Parameter Estimation in Hidden Markov Models with Intractable Likelihoods Using Sequential Monte Carlo

Abstract

We propose sequential Monte Carlo based algorithms for maximum likelihood estimation of the static parameters in hidden Markov models with an intractable likelihood using ideas from approximate Bayesian computation. The static parameter estimation algorithms are gradient based and cover both offline and online estimation. We demonstrate their performance by estimating the parameters of three intractable models, namely the -stable distribution, g-and-k distribution, and the stochastic volatility model with -stable returns, using both real and synthetic data.

Key words: hidden Markov models, maximum likelihood estimation, approximate Bayesian computation, intractable likelihood, sequential Monte Carlo.

1 Introduction

The hidden Markov model (HMM) is an important statistical model used in many fields including bioinformatics (e.g. Durbin et al., (1998)), econometrics (e.g. Kim et al., (1998)) and population genetics (e.g. Felsenstein and Churchill, (1996)); see Cappé et al., (2005) for a recent overview. A HMM is comprised of a latent process and an observed process . The latent process is a Markov chain with an initial density and the transition density , i.e.

| (1) |

It is assumed that and are densities on with respect to a dominating measure denoted generically as . The observation at time is conditionally independent of all other random variables given and its conditional observation density is on with respect to the dominating measure , i.e.

| (2) |

The law of the HMM is parametrised by a vector taking values in some compact subset of the Euclidean space .

In this paper we focus on HMMs where the probability density of the observations is intractable. By intractable we mean that cannot be evaluated (or it is computationally prohibitive to calculate). However, we are able to generate samples from despite its intractability.

We will denote the actual observed random variables of the HMM as and assume that they are generated by some unknown which is to be estimated. The maximum likelihood estimate of given is

where is the probability density, or the likelihood, of the observations , and from (1)-(2), is given by

| (3) |

Even when is a finite set, cannot be evaluated because is intractable. There is a sizeable literature on the use of sequential Monte Carlo (SMC) methods, also known as particle filters, to evaluate the gradient of with respect to , which is subsequently used to compute its maximiser, see e.g. the review in Kantas et al., (2009). However, these methods require a tractable and they are not directly applicable when this density is intractable. We thus propose new SMC based maximum likelihood estimation (MLE) algorithms to fill this void. We handle the intractable by drawing on ideas from approximate Bayesian computation (ABC), an inference technique initially developed for Bayesian models with an intractable likelihood, see Marin et al., (2012) for a recent review. Our static parameter estimation algorithms are gradient based and cover both offline (or batch) and online estimation.

Recently Ehrlich et al., (2013) have proposed a gradient based MLE algorithm for HMMs with an intractable observation density . The authors estimate the gradient of the likelihood in (3) using a finite difference approximation which ultimately relies on estimates of only, which itself is calculated using SMC. The major advantage of our method over that of Ehrlich et al., (2013) is that we characterise the gradient of the log likelihood directly, by using available information on how the intractable is simulated from, and subsequently approximate it using SMC, thus avoiding the added error of a finite difference approximation. Our online MLE algorithm is asymptotically unbiased (as our numerical results indicate) as the number of particles increases whereas the same cannot be said for Ehrlich et al., (2013) due to the finite difference approximation; their numerical results indicate a bias that does not diminish with increasing data, even when can be calculated exactly as they illustrate for a linear Gaussian state-space model (see Ehrlich et al., (2013, Figure 2)). Also, as observed from the results in Ehrlich et al., (2013), the variance of the parameter estimates of their recursive MLE algorithm does not diminish with more data while ours does (see the discussion in Section 3.1).

The remainder of this paper is organised as follows. The theory that underpins our MLE methodology is detailed in Section 2 and in Section 3 we describe its SMC implementation. Numerical examples using both simulated and real data sets are given in Section 4. The numerical work covers three intractable models, namely the -stable distribution, g-and-k distribution, and the stochastic volatility model with -stable returns. Finally, Section 5 provides a discussion of other possible methods for parameter estimation in HMMs when both state and observation densities intractable.

2 The ABC MLE approach for parameter estimation

The particle filter sequentially approximates the sequence of posterior densities of the HMM using a weighted discrete distribution with support points for which are called particles. At each time , the particles are resampled according to their current weights, and then the resampled particles are propagated independently of each other using a proposal transition density . The particles are then reweighed to correct for the discrepancy between and the law of the proposed particles which is . This is standard importance sampling and the assumption in the weight correction step is that the law of each resampled particle at time is , which is an erroneous but progressively correct as is increased (Del Moral, , 2004; Crisan and Doucet, , 2002; Chopin, , 2002). In the implementation of the particle filter the normalising constants of the sequence of target posteriors are not needed but calculating the new weights requires to be tractable. It was shown by Del Moral, (2004) that the weights of the particle approximation of can be used to obtain an unbiased estimate of the likelihoods . See the Appendix for an example code for a particle filter.

Jasra et al., (2012) consider the problem of constructing an SMC approximation of the filter , which is the marginal of the particle approximation for , for a HMM with an intractable observation density . Since it is not possible to calculate the weights of the particle filter for such an HMM where is intractable, they propose a particle filter approximation for the extended HMM where the joint process , which is now the latent process of the extended HMM, is defined by (1) and (2) and the new sequence is

| (4) |

where denotes the ball of radius centred at and is the uniform distribution over the set . Then, the density

of the extended HMM is regarded as an approximation for where reflects the error of the approximation and this error diminishes as ; see also Calvet and Czellar, (2012) and Martin et al., (2012) for theoretical results on this approximation. Note that does not coincide with because obeys the law (1)-(2) and not (4). Jasra et al., (2012) remark that is the ABC approximation for the filter of a HMM. Furthermore, they show it is straightforward to approximate with a bootstrap particle filter.

Consider now the extended HMM specified by (1), (2) and (4) and let denote the probability density (or likelihood function) of the process evaluated at some . (See (11) for the precise expression of this density.) Dean et al., (2011) study the theoretical properties of the following maximum likelihood estimate of :

| (5) |

They call this procedure ABC MLE. (Note that despite the word ‘Bayesian’ in ABC, the procedure is not Bayesian.) The bootstrap particle filter of Jasra et al., (2012) provides an unbiased SMC approximation of the likelihood and this likelihood may be maximised by evaluating the approximation over a grid of values for . This, however, is clearly not practical as the dimension of increases, has no straightforward extension for recursive estimation and is not an accurate convergent method.

It was shown in Dean et al., (2011) that the ABC MLE (5) leads to a biased estimate of the parameter vector in the sense that as , will converge to some point , and that this bias can be made arbitrarily small by choosing a sufficiently small value of , i.e. as . The bias of ABC MLE is due to the fact the observed sequence is the outcome of the law (2) for and not (4). Dean et al., (2011) suggest removing the bias of in (5) by adding noise to the real data and then computing the maximum likelihood estimate, i.e. let be a realisation of i.i.d. samples from and let

| (6) |

Note that the noisy data now obeys the law of when . Therefore, the procedure

| (7) |

can now produce a consistent estimator of the parameter vector as . This result proved by Dean et al., (2011) can be interpreted as the frequentist equivalence of Wilkinson’s observation that the ABC posterior distribution is exact under the assumption of model error (Wilkinson, , 2013).

Finally, Dean et al., (2011) also remark that the use of other types of noise in (4) is possible without compromising the asymptotics of noisy ABC MLE, i.e.

| (8) |

where is a smooth centred density. (Accordingly, noisy ABC MLE is performed with the noise corrupted observations (6) where now are realisations of i.i.d. samples from ) As we show, a continuously differentiable is important for the development of practical gradient based MLE techniques. In this work we choose to be the probability density of zero-mean unit-variance Gaussian random variable. Other choices are possible (but not investigated) and our framework would still be applicable.

We remark that although the theoretical basis for ABC MLE was established in Dean et al., (2011), the authors do not propose a practical methodology for implementing ABC MLE in their work; this is indeed an important void to be filled. In this paper we demonstrate how, by using ideas from Poyiadjis et al., (2011), both batch and online versions of noisy ABC MLE can be implemented with SMC.

3 Implementing ABC MLE with SMC

We assume that for all there exist a distribution on some auxiliary space with a tractable density with respect to and a function such that one can sample from by first sampling from and then applying the transformation ; i.e. the law of is . From this it follows that the process in (8) can be equivalently generated as

| (9) |

where is the hidden state of the original HMM given by (1) and for all . We will implement SMC based MLE for the following HMM: Let be the latent process and in (9) be the observation process. The initial and transition densities for (with respect to the dominating measure ) and the observation density of (with respect to the Lebesgue measure on ) are

| (10) |

where and . The density of the observed process of this HMM evaluated at some is

| (11) |

where . Note that in (11) is indeed the likelihood function to be maximised with respect to in ABC MLE in Section 2; see (5) and (7). Moreover all the densities declared in (10) are tractable and differentiable functions of (provided that , , and are differentiable with respect to ).

Henceforth, we will work exclusively with the HMM defined in (10). As discussed before, we corrupt the real measurements with a single realisation of independent samples from a -independent probability density , i.e.

to obtain a realisation of the observed process of the HMM .

3.1 Gradient ascent

One well known MLE algorithm is the following iterative gradient ascent method which updates the parameter estimate using the rule

| (12) |

where is an arbitrary initial estimate. Here is a sequence of step-sizes satisfying the constraints and so as to ensure that the algorithm converges to a local maximum of . The term is shorthand for the -valued vector

which is also called the score vector, and is given by Fisher’s identity (e.g. see Cappé et al., (2005))

| (13) |

with the convention that . Note that the method in (12) uses the whole data set at every parameter update step, which makes it a batch method. An alternative to it is the following online gradient ascent method which updates the parameter estimate every time a new data point is received

| (14) |

where

| (15) |

While the subscript indicates that is evaluated at , a necessary requirement for a truly online implementation is that the previous values of estimates (i.e. other than ) are also used in the evaluation of (Le Gland and Mevel, , 1997).

It is important to note that, for both batch (12) and online method (14), we require that the transition density of be tractable and differentiable with respect to , which is precisely why we propose to work with rather than whose state transition density contains the intractable . (We discuss suitable alternatives when the state transition density is intractable in Section 5.1.)

It is apparent from (12) and (14) that an SMC implementation of these MLE algorithms hinges on the availability of a particle approximation of the score in (13). Poyiadjis et al., (2011) discuss two methods to estimate the score using the SMC approximation of the full posterior . One method is nothing more than the substitution of the law in (13) with its particle approximation and has a cost, like the particle filter itself, which is . We will refer to this estimate of the gradient as the method (Poyiadjis et al., , 2011, Algorithm 1). Due to resampling step of the particle filter there is a lack of unique samples in the particle approximation of for much smaller than , which is called particle degeneracy in the literature. Poyiadjis et al., (2011) shows that the variance of this score estimate, where the variance is computed with respect to the particles being sampled while the observation sequence is held fixed, grows quadratically with time. While this may not be an issue for the batch method in (12), it is not suitable for online estimation (14) since the variance of the resulting estimate of grows linearly with time .

As an alternative to this standard score estimate, Poyiadjis et al., (2011) propose an estimate of the score computed using the same particle approximation to which aims to avoid the particle degeneracy problem mentioned. We will refer to this as the method (Poyiadjis et al., , 2011, Algorithm 2). The authors experimentally show that the variance of the score estimate now grows linearly in time while the variance of the resulting estimate of is time-uniformly bounded (i.e. does not grow); a proof of the latter fact can be found in Del Moral et al., (2011). Therefore, the SMC implementation of we adopt for online estimation (14) is the method.

Finally, we mention that the score (12) can also be estimated using a fixed-lag method which would have a computational cost which is and a variance which grows linearly in time. However there is the added error introduced by not smoothing beyond a certain lag; see Kantas et al., (2009) for a review of static parameter estimation techniques.

3.2 Controlling the variance of the gradient estimate

If the Monte Carlo estimates of the gradient terms have high or infinite variances, we expect failure of the gradient ascent methods. We can stabilise the variance by transforming the observed data, but without compromising the identifiability of the model, and then add noise as discussed in noisy ABC. This approach to stabilising the variance is novel as the issue of infinite variance has not been reported before in the SMC literature.

This issue of the potential for infinite variance (prior to stabilising by adopting a specific transformation) can be perfectly exemplified by the problem of learning the parameters of a distribution from a sequence of i.i.d. random variables which we now discuss. Let be an i.i.d. sequence with an intractable probability density on . For any , assume can be sampled from by first generating from the density and then followed by the application a certain transformation function , i.e. the law of is . (The -stable process is generated precisely in this way; see Example 1 below.) We are given a realisation from and the latter is to be estimated. Let be the noise corrupted observed sequence as in (8). In the context of the discussion in Section 3, the aim is to maximise the likelihood of the noisy observations (generated from the true model ) using the parametric family of HMMs . Since are i.i.d. the batch (12) and online (14) update rules become, respectively,

in (10) becomes and

| (16) |

where Therefore can be estimated using an -sample Monte Carlo approximation to , e.g. with either MCMC or importance sampling. One important point to note about this i.i.d. case is that the method becomes .

We now calculate the variance of the Monte Carlo estimate of (16) at given i.i.d. samples from (Note that in the numerical examples we actually use importance sampling to sample from but the following calculation is done assuming i.i.d. samples are available for illustrative purposes.) Dropping the index , given a noise corrupted measurement generated from the true model , and i.i.d. samples , an estimate of is

We are interested in the variance of this quantity with respect to the law of . We consider the case where has a finite second moment, e.g. see the example to follow. Then, the sum above has a finite second moment if and only if has a finite second moment with respect to the joint law of . One can show that

| (17) |

If the second moment of is infinite (or very high), we may circumvent this instability problem by transforming the actual observed process from using a suitable one-to-one function prior to adding noise. That is, we replace (8) with the following transformed noise corrupted process

| (18) |

The conditional density becomes

and the right hand side of (17) now is . In this paper we use throughout, and in the following example we show how (17) is infinite but subsequently stabilised with this transformation.

Example 1.

(The -stable distribution.) Let denote the -stable distribution. The parameters of the distribution,

represent the shape, skewness, location, and scale respectively. One can generate a random sample from by generating , where and are independent, and setting

The mapping is defined as (Chambers et al., , 1976)

where

Although it is hard to show for and , we can show that

unless . Therefore, it is not desirable to run the gradient ascent method for the process with since the variance of the gradient estimate will be infinite. Instead, we use the transformation , i.e. to make the gradient ascent method stable. One can indeed check that for the parameter

We also verify numerically in Section 4 that the gradients with respect to the other parameters , are stabilised with (while we can show that ).

4 Numerical examples

In this section we demonstrate the performance of the gradient ascent methods described in Section 3 on the i.i.d. -stable and g-and-k models as well as the stochastic volatility model with -stable returns.

4.1 MLE for i.i.d. -stable random variables

We first consider the problem of estimating the parameters of an -stable distribution (developed in Example 1) from a sequence of i.i.d. samples. Several methods for estimating parameter values for stable distributions have been proposed, including a Bayesian approach based on ABC, see Peters et al., (2011). In this example we consider estimating these parameters using the online gradient ascent method to implement noisy ABC MLE. Since the only discontinuity in the transformation function for generating an -stable random variable is at , we can safely use the gradient ascent method for estimating with being not in the close vicinity of .

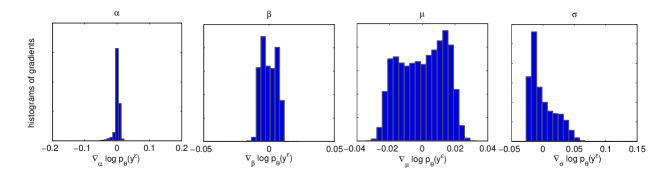

As recommended in Example 1, we transform the observations using for stability. In order to check, numerically, whether the transformation in (18) with stabilises the gradients, we can look at the empirical distribution of the Monte Carlo estimates of after transforming the observations . For this purpose, we generate samples from and from for , and for each sample we estimate , where , with , using self-normalised importance sampling with samples generated from . Figure 1 shows the histograms of the Monte Carlo estimates of which confirms that the transformation does stabilise the gradients.

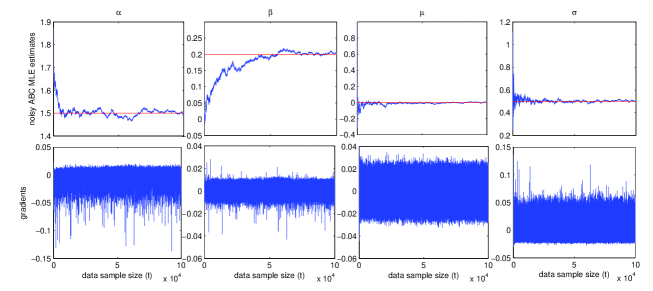

The outcome of online gradient ascent method to implement noisy ABC MLE for the same data set is shown in Figure 2. A trace plot of the sequence of gradient estimates (as is adjusted) is also shown as further confirmation of the stability of the estimated gradients.

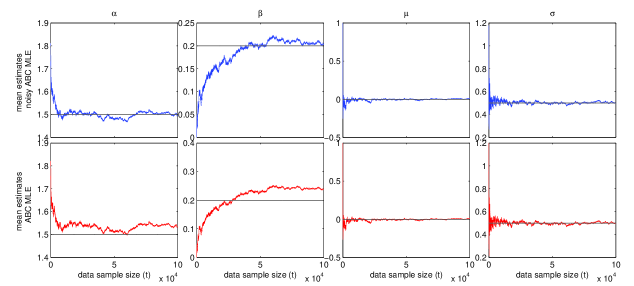

The next experiment contrasts the ABC MLE and noisy ABC MLE solutions for the same data set. The results in Figure 3 compare the online estimates averaged over 50 independent runs for both algorithms. Each run used the same data set but a new realisation of particles. The outcome of this comparison is that ABC MLE yields biased estimates for the shape and skewness parameters and whereas the bias is not present in noisy ABC MLE.

4.2 MLE for g-and-k distribution

The g-and-k distribution is defined by the following parameterised quantile (or inverse distribution) function

| (19) |

where is the ’th standard normal quantile. The parameters

are the skewness, kurtosis, location and scale, and is usually fixed to . Therefore one can generate from the g-and-k distribution by first sampling and then returning (Rayner and MacGillivray, , 2002).

Bayesian parameter estimation for the g-and-k distribution using ABC was recently proposed in Fearnhead and Prangle, (2012). We consider online MLE for using the noisy ABC likelihood. Note that in (19) is differentiable with respect to and so the gradient ascent method is applicable. To avoid gradients with very high variances resulting from the factor in , similar to the case of -stable distribution, we transform the actual observations using and add noise with . In our experiments it was noticed that our method performs better when the location parameter is closer to , which must be a result of the non-linear behaviour of the transformation function . Therefore, whenever possible, it is suggested to estimate using some (possibly heuristic) method (such as using the mean of the first few samples) as a preprocessing step, subtract the heuristically estimated value of from the samples, perform MLE on the (approximately) centred data, and then add back to the estimated location obtained by the MLE algorithm.

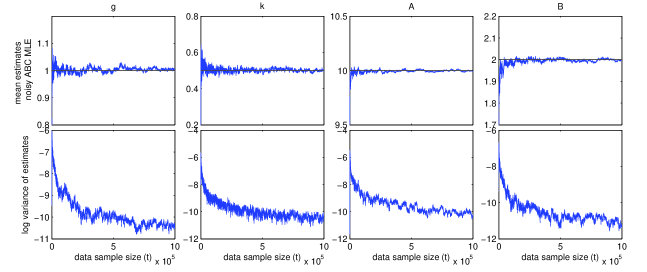

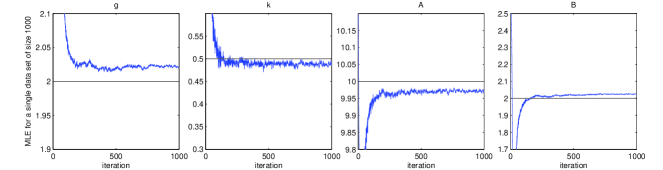

Figure 4 shows the results of online gradient ascent method (14) to implement noisy ABC MLE for estimating . In the figure we observe the mean and log-variance of 50 runs on the same noisy transformed data sequence. (Therefore, the accuracy and the variance of the estimates correspond to the performance of the Monte Carlo approximation of the gradients .) Self-normalised importance sampling is used with samples generated from . From the results in Figure 4, we can see that the bias introduced by the finite number of particles is negligible for and that the variance of the algorithm reduces in time suggesting the convergence of the estimates in each run to essentially the true parameter values.

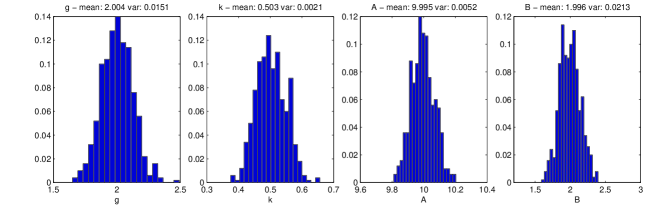

The next experiment shows how the noisy ABC MLE can be implemented with the batch gradient ascent method (12) when the data set is too small for the online method to converge. A detailed study of MLE for g-and-k distribution can be found in Rayner and MacGillivray, (2002) where MLE methods based on numerical approximation of the likelihood itself are investigated. We generated 500 data sets of size from the same g-and-k distribution with and executed the batch gradient ascent method with on each data set. Again, self-normalised importance sampling is used with samples. The upper half of Figure 5 shows the estimation results with noisy ABC MLE versus number of iterations for a single data set. Note that for short data sets, is usually not the true maximum likelihood solution. The lower half of Figure 5 shows the distributions (histograms over 20 bins) of the converged maximum likelihood solution for . The mean and variance of the estimates for are and respectively. Comparable values for these moments at this particular and data size were also obtained in Rayner and MacGillivray, (2002, Table 3).

4.3 The stochastic volatility model with symmetric -stable returns

The stochastic volatility model with -stable returns (SVR) is a financial data model (Lombardi and Calzolari, , 2009). The hidden process represents the log-volatility in time whereas the observation process is the log return values. The model for with parameters is:

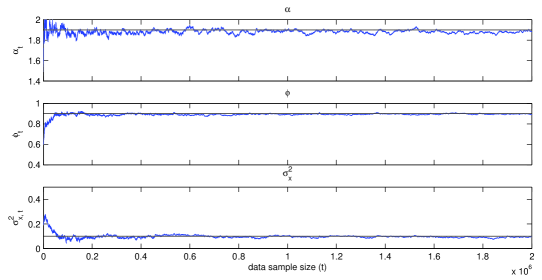

This model is an alternative to the stochastic volatility model with Gaussian returns to account for an observed series which is heavy-tailed and displays outliers. For more discussion on the model as well as a review of methods for estimating the static parameters of such models, see Lombardi and Calzolari, (2009) and the references therein. These existing methods for parameter estimation in SVR are batch and suitable for only short data sequences. We simulated a scenario where a very long data sequence generated from this model with is being received sequentially. We used online gradient ascent method (14) to find the noisy ABC MLE solution for this data sequence, where the method (Poyiadjis et al., , 2011, Algorithm 2) with particles was used to estimate (15). Again, we transform the actual observations with the function and then add noise. Figure 6 shows the online estimates of for data samples. The estimates seem to converge after around samples and are accurate.

4.4 Offline noisy ABC MLE for real data

We now consider a real data experiment, where the data are the daily GBP-DEM exchange rates between to containing samples ; these data are considered in Lombardi and Calzolari, (2009). Log-returns are obtained by , . The observations, , are the residuals of the AR(1) process that is fitted to . (We used the same model and data set as Lombardi and Calzolari, (2009) in order to compare our results with theirs). The SVR model above is assumed for , where the hidden process has an extra parameter :

hence .

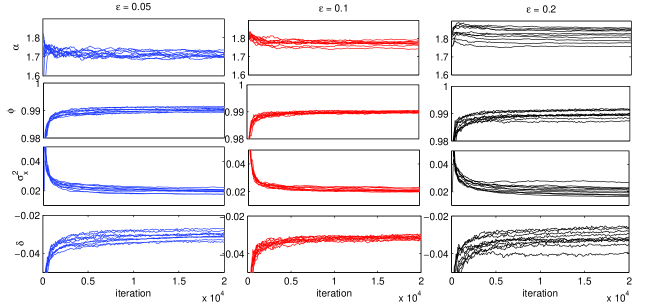

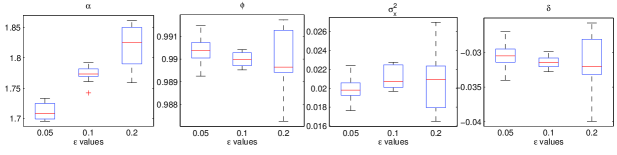

We implemented noisy ABC MLE using batch gradient ascent (12) with the method (Poyiadjis et al., , 2011, Algorithm 1) with particles to approximate (13). To measure the variability of the estimates as a function of the realisation of added noise and the value, we repeated the estimation with , , and , separately, where for each we ran the method with different added noise realisations. For all runs, we terminated the batch gradient ascent algorithm after iterations. particles were used to evaluate the gradients at each iteration. Figure 7 (top) shows the estimates versus number of iterations, where the trajectories for different noisy data sets for the same value of are superimposed. Also, the bottom part of Figure 7 shows the box-plots of the estimates of for different values, where the box-plots for each were created from the converged estimates of (the average of the estimates at the last 1000 iterations) obtained from 10 different noisy data sets generated using that value of . For the ease of explanation, we will denote them as

| (20) |

where is the converged estimate obtained from the ’th noisy data set that was generated using .

Figures 7 suggests a trade off between accuracy in the estimates and computational efficiency in the following sense. A smaller value of is expected yield less biased estimates (with respect to the maximiser of the true likelihood of the real data) with less variance (with respect to the added noise) provided that the maximisation is performed exactly, that is with infinitely many and infinitely many number of parameter updates. On the other hand, smaller results in the decrease of the effective sample size in the SMC algorithm and hence increases the variance of the SMC estimate of the gradient of the log likelihood. The effect of this on our results is the larger variance in the estimates obtained with compared to those obtained with (which would eventually be smaller if the maximisation were performed exactly). In conclusion, for a fixed batch data size and a given amount of computational resource, one must optimise the trade off between the (average) accuracy and the variability in the estimates, for which the effective sample size of the particles could be used as a rule of thumb.

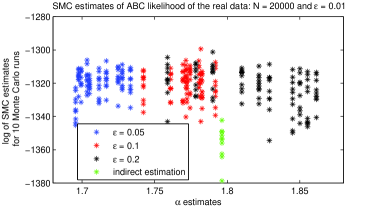

Lombardi and Calzolari, (2009) fitted the same model to the same data set using the indirect estimation method and their estimates of was , which is slightly different to our results. Both ours and their method aim for the maximum likelihood solution, which suggests that it would be sensible to compare the likelihood of the true data sequence for the estimates of obtained from both methods. However, this is not possible since neither nor an unbiased Monte Carlo estimator of it is available. Instead, we compared the unbiased SMC estimates of the ABC likelihoods using an small enough to make the effect of model mismatch negligible (see the discussion of model mismatch error in Section 2) for comparison and large enough to ensure that the variability of the SMC estimate of the likelihood across the particle realisations is not too much; for these reasons we chose and . (See Appendix for the details of the implementation.) The left hand side of Figure 8 shows the logarithms of the 10 independent SMC estimates of calculated at the value of each estimate in (20). For comparison, the results are shown with 10 independent SMC estimates of at . The figure shows that noisy ABC MLE has improved the results of Lombardi and Calzolari, (2009) for all values of that we used, in the sense that almost all the estimates resulting from the ABC MLE method yields a higher likelihood of the data set to which the model is fitted.

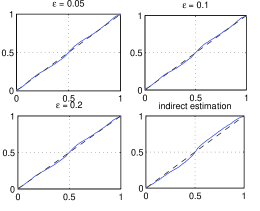

Finally, we perform a simple model check for by considering the conditional cumulative distribution functions

at the values of estimated using noisy ABC MLE and the indirect estimation method in Lombardi and Calzolari, (2009). Since are i.i.d. uniform random variables on (Diebold et al., , 1998), we expect the probability plot (for the uniform distribution) of the population to approximate the line under the hypothesis that is generated from the SVR model . However, we are unable to perform these calculations for the original HMM due to the intractability of . Instead, we use the modified HMM but with small enough for one to neglect the difference between the two models (as in the previous experiment). The probability plots at the right hand side of Figure 8 were generated from the SMC estimates of

(see Appendix for the details), with and , for four different values of : the first three are the means of for , and , respectively, and the fourth one is . The probability plots are all close to the line which justifies the SVR model; they also indicate that there is more agreement between the SVR model and the data when is the noisy ABC MLE solution than when it is the maximum likelihood solution of the indirect estimation method.

5 Discussion

In this paper, we have presented SMC implementations of MLE for HMMs with an intractable observation density. We showed how SMC versions of both batch and online gradient ascent algorithms can be used to implement noisy ABC MLE and how a further transformation of the data can stabilise the variance of the SMC gradient estimate. We have shown that SMC implementations of the methodology in Dean et al., (2011) is practical and yields convergent and accurate estimates of even when the exact procedures in Dean et al., (2011) are replaced by their SMC counterparts.

5.1 Other MLE methods for HMMs with an intractable density

Although not as general as the gradient ascent MLE approach, the expectation-maximisation (EM) algorithm may be available for some models, at least for a part of the parameters in , if the joint density belongs to an exponential family. Both and batch and online EM algorithms can be devised using SMC; details of such algorithms can be found in Cappé, (2009) and Del Moral et al., (2009).

There are other gradient MLE methods in the literature that are available for implementing noisy ABC MLE and we have discussed the technique of Ehrlich et al., (2013) in the introduction. One advantage of their finite difference method is that it is essentially a gradient free technique as it bypasses having to calculate the derivatives with respect to of the state transition and observation densities of the HMM and thus can cope, without modification, with an intractable state transition density. Another gradient based method that uses SMC to approximate the gradient of the log-likelihood without the need to calculate the derivatives of the HMMs densities is the iterated filtering algorithm of Ionides et al., (2011). In particular, one can use iterated filtering for or in order to estimate . However, the method does not have an extension to online estimation. Another downside is that the algorithm requires an increasing number of particles versus iteration for convergence.

Coquelin et al., (2009) study a HMM with a tractable observation density but an intractable state transition density . Assume one can generate from by sampling from and using a differentiable function such that . The gradient of the log likelihood in such HMMs can be estimated using the infinitesimal perturbation analysis (IPA) approach proposed in Coquelin et al., (2009), provided that , , and are differentiable with respect to as well as the state variable . We can straightforwardly adopt the IPA approach with our noisy ABC MLE to deal with a fully intractable model, where both the state transition and the observation densities are intractable. However, IPA is a path space method and suffers from particle degeneracy. This will lead to the variance of the estimate of the score in (13) increasing quadratically in time like the method in Poyiadjis et al., (2011). As the authors mention, fixed-lag smoothing could be use to control this variance growth but at the cost of a small bias.

Static parameter estimation for HMMs with intractable state and observation densities have been addressed in a Bayesian context by Campillo and Rossi, (2009). Campillo and Rossi, (2009) utilise the so called convolution particle filter, which uses ideas from kernel density estimation to replace the intractable densities needed for the weight evaluation in the particle filter with their kernel estimates, to sequentially estimate the posterior distribution of . While an SMC based Bayesian approach can potentially produce good estimates of for short data lengths, at least for tractable models where standard particle methods apply, particle degeneracy does bias the estimation results for long data sets (Andrieu et al., , 2005; Kantas et al., , 2009). In contrast our methods do give rise to practically consistent estimators as our numerical results indicate.

Finally, we remark that MLE using ABC is studied in the recent work Rubio and Johansen, (2013), but in a non-HMM setting where the likelihood of data given is intractable. The authors form a kernel density estimate of the likelihood from samples drawn from the ABC posterior distribution. They propose maximising the kernel density estimate as an approximation to MLE. Unlike Rubio and Johansen, (2013), we consider the HMM setting and our methods do not need samples of .

Acknowledgement

S.S. Singh and T. Dean’s research was funded by the Engineering and Physical Sciences Research Council (EP/G037590/1) whose support is gratefully acknowledged. A. Jasra was supported by an MOE Singapore grant and is also affiliated with the Risk Management Institute at the National University of Singapore.

References

- Andrieu et al., (2005) Andrieu, C., Doucet, A., and Tadić, V. B. (2005). On-line parameter estimation in general state-space models. In Proceedings of the 44th IEEE Conference on Decision and Control, pages 332–337.

- Calvet and Czellar, (2012) Calvet, C. and Czellar, V. (2012). Tracking beliefs: Accurate methods for approximate Bayesian computation filtering. Technical Report 236, HEC Paris.

- Campillo and Rossi, (2009) Campillo, F. and Rossi, V. (2009). Convolution particle filter for parameter estimation in general state-space models. Aerospace and Electronic Systems, IEEE Transactions on, 45(3):1063 –1072.

- Cappé, (2009) Cappé, O. (2009). Online sequential Monte Carlo EM algorithm. In Proceedings of the IEEE Workshop on Statistical Signal Processing.

- Cappé et al., (2005) Cappé, O., Moulines, E., and Rydén, T. (2005). Inference in Hidden Markov Models. Springer.

- Chambers et al., (1976) Chambers, J. M., Mallows, C. L., and Stuck, B. W. (1976). Method for simulating stable random variables. Journal of the American Statistical Association, 71(354):340–344.

- Chopin, (2002) Chopin, N. (2002). A sequential particle filter method for static models. Biometrica, 89(3):539–551.

- Coquelin et al., (2009) Coquelin, P., Deguest, R., and Munos, R. (2009). Sensitivity analysis in HMMs with application to likelihood maximization. In Bengio, Y., Schuurmans, D., Lafferty, J., Williams, C. K. I., and Culotta, A., editors, Advances in Neural Information Processing Systems 22, pages 387–395.

- Crisan and Doucet, (2002) Crisan, D. and Doucet, A. (2002). A survey of convergence results on particle filtering methods for practitioners. Signal Processing, IEEE Transactions on, 50(3):736–746.

- Dean et al., (2011) Dean, T., Singh, S., Jasra, A., and Peters, G. (2011). Parameter estimation for hidden Markov models with intractable likelihoods. Technical Report 1103.5399, arXiv.org.

- Del Moral, (2004) Del Moral, P. (2004). Feynman-Kac Formulae: Genealogical and Interacting Particle Systems with Applications. Springer-Verlag, New York.

- Del Moral et al., (2009) Del Moral, P., Doucet, A., and Singh, S. (2009). Forward smoothing using sequential Monte Carlo. Technical Report 638, Cambridge University, Engineering Department.

- Del Moral et al., (2011) Del Moral, P., Doucet, A., and Singh, S. (2011). Uniform stability of a particle approximation of the optimal filter derivative. Technical Report CUED/F-INFENG/TR 668, Cambridge University, Engineering Department.

- Diebold et al., (1998) Diebold, F. X., Gunther, T., and Tay, A. (1998). Evaluating density forecasts, with applications to financial risk management. International Economic Review, 39:863–883.

- Durbin et al., (1998) Durbin, R., Eddy, S., Krogh, A., and Mitchison, G. (1998). Biological Sequence Analysis: Probabilistic Models of Proteins and Nucleic Acids. CUP: Cambridge.

- Ehrlich et al., (2013) Ehrlich, E., Jasra, A., and Kantas, N. (2013). Gradient free parameter estimation for hidden Markov models with intractable likelihoods. Methodology and Computing in Applied Probability (to appear).

- Fearnhead and Prangle, (2012) Fearnhead, P. and Prangle, D. (2012). Constructing summary statistics for approximate Bayesian computation: semi-automatic approximate Bayesian computation. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 74(3):419–474.

- Felsenstein and Churchill, (1996) Felsenstein, J. and Churchill, G. (1996). A hidden Markov model approach to variation among sites in rate of evolution. Molecular Biology and Evolution, 13:93–104.

- Ionides et al., (2011) Ionides, E. L., Bhadra, A., and King, A. (2011). Iterated filtering. The Annals of Statistics, 39(3):1776–1802.

- Jasra et al., (2012) Jasra, A., Singh, S., Martin, J., and McCoy, E. (2012). Filtering via approximate Bayesian computation. Statistics and Computing, 22:1223–1237.

- Kantas et al., (2009) Kantas, N., Doucet, A., Singh, S. S., and Maciejowski, J. M. (2009). An overview of sequential Monte Carlo methods for parameter estimation in general state-space models. In Proceedings IFAC System Identification (SysId) Meeting.

- Kim et al., (1998) Kim, S., Shephard, N., and Chib, S. (1998). Stochastic volatility: Likelihood inference and comparison with ARCH models. The Review of Economic Studies, 65:361–393.

- Le Gland and Mevel, (1997) Le Gland, F. and Mevel, L. (1997). Recursive estimation in hidden Markov models. In Decision and Control, 1997., Proceedings of the 36th IEEE Conference on, volume 4, pages 3468–3473.

- Lombardi and Calzolari, (2009) Lombardi, M. J. and Calzolari, G. (2009). Indirect estimation of -stable stochastic volatility models. Computational Statistics & Data Analysis, 53(6):2298–2308.

- Marin et al., (2012) Marin, J.-M., Pudlo, P., Robert, C. P., and Ryder, R. J. (2012). Approximate Bayesian computational methods. Statistics and Computing, 22(6):1167–1180.

- Martin et al., (2012) Martin, J., Jasra, A., Singh, S. S., Whiteley, N., and McCoy, E. (2012). ABC smoothing. Technical report, Imperial College London.

- Peters et al., (2011) Peters, G., Sisson, S., and Fan, Y. (2011). Likelihood-free bayesian inference for alpha stable models. Computational Statistics and Data Analysis, 56(11):3743–3756.

- Poyiadjis et al., (2011) Poyiadjis, G., Doucet, A., and Singh, S. S. (2011). Particle approximations of the score and observed information matrix in state space models with application to parameter estimation. Biometrika, 98(1):65–80.

- Rayner and MacGillivray, (2002) Rayner, G. D. and MacGillivray, H. L. (2002). Numerical maximum likelihood estimation for the g-and-k and generalized g-and-h distributions. Statistics and Computing, 12(1):57–75.

- Rubio and Johansen, (2013) Rubio, D. B. and Johansen, A. M. (2013). A simple approach to maximum intractable likelihood estimation. Electronic Journal of Statistics, 7:1632–1654.

- Wilkinson, (2013) Wilkinson, R. (2013). Approximate Bayesian computation (ABC) gives exact results under the assumption of model error. Statistical Approaches in Genetics and Molecular Biology, (to appear, also available in arXiv:0811.3355v2).

Appendix

Algorithm 1.

SMC for estimating and

Begin with . For ,

-

•

Prediction: for , sample as follows:

-

–

If , sample ,

-

–

If , sample , .

-

–

-

•

Weighting: for , calculate the unnormalised weights

-

•

Likelihood estimate: Update the likelihood estimate by .

-

•

conditional cumulative distribution function: Calculate

-

•

Resampling: Sample from using the weights .