric information.

To apply convex OUQ, we assume that we are given the constraints

To apply Bertsimas and Popescu [3] (which has not been designed to incorporate the constraint ), we assume that we are given the constraints

for some fixed . All the constants, including and , are computed from the standard Gaussian distribution .

Table 1 lists the results obtained from the two algorithms. As a baseline of comparison, it also lists the exact value of as computed by numerically evaluating the integral

It can be seen that the above integral is related to the complementary error function as follows:

where the complementary error function is defined as:

The algorithm by Bertsimas and Popescu eventually gives a tighter bound by using more moment-based information, since it is capable of incorporating equality constraints. On the other hand, when higher moment () information is unavailable, convex OUQ gives a better bound by being able to handle more types of constraints such as . In terms of computational complexity, the algorithm by Bertsimas and Popescu requires solving a semidefinite program, whereas our convex OUQ formulation only requires solving a second-order cone program. It can be seen from Table 1 that the computational time of our convex OUQ formulation is also comparable to the algorithm by Bertsimas and Popescu.

| Method | Upper bound for | CPU time (in seconds, 100 runs) |

| B & P () | ||

| B & P () | ||

| B & P () | ||

| convex OUQ () | ||

| Exact value | — |

Revenue estimation

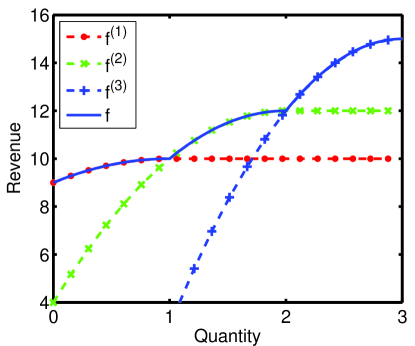

This numerical example follows from problem (4.4) presented in section 4. For simplicity, this example considers 3 customers, so that the revenue can be defined as

where is the revenue due to customer , and is the (random) quantity of the goods. We choose

where models the rate at which the price from customer drops, is the maximum quantity that customer is willing to purchase, and is maximum revenue from customer . It can be verified that each is concave, and thus is piecewise concave. The functions and each are plotted in Figure 3 based on the parameters used in this example.

The information constraints include constraints on the first and second moments, i.e.,

and tail probabilities

These information constraints specify the first and second order statistics on the (random) quantity of the goods , as well as the probabilities that the quantity goes below a given lower bound or above a given upper bound , respectively. As we mentioned in Example 4.2, both and are piecewise convex, and each can be constructed from 2 convex functions. Therefore, we have , and . Consequently, the total number of Dirac masses is .

The corresponding convex optimization problem that solves for an upper bound of the expected revenue is

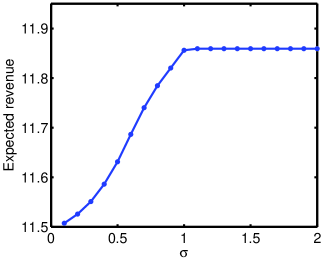

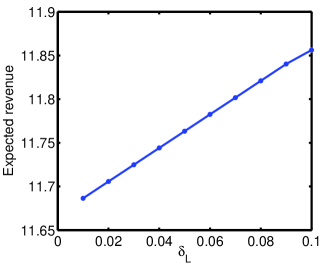

Figure 4 shows the effect of changing the second moment and the tail probabilities. As expected, loosening the constraints (i.e., increasing either or ) increases the upper bound of . In the case of changing the second moment (Figure 4), the upper bound stops increasing beyond a certain point, which implies that the information constraint on the second moment is no longer active.

6 Conclusions

This paper introduces the following new sufficient conditions under which an OUQ problem can be reformulated as a convex optimization problem: (1) the objective is piecewise concave, (2) the inequality information constraints are piecewise convex, and (3) the equality constraints are affine. Constraints on the support of the probability distribution can also be incorporated, as long as the support is a finite union of convex sets. We prove the result based on two different approaches, which start with the primal and the dual forms of the original OUQ problem, respectively. Through a number of examples, we also illustrate the use of the convex OUQ formulation in several different applications, such as estimating the maximum revenue of selling goods to customers and the operational cost of power systems.

Acknowledgment

This work was supported in part by NSF grant CNS-0931746 and AFOSR grant FA9550-12-1-0389.

References

- [1] N. I. Akhiezer and M. G. Kreĭn. Some Questions in the Theory of Moments, volume 2 of Translations of Mathematical Monographs. American Mathematical Society, 1962.

- [2] D. Bertsimas, X. V. Doan, K. Natarajan, and C.-P. Teo. Models for minimax stochastic linear optimization problems with risk aversion. Mathematics of Operations Research, 35(3):580–602, 2010.

- [3] D. Bertsimas and I. Popescu. Optimal inequalities in probability theory: A convex optimization approach. SIAM Journal on Optimization, 15(3):780–804, 2005.

- [4] D. Bertsimas and J. N. Tsitsiklis. Introduction to linear optimization. Athena Scientific, Belmont, MA, 1997.

- [5] S. P. Boyd and L. Vandenberghe. Convex optimization. Cambridge University Press, 2004.

- [6] C. I. Byrnes and A. Lindquist. A convex optimization approach to generalized moment problems. In K. Hashimoto, Y. Oishi, and Y. Yamamoto, editors, Control and Modeling of Complex Systems, Trends in Mathematics, pages 3–21. Birkhäuser Boston, 2003.

- [7] CVX Research, Inc. CVX: Matlab software for disciplined convex programming, version 2.0. http://cvxr.com/cvx, Aug. 2012.

- [8] E. Delage and Y. Ye. Distributionally robust optimization under moment uncertainty with application to data-driven problems. Operations Research, 58(3):595–612, 2010.

- [9] G. R. Grimmett and D. R. Stirzaker. Probability and Random Processes. Oxford University Press, 3rd edition, 2001.

- [10] K. Isii. On a method for generalizations of Tchebycheff’s inequality. Annals of the Institute of Statistical Mathematics, 10(2):65–88, 1959.

- [11] K. Isii. On sharpness of Tchebycheff-type inequalities. Annals of the Institute of Statistical Mathematics, 14(1):185–197, 1962.

- [12] K. Isii. Inequalities of the types of Chebyshev and Cramér–Rao and mathematical programming. Annals of the Institute of Statistical Mathematics, 16(1):277–293, 1964.

- [13] S. Karlin and W. J. Studden. Tchebycheff systems: With applications in analysis and statistics, volume 376. Interscience, New York, 1966.

- [14] M. G. Kreĭn. The ideas of P. L. C̆ebys̆ev and A. A. Markov in the theory of limiting values of integrals and their further development. In E. B. Dynkin, editor, Eleven papers on Analysis, Probability, and Topology, American Mathematical Society Translations, Series 2, Volume 12, pages 1–122. American Mathematical Society, New York, 1959.

- [15] J. B. Lasserre. Bounds on measures satisfying moment conditions. The Annals of Applied Probability, 12(3):1114–1137, 2002.

- [16] A. W. Marshall and I. Olkin. Multivariate Chebyshev inequalities. Annals of Mathematical Statistics, 31(4):1001–1014, 1960.

- [17] S. Mehrotra and H. Zhang. Models and algorithms for distributionally robust least squares problems. Mathematical Programming, 146(1–2):123–141, 2013.

- [18] Y. Nesterov and A. S. Nemirovskii. Interior-Point Polynomial Algorithms in Convex Programming. SIAM, Philadelphia, PA, 1994.

- [19] H. Owhadi and C. Scovel. Brittleness of Bayesian inference and new Selberg formulas. Communications in Mathematical Sciences, to appear; preprint available at arXiv:1304.7046.

- [20] H. Owhadi, C. Scovel, T. Sullivan, M. McKerns, and M. Ortiz. Optimal uncertainty quantification. SIAM Review, 55(2):271–345, 2013.

- [21] I. Popescu. A semidefinite programming approach to optimal-moment bounds for convex classes of distributions. Mathematics of Operations Research, 30(3):632–657, 2005.

- [22] W. W. Rogosinski. Moments of non-negative mass. Proceedings of the Royal Society of London. Series A. Mathematical and Physical Sciences, 245(1240):1–27, 1958.

- [23] A. Shapiro. On duality theory of conic linear problems. Nonconvex Optimization and its Applications, 57:135–155, 2001.

- [24] J. E. Smith. Generalized Chebychev inequalities: Theory and applications in decision analysis. Operations Research, 43(5):807–825, 1995.

- [25] B. Stott, J. Jardim, and O. Alsaç. DC power flow revisited. IEEE Transactions on Power Systems, 24(3):1290–1300, 2009.

- [26] L. Vandenberghe, S. Boyd, and K. Comanor. Generalized Chebyshev bounds via semidefinite programming. SIAM Review, 49(1):52–64, 2007.