Restricted likelihood representation and decision-theoretic aspects of meta-analysis

Abstract

In the random-effects model of meta-analysis a canonical representation of the restricted likelihood function is obtained. This representation relates the mean effect and the heterogeneity variance estimation problems. An explicit form of the variance of weighted means statistics determined by means of a quadratic form is found. The behavior of the mean squared error for large heterogeneity variance is elucidated. It is noted that the sample mean is not admissible nor minimax under a natural risk function for the number of studies exceeding three.

doi:

10.3150/13-BEJ547keywords:

copyrightownerIn the Public Domain

1 Parameter estimation in meta-analysis: Random-effects model

In the simplest random-effects model of meta-analysis involving, say, studies the data is supposed to consist of treatment effect estimators , which have the form

Here is an unknown common mean, is zero mean between-study effect with variance , , and represents the measurement error of the th study, with variance . Then the variance of is . In practice is often treated as a given constant, , which is the reported standard error or uncertainty of the th study.

The considered here problem is that of estimation of the common mean and of the heterogeneity variance from the statistical decision theory point of view under normality assumption. If is known, then the best unbiased estimator of is the weighted means statistic, , with the normalized weights,

| (1) |

. Its variance has the form

When is unknown, to estimate the common practice uses a plug-in version of ,

| (2) |

so that an estimator of is required in the first place.

Usually such an estimator is obtained from a moment-type equation [15]. For example, the DerSimonian–Laird [3] estimator of is

with denoting the Graybill–Deal estimator of . The popular DerSimonian–Laird -estimator is obtained from (2) by using the positive part of .

Similarly the estimator of ,

leads to the Hedges estimator of .

The paper questions the wisdom of using under all circumstances the tradition of plugging in estimators to get estimators. Indeed the routine of plug-in estimators may lead to poor procedures. For example, by replacing the unknown by in the above formula for , one can get a flagrantly biased estimator which leads to inadequate confidence intervals for .

A large class of weighted means statistics is motivated by the form of Bayes procedures derived in Section 2.2. These statistics which typically do not admit the representation (2) induce estimators of the weights (1) which shows the primary role of -estimation.

The main results of this work are based on a canonical representation of the restricted likelihood function in terms of independent normal random variables and possibly of some -random variables. An important relationship between the weighted means statistics with weights of the form (1) and linear combinations of ’s, which are shift invariant and independent, follows from this fact. Our representation transforms the original problem to that of estimating curve-confined expected values of independent heterogeneous -random variables. This reduction makes it possible to describe the risk behavior of the weighted means statistics whose weights are determined by a quadratic form.

We make use of the concept of permissible estimators which cannot be uniformly improved in terms of the differential inequality in Section 2.3. This inequality shows that the sample mean exhibits the Stein-type phenomenon being an inadmissible estimator of under the quadratic loss when . A risk function for the weights in a weighted means statistic whose main purpose is -estimation is suggested in Section 2.4. It is shown there that under this risk the sample mean is not even minimax. Section 2.5 discusses the case of approximately equal uncertainties, and Section 3 gives an example. The derivation of the canonical representation of the likelihood function is given in the Appendix; the proof of Theorem 2.1 is delegated to the Electronic Supplement [16].

2 Estimating the common mean

2.1 Restricted likelihood, heterogeneity variance estimation and quadratic forms

The setting with the common mean and the heterogeneity variance described in Section 1 is a special case of a mixed linear model where statistical inference is commonly based on the restricted (residual) likelihood function.

The (negative) restricted log-likelihood function ([17], Section 6.6) has the form

It is possible that some of are equal; let have the multiplicity , so that . Then with the index now taking values from to ,

Here, denotes the number of pairwise different , represents the average of ’s corresponding to the particular , and is their sample variance when . To simplify the notation, we write for , so that . In our problem and , , form a sufficient statistic for and .

Throughout this paper, we assume that . Otherwise all -estimators reduce to the sample mean (but see Section 2.5 where -estimation for equal uncertainties is considered). The results in the Appendix relate the likelihood function to the joint density of independent normal, zero mean random variables . The -dimensional normal random vector which is a linear transform of has zero mean (no matter what is) and the covariance matrix, , with larger than .

To find these numbers, we introduce the polynomial of degree , and its minimal annihilating polynomial which has degree . Define

| (3) |

Thus is a polynomial of degree which has only real (negative) roots, denoted by (coinciding with the roots of different from ). Thus . Note that . When , , and .

The representation (2.1) of the restricted likelihood function very explicitly takes into account one degree of freedom used for estimating , as it corresponds to independent zero mean, normal random variables with variances . In addition, this likelihood includes independent , each being a multiple of a -random variable with degrees of freedom. When , is an unbiased estimator of , . For , with probability one. According to the sufficiency principle, all statistical inference about involving the restricted likelihood can be based exclusively on and . Their joint distribution forms a curved exponential family whose natural parameter is formed by (and perhaps by some ).

Evaluation of the restricted maximum likelihood estimator (REML) is considerably facilitated by employing and . Indeed (2.1) shows that this estimator can be determined by simple iterations as

with as a good starting point, and truncation at zero if the iteration process converges to a negative number. Thus, is related to a quadratic form whose coefficients are inversely proportional to the estimated variances of and of (cf. [4], Section 8).

The form of the likelihood function also motivates the moment-type equations based on general quadratic forms, with positive constants . The moment-type equation written in terms of random variables and is

Then the estimator of by the method of moments is

Unless is large, the probability that takes negative values is non-negligible. Non-negative statistics are used to get -estimators of the form (2).

A different method-of-moments procedure suggested by Paule and Mandel [12] is based on solving the equation,

which has a unique positive solution, , provided that . If this inequality does not hold, . Because of (22), the equation can be rewritten in terms of ’s and ’s as

This representation allows for an explicit form of in some cases.

Indeed, when , , which is also the REML. When , ,

We conclude this section by noticing that the widely used heterogeneity index ([1], page 117) in terms of ’s and ’s takes the from

2.2 Weighted means statistics and suggested estimators

Let us look now at the generalized Bayes estimator of when is a prior distribution for while has the uniform (non-informative) prior. Under the quadratic loss this estimator has the form with given in (2.1)

| (5) |

Thus is a weighted means statistic with normalized weights, , , which are shift invariant, for any real . (Any function of is shift invariant.) Indeed the use of restricted likelihood is tantamount to the practice of weighted means statistics with invariant weights as estimators. (cf. [17], Section 9.2).

Formula (24) in the Appendix gives

with discussed in Section 2.1. Positive coefficients (the diagonal elements of the diagonal matrix defined in Lemma 1) can be found from (17) or rather from (25); is the posterior mean of ,

with . Thus positive is designed to estimate , , and as a function of , decreases. The inequalities, , and , are equivalent.

If and the support of has at least two points, does not admit representation (2) which suggests a more general class of -estimators. Namely, we propose to use weighted means statistics with weights . The Bayes weights belong to a smaller part of this polyhedron, namely to the convex hull of the vectors with coordinates for . If is an estimate of , the weights corresponding to (2),

| (6) |

lie on the boundary of this convex hull. A corner point, , of the convex hull always is an inner point of the polyhedron.

Thus the focus in this paper is on estimators of , which admit the representation,

| (7) |

with and as defined above. The last term in the right-hand side of (7) can be viewed as an arguably necessary heterogeneity correction to .

Notice that (7) does not need an estimate of as a prerequisite. Since is an approximation to , when , the form of the REML in Section 2.1 suggests such an estimator: . If some of the multiplicities exceed one, an estimator of can be derived from by replacing by . According to (24), as well as , has the form (7). In fact, all traditional statistics (2) admit this representation.

2.3 Estimation of multivariate normal mean and permissible procedures

We look now at the quadratic risk behavior of -estimators of the form (7). If is such an estimator with positive normalized weights which are shift invariant functions of , then it is unbiased. Its variance does not depend on and can be written as

| (8) |

by independence of and . This and more general decompositions of the mean squared error are discussed by Harville [5]. The second term in the right-hand side of this identity is an important variance component which shows how well approximates the optimal but unavailable , and which relates our setting to the classical estimation problem of the multivariate -dimensional normal mean.

Proposition 2.1

If the coefficients defining the estimator (7) are piecewise differentiable in ’s, then

where . When , is an inadmissible estimator of under the quadratic loss.

The omitted proof of Proposition 2.1 is based on (24), (25), and on familiar integration by parts technique. It demonstrates linkage of our situation to the differential inequality of a statistical estimation problem [2]. Namely, if for some vector , , then is an unbiased estimate of . Therefore , , improves on , , as a -estimator provided that for all values ,

| (9) |

Following [13], let us call a (piecewise differentiable) vector function permissible if (9) does not have any solutions providing a strict inequality at some point. Thus, is a permissible estimator of the vector normal mean if and only if the corresponding scalar -estimator, , cannot be improved upon in the sense of differential inequality (9). Since for , is not a permissible function, the sample mean is inadmissible in the original setting. Indeed the left-hand side of (9) is negative for proving this statement.

The differential operator in (9) does not involve ’s or ’s, but in our problem only functions such that and are of interest. Since is positive and cannot exceed , according to the first equality in Proposition 2.1, can be improved by .

The proof of Theorem 1 in [2] shows that any permissible in our situation is of the form

with some piecewise differentiable positive function . When and for a positive quadratic form , one gets . If there are multiplicities exceeding one, the quadratic form is to be replaced by . For example, the function, , leads to the estimator (7) with

| (10) |

The statistic , corresponding to , when is similar to the positive part of the Stein estimator of the vector normal mean which improves over . However, in the meta-analysis context it is desirable having the coefficients of the same ordering as , and this condition may not hold for . As a matter of fact, despite doing better than or , the weights do not produce a good estimator of . The same is true for many other procedures (10) satisfying condition (12) of Theorem 2.1 in the next section. This theorem shows that if , is an inadmissible estimator of although the function is permissible then.

2.4 -risk and asymptotic optimality

According to (8) the variance of estimator (7) is completely determined by the term, , which can be interpreted as a cost of not knowing when estimating , or as a new risk of viewed as a procedure providing approximations to . More conveniently, with , define

to be the -risk of . Because of (24) and (7), the ensuing random loss function has the form,

This loss is invariant under a scale change of (or of ). For ,

so that the normalizing factor in the definition of amplifies the error in approximating when is large. The results of this section show that for estimators satisfying conditions of the following Theorem 2.1,

when . Thus, is the dominating contribution to the variance of when is large. The -risk is a useful tool for the comparison of estimators (7), as unlike the normalized quadratic risk, , it removes this linear in term.

If with an invariant , then can be interpreted as a conventional risk of the estimator . However under this risk large values of are not penalized very much no matter what is. Indeed is not designed to estimate itself, but rather estimates (cf. [11], page 329). When , the estimator , which corresponds to , is even admissible which of course cannot happen for any unbounded loss function. This circumstance explains why an estimator may have a large quadratic risk, while the associated estimator in (2) has a small variance. That phenomenon is known to happen in the case of the DerSimonian–Laird procedure [6].

The estimator has a constant risk, , which raises the question of its -minimaxity, i.e., if . In contrast, for the Graybill–Deal estimator, , so that its -risk, which vanishes when , grows quadratically in . The next result gives a large class of estimators with bounded -risk improving on when .

Theorem 2.1

Under notation of Section 2.1, let for , be a quadratic form with positive coefficients . If has the form (7) such that for , then

where independent standard normal are independent of . Equal coefficients (and only they) provide the asymptotically optimal quadratic form. If , the optimal choice is . The sample mean is not -minimax, any estimator (7) with weights (10) improves on it if

| (12) |

Theorem 2.1 shows that the traditional weights (6) with are not asymptotically optimal unless the quadratic form coincides (up to a positive factor) with , and . Only then (2.1) is an equality. Thus, the Hedges estimator for which and , is not asymptotically optimal albeit its performance is the best when is large. For the Mandel–Paule estimator from Section 2.1, as well as for the REML, (2.1) also holds with the same quadratic form and the same . The DerSimonian–Laird estimator is defined by the quadratic form with . Therefore, these three statistics are not optimal for large either.

The case when was studied in [14]. Then is admissible (so that it is automatically minimax under ). Any estimator (7) has the form (2) with some , and its -risk grows linearly in ,

For , as , (see Electronic Supplement). By analogy with the Stein phenomenon, admissibility of the sample mean when is expected.

2.5 Equal uncertainties and minimax value

When , the minimax value, , (which does not exceed one since ) cannot be smaller than . Indeed for any estimator ,

This fact can be proven by constructing a sequence of proper prior densities for such that the corresponding sequence of the Bayes -risks converges to .

Thus for large , the estimators (7) with , , cannot be improved upon. The most natural of these statistics, say, has the form (7) with

| (13) |

Another modified Hedges estimator, , has the form (2) with and also is asymptotically optimal although in general its performance is worse than that of (13).

If , so that all and tend to , ,

Here and further is the distribution function of -law with degrees of freedom. Thus if , our problem is that of estimation of the reciprocal of the scale parameter under the restriction, . The “data” in this problem is -distributed, , and the invariant loss function, , corresponds to the -risk. Then the minimax value, , is the same as in the non-restricted () parameter case [8]. As in unrestricted scale parameter estimation, the generalized prior, , , or , provides a least favorable distribution. See also [9] for more general results.

Thus in meta-analysis problems with exhibiting little variation, the minimax value is expected to stay close to . Indeed when , ,

| (14) |

The formula (14) shows that the estimator (13) is minimax unlike for which .

The DerSimonian–Laird rule, , coincides in this situation with the REML and the Hedges estimator. For the proper maximum likelihood estimator of , . None of these procedures is minimax which indicates that their good properties in meta-analysis may be attributable to a large number of individual studies (large ) or to lack of interest in high heterogeneity (small ).

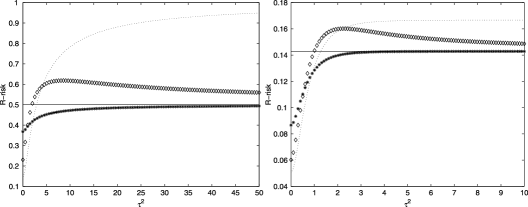

Figure 1 shows the graphs of the -risk in (14) when . It suggests that the estimator performs quite well for small/medium ’s. Indeed this estimator is better than other procedures except for small in which case dominates (at the price of higher risk for larger values of ).

3 Example:

When there are only two different values and with multiplicities and , ,

and if ,

Any estimator (7) has the form (2) for some ,

For , . The modified Hedges estimator with typically has its -risk at larger than that of . (The exact condition for to have a smaller -risk at than is: , and if , then , .)

The -risk of at can be larger than . Indeed

where is the distribution function of . With , according to the Okamoto inequality [10], . Thus, since is an increasing function of ,

This inequality shows that , if , where is monotonically increasing to in For small , cannot have its risk at the origin smaller than . For example, when , if and only if , i.e., iff .

The DerSimonian–Laird estimator with , has its -risk at of the form

with .

But is also competitive against . Indeed if and only if , that is, iff

Thus provided that , improves upon for small . If, say, , this domination means that . Thus, when one study reports a smaller uncertainty than all other studies whose standard errors are approximately equal, improves upon the DerSimonian–Laird estimator for small .

However, there is no uniform domination as the condition, , means that for large .

4 Conclusions

Author’s attempt was to give a perspective of a meta-analysis setting from the point of view of the statistical decision theory. Although concepts like admissibility or minimaxity have not so far generated much interest among meta-analysts, there is a realization that different desirable qualities of the employed procedures call for different loss functions. The quadratic loss for the mean effect estimators from a wide class leads in a natural way to the -risk suggested and studied in this paper. This risk strongly recommends against the use of the sample mean as a consensus estimate which still happens in some collaborative studies.

Moreover, the -risk questions well recognized excellent properties of the DerSimonian–Laird estimator in the situation when are almost equal, or when one study claims a high precision while all other studies report larger uncertainties which are about the same. The unsatisfactory performance of the Graybill–Deal estimator is well known in the latter case. It is of interest that improves on the DerSimonian–Laird estimator for moderate/small . Inference on the overall effect can be obtained before the heterogeneity variance is estimated, but even in the simplest cases considered here there is no unique rule dominating all others.

This paper is dedicated to the memory of George Casella who was always interested in implications of the statistical decision theory results to practical estimation problems [7].

Appendix

.1 Partial fraction decomposition and weighted means

Let denote unit coordinates vector whose dimension is clear from the context, and put , . In the used here notation of Section 2.1 the vector has the diagonal covariance matrix, .

Lemma .0

For any different from , and for any ,

| (15) |

where

| (16) |

For any ,

| (17) |

If the matrix is determined by its elements in (16), then

| (18) |

and

| (19) |

The matrices and are diagonal, and

| (20) |

With ,

| (21) |

and

| (22) |

[Proof.] By the definition of the polynomial in Section 2.1,

with the right-hand side of this identity being the ratio of two polynomials of degree and , respectively. The formulas (15) and (16) easily follow from the classical result on partial fraction decomposition for such ratios.

By equating coefficients at of and , one gets . The comparison of coefficients at of two equal polynomials, and , shows that

which implies (19).

For any different and

which implies that , or that is a diagonal matrix.

This argument also shows that

as

To prove (20), observe that for , the th element of the matrix has the form,

Here we used the facts that , and .

To determine the diagonal elements of , observe that according to the definition of . Therefore for any ,

Thus, (20) holds.

Because of (16),

| (23) |

To prove (21) for fixed , multiply (15) by , divide by , and sum up over to get the following expression for the th element of the matrix ,

where is the Kronecker symbol (, if otherwise). It is easy to see that , unless there are at least two equal indices among . When all three of these indices coincide,

If, say, ,

The last formula shows that off-diagonal elements of , for have the form

that is, (21) holds for the off-diagonal elements.

We demonstrate now the equality of the diagonal elements of matrices in (21). These elements for the matrix are

Define the polynomial by the formula,

Then the degree of is , and this polynomial is determined by its values at : , and . It follows that

Indeed, the polynomial in the right-hand side has degree . Since

it assumes the same values as at , which establishes (21).

The following important representation for

| (24) |

is a consequence of Lemma 1. Here are independent normal, zero mean random variables with the variances . Indeed the normal random vector has the covariance matrix . Since , and are independent implying independence of and in Section 2.3.

The coefficients provide a simple expression for . Indeed, by dividing (15) by and multiplying it by , one gets after summing up over all and and using (18), (19),

This formula can be written in the form,

| (25) |

which provides the representation of the left-hand side of (25) as a ratio of two polynomials of degree and , respectively and which allows numerical evaluation of ’s without calculating .

Restricted likelihood representation and decision-theoretic aspects of meta-analysis: Electronic supplement \slink[doi]10.3150/13-BEJ547SUPP \sdatatype.pdf \sfilenameBEJ547_supp.pdf \sdescriptionThe supplement contains the proof of Theorem 2.1.

References

- [1] {bbook}[auto:STB—2013/12/09—07:59:19] \bauthor\bsnmBorenstein, \bfnmM.\binitsM., \bauthor\bsnmHedges, \bfnmL.\binitsL., \bauthor\bsnmHiggins, \bfnmJ.\binitsJ. &\bauthor\bsnmRothstein, \bfnmH.\binitsH. (\byear2009). \btitleIntroduction to Meta-Analysis. \blocationNew York: \bpublisherWiley. \bptokimsref \endbibitem

- [2] {bincollection}[mr] \bauthor\bsnmBrown, \bfnmLawrence D.\binitsL.D. (\byear1988). \btitleThe differential inequality of a statistical estimation problem. In \bbooktitleStatistical Decision Theory and Related Topics, IV, Vol. 1 (West Lafayette, Ind., 1986) (\beditor\bfnmS.S.\binitsS.S. \bsnmGupta &\beditor\bfnmJ.O.\binitsJ.O. \bsnmBerger, eds.) \bpages299–324. \blocationNew York: \bpublisherSpringer. \bidmr=0927109 \bptokimsref \endbibitem

- [3] {barticle}[pbm] \bauthor\bsnmDerSimonian, \bfnmR.\binitsR. &\bauthor\bsnmLaird, \bfnmN.\binitsN. (\byear1986). \btitleMeta-analysis in clinical trials. \bjournalControl. Clin. Trials \bvolume7 \bpages177–188. \bidissn=0197-2456, pii=0197-2456(86)90046-2, pmid=3802833 \bptokimsref \endbibitem

- [4] {barticle}[mr] \bauthor\bsnmEfron, \bfnmBradley\binitsB. &\bauthor\bsnmMorris, \bfnmCarl\binitsC. (\byear1973). \btitleStein’s estimation rule and its competitors – an empirical Bayes approach. \bjournalJ. Amer. Statist. Assoc. \bvolume68 \bpages117–130. \bidissn=0162-1459, mr=0388597 \bptokimsref \endbibitem

- [5] {barticle}[mr] \bauthor\bsnmHarville, \bfnmDavid A.\binitsD.A. (\byear1985). \btitleDecomposition of prediction error. \bjournalJ. Amer. Statist. Assoc. \bvolume80 \bpages132–138. \bidissn=0162-1459, mr=0786599 \bptokimsref \endbibitem

- [6] {barticle}[mr] \bauthor\bsnmJackson, \bfnmDan\binitsD., \bauthor\bsnmBowden, \bfnmJack\binitsJ. &\bauthor\bsnmBaker, \bfnmRose\binitsR. (\byear2010). \btitleHow does the DerSimonian and Laird procedure for random effects meta-analysis compare with its more efficient but harder to compute counterparts? \bjournalJ. Statist. Plann. Inference \bvolume140 \bpages961–970. \biddoi=10.1016/j.jspi.2009.09.017, issn=0378-3758, mr=2574658 \bptokimsref \endbibitem

- [7] {barticle}[mr] \bauthor\bsnmMaatta, \bfnmJon M.\binitsJ.M. &\bauthor\bsnmCasella, \bfnmGeorge\binitsG. (\byear1990). \btitleDevelopments in decision-theoretic variance estimation. \bjournalStatist. Sci. \bvolume5 \bpages90–120. \bnoteWith comments and a rejoinder by the authors. \bidissn=0883-4237, mr=1054858 \bptnotecheck related\bptokimsref \endbibitem

- [8] {barticle}[mr] \bauthor\bsnmMarchand, \bfnmÉric\binitsÉ. &\bauthor\bsnmStrawderman, \bfnmWilliam E.\binitsW.E. (\byear2005). \btitleOn improving on the minimum risk equivariant estimator of a scale parameter under a lower-bound constraint. \bjournalJ. Statist. Plann. Inference \bvolume134 \bpages90–101. \biddoi=10.1016/j.jspi.2004.04.001, issn=0378-3758, mr=2146087 \bptokimsref \endbibitem

- [9] {barticle}[mr] \bauthor\bsnmMarchand, \bfnmÉric\binitsÉ. &\bauthor\bsnmStrawderman, \bfnmWilliam E.\binitsW.E. (\byear2012). \btitleA unified minimax result for restricted parameter spaces. \bjournalBernoulli \bvolume18 \bpages635–643. \biddoi=10.3150/10-BEJ336, issn=1350-7265, mr=2922464 \bptokimsref \endbibitem

- [10] {bbook}[mr] \bauthor\bsnmMarshall, \bfnmAlbert W.\binitsA.W. &\bauthor\bsnmOlkin, \bfnmIngram\binitsI. (\byear1979). \btitleInequalities: Theory of Majorization and Its Applications. \bseriesMathematics in Science and Engineering \bvolume143. \blocationNew York: \bpublisherAcademic Press. \bidmr=0552278 \bptokimsref \endbibitem

- [11] {bincollection}[mr] \bauthor\bsnmMorris, \bfnmC. N.\binitsC.N. &\bauthor\bsnmNormand, \bfnmS. L.\binitsS.L. (\byear1992). \btitleHierarchical models for combining information and for meta-analyses. In \bbooktitleBayesian Statistics, Vol. 4 (Peñíscola, 1991) (\beditor\bfnmJ.M.\binitsJ.M. \bsnmBernardo, \beditor\bfnmJ.O.\binitsJ.O. \bsnmBerger, \beditor\bfnmA.P.\binitsA.P. \bsnmDawid &\beditor\bfnmA.F.M.\binitsA.F.M. \bsnmSmith, eds.) \bpages321–344. \blocationNew York: \bpublisherOxford Univ. Press. \bidmr=1380284 \bptokimsref \endbibitem

- [12] {barticle}[auto:STB—2013/12/09—07:59:19] \bauthor\bsnmPaule, \bfnmR. C.\binitsR.C. &\bauthor\bsnmMandel, \bfnmJ.\binitsJ. (\byear1982). \btitleConsensus values and weighting factors. \bjournalJ. Res. Natl. Bur. Stand. \bvolume87 \bpages377–385. \bptokimsref \endbibitem

- [13] {barticle}[auto:STB—2013/12/09—07:59:19] \bauthor\bsnmRukhin, \bfnmA. L.\binitsA.L. (\byear1995). \btitleAdmissibility: Survey of a concept in progress. \bjournalInt. Stat. Rev. \bvolume63 \bpages95–115. \bptokimsref \endbibitem

- [14] {barticle}[mr] \bauthor\bsnmRukhin, \bfnmAndrew L.\binitsA.L. (\byear2012). \btitleEstimating common mean and heterogeneity variance in two study case meta-analysis. \bjournalStatist. Probab. Lett. \bvolume82 \bpages1318–1325. \biddoi=10.1016/j.spl.2012.03.031, issn=0167-7152, mr=2929781 \bptokimsref \endbibitem

- [15] {barticle}[mr] \bauthor\bsnmRukhin, \bfnmAndrew L.\binitsA.L. (\byear2013). \btitleEstimating heterogeneity variance in meta-analysis. \bjournalJ. R. Stat. Soc. Ser. B. Stat. Methodol. \bvolume75 \bpages451–469. \biddoi=10.1111/j.1467-9868.2012.01047.x, issn=1369-7412, mr=3065475 \bptokimsref \endbibitem

- [16] {bmisc}[author] \bauthor\bsnmRukhin, \bfnmAndrew L.\binitsA.L. (\byear2014). \bhowpublishedSupplement to “Restricted likelihood representation and decision-theoretic aspects of meta-analysis.” DOI:\doiurl10.3150/13-BEJ543SUPP. \bptokimsref \endbibitem

- [17] {bbook}[mr] \bauthor\bsnmSearle, \bfnmShayle R.\binitsS.R., \bauthor\bsnmCasella, \bfnmGeorge\binitsG. &\bauthor\bsnmMcCulloch, \bfnmCharles E.\binitsC.E. (\byear1992). \btitleVariance Components. \bseriesWiley Series in Probability and Mathematical Statistics: Applied Probability and Statistics. \blocationNew York: \bpublisherWiley. \biddoi=10.1002/9780470316856, mr=1190470 \bptokimsref \endbibitem