A Complete Method of Comparative Statics for Optimization Problems

(Unabbreviated Version)

Abstract

A new method of deriving comparative statics information using generalized compensated derivatives is presented which yields constraint-free semidefiniteness results for any differentiable, constrained optimization problem. More generally, it applies to any differentiable system governed by an extremum principle, be it a physical system subject to the minimum action principle, the equilibrium point of a game theoretical problem expressible as an extremum, or a problem of decision theory with incomplete information treated by the maximum entropy principle. The method of generalized compensated derivatives is natural and powerful, and its underlying structure has a simple and intuitively appealing geometric interpretation. Several extensions of the main theorem such as envelope relations, symmetry properties and invariance conditions, transformations of decision variables and parameters, degrees of arbitrariness in the choice of comparative statics results, and rank relations and inequalities are developed. These extensions lend considerable power and versatility to the new method as they broaden the range of available analytical tools. Moreover, the relationship of the new method to existing formulations is established, thereby providing a unification of the main differential comparative statics methods currently in use. A second, more general theorem is also established which yields exhaustive, constraint-free comparative statics results for a general, constrained optimization problem. Because of its universal and maximal nature, this theorem subsumes all other comparative statics formulations and as such represents a significant theoretical result. The method of generalized compensated derivatives is illustrated with a variety of models, some well known, such as profit and utility maximization, where several novel extensions and results are derived, and some new, such as the principal-agent problem, the efficient portfolio problem, a model of a consumer with market power, and a cost-constrained profit maximization model, where a number of interesting new results are derived and interpreted. The large arbitrariness in the choice of generalized compensated derivatives and the associated comparative statics results is explored and contrasted to the unique eigenvalue spectrum whence all comparative statics results originate. The significance of this freedom in facilitating empirical verification and hypothesis testing is emphasized and demonstrated by means of familiar economic models. Conceptual clarity and intuitive understanding are emphasized throughout the paper, and particular attention is paid to the underlying geometry of the problems being analyzed.

I INTRODUCTION

I.1 Résumé of Current Methods

Ever since Cournot (1838) proved that a profit maximizing monopoly would reduce its output and raise its price in response to an increase in the unit tax on its output, economic theorists have sought to examine the comparative statics properties of economic theories. The epitome of such comparative statics occurred in 1886 with Antonelli and in 1915 with Slutsky, when they independently showed that the comparative statics properties of the archetype utility maximization model are summarized in a negative semidefinite matrix, now known as the Antonelli and Slutsky matrices, respectively. But it was not until the publication of Samuelson’s (1947) dissertation that comparative statics became part of the economist’s tool kit. Samuelson (1947), building upon the pioneering work of Allen (1938), Hicks (1939), and others, formulated the following strategy for deriving comparative statics results associated with optimization problems: (i) assume the second-order sufficient conditions hold at the optimal solution and apply the implicit function theorem to the first-order necessary conditions to characterize the optimal choice functions, (ii) differentiate the identity form of the first-order necessary conditions with respect to the parameter of interest, and (iii) solve the resulting linear system of comparative static equations. This primal approach is indicative of most comparative statics analyses in economics to this day, and provides the general framework within which subsequent generalizations and refinements have been carried out. Indeed, despite several extensions of Samuelson’s (1947) basic analysis by subsequent authors, the treatment of comparative statics in textbooks and monographs (with the exception of Silberberg’s [1974] contributions, discussed below), as well as in most research work, essentially relies on his original framework and for the most part ignores the subsequent developments. This circumstance is partly a result of the desire for economy of presentation. But it is undoubtedly also a consequence of the fact that none of the later extensions and generalizations of Samuelson’s (1947) basic framework succeeded in arriving at a completely general, constraint-free semidefiniteness result involving the partial derivatives of the decision variables with respect to the parameters for the case of a constrained optimization problem. In fact the existing literature does not really contemplate the general existence of such an unrestricted result [see Silberberg, (1990)].

Our objective in this paper is to show that such a general result in fact exists, that the formalism for its construction is natural and grounded in intuition, and that the comparative statics results derived from it are sufficiently broad and powerful as to render it a worthwhile tool accessible to most economists. Indeed only one extra conceptual ingredient beyond Samuelson’s (1947) basic framework is needed in its construction, namely a clear understanding of the role of compensated derivatives in formulating a general comparative statics statement. This understanding in turn leads to a recipe for identifying a suitable class of compensated derivatives in terms of which the unrestricted semidefiniteness result for a general optimization problem is realized. Before delving into details, however, it is appropriate to briefly review a few highlights of the progress since Samuelson’s (1947) seminal work, partly with a view to the concepts and methods presented in this paper. It is also appropriate at this point to recall that the standard definition of definiteness or semidefiniteness for a matrix, to which we shall adhere, requires symmetry as a prerequisite (see §IIB for a definition).

Some twenty seven years after its inception, Samuelson’s (1947) primal method was significantly advanced and enriched by a new formulation of the problem. Silberberg (1974), building upon the work of Samuelson (1965), brought about the change by means of a clever construction that in retrospect seems quite natural. By changing one’s viewpoint of the optimization problem, that is, by simultaneously considering the set of parameters and choice variables of the original, primal problem as choice variables, Silberberg (1974) set up an excess optimization problem that simultaneously contained the primal optimization problem together with a dual optimization problem, hence the appellation primal-dual. Optimization of the primal-dual problem with respect to the original choice variables yields the primal optimality conditions, while optimization with respect to the parameters yields the envelope properties of the primal optimization problem as the first-order necessary conditions, and the fundamental comparative statics properties of the primal optimization problem as the second-order necessary conditions. Undoubtedly, the most important feat achieved by the introduction of the primal-dual method was the general construction of a semidefinite matrix that contains the comparative statics properties of the primal optimization problem. The most significant shortcoming of this method, on the other hand, is the fact that its final result is subject to constraints if the optimization problem is constrained and the constraint functions depend on the parameters.

A few years later, Hatta (1980) introduced the gain method to deal with a class of optimization problems that are essentially a nonlinear, multi-constraint generalization of the Slutsky-Hicks (basic utility maximization) problem. For unconstrained problems, the gain method is identical to the primal-dual method of Silberberg (1974). For constrained problems, on the other hand, the gain method yields constraint-free comparative statics results for the above-mentioned class of problems. This is accomplished by a procedure that amounts to applying the compensation scheme used in the standard Slutsky-Hicks problem (cf. §IIC), albeit in a generalized form. Similarly, the method avoids the use of Lagrange multipliers by a comparative scheme reminiscent of Silberberg’s (1974) primal-dual method, and in effect converts the constrained problem into an unconstrained one for the gain function. This procedure is in essence equivalent to the standard multiplier method, differing only in the manner in which the auxiliary functions are introduced. Otherwise, the flavor of the analysis with the gain method is similar to that of Silberberg’s (1974) primal-dual method. Hatta’s (1980) work represents a significant advance since it succeeded in overcoming an important shortcoming in the primal-dual method by deriving the first complete, constraint-free, comparative statics results for the above-mentioned class of problems. However, it has not spurred further progress in the subject, nor has it gained wide acceptance by workers in the field, primarily because its methods are not sufficiently general and lack a clear conceptual basis.

The methods described above, and indeed most any other comparative statics analysis, rely upon the differentiability of the primitives and solution functions of the optimization problem. The recent work of Milgrom and Shannon (1994) and Milgrom and Roberts (1994), on the other hand, breaks with that tradition of dealing with the local extrema of differentiable functions. These authors, in contrast, develop an ordinal method for comparative statics, where ordinality implies invariance with respect to order-preserving transformations. Milgrom and Roberts (1994) state the following properties in defense of the ordinal method: (i) it dispenses with most of the smoothness assumptions of the traditional methods, (ii) it is capable of dealing with multiple equilibria and finite parameter changes, and (iii) it includes a theory of the robustness of conclusions with respect to assumptions. It is clear that the ordinal method is intended to handle complications which lie outside the scope of differential comparative statics methodology. As such the ordinal method is an essentially different, and in certain ways a complementary, approach to comparative statics.

Before closing this section, it is appropriate to briefly review the use of compensated derivatives in differentiable comparative statics analysis. The interest in compensated comparative statics properties of economic models has its genesis in the Slutsky matrix of compensated derivatives of the Marshallian (or ordinary) demand functions. Research on compensated comparative statics properties of general optimization problems, however, is of a more recent origin. The best known contribution of this ilk is a set of three papers by Kalman and Intriligator (1973), and Chichilnisky and Kalman (1977, 1978), which introduced generalizations that actually predated the methods described above, albeit within a restricted framework. In particular, these authors emphasized the significance of compensated derivatives in the context of a general class of constrained optimization problems and established the existence of a generalized Slutsky-Hicks matrix for such problems. However, they did not succeed in establishing the crucial semidefiniteness properties of this matrix in general. Perhaps because their analysis was primarily concerned with establishing the existence of solutions using essentially primal methods, and because their comparative statics results were restricted to special forms, their work was largely superseded by subsequent developments. Similarly, their construction and use of compensated derivatives, although a significant advance toward a general method of dealing with constraints, was rendered in the same limited context and was not much pursued by others.

The last contribution to be mentioned here is the work of Houthakker (1951-52) which, while perhaps not as well recognized as the other post-Samuelsonian contributions mentioned above, actually predates them. In an attempt to quantify the role of quality in consumer demand, Houthakker (1951-52) clearly recognized the important role played by compensated derivatives, the large number of ways in which they can be constructed, and how they are related to a differential characterization of the constraints present in the problem, albeit in the context of specific examples. However, he only succeeded in deriving the desired semidefiniteness condition for a restricted class of problems, and his contribution did not lead to any significant development in the subject.

I.2 Generalized Compensated Derivatives

As mentioned before, the method presented here is based on the pivotal role played by compensated derivatives, and in effect unifies and generalizes the above-described formulations. As is often the case, this generalization leads to a conceptually simpler structure, while yielding a powerful method of deriving constraint-free comparative statics results. The basic idea originates in the observation that the natural parameters of a given optimization problem are not necessarily the most advantageous variables for formulating comparative statics results. This is plainly obvious in the Slutsky-Hicks problem where a linear combination of derivatives in the form of a compensated derivative must be employed in order to obtain the desired semidefiniteness properties. On the other hand, a linear combination of partial derivatives is, aside from an inessential scale factor, simply a directional derivative pointed in some direction in parameter space. Since an uncompensated (i.e., a partial) derivative is also a directional derivative, albeit a very particular one pointed along one of the coordinate axes in parameter space, it follows that the distinction between the two is merely a matter of the choice of coordinates in parameter space and has no intrinsic standing. Indeed a local rotation in parameter space, i.e., a rotation whose magnitude and direction may vary from point to point, can interchange the role of the two. Such a rotation is of course equivalent to adopting a new set of parameters for the optimization problem, suitably constructed as functions of the original ones. Clearly then, any general formulation of differential comparative statics must consider the possibility of choosing from this vastly enlarged class of directional derivatives in parameter space.

The question that arises at this juncture is whether there exists a universal criterion for choosing the compensated derivatives so as to guarantee the desired semidefiniteness properties free of constraints, and without requiring any restriction on the structure of the optimization problem. Remarkably, and in retrospect not surprisingly, there is a simple and natural answer to this question. One simply chooses the compensated derivatives in conformity with the constraint conditions, i.e., along directions that are tangent to the level surfaces of all the constraint functions at each point of the parameter space (for a given value of the decision variables). Equivalently, acting on the constraint functions, the compensated derivatives are required to return zero at all points of parameter space (for a given value of the decision variables). This requirement is in effect the ab initio, differential implementation of the constraints, as will become clear in the course of the following analysis. What is perhaps more remarkable, however, is that this procedure yields an operationally powerful, yet intuitively palatable framework that is capable of yielding varied and novel results, even in the case of unconstrained problems.

Before embarking upon the following development, it is worth identifying its main elements. The cornerstone of the analysis is Lemma 1 in §IIA, the main mathematical device is the generalized compensated derivative, also developed in §IIA, and the principal result of the analysis is Theorem 1 in §IIB. This is followed by several auxiliary developments and extensions, most of which are summarized in Theorem 2 and the Corollaries in §IIB and IIC. In §IID we establish a maximal extension of Theorem 1, a theoretically important result which implies all other comparative statics formulations. The method of generalized compensated derivatives is applied in §III to a number of models, some old and several new, where its power and flavor are illustrated.

II DEVELOPMENT OF THE MAIN RESULTS

This section is devoted to a detailed development of the main tools and results of the present method according to the ideas described above. Because the underlying structure of this method is simple and natural, we find it worthwhile to continue emphasizing the intuitive aspects of the analysis in the following development. It is our hope that a clear conceptual grasp of its basics will encourage its use among a wider segment of economists.

II.1 Geometry of Generalized Compensation

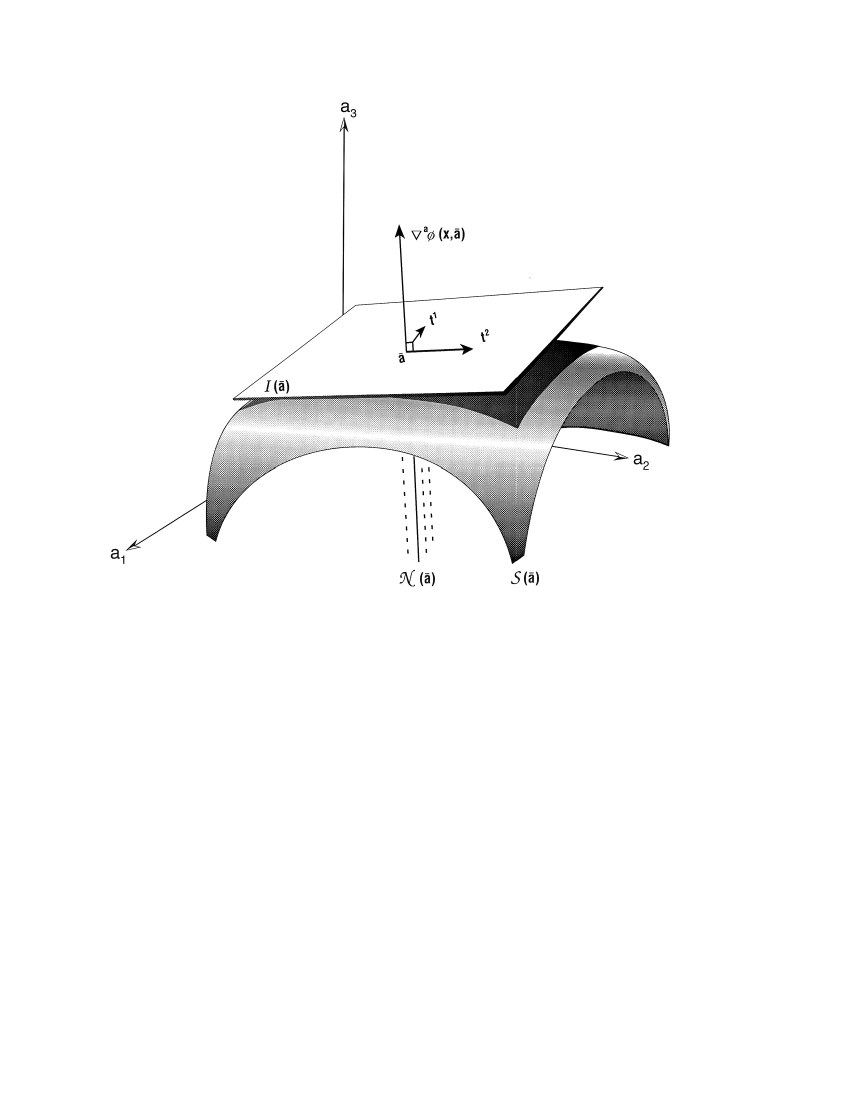

To convey a clear picture of how the ideas described in §IB are implemented, we find it helpful to describe the geometrical background involved in the construction of compensated derivatives in some detail. Let us first recall certain basic results from analysis. Consider a real-valued, continuously differentiable function defined for in some open subset of and in a subset of . This function will later be identified with an objective or constraint function, with the -dimensional vector representing the decision variables in the decision space, and the -dimensional vector representing a set of parameters in the parameter space . For most of this section, the dependence of on plays a secondary role in the discussion, so that it is useful to consider as fixed and as a continuously differentiable function defined on an open subset of . Throughout the paper, we will symbolize vectors and matrices both in “vector” and “matrix” notation, as in and , and in “component” notation, as in and . The inner product of two vectors and is denoted by . For a pair of matrices and , the product is denoted by . As for inner products between vectors and matrices, stands for the vector (column matrix) , stands for the vector (row matrix) , so that stands for the scalar .

Given a fixed value of , let be a point in and the -dimensional level surface of passing through , that is, the set of points in at which assumes the fixed value . In symbols, . Then the gradient of with respect to at point , denoted by , is a vector normal to at , and represents the direction of most rapid change for at that point. We shall denote this vector by and its normalized version by , where denotes the length of the vector . On the other hand, the hyperplane tangent to the level surface at , denoted by , is generated by the set of vectors that are tangent to at point , and represents the directions of no change for at . Note that is orthogonal to . In plain language, then, the normal vector represents the direction of maximum change, whereas the tangent hyperplane represents the directions of zero change, or the null directions. We shall refer to a vector in the tangent hyperplane as an isovector. Thus an isovector is any vector that points in a null direction. Together, the isovectors and the normal vector span all possible directions, thus providing a convenient local vector space at point of the parameter space. Figure 1 is an illustration of the structure just described in a three-dimensional parameter space, with and depicting two isovectors in the tangent hyperplane .

To define the geometric structure described above more generally, we first consider the vector space generated by the normal vector . While is a one-dimensional space in the present case, it will be generalized to higher dimensions in more general situations later, and can therefore be referred to as the normal hyperplane in general. Thus we have associated with each point of the parameter space a pair of orthogonal vector spaces and , the direct sum of which is the -dimensional local vector space referred to above. We will denote the latter by , and refer to it as the tangent space associated with point . This construction implies, among other things, that any real, -dimensional vector can be uniquely resolved into a pair of components, one lying in the normal hyperplane and the other in the tangent hyperplane.

If we now consider all points of as endowed with the tangent space structure just described, there emerges a configuration of local vector spaces covering all of . In terms of these local spaces, the differential structure of is essentially reduced to that of a function of one variable, namely the coordinate measured along the normal direction, since at a given point , the derivative of along any direction lying in the tangent hyperplane vanishes. We may summarize these results by saying that at every point , and for any direction specified by the (real, -dimensional) unit vector , (i) the decomposition , where represents the projection of onto the tangent hyperplane , is unique, and (ii) the directional derivative of at point in the direction is given by . The last property implies that if points in a null direction, i.e., if , then the corresponding derivative vanishes: . We shall refer to this condition as the null property of a directional derivative. Note that we have suppressed the dependence on in to avoid cluttered notation. Note also that the length of plays no role with respect to the null property, only the fact that it points in a null direction, or, equivalently, that it is an isovector. Thus if is an isovector of any length, then , so that possesses the null property as well. Observe that is a linear combination of partial derivatives, equal to . Since our primary focus is on the null property of this linear combination, we shall continue to (loosely) refer to as a directional derivative, overlooking the inessential scalar factor in doing so. We have thus arrived at the rather obvious conclusion that any directional derivative of a function in the direction of one of its isovectors has the null property with respect to that function.

This last property is the basis of our definition of compensated derivatives: Any linear combination of partial derivatives possessing the null property with respect to a function is a generalized compensated derivative (hereafter abbreviated as GCD) with respect to that function. To avoid trivialities, we shall exclude identically vanishing linear combinations from this definition. Thus any directional derivative in a null direction is a GCD, with the converse also holding except where vanishes. As an example, consider the case illustrated in Fig. 1 where and depict a pair of isovectors at point , which is located on the level surface of . For this case, then, the directional derivatives and are a pair of GCD’s with respect to . Their null property, on the other hand, is seen in Fig. 1to reflect the simple fact that the rate of change of a function is zero in directions tangent to its level surface. Moreover, the reason for making the null property a defining characteristic is the crucial fact that, when the GCD’s possess this property with respect to the constraint functions, the resulting semidefiniteness results emerge free of constraints. This basic result will be established in this and the following sections.

Although our construction has so far been limited to a one-dimensional normal hyperplane, we shall consider higher-dimensional normal hyperplanes in dealing with illustrative problems, where expressions involving the normal vectors and will be generalized to include a set of such vectors. Otherwise, the geometrical features discussed above, including the decomposition into normal and tangent components, remain unchanged.

Let us illustrate the construction of GCD’s by means of four basic economic problems. All but the third assume perfect information and are thus deterministic, while the third problem involves uncertainty as well as asymmetry of information between the transacting parties. In the first problem, the function is given by , where , , and is a fixed vector here. This is of course the generic form of the budget constraint that appears in the prototype utility maximization problem. Here the variables of interest are the parameters appearing in , identified according to . Then the normal direction is given by . Next, we must choose a set of vectors, all orthogonal to the normal direction just calculated, as a basis for the tangent hyperplane. A convenient choice is the set , , where the component equal to unity occupies the th position within the parenthesis. Note that these basis vectors are neither mutually orthogonal nor of unit length, but that they are all orthogonal to the gradient vector and constitute an independent set in the tangent hyperplane. Clearly, each is an isovector, so that the set of directional derivatives formed by taking the inner product possesses the desired null property with respect to and is therefore a set of GCD’s. Note that we have made the dependence of the GCD’s on the points of the decision space and of parameter space explicit in our notation, a practice which we shall henceforth follow. Remembering that here , one can easily derive the result . The latter is of course the compensated derivative that appears in the Slutsky-Hicks problem. It is worth noting here that (for ) any linear combination of will again yield a GCD. This fact corresponds to the infinite number of ways one can choose independent basis vectors in when , and already gives a hint of the generality of the present method, and as well of the diversity of the results it can generate. It is also worth noting here that the procedure described above and applied to this problem is not the only available method for constructing GCD’s, but one that reveals the underlying geometry most explicitly. Thus any procedure that yields a set of directional derivatives with the null property and such that the corresponding directions in the parameter space span the tangent hyperplane will suffice. Taking advantage of this freedom, we will in the following sections introduce simplified procedures for constructing the set of GCD’s for various applications.

While the above treatment illustrates the construction of a GCD for a constrained problem in the context of a well known model, our second problem will deal with an unconstrained model and will give an indication of the calculational novelty of the present method.

Consider , where . This is, except for the presence of the scale factor , the familiar function that describes the profit of a firm producing a single output from inputs under conditions of certainty and perfect competition; here is the vector of inputs, is a twice continuously differentiable production function, is the output price, and is the vector of input prices. Clearly, since the scale factor is stipulated to be positive, its magnitude does not affect the optimal values of the decision variables under profit maximization, nor does it have any effect on the comparative statics of the problem. In any case, will be treated as a parameter whose value will eventually be set equal to unity. It should be evident here that the scale factor serves an auxiliary purpose in this calculation and has no other purpose, even though there are economically meaningful interpretations of its role as will be discussed in §IIB.

Let the parameter set be identified as . Then , so that we find , where is the standard function describing the firm’s profit. Note that there are now parameters under consideration, so that . We can therefore choose the isovectors according to , , where the component equal to unity occupies the th position within the parenthesis, and . The corresponding set of compensated derivatives is easily found to be , , and . Note that each has the null property with respect to . Therefore these directional derivatives constitute a set of GCD’s for this problem and will be used in §IIIA to derive certain novel comparative statics results for the standard profit maximization model.

It is appropriate at this juncture to emphasize an important feature of GCD’s briefly mentioned earlier. While the customary meaning of compensation refers to a correction term that accounts for the effect of a constraint in the problem, the archetypical example being the correction for the income effect in the utility maximization problem, no necessary connection with constraints is implied in the case of generalized compensation, as is clearly illustrated in the profit maximization case treated above. Indeed any problem, constrained or not, will admit the use of generalized compensation if its parameter space is larger than one-dimensional. Furthermore, as the introduction of the scale parameter for the problem treated above shows, the parameter space can always be enlarged, so that the restriction to more than one dimension is really no restriction at all.

The next problem to be considered here involves multiple constraints. It is therefore appropriate to first generalize the notion of GCD’s to the case of a set of functions , , , each of which possesses the properties ascribed to in §IIA. To that end, consider a fixed value of , and let be a point in . Then the normal hyperplane is defined to be the vector space generated by the set of vectors , . Note that in case the normal vectors constitute an independent set, i.e., if the only solution to , where every is a real number, is for all , then the normal hyperplane will be -dimensional. The subset of the tangent space orthogonal to is then the tangent hyperplane as before. Note that when has dimension , i.e., when , then . The case of interest for economic problems usually corresponds to the condition (known in decision space as a constraint qualification condition) with . In any case, it should be emphasized here that what is needed for the construction of GCD’s is an independent set of isovectors which can be characterized as a set of independent, -dimensional vectors each of which is orthogonal to for every value of . Clearly, there is no need for an explicit construction of here.

Having established the generalization to the multiconstraint case, we now turn to the third problem illustrating the construction of GCD’s. This is the principal-agent problem with hidden actions (also known as moral hazard) where a firm, the principal, intends to hire an individual, the agent, to work on a certain venture on a contractual basis (see, e.g., Mas-Collel et al. 1995). We shall return to this problem in §IIIB, where we define and formulate the problem, then show that it can be transformed to the following convenient form:

Here , where , , , is the probability that the th profit level, , is realized for the firm given that the agent performs at effort level , with and corresponding to high and low effort respectively. The decision variable , on the other hand, is the agent’s compensation in case the th profit level is realized. Furthermore, , where is the agent’s disutility of working at effort level , is the market price of the agent’s services, and is the agent’s utility function. Finally, the parameters are a pair of positive auxiliary variables which are introduced for calculational convenience and will eventually be set equal to unity. The parameter set is thus identified as , with and , for a total of , to be eventually reduced to upon setting .

Rather than following the procedure used in the other illustrative problems of this section, here we shall develop an intuitive generalization of the GCD’s already constructed for the Slutsky-Hicks problem. We accomplish this in two steps. In the first step, we note that for each value of , the constraint is analogous to a budget constraint with standing for income, for the quantity of the th good, and the probability for the price of that good. This analogy immediately gives us the two-term structure , which is clearly compensated (i.e., possess the null property) with respect to the constraints involving . The second step is to amend this structure so as to extend the null property to the constraints involving . One can determine by analogy and verify by inspection that the addition of to the above structure provides the desired extension of the null property to the constraints involving without disturbing the same property with respect to the constraints involving . In short, the resulting structure, , has the required null property with respect to all constraints. We can thus define

as a set of GCD’s for our problem. We will use this set in §IIIB to derive comparative statics information for the principal-agent problem.

The fourth problem to be considered here is that of the Pareto-optimal allocation of a given bundle of goods to a number of individuals with given utility functions. We will treat this problem in full generality, primarily to illustrate the method for a case with multiple, nontrivial constraints. We shall assume here an appropriate set of regularity conditions (e.g., twice continuously differentiable, quasi-concave, strongly monotonic utility functions) such that the desired optimality condition can be formulated as a maximization problem subject to multiple constraints. Returning to the problem of allocating a resource bundle of goods, , , to individuals in a Pareto-optimal manner, we consider maximizing by an appropriate choice of the variables , , or equivalently , , subject to a set of constraints. These constraints are for , and for . Here is the utility function of the th agent, is a set of parameters, and is the fixed utility level of the th agent. Moreover, the set of parameters comprising the vector are identified as . We shall assume as given a continuously differentiable, interior solution to this maximization problem, and concern ourselves with the construction of the GCD’s for the problem.

As a first step in the construction of the GCD’s, we consider the normal vectors with components , . For , these components are given by for , by for , and they vanish for . For , the components of the normal vectors vanish for , and are equal to for . We can compactly rewrite these expressions as for , and for in a shorthand notation where denotes a -dimensional unit vector pointing in the th direction. The next step is the construction of a set of isovectors . There will be of these if the normal vectors are independent, which is the typical situation and will be assumed to be the case here. As in the case of the previous models, we can construct these by inspection. For example, we can choose, for , .

The set of compensated derivatives corresponding to the isovector set just constructed can be expressed as , . As usually formulated, the general Pareto-optimal allocation problem yields multiple solutions (the Pareto set). Consequently, additional conditions must be imposed in order to render the solution unique and comparative statics questions meaningful. Once this is done, the GCD set constructed above can be used to derive constraint-free comparative statics results for the Pareto-optimal allocation problem according to Eq. (7) of §IIB in a straightforward manner. Note that this GCD set does not involve the parameters , and that we would have arrived at the same GCD’s had we elected not to include the ’s in the parameter set in the first place. This is so since in any event the partial derivatives with respect to the remaining parameters and annihilate the resource constraint equations, i.e., they are already “compensated” with respect to the latter. This will always occur if (a) certain parameters are the only ones appearing in certain constraint equations, and (b) those parameters do not appear in any other constraint equations. Note also that the GCD’s just constructed were not compensated with respect to the objective function, i.e., does not vanish by construction. As we will show below, this property is not needed for obtaining constraint-free comparative statics results. The fact that this property was incorporated into the profit maximization problem treated above, on the other hand, was simply motivated by the calculational power that generalized compensation makes available for deriving various comparative statics results, as will be demonstrated in §IIC and in the applications.

Having demonstrated the construction of GCD’s for four basic economic models, we now resume the main development and proceed to establish the most important property of a GCD, namely its constraint conformance property mentioned earlier. To that end, we start by reversing the roles of and , consider the latter as fixed, and proceed to apply the construction developed above in parameter space to decision space. In particular, an isovector in decision space is an -dimensional vector which is orthogonal to all the normal directions associated with the set , i.e., , . If, moreover, some of the functions in the set, say those corresponding to , with , serve as constraint functions by virtue of the requirement that they must equal zero, then the corresponding isovectors in decision space are precisely those that conform to the constraints by virtue of pointing in directions that are tangent to the level surfaces defined by the constraints in decision space. The isovectors in decision space are therefore conforming vectors in this sense, and for that reason play a crucial role in the construction of the matrix that conveys constraint-free comparative statics results.

To make these assertions more transparent, let us now consider a restriction of the above constructions in the decision and parameter spaces to the case where the two vector arguments of the functions are functionally related. Specifically, let be a continuously differentiable function of , i.e., , and consider the restricted set of functions . In applications, the vector-valued function , which we shall refer to as a decision function, is derived from some optimality condition, subject to constraints if present. Such a constraint condition therefore implies that for and in some subset of . In other words, when restricted to , each function in the constraint set identically vanishes in the variable . To exploit this property, let us apply the now restricted parameter space GCD’s , henceforth abbreviated by , to the constraint identities. The result is that for all and ,

where , , and . However, owing to the null property of the GCD’s, the second term on the right hand side of the above equations vanishes, leaving behind the term involving the compensated derivatives of the decision functions. Note the appearance of decision space normal vectors in the surviving term of the above equation. Also note the introduction of a notational convention here whereby a subscript occurring to the right of a comma signifies partial differentiation, whereas a subscript occurring to the right of a semicolon signifies directional differentiation corresponding to a GCD. Moreover, Latin subscripts are used to denote differentiation with respect to decision variables, while Greek indices are used for differentiation in parameter space.

The surviving term in the last-stated equation above is in fact the inner product of with decision space normal vectors , so that its vanishing for every value of and implies the orthogonality of every generalized compensated derivative of to every normal vector associated with the constraint surfaces in decision space. Equivalently, the stated orthogonality implies the tangency of to the decision space surface (with fixed) for every value of and . We have thus established the fact that the application of parameter space GCD’s to the decision functions produces isovectors in decision space, i.e., vectors that conform to the constraints. It is useful to examine more closely how this crucial property of GCD’s emerges. Because the restricted constraint functions vanish identically in , and since a “small” change which points in a null direction induces no variation in arising from its dependence on the second argument, there cannot be any variation arising from the change in the first argument, , either. But the last statement characterizes as an isovector in decision space. Recalling that , we arrive at the desired result. This is the most important property of a GCD and, under the conditions stipulated above, may be summarized as

Lemma 1. Every generalized compensated derivative of a decision function conforms to the constraints in decision space.

We pause here to emphasize the profoundly dual nature of this result, as is already evident in the arguments preceding the statement of the lemma: a directional derivative which annihilates the constraint functions in parameter space, when applied to decision functions, will produce a vector which conforms to the constraints in decision space.

II.2 The Main Theorems

Having described the construction and properties of GCD’s in the previous section in some detail, we are now in a position to establish the main theorem of this paper. Consider the optimization problem

| (1) |

where are twice continuously differentiable with and . As stipulated above, and are points in decision and parameter spaces, respectively. To avoid trivialities, we shall furthermore require the set of constraint functions to be independent at the optimum point. This requirement implies that the set of parameter space normal vectors is linearly independent and the parameter space normal hyperplane is of dimension at the optimum point. It is a simple matter to show that this requirement also implies a parallel condition in decision space, the well known constraint qualification condition.

The task before us now is the establishment of the comparative statics corresponding to a given solution of the above problem. To that end, let us suppose there exists a unique, continuously differentiable, interior solution to the above problem specified by the (vector-valued) decision function . In other words, we suppose the existence of an open set in parameter space and a set in decision space together with a continuously differentiable function from to such that for each value of , the point is in the interior of and possesses the constrained maximum property stated in Eq. (1). Note that we have not included any inequality constraints, such as those arising from nonnegativity conditions imposed on decision variables, in Eq. (1) since the interior nature of the solution in effect obviates any such conditions.

In order to characterize the constrained maximum property of , we construct a set of GCD’s with respect to the constraint functions given in Eq. (1), possibly including the objective function as well, according to the procedure explained in §IIA. It is also useful to introduce the notation , where is an arbitrary vector of real numbers, is the number of GCD’s, and using the notation established in §IIA. According to Lemma 1 established above, conforms to the constraints in decision space for every value of . But then the same is implied for , since it is a linear combination of conforming vectors (recall that conforming vectors are elements of a linear space, the tangent hyperplane in decision space). By construction, then, the vector conforms to the constraints.

Using the above construction, we can use the maximum condition stated in (1) to assert that for any of sufficiently small magnitude, we have the condition

| (2) |

a statement that holds free of constraints. But then the arbitrary sign of in Eq. (2) can be used in conjunction with the differentiability property of to deduce that the directional derivative of in the direction of must be nonpositive as well as nonnegative, hence the result that it must vanish;

| (3) |

Eq. (3) is the constraint-free, necessary, first-order condition implied by the constrained maximum property stated in Eq. (1).

We next explore the consequences of the first-order condition just derived. This condition simply characterizes as being orthogonal to the tangent hyperplane in decision space, hence as belonging to the normal hyperplane in decision space. But the last statement implies that, for each value of , the gradient vector may be expressed as a linear combination of the normal vectors to the constraint surfaces in decision space. Since the latter are simply given by the gradients of the constraint functions in decision space, we find

| (4) |

The scalars that enter the linear combination on the right hand side of Eq. (4) are of course the familiar multipliers of Lagrange’s method of constrained maximization (with the negative sign inserted for convenience).

Thus far we have essentially established the validity of Lagrange’s method for dealing with constrained optimization problems using our construction. Having established that connection, we now recall the second-order, necessary conditions associated with the maximization problem of Eq. (1) (see, e.g., Mas-Colell et al. 1995; Takayama 1985). That condition states that for any conforming vector , i.e., any vector which satisfies the condition for every value of , we have the inequality

| (5) |

Since in the present instance the vector conforms to the constraints by construction, Eq. (5) would hold free of constraints if is substituted for . Recalling that is equal to , and remembering that the vector of real numbers appearing therein is arbitrary, we recognize in Eq. (5) the statement that the matrix

is positive semidefinite. The symmetry property of is a consequence of the symmetry of and , the latter following from the symmetry of the matrix of second-order partial derivatives for twice continuously differentiable functions. Let us recall here that a real matrix is by definition positive definite or semidefinite if (a) it is symmetric and (b) for every real vector , the quadratic form is positive definite or semidefinite respectively.

The above expression for can be rewritten by first applying a GCD, say , to Eq. (4), obtaining

| (6) |

If Eq. (6) is now multiplied by and summed over , the second term on the right hand side vanishes by the conformance property of that follows from Lemma 1 of §IIA, leaving a simplified expression for :

| (7) |

It is appropriate to recall here that the semidefiniteness property of implies that it is symmetric, i.e., , a fact that we have already used in writing Eq. (7) and will continue to utilize throughout this work. We have thus arrived at the result that the matrix , which is a linear combination of the partial derivatives of the decision functions with respect to the parameters, is positive semidefinite, free of constraints. We shall refer to a matrix possessing these properties as a comparative statics matrix (or CSM in abbreviated form) for the optimization problem. The unrestricted existence of a comparative statics matrix for a general, constrained optimization problem is the central result of our analysis:

Theorem 1. The constrained optimization problem defined by Eq. (1) et seq. admits of a constraint-free comparative statics matrix given in Eq. (7).

It is worth reemphasizing here that there is a large freedom of choice in the construction of CSM’s, a feature that will be explored in the following and summarized in Theorem 2. While this freedom may be exploited to generate different forms of comparative statics for a given optimization problem, it is well to remember that all such matrices convey no more information than is contained in the second-order, necessary conditions expressed in Eq. (5). These conditions in turn originate in the local concavity of the underlying constrained maximization problem defined in Eq. (1). A more intuitive discussion of these and related matters will be given at the end of §IIC.

Having established the main result of this paper, we now proceed to discuss how such features as the envelope and homogeneity properties are realized in the present framework. We will then consider the nonuniqueness features of our construction and develop a characterization of the associated arbitrariness in the resulting CSM’s.

As one might surmise, the null property of our GCD’s ensures that the envelope property holds for the general constrained optimization problem defined by Eq. (1) as a property of the optimized objective function and without the intrusion of constraint functions. To see this explicitly, let us start by introducing the value function , and observe that it is also equal to by the identical vanishing of the restricted constraint functions for all . Next consider the result of applying a GCD, say , to the value function as given by the second expression above. Then, using Eq. (4) and the null property , we find the desired result that , which is a statement of the envelope property in terms of GCD’s. Note that in case the GCD’s have the (optional) null property with respect to the objective function, i.e., if , then the envelope property reduces to the statement that , i.e., that the value function also possesses the null property. In other words, if the the null property of the GCD’s is extended to to the objective function, then the value function has vanishing derivatives in the null directions . Note that this condition is equivalent to a set of first-order partial differential equations satisfied by the value function. Needless to say, each of these is an invariance property of the value function.

Next we explore the consequences of any useful symmetry, or invariance property that the objective and constraint functions might possess. Consider the optimization problem defined by Eq. (1), together with the assumed solution , with . The task before us is to find out how a given invariance possessed by the objective and constraint functions of this problem, such as homogeneity of a given degree, gives rise to a corresponding property of the decision functions. To that end, let us start by characterizing the class of symmetries we would like to consider, limiting our attention to those invariances that are likely to play a significant role in economic applications.

Suppose there exist a pair of real, continuously differentiable vector functions and , from and to and respectively, and consider the differential operator defined by

Suppose further that the action of on the objective and constraint functions can be described by suitable functions, that is,

| (8) |

for every and . Here and are continuously differentiable functions from to , with , .

These conditions, obscure as they may appear, actually have a straightforward interpretation as invariance conditions. They essentially state that if the objective and constraint functions are evaluated at the “slightly” displaced values of their arguments and , instead of and respectively, where is a “small” real number, then the underlying optimization problem remains unchanged to first order in . Given a suitable uniqueness requirement on the solution function , this first-order invariance condition would imply that the modified objective and constraint functions define a solution that differs from the solution of the original problem only by quantities of second order in . In other words, they imply that the decision vector differs from the solution by second-order quantities only (Euclidean norm implied). The last statement can then be converted into the following invariance property for in the limit of vanishing : .

The heuristic argument given in the foregoing paragraph can be formalized in a straightforward manner. To do so, we start with the assumed invariance conditions obeyed by the objective and constraint functions, Eqs. (8), and proceed to differentiate these with respect to the decision variables. The result for the objective function is

where a prime signifies differentiation with respect to the argument. A similar equation results for each constraint function . Next we multiply the resulting equation for by , sum this over , and add the result to the above equation for in order to obtain an equation involving the partial derivatives of the combination , the Lagrange function associated with the optimization problem. Here, as elsewhere in this paper, the dependence of on the multipliers has been suppressed to avoid clutter in the notation. Since only partial derivatives of with respect to and will appear in our notation, the suppression of should not cause any confusion. Restricting the resulting equation for to the solution of the optimization problem by substituting for and using the first-order condition given in Eq. (4), we find

Similarly, restricting the assumed invariance condition for to the solution , we find . On the other hand, a differentiation of the th constraint equation with respect to leads to . Eliminating from the last two equations, we get

where . Note that the relation just derived is an orthogonality condition in decision space which identifies as a conforming vector. If the equation derived above for is multiplied by and summed over , we find, taking account of the conformance property of , the result

To develop this equation further, we differentiate the first-order condition given in Eq. (4) with respect to and use the conformance property of to rewrite the term as . Finally, using this last relation in the equation for , we arrive at the result

| (9) |

It is at this point that a local uniqueness condition must be imposed on the solution to insure the desired invariance property. To avoid inessential technical complications, we will assume here that the matrix is negative definite, a condition which is sufficient but not necessary. While it is common practice in textbook expositions to make this assumption throughout, we have only relied on the semidefiniteness of elsewhere in this paper. Given the stronger assumption then, we immediately conclude from Eq. (9) that must vanish, a conclusion which is equivalent to the invariance property we arrived at heuristically before [and incorporated in Theorem 2 as Eq. (16)].

To demonstrate the effectiveness of this invariance result, let us consider how it applies to the case of homogeneity, or scale invariance properties. Suppose the objective and constraint functions of a given optimization problem satisfy the invariance conditions given in Eqs. (8) with and . Then, according to Eq. (16), the solution to this problem will satisfy the invariance condition . This last condition characterizes as a homogeneous function of degree (via Euler’s Theorem). As an example of this, consider the problem of utility maximization treated in §IIA, where the underlying symmetry resides in the fact that a uniform inflation or deflation in income and all the prices has no effect on the consumption bundle demanded. Formally, this symmetry corresponds to the fact that the invariance conditions given in Eqs. (8) are satisfied by the objective (utility) and constraint (budget constraint) functions of the problem with and , hence . This characterizes the decision function as homogeneous of degree zero, in full harmony with the underlying symmetry; in symbols, . An even simpler case of scale invariance is one which we have already exploited, namely the introduction and use of the scale parameter in the basic profit maximization model in §IIA. This invariance can be interpreted in several economically meaningful ways. For example, one can consider the fact that the amount of revenues minus expenditures being maximized in that model may be expressed in various multiples of a given currency, or even in different currencies, and this should have no effect on the decision functions. Alternatively, one might interpret as a flat tax rate on profits and the objective function as the net profit of the firm, which again has no effect on the decision functions. Mathematically, on the other hand, one chooses and , so that and . Then the invariance conditions in Eqs. (8) are satisfied, and (with ) we have the result that , the obvious result. Other examples of the use of Eq. (16) will be considered in the applications.

Having dealt with the envelope and symmetry properties of the optimization problem defined by Eq. (1), we now proceed to study several structural features of , the general CSM constructed for that problem. The first question concerns the definiteness of , or more specifically, whether its rank is lower than its order, and if so, whether there exists an upper bound on this rank. Let us recall that we are dealing with decision variables, parameters, (independent) constraints, and a CSM of order defined by [the equation preceding Eq. (6)]

The task before us is to establish an upper bound for the rank of this matrix. Let us first emphasize that an upper bound is all that can in general be established, since the matrix that appears in the above equation can have an arbitrarily small rank, including zero, implying the same for . For example, for the optimization problem , the decision functions do not depend on the parameters at all, causing to vanish identically. This implies the vanishing of and its rank.

Let the rank of be denoted by . Then an upper bound to can be readily derived from the theorems that (a) the rank of an matrix cannot exceed , and (b) the rank of a product cannot exceed that of any of its factors. Now is a factor for , and its rank cannot exceed on account of the constraints, as an argument below will confirm. Therefore, the rank of cannot exceed the smaller of and , i.e., . To establish the rank property of the matrix just used, recall Lemma 1 of §IIA which states that each column of this matrix must conform to the constraints, i.e., for every value of , , . In other words, each of the derivative vectors is orthogonal to the normal vectors in decision space. Now if the constraints are independent, as we have assumed throughout, then the normal vectors constitute an independent set of dimension , forcing the derivative vectors to be linearly dependent and at most of dimension , since the sum of these two dimensions cannot exceed , the dimension of the decision space. We have thus established that when viewed as a matrix, can at most have linearly independent rows. But this implies that the rank of is no larger than , which is the desired result.

As a first example of the rank inequality formula established above, consider the profit maximization problem of §IIA where and . Here, we find , again implying that the full, CSM will be singular. However, if following standard practice one uses the submatrix of the latter corresponding to the partial derivatives of the input factors with respect to input prices, there will no longer be a necessary rank reduction. As a second example, consider the Slutsky-Hicks problem, also considered in §IIA. Then with , we have , implying that the Slutsky matrix is necessarily singular since its order exceeds its rank at least by one, a well known result. As a third example, we consider the allocation problem considered in §IIA, where , , and . The resulting CSM will have have a rank no larger than . As a typical situation, let us take . The corresponding CSM will then be of order and rank or less, and will not convey detailed comparative statics information about the optimum allocation levels since there are many more of these than there are rows in the CSM. Generally speaking, this state of affairs prevails when the dimensions of the decision and parameter spaces are widely different. Incidentally, with , one ends up with a highly redundant CSM with . It is appropriate at this point to emphasize that there may very well be further rank reductions of in specific cases resulting from the special properties of the objective function, and that the above result represents the rank reduction that is imposed by the underlying geometry of the GCD’s, independently of the specific properties of the objective function.

Our next task in this section is a characterization of the arbitrariness in the result of Theorem 1. Specifically, we must consider the problem defined by Eq. (1) et seq., and seek to classify and characterize all possible CSM’s associated with this problem. Note that we are taking the set of decision variables as well as the parameter set as given and fixed, thereby excluding from the present discussion the arbitrariness associated with these choices. It must be emphasized here that although ordinarily there is a “natural,” or “sensible,” choice of decision and parameter sets associated with a given problem, there does exist in principle the possibility of considering other sets constructed from the given ones, or even considering smaller or larger sets by, e.g., ignoring certain parameters as uninteresting or irrelevant and conversely augmenting the parameter set by introducing auxiliary parameters, or in the case of decision variables in a constrained problem, discarding a number of constraint equations by solving for a subset of the decision variables and conversely. Moreover, these alternative choices are not always mere mathematical curiosities devoid of meaning or use. Indeed we will exploit these extra degrees of freedom in our treatment of the models considered in §§IIIA and B, where the utility of the alternative choices of both the parameter and decision sets will be evident. However, as already stipulated, the following discussion will only consider the arbitrariness resulting from the choice of isovectors and GCD’s, relegating those corresponding to enlarging or contracting the parameter and decision sets to §III.

Let us recall, in connection with the problem defined by Eq. (1) et seq., that we defined and employed a complete set of GCD’s according to . Recall also that the set of isovectors , , is supposed to be linearly independent and span the tangent hyperplane (which is of dimension ). Consider now a different choice for the set of isovectors, , , with the same properties as , which must therefore have the same dimension . Since, by supposition, either set is linearly independent and spans the tangent hyperplane (viewed as a vector space), there must exist a nonsingular matrix of order that expresses the new set as a linear combination of the old, and conversely under the inverse matrix ; to wit, . The set of GCD’s corresponding to the new isovectors is related to the old set according to , with the inverse transformation effected by means of . The transformation rule between the corresponding CSM’s follows straightforwardly from that of the GCD’s. To wit,

| (10) |

where is the CSM constructed from the new isovector set and stands for the transpose of . Again, the inverse transformation from to exists and is implemented by . Note that according to Eq. (10), the two matrices and are congruent. As a pair of CSM’s, on the other hand, and are essentially equivalent in the sense that (a) the semidefiniteness of one implies that of the other, and (b) the two are of equal rank. Property (a) follows from the fact that the symmetry of implies that of , a fact which readily follows from Eq. (10), together with the observation that for every pair of real vectors and related by , the quadratic forms and are equal. Property (b) is a direct consequence of the nonsingular nature of the transformation matrix . Intuitively, properties (a) and (b) follow from the observation that each of the two sets of isovectors from which and are constructed forms a basis for the tangent hyperplane in the parameter space of the optimization problem, and as such must provide a description fully equivalent to the other. Following standard matrix nomenclature, we shall refer to a pair of CSM’s related according to Eq. (10) as a congruent pair. It should be pointed out here, however, that congruency does not imply similarity of properties as the two matrices can be quite different with respect to such matters as observability and empirical verification. An example of a congruent but rather dissimilar pair of CSM’s for the basic profit maximization model will be discussed in §IIIA.

Thus far we have only considered complete sets of GCD’s, i.e., those constructed from a set of isovectors which constitute a basis for the tangent hyperplane. At this point we shall relax the assumption of completeness and explore the consequences of a reduced or dependent set of isovectors. Specifically, we shall characterize the CSM’s that are constructed from such incomplete sets, thereby gaining further insight as to how several CSM’s, possibly of different order and rank, can provide comparative statics information about the same optimization problem.

Let us first deal with dependent sets of isovectors. Now a set of vectors is dependent if at least one member of the set is expressible as a linear combination of the rest. It is clear that GCD’s constructed from such sets will be redundant in the sense that at least one of them will be equal to a linear combination of the rest. Mathematically, this redundancy translates into the existence of a zero eigenvalue and a concomitant reduction of rank for the CSM (assuming full rank to start with). Clearly then, no comparative statics content is lost by discarding the redundancies until the isovector set becomes independent and none of the GCD’s is equal to a combination of the others. To restate this argument in quantitative terms, let us recall that a set of isovectors , , is dependent if there exists a set of scalars , not all zero, such that the vector represented by the linear combination vanishes. But this directly implies the vanishing of , hence also of , where and respectively represent the set of GCD’s and the CSM constructed from the isovector set . The vanishing of the last-stated sum verifies the claim that has a vanishing eigenvalue, hence a rank no larger than . Thus, carrying through the transformation process between the two sets of isovectors, GCD’s, and CSM’s as was done above, we arrive at the result that there exists a singular matrix , with the property , such that

| (11) |

Note that it follows directly from Eq. (11) that is a semidefinite matrix if is.

At this point one can discard a dependent isovector, i.e., one that can be expressed in terms of the others, and proceed to examine the remaining set for further linear dependences. It should be clear at this point that only redundant information is conveyed by means of dependent isovectors and GCD’s. This is essentially the reason for the stipulation that our isovector sets be independent. On the other hand, it must be emphasized that CSM’s resulting from dependent isovector sets and redundant GCD’s are nevertheless valid comparative statics statements, even though they are not optimally concise and may in fact fail to capture all the comparative statics information pertinent to the model in question.

The last remark returns us to the issue of completeness. Recalling that we are still dealing with the problem defined by Eq. (1) et seq., we proceed to contemplate a new, smaller set of isovectors , with , , and ; both sets are assumed to be linearly independent. Under these circumstances, we shall refer to as a contracted set and the transformation as a contraction. This transformation is implemented by a rectangular matrix of size : , . Continuing with the process of transformation as was carried out above, we arrive at the result that the matrix

| (12) |

is the CSM corresponding to the contracted set. Again one can show directly from Eq. (12) that is a semidefinite matrix. It is clear that the information conveyed by the contracted CSM is in general reduced relative to the original CSM. For example, if has full rank, then will be lower in rank by , hence lower in information content as well.

The last subject to be considered in this section is the effect of generalized transformations on the CSM. Here we are contemplating the possibility of defining new decision variables and parameters in terms of the old, essentially what amounts to a change of coordinates in the decision and parameter spaces. We shall require the transformation functions to be continuously differentiable with nonvanishing Jacobian determinants (in appropriate neighborhoods of the respective spaces) in order to insure a one-to-one mapping between the two sets of coordinates. While not as directly useful in applications as the specific ones considered above, these general transformations nevertheless provide a framework for contemplating a wide class of CSM’s associated with an optimization problem.

Consider the problem defined in Eq. (1) et seq. and the associated CSM in Eq. (7). Let us rewrite the latter in the generic form

This equation in effect defines the functions . Let us now consider a transformation to the generalized decision variables and parameters and , which are related to the original ones according to

| (13) |

where and . The transformation functions and are assumed to obey the regularity conditions stated above, so that the inverse transformations and exist and are continuously differentiable functions on and respectively. An application of the chain rule then leads to

| (14) |

as the transformed CSM. Here . These results clearly demonstrate that the freedom in deciding the complexion of the comparative statics information for a given optimization problem is essentially limitless. Whether any given complexion is useful or even meaningful for the problem at hand is an altogether separate question. We shall illustrate the workings of these general transformations in §IIIA and IIIB.

We close this section by summarizing the envelope, invariance, rank, and transformation properties established above.

Theorem 2. The following properties hold for the constrained optimization problem defined by Eq. (1) et seq.:

(i) The value function satisfies the envelope property

| (15) |

Furthermore, if the GCD’s possess the null property with respect to the objective function as well, the value function satisfies the stronger condition .

(ii) If the optimization problem satisfies the invariance conditions stated in Eq. (8), then the decision functions possess the invariance property

| (16) |

(iii) The rank of is no larger than the smaller of and , i.e., .

(iv) The matrix obtained from by means of the transformation , as in Eqs. (10)-(12), is semidefinite and constitutes a CSM. Furthermore, if is nonsingular, as in Eq. (10), then is equivalent to as a CSM, whereas if is singular, as in Eq. (11), or if is rectangular representing a contraction, as in Eq. (12), then has a rank lower than and may not be equivalent to as a CSM.

II.3 Further Developments

As mentioned in the Introduction, Samuelson (1947) established the foundations of comparative statics methodologies and Silberberg (1974) generalized and advanced that work to the point of constructing a semidefinite matrix conveying the comparative statics properties of a general optimization problem. However, Silberberg’s (1974) construction has a serious shortcoming in dealing with constrained optimization problems, namely, the subjection of the said matrix to the constraints. The construction described above and summarized in Theorem 1 removes this limitation in a general way. Naturally, this raises the question of just how this is accomplished, and the relation, if any, between the present method and that of Silberberg (1974). We will answer this question by deriving the result of Theorem 1 from that of Silberberg (1974).

To that end, let us recall Silberberg’s [1974, Eq. (10)] result as applied to the constrained optimization problem defined by Eq. (1) et seq. Stated in our notation, the result is the statement that the matrix

| (17) | |||||

is positive semidefinite, subject to constraints. Stated more explicitly, the latter qualification implies that for every real, -dimensional vector such that , , the quantity , or for short, is nonnegative. Restated in geometrical terms, the last statement implies that the quadratic form is nonnegative provided that the vector lies in the parameter space tangent hyperplane defined by the constraint functions. On the other hand, the isovectors , , possess this property by construction (given in §IIA), as does any linear combination of them. Let us consider then, for any arbitrary real vector , , the linear combination , and use this in place of in the quadratic form above. The resulting expression can in turn be viewed as another quadratic form composed of the symmetric matrix and the arbitrary vector . But then the arbitrary nature of permits one to conclude that is positive semidefinite. If the expression for given in Eq. (17) is now substituted in and the symmetry of the second-order partial derivatives of and are used, the parameter space partial derivatives in that expression turn into GCD’s by virtue of the identity . This causes the last term in the expression for to drop out of the resulting form by virtue of Lemma 1, leaving behind an expression that is found to be identical with the CSM matrix given in Eq. (7). This completes the deduction of Theorem 1 from Silberberg’s (1974) result.

Next we consider the work of Hatta (1980) referred to in the Introduction, and show that its main comparative statics result is in fact a special case of Theorem 1. The optimization problem treated by Hatta (1980), given in his Eq. (10), is a special case of our Eq. (1), and appears as

in our notation, where and are -dimensional vectors. The crucial property of this special form is the occurrence of the parameters in a separable, linear manner in the constraint equations, and their absence from the objective function. This special structure makes it possible to construct a set of GCD’s patterned after those customarily used for the Slutsky-Hicks problem (cf., §IIA or §IIIB), namely . Note that the parameter set here is identified as . Using these GCD’s in Eq. (7), we find the result that the matrix

is positive semidefinite. This statement is the same as Hatta’s (1980) Theorems 6 and 7, his main comparative statics results. Note that because of the special structure of the problem, compensation terms appear only in the partial derivatives of the decision functions, . These compensated derivatives are denoted by and termed “the Slutskian substitution matrix” by Hatta (1980), while the Lagrange multipliers are represented by in his notation. An examination of the manner in which the quantities are derived by Hatta (1980), on the other hand, reveals that they are constructed in conformity to the constraints, i.e., precisely according to the definition of our GCD’s, although this property is obscured by the presentation. Moreover, the method of their construction specifically relies on the special role played by the parameters and is therefore limited to the assumed form of the problem. This completes the discussion of how our method relates to the existing ones for dealing with constrained problems.

Next we turn to developing the results of Theorem 1 in more detail for certain generic forms that naturally arise within the context of economic problems. This will also allow us to introduce simplified variants of the construction methods given in §§IIA and B. The first such form arises in the case of unconstrained optimization, to wit, . As discussed in §IIA, it is expedient to deal instead with the modified problem , where , and where is viewed as the ()st parameter in the modified problem. Since the decision functions for these two problems must be the same, we have the statement that for the modified problem, so that we can use to denote the decision functions for both problems without any fear of confusion. Obviously, other quantities of interest in the original problem can be recovered from those of the modified version by setting the auxiliary parameter equal to unity.

An important advantage of introducing the auxiliary parameter is that it allows a natural choice of GCD’s, as well as a simple method of constructing them. The idea is to start with the set of partial derivatives and linearly combine each of these with in such a way that the application of the resulting combination to the (modified) objective function returns zero identically. Applying this prescription, one can readily construct the set of GCD’s given by , , where . This brute force method of constructing GCD’s will be referred to as the one-term compensation method. It is simple and direct, and will suffice when there is only one target function, such as in the present case, or the case of constrained optimization with only one constraint and no stipulation that the GCD’s have the null property with respect to the objective function of the problem. Needless to say, this already encompasses a number of important cases of interest in economic problems.

The next step is the construction of the CSM, using the GCD’s defined above by the method of one-term compensation. First, let us note that , and since the decision functions are independent of the auxiliary parameter. On the other hand, , . Restricting all of these expressions to the solution and substituting them in Eq. (7) while setting the auxiliary parameter equal to unity, we find, upon some rearrangement, the matrix

| (18) |

as a CSM for the original problem.

A useful variant of results upon carrying out the implied differentiations in Eq. (18) and using the first-order condition. However, it is more instructive to derive this variant directly from Theorem 1. To do so, let us recall that Theorem 1 requires the null property of the GCD’s only with respect to the constraint functions, leaving the same property with respect to the objective function as an option. Therefore, Theorem 1 can be applied to unconstrained problems provided that GCD’s are replaced with ordinary partial derivatives. This is because, for unconstrained problems, the null property required of the GCD’s with respect to the constraint functions is vacuously satisfied by ordinary partial derivatives. Therefore, we have a corollary of Theorem 1 stating that the matrix

| (19) |

is a CSM. This is the desired variant mentioned above, a form that also follows directly from Silberberg’s (1974) general theorem discussed earlier. Although Eqs. (18) and (19) are trivially related, it is useful to record them both since they do lead to different forms of CSM’s.

Corollary A. If in Theorem 1, i.e., in the absence of constraints, and given by Eqs. (18) and (19) respectively, are comparative statics matrices.