Fluctuation of similarity (FLUS) to detect transitions between distinct dynamical regimes in short time series

Abstract

Recently a method which employs computing of fluctuations in a measure of nonlinear similarity based on local recurrence properties in a univariate time series, was introduced to identify distinct dynamical regimes and transitions between them in a short time series N.Malik et al. (2012). Here we present the details of the analytical relationships between the newly introduced measure and the well known concepts of attractor dimensions and Lyapunov exponents. We show that the new measure has linear dependence on the effective dimension of the attractor and it measures the variations in the sum of the Lyapunov spectrum. To illustrate the practical usefulness of the method, we employ it to identify various types of dynamical transitions in different nonlinear models. Also, we present testbed examples for the new method’s robustness against the presence of noise and missing values in the time series. Furthermore, we use this method to analyze time series from the field of social dynamics, where we present an analysis of the US crime record’s time series from the year 1975 to 1993. Using this method, we have found that dynamical complexity in robberies was influenced by the unemployment rate till late 1980’s. We have also observed a dynamical transition in homicide and robbery rates in the late 1980’s and early 1990’s, leading to increase in the dynamical complexity of these rates.

pacs:

92.70.Gt, 05.45.tp, 92.30.BcI Introduction

One of the central challenges in nonlinear time series analysis has been to develop methodologies to identify and predict dynamical transitions, i.e., time points where the dynamics show a qualitative change N.Malik et al. (2012); Marwan et al. (2007); Kantz and Schreiber (2004); Small (2005); Abarbanel (1996); Schreiber (1997); Donges et al. (2011a); Livina and Lenton (2007); Donges et al. (2011b); Marwan et al. (2009); Lenton et al. (2008); Schütz and Holschneider (2011). Application of such methods is widespread in a variety of areas of science and society Scheffer (2009). For instance, in medical sciences such approaches could be useful in identifying pathological activities of vital organs such as the heart and the brain from ECG and EEG data sets Lehnertz and Elger (1998); Venegas et al. (2005); P.E.McSharry et al. (2003). Similarly, in earth sciences one can use these methods to identify tipping elements from modern and paleoclimate data sets Lenton et al. (2008); Ashwin et al. (2012); Marwan et al. (2007); Donges et al. (2011a, b); Marwan et al. (2009). Also, in the analysis of financial data these methods can be used to better comprehend the behaviour of markets and their vulnerabilities May et al. (2008); Mantegna and Stanley (1999); Chakrabarti et al. (2006). Apart from these applications, such methods could also be used in the analysis of the evolution of social and economic indictors to understand the well being of a society and to predict probable future changes and also in physics to study the response of an interacting many-body system to an external perturbation Scheffer (2009); May et al. (2008); Mantegna and Stanley (1999); Chakrabarti et al. (2006); Chakrabarti and Acharyya (1999).

What makes this challenge hard is that in a dynamical system there are a variety of reasons which can lead to different levels of qualitative changes in the dynamics of the system Kantz and Schreiber (2004); Small (2005); Ott (2002); Abarbanel (1996); Ruelle (1989); Guckenheimer and Holmes (1983). Some of the most common reasons are the evolving control parameters of the system passing through a bifurcation point, rate of change of these control parameters, internal feedbacks, and noise induced effects Kantz and Schreiber (2004); Small (2005); Ott (2002); Abarbanel (1996); Guckenheimer and Holmes (1983). In many natural systems it has been suggested that dynamic bifurcations lead to critical transitions in their dynamical state E.Benoît (1991); Kuehn (2011); Guckenheimer and Holmes (1983). In some cases these transitions are visually more apparent and can be identified with little effort but in some other cases these transitions are much more subtle, especially where transition occurs from one chaotic regime to other complex chaotic regime. For example, in palaeoclimate Dansgaard-Oeschger events on millennial time scales are visible in ice records to the naked eye and have been hypothesised to be caused by a noise induced transition Ditlevsen et al. (2005); Ditlevsen and Johnsen (2010); Ganopolski and Rahmstorf (2002). In contrast, on similar time scales we do not observe such visibly apparent transitions in many other components of climate, such as the Indian summer monsoon, though it has also gone through dynamical transitions between distinct chaotic regimes due to variations of Milankovitch cycles Levermann et al. (2009); N.Malik et al. (2012); Marwan et al. (2013). In this case we need more careful analysis. Similarly in neuroscience, certain brain states like sleep cycling or epileptic seizure are easily detectable from EEG data sets but gamma rhythms or the ultra-slow BOLD rhythms are harder to detect. Again, we need to employ more sophisticated mathematical tools to identify such dynamical states Steyn-Ross and Steyn-Ross (2010). In our understanding, the intricacies and diversities involved in the origin of dynamical transitions makes it difficult to develop one single method to identify and quantify all possible types of transitions. Rather we need to have a toolbox consisting of several methodologies and approaches inspired from the paradigm of nonlinear dynamics to solve such problems. The case we will be mostly interested in here is the one where the changes in one single control parameter takes the system from a regime of one dynamical complexity to other dynamics of less or higher complexity, with an important constraint that time series available for the analysis are relatively short (ranging between several hundred to few thousand time points).

Most widely used methods for some of the above mentioned problems are linear such as auto correlation function and detrended fluctuation analysis etc. Tredicce et al. (2004); Held and Kleinen (2004); Guttal and Jayaprakash (2008); Livina and Lenton (2007); Lenton et al. (2008). But certain methods for the analysis of time series using the paradigm of nonlinear dynamics have also shown tremendous promise. Significant among them are the recurrence plot based methodologies such as the recurrence quantification analysis and the recurrence network analysis Marwan et al. (2007); Iwayama et al. (2013); Gao and Jin (2009); Gao et al. (2010); Donges et al. (2011a, b); Marwan et al. (2009); Zou et al. (2012); Donner et al. (2011a, b). The method discussed here is called FLUS (FLUctuation of Similarity) in short, and it is based on the concept of nonlinear similarity between two time points. It was recently introduced in order to study short paleoclimatic time series of the Indian summer monsoon N.Malik et al. (2012). This new method is computationally simple, more automatized, and yet extremely robust in distinguishing distinct dynamical regimes and in identifying time points where transitions occur between these distinct dynamical regimes, even in the case where available time series is short. This method also tends to work well in the presence of noise and missing values. In this paper we present analytical findings which relates the new measure to more classical concepts in nonlinear time series analysis such as attractor dimensions and Lyapunov exponents. To demonstrate the strengths of this method in distinguishing dynamical regimes and in identifying transitions between them, we present a new set of challenging numerical tests and examples of dynamical transition in different nonlinear models. We also include tests for the new method’s robustness against noise and missing values.

This paper is organized as follows: first we describe the method and some of the analytical results on it with supporting numerics. Then we illustrate the strengths and practical usefulness of this method using several different numerical cases of dynamical transitions in nonlinear systems. Also, we test the method’s robustness against the presence of noise and missing values in a pragmatic nonlinear model. This is followed by an application in social dynamics, where we attempt to understand the role of unemployment in the crimes related to robberies and homicides in the US over the period 1975-1993.

II Method

Let represent the -th vector of a delay embedded time series of length . The embedding dimension and time delay are estimated respectively by fixed nearest neighbours and mutual information, as often done in nonlinear time series analysis Kantz and Schreiber (2004); Small (2005); Abarbanel (1996); Gibson et al. (1992); Packard et al. (1980). In this reconstructed phase space we denote the neighbourhood of any point as containing nearest neighbors, namely , where the set contains indices of the nearest neighbours and is a norm. A fixed number of close-neighbours is chosen for a point , hence varies with the change in the values of i.e., . In the text will be expressed as percentage of total number of points . We use Euclidean distance if not mentioned otherwise. The point-wise closeness of to its neighbours is obtained as the mean distance

| (1) |

Next we analyze the evolution of the neighbourhood of . At a later time , the neighbourhood of is generally different. But we are mainly interested in the evolution of , i.e., the neighbourhood of .Therefore, we calculate the closeness of to the neighbourhood of by means of a conditional distance, defined as

| (2) |

The dynamical similarity of conditioned to can then be defined by

| (3) |

Larger values of indicate higher similarities in the signal (i.e., a periodic trajectory with period , yields a periodic variation of ). It is easy to see that is time dependent, relying on the initial conditions. The distribution of inter-spike interval of reflects the associated recurrent period information, which shows unique properties for different dynamics (i.e., quasiperiodic or chaotic Zou et al. (2007)). In a full analogy, characterising the similarity of conditioned to can be calculated, which often yields since . Previously a similar measure has been used to estimate the nonlinear interdependency between two time series i.e., for bivariate studies Arnhold et al. (1999), where the conditional distance was calculated between time points coming from two separate time series.

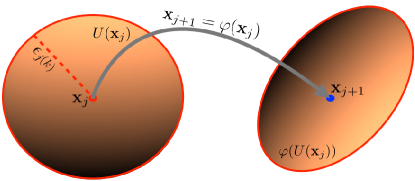

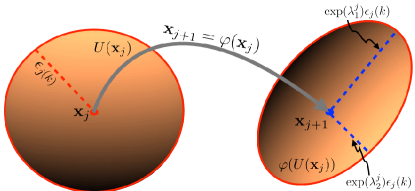

is a local measure and indicates local properties of the attractor and also it is computationally cumbersome to calculate all the possible for a complete time series. Next, we devise a strategy to obtain a measure from which is not only computationally simpler, but also has a dependence on the global properties of the attractor and hence, it will be sensitive to dynamical transitions. To achieve this task, we first need to understand what could be recognized as a dynamical transition. Let say exists between two consecutive time points i.e., there exists a smooth mapping such that

| (4) |

In the case of a dynamical transition, this determinism breaks down and then we must not have any such . If we fix and if there is no dynamical transition between and . Then we expect for a finite time series to fluctuate close to a constant value specific to the mapping . This particular feature of will be explained in some detail in the next section (also see Fig. 1, it gives a schematic representation of the above introduced measures and concepts). If a dynamical transition occurs between and , then this leads to substantially large and sharp fluctuations in . Which in turn could be quantified by the variance of over a window of points and given as

| (5) |

where , and denotes an average over points. We call as the fluctuation of similarity. Our numerical experimentation with a variety of nonlinear models with different kinds of transition has shown that is a robust measure to identify distinct dynamical regimes and corresponding transitions. It shows even more subtle transitions comparing to the standard measure of Lyapunov exponent, and its potential has been demonstrated using chaotic transitions in the logistic map N.Malik et al. (2012). Here we will be analysing several other nonlinear models by using this measure.

In the next section we will attempt to establish the relationship between and the dimension of the attractor as a first order approximation. We will also be providing some numerical results to support our analytical arguments. This will be followed up with a discussion on the relationship between the above introduced measures and the Lyapunov spectrum of the system.

III Relationship with attractor dimensions

The method presented above relies on comparing dynamical similarity of two consecutive time points in the embedded space, namely we only need to calculate for intended application. To get detailed insights into the properties of , we make use of scaling laws that exist for (the mean distance of point to its nearest neighbours) and (the mean distance of to the nearest neighbours defined by the neighbourhood of ), in case model/map (4) is true Arnhold et al. (1999). Suppose that a vector in phase space has nearest neighbours then for , we will have the following scaling law (for further extensive analytical details cf. Termonia and Alexandrowicz (1983); Arnhold et al. (1999); Pettis et al. (1979); Parker and Chua (1989); Badii and Politi (1985); Grassberger (1985)):

| (6) |

where is the length of the time series, is a scaling coefficient and is the mean density of the whole point cloud around , i.e., . For , , where is the effective dimension of the attractor. was first introduced in Termonia and Alexandrowicz (1983) and it has been conjectured in Badii and Politi (1985); Grassberger (1985) that is related to the th order Renyi dimension by the following implicit relationship

| (7) |

For a stochastic time series where is the embedding dimension.

As the conditional distance between and , namely also has a similar geometric formulation as the distance , hence conditional distance also scales with the ratio , and we can write

| (8) |

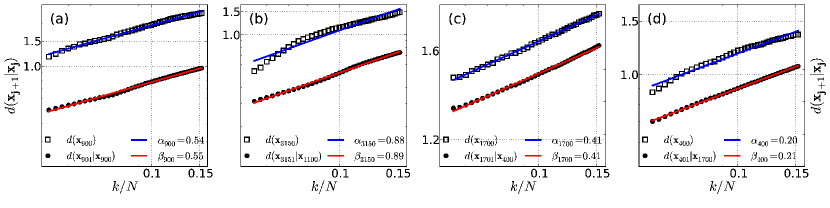

where is a scaling coefficient. In Fig. 2(a-d) we have numerically demonstrated the above stated scaling laws for and , by employing two different nonlinear systems. The first one is the Rössler system described by the following set of equations

| (9) |

where parameter corresponds to screw type chaos (see Fig. 2(a-b) for scaling behaviour). The second one is the logistic map described by

| (10) |

and corresponding scaling behaviour is plotted in Fig. 2(c-d). Generally such scaling laws require extremely large amount of data points Small (2005); Kantz and Schreiber (2004); Grassberger and Procaccia (1983a, b); Grassberger (1983); Gao (1999); Zou et al. (2012), but here we have attempted to obtain them using smaller amount of data points, namely with a time series of length . In Fig. 2 we can clearly observe that scaling laws introduced in Eq. (6) and Eq. (8) hold even for short time series, though there are fluctuations in the values of the exponents. Therefore, in case of short time series we assume that , where are fluctuations due to the shortness of the time series and numerical errors. Our attempt here is to provide the relationship between and under the constraint that we are only considering short time series, i.e., for finite value of .

Since the definition of the similarity between two consecutive time points is , we write the scaling law for similarity by taking into account Eqs. (6, 8) in the following form

| (11) |

where , and . The dynamical similarities between two consecutive time points and will be determined by the relationship between the exponents and . If no abrupt transition has occurred at the time point then determinism should exist between time points and , i.e., a mapping of the kind exists and Eq. (4) holds. Then we expect , i.e., if is infinity. In other words and are expected to scale by the same exponent. We provide an intuitive explanation of this in the sketch in Fig. 1. Locally at the mapping can be approximated to be a linear transformation, which means that the neighbourhood will be deformed into an ellipsoid due to the application of mapping . Any expansion in the ball by inclusion of more points will lead to rescaling of the size of by stretching or contraction in different directions. Hence, we will observe scaling of radii of these balls with the same exponent. We also expect in Eq. (11) that if . Hence, we could also say that for . For rigorous mathematical expression for c.f. Pettis et al. (1979); Badii and Politi (1985); Grassberger (1985); Parker and Chua (1989). The important point to note is that all these scalings are only asymptotically valid. In the practical case of time series of finite length, we observe fluctuating deviations of the exponents of the scaling, similar to what we have observed in our numerical examples in Fig. 2. Next we will attempt to study the influence of these fluctuations on our method and find an approximate expression for , the measure used for identifying transitions. For convenience, lets define a variable such that . Then Eq. (11) can be written as

| (12) |

In the considered examples we did not introduce any dynamical transitions hence determinism holds between two consecutive time points, and we do observe in Figs. 2. For both cases of Rössler system and logistic map we obtained as expected. Further we can write , defining . Therefore, for the case when determinism holds then for tending to infinity. As mentioned above that , therefore we can write . Substituting this form of in Eq. (12) we get

| (13) |

As and are small terms, we can neglect their product. Then we log transform Eq. (13) to finally yield

| (14) |

Expanding the right hand side of Eq. (14) in terms of exponential series and neglecting the higher order terms in , we get

Writing , the above expression becomes

Therefore the average of taken over a window of size is,

Finally, for the standard deviation we obtain the following expression,

| (15) |

Equation (15) shows the explicit dependence of on the dimension of the attractor (commonly is referred as the effective dimension of the attractor Arnhold et al. (1999)), since the term is kept constant over the whole length of the time series. Consequently, changes in the structure of the attractor will lead to changes in the value of .

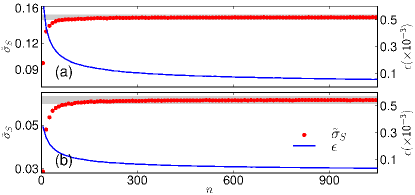

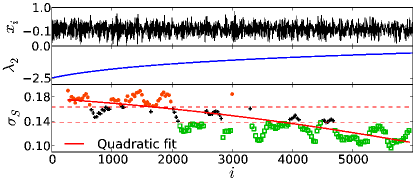

The law of large numbers must lead to converge, as the two constituents of , i.e. and are themselves expected to converge to constant values for large . If the fluctuation term converges for a large enough window size, then will also converge to a value which is a multiple of the attractor dimension. Let us next put this argument to a numerical test, in order to answer the question whether an increase in the number of observations in calculation of leads to convergence (Fig. 3) ? In Fig. 3 we show this convergence of . In Fig. 3(a) we consider the logistic map time series of length . We calculate with increasing window size i.e., including increasing number of time points in the calculation of . The median of i.e., is calculated for window size taking realisation of by boot strapping. The value of quickly converges as the window size is increased. The standard error in calculation of also show a continuous drop before saturating to small value around . A similar conclusion was reached for the Rössler system in Fig. 3(b). This also supports the usefulness of the windowing technique we have used in this work.

Our extensive numerical experimentation has demonstrated that is extremely sensitive to changes in the dynamics. The reason for this seems to be that any dynamical transition will lead to the breakdown of determinism between consecutive time points, i.e., Eq. (4) will not be valid anymore. This simply means that (or ), which in turn will produce a large fluctuation in the values of . These fluctuations will be captured by . The statistically most significant fluctuations indicate dynamical transitions, and could be identified by means of statistical significance tests as described later in Sec.V. We will continue this discussion about the analytical properties of and its average and variance in the Section IV. Next we present a numerical example to demonstrate, that is sensitive to changes in the dimension or complexity of the attractor.

The strange non-chaotic attractors (SNA) appear in various quasi-periodically driven dissipative dynamical systems Grebogi et al. (1984); Yalçinkaya and Lai (1997); Lai (1996). The transition between chaos and SNA are quite subtle and identifying them is a challenging numerical problem Ngamga et al. (2012, 2007). Here, we apply the presented method for identifying dynamical transitions to and from SNA. We will attempt to identify transitions in a coupled map of the form:

| (16) | |||||

The two types of Lyapunov exponents namely, the largest transverse Lyapunov exponent and the largest Lyapunov exponent of the subsystem , are given by the following set of equations Yalçinkaya and Lai (1997); Lai (1996)

| (17) | |||||

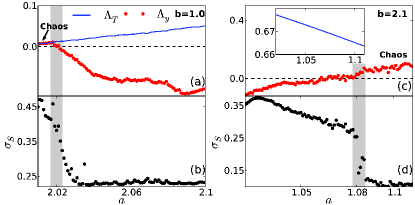

It is known that in the case of and we have SNA while for and we have a chaotic regime. In Fig. 4 (a, b) the grey band represents the transition to SNA from chaos. This transition known to occur via on-off intermittency. Whereas the grey band in Fig. 4 (c, d) highlights the transition from SNA to chaos.

We generate a short time series of length at different values of separated by . Then we calculate using embedding parameters and . In Fig. 4 we have plotted with the and . An abrupt change in the values of would indicate a transition. Comparing Fig. 4 (a, b) we observe that as starts to decrease and becomes negative, the values of show a simultaneous drop, signifying the dependence of on the complexity or qualitative features of the dynamics. We observe lower values of for SNA than for chaos. A similar change is observed if we reverse this transitions i.e., going from SNA to chaos (Fig.4 (c, d)). As the values of increase to positive values there is again a sharp drop in the values of . This example demonstrates that is able to capture even a subtle change in dynamics, like the ones that occur in transitions between the SNA and the chaos. In N.Malik et al. (2012) we have shown that can uncover all the transitions that are induced by the variation of the parameter in a logistic map like period-chaos transitions, intermittency, chaos-chaos transitions, etc..

IV Relationship with Lyapunov spectrum

Lyapunov exponents are the most extensively used measures for a quantitative characterization of nonlinear dynamics Ruelle (1989); Small (2005); Kantz and Schreiber (2004); Parker and Chua (1989); Abarbanel (1996). Several dynamical invariants are conjectured in terms of them such as Lyapunov dimension. However, a reliable numerical method to estimate from short time series remains to be a challenging problem Wolf et al. (1985); Parker and Chua (1989); Kurths and Herzel (1987), which we frequently encounter in various real time systems. The main objective of this section is to understand the new measure , its mean and variance in terms of these well known dynamical measures of Lyapunov exponents.

Suppose that Eq. (4) holds and are the eigenvalues of the Jacobian matrix . Then the deformation of the infinitesimal ball neighbourhood of in any direction will be multiple of (see Fig. 5).

Defining , where are called the Lyapunov numbers. The local Lyapunov exponents, are given by

| (18) |

The global Lyapunov exponent corresponding to the direction is the asymptotic value of

| (19) |

If the distance metric used for calculation of is the Euclidean then a simple geometrical consideration yields

which directly leads to

| (20) |

Hence, measures the total deformation of the ball neighbourhood of point when a mapping is applied on it.

From Eq. 20, we find that the average of taken over a window of size is,

| (21) |

Comparing, Eq. (21) with Eq. (18) and Eq. (19) we can conclude that will be structurally the same as the sum of the local Lyapunov exponents, while over large will be structurally the same as the sum of the global Lyapunov exponents. This is shown numerically for the Logistic map in Fig. 6. In case of a chaotic system we always have a direction such that the i.e., , representing the expansion in the direction . In other directions we will either have contraction, , i.e., or , i.e., . Therefore, in a chaotic system with few degrees of freedom the most dominant contribution to in Eq. (20) comes from the largest positive eigenvalue corresponding to the expansion. Hence, for such a systems will be structurally similar to the Lyapunov exponent. In Fig. 6 we observe a structural correspondence between and the Lyapunov exponent of the logistic map in form of an anti-phase relationship. We know the sum of the largest Lyapunov exponents is proven for certain systems to be related with dynamical invariants such as Lyapunov dimension, topological entropy, and information dimension (due to Kaplan-Yorke conjecture) Ruelle (1989); Young (1982); Frederickson et al. (1983); Ott (2002). Therefore, we may think that could also be used in quantifying dynamics but our numerical analysis has shown that is not well suited for detecting dynamical transitions in the series because it is less sensitive in quantifying and capturing large fluctuations in . It will be better to use for this purpose, also is better suited to quantify variation in parameters of a dynamical system and corresponding changes in the dynamics, because any variation in the parameters of a dynamical system will lead to variation in the Lyapunov spectrum too. Transitions lead to large deformations of the neighbourhood, leading to large fluctuations in the magnitude of , which are then captured by . A point to note is that the global Lyapunov exponents are not defined for a time series with a transition, due to the constraints imposed by ergodicity.

In order to get further insights into the properties of measure we take a look at the distribution of (dropping subscript for simplicity) over window size of vectors, . are in a sense random numbers for chaotic systems. The expression of , Eq. (20) consists of a summation over , therefore, the central limit theorem implies that follows a Gaussian distribution at least asymptotically. Following Ott (2002), we find that asymptotically has the following general analytical form,

| (22) |

where is a convex quadratic function with minimum zero, occurring at i.e., also, , . Expanding around and neglecting higher order terms, we write Eq. (22) as,

| (23) |

which gives a familiar looking form of a Gaussian distribution. Then

| (24) |

A similar expression for distribution and variance could also be written for the local Lyapunov exponents Ott (2002), where is known as the spectrum of the local Lyapunov exponents and can be used for characterising the dynamics of the system Grassberger et al. (1988); Sepúlveda et al. (1989); Prasad and Ramaswamy (1999). So as an analogy we propose that can also be used to characterise the dynamics. The distribution of for different types of dynamics may follow a Gaussian distribution of the type asymptotically but each type of dynamics must correspond to unique and . This is because of the fact that each type of dynamics has a unique (see Eq. (4)) and hence unique eigenvalues and the corresponding deformations and values of should also be unique. In future research we intend to develop a method based on estimation of to classify distinct dynamics.

V Dynamical transition induced by co-evolving parameters

In the numerical example above values of could distinguish between two distinct chaotic regimes and SNA, demonstrating that can be used to distinguish different types of dynamics. A similar conclusion about the capability of in identifying distinct dynamics could be made from an example of logistic map presented in N.Malik et al. (2012), where was used to uncover all the transitions that are induced by the variation of the parameter in a logistic map like period-chaos transitions, intermittency, chaos-chaos transitions, etc.. One important point is that in these examples we had one whole time series at each value of the parameter. In many realistic systems we do not have the luxury of a whole time series being available at a single value of the control parameter. Rather, the most common real situation is when control parameter also co-evolves with the dynamics Scheffer (2009); Guckenheimer and Holmes (1983); E.Benoît (1991); Kuehn (2011). We only have very few points available at a particular value of the control parameter. For example, in palaeoclimate we have few observation of a climatic variable via proxies,while parameters which drive climate like solar insolation co-evolve with these climatic variable at time leading to transitions in the dynamics N.Malik et al. (2012); Lenton et al. (2008); Ashwin et al. (2012); Levermann et al. (2009); Kuehn (2011). Another example of this situation is observed in social dynamics, where we have very few observation of social indices while the parameters driving social dynamics, like the economic and political situations, coevolve with it Scheffer (2009); May et al. (2008); Mantegna and Stanley (1999); Chakrabarti et al. (2006). A further example of this situation is in neuroscience, where event-related potentials (ERP) measured by EEG show several distinct dynamical behaviours as a response to changing stimuli Allefeld et al. (2008); Luck (2005). One possible conceptual model for such transitions could be:

| (25) |

where is a set of variables of a dynamical system, with being a parameter evolving with time. Rate of change of , or passing of through the bifurcation point of the system can lead to a variety of qualitative changes in the dynamics of the system, including the more subtle one of shifting of the system from regime of one complex chaotic dynamics to other chaotic dynamics of higher or lower complexityE.Benoît (1991); Kuehn (2011); Guckenheimer and Holmes (1983); Ashwin et al. (2012); Kantz and Schreiber (2004). In the numerical examples following this section, we let the parameter simultaneously evolve with variables of the system. This would provide us more realistic model examples to test our method for its practical usefulness.

We have also introduced a statistical test for assisting a more automatized identification of dynamical transitions in N.Malik et al. (2012). For convenience we describe it here again : We have used the temporal evolution of to identify the changes in dynamics. To test the relative statistical significance of two values of to belong to distinct or same dynamics, we use a bootstrapping procedure, where we randomly draw values with replacement from the series of , where is the window size used in calculation of . Repeating this procedure several thousand times we generate an ensemble of values of . Then we interpret 0.05 and 0.95 percent quantiles of this ensemble as the confidence bounds. The values of outside this bound are less probable to occur. Hence, we can classify these points as belonging to dynamics of two distinct complexity with confidence. The time band over which the crossover between the two levels occurs contains the point of dynamical transition. The points with lower values of may be regarded as belonging to dynamical regimes which are relatively more stable and lower in dynamical complexity.

V.1 Identifying drift in the dynamics (nonstationarity)

One of the challenging problems could be identifying a continuous drift in the dynamics of a time series. For this purpose we use the generalized Baker’s map Farmer et al. (1983) and generated a time series following the same procedure as described in Schreiber (1997).

| (26) |

The Lyapunov exponents for the above set of equations are

| (27) | |||||

| (28) |

Now we introduce a drift in the parameter as done in Schreiber (1997), namely, by generating a time series of length by varying in each iteration by and fixing the value of . This creates a nonstationary time series with drift in dynamics, while the maximal Lyapunov exponent is constant (Eq. 27). The trend from the time series is removed by taking

where and we took = 50. We consider only a short section of the time series by taking points from to , which means we have considered only time points. However, in the original work of Schreiber (1997), data points were used. We use the embedding parameters and . The result is shown in Fig. 7, where we observe that values of go from significantly higher values to significantly lower ones, which is representative of the dynamical drift that has taken over the time points.

V.2 Transition between transient chaos and Lorenz’s attractor

Another example somewhat similar to the above one, but in case of a time continuous system, is the formation of Lorenz’s attractor from transient chaos :

| (29) | |||||

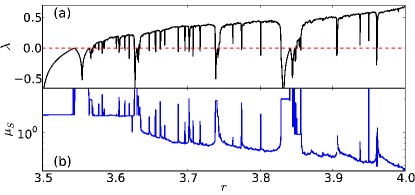

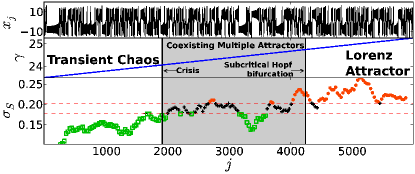

The chaotic Lorenz’s attractor exists for , whereas transient chaos exists for . For the transition zone , there is a coexistence of three attractors: two being steady states and one a chaotic attractor Sparrow (1982). The transient chaos disappears due to a crisis at and Lorenz’s attractor emerges as the only possible stable attractor due to a subcritical Hopf bifurcation at . We generate a time series of the variable by solving Eq. (V.2), using a Runge-Kutta fourth order procedure at time step resolution of , while sampling a point after time steps. We have sampled time points and varied linearly between to . So, we can substitute in Eq. (V.2), where and is a small increment of the order of . This variation leads the system to pass through the transient chaos to a transition zone (crisis and subcritical Hopf transitions) to the formation of Lorenz’s attractor (Fig. 8).

To calculate we have used , and a window size of with overlap. A detailed explanation for our choice of rather higher values of embedding parameters is provided in Sec. V.5. The calculated values of are shown in the lowest panel of Fig. 8, with color of markers standing the same as in previous example. We observe lower values of (green open squares) below the confidence bound for transient chaos and higher values (orange dots) above the confidence bound for Lorenz’s attractor, hence distinguishing both dynamical regimes in this time series. The transition zone (grey shaded region) not only contains multiple transition but also multiple attractors which is also reflected in the values of , while it jumps between green open squares and orange dots few times. Due to the fact that the formation of an attractor is temporally delayed Baer et al. (1989), and we also loose few initial points due to windowing and embedding, the transitions are usually rightward shifted.

V.3 Tolerance of the measure against observational noise

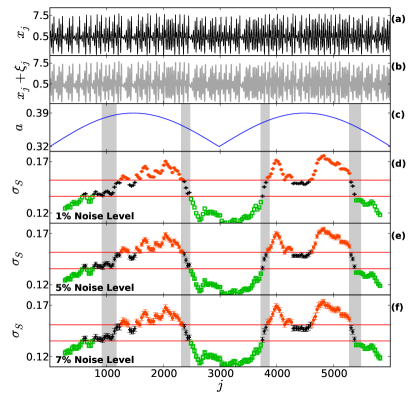

To test the influence of observational noise on the above introduced measure, we consider the example of the Rössler model Eq. (9). In this system two topologically distinct attractors exist, namely spiral type chaos for and screw type chaos for Gaspard and Nicolis (1983); Gaspard (1993). The transition behaviour occurs via the formation of a homoclinic orbit at Gaspard and Nicolis (1983). We generate a test time series for our method by varying the control parameter and by defining its temporal evolution as at every six hundredth integration step. is the step size for the fourth order Runge-Kutta integrator (). Then we sample points of the -component at the rate of . This leads to cross the transition point four times (see Fig. 9 (c)). This example was also discussed in N.Malik et al. (2012). Here we discuss it in the context of presence of observational noise in this section and missing values in the next section.

To add white noise into the time series we generate normally distributed random variable with its mean and its standard deviation , where is the standard deviation of the whole time series. Then we simply add a to each value of in the time series (see Fig. 9 (b)). We can vary the strength of noise by varying , for instance when we have noise level or noise in the signal. We test the tolerance of the measure against three different noise levels here, viz. , , and (see Fig. 9 (d-f)). The error bars on the values of are obtained by generating different realizations of noise at each level. We have replaced the significance levels from dotted red lines to solid red lines, as these are the mean of the significance levels for all the different realizations of the noise. In Fig. 9(d-f) we observe that all the transitions seems to remain intact for all the different levels of noise. This is a clear indication that this method is robust against nominal levels of noise. We have also attempted the above numerical experiment with some other models, and the results of those experiments also demonstrate similar robustness of this method against nominal levels of noise. The embedding parameters used for every level of noise are exactly the same, we had set and and window size of with overlap. These parameters are also the same as used in N.Malik et al. (2012), while discussing this example in noise free case.

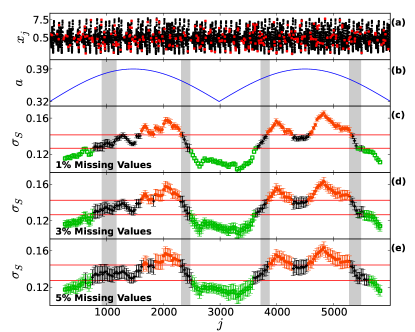

V.4 Strategy for treatment of missing values

Apart from shortness of the data, another central problem which surrounds data analysis is irregular sampling or missing values Rehfeld1 et al. (2011); Scargle (1989); Schulz and Stattegger (1997). This is a common problem in fields such as astronomy, medical, earth, and social sciences Rehfeld1 et al. (2011); Scargle (1989); Schulz and Stattegger (1997); Kim et al. (2009); Čepar et al. (1992); King (2010). We here propose a strategy to deal with missing values while using the fluctuation of similarity method. To generate a test time series, we consider the same Rössler model as introduced in the previous section and randomly remove some of the values in the time series. The amount of time points removed from the time series are given in terms of percentage of missing values. A straightforward application of the fluctuation of similarity method will not work in such a case, due to the incompatibility of embedding a time series in delayed coordinates with missing values. The first step of our strategy for dealing with treatment of missing values involves replacing the missing values with a flag (e.g. a NaN character). Then we continue to embed the time series in time delayed coordinates, with some of the coordinates just being the flags. But this would make the numerical calculation of a distance metric impossible, to get over this issue we recommend to use the Chebyshev distance, rather then euclidean distance as done all throughout this work. Chebyshev distance between two vectors and is given by , where is the th component of the vector . It ignores the non-numerical flags and maximum is only calculated over the numerical values. Thus, it returns non-numerical values only in the rare case when all the components of both the vectors are non-numerical flags. Whereas euclidean distance cannot be calculated even if there is a single non-numerical flag present, which is the most common occurrence when we have missing values. Therefore, we prefer using Chebyshev distance over euclidean distance. Using the same delay and embedding dimensions as in the previous section, we present the result at different amounts of missing values in Fig. 10 (c-e). The error bar on the values of were obtained from different realizations of missing values. The solid horizontal red lines are again the mean significance levels for different realizations of missing values. In Fig. 10 we observe that the above strategy seems to work to certain amount of missing values in the data. The embedding parameter used in this case were exactly the same as used in previous example.

V.5 A note about embedding parameters and window size

In the examples above, we have used a rather high embedding dimension, which is due to the fact that the systems we are considering have one of its parameters varying with time (such as Bakers’ map and Lorenz system with a drift and Rössler system with nonlinear transitions). This converts the systems into non-autonomous systems. Taken’s theorem is not valid for such a system. Hence, we cannot take the embedding dimension as prescribed by the Taken’s theorem ( is the known dimension of the system) Takens (1981); Packard et al. (1980). Though, there is no specific embedding theorem for such systems but heuristic arguments in Hegger et al. (2000) state that a proper choice for the embedding dimension should be larger than where is the number of time varying parameters of the system. It has been suggested that this technique of “overembedding” a time series helps in overcoming both nonstationarity and noise effects Hegger et al. (2000); Verdes et al. (2006). We will continue using high embedding dimension in the next section, where we would be applying our method in the analysis of crime record’s time series, as these time series have originated from a system (society) which is not only high dimensional but also a large parameter space. So, must be a large number. In the crime record’s time series used below, apart from visible non-stationarity the time series also has a high amount of noise which is also visible by eye and via its power spectrum. Hence, a high embedding dimension is an appropriate choice.

In Fig. 3 we have shown a quick convergence of on taking large enough window sizes, which in turn gives the measure dependence on the structure of the attractor through the effective dimension . By taking overlapping windows, we avoid reducing the amount of data appreciably. The presented method differs in one very basic aspect from other methods, in particular those based on recurrence properties. In many of them one first takes a window over the data (or embedded vectors) and then calculate some measure based on the recurrence property Casdagli (1997); Marwan et al. (2007); Donges et al. (2011a, b); Marwan et al. (2009). This brings the relationship between windowing, dimension and delay. In our method we follow a different approach, first of all the recurrence distances of a point over the whole time series are calculated and, then, by comparing each consecutive time point, we calculate the measure for each point. Till this step we have no windowing. In the next step we calculate the fluctuations in this measure by taking windows. The way we have defined the significance test, the window size now helps in resolving time scales on which we wish to see the transitions. The real task of windowing is to give control over resolving time scales for transitions.

VI Application to social dynamics

Now we present an application of our method to an observed time series in social dynamics. Crime rates in society might be interpreted as following some nonlinear dynamics and affected by political, economic, and social situations McDowall (2002). Analytic methods of time series analysis and agent based modeling have been used to predict and quantify the evolution of crime rates in different settings and societies Greenberg (2001); Box-Steffensmeier et al. (2008); Pratt and Lowenkamp (2002); Makowsky (2006); Malleson et al. (2013). Various methods from the rich paradigm of nonlinear time series analysis do not appear to have been applied to available data sets of crime records. We here analyze time series of robberies and homicides in the United States from 1975 to 1993 with monthly resolution. With this analysis we attempt to understand the nature of relationship if any between unemployment and robberies, and unemployment and homicides over this period Chiricos (1987); Freeman (1983); Box-Steffensmeier et al. (2008).

VI.1 Data source

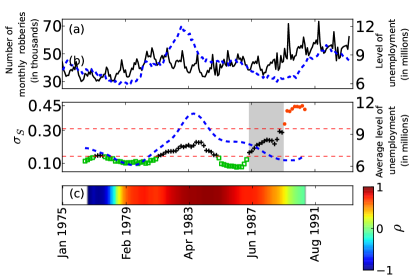

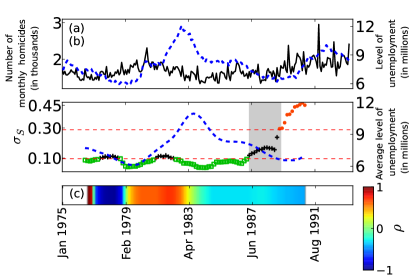

The source of data studies here on monthly robberies and monthly homicides is ICPSR (Inter-university Consortium for Political and Social Research) study 6792 (Uniform Crime Reports: Monthly Weapon-Specific Crime and Arrest Time Series, 1975-1993). The source of unemployment data is the US Bureau of Labour Statistics (http://www.bls.gov/data/), using the monthly levels of unemployment for the whole US for the period 1975-1993. In Fig. 11 (a) and Fig. 12 (a), black lines correspond to monthly robberies and monthly homicides respectively and blue dotted lines represent the unemployment rate over the same period. We have removed the linear trend from monthly robberies and monthly homicides time series by subtracting a linear least squares fit to the data.

VI.2 Results

The calculation of for monthly robberies and homicides time series was done using a window size of months with overlap, embedding dimension , and delay of , plotted in Fig. 11(b) and Fig. 12(b). As emphasised in the discussion above, higher values of correspond greater variability or complexity in the dynamics; while low values correspond to low complexity in the dynamics. For monthly robberies time series in Fig. 11(b) we observe low values of until 1982 (green open squares). Between 1983-1985 we also observe lower values of but in a statistically insignificant regime (black plus signs). Then close to 1987 there is a significant increase in the values of (orange dots) and the values cross the significance band during a transition between the period 1987–1990 (highlighted by a grey band). We uncover a similar transition in Fig. 12(b) occurring close to 1987 (see the grey band in both figures covering the period between 1987–1990.)

If we closely observe the original time series of robberies and homicides, then it is visible even to the naked eye that there are higher variabilities and larger fluctuations after this period. A fact to be noted here is that crimes in the US across all the categories of crime started to drop in the 1990’s and this drop has continued since Levitt (2004); LaFree (1999); Farrell et al. (2011); Ouimet (2002). Several reasons have been hypothesized for this decrease, including increased incarceration Marvell and Moody (1994), more police Marvell and Moody (1996), the decline of crack use Blumstein and Rosenfeld (1998), legalized abortion Levitt (2004), improvement in the quantity and quality of security Farrell et al. (2011) and changing demographics Ouimet (2002). Our time series analysis above only brings forward the point that some fundamental change in the dynamics of crime in the US occurred in the late 1980’s and early 1990’s, leading to continuous drop in the crime rate in the following decades.

In Fig. 11 (c) and Fig. 12 (c), the continuous color variation gives the cross correlation between and unemployment rate averaged over exactly the same time windows as . The blue curves in the middle panels of Fig. 11 and Fig. 12 correspond to this averaged unemployment rate. In the case of unemployment and robberies, we observe high positive values of cross correlation () between the two curves from 1979 to 1989 and then an abrupt breakdown of this correlation, indicating some fundamental shift in the crimes related to robberies around this time. In our second case of homicides, however we do not observe any such relation between unemployment and homicides: the values of cross correlation between and average unemployment are rather low and fluctuating between negative and positive values. That is, the signals of unemployment rate driving variability and complexity in dynamics of robberies before the 1990’s are quite apparent but they do not seem to play any significant role in homicides.

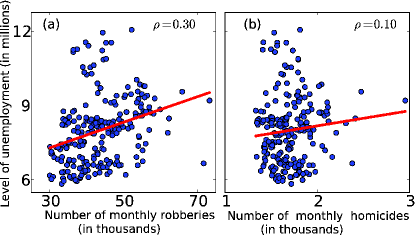

Sociologists have pointed out that the relationship between unemployment and robberies is a rather complex one: increasing unemployment increases the criminal motivation (unemployed individuals are more motivated to indulge in robbery for their financial needs and survival) but it also decreases the criminal opportunity (more men start to stay at home, so less opportunity for criminals to break into homes), creating a counter balancing effect Kleck and Chirico (2006). Hence, we cannot expect a linear relationship between both. We have also not observed a strong linear correlation (see Fig. 13) or a Granger causal relationship between these two variables. What our above analysis shows is that unemployment may have been driving the complexity or variability in the dynamics of robberies prior to the late 1980’s and early 1990’s. The breakdown in this relationship corresponds to a time period when the crime rate in the US started to steadily drop, due to several reasons discussed in detail in the references Levitt (2004); LaFree (1999); Farrell et al. (2011); Ouimet (2002); Marvell and Moody (1994, 1996); Blumstein and Rosenfeld (1998).

An important perspective in criminology has been conflict theory, where it is considered that economic deprivations influence crime rates Pratt and Lowenkamp (2002), but there does not exist a conclusive empirical support for this relationship Chiricos (1987); Freeman (1983); Piehl (1998). In our analysis, if we treat the unemployment rate as being one of the economic indicators then we observe an episodic relationship between robberies and unemployment but the same cannot be said for homicides. Undoubtedly multiple interconnected factors including economic indicators drive crime rates. To accept or reject the economic deprivations perspective of crime, one would need to do extensive analysis of different social and economic indicators. As demonstrated above, our method could be useful in such analyzes and in other endeavours where similar questions could arise.

VII Conclusion

Developing a set of methods that can be used to distinguish distinct dynamical regimes and transitions between them in a given time series has been a challenge in nonlinear time series analysis with wide applicability in a variety of fields. We have recently proposed a new method, based on computation of nonlinear similarities between time points of a univariate time series N.Malik et al. (2012). The method is robust, automatized, and computationally simple and can be used even in cases with shorter time series, or missing values, or observational noise. Here we have presented some new analytical findings, where we have related this measure to some classical concepts in nonlinear dynamics such as attractor dimensions and Lyapunov exponents. We have shown that the new measure has linear dependence on the variation of change in dimensionality or complexity of the attractor. Also, it measures the variance of the sum of the Lyapunov spectrum. One of the problems we have studied in detail with this method is identification of transitions in dynamics when the parameters of the system are also evolving with dynamics. The proposed method is able to identify these most subtle of transitions, even including those where such evolution of parameter induces only a drift or nonstationarity in the dynamics. Also, employing a wide variety of prototypical model systems we have demonstrated the practical usefulness of this method.

Furthermore, we have used this method to analyze a time series from social dynamics, studying time series of US crime from 1975 to 1993. In doing so we have attempted to understand the nature of the relationship between crime rates (robbery and homicides) and unemployment levels during this period. We have found a dynamical transition in the late 1980’s in both homicide and robbery rates and also found the dynamical complexity in robbery rates was driven by unemployment before this transition in 1990’s.

Acknowledgements.

N Malik and P J Mucha acknowledge support from Award Number R21GM099493 from the National Institute of General Medical Sciences. The content is solely the responsibility of the authors and does not necessarily represent the official views of the National Institute of General Medical Sciences or the National Institutes of Health. Y Zou is supported by the National Natural Science Foundation of China (Grant Nos. 11305062, 11135001). N Marwan and J Kurths are supported by the Potsdam Research Cluster for Georisk Analysis, Environmental Change and Sustainability (PROGRESS, support code 03IS2191B).References

- N.Malik et al. (2012) N.Malik, Y. Zou, N. Marwan, and J. Kurths, Europhysics Letters 97, 40009 (2012).

- Marwan et al. (2007) N. Marwan, M. Romano, M. Thiel, and J. Kurths, Phys. Rep. 438, 237 (2007).

- Kantz and Schreiber (2004) H. Kantz and T. Schreiber, Nonlinear Time Series Analysis (Cambridge University Press, Cambridge, 2004), 2nd ed.

- Small (2005) M. Small, Applied Nonlinear Time Series Analyses (World Scientific, 2005).

- Abarbanel (1996) H. Abarbanel, Analysis of Observed Chaotic Data (Springer, 1996), 1st ed.

- Schreiber (1997) T. Schreiber, Phys. Rev. Lett. 78, 843 (1997).

- Donges et al. (2011a) J. F. Donges, R. V. Donner, K. Rehfeld, N. Marwan, M. H. Trauth, and J. Kurths, Nonlinear Processes in Geophysics 18, 545 (2011a).

- Livina and Lenton (2007) V. N. Livina and T. Lenton, Geophys. Res. Lett. 34, L03712 (2007).

- Donges et al. (2011b) J. F. Donges, R. V. Donner, M. H. Trauth, N. Marwan, H. J. Schellnhuber, and J. Kurths, PNAS 108, 20422 (2011b).

- Marwan et al. (2009) N. Marwan, J. F. Donges, Y. Zou, R. V. Donner, and J. Kurths, Phys. Lett. A 373, 4246 (2009).

- Lenton et al. (2008) T. M. Lenton, H. Held, E. Kriegler, J. W. Hall, W. Lucht, S. Rahmstorf, and H. J. Schellnhuber, PNAS 105, 1786 (2008).

- Schütz and Holschneider (2011) N. Schütz and M. Holschneider, Phys. Rev. E 84, 021120 (2011).

- Scheffer (2009) M. Scheffer, Critical Transitions in Nature and Society (Princeton University Press, 2009).

- Lehnertz and Elger (1998) K. Lehnertz and C. E. Elger, Phys. Rev. Lett. 80, 5019 (1998).

- Venegas et al. (2005) J. Venegas, T. Winkler, G. Musch, M. V. Melo, D. Layfield, N. Tgavalekos, A. Fischman, R. Callahan, G. Bellani, and R. Harris, Nature 434, 777 (2005).

- P.E.McSharry et al. (2003) P.E.McSharry, L.A.Smith, and L.Tarassenko, Nature Med. 9, 241 (2003).

- Ashwin et al. (2012) P. Ashwin, S. Wieczorek, R. Vitolo, and P. Cox, Phil. Trans. R. Soc. A 370, 1166 (2012).

- May et al. (2008) R. May, S. Levin, and G. Sugihara, Nature 451 (2008).

- Mantegna and Stanley (1999) R. N. Mantegna and H. E. Stanley, An Introduction to Econophysics: Correlations and Complexity in Finance (Cambridge University Press, Cambridge, UK, 1999).

- Chakrabarti et al. (2006) B. K. Chakrabarti, A. Chakraborti, and A. Chatterjee, Econophysics and Sociophysics : Trends and Perspectives (Wiley-VCH, Berlin, 2006).

- Chakrabarti and Acharyya (1999) B. K. Chakrabarti and M. Acharyya, Rev. Mod. Phys. 71, 847 (1999).

- Ott (2002) E. Ott, Chaos in Dynamical Systems (Cambridge University Press, Cambridge, 2002), 2nd ed.

- Ruelle (1989) D. Ruelle, Chaotic evolution and strange attractors - The statistical analysis of time series for deterministic nonlinear systems (Cambridge, Cambridge, UK, 1989).

- Guckenheimer and Holmes (1983) J. Guckenheimer and P. Holmes, Nonlinear Oscillations, Dynamical Systems, and Bifurcations of Vector Fields (Springer, 1983).

- E.Benoît (1991) E.Benoît, ed., Dynamic bifurcations. Lecture Notes in Mathematics,, vol. 1493 (Springer-Verlag, Berlin, Germany, 1991).

- Kuehn (2011) C. Kuehn, Physica D 240, 1020 (2011).

- Ditlevsen et al. (2005) P. D. Ditlevsen, M. S. Kristensen, and K. K. Andersen, Journal of Climate 18, 2594 (2005).

- Ditlevsen and Johnsen (2010) P. D. Ditlevsen and S. Johnsen, Geophys. Res. Lett. 37, L19703 (2010).

- Ganopolski and Rahmstorf (2002) A. Ganopolski and S. Rahmstorf, Phys. Rev. Lett. 88 (2002).

- Levermann et al. (2009) A. Levermann, J. Schewe, V. Petoukhov, and H. Held, PNAS 106, 20572 (2009).

- Marwan et al. (2013) N. Marwan, S. Schinkel, and J. Kurths, EPL (Europhysics Letters) 101, 20007 (2013).

- Steyn-Ross and Steyn-Ross (2010) D. A. Steyn-Ross and M. Steyn-Ross, eds., Modeling Phase Transitions in the Brain (Springer, 2010).

- Tredicce et al. (2004) J. R. Tredicce, G. L. Lippi, P. Mandel, B. Charasse, A. Chevalier, and B. Picque, Am. J. Phys. 72 (2004).

- Held and Kleinen (2004) H. Held and T. Kleinen, Geophys. Res. Lett. 31, L23207 (2004).

- Guttal and Jayaprakash (2008) V. Guttal and C. Jayaprakash, Theoret. Ecol. 2, 3 (2008).

- Iwayama et al. (2013) K. Iwayama, Y. Hirata, H. Suzuki, and K. Aihara, Nonlinear Theory and Its Applications, IEICE 4, 160 (2013).

- Gao and Jin (2009) Z. Gao and N. Jin, Chaos 19, 033137 (2009).

- Gao et al. (2010) Z.-K. Gao, N.-D. Jin, W.-X. Wang, and Y.-C. Lai, Phys. Rev. E 82, 016210 (2010).

- Zou et al. (2012) Y. Zou, J. Heitzig, R. Donner, J. Donges, J. Farmer, R. Meucci, S. Euzzor, N. Marwan, and J. Kurths, Europhysics Letters 98, 48001 (2012).

- Donner et al. (2011a) R. V. Donner, M. Small, J. F. Donges, N. Marwan, Y. Zou, R. Xiang, and J. Kurths, Int. J. Bifurc. Chaos 21, 1019 (2011a).

- Donner et al. (2011b) R. V. Donner, J. Heitzig, J. F. Donges, Y. Zou, N. Marwan, and J. Kurths, Eur. Phys. J. B 84, 653 (2011b).

- Gibson et al. (1992) J. F. Gibson, J. D. Farmer, M. Casdagli, and S. Eubank, Physica D 57, 1–30 (1992).

- Packard et al. (1980) N. H. Packard, J. P. Crutchfield, J. D. Farmer, and R. S. Shaw, Phys. Rev. Lett. 45, 712 (1980).

- Zou et al. (2007) Y. Zou, D. Pazó, M. C. Romano, M. Thiel, and J. Kurths, Phy. Rev. E 76, 016210 (2007).

- Arnhold et al. (1999) J. Arnhold, P. Grassberger, K. Lehnertz, and C. Elger, Physica D 134, 419 (1999).

- Termonia and Alexandrowicz (1983) Y. Termonia and Z. Alexandrowicz, Phys. Rev. Lett. 51, 1265 (1983).

- Pettis et al. (1979) K. W. Pettis, T. A. Bailey, A. K. Jain, and R. C. Dubes, IEEE Transactions on Pattern Analysis and Machine intelligence PAM-1(1), 25 (1979).

- Parker and Chua (1989) T. S. Parker and L. Chua, Practical Numerical Algorithms for Chaotic Systems (Springer-Verlag, 1989).

- Badii and Politi (1985) R. Badii and A. Politi, J.Stats. Phys. 40 (1985).

- Grassberger (1985) P. Grassberger, 107A (1985).

- Grassberger and Procaccia (1983a) P. Grassberger and I. Procaccia, Physica D Nonlinear Phenomena 9, 189 (1983a).

- Grassberger and Procaccia (1983b) P. Grassberger and I. Procaccia, Phys. Rev. Lett. 50, 346 (1983b).

- Grassberger (1983) P. Grassberger, Phys. Lett. A 97, 227 (1983).

- Gao (1999) J. B. Gao, Phys. Rev. Lett. 83, 3178 (1999).

- Grebogi et al. (1984) C. Grebogi, E. Ott, S. Pelikan, and J. A. Yorke, Physica D: Nonlinear Phenomena 13, 261 (1984).

- Yalçinkaya and Lai (1997) T. Yalçinkaya and Y.-C. Lai, Phys. Rev. E 56, 1623 (1997).

- Lai (1996) Y.-C. Lai, Phys. Rev. E 53, 57 (1996).

- Ngamga et al. (2012) E. J. Ngamga, D. V. Senthilkumar, A. Prasad, P. Parmananda, N. Marwan, and J. Kurths, Phys. Rev. E 85, 026217 (2012).

- Ngamga et al. (2007) E. J. Ngamga, A. Nandi, R. Ramaswamy, M. C. Romano, M. Thiel, and J. Kurths, Phys. Rev. E 75, 036222 (2007).

- Wolf et al. (1985) A. Wolf, J. B. Swift, H. L. Swinney, and J. A. Vastano, Physica D 16D, 285 (1985).

- Kurths and Herzel (1987) J. Kurths and H. Herzel, Physica D 25, 165 (1987).

- Young (1982) L. S. Young, Ergodic Theory and Dyn. Systems 2, 109 (1982).

- Frederickson et al. (1983) P. Frederickson, J. L. Kaplan, E. D. Yorke., and J. A. Yorke, J. Diff. Eq. p. 185 (1983).

- Grassberger et al. (1988) P. Grassberger, R. Badii, and A. Politi, Jour. of Stats. Phys. 51, 135 (1988).

- Sepúlveda et al. (1989) M. A. Sepúlveda, R. Badii, and E. Pollak, Phys. Rev. Lett. 63, 1226 (1989).

- Prasad and Ramaswamy (1999) A. Prasad and R. Ramaswamy, Phys. Rev. E 60, 2761 (1999).

- Allefeld et al. (2008) C. Allefeld, P. Beim Graben, and J. Kurths, Advanced methods of electrophysiological signal analysis and symbol grounding? : dynamical systems approaches to language / C. Allefeld, P. Beim Graben, and J. Kurths, editors (New York : Nova Science Publishers, 2008), ISBN 9781604560220 (hardcover), formerly CIP.

- Luck (2005) S. J. Luck, An Introduction to the Event-Related Potential Technique (The MIT Press, 2005).

- Farmer et al. (1983) J. D. Farmer, E. Ott, and J. A. Yorke, Physica D 7, 153 (1983).

- Sparrow (1982) C. Sparrow, The Lorenz Equations: Bifurcations, Chaos and Strange Attrcators (Springer-Verlag, 1982).

- Baer et al. (1989) S. M. Baer, T. Erneux, and J. Rinzel, SIAM J. Appl. Math. 49, 55–71 (1989).

- Gaspard and Nicolis (1983) P. Gaspard and G. Nicolis, J. of Stat. Phys. 31, 499 (1983).

- Gaspard (1993) P. Gaspard, Physica D 62, 94 (1993).

- Rehfeld1 et al. (2011) K. Rehfeld1, N. Marwan, J. Heitzig, and J. Kurths, Nonlin. Processes Geophys. 18, 389 (2011).

- Scargle (1989) J. D. Scargle, Astrophys. J. 343 (1989).

- Schulz and Stattegger (1997) M. Schulz and K. Stattegger, Comput. Geosci. 23, 929 (1997).

- Kim et al. (2009) K. K. Kim, J. S. Kim, Y. G. Lim, and K. S. Park, Physiol. Meas. 30, 1039 (2009).

- Čepar et al. (1992) D. Čepar, Z. Radalj, and B. Vovk, in Proceedings of the Sixth European Conference on Mathematics in Industry August 27–31, 1991 Limerick, edited by F. Hodnett (Vieweg+Teubner Verlag, 1992), European Consortium for Mathematics in Industry, pp. 103–106, ISBN 978-3-663-09835-5.

- King (2010) J. H. G. King, American Journal of Political Science 54, 561 (2010).

- Takens (1981) F. Takens, in Dynamical Systems and Turbulence, Lecture Notes in Mathematics, edited by D. A. Rand and L.-S. Young (Springer-Verlag, 1981), vol. 898, pp. 366–381.

- Hegger et al. (2000) R. Hegger, H. Kantz, L. Matassini, and T. Schreiber, Phys. Rev. Lett. 84, 4092 (2000).

- Verdes et al. (2006) P. F. Verdes, P. M. Granitto, and H. A. Ceccatto, Phys. Rev. Lett. 96, 118701 (2006).

- Casdagli (1997) M. Casdagli, Physica D 108, 12 (1997).

- McDowall (2002) D. McDowall, Criminology 40, 711 (2002).

- Greenberg (2001) D. F. Greenberg, Journal of Quantitatiûe Criminology 17, 291 (2001).

- Box-Steffensmeier et al. (2008) J. M. Box-Steffensmeier, J. Freeman, and J. Pevehouse, Modeling Social Dynamics (2008), http://www.empiwifo.uni-freiburg.de/freeman_files/TimeSeriesBookChp1.

- Pratt and Lowenkamp (2002) T. C. Pratt and C. T. Lowenkamp, Homicide Studies 6, 61 (2002).

- Makowsky (2006) M. Makowsky, Journal of Artificial Societies and Social Simulation 9 (2006).

- Malleson et al. (2013) N. Malleson, A. Heppenstall, L. See, and A. Evans, Environment and Planning B: Planning and Design 40, 405 (2013).

- Chiricos (1987) T. G. Chiricos, Social Problems 34, 187 (1987).

- Freeman (1983) R. B. Freeman, in Crime and public policy, edited by J. Q. Wilson (ICS, San Francisco, 1983), pp. 89–106.

- Levitt (2004) S. D. Levitt, Journal of Economic Perspectives 18, 163 (2004).

- LaFree (1999) G. LaFree, Annual Review of Sociology 25, 145 (1999).

- Farrell et al. (2011) G. Farrell, A. Tseloni, J. Mailley, and N. Tilley, Journal of Research in Crime and Delinquency 48, 147 (2011).

- Ouimet (2002) M. Ouimet, Canadian J. Criminology 44, 33 (2002).

- Marvell and Moody (1994) T. Marvell and C. Moody, Journal of Quantitative Criminology 10, 109 (1994).

- Marvell and Moody (1996) T. Marvell and C. Moody, Criminology 34, 609 (1996).

- Blumstein and Rosenfeld (1998) A. Blumstein and R. Rosenfeld, Journal of Criminal Law and Criminology 88, 1175 (1998).

- Kleck and Chirico (2006) G. Kleck and T. Chirico, Criminology 40, 649 (2006).

- Piehl (1998) A. Piehl, in The handbook of crime and justic, edited by M. Tonry (Oxford University Press,New York, 1998), pp. 302–319.