Real-time covariance estimation for the local level model

Abstract

This paper develops on-line inference for the multivariate local level model, with the focus being placed on covariance estimation of the innovations. We assess the application of the inverse Wishart prior distribution in this context and find it too restrictive since the serial correlation structure of the observation and state innovations is forced to be the same. We generalize the inverse Wishart distribution to allow for a more convenient correlation structure, but still retaining approximate conjugacy. We prove some relevant results for the new distribution and we develop approximate Bayesian inference, which allows simultaneous forecasting of time series data and estimation of the covariance of the innovations of the model. We provide results on the steady state of the level of the time series, which are deployed to achieve computational savings. Using Monte Carlo experiments, we compare the proposed methodology with existing estimation procedures. An example with real data consisting of production data from an industrial process is given.

Some key words: multivariate time series, covariance estimation, adaptive estimation, dynamic linear models, multivariate control charts.

1 Introduction

Let be a vector process, generated from the state space model:

| (1) |

where is the conditional level of , is a scalar hyperparameter, and the innovation vectors and follow -variate Gaussian distributions and , for some covariance matrices and , and for some integer . It is assumed that the sequences and are individually and mutually uncorrelated and they are also uncorrelated with the initial state , which follows a -variate Gaussian distribution too. For the above model gives the popular local level model, known also as random walk plus noise model or as steady forecasting model, which is extensively covered in Harvey (1986, 1989) and in West and Harrison (1997). If lies inside the unit circle, but , then (1) can be interpreted as a vector autoregressive model (Lütkepohl, 2005) with common structure over the component time series. In this paper we focus on the local level model, but the choice may allow some small flexibility around it, for example considering nearly local level when .

Despite its simplicity, the local level model can be used to analyze real data sets in various settings and scenarios, as it has been pointed out by many authors, see e.g. Durbin (2004, p. 6). In the context of model (1) with , is referred to as the conditional level or simply level of , since and then is local as , where denotes expectation. The local level model has been used to analyze the volume of the river Nile (Pole et al., 1994, §7.1; Durbin and Koopman, 2001, §2.2.2), market research data for a drug development (West and Harrison, 1997, §2.3), temperature data for assessing global warming (Shumway and Stoffer, 2006, §6.1), and annual precipitation at Lake Superior (Petris et al., 2009, §3.2.1). A detailed account of the local level model in econometrics, including many examples, is given in Commandeur and Koopman (2007, Chapters 1-7). Furthermore, local level models play a significant role to financial econometrics as they form basic components for unit root tests (Kwiatkowski, 1992). Finally, as pointed out by Triantafyllopoulos (2006), model (1) is a generalization of the Shewhart-Deming model for quality control, and it can be deployed in the context of multivariate control charts for autocorrelated processes (Bersimis et al., 2007), where the aim is to signal deviations from the mean and the covariance matrix of these processes.

A central problem associated with inference of model (1), is the specification or estimation of the covariance matrices and . For the estimation of these matrices there are several algorithms based on direct likelihood maximization (Harvey, 1986, 1989) and in particular using analytical score functions (Shephard and Koopman, 1992). Iterative methods for indirect likelihood maximization are also available, e.g. Newton-Raphson algorithms (Shephard and Koopman, 1992; Shumway and Stoffer, 2006, §6.3) and expectation maximization (EM) algorithms (Dempster et al., 1977; Shumway and Stoffer, 1982; Koopman, 1993); Fahrmeir and Tutz (2001, §8.1.2) and Shumway and Stoffer (2006, §6.3) have detailed discussions of these algorithms with useful references and recursive versions of the EM algorithm is also possible for on-line application. Simulation based methods, such as Markov chain Monte Carlo (MCMC) (Carter and Kohn, 1994; Gamerman and Lopes, 2006) and sequential Monte Carlo methods (Doucet et al., 2001) are also available. Although in recent years the advance in computing power has resulted in sophisticated simulation based and iterative estimation procedures, such as those discussed in the above references, it is still desirable to develop inference that is not based on simulation or on iterative methods, in particular for enabling fast statistical analysis of high dimensional data and sequential model monitoring in real-time (Harrison and West, 1991). The need for real-time estimation has been pointed out in Cantarelis and Johnston (1982) and in many references in machine learning and signal processing, see e.g. Haykin (2001) and Malik (2006). Furthermore, MCMC and maximum likelihood based methods, as those mentioned above, are effectively designed for a “static” or in-sample application where a complete set of data is available and the interest is focused on smoothing, rather than on forecasting. Instead, our interest is centred on sequential or “dynamic” application, where each time we collect a new observation vector we update the estimates or predictions in an adaptive way. For the remainder of this paper we discuss approximate conjugate estimation procedures, but in section 4 we also consider the EM algorithm for comparison purposes.

Assuming that is proportional to in the sense that , for some scalar , learning for is possible either by adopting Bayesian methods, considering a Wishart prior for (West and Harrison, 1997), or by adopting maximum likelihood estimation procedures (Harvey, 1986; 1989). The above proportional structure of and can be seen as a matrix generalization of the proportionality in the univariate case that leads to the scale observational dynamic model (West and Harrison, 1997; Triantafyllopoulos and Harrison, 2008), but when it imposes the restrictive assumption that the correlation matrix of is equal to the correlation matrix of . This limitation can be understood by noting that the above model belongs to the relatively restricted class of “seemingly unrelated time series equations” (SUTSE) (Harvey, 1989, §8.2), which is a time series extension of the “seemingly unrelated regression equation models” (Zellner, 1962). In our opinion, efforts devoted to the estimation of the above models have been focused primarily on mathematical convenience, and the correlation structure problem mentioned above appears to have been overlooked.

The purpose of this paper is to develop an on-line estimation procedure for adaptive and fast estimation of and forecasting of . The adaptive estimation methods proposed in this paper, may allow for analysis of high dimensional data, although in this paper this is only briefly explored via Monte Carlo experiments. In order to achieve the above goal we propose the deterministic specification of as , where denotes the symmetric square root of and is a covariance matrix to be specified. In our development, is initially assumed known, but we propose an application of the Newton-Rapshon method for adaptive estimation of this matrix in real problems. We observe that when , where is the identity matrix, then (leading to being proportional to ), but when is not proportional to , then the correlation matrices of and are different. Thus we extend the SUTSE models of Harvey (1989, §8.2) and West and Harrison (1997, §16.4) to allow for a more general covariance setting. For estimation purposes, we deploy approximate Bayesian inference, by adopting a prior distribution for which leads to a generalization of the inverse Wishart distribution. We provide convergence results of the posterior covariance matrix of leading to the steady state of and this is used in the estimation algorithm in order to increase its computational speed.

The remaining of the paper is organized as follows. Section 2 generalizes the inverse Wishart distribution and discusses some properties of the new distribution. In section 3 we develop approximate Bayesian inference for model (1) and section 4 includes two illustrations, consisting of Monte Carlo experiments that compare and contrast the performance of our algorithms with existing methods in the literature and an example of monitoring a 5-dimensional process in quality control. Finally, section 5 gives concluding comments.

2 Generalized inverse Wishart distribution

Let denote that the matrix follows an inverse Wishart distribution with degrees of freedom and with parameter matrix . Given , we use the notation for the determinant of , for the trace of , and for the exponent of the scalar . The following theorem introduces a generalization of the inverse Wishart distribution.

Theorem 1.

Consider the random covariance matrix and denote with the symmetric square root of . Given covariance matrices and and a positive scalar , define so that follows an inverse Wishart distribution . Then the density function of is given by

where denotes the multivariate gamma function.

Proof.

From Olkin and Rubin (1964) the determinant of the Jacobian matrix of with respect to is , where are the eigenvalues of and are the eigenvalues of . We observe that if , then is an inverse Wishart distribution, since . The Jacobian does not depend on and so we can determine from the special case of . With , and and from the transformation we get

Since it must be and so .

Now, in the general case of a covariance matrix , we see

since . ∎

The distribution of the above theorem proposes a generalization of the inverse Wishart distribution, since if we have and if , we have . This is a new generalization of the inverse Wishart distribution, differing clearly from the generalizations of Dawid and Lauritzen (1993), Brown et al. (1994), Roverato (2002), and Carvalho and West (2007). In the following we refer to the distribution of Theorem 1 as generalized inverse Wishart distribution, and we write . The next result gives some expectations of the distribution.

Theorem 2.

Let for some known and . Then we have

-

(a)

; ;

-

(b)

,

where denotes expectation and .

Proof.

First we prove (a). From the proof of Theorem 1 we have that

and so

and . Proceeding

with (b) we note from the proof of Theorem 1 that for any

where is the normalizing constant of the distribution of . Then

where

and the range of makes sure that . The result follows by eliminating the factor in the fraction , and by noting that from well known properties of the multivariate gamma function we have

where denotes the gamma function. ∎

The following property reflects on the symmetry of and in the distribution.

Theorem 3.

If , for some known , and , then .

Proof of Theorem 3.

Suppose that . From the normalizing constant of the density of Theorem 1, we can exchange the roles of and . And from we have that . ∎

Next we show that the mode of a distribution can be obtained by the solution of a matrix equation. First we give the following lemma.

Lemma 1.

If is a real-valued symmetric matrix of variables and are symmetric matrices of constants, then

| (2) |

where and .

Proof.

Let and thus

Now let be the -th column vector of the identity matrix (a zero vector having one unit in its -th position). For we have

| (3) |

where denotes the row vector of .

Theorem 4.

The mode of satisfies the matrix equation

| (5) |

Furthermore, is unique, i.e. is a unimodal distribution.

Proof.

Now

Next we show that at the second partial derivative of is a negative definite matrix. Let and , where denotes the vec permutation operator of symmetric matrices. Also, let be the duplication matrix and be any left inverse of it and denote with the Kronecker product of two matrices. Then

since both and are positive definite matrices.

Some comments are in order.

-

1.

If , then is reduced to an inverted Wishart distribution with mode and this satisfies equation (5).

- 2.

-

3.

If is symmetric (i.e. if and commute), then . To prove this first we show that if and commute, then and commute too. Indeed, assume that , then and , which is a contradiction. Now define with and then substitute into (5), i.e.

Note that the cases (1) and (2) above, are embedded in (3).

-

4.

In the general case we can obtain the solution of (5) numerically, by considering it as a special case of generalized Sylvester matrix equations (Wu et al., 2008).

The next result proposes a way to obtain the unique solution of (5), avoiding numerical methods.

Theorem 5.

Proof.

For simplicity we write . Then equation (5) becomes , which by taking the vectorized operator in both sides, can be written as

| (6) |

With as in the theorem and by taking again the vectorized operator in both sides of (6) we have

Now we can see that the matrix is of full rank and so the solution of the above system is given by

as required. ∎

In order to find the mode using Theorem 5 we follow the next steps: first we calculate , then we extract the matrix from , then using the formula and rearranging again we find and finally by inverting this matrix we obtain .

However, the above method for the computation of the mode may not be efficient for high dimensional data. Even in low dimensions, as the time series problem we consider in the next section has a sequential application, if we want to use the above procedure for the determination of the mode or if we want to solve the matrix equation of Theorem 5 using numerical methods, we will have to perform these operations at each time . In our experience this is a heavy computational job, even for relatively short time series. In order to circumvent this difficulty we propose instead to use the estimator

| (7) |

which is motivated by noting that for cases (1)-(3) above, we have . Even when , we have , the approximation here refers to matrix similarity, meaning that the matrices and have the same determinant, the same trace, the same eigenvalues, and the same spectrum (see Theorem 21.3.1 of Harville, 1997, p. 525). Thus and can be thought of being close to each other and estimator (7) basically suggests considering the average of and . Moreover, a close look at and shows that the diagonal elements of and are the same and that in (7) the off-diagonal elements of are averages of the off-diagonal elements of and . When , and for large , the estimator is close to , which from (b) of Theorem 2 is equal to .

It is easy to verify that if and considering the partition

where , , are and , , are covariance matrices, then and , for . The verification of this is just by noting that and so that . From the latter it follows that and are independent. This result has the following interesting consequence. Suppose that are independent random covariance matrices, each following an inverse Wishart distribution , for some and some covariance matrix , with . Then the random matrix (the block diagonal matrix of ) follows the GIW distribution, , where , and . In words, the GIW distribution with the above block diagonal structure on and is generated from the superposition of independent inverse Wishart matrices. This gives an interpretation of the matrices and in GIW as well as it gives a useful model building approach when we wish to consider the superposition of local level models as in West and Harrison (1997, Chapter 6).

It is also easy to verify that if , then the density of is

This distribution generalizes the Wishart distribution; we will say that follows the generalized Wishart distribution with degrees of freedom, covariance matrices and , and we will write . We can observe that when or , the above density reduces to a Wishart density. Again our terminology and notation, should not cause any confusion with other generalizations of the Wishart distribution, proposed in the literature (Letac and Massam, 2004).

The next theorem is a generalization of the convolution of the Wishart and multivariate singular beta distributions (Uhlig, 1994; Díaz-García and Gutiérrez, 1997; Srivastava, 2003). For some integers , let the random matrix follow the multivariate singular beta distribution with and degrees of freedom, respectively, writing . The singularity of the beta distribution considered here is due to being smaller than , meaning that is singular (a similar argument can be stated for the singularity of , if ), and thus the density of does not exist under the Lebesgue measure in the space of the real-valued covariance matrices, but it does exist under the Steifel manifold. Under this consideration the density function of is obtained if we replace the determinant of (which is zero) by the product of the positive eigenvalues of ; for more details the reader is referred to the above references.

Theorem 6.

Let and be positive integers and let . Let and be independent, where and are known covariance matrices. Then

where denotes the upper triangular matrix of the Choleski decomposition of .

In order to prove this theorem, we prove the somewhat more general result in the following lemma.

Lemma 2.

Let , , with and , where , and are independent. Define , , and . Then are independent and , , , where .

Proof.

The proof mimics the proof of Uhlig (1994) for the Wishart case. Define and note that . From Theorem 1 and from Uhlig (1994), the Jacobian is . Then, the joint density function of can be written as

where , and are used. ∎

3 Bayesian inference

3.1 Estimation forward in time

In this section we consider estimation for model (1). The prior distributions of and are chosen to be Gaussian and generalized inverse Wishart respectively, i.e.

| (8) |

for some known parameters , , and . is the limit of , where is a covariance matrix. The next result states that the limit of (and hence the limit of ) exist and it provides the value of this limit as a function of and .

Theorem 7.

If , with , where is a positive definite matrix and considering the prior , for a known constant , it is

for and , for .

Before we prove this result we give some background on the limit of covariance matrices. Let denote that the matrix is non-negative definite, let denote that the matrix is positive definite and let denote that the matrices and satisfy . If , then (Horn and Johnson, 1999). The sequence of symmetric matrices is said to be monotonic and bounded if the scalar sequence is monotonic and bounded, for all real-valued vectors . If for all the matrix is a non-negative definite matrix, then the above definition implies that is bounded if there exist matrices and satisfying and monotonic if or , for any and . If is both monotonic and bounded, then it is convergent, since the sequence is also monotonic and bounded and so it is convergent. The following two lemmas are needed in order to prove the limit of Theorem 7.

Lemma 3.

If , with , where is a positive definite matrix and is a real number, then the sequence of positive matrices is convergent.

Proof.

First suppose that . Then , for all , and so , which of course is convergent.

Suppose now that . It suffices to prove that is bounded and monotonic. Clearly, and since and is positive definite , for all . Since , and so . For the monotonicity it suffices to prove that, if (equivalent ), then (equivalent ). From we have , since . With an analogous argument we have that, if , then , from which the monotonicity follows. ∎

Lemma 4.

Proof.

First we prove that if commutes with , then also commutes with . Indeed from we have that and then

which implies that and so and commute. Because , commutes with and so by induction it follows that the sequence of matrices commutes with . Since exists (Lemma 3) we have

and so commutes with . ∎

Theorem 7 generalizes relevant convergence results for the univariate random walk plus noise model (Anderson and Moore, 1979, p. 77; Harvey, 1989, p. 119). Following a similar argument as in Harvey (1989, p. 119), we can see that the speed of convergence is exponential; for a related discussion on the rate of convergence the reader is referred to Chan et al. (1984).

Let denote that the -dimensional random vector follows a multivariate Student distribution with degrees of freedom, mean and scale or spread matrix (Gupta and Nagar, 1999, Chapter 4). Let be the information set at time , comprising data up to time , for The next result gives an approximate Bayesian algorithm for the posterior distributions of and as well as for the one-step forecast distribution of .

Theorem 8.

Proof.

The proof is inductive in the distribution of . Assume that given the distribution of is .

From the Kalman filter, conditionally on , the one-step forecast density of is

where , and are as in the theorem.

Given the joint distribution of and is

| (9) | |||||

where

The one-step forecast density of is

and so , as required.

Now we derive the distribution of . Applying Bayes theorem we have

and from equation (9) we have

and , where is as in the theorem and the proportionality constant is , not depending on . Thus as required. Conditionally on , the distribution of follows directly from application of the Kalman filter and this provides the stated posterior distribution of . ∎

From Theorem 8, if , the posterior distribution of is reduced to an inverse Wishart, i.e. , where now is a variance. In this case Theorem 8 reduces to the well known variance learning of the random walk plus noise model of West and Harrison (1997). For the application of Theorem 8, one can use any estimator of , e.g. its mode ; here, following the motivation of in page 7, we have used for presentation purposes, and this is the estimator we have used and tested in Section 4.

3.2 Choice of hyperparameters

The hyperparameter can be chosen a priori, e.g. the application may require a local level model so that . The covariance matrix can be optimized by indirect maximization of the log-likelihood function, which using the prediction decomposition can be expressed as

| (10) | |||||

where and . Maximizing the above likelihood is equivalent of minimizing , given that is bounded. In this objective function to be minimized, is involved in via the recursion of . To simplify notation we consider . From Theorem 7, is obtained as a function of as , given that is non-singular. Thus we propose finding which maximizes the log-likelihood function, conditional on a value of ; this conditioning is proposed for simplification reasons. Instead of working with , we work with , because from the above relationship, we can calculate from . Even with these simplifications in place that minimizes , given can not be obtained by direct differentiation. Thus we use a Newton-Raphson method to achieve this.

We start by writing recurrently from Theorem 8 as

and then by ignoring the first term (which is justified if or if the eigenvalues of lie inside the unit circle), we obtain as

| (11) | |||||

Since or do not depend on , we proceed by estimating independently of , as if were proportional to . With this in place, using the chain rule of matrix differentiation (Harville, 2007, §15.7), we obtain the first partial derivative of (11) as

where , is the partial derivative of , , and is the element of the matrix derivative , for . For the calculation of we can see that , where , which, by defining as the zero -dimensional column vector having a unit in the th place, is equal to when and it is equal to when (Harville, 1997, p. 300). The recursion of follows by using the multiplicative rule of differentiation on the function and writing as a function of .

For the second derivative we have

From before we know and so . Thus

where from the recursion of we have

with . This completes the first and second partial derivatives of with respect to elements of . Then the Newton-Raphson method at each time and for iterations , approximates the true minimum by , using the formula

| (12) |

where and denotes the column stacking operator of an unrestricted matrix. Under some regularity conditions (Shumway and Stoffer, 2006, §6.3), the algorithm converges to the true minimum . Convergence is assumed at iteration , for which , for some small tolerance value , where denotes the Frobenius norm or distance; similar stoppage rules are discussed in Shumway and Stoffer (2006, §6.3). Note that typically not many iterations are needed for convergence, although this may depend on the specific application and on the dimension on the data; for the examples in the next section we have used .

An alternative approach is to consider indirect optimization of the conditional log-likelihood function using the Expectation Maximization (EM) algorithm. Some recursive type or on-line version of the EM algorithm is possible (not discussed further in this paper), but if the reader is more familiar with the typical off-line EM algorithm described in Koopman (1993) and Shumway and Stoffer (2006, §6.3), such an approach would prevent the application of real-time estimation.

Finally, we discuss the specification of using discount factors (West and Harrison, 1997, Chapter 6). According to this, we introduce (not necessarily distinct) discount factors , forming a discount matrix . The idea of this specification is that the prior covariance matrix is increased compared to , reflecting on the increased uncertainty or loss of information going from to , prior to observing . From the above, the expression of in Theorem 7 and by equating , we obtain the matrix equation . For (known as single discounting), the solution of this equation is , which is proportional to , and so, in this case, the GIW distribution reduces to an IW, as discussed in section 2. In the general case, it can be shown that the solution of the above matrix equation yields to be diagonal (but not necessarily proportional to ), i.e. . However, still there remains the problem of the specification of the discount factors. A commonly adopted approach, is to include the discount factors to the likelihood function, and to maximize it with respect to them, but this takes us again back to the indirect maximization procedure. In this paper, we favour the Newton-Raphson methodology as described above, but we do recognize its limitations, in particular regarding high dimensional data where the inversion of the Hessian matrix may be difficult or even impossible. In such cases a suitable approach involving discount factors may be favoured.

3.3 Time-varying covariance matrices

So far our discussion has been focused on situations where , the conditional covariance matrix of is time-invariant. However, in many situations, in particular in finance, this is not the case. For example consider that denotes the logarithm of the price of assets, or the logarithm of foreign exchange rates. It is evident that model (1) would not be an appropriate model to consider as , interpreted here as the volatility of , should be time-varying. We can thus extend model (1) by replacing by a time-varying and including a stochastic process to describing the evolution of . For the volatility covariance matrix , we propose a multiplicative stochastic law of its precision , i.e.

| (13) |

where , for a discount factor , and denotes the unique upper triangular matrix based on the Choleski decomposition of . Here is a random matrix following the multivariate singular beta distribution , where . The motivation behind the above evolution has been discussed in the literature, see e.g. Uhlig (1994, 1997). Here are chosen so that a random walk type evolution for is preserved, i.e. . This model is a generalization of Shephard’s local scale models (Shephard, 1994), which were suggested as an alternative to integrated GARCH modelling and which are exploiting the gamma/beta convolution proposed by Smith and Miller (1986).

If we combine Theorems 6 and 8 we can obtain the full estimation of the above model; in brief Theorem 6 is responsible for the prior estimation or prediction of , given data and Theorem 8 is responsible for the posterior estimation of given and of the estimation of and the prediction of . Next we give the result, the proof of which is trivial by the discussion above.

Theorem 9.

In the local level model (1) with a time-varying volatility covariance matrix and evolution (13), let the initial priors for and be specified as in equation (8). The one-step forecast and posterior distributions are approximately given, for each , as follows:

-

(a)

One-step forecast at time : and , where and , , are known at time .

- (b)

Some comments are in order. First note that if we set , then and with probability 1 and Theorem 9 is very similar to Theorem 8, the only difference being that the finite in Theorem 8 becomes in Theorem 9 and this means that the distribution of practically becomes a normal distribution under Theorem 9. Another point refers to the suitability of the evolution (13) and the related local level model. Multivariate stochastic volatility models that allow for and/or for to follow a vector or matrix autoregressive processes have been proposed in the literature (Chib et al., 2006; Philipov, 2006; Maasoumi and McAleer, 2006), but they have to rely on simulation-based methods, typically on Markov chain Monte Carlo or on particle filters, and they may not be suitable for real-time prediction of high dimensional data. Such a demand has recently become more and more prevalent as hedge funds and other investment boutiques require reliable automatic forecasting procedures that are suitable for algorithmic statistical arbitrage (Montana et al., 2009). In this direction the above algorithm offers an option, which extends a series of papers in this area, see e.g. Quintana and West (1987), Quintana et al. (2003), Soyer and Tanyeri (2006), Carvalho and West (2007) and references therein.

4 Illustrations

In this section we report on Monte Carlo experiments, in order to compare the performance of the proposed algorithm with existing estimation procedures, and also we present an application to multivariate control charting.

4.1 Monte Carlo experiments

We have generated realizations of observation and evolution covariance matrices and according to the following scheme: for each covariance matrix, first we generate independently correlations from a beta distribution and we multiply them by or generated by a bernoulli distribution with probability 1/2. Next we generate independently variances from a gamma distribution, and then we use the correlation decomposition of the covariance matrix, i.e. , where is the diagonal matrix with elements the square roots of the simulated variances and is the correlation matrix with off-diagonal elements the simulated correlations and with units in the main diagonal.

With this scheme in place we have performed a Monte Carlo study, over a set of 100 simulated -variate time series vectors according to the local level model (1) with and for three time series lengths . We have considered , covering from low to relatively high dimensional time series, and for their estimation we contrast the algorithm of the previous section (this model is referred to as GIW) with a local level model where the observation covariance matrix is estimated via an inverted Wishart distribution (this model is referred to as IW), a local level model where both of and are estimated using the EM algorithm of Shumway and Stoffer (1982) (this model is referred to as EM), and the local level model using the true simulated values of and (this model is referred to as Kalman). For the IW model was estimated by assuming an inverse Wishart prior and , where was estimated by direct maximum likelihood methods as in Harvey (1986, 1989). For all models we used the priors (8) with and , the latter of which reflects on a weakly informative or vague prior specification for . Also, for both the IW and GIW models we used the prior (8) for , the difference being that when is a covariance matrix (for the GIW) this prior becomes , while when is s scalar variance (for the IW), this prior reduces to ; for both cases and . For the estimation of the GIW, at each time , is estimated by the Newton-Raphson method of section 3.2.

Table 1 reports on the average mean of squared standardized one-step forecast errors (MSSE), which if the fit is perfect should be equal to the unit. Here, due to the high dimensions considered, we witness the quality of the estimation of and via the accuracy of the one-step forecast covariance matrix for each model. First of all we note that the values of the MSSE for the Kalman model are nearly equal to one and clearly this model is the benchmark or the gold standard here, but artificial as in practice we will not know these covariance matrices. We observe that the GIW produces consistent results, outperforming the IW, and producing MSSE close to the gold standard. In comparison with the EM we observe that at low dimensions and for small values of , the GIW is better, although as increases the performance of EM is improved and for the EM model produces marginally better results than the GIW. The improved performance of the EM model at is expected as it is well known that, under certain conditions, the EM estimators of and converge to their true values (Shumway and Stoffer, 2006, §6.3). But as increases we observe a deterioration in the performance of the EM model as compared to the GIW; in particular for and we still obtain reasonable performance with the GIW model, while both the EM and IW models clearly overestimate and . Here it should be noted that in our setup both the IW and the EM models are aimed at off-line application, since they need the whole data path for the computation of maximum likelihood estimates. For the EM algorithm we used the convergence criterion used in Shumway and Stoffer (2006, p. 345) that convergence is assumed when the likelihood function does not change by more than 0.001. However, this has resulted in slower algorithms, in particular at the higher dimensions considered here. For a single model, the algorithm of the GIW run in 1 minute and 31 seconds (for and ) and in 3 minutes and 19 seconds (for and ); the respective results for the other models were, for the IW 41 seconds (for and ) and 1 minute and 43 seconds (for and ), for the EM 1 minute and 47 seconds (for and ) and 3 minutes and 53 seconds (for and ), and for the Kalman 11 seconds (for and ) and 55 seconds (for and ). The experiments were run on an Intel(R) Celeron(R) M processor 1.60GHz, 504MB of RAM and the software we used was the freeware R, version 2.9.1, downloadable from http://www.r-project.org/.

| GIW | IW | EM | Kalman | ||

|---|---|---|---|---|---|

| 10 | 100 | 0.983 (0.002) | 0.963 (0.003) | 0.972 (0.050) | 0.999 (0.000) |

| 500 | 0.995 (0.002) | 0.975 (0.003) | 0.996 (0.003) | 0.998 (0.000) | |

| 1000 | 0.997 (0.000) | 0.988 (0.001) | 0.998 (0.001) | 1.001 (0.000) | |

| 50 | 100 | 0.969 (0.001) | 0.911 (0.001) | 1.060 (0.003) | 0.998 (0.001) |

| 500 | 0.985 (0.004) | 1.045 (0.004) | 1.066 (0.002) | 1.002 (0.000) | |

| 1000 | 1.011 (0.003) | 1.039 (0.001) | 1.009 (0.002) | 1.002 (0.000) | |

| 100 | 100 | 0.969 (0.001) | 0.899 (0.001) | 1.160 (0.002) | 0.995 (0.001) |

| 500 | 0.972 (0.003) | 1.074 (0.002) | 1.082 (0.001) | 1.003 (0.000) | |

| 1000 | 1.005 (0.001) | 1.032 (0.001) | 1.004 (0.003) | 1.001 (0.000) |

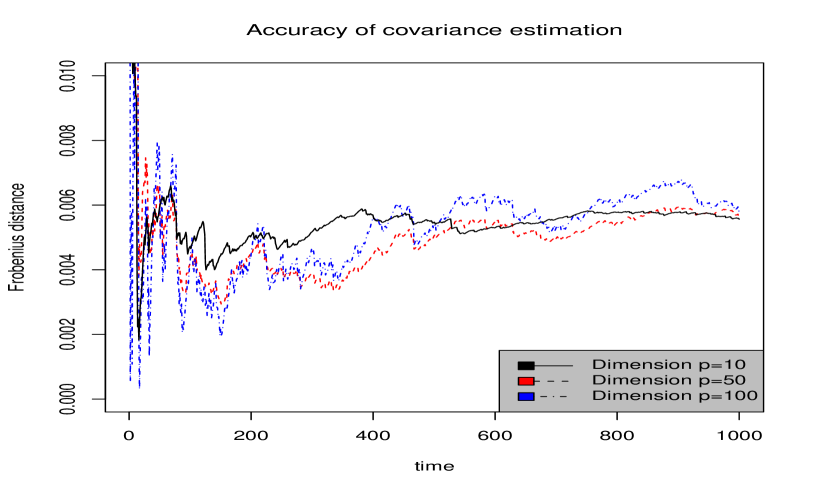

To mark the quality of the estimation for the GIW model, Figure 1 plots the Frobenius distance of the estimated at each time point () from its true simulated value, for . We note that in all three cases the algorithm achieves an upper bound 0.008 quite quickly. The distances of and are much more volatile in comparison to the distance of , but all eventually converge. The means of the three distances were 0.0050, 0.0053 and 0.0054 respectively and their respective variances were , and , respectively. The respective distances of the estimated follow a similar pattern to that of Figure 1 and their accurate estimation appears to be an important element of the successful estimation of .

4.2 Multivariate control charts

In this section we consider a multivariate control charting scheme for autocorrelated data (Bersimis et al., 2007). Typically multivariate control charts focus on the detection of signals of multivariate processes, which may exhibit out of control behaviour, defined as deviating from some prespecified target mean vector and a target covariance matrix. The Hotteling chart is the standard control chart as it is capable of detecting out of control signals of the joint effects of the variables of interest.

However, many authors have pointed out that in the presence of autocorrelation, this chart is a poor performer (Vargas, 2003). As a result over the past decade researchers have focused considerable efforts on to the development of control charts for multivariate time series data (Bersimis et al., 2007). Pan and Jarrett (2004) point out the importance of accurate estimation of the observation covariance matrix and they study the effects its miss-specification has in the detection of out of control signals. These authors suggest using the chart as above, after estimating the covariance matrix deploying some suitable time series method.

The multivariate local level model is a natural candidate model for the above situation, as it is a generalization of the popular Shewhart-Deming model, according to which the observed data are modelled as noisy versions of a constant level , or , where . This model is valid for serially uncorrelated data, but it is clearly not suitable for time series data. In this context, the motivation for the local level model is that the level of the time series at time , , follows a slow evolution described by a random walk. Using this model and considering an inverted Wishart distribution for , Triantafyllopoulos (2006) proposes that first the one-step forecast distribution is sequentially produced, then the logarithm of the Bayes factors of the current forecast distribution against a prespecified target distribution forms a new univariate non-Gaussian time series, which control chart is designed using the modified exponentially weighted moving average (EWMA) control chart. If the process is on target, then the log Bayes factor (West and Harrison, 1997, §11.4) will fluctuate around zero and the EWMA control chart will not signal significant deviations from this target. If, on the other hand, the EWMA signals out of control points, this will in turn signal deviations of the original process from its target. In the above reference, the target distribution is chosen to be a multivariate normal distribution, but, depending on experimentation and historical information, other distributions may be selected. As in Pan and Jarrett (2004) and in other studies, a critical stage in the application of this method, is that the estimate of and the forecast of are accurate, so that the fitted model is a good representation of the generating process.

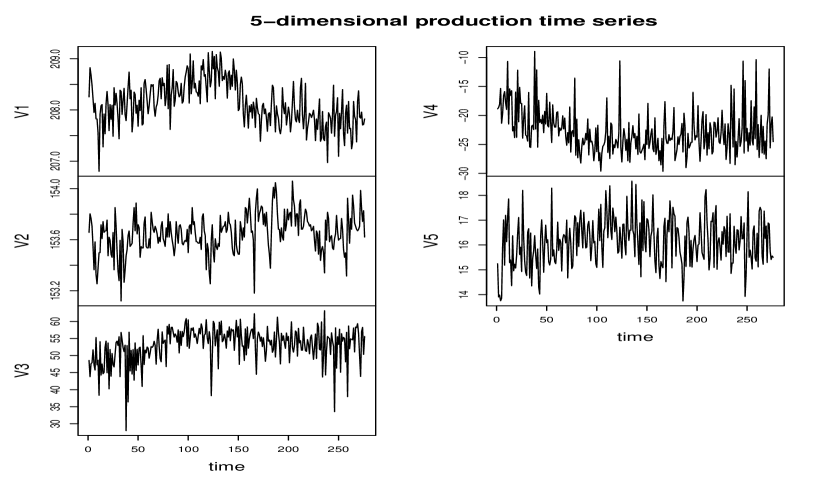

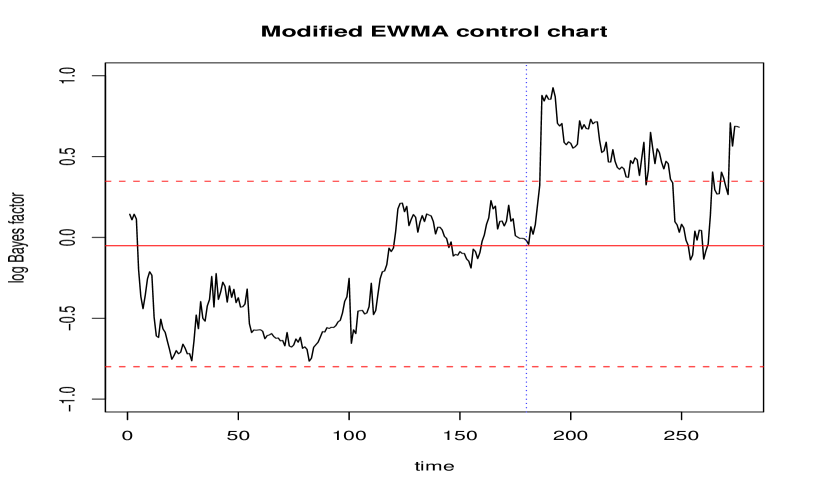

We consider data from an experiment of production of a plastic mould the quality of which is centered on the control of temperature and its variation. For this purpose five measurements of the temperature of the mould have been taken, for time points; for more details on the set up of this experiment the reader is referred to Pan and Jarrett (2004). From Figure 2, which is a plot of the data, we can argue that this data possesses a local level type evolution. We have applied the above control charting methodology using the local level model with the GIW distribution. For the model fit we note that the MSSE is , which marks a much improved performance compared to Pan and Jarrett (2004) and to Triantafyllopoulos (2006); similar improved results (not shown here) apply considering other measures of goodness of fit, e.g. the mean of squared forecast errors and the mean absolute deviation. For the design of the control chart, with a small smoothing factor equal to 0.05 we use the EWMA chart, which control limits are modified from its usual control limits, to accommodate for both the non-Gaussianity of the Bayes factor series and its autocorrelation. Figure 3 shows the EWMA control chart, from which we can see the improved behaviour: in Phase I where the model is applied and tested, we see that all EWMA points are within the control limits and in Phase II we see that the model signals a clear out of control behaviour. In contrast to the studies above, our model manages to avoid having out of control signals in Phase I, which reflects on the more accurate estimation of the observation covariance matrix and of the overall fit. In Phase II it shows a deterioration of the process, which is not signaled in Pan and Jarrett (2004) as very few out of control points are detected in that study. We also note that this deterioration can not be detected or suspected by either looking at the time series plot in Figure 2 or performing univariate control charts to each of the individual series. For this data set, applying the control chart after estimating using our method and Pan and Jarrett (2004) again favoured our proposal (results not shown here). Finally we report that the improved performance of our chart in Phase I is evident, by noting that the control limits are much tighter as compared to those in Triantafyllopoulos (2006) and thus the deployed fitted model here, is a more accurate representation of the data.

5 Conclusions

In this paper we propose on-line estimation for the multivariate local level model with the focus placed on the estimation of the covariance matrix of the innovations of the model. We criticize the application of the inverse Wishart prior distribution in this context as restrictive and often lacking empirical justification. Motivated from the conjugate model, we generalize the inverse Wishart distribution to account for wider application, but still manage to achieve approximate conjugacy, which is useful for real-time estimation. This approach results in fast recursive estimation, which resembles the Kalman filter, but allowing for covariance learning too. It is shown that our proposal delivers under Monte Carlo experiments and also in comparison with existing methods. An application of multivariate control charts is used to illustrate the proposed methodology. Future research efforts will be devoted on to the application of this methodology to high dimensional data.

Acknowledgements

I am grateful to two anonymous referees for providing useful comments on an earlier draft of the paper.

References

- [1] Anderson, B.D.O. and Moore, J.B. (1979) Optimal Filtering. Prentice Hall, Englewood Cliffs NJ.

- [2] Bersimis, S., Psarakis, S. and Panaretos, J. (2007) Multivariate statistical process control charts: an overview. Quality and Reliability Engineering International, 23, 517-543.

- [3] Brown, P.J., Le, N.D. and Zidek, J.V. (1994) Inference for a covariance matrix, in: P.R. Freeman and A.F.M. Smith, eds. Aspects of Uncertainty. Wiley, Chichester.

- [4] Cantarelis, N. and Johnston, F.R. (1982) On-line variance estimation for the steady state Bayesian forecasting model. Journal of Time Series Analysis, 3, 225-234.

- [5] Carter, C.K. and Kohn, R. (1994) On Gibbs sampling for state space models. Biometrika, 81, 541-553.

- [6] Carvalho, C.M. and West, M. (2007) Dynamic matrix-variate graphical models. Bayesian Analysis, 2, 69-98.

- [7] Chan, S.W., Goodwin, G.C. and Sin, K.S. (1984) Convergence properties of the Riccati difference equation in optimal filtering of nonstabilizable systems. IEEE Transactions on Automatic Control, 29, 10-18.

- [8] Chib, S., Nardari, F. and Shephard, N. (2006) Analysis of high dimensional multivariate stochastic volatility models. Journal of Econometrics, 134, 341-371.

- [9] Commandeur, J.J.F. and Koopman, S.J. (2007) An Introduction to State Space Time Series Analysis. Oxford University Press, Oxford.

- [10] Dawid, A.P. and Lauritzen, S.L. (1993) Hyper Markov laws in the statistical analysis of decomposable graphical models. Annals of Statistics, 21, 1272-1317.

- [11] Dempster, A.P., Laird, N.M. and Rubin, D.B. (1977) Maximum likelihood from incomplete data via the EM algorithm (with discussion). Journal of the Royal Statistical Society Series B, 39, 1-38.

- [12] Díaz-García, J.A. and Gutiérrez, J.R. (1997) Proof of the conjectures of H. Uhlig on the singular multivariate beta and the jacobian of a certain matrix transformation. Annals of Statistics, 25, 2018-2023.

- [13] Doucet, A., de Freitas, N. and Gordon, N.J. (2001) Sequential Monte Carlo Methods in Practice. Springer-Verlag, New York.

- [14] Durbin, J. and Koopman, S.J. (2001) Time Series Analysis by State Space Methods. Oxford University Press, Oxford.

- [15] Durbin, J. (2004) Introduction to state space time series analysis. In State Space and Unobserved Components Models: Theory and Applications, A. Harvey, S.J. Koopman and N. Shephard (Eds.), Cambridge University Press, Cambridge, 3-25.

- [16] Fahrmeir, L. and Tutz, G. (2001) Multivariate Statistical Modelling Based on Generalized Linear Models. 2nd edition, Springer, New York.

- [17] Franses, P.H. and van Dijk, D. (2000) Nonlinear Time Series Models in Empirical Finance. Cambridge University Press, Cambridge.

- [18] Frühwirth-Schnatter, S. (1994) Data augmentation and dynamic linear models. Journal of Time Series Analysis, 15, 183-202.

- [19] Gamerman, D. and Lopes, H.F. (2006) Markov Chain Monte Carlo: Stochastic Simulation for Bayesian Inference. 2nd edition, Chapman and Hall, London.

- [20] Gupta, A.K. and Nagar, D.K. (1999) Matrix Variate Distributions. Chapman and Hall, New York.

- [21] Harrison, P.J. and West, M. (1991) Dynamic linear model diagnostics. Biometrika, 78, 797-808.

- [22] Harvey, A.C. (1986) Analysis and generalisation of a multivariate exponential smoothing model. Management Science 32, 374-380.

- [23] Harvey, A.C. (1989) Forecasting Structural Time Series Models and the Kalman Filter. Cambridge University Press, Cambridge.

- [24] Harville, D.A. (1997) Matrix Algebra from a Statistician’s Perspective. Springer-Verlag, New-York.

- [25] Haykin, S. (2001) Adaptive Filter Theory. 4th edition, Prentice Hall.

- [26] Horn, R.A. and Johnson, C.R. (1999) Matrix Analysis. Cambridge University Press, Cambridge.

- [27] Koopman, S.J. (1993) Disturbance smoother for state space models. Biometrika, 80, 117-126.

- [28] Koopman, S.J. and Shephard, N. (1992) Exact score for time series models in state space form. Biometrika, 79, 823-826.

- [29] Kwiatkowski, D., Phillips, P.C.B., Schmidt, P. and Shin, Y. (1992) Testing the null hypothesis of stationarity against the alternative of a unit root: how sure we are that economic time series have a unit root? Journal of Econometrics, 44, 159-178.

- [30] Letac, G. and Massam, H. (2004) All invariant moments of the Wishart distribution. Scandinavian Journal of Statistics, 31, 295-318.

- [31] Lütkepohl, H. (2005) New Introduction to Multiple Time Series Analysis. Springer-Verlag, New-York.

- [32] Maasoumi, E. and McAleer, M. (2006) Multivariate stochastic volatility: An overview. Econometric Reviews, 25, 139-144.

- [33] Malik, M. (2006) State-space recursive least-squares with adaptive memory. Signal Processing, 86, 1365 1374.

- [34] Montana, G., Trianatafyllopoulos, K. and Tsagaris, T. (2009) Flexible least squares for temporal data mining and statistical arbitrage. Expert Systems with Applications, 36, 2819-2830.

- [35] Olkin, I. and Rubin, H. (1964) Multivariate beta distributions and independence properties of Wishart distribution. Annals of Mathematical Statistics, 35, 261-269.

- [36] Philipov, A. and Glickman, M.E. (2006) Multivariate stochastic volatility via Wishart processes. Journal of Business and Economic Statistics, 24, 313-328.

- [37] Pan, X. and Jarrett, J. (2004) Applying state space to SPC: monitoring multivariate time series. Journal of Applied Statistics, 31, 397-418.

- [38] Pole, A., West, M. and Harrison, P.J. (1994) Applied Bayesian Forecasting and Time Series Analysis. Chapman and Hall, New-York.

- [39] Petris, G., Petrone, S. and Campagnoli, P. (2009) Dynamic Linear Models with R. Springer, New-York.

- [40] Quintana, J.M. and West, M. (1987) An analysis of international exchange rates using multivariate DLMs. The Statistician, 36, 275-281.

- [41] Quintana, J.M., Lourdes, V., Aguilar, O. and Liu, J. (2003) Global gambling (with discussion). In Proceedings of Bayesian Statistics 7, J.M. Bernardo, M.J. Bayarri, J.O. Berger, A.P. Dawid, D. Heckerman, A.F.M. Smith and M. West (Eds.). Oxford University Press, Oxford, 349-367.

- [42] Roverato, A. (2002) Hyper inverse Wishart distribution for non-decomposable graphs and its application to Bayesian inference for Gaussian graphical models. Scandinavian Journal of Statistics, 29, 391- 411.

- [43] Shephard, N. (1994) Local scale models: state space alternatives to integrated GARCH processes. Journal of Econometrics, 60, 181-202.

- [44] Shumway, R.H. and Stoffer, D.S. (1982) An approach to time series smoothing and forecasting using the EM algorithm. Journal of Time Series Analysis, 3, 253-264.

- [45] Shumway, R.H. and Stoffer, D.S. (2006) Time Series Analysis and its Applications: With R Examples. 2nd edition. Springer, New-York.

- [46] Smith, R.L. and Miller, J.E. (1986) A non-Gaussian state space model and application to prediction of records. journal of the Royal Statistical Society Series B, 48, 79-88.

- [47] Soyer, R. and Tanyeri, K. (2006) Bayesian portfolio selection with multi-variate random variance models. European Journal of Operational Research, 171, 977 990.

- [48] Srivastava, M.S. (2003) Singular Wishart and multivariate beta distributions. Annals of Statistics, 31, 1537-1560.

- [49] Triantafyllopoulos, K. and Harrison, P.J. (2008) Posterior mean and variance approximation for regression and time series problems. Statistics, 42, 229-250.

- [50] Uhlig, H. (1994) On singular Wishart and singular multivariate beta distributions. Annals of Statistics, 22, 395-405.

- [51] Uhlig, H. (1997) Bayesian vector autoregressions with stochastic volatility. Econometrica, 65, 59-73.

- [52] Vargas, N.J.A. (2003) Robust estimation in multivariate control charts for individual observations. Journal of Quality Technology, 35, 367-376.

- [53] West, M. (1997) Time series decomposition. Biometrika, 84, 489-494.

- [54] West, M. and Harrison, P.J. (1997) Bayesian Forecasting and Dynamic Models. 2nd edition. Springer Verlag, New York.

- [55] Wu, A., Zhub, F., Duan, G., and Zhanga, Y. (2008) Solving the generalized Sylvester matrix equation via a Kronecker map. Applied Mathematics Letters, 21, 1069- 1073.

- [56] Zellner, A. (1962) An efficient method of estimating seamingly unrelated regression equations and tests for aggregation bias. Journal of the American Statistical Association, 57, 348-368.