Robust estimation of risks from small samples

Abstract

Data-driven risk analysis involves the inference of probability distributions from measured or simulated data. In the case of a highly reliable system, such as the electricity grid, the amount of relevant data is often exceedingly limited, but the impact of estimation errors may be very large. This paper presents a robust nonparametric Bayesian method to infer possible underlying distributions. The method obtains rigorous error bounds even for small samples taken from ill-behaved distributions. The approach taken has a natural interpretation in terms of the intervals between ordered observations, where allocation of probability mass across intervals is well-specified, but the location of that mass within each interval is unconstrained. This formulation gives rise to a straightforward computational resampling method: Bayesian Interval Sampling. In a comparison with common alternative approaches, it is shown to satisfy strict error bounds even for ill-behaved distributions.

I Motivation: risk analysis for grids

Managing a critical infrastructure such as the electricity grid requires constant vigilance on the part of its operator. The system operator identifies threats, determines the risks associated with these threats and, where necessary, takes action to mitigate them. In the case of the electricity grid, these threats include sudden outages of lines and generators, misprediction of renewable generating capacity, and long-term investment shortages.

Quantitative risk assessments often amounts to data analysis. In cases where directly relevant data is available (e.g. historical wind variability), it can be used directly to estimate future performance (hindcasting). In other cases, risk analysis is based on models, for example in distribution network outage planning. Even so, for sufficiently complex models, risks are rarely computed directly. Instead, Monte Carlo simulations are used to generate ‘virtual’ observations, which are analysed statistically.

A particular challenge is the management of high-impact low-probability events. By definition, such events are exceedingly rare, but misjudging their likelihood of occurrence can have significant consequences. Cascading outages that can lead to partial or full system blackouts are a prime example of such events. In recent years, their modelling and analysis has become a very active area of research. Models are typically evaluated using Monte Carlo simulations AlizadehMousavi2012 ; Henneaux2012 , although other innovative approaches are also being developed Rezaei2015 .

The statistical validity of simulation outcomes is often not addressed, and when it is, this is typically by means of the standard error with the implicit invocation of the central limit theorem (e.g. AlizadehMousavi2012 ). One recent exception is Dobson2013 , which explicitly asked how many blackout occurrences were required to estimate event probability with sufficient accuracy. However, this analysis was limited to a single binary outcome (i.e. a Bernoulli random variable).

This paper contributes to closing this methodological gap, by introducing a method for the robust analysis of rare event data, which is applicable to generic real-valued observations. A simple example in Section VIII illustrates how the method can be applied to cascading outage simulations. Critically, the method satisfies strict accuracy requirements, which will become increasingly important as operators move away from deterministic security standards (e.g. ‘’) to probabilistic standards that are enforced using Monte Carlo-based tools.

II Introduction

We consider the problem of inferring properties of a random variable from independent observations . For example, one may attempt to estimate its expectation or distribution . This problem can be found in idealised form in the analysis of Monte Carlo simulations, where independence of observations is often guaranteed.

A range of approaches exist for addressing this elementary inference problem, differing in their underlying assumptions and applicability Robert1999 . On one end of the scale there are simple point estimates, such as the sample mean or - when a distribution is concerned - the empirical distribution. When more accuracy is required it is common practice to report a confidence interval, usually by means of an implicit invocation of the central limit theorem. However, this approach is not suitable when sample sizes are small or the distribution of is sufficiently heavy-tailed or skewed. In such cases the bootstrap method Efron1979 is a well-established alternative, but it is limited to resampling of observed values, so there is no way to account for features of the distribution that have not been sampled. This shortcoming is shared by its Bayesian variant, the Bayesian bootstrap Rubin1981 . It is particularly restrictive when sample sizes are very small, or for the analysis of rare events where a small fraction of the probability mass has a disproportionate effect on the parameter of interest.

Ferguson’s Dirichlet process Ferguson1973 may be used for inference beyond strictly observed values, but this requires the selection of a prior measure. Furthermore, the resulting inferred (random) distributions are ultimately discrete. A different approach is taken by the Nonparametric Predictive Inference (NPI) method Coolen2006 , which makes use of imprecise probabilities to circumvent these issues. However, its definition as an incremental predictive process makes it less suitable for the inference of the underlying time-invariant distribution or for efficient computational implementations.

In this paper we introduce a robust method for inference from independent real-valued observations with minimal assumptions. The method relies only on the observations and the specification of a bounding interval for the random variable (which may be taken as the entire real line ). It results in conservative posterior distributions for any quantities under consideration, but credible intervals for such quantities remain valid even for ill-behaved distributions. This is a desirable feature for applications where accuracy is paramount, such as risk assessment of critical systems. Specific contributions of this paper are as follows:

-

•

The Dirichlet process is reformulated in a way that separates its expectation and random fluctuations (Section IV)

-

•

A non-parametric robust posterior distribution is defined, making use of imprecise probabilities in the form of probability boxes (Section V).

- •

-

•

Examples illustrate the robust nature of the proposed method, including an application to blackout risk estimation (Section VIII).

III Preliminaries

Notation

The summary notation is used to indicate a sequence of values with consecutive indices . Capital symbols refer to random variables or non-decreasing functions on the real line (e.g. cumulative distribution functions); it will be clear which is intended from the context. Caligraphic letters (e.g. ) indicate random non-decreasing functions, i.e. realisations of distributions-of-distributions.

III.1 Dirichlet distribution

Let us consider the problem of determining an unknown discrete (categorical) probability distribution on a set of disjoint events , i.e. . To estimate from independent realisations of the corresponding random variable we may use Bayesian inference with the Dirichlet distribution as a prior distribution. The Dirichlet distribution is parametrised by and its probability density is structured as

| (1) |

with the constraint . Note that the density is formally only defined as a function of , and the final component is computed as . Nevertheless we include in Eq. (1) to highlight the symmetry of the expression. Permissible values of are restricted to the unit -simplex that is defined as

| (2) |

The values represent the probabilities associated with the events . The Dirichlet distribution thus represents a continuous distribution on the space of -dimensional discrete probability distributions. Let us define the random variables as

| (3) |

The expectation of the event probabilities is given by

| (4) |

Because the Dirichlet distribution is a conjugate prior, the Bayesian posterior distribution is also a Dirichlet distribution. Specifically, let us consider a set of observation counts for each event, with and a prior distribution . The posterior distribution is then given by with . This illustrates that the parameters may be considered ‘pseudo-observations’ on the same footing as the actual observations . As a result, the posterior expectation of conditional on the observations is

| (5) |

The probability associated with the union of two disjoint events and is given by the sum of their probabilities and . In the case of a Dirichlet distribution, these probabilities are random variables and . The Dirichlet distribution has the property that the resulting -dimensional distribution is obtained simply by summing the relevant parameters and .

| (6) |

Repeated application of this process until only the events and its complement are left (e.g. ‘heads’ and ‘tails’) yields

| (7) |

Because by definition, we may simply consider the marginal distribution of the random variable , which is the beta distribution with parameters and

| (8) |

III.2 Dirichlet process

Ferguson’s Dirichlet process Ferguson1973 provides a natural extension of the discrete Dirichlet distribution to an infinite set of events, and the continuous domain in particular. The Dirichlet process on is a distribution of probability distributions (i.e. a random probability measure) that is parametrised by the measure . It is defined by the condition

| (9) |

where is a random probability measure and is any arbitrary disjoint covering of . It deserves mention that even when the measure has a continuous density on , samples from the corresponding Dirichlet process distribution will have discrete features Ferguson1973 (see also Figure 1).

Like the Dirichlet distribution for discrete distributions, the Dirichlet process on the real line is a conjugate prior for Bayesian inference Ferguson1973 . Using as a prior, and independent observations , it follows from (9) that

| (10) |

Here, are measures corresponding to a unit mass located at , within the support set of .

III.3 Probability box representation of imprecise probabilities

In probability theory as defined using Kolmogorov’s axioms, each event has a specific probability . When our state of knowledge does not permit us to make such precise statements one can resort to imprecise probabilities Walley1991 : instead of the value we assign an interval probability consisting of a pair of lower and upper probability bounds and .

A particular representation of imprecise probabilities on is the probability boxFerson2003 (also summarised as p-box), defined by a lower probability distribution and an upper probability distribution . We write

| (11) |

as a shorthand for the set of distribution functions enclosed by and :

| (12) |

Probability boxes define a set of permissible distribution functions, but do not assign any preference of probabilities to set members. A probability box associates a probability interval with the event . The upper and lower bounds of this interval are given by:

| (13a) | ||||

| (13b) | ||||

Probability boxes may also be interpreted in terms of possibility theory Flage2012 or belief functions in Dempster-Shafer theory Ferson2003 . Defined only by a pair of upper and lower distributions, the probability box is restricted to representing uncertainty in terms of simple intervals. Whereas every probability box can be expressed as a belief function, the converse is not true Ferson2003 . For example, it cannot be used to represent the knowledge that a random variable has a known ‘dead band’ between and . As such it is not the most general representation of imprecise probabilities, but it is sufficient for the purpose of our analysis.

IV Inference using the Unit Dirichlet Process

In this section we reformulate the Dirichlet process to disentangle its expected distribution and the random fluctuations around that distribution, and we use this formulation to restate the Bayesian posterior distribution for the Dirichlet process.

Definition (Cumulative Dirichlet Process).

For a given Dirichlet process on the real line, the corresponding Cumulative Dirichlet Process (CDP) is parametrised by the cumulative function

| (14) |

is defined such that satisfies the cumulative identity

| (15) |

where denotes equality in distribution.

Lemma IV.1.

Let , with . We express in terms of a scalar concentration parameter and a cumulative probability distribution . Then the following properties hold:

| (16) | ||||

| (17) |

Proof.

, which, following (8), is distributed according to a beta distribution . Therefore, so that . In addition, it follows from the properties of the beta distribution that , so that . ∎

Definition (Unit Dirichlet Process).

Let the Unit Dirichlet Process be the CDP that is generated by the concentration parameter and the identity function on the unit interval :

| (18) |

The unit Dirichlet process may be interpreted as a random non-decreasing map from the interval to . From (16) and (17) it follows that and . Figure 1 shows several realisations of the random distribution . The case clearly demonstrates the discrete nature of the Dirichlet process, whereas illustrates the approximation of the identity map for . Finally, The Unit Dirichlet Process has a tidy expression in terms of the ‘stick breaking process’ definition of the Dirichlet process Sethuraman1994 :

| (19) |

Here is the unit step function at , and the sequences of independent random variables and are defined as and .

Theorem IV.1.

Every Cumulative Dirichlet Process can be expressed as

| (20) |

where is a Unit Dirichlet Process and the symbol indicates composition of functions.

Proof.

Consider the cumulative Dirichlet process and an arbitrary partitioning of the real line into half-open intervals . This partioning is defined by the ordered set of points , with , and . Together, the set and generate the non-decreasing sequence of random variables

| (21) |

The difference between two adjacent variables is the random probability associated with interval . It follows from (9) that

| (22) |

Defining , this can be written as

| (23) |

Therefore, inverting the steps above,

| (24) |

and a comparison with (21) gives

| (25) |

This holds for any partioning , so the equality can be extended to the entire domain. ∎

Theorem IV.1 neatly splits the cumulative Dirichlet process into the expected shape () of the distribution and its inherent randomness (). It shows that can be understood as a random distortion of the generating distribution with fluctuations that decrease in amplitude as increases. The same procedure can be applied to the Bayesian posterior of the Dirichlet process.

Corollary IV.1.

The implication of the decomposition (27) is that the (cumulative) posterior distribution may be considered a random deformation () of a weighted combination of the prior () and empirical () distributions.

V Robust inference of distributions

The tools developed in the previous section can be applied to the central challenge in this paper: inferring the distribution from a set of independent observations of . The prior assumption is that is restricted to an interval . This lack of knowledge is represented by the vacuous p-box

| (28) |

Recall that is the unit step function at and that and may take the values and , respectively.

Definition (P-box transformation).

Let be the space of all distribution functions on the interval , and the space of probability boxes on . Let be the set of all non-decreasing unit maps with and . For every we define (with a slight abuse of notation) an identically named map so that

| (29) |

for any probability box , with . The map is order-preserving, so the transformed upper and lower bound distributions are sufficient to define the transformed p-box. In the following, the appropriate domain of the map ( or ) will be clear from the context.

The Unit Dirichlet Process is a random element of . It therefore defines a p-box randomisation in an analogous manner:

| (30) |

Note that the UDP acts identically on the lower and upper bounds (each realisation transforms both identically).

V.1 Robust posterior distributions

Theorem V.1.

Define the -robust posterior distribution as

| (31) | ||||

| (32) |

Then:

-

1.

is a posterior distribution corresponding to the vacuous prior (28) with concentration parameter and observations .

-

2.

is a consistent estimator that converges to as .

Proof.

Remark.

In the limit the upper and lower distributions coalesce into the single random distribution

| (33) |

This is the Bayesian Bootstrap method introduced by Rubin Rubin1981 as a Bayesian analog of the bootstrap method. It has assigns a (random) probability mass only to observed values , so it has no ability to extrapolate beyond the lowest and highest observed values, and the posterior is always discrete.

Remark.

Conceptually, the -robust posterior distribution is closely related to the posterior distribution obtained using a Robust Bayes approach. However, it differs in the way it embeds continuous functions in the posterior. Using a prior set and concentration parameter , the Robust Bayes posterior can be written as , with . Although its range is identical to that of the -robust posterior distribution, the discrete nature of the Dirichlet process means that members of the posterior distribution are smooth with zero probability. In contrast, the -robust posterior distribution is a random p-box. Although its bounds have discrete features, continuous functions that fit within the p-box are equally part of the posterior distribution.

The parameter determines the relative weight of the prior and observations. It can therefore be considered the inverse of an effective ‘learning rate’: small values result in faster convergence, but picking a value that is too small leads to an underappreciation of parts of the distribution that have not been observed, as represented by the vacuous prior.

Theorem V.2.

Let be an -robust posterior distribution. The posterior is compatible with continuous distributions only if .

Proof.

If the original distribution is (locally) continuous, the observations are almost surely distinct. Take the -th smallest observation and consider the posterior distributions at . To avoid necessary discontinuities in the posterior distribution, the upper bound distribution at must equal or exceed the lower bound distribution at :

| (34) |

Because the LHS and RHS distributions are linked through the order-preserving random map , the inequality should be interpreted as first order stochastic dominance Hadar1969 (ordering of quantiles). Making use of (8), (34) can be expressed in terms of beta distributions

| (35a) | ||||

| (35b) | ||||

It follows from the properties of the beta distribution that (35a) can only hold if . ∎

Definition.

The robust posterior distribution is defined as the -robust posterior distribution with .

| (36) | ||||

| (37) |

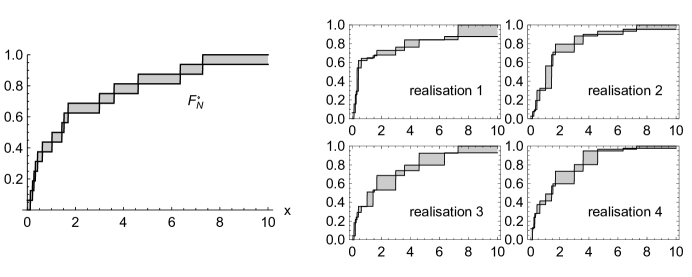

The ‘input’ p-box can be considered the spanning distribution of empirical distributions generated by the observations and one unknown observation in the interval . Figure 2 (left) depicts for the observations in Table 1. The right panel shows four random realisations of . The realisations visually resemble a ‘chain of blocks’ with the lower and upper bounds touching at each observation . These upper and lower bound pairs force compatible distributions to traverse particular values at but leave them otherwise unconstrained, in line with theorem V.2. The choice also ensures that an expected posterior probability of is assigned to each of the tail intervals and . Further properties of , including comparisons with other methods, are discussed in the Supplementary Materials, Section S3.

| 1.435 | 0.276 | 3.603 | 0.211 | 2.996 |

| 7.289 | 0.426 | 0.124 | 1.523 | 4.603 |

| 1.696 | 0.620 | 0.338 | 6.351 | 1.026 |

V.2 Interval-associated posterior probabilities

The upper and lower bounds of the p-box only take on distinct values. As a result, the (random) upper and lower values of the random probability box are given by , with and . This partitioning allows for the projection of (18) onto an -dimensional Dirichlet distribution. Making use of (9), we can specify directly as a random p-box:

| (38) |

with and is the ordered data set , augmented by and .

The fact that the robust posterior distribution can be expressed in this simple manner has significant implications. Eq. (38) provides an intuitive understanding of the method that has been developed. The interval is partitioned into closed intervals with boundaries at the observed points . Each of these intervals is assigned a random weight , drawn from a Dirichlet distribution. Note that this Dirichlet distribution with unit parameters is in fact the uniform distribution on the unit simplex , as can be seen from Eqs. (1) and (2).

Although a specific probability distribution governs the probability mass assigned to each interval, the method provides no guidance regarding the way this mass is distributed within each interval. This dichotomy can be interpreted as follows. The limited number of observations can only provide meaningful information about the large scale features (probability associated with intervals) of the probability distribution . Without additional observations or assumptions no substantiated statements can be made about the features of on a smaller scale.

VI Estimating population parameters

In practical applications the object of interest is often not the distribution , but a particular real-valued function of that distribution, such as the expectation, median or various measures of tail risk. In the context of this paper, we restrict ourselves to the case where is monotonic.

Definition.

A function is monotonic if the following is true for any two random variables and :

| (39) |

Where the partial ordering ’’ denotes first order stochastic dominance Hadar1969 , which is equivalent to the statement , with a strict inequality holding for at least one point.

The strong condition of monotonicity holds for many basic population parameters, including the mean, quantiles (value-at-risk), and truncated means (conditional value-at-risk). More generally, it holds for the class of coherent risk measures Artzner1999 , although a customary minus sign is usually incorporated into the definition of monotonicity.

Consider the set of permitted -values for a given p-box , which we summarise by its minimum and maximum values. Due to the monotonicity of , we have . For the random p-box defined by , this induces the random -interval

| (40) |

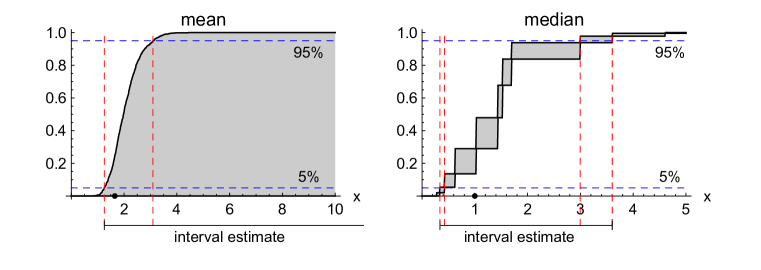

The distributions of the bounding random variables and can be interpreted as the definition of a probability box for the population parameter (see also Figure 3):

| (41) |

Reporting intervals

In applications, it is usually preferable to summarise the estimate of a population parameter in the form , for a given credibility level (e.g. 95%):

| (42) |

In keeping with our robust approach, this is achieved by taking the span of the -credible values for the upper and lower bound processes, resulting in

| (43) |

The construction of the interval estimate is illustrated in Figure 3. Under the stated assumptions (independence of observations and the range of being confined to ) the credibility is a lower bound for the probability that the real value is contained in the interval estimate. To emphasise both the accuracy and the inherent conservativeness of the interval estimate, this can be expressed as a ” credible interval” (e.g. 95%+ credible interval).

VII Bayesian Interval Sampling

The posterior distribution as expressed in (38) associates random probabilities with the intervals , for . This formulation suggests a computationally straightforward resampling method that can be used to probe the upper and lower bounds of , and therefore (through (40)) the distributions of and . The algorithm, Bayesian Interval Sampling (BIS), is described below.

-

1.

For to

-

(a)

Sample an -dimensional weight vector from

-

(b)

Compute

-

(c)

Compute

-

(a)

-

2.

Compute as the empirical CDF of

-

3.

Compute as the empirical CDF of

-

4.

Compute the -credible interval estimate using (43)

As a rule of thumb we use to ensure that we have 100 observations in the tails of the empirical distributions for and . This ensures reasonable statistical stability for the computation of the interval . A modified algorithm for data sets with many identical observations is given in the Supplementary Materials, Section S1.

Remark.

Bayesian Interval Sampling also has a natural interpretation in terms of the Bayesian bootstrap method Rubin1981 , a Bayesian variation of the (frequentist) bootstrap method Efron1979 . The connection between the algorithm above and the Bayesian bootstrap method is readily apparent through comparison with (33) and (41). The upper bound distribution for is the Bayesian bootstrap posterior distribution for the dataset augmented with a ‘pseudo-observation’ of the lower domain boundary . Similarly, is the Bayesian bootstrap posterior distribution for augmented with the upper domain boundary . In Bayesian Interval Sampling, both bounds are sampled simultaneously, guaranteeing sample-wise coherence ().

VIII Examples

Bayesian Interval Sampling was used to analyse the data in Table 1, using the bounds . The population parameters considered were the median and the mean, resulting in the probability boxes in Figure 3. The probability box for the median (right) is well-behaved and results in a finite interval estimate. In contrast, the equivalent analysis for the mean (left) does not result in a finite interval estimate. This is caused by the lower bound distribution for the mean, which has a constant value of . This perhaps surprising result is a consistent outcome of our robust approach. No assumption was made on the long tail behaviour of , other than a data-driven bound on the probability . Therefore one cannot rule out the existence of a small probability mass at , which makes an arbitrarily large contribution to the mean. This result also reflects the common understanding that the mean is not a robust statistic, whereas the median is. Further examples for the Value at Risk (VaR) and truncated mean are included in the Supplementary Materials, Section S2.

To illustrate the robustness of the Bayesian Interval Sampling method, its performance was analysed for the estimation of the mean in two variants of the (0,1)-log-normal distribution. The first variant truncated the distribution to the interval [0,50]. In realistic cases, such a truncation could reflect the maximum size of imposed by a finite system size, for example the highest possible cost of a system malfunction. The second variant took the truncated distribution and additionally included a 1% probability to observe the maximum value (equal to the upper bound of the truncated distribution). The inference performance on these distributions was assessed using 10,000 repeated experiments. For each experiment, 50 random observations were generated and used to compute an interval estimate for the mean. This interval was compared with the true mean of the distribution ( and , respectively), and a tally was kept to determine the overall accuracy of the method (i.e. proportion of correct predictions). Note that this is essentially a frequentist test, so both (frequentist) confidence and (Bayesian) credible intervals should satisfy (42). The accuracy of BIS was compared with the common Student and bootstrap approaches

| distribution | method | accuracy | median | median |

|---|---|---|---|---|

| (target: 95%) | ||||

|

Truncated log-normal

(mean: ) |

Student t | 1.08 | 2.12 | |

| Bootstrap | 1.15 | 2.14 | ||

| BIS | 1.17 | 5.10 | ||

|

Truncated log-normal

with extreme events (mean: ) |

Student t | 0.98 | 2.60 | |

| Bootstrap | 1.20 | 2.64 | ||

| BIS | 1.26 | 5.42 |

The results are shown in Table 2. Both the Student t and bootstrap methods have success rates well below 95%, so neither method satisfies the objective stated in (42). This is a direct consequence of the long tail of the distribution, the impact of which is significantly exacerbated in the extreme event distribution. In contrast, the Bayesian interval sampling method has much lower misprediction rates of only 1.3% and 1.2%, well below the 5% bound imposed by the 95% credibility requirement. The rightmost columns of Table 2 show the median values of the lower and upper interval bounds (across 10,000 experiments). They illustrate that the improved accuracy of BIS is a direct consequence of more conservative interval estimates.

Estimation of blackout risks

Finally, BIS was applied to the motivating example of estimating blackout risks in power systems. A simple minimal electrical network model was constructed as follows: a random -node topology was generated using a modified Barabási-Albert model with non-preferential random attachment of two edges (transmission lines) for each new node, resulting in 1998 lines. Customer loads were uniformly allocated to nodes (with a value ‘1’ in rescaled units), and an equal amount of generating capacity was distributed across the nodes using a Dirichlet distribution . The power flows across the transmission lines were computed using the DC power flow approximation, assuming identical reactances for all lines. Line capacities were initialised according to the common ‘N-1’ security criterion, enforcing that single line failures do not lead to overloads. An additional 10% margin was added to generator capacities and transmission lines.

For this random network, we investigated the risk (expected impact) of line outages that occur independently with a probability (in a given period of interest). The simultaneous occurrence of line outages can result in overloads in other lines: overloaded lines are tripped one by one until no more overloads are present. Simultaneously overloaded lines are tripped one by one in random order. If the network breaks up into multiple components, supply and demand are balanced in each island individually. If insufficient local generating capacity is available, load is shed uniformly across the nodes in the island. The total fraction of load shed is used as an indicator for the severity of the cascading event.

| mean fraction of load lost | risk contribution | ||

| (99%+ interval estimate) | ( loss of load) | ||

| 0, 1 | 0.98 | 0 (by design) | 0 |

| 2 | [, ] | [, ] | |

| 3 | [, ] | [, ] | |

| 4 | [, ] | [, ] | |

| 5 | [, ] | [, ] | |

| ¿5 | [0,1] (no assumptions) | [0, ] | |

| Total | 1 | [,] |

The analysis was structured by conditioning on the number of simultaneous outages . By design, and have no impact, and is treated as a potential full blackout (load loss can take any value in ), without further analysis. For intermediate , the mean loss of load was estimated using 10,000 simulated -line outages. 99% credible intervals were computed using BIS. In this case, the The intermediate results and the computation of the overall 99%+ risk estimate ( ) are shown in Table 3.

IX Discussion

We have described a robust nonparametric Bayesian method to estimate properties of a distribution function from a set of independent observations . It assumes only the existence of a bounding interval , which may be taken equal to the real line.

The resulting posterior distribution (38) is expressed as a random probability box. It has the intriguing feature that posterior probabilities are associated with the intervals between observations, but the allocation of probability mass within each interval is left undetermined. Therefore, one can consider as a probabilistic estimate of only the low-frequency (coarse grained) content of . As expected, the resolution of this low-frequency estimate improves with the sample size .

In applications, one often aims to infer real-valued properties of (e.g. mean, median, any coherent risk measure). We have shown how the posterior distribution induces a probability box for the estimation of . In turn, this probability box can be used to define a robust credible interval for . Due to the robust construction, this interval may be interpreted as the range of values for that is not ruled out by the observations. The Bayesian Interval Sampling (BIS) method described in Section VII provides a straightforward resampling algorithm to perform this estimation.

The imprecise nonparametric Bayesian method (and the BIS implementation) is uniquely suitable for applications that require strict accuracy bounds, where (i) the set of (relevant) data points is small (roughly 100 or less) or (ii) unobserved events can have a disproportionate effect on the quantity that is being estimated.

When only a small number of data points is available, the set of observations may be significantly skewed compared to the generating distribution . The nonparametric Bayesian approach results in an inferred distribution for that correctly accounts for such small sample variations. It should be noted that this same argument also applies when the total number of samples is large, but the number of relevant samples is small. For example, this occurs when one characterises rare failures in reliable systems.

Furthermore, the interval probability approach provides a robust framework to deal with unobserved events. Such events may be so-called high-impact low-probability events, which have a disproportionate impact on the population parameter . In applications where it is necessary to analyse largely unobserved tails of a distribution it is generally advisable to use Extreme Value Theory (EVT) (see e.g. Coles Coles2001 ). However, the application of EVT assumes that the long-tail behaviour of the process is sufficiently well-described by the data set. This may not be the case if the data set is very small, or when the underlying process is prone to exhibit very rare events that are qualitatively different from other large events. Events of the latter type are sometimes referred to as ‘Dragon kings’ Sornette2012 .

The method described in this paper is conservative by design, and the resulting uncertainty bands may be dishearteningly large (see e.g. Figure 3). Conventional methods will usually provide estimates with tighter bounds, and their use may well be justified if the underlying distribution is well-behaved. However, the robust posterior distribution (and BIS implementation) can still be used for comparison purposes. Significant differences in results will highlight the impact of explicit and implicit assumptions made in the analysis, pointing out the need to confirm their validity in a particular application.

Acknowledgments

The authors thank Martin Clark, Richard Vinter, Matthias Troffaes, Frank Coolen, Alastair Young and Chris Dent for thought-provoking discussions and helpful comments at various stages during the development of this research. The research leading to these results has received funding from the European Union Seventh Framework Programme (FP7/2007-2013) under grant agreement n∘ 274387.

References

- (1) Alizadeh Mousavi O, Cherkaoui R, Bozorg M. 2012 Blackouts risk evaluation by Monte Carlo Simulation regarding cascading outages and system frequency deviation. Electric Power Systems Research 89, 157–164.

- (2) Henneaux P, Labeau PE, Maun JC. 2012 A level-1 probabilistic risk assessment to blackout hazard in transmission power systems. Reliability Engineering and System Safety 102, 41–52.

- (3) Rezaei P, Hines PDH, Eppstein MJ. 2015 Estimating Cascading Failure Risk With Random Chemistry. IEEE Transactions on Power Systems 30, 2726–2735.

- (4) Dobson I, Carreras BA, Newman DE. 2013 How Many Occurrences of Rare Blackout Events Are Needed to Estimate Event Probability? IEEE Transactions on Power Systems 28, 3509–3510.

- (5) Robert CP, Casella G. 1999 Monte Carlo Statistical Methods. Springer-Verlag GmbH.

- (6) Efron B. 1979 Bootstrap Methods: Another Look at the Jackknife. The Annals of Statistics 7, 1–26.

- (7) Rubin DB. 1981 The Bayesian Bootstrap. The Annals of Statistics 9, 130–134.

- (8) Ferguson TS. 1973 A Bayesian Analysis of Some Nonparametric Problems. The Annals of Statistics 1, 209–230.

- (9) Coolen FPA. 2006 On Nonparametric Predictive Inference and Objective Bayesianism. Journal of Logic, Language and Information 15, 21–47.

- (10) Walley P. 1991 Statistical Reasoning with Imprecise Probabilities. Chapman and Hall/CRC.

- (11) Ferson S, Kreinovich V, Ginzburg L, Myers DS, Sentz K. 2003 Constructing Probability Boxes and Dempster-Shafer Structures. Technical Report January, Sandia National Laboratories.

- (12) Flage R, Aven T, Baraldi P, Zio E. 2012 An imprecision importance measure for uncertainty representations interpreted as lower and upper probabilities, with special emphasis on possibility theory. Proceedings of the Institution of Mechanical Engineers, Part O: Journal of Risk and Reliability 226, 656–665.

- (13) Sethuraman J. 1994 A Constructive Definition of Dirichlet Priors. Statistica Sinica 4, 639–650.

- (14) Hadar J, Russell WR. 1969 Rules for Ordering Uncertain Prospects. The American Economic Review 59, 25–34.

- (15) Artzner P, Delbaen F, Eber JM, Heath D. 1999 Coherent Measures of Risk. Mathematical Finance 9, 203–228.

- (16) Coles S. 2001 An Introduction to Statistical Modeling of Extreme Values. Springer.

- (17) Sornette D, Ouillon G. 2012 Dragon-kings: Mechanisms, statistical methods and empirical evidence. The European Physical Journal Special Topics 205, 1–26.