Copulas and time series with long-ranged dependences

Abstract

We review ideas on temporal dependences and recurrences in discrete time series from several areas of natural and social sciences. We revisit existing studies and redefine the relevant observables in the language of copulas (joint laws of the ranks). We propose that copulas provide an appropriate mathematical framework to study non-linear time dependences and related concepts — like aftershocks, Omori law, recurrences, waiting times. We also critically argue using this global approach that previous phenomenological attempts involving only a long-ranged autocorrelation function lacked complexity in that they were essentially mono-scale.

pacs:

05.45.Tp, 02.50.-r, 87.85.NgI Introduction

A thorough understanding of the occurences and statistics of extreme events is crucial in fields like seismicity, finance, astronomy, physiology, etc. Kotz and Nadarajah (2000); Embrechts et al. (1997). The analyses of extreme events plays a pivotal role every time an addressed problem has a stochastic nature, since the rare extreme events can have rather strong or drastic consequences— making it widely useful. One theoretical motivation for studying extreme events in a particular field like finance, is to account for the observed fat tails of log-returns (deviation from the Normal distribution in the tails) of stock prices Chakraborti et al. (2011). A more practical motivation is that the extreme events such as “market crashes” or “shocks”, pose a substantial risk for investors, even though these events are rare and do not provide enough data for reliable statistical analyses Politi et al. (2012). It has been observed that common financial shocks are relatively smaller in magnitudes of volatility, the duration, and the number of stocks affected. However, the extremely large and infrequent financial crashes, such as the Black Monday crash, have significant “aftershocks” that can last for many months. This observation is very similar to the “dynamic relaxation” of the aftershock cascade following an earthquake. Hence, it is meaningful to also ask the general scientific question: How is the dynamics of a “complex” system, such as an earthquake fault Bak et al. (2002); Bunde et al. (2003); Corral (2004a); Molchan (2005); Altmann and Kantz (2005); Saichev and Sornette (2007); Sornette et al. (2008); Blender et al. (2008) or a financial market Yamasaki et al. (2005); Wang et al. (2006); Weber et al. (2007); Sazuka et al. (2009); Ren and Zhou (2010), affected when the system undergoes an extreme event? The statistics of return intervals between extreme events is a powerful tool to characterize the temporal scaling properties of the observed time series and to estimate the risk for such hazardous events like earthquakes or financial crashes. Evaluating the return time statistics of extreme events in a stochastic process, is one of the classical problems in probability theory.

Earlier, from an analysis of the probability density functions (PDF) of waiting times for earthquakes, Bak et al. Bak et al. (2002) had suggested a unified scaling law combining the Gutenberg-Richter law, the Omori law, and the fractal distribution law in a single framework. This global approach was later extended by Corral Corral (2003, 2004b), who proposed the existence of a universal scaling law for the PDF recurrence times between earthquakes in a given region. This is useful because, due to the scaling properties, it is possible to analyse the statistics of return intervals for different thresholds by studying only the behavior of small fluctuations occurring very frequently, which have much better statistics and reliability than those of the rare extreme large flucutations. It also reveals a spatiotemporal organization of the seismicity, as suggested by Saichev and Sornette (2007).

In this paper, we review the ideas on temporal dependences and recurrences in discrete time series from several areas of earthquakes, etc.(̃natural sciences) and financial markets (social sciences). We revisit the existing studies, cited above, and redefine the relevant observables in the mathematical language of “copulas”. We propose that copulas is a very general and appropriate framework to study non-linear time dependences and related concepts — like aftershocks, Omori law, recurrences, waiting times. Our overall aim is to study several properties of recurrence times and the statistic of other observables (waiting times, cluster sizes, records, aftershocks) described in terms of the diagonal copula. We hope that these studies can shed light on the -points properties of the process. We also critically argue that that previous phenomenological attempts involving only a long-ranged autocorrelation function, lacked complexity in that they were essentially mono-scale.

The copula

As a tool to study the — possibly highly non-linear — correlations between random variables, “copulas”, i.e. joint distributions of the ranks (see formal definition below), have long been used in actuarial sciences and finance to describe and model cross-dependences of assets, often in a risk management perspective Embrechts et al. (2003, 2002); Malevergne and Sornette (2006). Although the widespread use of simple analytical copulas to model multivariate dependences is more and more criticized Mikosch (2006); Chicheportiche and Bouchaud (2012), copulas remain useful as a tool to investigate empirical properties of multivariate data Chicheportiche and Bouchaud (2012).

More recently, copulas have also been studied in the context of serial dependences in univariate time series, where they find yet another application range: just as Pearson’s coefficient is commonly used to measure both linear cross-dependences and temporal correlations, copulas are well-designed to assess non-linear dependences both transversally or serially Beare (2010); Ibragimov and Lentzas (2008); Patton (2009) — we will speak of “self-copulas” in the latter case.

Notations

We consider a time series of length , as a realization of a discrete stochastic process. The joint cumulative distribution function (CDF) of occurrences () of the process is

| (1) |

We assume that the process is stationary with a distribution , and a translational-invariant joint distribution with long-ranged dependences, as is typically the case e.g. for seismic and financial data.

A realization of at date will be called an “event” when its value exceeds a threshold : “negative event” when , and “positive event” when . The probability of such a ‘negative event’ is , and similarly, the probability that is above a threshold is the tail probability .

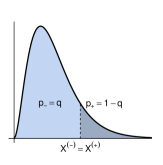

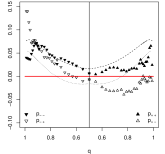

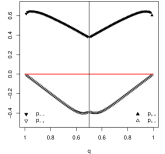

If a unique threshold is chosen, then obviously . This is appropriate when the distribution is one-sided, typically for positive only signals, and one wishes to distinguish between two regimes: extreme events (above the unique threshold), and regular events (below the threshold). This case is illustrated schematically in Fig. 1(b). When the distribution is two-sided, it is more convenient to define, as the -th quantile of , and as the -th quantile, for a given , so that . This allows to investigate persistence and reversion effects in signed extreme events, while excluding a neutral zone of regular events between and , see Fig. 1(a)

When the threshold for the recurrence is defined in terms of quantiles like above (a relative threshold), stationarity is not needed theoretically but much wanted empirically as already said, otherwise the height of the threshold might change every time. In contrast, when the threshold is set as a number (an absolute threshold), there’s no issue on the empirical side, but the theoretical discussion makes sense only under stationary marginal.

The next section recalls several two-points and many-points properties of stationary processes, and discusses associated measures of dependence in light of the copula. This rather theoretical content is followed in Section III by applications to financial data. The definition and some properties of copulas are recalled in appendix, and the Gaussian case with long-ranged correlations is treated.

II Dependences in discrete-time processes

We consider the case where the discrete times in the definition (1) are equidistant (“regularly sampled”).

II.1 Two-points dependence measures

Typical measures of dependences in stationary processes are two-points expectations that only involve one parameter: the lag separating the points in time. For example, the usefulness of the linear correlation function

| (2) |

is rooted in the analysis of Gaussian processes, as those are completely characterized by their covariances, and multi-linear correlations are reducible to all combinations of -points expectations, according to Isserli’s theorem. Some non-linear dependences, like the tail-dependence for example Embrechts et al. (2002); Malevergne and Sornette (2006), are however not expressed in terms of simple correlations, but involve the whole bivariate copula:

| (3) |

where . can be understood as the distribution of the marginal ranks , and contains the full information on bivariate dependence that is invariant under increasing transformations of the marginals. For example, the conditional probability

| (4) |

which is a measure of persistence of the “positive” events, can be written in terms of copulas, together with all three other cases of conditioning

| (5a) | ||||

| (5b) | ||||

| (5c) | ||||

| (5d) | ||||

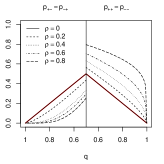

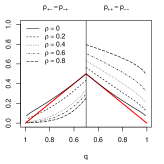

where and are defined similarly to Eq. (4) with obvious inequality sign choices. When and , this is exactly the definition of Boguná and Masoliver (2004), with accordingly , see Fig. 1. Note also that and are straightforwardly related to the so-called ‘tail dependence coefficients’ Chicheportiche (2013).

As an example, consider the Gaussian bivariate copula of the pair , whose whole -dependence is in the linear correlation coefficient . Fig. 2(a) illustrates the conditional probabilities (5) as a function of the threshold, when . A similar plot for the Student copula (with degrees of freedom) is shown in Fig. 2(b): the fatter tails of the joint distribution are responsible for the abnormal behavior of the conditional probabilities in the region . When , the coefficients (5) are all equal to

for any elliptical copula Chicheportiche (2013).

Aftershocks

Omori’s law characterizes the dependence of , i.e. the average frequency of events occurring time steps after a main event. It was first stated in the context of earthquakes occurrences Omori (1895), where this time dependence is power-law:

| (6) |

Notice that any dependence on the threshold must be hidden in according to this description. The average cumulated number of these aftershocks until is thus

| (7) |

with in fact since, when , has no time-dependence, i.e. it counts independent events (white noise), and must thus tend to the unconditional probability.

In order to give a phenomenological grounding to this empirical law also later observed in finance Weber et al. (2007); Petersen et al. (2010), Lillo and Mantegna (2003) model the aftershock volatilities in financial markets as a decaying scale times an independent stochastic amplitude with CDF . As a consequence, and the power-law behavior of Omori’s law results from (i) power-law marginal , and (ii) scale decaying as power-law , so that relation (6) is recovered with . The non-stationarity described by is only introduced in a conditional sense, and might be appropriate for aging systems or financial markets, but we believe that Omori’s law can be accounted for in a stationary setting and without necessarily having power-law distributed amplitudes.

The scaling of with the magnitude of the main shock is encoded in the prefactor , which, for example, accounts for the exponentially distributed magnitudes of earthquakes (Gutenberg-Richter law Gutenberg and Richter (1936)). The linear dependence of on shall be reflected in the diagonal of the underlying copula:

| (8) |

a prediction that can be tested empirically.

Note that Omori’s law is a measure involving only the two-points probability. In the next subsection, we show what additional information many-points probability can reflect.

II.2 Multi-points dependence measures

Although the -points expectations of Gaussian processes reduce to all combinations of -points expectations (2), their full dependence structure is not reducible to the bivariate distribution, unless the process is also Markovian (i.e. only in the particular case of exponential correlation). Furthermore, when the process is not Gaussian, even the multi-linear correlations are irreducible. In the general case, the whole multivariate CDF is needed, but many measures of dependence that we introduce below only involve the diagonal -points copula:111We use a calligraphic in order to make it clearly distinct from the bivariate copula discussed in the previous section.

| (9) |

which measures the joint probability that all consecutive variables are below the upper -th quantile of the stationary distribution (, and is a shorthand for ). Clearly, and we set by convention .

Empirically, the -points probabilities are very hard to measure due to the large noise associated with such rare joint occurrences. However, there exist observables that embed many-points properties and are more easily measured, such as the length of sequences (clusters) of thresholded events, and the recurrence times of such events, that we study next.

Recurrence intervals

The probability of observing a recurrence interval between two events is the conditional probability of observing a sequence of “non-events” bordered by two events:

| (10) |

where

| (11) |

designates a sequence of ‘non-events’ starting in and terminated by a ‘positive event’ at . (We focus on positive events, but the recurrence of negative events can be studied with the substitution , and the case of recurrence in amplitudes with the substitution ). After a simple algebraic transformation flipping all ‘’ signs to ‘’, it can be written in the language of copulas as:

| (12) |

The cumulative distribution

| (13) |

is more appropriate for empirical purposes, being less sensitive to noise. These exact expressions make clear — almost straight from the definition — that (i) the distribution of recurrence times depends only on the copula of the underlying process and not on the stationary law, in particular its domain or its tails (this is because we take a relative definition of the threshold as a quantile); (ii) non-linear dependences are highly relevant in the statistics of recurrences, so that linear correlations can in the general case by no means explain alone the properties of ; and (iii) recurrence intervals have a long memory revealed by the -points copula being involved, so that only when the underlying process is Markovian will the recurrences themselves be memoryless.222It may be mentioned that in a non-stationary context, renewal processes are also able to produce independent consecutive recurrences Santhanam and Kantz (2008); Sazuka et al. (2009). Hence, when the copula is known (Eq. (25) in appendix for Gaussian processes), the distribution of recurrence times is characterized by the exact expression in Eq. (12).

The average recurrence time is found straightforwardly by summing the series

| (14) |

and is universal whatever the dependence structure. This result was first stated and proven by Kac in a similar fashion Kac (1947). It is intuitive as, for a given threshold, the whole time series is the succession of a fixed number of recurrences whose lengths necessarily add up to the total size , so that . Note that Eq. (14) assumes an infinite range for the possible lags , which is achieved either by having an infinitely long time series, or more practically when the translational-invariant copula is periodic at the boundaries of the time series, as is typically the case for artificial data which are simulated using numerical Fourier Transform methods. Introducing the copula allows to emphasize the validity of the statement even in the presence of non-linear long-term dependences, as Eq. (14) means that the average recurrence interval is copula-independent.

More generally, the -th moment can be computed as well by summing over :

In particular, the variance of the distribution is

| (15) |

It is not universal, in contrast with the mean, and can be related to the average unconditional waiting time, see below. Notice that in the independent case the variance is not equal to the mean , as would be the case for a continuous-time Poisson process, because of discreteness effects.

It is important to notice that the main ingredient in the distribution of recurrence times (13) is the copula (i.e. the serial dependence structure) rather than the stationary distribution , a finding already noted by Olla (2007), but which the current description highlights. The sensitivity to the extreme statistics of the process is in fact hidden in , but what matters more is the (possibly multi-scale) dependence structure .

Conditional recurrence intervals, clustering

The dynamics of recurrence times is as important as their statistical properties, and in fact impacts the empirical determination of the latter.333Distribution testing for involving Goodness-of-fit tests Ren and Zhou (2010) should be discarded because those are not designed for dependent samples and rejection of the null cannot be relied upon. See Chicheportiche and Bouchaud (2011) for an extension of GoF tests when some dependence is present. It is now clear, both from empirical evidences and analytically from the discussion on Eq. (12), that recurrence intervals have a long memory. In dynamic terms, this means that their occurrences show some clustering. The natural question is then: “Conditionally on an observed recurrence time, what is the probability distribution of the next one?” This probability of observing an interval immediately following an observed recurrence time is

| (16) |

Again, flipping the ‘’ to ’’ allows to decompose it as

where the -points probability

shows up. Of course, this exact expression has no practical use, again because there is no hope of empirically measuring any many-points probabilities of extreme events with a meaningful signal-to-noise ratio. We rather want to stress that non-linear correlations and multi-points dependences are relevant, and that a characterization of clustering based on the autocorrelation of recurrence intervals is an oversimplified view of reality.

Waiting times

The conditional mean residual time to next event, when sitting time steps after a (positive) event, is

| (17) |

One is often more concerned with unconditional waiting times, which is equivalent to asking what the size of a sequence of ‘non-events’ starting now will be, regardless of what happened previously. The distribution of these waiting times is equal to

| (18) |

and its expected value is

| (19) |

consistently to what would be obtained by averaging over all possible elapsed times in Eq. (17). From Eq. (15), we have the following relationship between the variance of the distribution of recurrence intervals, and the mean waiting time:

| (20) |

Sequences lengths

The serial dependence in the process is also revealed by the distribution of sequences sizes. The probability that a sequence of consecutive negative events444We consider the case of “negative” events, i.e. those with because it expresses simply in terms of diagonal copulas. The mirror case with “positive” events has the exact same expression but must be inverted around the median. For a symmetric , this distinction is irrelevant., starting just after a ‘non-event’, will have a size is

| (21) |

and the average length of a random sequence

| (22) |

is universal, just like the mean recurrence time. This property rules out the analysis of Boguná and Masoliver (2004) who claim to be able to distinguish the dependence in processes according to the average sequence size.

Record statistic

We conclude this theoretical section on multi-points non-linear dependences by mentioning that the diagonal -points copula can be alternatively understood as the distribution of the maximum of realizations of in a row, since

is equal to . Thus, studying the statistics of such “local” maxima in short sequences (see e.g. Eichner et al. (2006)) can provide information on the multi-points properties of the underlying process. The CDF of the running maximum, or record, is and the probability that will be a record-breaking time is the joint probability

which is irrespective of the marginal law !

III Financial self-copulas

| Stock Index | Country | From | To | |

|---|---|---|---|---|

| S&P-500 | USA | Jan. 02, 1970 | Dec. 23, 2011 | 10 615 |

| KOSPI-200 | S. Korea | Jan. 03, 1990 | Dec. 26, 2011 | 5 843 |

| CAC-40 | France | Jul. 09, 1987 | Dec. 23, 2011 | 6 182 |

| DAX-30 | Germany | Jan. 02, 1970 | Dec. 23, 2011 | 10 564 |

| SMI-20 | Switzerland | Jan. 07, 1988 | Dec. 23, 2011 | 5 902 |

We illustrate some of the quantities introduced above on series of daily index returns. The properties of the time series used are summarized in Tab. 2.

III.1 Conditional probabilities and 2-points dependences

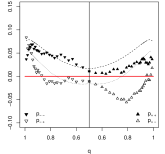

We reproduce the study of Boguná and Masoliver (2004) on the statistic of price changes conditionally on previous return sign, and extend the analysis to any threshold and to remote lags. In addition to the time series of the five stock indices presented in Tab. 2, we look at electroencephalogram (EEG) data from Andrzejak et al. (2001). We first illustrate on Fig. 3 the conditional probabilities (filled symbols) and (empty symbols) with varying threshold , for . To study the departure from the independent case, it is more convenient to subtract the White Noise contribution, to get the corresponding excess probabilities.

First, the EEG data, Fig. 3(f), exhibit a very strong and symmetric persistence; reversion on the other side is shut down for extreme events (like for WN), and is more suppressed than WN for intermediate values. As of the plots relative to financial indices, several features can be immediately observed : positive events (upward triangles) trigger more subsequent positive (filled) than negative (empty) events; negative events (downward triangles) trigger more subsequent negative (filled) than positive (empty) events, except in the far tails where reversion is stronger than persistence after a negative event. Both these effects dominate the WN benchmark, but the latter effect is however much stronger. This overall behavior is similar for the time series of returns of all the stock indices studied. The shapes of and versus are not compatible with the Student copula benchmarks (correlation and d.o.f. ) shown in dashed and dotted lines, respectively. Notice that, due to its non-trivial tail-correlations, see Ref. Chicheportiche and Bouchaud (2012), the Student copula does generate increased persistence with respect to WN, lower reversion in the core and higher reversion in the tails. But empirically the reversion is asymmetric and typically stronger when conditioning on negative events rather than on positive events, a property reminiscent of the leverage effect which cannot be accounted for by a pure (symmetric) Student copula. Some of the indices exhibit more pronounced reversion and persistence effects. Interestingly, the CAC-40 returns have a regime close to a white noise (with, in particular, a value of very close to 0 at , revealing an inefficient conditioning, i.e. as many positive and negative returns immediately following positive or negative returns), but the extreme positive events show a very strong persistence, and the extreme negative events a very strong reversion.

Chicheportiche and Bouchaud (2011) study in detail the - and - dependence of and — which are straightforwardly related to and , respectively — and find that the self-copula of stock returns can be modeled with a high accuracy by a log-normal volatility with log-decaying correlation, in agreement with multifractal volatility models. We give an overview of the results in Fig. 4, for the aggregated copula of all stocks in the S&P500 in 2000–2004. It is possible to show precisely how every kind of dependence present in the underlying process (discussed in Perelló et al. (2004)) reflects itself in for different ’s: short ranged linear anti-correlation accounts for the central part () departing from the WN prediction, long-ranged amplitude clustering is responsible for the “M” and “W” shapes that reveal excess persistence and suppressed reversion, and the leverage effect can be observed in the asymmetric heights of the “M” and “W”.

III.2 Recurrence intervals and many-points dependences

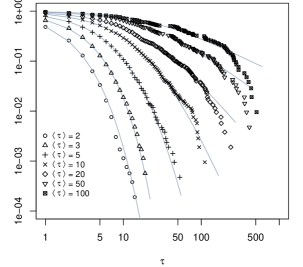

Even the simple, two-points measures of self-dependence studied up to now show that non-linearities and multi-scaling are two ingredients that must be taken into account when attempting to describe financial time series; we now examine their many-points properties. As an example, we compute the distribution of recurrence times of returns above a threshold .

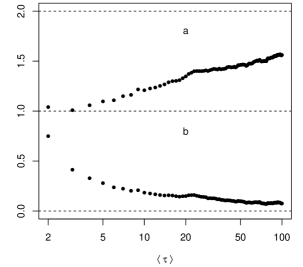

Fig. 5 shows the tail cumulative distribution of the recurrence intervals of DAX returns, at several thresholds — the distribution for other indices is very similar. In the log-log representation used, an exponential distribution (corresponding to independent returns) would be concave and rapidly decreasing, while a power-law would decay linearly. The empirical distributions fit neither of those, and Ludescher et al. (2011) suggested a parametric fit of the form

| (23) |

However, important deviations are present in the tail regions for thresholds at , i.e. : as a consequence, there is no hope that the curves for different threshold collapse onto a single curve after a proper rescaling Chicheportiche and Chakraborti (2013), as is the case e.g. for seismic data. A more fundamental determination of the form of should rely on Eq. (13) and a characterization of the -points copula.

Similarly to the statistic of the recurrence intervals, their dynamics must be studied carefully. We have shown that the conditional distribution of recurrence intervals after a previous recurrence is very complex and involves long-ranged non-linear dependences, so that a simple assessment of recurrence times auto-correlation may not be informative enough for a deep understanding of the mechanisms at stake.

IV Discussion

IV.1 Conditional Expected Shortfall

In addition to caring for frequencies of conditional events, one can try to characterize their magnitudes. This of course does no longer fit in the framework of copulas (that “count” joint events) but can instead be quantified by a multivariate generalization of the Expected Shortfall (or Tail Conditional Expectation). For a single random variable with cdf , the Expected Shortfall is the average loss when conditioning on large events:

In the same spirit, for bivariate distributions, the mean return conditionally on preceding return ‘sign’ is defined:

| (24a) | ||||

| (24b) | ||||

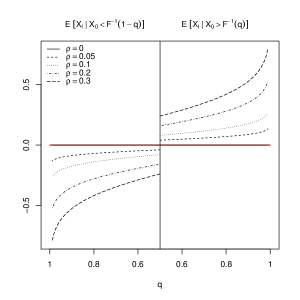

As an example, consider the Gaussian bivariate pair , whose whole -dependence is in the linear correlation coefficient . Fig. 6 shows the conditional Expected Shortfall that can be computed exactly from Eqs. (24), and is proportional to the inverse Mill ratio:

where denotes the CDF of the univariate standard normal distribution.

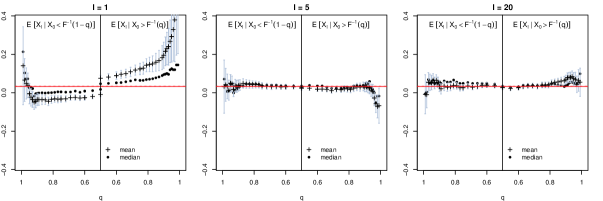

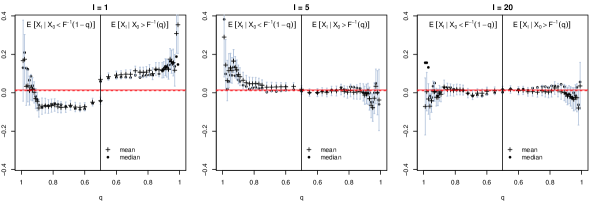

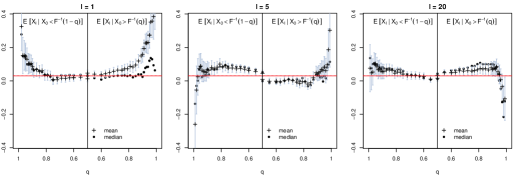

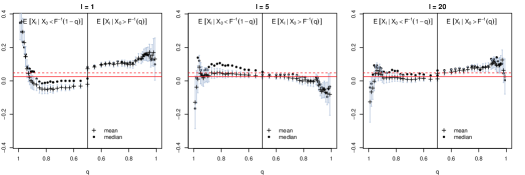

This Gaussian prediction is to be compared with an empirical assessment of the same quantity for series of returns of stock indices. Fig. 7 displays the behavior of versus (we also show the median ) at lags corresponding to one day (), one week () and one month (). The conditional amplitudes measure “how large” a realization will be on average after an event at a given threshold, whereas the conditional probabilities and quantify “how often” repeated such events occur. Mind the unconditional mean and median values, both above zero and distinct from each other. At , the reversion of extreme events is revealed again by the change of monotonicity from on, and more strongly for where has an opposite sign than the preceding return; this corroborates the observation made on conditional probabilities above. Beyond the next day, the general picture is that dependences tend to vanish and the empirical measurements get more concentrated around the WN prediction. However, tail effects are strongly present, with unexpectedly a typical behavior opposite to that of : weekly, monthly reversion of extreme positive jumps. See the caption for a detailed discussion of the specificities of each stock index at every lag .

IV.2 Conclusion

We report several properties of recurrence times and the statistic of other observables (waiting times, cluster sizes, records, aftershocks) in light of their description in terms of the diagonal copula, and hope that these studies can shed light on the -points properties of the process by assessing the statistics of simple variables rather than positing an a priori dependence structure.

The exact universality of the mean recurrence interval imposes a natural scale in the system. A scaling relation in the distribution of such recurrences is only possible in absence of any other characteristic time. When such additional characteristic times are present (typically in the non-linear correlations), no such scaling is expected, in contrast with time series of earthquake magnitudes.

We also stress that recurrences are intrinsically multi-points objects related to the non-linear dependences in the underlying time-series. As such, their autocorrelation is not a reliable measure of their dynamics, for their conditional occurrence probability is much history dependent.

Ultimately, recurrences may be used to characterize risk in a new fashion. Instead of — or in addition to — caring for the amplitude and probability of adverse events at a given horizon, one should be able to characterize the risk in a dynamical point of view. In this sense, an asset could be said to be “more risky” than another asset if its distribution of recurrence of adverse events has such and such “bad” properties that does not share. This amounts to characterizing the disutility by “When?” shocks are expected to happen, in addition to the usual “How often?” and “How large?”.

It would be interesting to study many-points dependences in continuous-time proceses, where the role of the -points copula is played by a counting process. The events to be counted can either be triggered by an underlying continuous process crossing a threshold, or more directly be modeled as a self-exciting point process, like a Hawkes process. A typical financial application could be found in transaction times in a Limit Order Book.

Acknowledgements.

We thank F. Abergel, D. Challet and G. Tilak, for helpful discussions and comments. R. C. acknowledges financial support by Capital Fund Management, Paris.Appendix A Simple copulas and Sklar’s theorem

Sklar’s theorem Sklar (1959) states that any multivariate distribution can be written in terms of univariate marginal distribution functions () and a ‘copula’ function on which, by definition, characterizes the dependence structure between the variables. In practice, constructing the copula is achieved letting for every variable . This is expressed mathematically by Eq. (3) for bivariate distributions, and can be generalized straightforwardly (see Eq. (9) for the diagonal of the -points copula).

As an example, the Gaussian diagonal copula is

| (25) |

where is the univariate inverse CDF, and denotes the multivariate CDF with covariance matrix , which is Tœplitz with symmetric entries

| (26) |

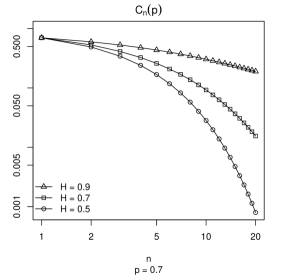

The White Noise (WN) product copula is recovered in the limit of vanishing correlations , and other examples include the exponentially correlated Markovian Gaussian noise, the logarithmically correlated multi-fractal Gaussian noise, and the power-law correlated (thus scale-free) fractional Gaussian noise.

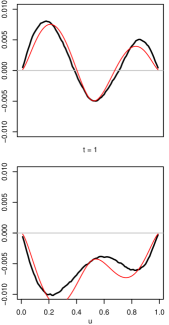

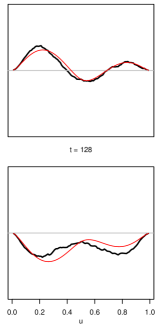

Fig. 8 displays versus for different Hurst indices . The asymptotic behaviour at large cannot be displayed here because of numerical restrictions, but the small properties are more relevant for characterizing short-time conditional dynamics.

References

- Kotz and Nadarajah (2000) S. Kotz and S. Nadarajah, Extreme value distributions (Imperial college press, London, 2000).

- Embrechts et al. (1997) P. Embrechts, C. Klüppelberg, and T. Mikosch, Modelling extremal events: for insurance and finance (Springer Verlag, Berlin, 1997).

- Chakraborti et al. (2011) A. Chakraborti, I. Muni Toke, M. Patriarca, and F. Abergel, Quantitative Finance 11, 991 (2011).

- Politi et al. (2012) M. Politi, N. Millot, and A. Chakraborti, Physica A: Statistical Mechanics and its Applications 391, 147 (2012).

- Bak et al. (2002) P. Bak, K. Christensen, L. Danon, and T. Scanlon, Physical Review Letters 88, 178501 (2002).

- Bunde et al. (2003) A. Bunde, J. F. Eichner, S. Havlin, and J. W. Kantelhardt, Physica A: Statistical Mechanics and its Applications 330, 1 (2003).

- Corral (2004a) A. Corral, Physical Review Letters 92, 8501 (2004a).

- Molchan (2005) G. Molchan, Pure and Applied Geophysics 162, 1135 (2005).

- Altmann and Kantz (2005) E. G. Altmann and H. Kantz, Physical Review E 71, 056106 (2005).

- Saichev and Sornette (2007) A. Saichev and D. Sornette, Journal of Geophysical Research: Solid Earth (1978–2012) 112 (2007).

- Sornette et al. (2008) D. Sornette, S. Utkin, and A. Saichev, Physical Review E 77, 066109 (2008).

- Blender et al. (2008) R. Blender, K. Fraedrich, and F. Sienz, Nonlinear Processes in Geophysics 15, 557 (2008).

- Yamasaki et al. (2005) K. Yamasaki, L. Muchnik, S. Havlin, A. Bunde, and H. E. Stanley, Proceedings of the National Academy of Sciences of the United States of America 102, 9424 (2005).

- Wang et al. (2006) F. Wang, K. Yamasaki, S. Havlin, and H. E. Stanley, Physical Review E 73, 6117 (2006).

- Weber et al. (2007) P. Weber, F. Wang, I. Vodenska-Chitkushev, S. Havlin, and H. E. Stanley, Physical Review E 76, 6109 (2007).

- Sazuka et al. (2009) N. Sazuka, J.-I. Inoue, and E. Scalas, Physica A: Statistical Mechanics and its Applications 388, 2839 (2009).

- Ren and Zhou (2010) F. Ren and W.-X. Zhou, New Journal of Physics 12, 5030 (2010).

- Corral (2003) A. Corral, Physical Review E 68, 035102 (2003).

- Corral (2004b) Á. Corral, Physica A: Statistical Mechanics and its Applications 340, 590 (2004b).

- Embrechts et al. (2003) P. Embrechts, F. Lindskog, and A. McNeil, Handbook of heavy tailed distributions in finance 8, 329 (2003).

- Embrechts et al. (2002) P. Embrechts, A. J. McNeil, and D. Straumann, “Correlation and dependence in risk management: properties and pitfalls,” in Risk management: value at risk and beyond (Cambridge University Press, Cambridge, 2002) pp. 176–223.

- Malevergne and Sornette (2006) Y. Malevergne and D. Sornette, Extreme Financial Risks: From Dependence to Risk Management (Springer Verlag, Berlin Heidelberg New York, 2006).

- Mikosch (2006) T. Mikosch, Extremes 9, 3 (2006).

- Chicheportiche and Bouchaud (2012) R. Chicheportiche and J.-P. Bouchaud, International Journal of Theoretical and Applied Finance 15 (2012).

- Beare (2010) B. K. Beare, Econometrica 78, 395 (2010).

- Ibragimov and Lentzas (2008) R. Ibragimov and G. Lentzas, “Copulas and long memory,” (2008), harvard Institute of Economic Research discussion paper.

- Patton (2009) A. J. Patton, Handbook of financial time series , 767 (2009).

- Boguná and Masoliver (2004) M. Boguná and J. Masoliver, The European Physical Journal B - Condensed Matter and Complex Systems 40, 347 (2004).

- Chicheportiche (2013) R. Chicheportiche, Non linear Dependences in Finance, Ph.D. thesis, École Centrale Paris (2013).

- Omori (1895) F. Omori, Journal of the College of Science 7, 111 (1895).

- Petersen et al. (2010) A. M. Petersen, F. Wang, S. Havlin, and H. E. Stanley, Physical Review E 82, 6114 (2010).

- Lillo and Mantegna (2003) F. Lillo and R. N. Mantegna, Physical Review E 68, 016119 (2003).

- Gutenberg and Richter (1936) B. Gutenberg and C. F. Richter, Science 83, 183 (1936).

- Note (1) We use a calligraphic in order to make it clearly distinct from the bivariate copula discussed in the previous section.

- Note (2) It may be mentioned that in a non-stationary context, renewal processes are also able to produce independent consecutive recurrences Santhanam and Kantz (2008); Sazuka et al. (2009).

- Kac (1947) M. Kac, Bulletin of the American Mathematical Society 53, 1002 (1947).

- Olla (2007) P. Olla, Physical Review E 76, 011122 (2007).

- Note (3) Distribution testing for involving Goodness-of-fit tests Ren and Zhou (2010) should be discarded because those are not designed for dependent samples and rejection of the null cannot be relied upon. See Chicheportiche and Bouchaud (2011) for an extension of GoF tests when some dependence is present.

- Note (4) We consider the case of “negative” events, i.e. those with because it expresses simply in terms of diagonal copulas. The mirror case with “positive” events has the exact same expression but must be inverted around the median. For a symmetric , this distinction is irrelevant.

- Eichner et al. (2006) J. F. Eichner, J. W. Kantelhardt, A. Bunde, and S. Havlin, Physical Review E 73, 016130 (2006).

- Andrzejak et al. (2001) R. G. Andrzejak, K. Lehnertz, F. Mormann, C. Rieke, P. David, and C. E. Elger, Physical Review E 64, 061907 (2001).

- Chicheportiche and Bouchaud (2011) R. Chicheportiche and J.-P. Bouchaud, Journal of Statistical Mechanics: Theory and Experiment 2011, P09003 (2011).

- Perelló et al. (2004) J. Perelló, J. Masoliver, and J.-P. Bouchaud, Applied Mathematical Finance 11, 27 (2004).

- Ludescher et al. (2011) J. Ludescher, C. Tsallis, and A. Bunde, EPL (Europhysics Letters) 95, 68002 (2011).

- Chicheportiche and Chakraborti (2013) R. Chicheportiche and A. Chakraborti, arXiv preprint physics.data-an/1302.3704 (2013).

- Sklar (1959) A. Sklar, Publ. Inst. Statist. Univ. Paris 8, 229 (1959).

- Santhanam and Kantz (2008) M. S. Santhanam and H. Kantz, Physical Review E 78, 1113 (2008).