Inference in nonstationary asymmetric GARCH models

Abstract

This paper considers the statistical inference of the class of asymmetric power-transformed models in presence of possible explosiveness. We study the explosive behavior of volatility when the strict stationarity condition is not met. This allows us to establish the asymptotic normality of the quasi-maximum likelihood estimator (QMLE) of the parameter, including the power but without the intercept, when strict stationarity does not hold. Two important issues can be tested in this framework: asymmetry and stationarity. The tests exploit the existence of a universal estimator of the asymptotic covariance matrix of the QMLE. By establishing the local asymptotic normality (LAN) property in this nonstationary framework, we can also study optimality issues.

doi:

10.1214/13-AOS1132keywords:

[class=AMS]keywords:

and

t2Supported by the Project ECONOM&RISK (ANR 2010 blanc 1804 03).

1 Introduction

Following more than twenty years of tremendous development of the theory of unit roots in linear time series models [see the seminal papers by Dickey and Fuller (1979) and Phillips and Perron (1988)], there has been, in the last decade, much interest in the statistical analysis of nonlinear time series models under nonstationarity assumptions; see, for example, Karlsen and Tjøstheim (2001), Karlsen, Myklebust and Tjøstheim (2007), Ling and Li (2008), Aue and Horváth (2011). In the framework of GARCH (Generalized Autoregressive Conditional Heteroscedasticity) models, Jensen and Rahbek (2004a, 2004b) were the first to establish an asymptotic theory for the quasi-maximum likelihood estimator (QMLE) of nonstationary , assuming that the intercept is fixed to an arbitrary value. Aknouche, Al-Eid and Hmeid (2011) and Aknouche and Al-Eid (2012) studied the properties of weighted least-squares estimators. Francq and Zakoïan (2012) established the asymptotic properties of the standard QMLE of the complete parameter vector: they showed that, while the intercept cannot be consistently estimated, the QMLE of the remaining parameters is consistent (in the weak sense at the frontier of the stationarity region, and in the strong sense outside) and asymptotically normal with or without strict stationarity. Asymptotic results for stationary had been established for the first time under mild conditions by Berkes, Horváth and Kokoszka (2003).

Financial series are well known to present conditional asymmetry features, in the sense that large negative returns tend to have more impact on future volatilities than large positive returns of the same magnitude. This stylized fact, known as the leverage effect, was first documented by Black (1976) and led to various generalizations of the GARCH models of the first generation; see among others, Glosten, Jaganathan and Runkle (1993), Rabemananjara and Zakoïan (1993), Higgins and Bera (1992), Li and Li (1996), Francq and Zakoïan (2010). Motivated by the Box–Cox transformation, Hwang and Kim (2004) introduced a power transformed ARCH model, and the GARCH extension was studied by Pan, Wang and Tong (2008). In this paper we consider an asymmetric power-transformed model defined, for a given positive constant , by

| (1) |

with initial values and , where , , , , and using the notation . In this model, is a sequence of independent and identically distributed (i.i.d.) variables such that

| (2) |

Most commonly used extensions of the standard GARCH of Engle (1982) and Bollerslev (1986) can be written in the form (1).

The first goal of the present paper is to derive a strict stationarity test in the framework of model (1). In this model, strict stationarity is characterized by the negativity of the so-called top Lyapunov exponent [see Bougerol and Picard (1992)] which depends on the parameters (except ) and the errors distribution. By deriving the asymptotic behavior of the QMLE of the top-Lyapunov exponent, under stationarity and nonstationarity, a strict stationarity test can be derived. The second goal of the paper is to propose a test for the symmetry assumption in model (1), namely . Existing tests, to our knowledge, rely on the stationarity assumption. Our aim is to derive a test which can be used without bothering about stationarity.

The rest of the paper is organized as follows. In Section 2, we study the convergence of the volatility to infinity, in a model encompassing (1), when stationarity does not hold. Section 3 is devoted to the asymptotic properties of the QMLE. In Section 4, we consider strict stationarity testing and asymmetry testing. In Section 5, the LAN property is established and used to derive the local asymptotic power of the proposed tests. Local alternative allowing for an arbitrary rate of convergence with respect to are considered. Optimality issues are discussed. Necessary and sufficient conditions on the noise density are derived for the tests to be uniformly locally asymptotically most powerful. Section 6 is devoted to the case where the power is unknown and is jointly estimated with the volatility coefficients. Proofs and technical lemmas are in Section 7. The possibility of extensions is discussed in Section 8. Due to space restrictions, several lemmas and proofs, along with a study of the finite sample performance of the stationarity and asymmetry tests and an empirical application, are included in the supplementary file [Francq and Zakoïan (2013)].

2 Explosivity in the augmented

In this section, we analyze the convergence of the volatility to infinity, for a class of augmented GARCH processes encompassing (1) and many models introduced in the literature; see Hörmann (2008). Given a sequence , let be defined by

| (3) |

where is a positive constant, is a given initial value and the functions and satisfy and , for some . When is assumed to be a white noise, is called an augmented GARCH process. We purposely use a different notation for in (3) and in (1) because, for the moment, we only assume that is stationary and ergodic. Define in the top Lyapunov exponent

The following proposition is an extension of results proven for the standard by Nelson (1990) and completed by Klüppelberg, Lindner and Maller (2004) and Francq and Zakoïan (2012).

Proposition 2.1

For the process satisfying (3), the following properties hold:

-

[(ii)]

-

(i)

When , a.s. at an exponential rate: for any ,

-

(ii)

When and is time reversible [i.e., for all the distributions of and are identical], the following convergences in probability hold as :

Moreover, if is a decreasing bijection from to , if [resp., and ], then

(4)

The main ideas of the proof are as follows. The a.s. convergence of to infinity in the case follows from the minoration , and the fact that the latter sum is strictly increasing, in average, as goes to infinity. The argument is in failure when , the expectation of the sum being equal to zero. The key argument in this case is that the sequence is increasing in distribution. Indeed, taking we have and under the reversibility assumption, and the same argument applies for any .

In the rest of the paper, these results will be applied with to model (1), for which the top Lyapunov exponent is given by

3 Asymptotic properties of the QMLE

We wish to estimate from observations , in the stationary and the explosive cases under mild assumption. Denote by the parameter and define the QMLE as any measurable solution of

where is a compact subset of containing the true value , and for [with initial values for and ]. The rescaled residuals are defined by where for .

Write and let .

3.1 Consistency and asymptotic normality of

The following theorem extends, to the nonstationary framework, results obtained for the stationary case [see Hamadeh and Zakoïan (2011) and the references therein], which we recall for convenience. We introduce the assumptions:

A1: The support of contains at least 3 points and is not concentrated on the positive or the negative line.

A2: When tends to infinity,

Note that A2, which is only required in the case , is obviously satisfied in the degenerate case when , a.s., since the expectation is then equal to .

To handle initial values we introduce the following notation. For any asymptotically stationary process , let provided this limit exists. Let also denote the interior of .

Theorem 3.1

Let (1)–(2) and A1 hold. Then the QMLE defined in (3) satisfies the following properties:

-

[(iii)]

-

(i)

Stationary case. When , and for all ,

If, in addition, and , we have

(6) where

(7) -

(ii)

Explosive case. When , if ,

If, in addition, , and ,

(8) as , where is a positive definite matrix.

-

(iii)

At the boundary of the stationarity region. When , if , and , for some ,

If, in addition, , , and A2 is satisfied, then (8) holds.

The key ideas of the proof can be summarized as follows. First, we note that can be equivalently defined as the minimizer of , where is a function of and the ratio . While the numerator and the denominator explode to infinity as increases, the ratio is close to a stationary process for sufficiently large. For instance, in the symmetric ARCH(1) case ( and ), we have , a.s. in the strictly explosive case (in probability in the case ). The situation is much more intricate when , but we can show that, when ,

uniformly on some compact set included in , where is a strictly stationary and ergodic process. The a.s. convergence is replaced by a convergence in the case . The consistency results are established by showing that the criterion in which is replaced by produces an estimator which is consistent to . Similar arguments are used to prove the asymptotic normality results, but we now show that

for some strictly stationary and ergodic process .

An explicit expression of is given in the supplementary file [Francq and Zakoïan (2013)]. To conclude the section, it can be noted that no asymptotically valid inference on can be done in the nonstationary case; see Propositions 2.1 and 3.1 in Francq and Zakoïan (2012), denoted hereafter FZ, for the standard model.

3.2 A universal estimator of the asymptotic variance of

In view of (6)–(7), when the asymptotic distribution of the QMLE of (the parameter without ) is given by

| (9) |

with

| (10) |

and . Letting

and defining and accordingly, it can be shown that

is a strongly consistent estimator of in the stationary case . The following result shows that this estimator also provides a consistent estimator of the asymptotic variance of in the nonstationary case .

Theorem 3.2

Let the assumptions required for the consistency results in Theorem 3.1 hold, assume and let , where .

-

[(iii)]

-

(i)

When , we have and a.s. as .

-

(ii)

When , we have and a.s.

-

(iii)

When , we have and, if A2 is satisfied, in probability.

In any case, is a consistent estimator of the asymptotic variance of the QMLE of .

It follows that asymptotically valid confidence intervals for the parameter can be constructed without knowing if the underlying process is stationary or not. This theorem also has interesting applications for testing problems, which we now consider.

4 Testing

In this section we consider testing stationarity and testing asymmetry.

4.1 Strict stationarity testing

Consider the strict stationarity testing problems

| (11) |

and

| (12) |

Let be the empirical estimator of , with for any ,

| (13) |

where . The following result shows that the asymptotic distribution of is particularly simple in the nonstationarity case.

Theorem 4.1

Let be the empirical variance of , for . Under the assumptions of Theorem 4.1, it can be shown that is a weakly consistent estimator of . The statistics

are thus asymptotically distributed when . For the testing problem (11) [resp., (12)], at the asymptotic significance level , this leads to consider the critical region

| (15) |

4.2 Asymmetry testing

It is of particular interest to test the existence of a leverage effect in stock market returns. In the framework of model (1), this testing problem is of the form

| (16) |

Consider the test statistic for symmetry

with . The following result is a direct consequence of (8), (9) and Theorem 3.1.

Corollary 4.1

We emphasize the fact that this test for symmetry does not require any stationarity assumption. The somewhat surprising output is that the usual Wald test, based on the asymptotic theory for the stationary case, also works in the nonstationary situation.222For instance, in ARMA models, Wald tests on the parameters are not the same in the stationary and nonstationary cases.

5 Asymptotic local powers

This section investigates the asymptotic behavior under local alternatives of the asymmetry test (17) and of the strict stationarity test (15). We first establish the LAN of the power-transformed GARCH model without imposing any stationarity constraint. This LAN property will be used to derive the asymptotic properties of our tests, but the result is of independent interest; see van der Vaart (1998) for a general reference on LAN and its applications, and see Drost and Klaassen (1997), Drost, Klaassen and Werker (1997) and Ling and McAleer (2003) for applications to GARCH and other stationary processes.

5.1 LAN without stationarity constraint

Assume that has a density which is positive everywhere, with third-order derivatives such that

| (18) |

and that, for some positive constants and ,

| (19) | |||||

| (20) |

These regularity conditions are satisfied for numerous distributions, in particular for the Gaussian distribution with , and entail the existence of the Fisher information for scale

Given the initial values and , the density of the observations satisfying (1) is given by . Around , let a sequence of local parameters of the form

| (21) |

where is a bounded sequence of . Without loss of generality, assume that is sufficiently large so that . Under the strict stationarity condition , Drost and Klaassen (1997) showed that, for standard GARCH, the log-likelihood ratio satisfies the LAN property

| (22) |

where under as . Note that the so-called central sequence is conditional on the initial values. In the stationary case, Lee and Taniguchi (2005) showed that the initial values have no influence on the LAN property. The following proposition shows that (22) holds regardless of .

5.2 Near-global alternatives with respect to

We now show that, in the nonstationary case, LAN continues to hold when the local alternative allows for an arbitrary rate of convergence with respect to . To this aim we assume that

| (24) |

where , is as in (21), and is a deterministic sequence converging to zero. The next result shows that, in the nonstationary case, (22) which was established under (21), continues to hold under the more general alternatives (24). For simplicity, take and .

Note that this Gaussian law is the distribution of the log-likelihood ratio in the statistical model of parameter , or equivalently in the statistical model . To interpret this result in terms of convergence of statistical experiments [see van der Vaart (1998) for details], assume that where and is a given sequence converging to zero as . Denoting by a subset of containing a neighborhood of , the so-called local experiments converge to the Gaussian experiment .

Interestingly, the parameter vanishes in the limiting experiment. Consequently, in the limit experiment there exists no test on the parameter (except of trivial power equal to the level). On the other hand, the limit of any converging sequence of power functions in the local experiments is a power function in the Gaussian limit experiment, by the asymptotic representation theorem. We can conclude that there exists no test with a nontrivial asymptotic power, for local alternatives on the parameter at the rate . Given that the rate of convergence of to zero is arbitrary, the LAN approach shows that no asymptotically valid inference can be made on the parameter .333This is in accordance with the observation that, at least in the explosive case, the Fisher information with respect to is bounded as increases. A proof is available from the authors.

5.3 Local asymptotic powers of the tests

The LAN property, with the help of Le Cam’s third lemma, allows us to easily compute local asymptotic powers of tests. In view of Theorem 4.1,

when is such that . For such that , we denote by the distribution of the observations when the parameter is . We should use the notation instead of because the parameter varies with , but we will avoid this heavy notation. Let

Local alternatives for the -test (resp., the -test) are obtained for such that (resp., ).

Proposition 5.3

We now compute the local asymptotic power of the asymmetry test defined by (17). We thus consider a sequence of local parameters of the form where and (with under a local alternative). We denote by the distribution of the observations under the assumption that the parameter is .

5.4 Optimality issues

We discuss, in this section, the optimality of the symmetry test defined in (17). Let be a parameter value corresponding to a symmetric GARCH. Assume that, at this point, . If , it suffices to replace by in the sequel. A sequence of local alternatives to this symmetric parameter is defined by where is such that . Relations (22)–(23) imply that

with , which is the distribution of the log-likelihood ratio in the statistical model of parameter . In other words, denoting by a subset of containing a neighborhood of , for any , the so-called local experiments converge to the Gaussian experiment .

The asymmetry test (16) corresponds to the test

in the limiting experiment. The uniformly most powerful unbiased (UMPU) test based on is the test of rejection region

This UMPU test has the power

| (26) |

with . A test of (16) whose level converges to , which is asymptotically unbiased, and whose power converges to the bound in (26) will be called asymptotically locally UMPU.

Proposition 5.5

A figure displaying the density (27) for different values of is in the supplementary file [Francq and Zakoïan (2013)]. Note that the Gaussian density is obtained for . The result was expected because the -test is based on the QMLE of , and the QMLE is obviously efficient in the Gaussian case. It can be shown that when the distribution of is of the form (27), the MLE does not depend on . The QMLE is then equal to the MLE, which makes obvious the “if part” of Proposition 5.5. The “only if” part of the proposition shows that there is necessarily an efficiency loss when the test is not based on the MLE of .

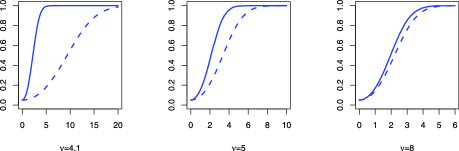

This point is illustrated by Figure 1, in which the local asymptotic power of the asymmetry test (in dotted lines) is compared to the optimal asymptotic power given by (26). In this figure, the noise is assumed to satisfy a Student distribution with degrees of freedom, standardized in such a way that . The parameters of the model under the null are , and , which corresponds to a nonstationary model with . In the figure, it can be seen that the local asymptotic power is far from the optimal power when is small, but, as expected, the discrepancy decreases as increases.

6 Estimation when the power is unknown

In this section, we consider the case where the power , now denoted , is unknown and is jointly estimated with . We rewrite the vector of parameters as , which is assumed to belong to a compact parameter space . The true parameters value is denoted by . A QMLE of is defined as any measurable solution of

| (28) |

where

| (29) |

for [with initial values for and ]. The rescaled residuals are defined by where for . For identifiability reasons, we need to slightly reinforce assumption A1 as follows.

A3: The support of contains at least three points of the same sign, and at least two points of opposite signs.

We also introduce the following technical assumption to handle the derivatives of with respect to the exponent .

A4: , and for some .

For brevity, we only present results for the nonstationary cases.

Theorem 6.1

Let (1)–(2) and A3 hold. Then the QMLE defined in (28) satisfies the following properties:

-

[(ii)]

-

(i)

Explosive case. When , if

If, in addition, , , , and A4 holds, then

(30) as , where is a positive definite matrix (see Lemma 3.1).

-

(ii)

At the boundary of the stationarity region. When , if , and , for some ,

If, in addition, , , and A2 and A4 are satisfied, then (30) holds.

The presence of parameter induces specific difficulties. It turns out that the derivative of the criterion with respect to involves the process . A strictly stationary approximation to this process can then be obtained, but in a more complicated way than for the other parameters. To save space, the proofs of this section are given in the supplementary file [Francq and Zakoïan (2013)].

7 Proofs and complementary results

Proof of Proposition 2.1 Writing and , we have, for all and ,

| (31) |

We begin by showing (i). Since all the random variables involved in (31) are positive, . For any constant , we thus have, a.s.

by the ergodic theorem. It follows that , and hence , tend to a.s. as . The second convergence is shown in just the same way, arguing that entails a.s. as .

To show (ii), first consider the case where . Note that, for all , the distribution of is equal to that of

| (32) |

Note that, contrary to , the sequence increases with . The Chung–Fuchs theorem applied to the random walk entails that a.s. It follows that as . We thus have for all , from which the first part of (ii) easily follows. To prove the first convergence of (4), note that the dominated convergence theorem entails

The second convergence is shown similarly. Now consider the case where the initial value is not equal to zero. It is clear from (31), with , that is an increasing function of . So the convergences to infinity obtained when , and the convergences in (4), hold a fortiori when .

7.1 Asymptotic behavior of the QMLE of

Define the -valued process

with the convention when . Let and .

Lemma 7.1

(i) When , for any the process is stationary and ergodic. Moreover, for any compact ,

Finally, for any it holds that a.s.

(ii) When , for any with , the process is stationary and ergodic. Moreover, for any compact ,

Assuming, with no generality loss, that , we have where and

| (33) |

Noting that

| (34) |

the rest of the proof follows from arguments similar to those used in the proof of Lemma A.1 in FZ. Therefore is it omitted.

Lemma 7.2

If , we have , a.s. if and only if .

Straightforward algebra shows that

| (35) |

Hence

It follows that a.s. if and only if

Thus if , takes at most two values of different signs, in contradiction with assumption A1. The conclusion follows.

Let , , , , , . Denote by any constant whose value is unimportant and can change throughout the proofs. Let be the compact set of the ’s such that .

Lemma 7.3

Suppose that . Then, for any ,

Let such that . If , since the sum is greater than its first term, we have

Iterating this method, we can write

where . It follows that, for any integer ,

Noting that and , we have for sufficiently small. The first result of the lemma is thus proven.

Similarly, we have for ,

and for and ,

More generally,

The conclusion follows by the same arguments as before.

Proof of the consistency results in cases (ii) and (iii) of Theorem 3.1 Note that , where . We have

where

and

It suffices to consider the case where is an arbitrary compact subset of , because by Lemma 7.1(i) a.s. if . We have by stationarity and ergodicity of , a.s.

because for . The inequality is strict except when a.s. By Lemma 7.2 we thus have , with equality only if .

By Lemma 7.3 we prove, as in FZ, that

| (36) |

when (resp., ) and are defined in Lemma 7.1, which completes the proof.

We now need to introduce new -valued processes. Let and

Lemma 7.4

Assume and . We have

where and . Moreover, is nonsingular.

Since , by the Cauchy root test, the processes and are stationary and ergodic. Still assuming , we have

Thus, using a direct extension of (34),

where the first inequality stands componentwise. Moreover, we have

where

For all , as because and . Since, in addition, , and

as by the dominated convergence theorem, converges to 0 in as . The same derivations hold true when is replaced by and . Therefore, and have moments of any order, and

| (37) |

in for any .

Using (37) and the ergodic theorem, we thus have, as ,

Moreover, it can be shown as in FZ that the Lindeberg condition is satisfied, allowing us to apply the Lindeberg central limit theorem for martingale differences; see Billingsley (1995), page 476.

Now we show that is nonsingular. Suppose there exists such that . Then we get , that is,

It follows that , a.s. where is a measurable function of the with . Because is independent of , this variable must be a.s. constant. In view of assumption A1, this entails and then . Therefore, is nonsingular.

Lemma 7.5

Let be an arbitrary compact subset of . Assume that . When we have, a.s.

When we have, for all ,

| (38) | |||||

| (39) |

This is similar to that of Lemma A.5. in FZ, therefore is it omitted.

Proof of the asymptotic normality in case (ii) of Theorem 3.1 An expansion of the criterion derivative gives

| (40) |

where is a matrix whose elements have the form

where is between and . Moreover, it can be shown that, for ,

| (41) |

The conclusion follows from the last rows of (40) and Lemma 7.4.

Proof of the asymptotic normality in case (iii) of Theorem 3.1 Note that (40) continues to hold. In view of (38)–(39), we have

To conclude, by the arguments used in case (ii), it suffices to show that

| (42) |

Noting that

| (43) |

and for large enough, and using the compactness of , we obtain

Hence, by Lemma 7.3 and Hölder’s inequality

for any . The same bound is obtained when is replaced by and . Moreover,

Hence

By assumption A2, the conclusion follows.

7.2 Stationarity test

Proof of Theorem 4.1 In the stationary case , standard arguments show that

| (44) |

with

where and . Moreover the QMLE satisfies

| (46) |

In view of (44), (7.2) and (46), we have

Note that

where . The Slutsky lemma and the central limit theorem for martingale differences thus entail

Now let . Noting that almost surely, we have

which entails and . It follows that

We also have , which completes the proof of the asymptotic distribution (14) in the case .

Now consider the case . Let be a sequence such that . By Proposition 2.1 (using assumption A2 when ), we have

when (resp., when ). It can be deduced that, under the same conditions, , and , which entails that (44) still holds. The previous arguments show that (7.2) holds with

The conclusion follows.

7.3 Asymptotic local powers

Proof of Proposition 5.1 The LAN of GARCH models has already been established in the stationary case; see Drost and Klaassen (1997), Lee and Taniguchi (2005). The nonstationary case will be studied under more general assumptions in the proof of Proposition 5.2.

Proof of Proposition 5.2 Let the functions

Introduce also the notation

A Taylor expansion of around yields

| (47) |

where is between and ,

and is a reminder which is displayed below. As in the proof of Lemma 7.4, it can be seen that

Using (18), it is easy to see that , and thus . The Lindeberg central limit theorem for martingale differences then shows that

| (49) |

Turning to the second term of (47) we first note that, similar to (37),

Moreover, integrations by parts show that, under (18), . It follows that . We thus have, using,

Next, it can be shown that, as ,

| (50) |

Finally, we show the convergence in probability to zero of

Noting that is constant and that converges to 0 in by Proposition 2.1, the first term in the right-hand side converges to zero in probability. The two other terms can be handled similarly. The conclusion then follows from (47)–(50).

Proof of Proposition 5.3 For simplicity, write instead of . In the proof of Theorem 4.1 we have seen that

By (22) and (7.3), it follows that under

where , . Le Cam’s third lemma [see, e.g., van der Vaart (1998), page 90] shows that

The conclusion easily follows.

Proof of Proposition 5.4 First consider the case . In the proof of (8) it has been shown that

Moreover

with . Note also that, since implies as , we have

| (51) |

It follows that under

Le Cam’s third lemma [see, e.g., van der Vaart (1998), page 90] shows that

We thus have shown that, in the case , is a regular estimator of , in the sense that converges to a distribution which does not depend on . More precisely

| (52) |

When , the same arguments show that is a regular estimator of

In the case , we thus have (52) with replaced by . Now, noting that , and by the same arguments, it follows that , under and more generally , under , where . The conclusion easily follows.

Proof of Proposition 5.5 Recall that we assume . The case is obtained similarly, replacing by . In view of Proposition 5.4 and (26), the -test is asymptotically locally UMPU if and only if , which is equivalent to . By Corollary 1 in Francq and Zakoïan (2006), the solutions of this equation are given by (27).

8 Concluding remarks

Our framework covers the most widely used GARCH models in financial applications. Strictly stationary models are a special case, but symmetry tests and asymptotically valid confidence intervals for the parameters (except the intercept) can be built without this assumption. Surprisingly, while the asymptotic covariance matrix of the estimators is sensitive to the stationarity of the underlying process, an estimator which converges to the appropriate covariance matrix in every situation can be built. Nevertheless, if the interest is on the whole parameter vector, including the intercept, it is important to know whether the observations come from a stationary process or not. To this aim we derived strict stationarity/nonstationarity tests which are very easy to implement.

Are our results extendable to higher-order models? It seems likely that for particular extensions involving univariate stochastic recurrence equations for the volatility, the asymptotic theory derived in this paper can also be established. One key problem, to show consistency, is to find stationary approximations to for . For an ARCH-type model of order it suffices to take . Consider standard symmetric GARCH models for simplicity. In the case, the problem can be circumvented because

can be approximated by a stationary process, in view of

To have a glimpse of the considerable difficulties encountered when the orders increase, consider a standard ARCH(2) model

We have, neglecting and for large enough and where

It is not difficult to show that the first stochastic recurrence equation admits a strictly stationary solution under mild assumptions on the density of , whatever the values of and . From this solution we deduce a strictly stationary solution to the second equation. We thus believe that, at least for the consistency, the ARCH(2) model is amenable to a treatment similar to that developed in this paper, but at the price of increasing technical difficulties. To summarize, the ratio is, for large , close to (i) a constant in the ARCH(1) case, (ii) an i.i.d. process in the case and (iii) the stationary solution of a nonlinear times series model in the ARCH(2) case. Whether or not this approach based on the resolution of nonlinear stochastic recurrence equations could be extended is left for further investigation.

Acknowledgments

We are most thankful to the Editor and to three referees for their constructive comments and suggestions. We are also grateful to the Agence Nationale de la Recherche (ANR).

Supplement to “Inference in nonstationary asymmetric GARCH models.” \slink[doi]10.1214/13-AOS1132SUPP \sdatatype.pdf \sfilenameaos1132_supp.pdf \sdescriptionThe supplementary file contains an illustration concerning the optimality of the asymmetry test, a Monte Carlo study of finite sample performance, an application to real time series, an explicit expression for the matrix in Theorem 3.1, the proofs of Theorems 3.2 and 6.1.

References

- Aknouche, Al-Eid and Hmeid (2011) {barticle}[mr] \bauthor\bsnmAknouche, \bfnmAbdelhakim\binitsA., \bauthor\bsnmAl-Eid, \bfnmEid M.\binitsE. M. and \bauthor\bsnmHmeid, \bfnmAboubakry M.\binitsA. M. (\byear2011). \btitleOffline and online weighted least squares estimation of nonstationary power processes. \bjournalStatist. Probab. Lett. \bvolume81 \bpages1535–1540. \biddoi=10.1016/j.spl.2011.05.002, issn=0167-7152, mr=2818665 \bptokimsref \endbibitem

- Aknouche and Al-Eid (2012) {barticle}[mr] \bauthor\bsnmAknouche, \bfnmAbdelhakim\binitsA. and \bauthor\bsnmAl-Eid, \bfnmEid\binitsE. (\byear2012). \btitleAsymptotic inference of unstable periodic ARCH processes. \bjournalStat. Inference Stoch. Process. \bvolume15 \bpages61–79. \biddoi=10.1007/s11203-011-9063-1, issn=1387-0874, mr=2892588 \bptokimsref \endbibitem

- Aue and Horváth (2011) {barticle}[mr] \bauthor\bsnmAue, \bfnmAlexander\binitsA. and \bauthor\bsnmHorváth, \bfnmLajos\binitsL. (\byear2011). \btitleQuasi-likelihood estimation in stationary and nonstationary autoregressive models with random coefficients. \bjournalStatist. Sinica \bvolume21 \bpages973–999. \bidissn=1017-0405, mr=2817009 \bptokimsref \endbibitem

- Berkes, Horváth and Kokoszka (2003) {barticle}[mr] \bauthor\bsnmBerkes, \bfnmIstván\binitsI., \bauthor\bsnmHorváth, \bfnmLajos\binitsL. and \bauthor\bsnmKokoszka, \bfnmPiotr\binitsP. (\byear2003). \btitleGARCH processes: Structure and estimation. \bjournalBernoulli \bvolume9 \bpages201–227. \biddoi=10.3150/bj/1068128975, issn=1350-7265, mr=1997027 \bptokimsref \endbibitem

- Billingsley (1995) {bbook}[mr] \bauthor\bsnmBillingsley, \bfnmPatrick\binitsP. (\byear1995). \btitleProbability and Measure. \bpublisherWiley, \blocationNew York. \bptokimsref \endbibitem

- Black (1976) {binproceedings}[auto:STB—2013/06/05—13:45:01] \bauthor\bsnmBlack, \bfnmF.\binitsF. (\byear1976). \btitleStudies of stock price volatility changes. In \bbooktitleProceedings from the American Statistical Association, Business and Economic Statistics Section \bpages177–181. \bpublisherAmer. Statist. Assoc., \blocationAlexandria, VA. \bptokimsref \endbibitem

- Bollerslev (1986) {barticle}[mr] \bauthor\bsnmBollerslev, \bfnmTim\binitsT. (\byear1986). \btitleGeneralized autoregressive conditional heteroskedasticity. \bjournalJ. Econometrics \bvolume31 \bpages307–327. \biddoi=10.1016/0304-4076(86)90063-1, issn=0304-4076, mr=0853051 \bptokimsref \endbibitem

- Bougerol and Picard (1992) {barticle}[mr] \bauthor\bsnmBougerol, \bfnmPhilippe\binitsP. and \bauthor\bsnmPicard, \bfnmNico\binitsN. (\byear1992). \btitleStrict stationarity of generalized autoregressive processes. \bjournalAnn. Probab. \bvolume20 \bpages1714–1730. \bidissn=0091-1798, mr=1188039 \bptokimsref \endbibitem

- Dickey and Fuller (1979) {barticle}[mr] \bauthor\bsnmDickey, \bfnmDavid A.\binitsD. A. and \bauthor\bsnmFuller, \bfnmWayne A.\binitsW. A. (\byear1979). \btitleDistribution of the estimators for autoregressive time series with a unit root. \bjournalJ. Amer. Statist. Assoc. \bvolume74 \bpages427–431. \bidissn=0003-1291, mr=0548036 \bptokimsref \endbibitem

- Drost and Klaassen (1997) {barticle}[mr] \bauthor\bsnmDrost, \bfnmFeike C.\binitsF. C. and \bauthor\bsnmKlaassen, \bfnmChris A. J.\binitsC. A. J. (\byear1997). \btitleEfficient estimation in semiparametric GARCH models. \bjournalJ. Econometrics \bvolume81 \bpages193–221. \biddoi=10.1016/S0304-4076(97)00042-0, issn=0304-4076, mr=1484585 \bptokimsref \endbibitem

- Drost, Klaassen and Werker (1997) {barticle}[mr] \bauthor\bsnmDrost, \bfnmFeike C.\binitsF. C., \bauthor\bsnmKlaassen, \bfnmChris A. J.\binitsC. A. J. and \bauthor\bsnmWerker, \bfnmBas J. M.\binitsB. J. M. (\byear1997). \btitleAdaptive estimation in time-series models. \bjournalAnn. Statist. \bvolume25 \bpages786–817. \biddoi=10.1214/aos/1031833674, issn=0090-5364, mr=1439324 \bptokimsref \endbibitem

- Engle (1982) {barticle}[mr] \bauthor\bsnmEngle, \bfnmRobert F.\binitsR. F. (\byear1982). \btitleAutoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. \bjournalEconometrica \bvolume50 \bpages987–1007. \biddoi=10.2307/1912773, issn=0012-9682, mr=0666121 \bptokimsref \endbibitem

- Francq and Zakoïan (2006) {bincollection}[mr] \bauthor\bsnmFrancq, \bfnmChristian\binitsC. and \bauthor\bsnmZakoïan, \bfnmJean-Michel\binitsJ.-M. (\byear2006). \btitleOn efficient inference in GARCH processes. In \bbooktitleDependence in Probability and Statistics (\beditorP. Bertail, \beditorP. Doukhan and \beditorP. Soulier, eds.). \bseriesLecture Notes in Statistics \bvolume187 \bpages305–327. \bpublisherSpringer, \blocationNew York. \biddoi=10.1007/0-387-36062-X_14, mr=2283261 \bptokimsref \endbibitem

- Francq and Zakoïan (2010) {bbook}[auto:STB—2013/06/05—13:45:01] \bauthor\bsnmFrancq, \bfnmC.\binitsC. and \bauthor\bsnmZakoïan, \bfnmJ. M.\binitsJ. M. (\byear2010). \btitleGARCH Models: Structure, Statistical Inference and Financial Applications. \bpublisherWiley, \blocationChichester. \bptokimsref \endbibitem

- Francq and Zakoïan (2012) {barticle}[mr] \bauthor\bsnmFrancq, \bfnmChristian\binitsC. and \bauthor\bsnmZakoïan, \bfnmJean-Michel\binitsJ.-M. (\byear2012). \btitleStrict stationarity testing and estimation of explosive and stationary generalized autoregressive conditional heteroscedasticity models. \bjournalEconometrica \bvolume80 \bpages821–861. \biddoi=10.3982/ECTA9405, issn=0012-9682, mr=2951950 \bptokimsref \endbibitem

- Francq and Zakoïan (2013) {bmisc}[auto:STB—2013/06/05—13:45:01] \bauthor\bsnmFrancq, \bfnmC.\binitsC. and \bauthor\bsnmZakoïan, \bfnmJ. M.\binitsJ. M. (\byear2013). \bhowpublishedSupplement to “Inference in nonstationary asymmetric GARCH models.” DOI:\doiurl10.1214/13-AOS1132SUPP. \bptokimsref \endbibitem

- Glosten, Jaganathan and Runkle (1993) {barticle}[auto:STB—2013/06/05—13:45:01] \bauthor\bsnmGlosten, \bfnmL. R.\binitsL. R., \bauthor\bsnmJaganathan, \bfnmR.\binitsR. and \bauthor\bsnmRunkle, \bfnmD.\binitsD. (\byear1993). \btitleOn the relation between the expected values and the volatility of the nominal excess return on stocks. \bjournalJ. Finance \bvolume48 \bpages1779–1801. \bptokimsref \endbibitem

- Hamadeh and Zakoïan (2011) {barticle}[mr] \bauthor\bsnmHamadeh, \bfnmTawfik\binitsT. and \bauthor\bsnmZakoïan, \bfnmJean-Michel\binitsJ.-M. (\byear2011). \btitleAsymptotic properties of LS and QML estimators for a class of nonlinear GARCH processes. \bjournalJ. Statist. Plann. Inference \bvolume141 \bpages488–507. \biddoi=10.1016/j.jspi.2010.06.026, issn=0378-3758, mr=2719513 \bptokimsref \endbibitem

- Higgins and Bera (1992) {barticle}[auto:STB—2013/06/05—13:45:01] \bauthor\bsnmHiggins, \bfnmM. L.\binitsM. L. and \bauthor\bsnmBera, \bfnmA. K.\binitsA. K. (\byear1992). \btitleA class of nonlinear ARCH models. \bjournalInternat. Econom. Rev. \bvolume33 \bpages137–158. \bptokimsref \endbibitem

- Hörmann (2008) {barticle}[mr] \bauthor\bsnmHörmann, \bfnmSiegfried\binitsS. (\byear2008). \btitleAugmented GARCH sequences: Dependence structure and asymptotics. \bjournalBernoulli \bvolume14 \bpages543–561. \biddoi=10.3150/07-BEJ120, issn=1350-7265, mr=2544101 \bptokimsref \endbibitem

- Hwang and Kim (2004) {barticle}[mr] \bauthor\bsnmHwang, \bfnmS. Y.\binitsS. Y. and \bauthor\bsnmKim, \bfnmTae Yoon\binitsT. Y. (\byear2004). \btitlePower transformation and threshold modeling for ARCH innovations with applications to tests for ARCH structure. \bjournalStochastic Process. Appl. \bvolume110 \bpages295–314. \biddoi=10.1016/j.spa.2003.11.001, issn=0304-4149, mr=2040970 \bptokimsref \endbibitem

- Jensen and Rahbek (2004a) {barticle}[mr] \bauthor\bsnmJensen, \bfnmSøren Tolver\binitsS. T. and \bauthor\bsnmRahbek, \bfnmAnders\binitsA. (\byear2004a). \btitleAsymptotic normality of the QMLE estimator of ARCH in the nonstationary case. \bjournalEconometrica \bvolume72 \bpages641–646. \biddoi=10.1111/j.1468-0262.2004.00504.x, issn=0012-9682, mr=2036735 \bptokimsref \endbibitem

- Jensen and Rahbek (2004b) {barticle}[mr] \bauthor\bsnmJensen, \bfnmSøren Tolver\binitsS. T. and \bauthor\bsnmRahbek, \bfnmAnders\binitsA. (\byear2004b). \btitleAsymptotic inference for nonstationary GARCH. \bjournalEconometric Theory \bvolume20 \bpages1203–1226. \biddoi=10.1017/S0266466604206065, issn=0266-4666, mr=2101955 \bptokimsref \endbibitem

- Karlsen, Myklebust and Tjøstheim (2007) {barticle}[mr] \bauthor\bsnmKarlsen, \bfnmHans Arnfinn\binitsH. A., \bauthor\bsnmMyklebust, \bfnmTerje\binitsT. and \bauthor\bsnmTjøstheim, \bfnmDag\binitsD. (\byear2007). \btitleNonparametric estimation in a nonlinear cointegration type model. \bjournalAnn. Statist. \bvolume35 \bpages252–299. \biddoi=10.1214/009053606000001181, issn=0090-5364, mr=2332276 \bptokimsref \endbibitem

- Karlsen and Tjøstheim (2001) {barticle}[mr] \bauthor\bsnmKarlsen, \bfnmHans Arnfinn\binitsH. A. and \bauthor\bsnmTjøstheim, \bfnmDag\binitsD. (\byear2001). \btitleNonparametric estimation in null recurrent time series. \bjournalAnn. Statist. \bvolume29 \bpages372–416. \biddoi=10.1214/aos/1009210546, issn=0090-5364, mr=1863963 \bptokimsref \endbibitem

- Klüppelberg, Lindner and Maller (2004) {barticle}[mr] \bauthor\bsnmKlüppelberg, \bfnmClaudia\binitsC., \bauthor\bsnmLindner, \bfnmAlexander\binitsA. and \bauthor\bsnmMaller, \bfnmRoss\binitsR. (\byear2004). \btitleA continuous-time GARCH process driven by a Lévy process: Stationarity and second-order behaviour. \bjournalJ. Appl. Probab. \bvolume41 \bpages601–622. \bidissn=0021-9002, mr=2074811 \bptokimsref \endbibitem

- Lee and Taniguchi (2005) {barticle}[mr] \bauthor\bsnmLee, \bfnmSangyeol\binitsS. and \bauthor\bsnmTaniguchi, \bfnmMasanobu\binitsM. (\byear2005). \btitleAsymptotic theory for ARCH-SM models: LAN and residual empirical processes. \bjournalStatist. Sinica \bvolume15 \bpages215–234. \bidissn=1017-0405, mr=2125729 \bptokimsref \endbibitem

- Li and Li (1996) {barticle}[auto:STB—2013/06/05—13:45:01] \bauthor\bsnmLi, \bfnmC. W.\binitsC. W. and \bauthor\bsnmLi, \bfnmW. K.\binitsW. K. (\byear1996). \btitleOn a double-threshold autoregressive heteroscedastic time series model. \bjournalJ. Appl. Econometrics \bvolume11 \bpages253–274. \bptokimsref \endbibitem

- Ling and Li (2008) {barticle}[mr] \bauthor\bsnmLing, \bfnmShiqing\binitsS. and \bauthor\bsnmLi, \bfnmDong\binitsD. (\byear2008). \btitleAsymptotic inference for a nonstationary double model. \bjournalBiometrika \bvolume95 \bpages257–263. \biddoi=10.1093/biomet/asm084, issn=0006-3444, mr=2409729 \bptokimsref \endbibitem

- Ling and McAleer (2003) {barticle}[mr] \bauthor\bsnmLing, \bfnmShiqing\binitsS. and \bauthor\bsnmMcAleer, \bfnmMichael\binitsM. (\byear2003). \btitleOn adaptive estimation in nonstationary ARMA models with GARCH errors. \bjournalAnn. Statist. \bvolume31 \bpages642–674. \biddoi=10.1214/aos/1051027884, issn=0090-5364, mr=1983545 \bptokimsref \endbibitem

- Nelson (1990) {barticle}[mr] \bauthor\bsnmNelson, \bfnmDaniel B.\binitsD. B. (\byear1990). \btitleStationarity and persistence in the GARCH model. \bjournalEconometric Theory \bvolume6 \bpages318–334. \biddoi=10.1017/S0266466600005296, issn=0266-4666, mr=1085577 \bptokimsref \endbibitem

- Pan, Wang and Tong (2008) {barticle}[mr] \bauthor\bsnmPan, \bfnmJiazhu\binitsJ., \bauthor\bsnmWang, \bfnmHui\binitsH. and \bauthor\bsnmTong, \bfnmHowell\binitsH. (\byear2008). \btitleEstimation and tests for power-transformed and threshold GARCH models. \bjournalJ. Econometrics \bvolume142 \bpages352–378. \biddoi=10.1016/j.jeconom.2007.06.004, issn=0304-4076, mr=2408740 \bptokimsref \endbibitem

- Phillips and Perron (1988) {barticle}[mr] \bauthor\bsnmPhillips, \bfnmPeter C. B.\binitsP. C. B. and \bauthor\bsnmPerron, \bfnmPierre\binitsP. (\byear1988). \btitleTesting for a unit root in time series regression. \bjournalBiometrika \bvolume75 \bpages335–346. \biddoi=10.1093/biomet/75.2.335, issn=0006-3444, mr=0946054 \bptokimsref \endbibitem

- Rabemananjara and Zakoïan (1993) {barticle}[auto:STB—2013/06/05—13:45:01] \bauthor\bsnmRabemananjara, \bfnmR.\binitsR. and \bauthor\bsnmZakoïan, \bfnmJ. M.\binitsJ. M. (\byear1993). \btitleThreshold ARCH models and asymmetries in volatility. \bjournalJ. Appl. Econometrics \bvolume8 \bpages31–49. \bptokimsref \endbibitem

- van der Vaart (1998) {bbook}[mr] \bauthor\bparticlevan der \bsnmVaart, \bfnmA. W.\binitsA. W. (\byear1998). \btitleAsymptotic Statistics. \bseriesCambridge Series in Statistical and Probabilistic Mathematics \bvolume3. \bpublisherCambridge Univ. Press, \blocationCambridge. \bidmr=1652247 \bptokimsref \endbibitem