1. Introduction

During the last decade, several significant model-free formulas, describing the asymptotic behavior of the implied volatility at extreme strikes, were found. We only mention here R. Lee’s moment formulas (see [15]), tail-wing formulas due to S. Benaim and P. Friz (see [2, 3], see also [4]), asymptotic formulas with error estimates established by the author (see [13, 14]), and

higher order formulas found by K. Gao and R. Lee (see [10]). We refer the interested reader to the book [12] by the author for more information.

The present work was inspired by the paper [8] of S. De Marco, C. Hillairet, and A. Jacquier. The authors of [8] obtained interesting results concerning the asymptotic behavior of the implied volatility at small strikes in the case where the asset price distribution has an atom at zero (see Theorem 3.7 in [8]). Special examples of such models are the constant elasticity of variance model, jump-to-default models, and stochastic models described by processes stopped at the first hitting time of zero (more information can be found in [8]). It is not hard to see that the right-wing behavior of the implied volatility in models with and without atoms is similar. Therefore, general model-free asymptotic formulas for the implied volatility at large strikes, discussed in Chapter 9 of [12], can be used

in stochastic asset price models with atoms. However, the left-wing behavior of the implied volatility in models with and without atoms is qualitatively different. This fact was noticed and explored in [8]. It was also shown in [8] that the general formula formulated in Corollary 9.31 in [12], which describes the left-wing behavior of the implied volatility in terms of the put pricing function, holds for asset price models with atoms (see formula (9) below). For such models, the above-mentioned formula provides only the leading term in the asymptotic expansion of the implied volatility and an error estimate. The authors of [8] found a sharper asymptotic formula, characterizing the left-wing behavior of the implied volatility in models with atoms (see formula (11) below). Note that the impact of an atom at zero on the left-wing asymptotics of the implied volatility was not taken into account in

Section 9.9 of [12]. This omission led to an incorrect description of the asymptotic behavior of the implied volatility at small strikes in the CEV model (see formula (11.22) in Theorem 11.5 in [12]). Only the absolutely continuous part of the distribution of the asset price was taken into account in formula (11.22) mentioned above, while the influence of the atom at zero was ignored.

In this paper, we establish new asymptotic formulas for the implied volatility at small strikes in models with atoms

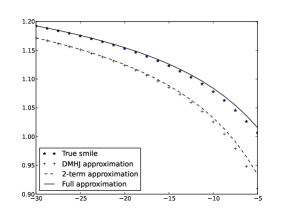

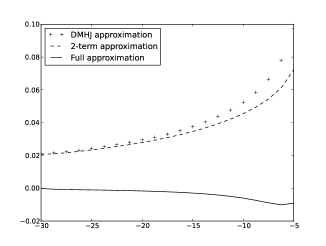

(see formulas (17), (19), and (20) below). These formulas contain three explicit terms in the asymptotic expansion of the implied volatility and an error estimate. Note that the asymptotic formula found in [8] contains two terms and only an incomplete information about the third term is provided. Moreover, there is a qualitative difference between the new formulas and the De Marco-Hillairet-Jacquer formula. In the new formulas, we use the inverse function of a strike-dependent function, while the inverse function of the cumulative standard normal distribution function is employed in [8]. It is shown numerically in Section 5 of the present paper that formula (20) provides a significantly better approximation to the left wing of the implied volatility in the constant elasticity of variance model than the De Marco-Hillairet-Jacquier formula.

Our next goal is to introduce several known objects, which will be used in the rest of the paper, and then formulate our main results. The asset price will be modeled by a non-negative martingale defined on a filtered probability space

. The initial condition for the process is denoted by , and it is assumed that is a positive number. It is also assumed that the interest rate is equal to zero. In the sequel, the symbols and stand for the call and put pricing functions, associated with the price process . These functions are defined

as follows:

|

|

|

In the previous formulas, is the strike price, and is the maturity. The implied volatility is the function, satisfying the following condition:

|

|

|

(1) |

The expression on the left-hand side of (1) is the call pricing function in the Black-Scholes model with the volatility parameter equal to . The function is defined by

|

|

|

(2) |

where is the standard normal cumulative distribution function,

that is, the function

|

|

|

The functions and in (2) are defined by

|

|

|

and

|

|

|

Let , , and set

.

If for every , we have , then the function defined by

|

|

|

(4) |

is a call pricing function (see [12]). The function plays the role of a link between the left-wing and the right-wing asymptotics of the implied volatility (see [12]).

Now, suppose for some . Let us fix such a maturity , and consider , , and as functions of the strike price . Note that for models with atoms, the function , given by (4), is not a call pricing function. Indeed, the function does not satisfy the condition as . However, the function has many features of a call pricing function. For example, it is not hard to see that the Black-Scholes implied volatility exists for all (see Remark 1), and, in addition,

|

|

|

(5) |

for all with . We also have

|

|

|

(6) |

where is a positive function such that

|

|

|

(7) |

The proof of (6) and (7) is simple. Indeed, it follows from

the definition of the put pricing function that

|

|

|

where is the distribution of on the open half-line . Hence,

|

|

|

(8) |

Now it is clear that (8) implies (6). Finally, the proof of the equality in (5)

for asset price models with atoms is the same as the proof of Lemma 9.23 in [12].

We have already mentioned the asymptotic formula in Corollary 9.31 in [12]. This formula is as follows:

|

|

|

|

|

|

|

|

(9) |

as . Using the mean value theorem and the formula

|

|

|

for small values of (the previous formula follows from (4) and (6)), we obtain

|

|

|

(10) |

as . This means that in the presence of atoms, the general formula given in (9) provides only the leading term in the asymptotic expansion of the implied volatility near zero. The expression for the leading term given in (10) can also be predicted from Lee’s moment formula (see [15]). Indeed, for models with atoms, all the moments of negative order of the distribution of the asset price explode.

We will next formulate the main result of [8], adapting it to our notation. Suppose there exists such that

|

|

|

as . Then

|

|

|

|

|

|

|

|

(11) |

as . In (11), the symbol stands for the inverse function of the standard normal cumulative distribution function .

In addition, the function in (11) satisfies a special estimate of order as (see Theorem 3.7 in [8] for more details). Note that the term

|

|

|

(12) |

in (11) is not really the third term in the asymptotic expansion of , because of an interplay

between the expression in (12) and the function as .

In Theorem 7 and Corollary 9 below, we provide asymptotic formulas for the implied volatility at small strikes with three terms and error estimates of order

as . The main novelty in our approach is that instead of the function used in formula (11), we employ a family of strike-dependent inverse functions , , where

|

|

|

(13) |

It is easy to see that for every , the function is strictly increasing on the interval (differentiate!),

and moreover

|

|

|

It follows from the reasoning above that the inverse function exists for all with

|

|

|

(14) |

is strictly increasing on the interval , and maps this interval onto the interval .

According to Remark 5, is defined for all provided that .

In addition, if , then is defined under the following restriction:

|

|

|

(16) |

Note that, given , there exists such that (16) holds for all

and moreover . Therefore, for all ,

we can solve the equations

and by inverting the function .

The next lemma is simple, and we omit the proof.

Lemma 6.

Let , and suppose satisfies (15).

Then the inequality holds if and only if

|

|

|

The next two statements are the main results of the present paper.

Theorem 7.

Let . Then the following asymptotic formula holds for the implied volatility in the asset price models such as above:

|

|

|

|

|

|

|

|

|

(17) |

as .

Corollary 8.

Let , and suppose the random variable is such that

|

|

|

(18) |

as . Then

|

|

|

|

|

|

|

|

|

(19) |

as .

Corollary 9.

Let , and suppose the random variable satisfies condition (18). Then

|

|

|

|

|

|

|

|

|

(20) |

as .

It is not hard to see that Corollary 9 follows from Theorem 7, Remark 4, formulas (6) and (8), and the mean value theorem.

We will prove Theorem 7 in Section 2, while in Section 3 we will derive the De Marco-Hillairet-Jacquier formula from our Theorem 7. In addition, in Section 3

we give estimates for the difference

|

|

|

at small strikes. Section 4 deals with

the left-wing behavior of the implied volatility in the CEV model. Finally, in the last section of the paper (Section 5), we compare the performance of two formulas, providing approximations to the implied volatility at small strikes in the CEV model: the De Marco-Hillairet-Jacquier formula and the formula in Corollary 9 in the present paper.

2. Proof of Theorem 7

We have already mentioned that it suffices to prove the theorem in the case where .

For every small number , set

|

|

|

(21) |

The following assertion provides two-sided estimates for the implied volatility.

Theorem 13.

Let . Then there exists such that

|

|

|

|

|

|

(22) |

for all . In (22), the functions and are defined as follows:

|

|

|

|

|

|

|

|

(23) |

and

|

|

|

|

|

|

|

|

(24) |

Proof of Theorem 13. Our first goal is to find two functions and

satisfying the following conditions:

|

|

|

(25) |

for sufficiently large values of . The inequalities in (25) will allow us to estimate the implied

volatility for large strikes, and hence to characterize the left-wing behavior of the implied volatility .

Let be a real function growing slower than . The function will be chosen later. Put

|

|

|

Then we have

|

|

|

and

|

|

|

Therefore,

|

|

|

|

|

|

|

|

|

(26) |

Our next goal is to estimate the last term in (26). We will use the following known inequalities:

|

|

|

(27) |

The estimates in (27) follow from stronger inequalities formulated in [1], 7.1.13. Taking into account (27), we see that

|

|

|

|

|

|

(28) |

and

|

|

|

|

|

|

|

|

|

(29) |

Let us next suppose that the function has the following form:

|

|

|

(30) |

where is such that

|

|

|

(31) |

In (31), is a real number. Then we have

|

|

|

|

|

|

|

|

|

(32) |

for all . It follows from (28) and the first inequality in (32) that

|

|

|

(33) |

for all . Note that

|

|

|

as .

To get a lower estimate for , we observe that

|

|

|

|

|

|

|

|

|

|

|

|

(34) |

In the proof of (34), we used the inequality

|

|

|

It follows from (29), (30), (32), and (34) that

|

|

|

|

|

|

for all . Therefore, condition (31) implies that for every there

exists a sufficiently large number

such that for every ,

|

|

|

|

|

|

|

|

Next, taking into account (26), (33), and the previous inequality, we see that the following statement holds.

Lemma 14.

For every and all ,

|

|

|

where

|

|

|

|

|

|

|

|

(35) |

Lemma 14 provides estimates for the function , which differ by a quantity of the higher order of smallness than .

Let us next choose the function so that the function , given by the formula in (35)

with instead of , satisfies . It follows from (35)

that

|

|

|

(36) |

Now, using (36) we see that in order to find the value of we should solve the following

quadratic equation:

|

|

|

|

|

|

(37) |

Solving (37) and taking into account (36), we obtain

|

|

|

(38) |

where is defined by (23).

We will next check that the function defined by (38) is admissible, that is,

condition (31) holds for . Recall that , and hence (6)

gives

|

|

|

It follows from the definition of the function

(see (35)) that

|

|

|

Thus

|

|

|

(39) |

It is not hard to see that is a bounded function. Indeed, (39) implies that

|

|

|

where is a positive constant. Therefore,

|

|

|

and thus the function is bounded for large values of . Now, using (39), we see

that

|

|

|

and hence , where is the constant appearing in (31) for the function .

It follows from Lemma 14 and the equality that

|

|

|

where

|

|

|

(40) |

and is given by (23). Therefore,

|

|

|

(41) |

To get a lower estimate for , we will reason similarly. The only difference here is that we replace the equation

by the equation ,

where is defined by (21),

is fixed, and is a function such as in (35), but with an unknown function

instead of the function . Next, we can prove that

|

|

|

where the function is given by (24).

Moreover, the function is bounded for large values of , and

|

|

|

Therefore , where is the constant appearing in (31) for the function .

Let us set

|

|

|

(42) |

with given by (24). It follows that

|

|

|

and hence

|

|

|

(43) |

Now, it is clear that formula (22) in Theorem 13 follows from (5), (40), (41), (42), and (43).

This completes the proof of Theorem 13.

We will next estimate the difference between the lower and the upper estimates for the implied volatility

in formula (22). First, note that since the function is eventually bounded, formula

(36) shows that the function is also eventually bounded. Similarly,

the function is eventually bounded. It follows from (23)

and (24) that the functions and , are equivalent to the function near infinity. Therefore,

|

|

|

|

|

|

|

|

|

(44) |

as .

To estimate the difference , we observe that the function is Lipschitz on every proper subinterval of the interval with the Lipschitz constant independent of on every such interval. Now, it is not hard to see, using (21), (23), and (24) that

|

|

|

as . Next, by taking into account (44), we obtain

|

|

|

(45) |

as .

Theorem 15.

The following formula holds for the implied volatility as :

|

|

|

(46) |

In (46), the function is defined by (23).

Theorem 15 follows from Theorem 13 and (45).

Proof of Theorem 7 (continuation). Expanding the function near zero, we obtain

|

|

|

(47) |

as . Now, using (47) and the fact that the function grows like

, we see that

|

|

|

|

|

|

|

|

|

|

|

|

(48) |

as . Moreover, (23) and (47) imply that

|

|

|

|

|

|

|

|

|

|

|

|

(49) |

as . Next, combining (48) and (49), we see that

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(50) |

as . Now, it is clear that (17) follows from (46) and (50).

This completes the proof of Theorem 7.

3. Corollaries

In the present section, we explain how to derive the asymptotic formula for the left wing of the implied volatility due to De Marco, Hillairet, and Jacquier from our formula (17). Note that formula (17)

is very sensitive to even small changes. Such changes often produce errors of order

as .

The next statement is essentially the result obtained in Theorem 3.7 in [8].

Corollary 17.

Let . Then

|

|

|

|

|

|

(51) |

In (51), the function satisfies the following condition:

|

|

|

where

|

|

|

(52) |

Proof. Our first goal is to replace the expression in formula (17) by the expression , and estimate the error. For the sake of shortness, we put

|

|

|

(53) |

Lemma 18.

Let . Then the following asymptotic formula is valid as :

|

|

|

|

|

|

where

|

|

|

and is defined by (53).

Lemma 18 follows from Theorem 7 and (53).

The next lemma provides an estimate for the function .

Lemma 19.

The following formula holds:

|

|

|

where the function is given by (52).

Proof. Let us first assume that . This assumption is equivalent to the following:

. Then, using (13), we see that for

,

we have

|

|

|

Therefore, for ,

|

|

|

|

|

|

(54) |

and

|

|

|

|

|

|

|

|

Since

|

|

|

the mean value theorem implies that

|

|

|

(55) |

where

|

|

|

|

|

|

Next, using

(6) and (7), we see that

for every there exists such that

|

|

|

(56) |

Moreover, (6), (7), and the mean value theorem imply that

|

|

|

(57) |

where the function is positive and satisfies the following condition:

|

|

|

(58) |

Next, taking into account formulas (55) - (58),

we see that Lemma 19 holds under the condition .

It remains to prove Lemma 19 in the case where . The previous condition means that

. Fix such that . In addition, fix so large that

the following inequalities hold:

|

|

|

(59) |

|

|

|

(60) |

and

|

|

|

(61) |

Next, taking into account (59), we assume that

|

|

|

Then, using (60), we obtain

|

|

|

In addition,

|

|

|

|

|

|

provided that

|

|

|

It follows from (59) and (61) that the number satisfies the previous condition. Therefore,

|

|

|

|

|

|

(62) |

Moreover, (62) and the mean value theorem imply that for ,

|

|

|

where is determined from (55), and

|

|

|

|

|

|

|

|

It is easy to see that

|

|

|

Therefore, for every there exists such that the inequality in

(56) holds for all . Now, the proof of Lemma 19 in the

case where can be completed exactly as in the case when .

Finally, it is not hard to see that Corollary 17 follows from Lemmas 18 and 19.

Let us assume and . We will next compare the numbers and

appearing in formula (20) in Corollary 9 and in the De Marco-Hillairet-Jacquier formula (51), respectively. Recall that if , then

the number is defined for all . On the other hand, if ,

then is defined under the additional restriction

|

|

|

It is clear that if , then and

are positive numbers for all . If , then we have

and .

The remaining case where

|

|

|

(63) |

is interesting. In this case, the number is negative, while the sign of the number

can be positive or negative. We will next clarify the previous statement.

Lemma 20.

Suppose condition (63) holds. Then the following are true:

-

(1)

Let the number be such that

|

|

|

Then .

-

(2)

Let the number be such that

|

|

|

Then .

-

(3)

Let the number be such that

|

|

|

Then .

The proof of Lemma 20 is simple, and we leave it as an exercise for the reader.

The next assertion characterizes the limiting behavior of the difference

.

Theorem 22.

Let . Then

|

|

|

(64) |

Proof of Theorem 22. Suppose , and set

|

|

|

(66) |

and

|

|

|

(67) |

Lemma 24.

For all ,

|

|

|

|

|

|

|

|

where , , and are given by (66) and (67).

Proof of Lemma 24. Using the mean value theorem, we see that

|

|

|

(68) |

where . It follows from (68) that

|

|

|

(69) |

Now, the estimates in Lemma 24 follow from (54) and (69).

Let us continue the proof of Theorem 22. Lemma 24 implies that

|

|

|

|

|

|

|

|

(70) |

Since as , formula (64) follows from (70).

The remaining part of the proof of Theorem 22 resembles that of the second part of Lemma

19. Let us assume . Then we have . Fix such that

|

|

|

(71) |

and suppose is such that

|

|

|

(72) |

and

|

|

|

(73) |

Let

|

|

|

(74) |

Then we have

|

|

|

(75) |

Therefore,

|

|

|

|

|

|

provided that

|

|

|

Since the previous estimates hold for the number , we have

. Here and are defined by (66), and

|

|

|

Next, using (71) and (74), we obtain

.

It follows from (69) and from the inequalities

that

|

|

|

Finally, it is not hard to see that formula (64) with can be derived from the previous estimates and from the equality

.

4. The CEV model

The constant elasticity of variance model (the CEV model) is described by the following stochastic differential equation:

|

|

|

where , , and . If , then the boundary at is naturally absorbing, while for , we impose an absorbing boundary condition. The CEV model was introduced by

J. C. Cox in [6] (see also [7]). A useful information about the CEV model, including some of the results formulated below, can be found in [5]. The CEV process is used in the financial industry to model spot prices of equitites and commodities (see, e.g., [9, 11], and the references therein).

Fix . Then we have

|

|

|

(76) |

Moreover, the density of the absolutely continuous part of the distribution

of is as follows:

|

|

|

|

|

|

(77) |

In (76), is the normalized incomplete gamma function given by

|

|

|

while in (77), the parameter is defined by , the function is the modified Bessel function of the first kind,

and the constant is given by

|

|

|

It is known that as ,

|

|

|

for all . Therefore, it follows from (77) that as ,

|

|

|

(78) |

where

|

|

|

|

|

|

|

|

(79) |

Now, taking into account (78) and (79), we see that as ,

|

|

|

Therefore, condition (18) holds. Finally, applying Corollary 9,

we derive the following statement.

Corollary 26.

Formula (20)

with given by (77) holds for the implied volatility in the CEV model.