Large deviations for the Ornstein-Uhlenbeck process with shift

Abstract.

We investigate the large deviation properties of the maximum likelihood estimators for the Ornstein-Uhlenbeck process with shift. We propose a new approach to establish large deviation principles which allows us, via a suitable transformation, to circumvent the classical non-steepness problem. We estimate simultaneously the drift and shift parameters. On the one hand, we prove a large deviation principle for the maximum likelihood estimates of the drift and shift parameters. Surprisingly, we find that the drift estimator shares the same large deviation principle as the one previously established for the Ornstein-Uhlenbeck process without shift. Sharp large deviation principles are also provided. On the other hand, we show that the maximum likelihood estimator of the shift parameter satisfies a large deviation principle with a very unusual implicit rate function.

Key words and phrases:

Ornstein-Uhlenbeck process with shift, Maximum likelihood estimates, Large deviations1. INTRODUCTION

Consider the Ornstein-Uhlenbeck process with linear shift , observed over the time interval

| (1.1) |

where the drift parameter , the initial state and the driven noise is a standard Brownian motion. This process is widely used in financial mathematics and it is known as the Vasicek model, see e.g. [9, 12]. The maximum likelihood estimates of the unknown parameters and are given by

| (1.2) |

and

| (1.3) |

A wide range of literature is available on the asymptotic behavior of and . It is well-known [11] that and are both strongly consistent estimators of and and their joint asymptotic normality is given by

| (1.4) |

where the limiting matrix

with . Moreover, concentration inequalities for and and moderate deviations were established by Gao and Jiang [7], while Jiang [10] recently obtained the joint law of iterated logarithm as well as Berry-Esseen bounds. In the particular case , Florens-Landais and Pham [6] proved the large deviation principle (LDP) for , while sharp large deviation principles (SLDP) were established in [2]. We also refer the reader to [1] for the sharp large deviations in the non-stationary case and .

Our goal is to extend these investigations by establishing the large deviations properties of the maximum likelihood estimators of the drift and shift parameters and in the situation where and are estimated simultaneously. We shall propose a new approach to prove LDP which allows us, via a suitable transformation, to circumvent the classical non-steepness problem. In particular, it could be possible to apply the same approach for Jacobi or Cox-Ingersoll-Ross processes [4, 13].

The paper is organized as follows. In Section 2, we establish an LDP for the couple Via the contraction principle, one can realize that shares the same LDP as the one previously established for the Ornstein-Uhlenbeck process without shift. One can also observe that satisfies an LDP with a very unusual implicit rate function. An SLDP for the sequence is also provided. Section 3 is devoted to three keystone lemmas which are at the core of our analysis. All the technical proofs of Sections 2 and 3 are postponed to Appendices A, B, and C.

2. Large deviations results.

Our large deviations results are as follows.

Theorem 2.1.

The couple satisfies an LDP with good rate function

| (2.1) |

A direct application of the contraction principle [3] immediately leads to the two following corollaries.

Corollary 2.2.

The sequence satisfies an LDP with good rate function

| (2.2) |

Corollary 2.3.

The sequence satisfies an LDP with good rate function

| (2.3) |

Proof.

The proofs are given is Section 4. ∎

Remark 2.4.

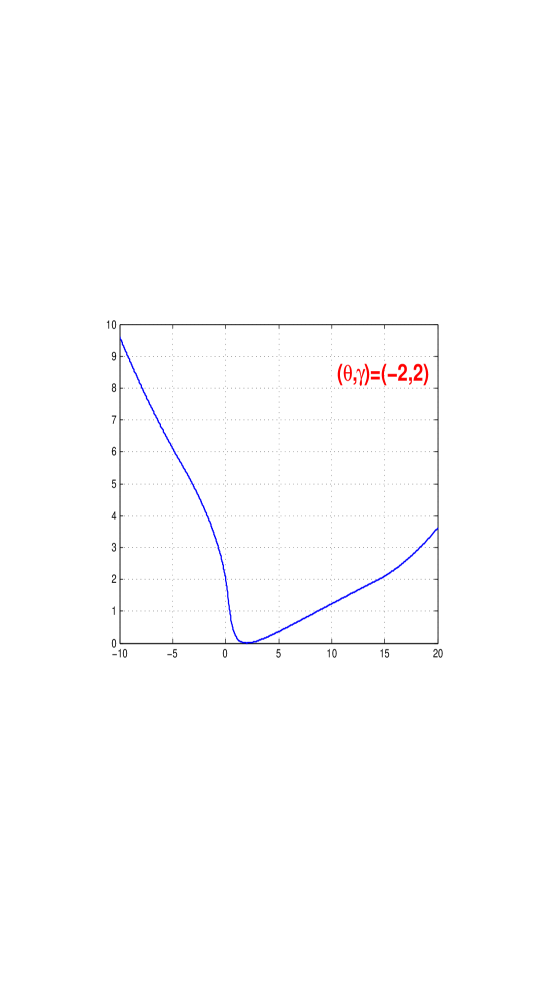

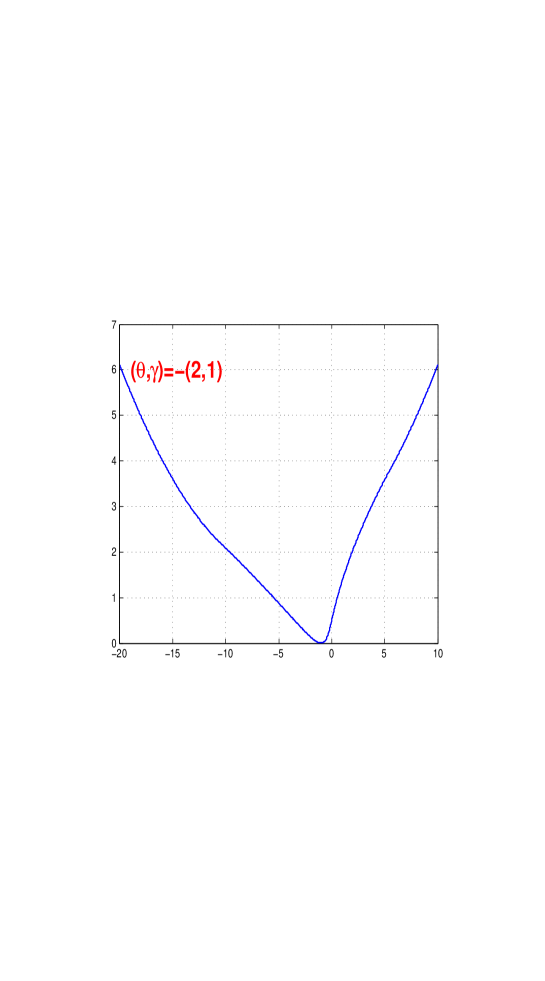

On the one hand, one can observe that shares exactly the same LDP as the one previously established by Florens-Landais and Pham [6] for the Ornstein-Uhlenbeck without shift . On the other hand, satisfies an LDP with a very unusual rate function. Unfortunately, an explicit expression for this rate function is quite complicated. Its very particular form is given in the special cases and in Figure 1 below.

Our goal is now to improve Corollary 2.2 by a first order SLDP for . It is of course possible to establish SLDP of any order for the sequence . However, for clearness sake, we have chosen to restrict ourself to a first order expansion.

Theorem 2.2.

Consider the Ornstein-Uhlenbeck process with shift given by (1.1) where the drift parameter .

-

a)

For all , we have for large enough,

(2.4) while for ,

(2.5) where

(2.6) (2.7) -

b)

For all with , we have for large enough,

(2.8) where

(2.9) (2.10) -

c)

For , we have for large enough,

(2.11) where

(2.12) -

d)

For , we have for large enough,

(2.13)

3. Three keystone lemmas.

First of all, let us recall some elementary properties of the Ornstein-Uhlenbeck process with linear shift [9], [11]. One can observe that the process can be rewritten as where

and is the Ornstein-Uhlenbeck process without shift

By the same token, if

we clearly have where

Therefore, the random vector

where the covariance matrix is given by

| (3.1) |

with

Denote by the normalized cumulant generating function of the triplet

defined, for all , by

Our first lemma deals with the extended real function defined as the pointwise limit of .

Lemma 3.1.

Let be the effective domain of

and set . Then, for all , we have

| (3.2) |

Proof.

The proof in given in Appendix A. ∎

A direct calculation shows that the function is steep, which means that the norm of its gradient goes to infinity for any sequence in the interior of converging to a boundary point of . This is the reason why we are able to deduce an LDP for the couple . In order to establish the SLDP for the drift parameter , it is necessary to modify our strategy. To be more precise, we shall now focus our attention on the normalized cumulant generating function of the couple

where

which is given, for all , by

The reason for this is twofold. On the one hand, it is not possible to deduce an SLDP for via . On the other hand, it immediately follows from (1.2) that

| (3.3) |

However, one can observe that for all , where, for all , stands for the random variable

| (3.4) |

Our second lemma provides the full asymptotic expansion for . Denote by the extended real function defined as the pointwise limit of .

Lemma 3.2.

Let be the effective domain of

and set , . Then, for all and large enough, we have

| (3.5) |

where

| (3.6) | |||||

| (3.7) |

Moreover, the remainder may be explicitly calculated as a rational function of , , and . In addition, can be extended to the two-dimensional complex plane and it is a bounded analytic function as soon as the real parts of its arguments belong to the interior of .

Proof.

The proof in given in Appendix B. ∎

Our third lemma relies on the Karhunen-Loève expansion of the process . Denote by the class of all real-valued continuous functions such that where is continuous. Moreover, let be the spectral density of the stationary Ornstein-Uhlenbeck process without shift given, for all , by

| (3.8) |

Lemma 3.3.

One can find two sequences of real numbers and both in such that

| (3.9) |

where are independent standard random variables. Moreover, for all , there exist two constants and that do not depend on such that, for large enough, for all and

| (3.10) |

Consequently, for all and such that , and for large enough, we have

Finally, if , the empirical spectral measure

| (3.11) |

satisfies, for any continuous with compact support

| (3.12) |

Proof.

The proof is given in Appendix C. ∎

4. Proofs of the large deviations results.

First of all,

where

| (4.1) |

The following lemma shows that the sequences and share the same LDP. We refer the reader to [3] for the classical notion of exponential approximation.

Lemma 4.1.

The sequences of random vectors and are exponentially equivalent, that is to say, for all ,

| (4.2) |

In particular, if satisfies an LDP with good rate function , then the same LDP holds for .

Proof.

It is easy to see from the very definition of our estimates given in (1.2), (1.3) and (4.1) that

where . On the event with , we have

Hence, for all ,

| (4.3) |

On the one hand, it is not hard to see that for all ,

| (4.4) |

As a matter of fact, we recall that is a Gaussian random variable. Consequently, for all ,

which immediately leads to (4.4), as . By the same token, we already saw at the beginning of Section 3 that is a Gaussian random variable. It implies that for all such that ,

| (4.5) |

On the other hand, we immediately deduce from Lemma 3.2 together with Gärtner-Ellis’s theorem that the sequence satisfies an LDP with speed and good rate function

Therefore, for all such that ,

| (4.6) |

Finally, it follows from the conjunction of (4.3), (4.4), (4.5), and (4.6) that, for all and for large enough,

| (4.7) |

where

One can observe that if goes to infinity, tend to infinity, which is exactly what we wanted to prove. ∎

We are now in the position to prove our LDP results. Our strategy is to establish an LDP for the triplet

and then to make use of the contraction principle [3] in order to prove Theorem 2.1 via Lemma 4.1. The limiting cumulant generating function of the above triplet was already calculated in Lemma 3.1. It is not difficult to check that the function is steep on its effective domain . Consequently, we deduce from Gärtner-Ellis’s theorem that the above triplet satisfies an LDP with good rate function given by the Fenchel-Legendre transform of ,

We can prove after some straightforward calculations that

| (4.8) |

Hereafter, it follows from the well-known Itô’s formula that

| (4.9) |

which implies that

where is the continuous function given, for all such that , by

Therefore, we infer from the contraction principle given e.g. by Theorem 4.2.1 of [3], together with Lemma 4.1, that the sequences of random vectors and share the same LDP with good rate function

where the infimum over the empty set is equal to .

Finally, we obtain the rate function given by (2.1) thanks to elementary calculations, which completes the proof of Theorem 2.1.

5. Proofs of the sharp large deviations results.

5.1. Proof of Theorem 2.2, first part

First of all, it follows from straightforward calculations that the effective domain given in Lemma 3.2 can be rewritten as

In addition, for all , let and denote

| (5.1) | |||||

| (5.2) |

The function is not steep as the derivative of is finite at the boundary of . Moreover, if and only if with given by (2.6). Finally, one can observe that only if . We shall focus our attention on the SLDP in the easy case . Denote by the normalized cumulant generating function of the random variable . We can split into two terms, with

| (5.3) | |||||

| (5.4) |

where stands for the expectation after the usual change of probability

| (5.5) |

On the one hand, we can deduce from Lemma 3.2 that

| (5.6) |

It remains to establish an asymptotic expansion for which can be rewritten as

| (5.7) |

Lemma 5.1.

For all , we have

| (5.8) |

Proof.

Denote by the characteristic function of under . As , it follows from (2.6) that and . Moreover, (5.5) immediately implies that

| (5.9) |

First of all, we deduce from Lemma 3.3 that for large enough, belongs to . As a matter of fact, as soon as for all and large enough, we obtain from Lemma 3.3 and (5.9) that

| (5.10) | |||||

For all small enough such that we denote

It follows from Lemma 3.3 that it exists some constants and , depending only on , such that

| (5.11) |

Hence, we infer from (5.10) and (5.11) that for large enough,

| (5.12) |

which clearly ensures, whenever , that

| (5.13) |

Consequently, we find from (5.13) that for large enough, belongs to . Therefore, we obtain from Parseval’s formula that , given by (5.7), can be rewritten as

| (5.14) |

However, we deduce from Lemma 3.2 that, for all ,

| (5.15) |

as , which means that the distribution of under converges to the standard distribution. Finally, (5.8) follows from (5.14), (5.15) and the Lebesgue dominated convergence theorem. ∎

5.2. Proof of Theorem 2.2, second part

We shall now proceed to the proof of the SLDP in the more complex case with . One can easily check that the function , given by (5.1), is decreasing and reaches its minimum at the right boundary point of the domain . Therefore, as in [2] or [1], it is necessary to make use of a slight modification of the usual strategy of change of probability given in (5.5). There exists a unique , which belongs to the interior of and converges to its border , solution of the implicit equation

| (5.16) |

It leads to the decomposition with

| (5.17) | |||||

| (5.18) |

where stands for the expectation after the time-varying change of probability

| (5.19) |

We deduce from (5.1), (5.2) together with (5.16) that

where and . Consequently, it follows from straightforward calculations that

| (5.20) | |||

| (5.21) | |||

| (5.22) |

Moreover, we can show via (B.4) and (B.5) that remains bounded when goes to infinity. Hence, Lemma 3.2 together with (5.20), (5.21), and (5.22) imply that

| (5.23) | |||||

Moreover, the second term can be rewritten as

| (5.24) |

Lemma 5.2.

For with , we have

| (5.25) |

where

| (5.26) |

Proof.

Denote by the characteristic function of under . We infer from (5.19) that for all ,

| (5.27) |

Moreover, we obtain from (5.20) and (5.21) that for large enough and for all such that ,

where and are given by (2.9) and (5.26). Consequently, as soon as ,

| (5.28) |

and the remainder is uniform. By the same token,

| (5.29) |

Therefore, we deduce from Lemma 3.2 together with (5.28), (5.29) and the boundedness of , that for all such that ,

| (5.30) |

where

It means that the distribution of under converges to , where stands for an random variable. It also implies that, for large enough, belongs to . Hereafter, we deduce from Parseval’s formula that , given by (5.24), can be rewritten as

| (5.31) |

We split into two terms, , where

| (5.32) | |||||

| (5.33) |

with . On the one hand, it follows from (5.33) that is negligible, as

| (5.34) |

On the other hand, we find from (5.30) that for large enough

which leads, thanks to Lemma 7.3 in [2], to

| (5.35) |

5.3. Proof of Theorem 2.2, third part

Assume now that which means that with . There exists a unique , which belongs to the interior of and converges to its border , solution of the implicit equation

| (5.36) |

We deduce from (5.1), (5.2) together with (5.36) that

where and . We obviously have

which leads to

It implies after some elementary calculations that

| (5.37) | |||

| (5.38) | |||

| (5.39) |

Hereafter, we shall make use of the decomposition given by

| (5.40) | |||||

| (5.41) |

where stands for the expectation after the time-varying change of probability

| (5.42) |

We obtain from (B.4) and (B.5) that remains bounded when goes to infinity. Hence, it follows from Lemma 3.2 together with (5.37), (5.38), and (5.39) that

| (5.43) |

On the other hand, can be rewritten as

| (5.44) |

Lemma 5.3.

For , we have

| (5.45) |

Proof.

Via the same lines as in the proof of Lemma 5.1, we find that the characteristic function of , under , belongs to . Hence, it follows from Parseval’s formula that

| (5.46) |

However, we obtain from (5.37) and (5.38) that

| (5.47) |

where is given by (2.12) and . By the same token,

| (5.48) |

Therefore, we deduce from Lemma 3.2 together with (5.47), (5.48) and the boundedness of , the pointwise convergence

| (5.49) |

It shows that the distribution of under converges to , where and are two independent random variables sharing the same distribution. Finally, we obtain from (5.46) together with (5.49) and the Lebesgue dominated convergence theorem that

which achieves the proof of Lemma 5.3. ∎

5.4. Proof of Theorem 2.2, fourth part

Assume now that . We want to obtain the leading asymptotic behavior of . For all , we have the decomposition where

First of all, if

it is not hard to see that is negligible. As a matter of fact, we deduce from the simple upper bound together with (4.5) that

Next, we recall that the sequence satisfies an LDP with good rate function given by (2.2). Consequently,

which clearly implies that . From now on, it only remains to establish the leading asymptotic behavior of . We already saw at the beginning of Section 3 that the random vector

Therefore,

and is the Gaussian probability density function of . Moreover, as , the conditional distribution of given is with and . Furthermore, for all , can be rewritten as

where

One can easily check that

It follows from standard asymptotic analysis of Gaussian distribution tails that

where is uniform with respect to . We split into two terms,

We find from a careful asymptotic expansion inside the integral together with the change of variables and Lebesgue’s dominated convergence theorem, that

By the same token, we also obtain that

which is exactly what we wanted to prove.

Appendix A: Proof of Lemma 3.1.

For all , let

We shall calculate the limit of the normalized cumulant generating function of the random variable . First of all, as in [5], it follows from Girsanov’s formula associated with (1.1) that

where stands for the expectation after the change of probability,

with and

Consequently, if we assume that and if we choose and , reduces to

| (A.1) |

where the vectors and are given by

and is the diagonal matrix of order two

Under the new probability , is Gaussian random vector with zero mean and covariance matrix given by (3.1). Denote by the square matrix of order two

where stands for the identity matrix of order two. We clearly have

which leads to

| (A.2) |

Hence, as , it follows from (A.2) that for large enough, the matrix is positive definite. It is also not hard to see from (3.1) that

| (A.3) |

Therefore, we obtain from standard Gaussian calculations that

| (A.4) |

where . On the one hand, we immediately obtain from (A.2) that

| (A.5) |

On the other hand, we clearly have

where and . Consequently, we obtain from (A.2) and (A.3) that

| (A.6) |

Finally, we deduce from (A.4) together with (A.5) and (A.6) that

| (A.7) |

which is exactly what we wanted to prove.

Appendix B: Proof of Lemma 3.2.

Our goal is to establish the full asymptotic expansion for the normalized cumulant generating function of the random variable . First of all, as in the proof of Lemma 3.1, it follows from Girsanov’s formula associated with (1.1) that

where and . Consequently, if we assume that and if we choose and , reduces to

with , where the vectors and are given by

and is the diagonal matrix of order two

We already saw in Appendix A that under the new probability , is Gaussian random vector with zero mean and covariance matrix given by (3.1). Let be the square matrix of order two

It is not hard to see that

| (B.1) |

Hence, we deduce from (A.3) that

| (B.2) |

Consequently, as soon as , we find from (B.2) that for large enough, the matrix is positive definite. Therefore, it follows from standard Gaussian calculations that

| (B.3) |

We shall now to improve convergence (B.2) as follows. We have for large enough

| (B.4) |

where is given by

and is such that with a rational function. As a matter of fact, we already saw from (B.1) that

where . We obtain from straightforward calculations that

In addition, we deduce from the definition of and that

Consequently,

where and are rational functions, leading to (B.4). Furthermore, concerning the last term in (B.3), we have for large enough

| (B.5) |

where is given by

with

Moreover, the remainder is such that with a rational function. As a matter of fact, we have previously remark that for large enough, . Consequently, is well defined. With very tedious but straightforward calculations, we obtain that

with

where and are polynomial functions, which clearly implies

(B.5). Finally, Lemma 3.2 follows from the conjunction

of (B.3), (B.4) and (B.5).

Appendix C: Proof of Lemma 3.3.

It follows from (3.4) together with Itô’s formula (4.9) that

| (C.1) |

In addition, we already saw at the beginning of Section 3 that we can split and . Consequently, we have the decomposition

where ,

By using the same notations as in Chapters 2 and 6 of Janson [8], we clearly have

where stands for the homogeneous chaos of order . Hence, we deduce from Theorem 6.2 of [8] that

| (C.2) |

where are independent standard random variables. We also obtain from Theorem 6.2 of [8] that

| (C.3) |

In addition, some rough estimates give us that the right-hand side of (C.3) is uniformly bounded by some constant , depending only on and . As a matter of fact, it exists some constant such that

| (C.4) |

where

and

Therefore, we obtain (3.10) from (C.3) and (C.4). It now remains to show that it exists some constant that do not depend on , such that for all . Since is an open set and the origin belongs to the interior of , it exists such that . For all and for large enough, we deduce from Lemma 3.2 that is finite. It means that the Laplace transform of is well defined on . Hence, Theorem 6.2 of [8] ensures that the characteristic function of is analytic in the strip

So, we necessarily obtain that for large enough, with . Hereafter, the decomposition of given in Lemma 3.3, directly follows from equation (6.7) in Theorem 6.2 of Janson [8]. Our goal is now to pass through the limit in . If we choose such that , we have

| (C.5) |

Moreover, we deduce from Lemma 3.2 that

| (C.6) |

Furthermore, it follows from the properties of and given at the beginning of Section 3 that

which clearly implies

Then, we find from (C.1) that

| (C.7) |

Finally, we obtain from the decomposition of , (C.5), (C.6), (C.7) that

| (C.8) |

where the spectral density is given by (3.8) and for all such that ,

Hence, it follows from (C.8) together with the elementary Taylor expansion of the logarithm and classical complex analysis results that, for any integer ,

Therefore, we obtain the weak convergence (3.12) on the class of functions from the Stone-Weierstrass theorem, which completes the proof

of Lemma 3.3.

References

- [1] Bercu, B., Coutin, L., and Savy, N. Sharp large deviations for the non-stationary Ornstein-Uhlenbeck process. Stochastic Process. Appl. 122, 10 (2012), 3393–3424.

- [2] Bercu, B., and Rouault, A. Sharp large deviations for the Ornstein-Uhlenbeck process. Theory Probab. Appl. 46, 1 (2002), 1–19.

- [3] Dembo, A., and Zeitouni, O. Large deviations techniques and applications, second ed., vol. 38 of Applications of Mathematics (New York). Springer-Verlag, New York, 1998.

- [4] Demni, N., and Zani, M. Large deviations for statistics of the Jacobi process. Stochastic Process. Appl. 119, 2 (2009), 518–533.

- [5] Donati-Martin, C., and Yor, M. On some examples of quadratic functionals of Brownian motion. Adv. in Appl. Probab. 25, 3 (1993), 570–584.

- [6] Florens-Landais, D., and Pham, H. Large deviations in estimation of an Ornstein-Uhlenbeck model. J. Appl. Probab. 36, 1 (1999), 60–77.

- [7] Gao, F., and Jiang, H. Deviation inequalities and moderate deviations for estimators of parameters in an Ornstein-Uhlenbeck process with linear drift. Electron. Commun. Probab. 14 (2009), 210–223.

- [8] Janson, S. Gaussian Hilbert spaces, vol. 129 of Cambridge Tracts in Mathematics. Cambridge University Press, Cambridge, 1997.

- [9] Jeanblanc, M., and Yor, M., and Chesney, M. Mathematical methods for financial markets, Springer Finance. Springer-Verlag London Ltd., London, 2009.

- [10] Jiang, H. Berry-Esseen bounds and the law of the iterated logarithm for estimators of parameters in anOrnstein-Uhlenbeck process with linear drift. J. Appl. Probab. 49, 4 (2012), 978–989.

- [11] Kutoyants, Y. A. Statistical inference for ergodic diffusion processes. Springer Series in Statistics. Springer-Verlag London Ltd., London, 2004.

- [12] Vasicek, O. An equilibrium characterization of the term structure. J. J. Financial Economics 5, (1977), 177–188.

- [13] Zani, M. Large deviations for squared radial Ornstein-Uhlenbeck processes. Stochastic Process. Appl. 102, 1 (2002), 25–42.