Bandwidth Selection In Pre-Smoothed Particle Filters

Abstract

For the purpose of maximum likelihood estimation of static parameters, we apply a kernel smoother to the particles in the standard SIR filter for non-linear state space models with additive Gaussian observation noise. This reduces the Monte Carlo error in the estimates of both the posterior density of the states and the marginal density of the observation at each time point. We correct for variance inflation in the smoother, which together with the use of Gaussian kernels, results in a Gaussian (Kalman) update when the amount of smoothing turns to infinity. We propose and study of a criterion for choosing the optimal bandwidth in the kernel smoother. Finally, we illustrate our approach using examples from econometrics. Our filter is shown to be highly suited for dynamic models with high signal-to-noise ratio, for which the SIR filter has problems.

Keywords: adaptive bandwidth selection; kernel smoothing; likelihood estimation; particle filter; state space model; variance inflation

1 Introduction

State space models are commonly used to represent dynamical systems in a wide range of scientific fields. For linear and Gaussian state space models, the Kalman Filter can be used to sequentially obtain the posterior mean and covariance of the current state vector, as well as the likelihood function required for estimation of model parameters. Gaussian mixture filters (Alspach and Sorenson, 1972) were among the first attempts to account for non-normality in the posterior, resulting from non-linearity, either in the state equation or in the observation equation. Later, sequential Monte Carlo (MC) based filtering methods, collectively known as particle filters, were introduced (Gordon et al., 1993; Kitagawa, 1996; Liu and Chen, 1998). The particle filter has the prospect of providing a sampling-based consistent estimate of the posterior distribution, but in many cases the sample size (number of particles) required to bring the MC error within tolerable bounds is prohibitively large. Consequently, there is now a large literature on improving the baseline particle filtering algorithms to work for a moderate numbers of particles. These include Pitt and Shephard (1999), various methods proposed in the chapters of Doucet et al. (2001) and more recently Polson et al. (2008), Chorin and Tu (2009) and Chopin et al. (2013).

Recently, a renewed interest in the use of particle filters for computing marginal likelihood (integrating over state variables) for the purpose of parameter estimation has emerged (Fernandez-Villaverde and Rubio-Ramirez, 2007; Andrieu et al., 2010; Kantas et al., 2009; Malik and Pitt, 2011; DeJong et al., 2013). This is also the context of the present paper. Similar to Malik and Pitt (2011) and DeJong et al. (2013) we obtain a likelihood approximation which is continuous in the parameters, hence facilitating numerical optimization. We target situations with highly non-linear state evolution, high signal-to-noise ratios, and with low-to-moderate dimensional state vector, for which adaptation is difficult.

Throughout, we assume that the measurement model is linear and Gaussian, which at first glance may appear restrictive. However, non-linear measurement equations with additive Gaussian noise can also be handled by a simple augmentation of the state vector, as shown in Section 3.1 below.

Let and denote the state vector and observation vector, respectively, at time , and define . In particle or ensemble methods the predictive density is represented by a random sample. We use a kernel smoother which can be updated analytically against a linear Gaussian measurement model . From the resulting mixture approximation of the posterior we draw a uniformly weighted sample of particles, which after a parallel run through the state equations, constitutes the approximation of the next predictive distribution . The resulting filter, which we call the Pre-Smoothed Particle Filter (PSPF) is a special case of the preregularized particle filter (Le Gland et al., 1998; Hürzeler and Künsch, 1998).

The main contribution of the present paper is to determine the optimal amount of smoothing in each updating step of the PSPF. This is done adaptively, i.e. for each time point an optimal bandwidth paramter is sought. For small the PSPF approaches the SIR filter, i.e. has low bias but high variance. Further, we correct for variance inflation (Jones, 1991), and hence when the kernel estimate reduces to a Gaussian density with mean and covariance calculated from the ensemble representation of . At this end of the spectrum the PSPF is strongly related to the Ensemble Kalman Filter (Stordal et al., 2011), which has low MC variance but high bias.

The rest of this paper is laid out as follows. Section 2 introduces notation and explains challenges related to particle filtering. Section 3 explains the pre-smoothed update and provides a method for automatic bandwidth selection. Section 4 introduces the PSPF, and also compares the PSPF to other particle filters using simulation experiments. Finally, Section 5 outlines two realistic applications, and Section 6 provides a discussion.

2 Model, Notation and Background

2.1 Model and notation

We consider a generic state space model consisting of a state transition equation and an observation equation, with the former given by

| (1) |

where is the state transition function

().

The random disturbance term , which can account for incomplete

model specification, may be either absent, of fixed dimension, or

of infinite dimension in the case that the state dynamics are governed

by a stochastic differential equation. Under the assumption that the

s are independent (1) describes

a Markov process, with transition probability density denoted

by . Given the realization of , evaluation

of typically amounts to solving a differential equation.

The system (1) is initialized by drawing

from a distribution with density . It is assumed

that and are sufficiently regular to ensure that is continuous, and thereby that all involved conditional distributions can be estimated consistently using kernel density estimators.

The observation equation is

| (2) |

where , is non-degenerate and the matrix is independent of the state, but may vary non-stochastically with time . Moreover, we use the notation , . denotes the multivariate Gaussian probability density function evaluated at , the identity matrix. Finally, we indicate which stochastic variable an expectation or variance is taken over using subscripts (e.g. when expectation is taken over variable ).

2.2 The SIR filter and sample impoverishment

This section introduces particle filters and the Sampling Importance Resampling (SIR) filter of Gordon et al. (1993), which is the limit of PSPF as . Any particle filtering approach relies on alternating between two steps: prediction (p) in which is represented by a random sample , and filtering (f) in which similarly is approximated by . These random samples of size are referred to as filter- and predictive swarms, respectively, and are updated iteratively from each other. The prediction step, used in both SIR and PSPF, consists of , where the are independent random draws from the distribution of . In the filtering step Bayes formula is invoked:

| (3) |

The SIR filter approximates (3) by performing a SIR update (Rubin, 1987), representing as a weighted sample with locations and corresponding weights

| (4) |

where is a normalizing constant. Obtaining a uniformly weighted sample to complete next time-step’s prediction is simply a matter of drawing multinomially from with weights (4). A byproduct of the SIR filter is that the marginal likelihood of needed for parameter estimation can be approximated as

| (5) |

for large (see e.g. Del Moral (2004, Proposition 7.4.1.)).

Sample impoverishment in the SIR filter occurs when, at time step , the predictive particle swarm and the data likelihood are poorly aligned (see e.g. Pitt and Shephard (1999)). The multinomial probabilities (4) then become very unevenly distributed, and the multinomial sampling will yield many repeated particles. Over time the swarm will degenerate in the sense that all particles can be traced back to a single particle in the initial swarm ( Sample impoverishment also increases the MC error of the likelihood estimator (5). This is likely to occur during numerical optimization of the likelihood, when the optimization algorithm tries an infeasible parameter value rendering the particle swarm and the data likelihood incompatible. The effect is amplified by a high signal-to-noise ratio in the system. Numerous strategies have been proposed for aligning (adapting) the predictive swarm to the coming observation (see e.g. Cappe et al. (2007) for an overview), but these typically rely on evaluation of (or some of the characteristics of ) which may be costly. The PSPF, on the other hand, avoids evaluation of , and relies only on the ability to simulate (1) efficiently.

3 The Pre-Smoothing Update

In this section we consider the pre-smoothing (PS) update, as an alternative to Rubin (1987)’s SIR update when the observation equation is linear in the state and additively Gaussian. Focusing on a single updating step we can drop the index in our noation. In a general perspective, the problem we address is the Bayesian updating problem of evaluating the posterior density and the marginal density when the prior is represented by a random sample. In particular, we focus on optimal selection of the smoothing parameter in the PS update, with the overarching objective of producing accurate estimates of . In Section 4 we again return to the filter setting.

3.1 The updating problem

Consider the evaluation of the posterior and marginal , for the model

| (6) | |||||

| (7) |

in a setting where is an unknown prior density, while and are given matrices. The available information about is a random sample drawn from . Our aim is to estimate both and for a given . We denote by and the empirical mean and covariance matrix of the sample , respectively.

Consider the shrunk kernel estimate (Jones, 1991; West, 1993)

| (8) | |||||

| (9) | |||||

| (10) |

where the smoothing parameter governs the proportions of the total variance under stemming from inter-kernel variance () and intra-kernel variance () in the Gaussian mixture (8). The replacement of the more conventional bandwidth parameter by simplifies certain expressions in what follows. The estimator (8) avoids the “variance inflation” to which the standard kernel estimator (Silvermann, 1986) is prone, as it is easily verified that the mean and variance under is and , respectively. For close to 1 ( close 0) behaves as a standard kernel estimator with equally weighted point masses located at as the limit. For () a Gaussian limit is obtained, i.e. .

By substituting for in the Bayes rule (3), we obtain the PS estimators

| (11) |

| (12) |

where

In our notation we have omitted the dependence on .

| Gaussian () | SIR () | |

| Property | High bias, low variance | Low bias, high variance |

As varies from 1 to 0 the PS updates moves from a SIR update to the Gaussian update, both of which are summarized in Table 1. The mean of each posterior mixture component concurrently moves smoothly from () toward what is dictated by the likelihood, reducing the potential for sample impoverishment. In the same vein, we have as , i.e. uniform weighting. These properties of the PS update (and the updates employed in other pre-regularized filters) differ from those of the update mechanisms employed in post-smoothed particle filters advocated by Musso et al. (2001) and Flury and Shephard (2009), where the (one step) posterior locations and weights are unchanged relative to the SIR. However, these latter approaches do not require the Gaussian data-likelihood which is underlying the PS update.

The fact that is a finite Gaussian mixture (for ) has a number practical advantages. Firstly, moments, marginal- and conditional distributions of the approximate posterior are easily derived from the representation (12). Further, has continuous support, and therefore direct copying of particles, which is applied in the SIR filter, is avoided in the resampling step. Sampling from is trivial. Moreover continuous (with respect to the parameters) sampling, resulting in a continuous simulated likelihood function, can be implemented.

The apparently restrictive linearity assumption (6) can be relaxed by augmenting the state variable . The case of a non-linear measurement function with additive Gaussian noise can be accommodated without any conceptual change to the framework. The measurement variance is then split in two parts and , , and the augmented state vector is where is an auxiliary variable introduced for convenience. For the augmented system, equations (6)-(7) take the form

where is the induced prior and is the matrix that selects from . Now, is a tuning parameter that must be chosen jointly with . Estimates of are easily obtained as a marginal in the finite mixture representation of . An application of this approach is given in section 5.2 below.

3.2 Criterion for smoothing parameter selection

A critical part of the PS update is the selection of the smoothing parameter, with the aim of obtaining both a representative posterior particle swarm and and accurate estimate of the marginal likelihood. For this purpose Flury and Shephard (2009) argue that the integrated mean squared error (MISE) of , which is commonly used in the kernel smoothing literature (Silvermann, 1986) is not a suitable criterion in a particle filter setting. Nevertheless, is has been used for pre- and post-smoothed particle filters by e.g. Le Gland et al. (1998); Hürzeler and Künsch (1998); Musso et al. (2001). Instead, Flury and Shephard (2009) propose to minimize the MISE of the posterior cumulative distribution function. We propose a third criterion, namely to minimize the mean squared error (MSE) of , which is given as

| (13) | |||||

This criterion has the advantage of being analytically simple, in addition to targetting minimal Monte Carlo error in the likelihood function as explained below. Minimization of gives an optimal bias-variance balance that depends on the observation .

Switching momentarily to a dynamical system setting (with ) for the reminder of this paragraph, estimates , and thus choosing (13) as the criterion targets directly the factors involved in the likelihood function (5). However, it should be noted in the dynamic setting that current period’s filter distribution must be represented accurately as it serves as an important input to next period’s likelihood evaluation. We show in section 4.2 that using an approximation to (which targets ) also leads to competitive estimates of the filtering distribution (i.e. ). This will in particular be true whenever most of the information carried in comes from the likelihood (which is typical for the class of models we consider) as is almost proportional to , and therefore the posterior estimator is relatively insensitive to the choice of smoothing parameter. On the other hand, assuming a concentrated observation likelihood, and in addition that is invertible (i.e. ), will be highly sensitive to the choice of smoothing parameter since a zeroth order approximation of is proportional to . Hence it appears sensible to choose even in a dynamic setting, in particular in high signal-to-noise situations.

3.3 Plug-in and approximation

There are two obstacles to direct use of the criterion as given in (13). First, the expectation is taken over which has unknown distribution (see (7)). The same problem occurs in standard kernel estimation, and is solved by the use of a plug-in estimator (Silvermann, 1986). The second problem is caused by the use of the shrunk kernel estimator, which involves the empirical (depending on ) quantities and through (9) and (10). Even if was known, analytical evaluation of the expectation in (13) would not be possible, and we have to resort to an approximation. Jones (1991) encounters the same problem, but argues that the effect can be ignored asymptotically when and . However, we consider the full range so the same asymptotic arguments do not apply. Instead we attempt to approximate the expectation (13) for finite .

We start by addressing the second problem. For the purpose of evaluating the mean and variance in (13) we replace and in expressions (8-11) by new random variables, and , respectively, both taken to be independent of . The simplification (approximation) lies mostly in this independence assumption, but also in the distributional assumptions made about and below. The reason that we cannot ignore the sampling variability in and is that the variance term in (13) would then be exactly zero for . Hence, for small we would underestimate the MSE of .

We make the following distributional choices

| (14) |

and

| (15) |

i.e. and are distributed as if they where calculated from a sample of iid vectors. Plug-in versions of (14) and (15), i.e. where has been replaced by and by , are used immediately below for notational convenience. Strictly speaking these replacements take place after all moment calculations have been carried out.

After these simplifications, it is necessary to restate our criterion

| (16) |

where expectation and variance now is taken relative to , and , which we emphasize are independent by assumption. Writing out the details of (16) we get where

| (17) |

with and .

The next sections outline pilot distributions and develop asymptotic approximations (in ) that will enable us to evaluate the mean and variance in (16).

| Expression | Interpretation |

|---|---|

| , | . |

| where . | |

| . | . |

| . | . |

| , | . |

| where and . |

3.3.1 Pilot distributions

For the variance term in , we employ for convenience a Gaussian pilot,

| (18) |

For the squared bias term in (16) a Gaussian pilot is ruled out because, as shown below, this leads asymptotically to zero bias for all . Instead a two-component Gaussian mixture

| (19) |

is used. The bias pilot is flexible, allowing for analytical

computations of moments, and

may be estimated from using an EM-algorithm (see e.g. McLachlan and

Peel, 2000, section 2.8 for details).

To minimize the computational burden we perform only a few EM-iterations,

and further computational savings are obtained by running the EM on

a subsample of when is large.

3.3.2 Practical squared bias

Under the above introduced simplifying approximations, and in particular under pilot density , we have that

| (20) | |||||

A closed form expression for is given in Table 2. The expectation over in (20) does not appear to have closed form, and we therefore employ the asymptotical (in ) mean statement of Corollary 2.2 of Iwashita and Siotani (1994) to obtain

| (21) |

where serves as the practical approximation to .

Note that in (27) depends on and is hence estimated using the pilot density needs to be estimated. Under the pilot density it has a closed form expression

| (22) | |||||

Finally, is taken as the practical squared bias term. Note in particular that it is easily verified that also the practical squared bias vanishes for , as in this case.

To underpin the claim that a non-Gaussian bias pilot is needed, we momentarily choose the parameters of so that coincides with , e.g. via , , , . Then whereas which shows that the practical bias would vanish as for all if a Gaussian bias pilot was employed.

3.3.3 Practical variance

The variance of , taken under pilot density , relies on the identity developed in Appendix A:

| (23) | |||||

where explicit expressions for are can be found in Table 2. As in the calculations leading to the squared bias, the expectations and variance over in (23) do not appear to have closed form expressions. Consequently we employ mean statement of Corollary 2.2 of Iwashita and Siotani (1994) to obtain

| (24) | |||||

The variance of in (23) is treated using the delta rule variance statement of Corollary 2.2 of Iwashita and Siotani (1994):

| (25) | |||||

Here, is the Jacobian matrix of up to a factor with explicit expression given in Table 2, and tr denotes the matrix trace. Combining (24) and (25) with (23) yields the practical variance approximation as

| (26) |

Finally, collecting the results obtained in (21), (22) and (26) yields the practical MSE approximation

| (27) |

which will be used throughout the rest of the paper.

3.3.4 Implementation

Given a prior sample , observation and matrices , , the location of one approximately optimal smoothing parameter involves the following steps:

-

1.

Calculate , from and estimate from (possibly a subset of) using a few iterations of the EM-algorithm.

-

2.

Compute using (22).

-

3.

Numerically minimize (27) with respect to , and return the minimizer as .

Our MATLAB implementation of the smoothing parameter selection procedure uses the built in function gmdistribution.fit for estimating and the minimization of is carried out using the fminbnd optimizer. Our corresponding C++ implementation uses routines similar to those provided in Press et al. (2007), section 16.1 (EM) and section 10.4 (minimization).

4 Pre-Smoothed Particle Filters

Equipped with an optimal one-step PS update, PSPF for accumulating the log-likelihood follows quite directly, and consists of the following steps:

-

1.

Simulate , set and .

-

2.

As for the SIR filter (section 2.2) set to obtain an approximate sample from .

-

3.

Compute optimal smoothing parameter using the algorithm given in section 3.3.4 with , and given by the model specification.

- 4.

-

5.

Sample from the posterior representation (12) to obtain an equally weighted approximate sample from .

-

6.

Set so that now approximates .

-

7.

If , set and go to step 2, else stop.

Various bias reduction techniques are available (see e.g. Shephard and Pitt (1997)) for computing the log-likelihood increment , but we do not employ those here in order to make comparisons easy. The PSPF has, like the SIR filter computational complexity . We have found that in practice the bottleneck in the PS update is actually fitting the prior pilot using the EM algorithm. Other, more problem specific pilots are conceivable, but we do not discuss this further here.

4.1 Continuous resampling

The resampling step obtains equally weighted particles from a finite mixture representation (12) of the filter distribution. Resampling is typically done by repetition of first drawing a component in the mixture, and subsequently sampling from this component. This process originates discontinuities in the simulated likelihood function, even if common random numbers are applied for repeated evaluation, and makes maximizing the simulated log-likelihood difficult. This issue was first addressed by Pitt (2002), who obtains continuous draws from a univariate mixture of point masses. For multivariate finite Gaussian mixture representations, Malik and Pitt (2011) provide an algorithm that may be used to as the resampling step in the PSPF for arbitrary (as the variance in each component of are equal). However for we have found algorithms based on computing on a fine grid using fast Fourier transform (FFT) methods and sampling from the corresponding CDFs desirable (more detailed descriptions are given in Appendix B). Like Malik and Pitt (2011)’s algorithm, these FFT-based algorithms have linear complexity in , but we find them easier to program and tune.

4.2 Comparison with other particle filters

To compare the proposed methodology with currently preferred particle filters, we carry out some simulation experiments.

4.2.1 Experiment 1

The first model we consider is is given as

| (28) | |||||

| (29) |

where denotes a matrix with each element equal to 1.

The distribution of is a Gaussian mixture consisting of three equally weighted components

, and

.

We consider each combination of dimensions and measurement error scales ,

The log-likelihood

is available via the Kalman filter by conditioning

on each component in the mixture, and therefore admit comparison

between the particle filter-based log-likelihood approximations and

the truth for this globally non-Gaussian model. We consider a short

time series so that the non-Gaussian features introduced

by the initial Gaussian mixture do not die out. The contending filters

are PSPF, SIR, Ensemble Kalman Filter (EnKF), and post- and pre-smoothed

regularized filters as described in Musso

et al. (2001). The latter

two are implemented using Gaussian kernels with bandwidth selection

based on the standard MISE-based plug-in formulas (Musso

et al., 2001, equation 2.3),

and are therefore referred to as MISE-Post and MISE-Pre respectively.

The above mentioned filters rely

only on simulation from the state equation, and are therefore directly

comparable with respect to scope. As additional references, we also

compare with Auxiliary SIR (ASIR, based on the mean of

as described in section 3.2 of Pitt and

Shephard (1999)) and a fully

adapted Auxiliary SIR (FASIR, Pitt and

Shephard (1999)). ASIR and

FASIR use knowledge of the mean of , and knowledge

of the full distribution of respectively, and are

therefore not directly comparable to PSPF with respect to scope. We

report in Table 3 the bias (loglike. bias), standard error

(loglike. std.dev.) and RMSE (loglike. RMSE) of the respective estimates

of across 10,000 data sets simulated from (28-29).

In addition, as a crude measure for comparing

the posterior simulation performance, we also

report the square root of the expected squared Euclidian distance between

the mean of and the simulated (filter RMSE).

We used for PSPF and for the other filters so

that the computing times for each filter are comparable when implemented

in MATLAB. The mean computing times relative to PSPF (relative CPU time)

are also reported in Table 3.

For all filters but EnKF, non-continuous resampling was

performed in each time step.

From Table 3, we see that PSPF produces smaller log-likelihood RMSEs then other filters that are based only on simulation of the state, except in the case where MISE-Pre has the smallest log-likelihood RMSE. However, assuming momentarily that the log-likelihood RMSEs are , it should be noted that even in case, the log-likelihood RMSE would be the smallest for PSPF if the same was applied. The log-likelihood performances of the PSPF and the EnKF are fairly similar, but it should be noted that the EnKF is not consistent, and therefore the biases cannot be eliminated. For increasing dimensions and fixed , PSPF and EnKF becomes more similar, which is a consequence of being chosen closer to 0 in the high- cases (to counteract the curse of dimensionality). SIR and MISE-Post perform poorly with respect to log-likelihood estimation in all the high signal-to-noise ratio () cases, and also in the moderate signal-to-noise ratio () cases for . MISE-Pre performs well in the cases, but the performance relative to PSPF deteriorates as grows.

The ASIR exhibit highly variable second stage weights, suggesting that the generic importance sampling density implicitly introduced works poorly for this model. As it is the optimal one step ahead particle filter, FASIR works extremely well in all cases, with log-likelihood RMSEs that are two orders of magnitude smaller than PSPF. Thus in the (not too often encountered) cases where full adaptation is possible, one should opt for the FASIR over the PSPF.

With respect to posterior simulation performance, PSPF produces filter RMSE results almost identical to those of FASIR, indicating that the posterior samples of PSPF are close to those of the optimal one step ahead filter. MISE-Pre also produces filter RMSEs close to those of FASIR, which underpins the claim made in Section 3.2 for this model, namely that the posterior estimator of pre-smoothed updates are relatively insensitive to the choice of smoothing parameter. In the same vein, the log-likelihood results of PSPF relative to those of MISE-Pre show that log-likelihood estimation is more sensitive to smoothing parameter selection and therefore targeting MSE() as is done here seems highly sensible.

| PSPF | SIR | EnKF | MISE | MISE | ASIR | FASIR | |

| -Post | -Pre | ||||||

| log-like. bias | -0.070 | -3.561 | -0.109 | -3.468 | -0.022 | -96.33 | 1.6e-5 |

| log-like. std. dev. | 0.303 | 27.49 | 0.418 | 24.82 | 0.328 | 27.55 | 0.006 |

| log-like. RMSE | 0.311 | 27.72 | 0.432 | 25.06 | 0.329 | 100.2 | 0.006 |

| filter RMSE | 0.014 | 0.017 | 0.014 | 0.017 | 0.014 | 0.017 | 0.014 |

| relative CPU time | 1.0 | 0.6 | 0.5 | 1.2 | 1.0 | 0.9 | 1.2 |

| log-like. bias | -0.293 | -1.6e3 | -0.356 | -1.6e3 | -0.572 | -1.5e3 | 9.0e-5 |

| log-like. std. dev. | 0.608 | 649.5 | 0.676 | 647.4 | 1.192 | 585.2 | 0.007 |

| log-like. RMSE | 0.675 | 1.8e3 | 0.764 | 1.8e3 | 1.322 | 1.6e3 | 0.007 |

| filter RMSE | 0.022 | 0.183 | 0.022 | 0.183 | 0.022 | 0.180 | 0.022 |

| relative CPU time | 1.0 | 1.1 | 1.2 | 2.4 | 1.7 | 1.6 | 2.1 |

| log-like. bias | -0.612 | -2.2e4 | -0.634 | -2.3e4 | -4.086 | -2.1e4 | -3.8e-6 |

| log-like. std. dev. | 0.813 | 4.6e3 | 0.798 | 4.6e3 | 2.540 | 4.3e3 | 0.008 |

| log-like. RMSE | 1.018 | 2.3e4 | 1.019 | 2.3e4 | 4.811 | 2.2e4 | 0.008 |

| filter RMSE | 0.032 | 0.674 | 0.032 | 0.674 | 0.032 | 0.671 | 0.032 |

| relative CPU time | 1.0 | 1.4 | 1.7 | 2.9 | 2.1 | 2.1 | 2.6 |

| log-like. bias | -0.066 | -0.024 | -0.104 | -0.019 | -0.013 | -16.53 | 3.5e-5 |

| log-like. std. dev. | 0.291 | 0.300 | 0.404 | 0.244 | 0.173 | 6.772 | 0.006 |

| log-like. RMSE | 0.299 | 0.301 | 0.417 | 0.245 | 0.174 | 17.86 | 0.006 |

| filter RMSE | 0.139 | 0.140 | 0.139 | 0.140 | 0.139 | 0.152 | 0.139 |

| relative CPU time | 1.0 | 0.8 | 0.5 | 1.5 | 1.0 | 1.0 | 1.1 |

| log-like. bias | -0.278 | -3.423 | -0.340 | -3.381 | -0.304 | -50.47 | 3.8e-5 |

| log-like. std. dev. | 0.597 | 4.510 | 0.671 | 4.420 | 0.761 | 8.899 | 0.009 |

| log-like. RMSE | 0.658 | 5.662 | 0.752 | 5.564 | 0.819 | 51.25 | 0.009 |

| filter RMSE | 0.220 | 0.244 | 0.220 | 0.244 | 0.221 | 0.258 | 0.220 |

| relative CPU time | 1.0 | 1.1 | 1.2 | 2.2 | 1.7 | 1.7 | 2.0 |

| log-like. bias | -0.584 | -131.2 | -0.611 | -131.6 | -2.694 | -129.2 | 7.6e-5 |

| log-like. std. dev. | 0.809 | 41.74 | 0.797 | 41.99 | 1.983 | 29.49 | 0.012 |

| log-like. RMSE | 0.998 | 137.7 | 1.005 | 138.1 | 3.345 | 132.5 | 0.012 |

| filter RMSE | 0.309 | 0.678 | 0.309 | 0.677 | 0.312 | 0.603 | 0.309 |

| relative CPU time | 1.0 | 1.4 | 1.7 | 2.7 | 2.1 | 2.1 | 2.6 |

4.2.2 Experiment 2

For the near-Gaussian model (28-29), the EnKF has a similar performance to PSPF. To further explore the difference between PSPF and EnKF, we consider a second simulation experiment that involves the non-linear model

| (30) | |||||

| (31) | |||||

| (32) |

where . The non-linear measurement equation is taken from a well-known test case used by e.g. Andrieu et al. (2010). In particular, such models are capable of generating bimodal filtering distributions as the sign of cannot be determined from observations . For the PSPF and EnKF filters to be applicable, we need to augment the state as indicated in section 3.1, namely

| (33) | |||||

| (34) | |||||

| (35) | |||||

| (36) |

where . The observation noise in (30) is for simplicity split evenly between (33) and (34).

| Method | PSPF | EnKF | SIR | PSPF | EnKF | SIR | |

|---|---|---|---|---|---|---|---|

| log like. bias | -0.188 | -0.437 | -0.094 | -0.098 | -0.437 | -0.044 | |

| log like. std. dev. | 0.815 | 1.426 | 0.605 | 0.546 | 1.426 | 0.387 | |

| bias | 0.042 | 0.137 | 0.021 | 0.024 | 0.137 | 0.011 | |

| std. dev. | 0.323 | 0.602 | 0.226 | 0.235 | 0.601 | 0.174 | |

| bias | 0.051 | 0.120 | 0.025 | 0.033 | 0.120 | 0.014 | |

| std. dev. | 0.396 | 0.464 | 0.350 | 0.321 | 0.464 | 0.264 | |

| bias | 0.028 | 0.053 | 0.015 | 0.025 | 0.053 | 0.013 | |

| std. dev. | 0.434 | 0.309 | 0.398 | 0.432 | 0.308 | 0.355 | |

| relative CPU time | 1.0 | 0.4 | 0.8 | 1.0 | 0.8 | 1.9 | |

We are unaware of any computationally feasible exact method for calculating and under either representation, and therefore resort to a SIR filter with 1,000,000 particles applied to representation (30-32) as the reference. We choose and relatively low autocorrelation and low signal to noise ratio to ensure that this reference method produces reliable results. Specifically, repeated application of the reference filter to a single simulated data set yields a standard error of the log-likelihood estimate on the order of 0.001 and the standard error of the estimated quantiles are on the order of 0.01 or better. The setup of the simulation experiment is as follows. The reference method, PSPF, EnKF and SIR (based on the representation in Equations 33-36) where applied to 10,000 simulated data sets. We report bias and standard deviation of the log-likelihood estimates relative to the reference method. Further, for each of the contending filters we compare the estimated -quantiles of () to the corresponding quantiles of the reference method, and report bias and standard deviation. We consider two situations where the PSPF has particles and the contending filters have particles. This ensures that the filters within each situation have similar computing times. The simulated data sets are the same in both situations. The results are reported in Table 4.

It is seen that the results for EnKF are close to identical when the number of particles increases, indicating that we incur substantial large- biases by applying the EnKF to this model, in particular with respect to log-likelihood evaluation and for the -quantiles. This is in contrast to PSPF, which as expected has diminishing biases and standard deviations as increases. Comparing PSPF to the SIR with (columns 1 and 3), it is seen that PSPF and SIR provide comparable results for comparable amounts of computing. Further, comparing PSPF in column 4 and SIR in column 3, where both filters have , it is seen that PSPF has a somewhat better log-likelihood performance whereas the filtering performance is roughly the same. This indicates that is a sensible criterion for choosing the smoothing parameter both for the purpose of filtering and likelihood evaluation, also for models with low signal to noise ratio.

5 Illustrations

Different aspects of PSPF are illustrated through two example models. In section 5.1 we consider a simple non-linear interest rate model with high signal-to-noise ratio, under which the PSPF is compared to other filters. The second model (section 5.2) is included to show that the PSPF can easily handle multiple states, and even non-linear measurement equations via augmentation of the state vector.

Throughout this section we refer to the quantity which is accumulated on step 7 of the PSPF algorithm (Section 4) as the simulated likelihood. Moreover we refer to the maximizer of the simulated likelihood as the (off-line) simulated maximum likelihood estimator along the lines of Malik and Pitt (2011). Throughout both examples, the simulated maximum likelihood estimator is located using a BFGS numerical optimizer and finite difference gradients. Statistical standard errors are approximated using the (finite difference) observed information matrix at the optimizer. We prefer this approach over methods based on accumulating the score vector (and possibly on-line optimization) at each time step (Kantas et al., 2009; Del Moral et al., 2011; Poyiadjis et al., 2011) as it is easier to program and adapt to new models.

5.1 One-factor interest rate model with micro-structure noise

The first example model we consider is the continuous time CEV diffusion,

| (37) |

of Chan et al. (1992), where denotes a canonical Brownian motion. We shall consider interest rate data available at daily frequency, and a yearly time scale, corresponding to observations at times where . We apply an Euler-Maruyama discretization of (37),

| (38) | |||||

It is well known that interest rate data are subject to micro structure noise at daily frequency and a common workaround is to use data at slower frequencies (see e.g. Aït-Sahalia (1999) who use monthly data). To enable the usage of daily data, we model the micro structure noise as being zero-mean Gaussian, i.e.

| (39) |

Equations (38) and (39) constitute state-space systems on the form (1-2) with , and parameter vector . Thus we may estimate the parameters using PSPF-based simulated maximum likelihood.

The dataset considered is one-week nominal Norwegian Inter Bank Offered Rate (NIBOR, in %, ) between Jan. 2nd 2009 and Nov. 23rd 2011 obtained from the Norwegian central bank’s website (http://www.norges-bank.no/). Table 5, lower panel, provides estimates and statistical standard errors based on the observed Fisher information. MC errors in both parameter estimates and standard deviation are evaluated across 50 different seeds for the random number generator. We use as we aim for MC standard errors of the parameter estimates on the order of 10% of the statistical standard errors.

| log-like | ||||||

| 2.084 | 1.314 | -0.970 | 0.104 | 1038.508 | ||

| (0.122) | (0.123) | (0.013) | (0.015) | |||

| 1.570 | 0.815 | -1.612 | 0.486 | -3.739 | 1050.607 | |

| [0.022] | [0.023] | [0.017] | [0.009] | [0.013] | [1.229] | |

| (0.389) | (0.397) | (0.176) | (0.114) | (0.100) | ||

| [0.007] | [0.008] | [0.001] | [0.001] | [0.003] | ||

Typical computing times to maximize a simulated log-likelihood are approximately seconds using a C++ implementation. Four EM iterations based on all particles were employed, with the EM computations distributed on 4 kernels of the 2010 laptop used for calculations.

To contrast with not accounting for micro structure noise, we also fitted the time-discretized CEV diffusion (38) directly to the data using maximum likelihood, and report the results in the upper panel of Table 5. Judging from the log-likelihood values, we find significantly better fit for the model accounting for noise, and the estimates for the volatility structure, i.e. and are significantly different. As the PSPF does not require the evaluation of transition probability densities , it is straight forward to apply more finely time-discretized versions of (37) to the data. We found the single step discretization (38) to be sufficiently accurate.

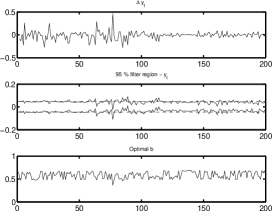

Figure 1 provides some diagnostic plots for and a randomly selected seed in the PSPF. There are no signs of sample degeneracy, as the filter density is well spread out during the whole time frame (and beyond). The fact that solid and dashed lines almost overlap suggests that the model has a high signal-to-noise ratio whereby most of the information in originates from . In the lower panel, it is seen that the PS update is closer to the parametric update in cases with large absolute returns , whereas less smoothing is imposed in easier cases corresponding to smaller returns.

As references for the PSPF, we also implemented FASIR, SIR and MISE-Pre for this model. To avoid the complications associated with obtaining a continuous simulated log-likelihood for these filters (Pitt, 2002), the reference filters where run with the parameters in Table 5, lower panel, and the figures reported below are across 100 replications. The mean and MC standard error of the simulated log-likelihood for FASIR with reads 1051.5 and 0.52 respectively, showing that the PSPF is fully capable of competing with specialized filters that exploit model-dependent structures. The SIR filter with obtains an expected log-likelihood 1016.9 and MC standard error of 7.3. Thus allowing for the finite bias in the likelihood intrinsic to the PSPF may be preferable over the highly variable but unbiased particle filter. Finally, the MISE-Pre filter with yields expected log-likelihood 1020.4 with a MC standard error of 6.9. This highlights the need for dynamic smoothing parameter selection for this model, even if pre-smoothing with conjugate kernels is employed.

5.2 Dynamic stochastic general equilibrium model

A renewed interest in particle filters in the econometric literature have at least partly been driven by the aim of estimating non-linear solutions to dynamic stochastic general equilibrium (DSGE) models (Fernandez-Villaverde and Rubio-Ramirez, 2007; Amisano and Tristani, 2010; Andreasen, 2011; DeJong et al., 2013; Flury and Shephard, 2011; Malik and Pitt, 2011). We consider a simple neoclassical growth DSGE model (King et al., 1988; Schmitt-Grohe and Uribe, 2004), with equilibrium condition given as

where denotes optimal consumption, is capital and is a positive productivity shock. A second order polynomial approximation (replicating Schmitt-Grohe and Uribe (2004)) to the solution process in the log-deviation from non-stochastic steady states , and is applied. The resulting system may be written in state space form with observation equation augmented with Gaussian noise

| (40) |

and state evolution , , where are quadratic forms in their arguments and .

As the observation equation (40) is non-linear in the state , we use the augmentation-of-state trick introduced in Section 3.1. Specifically we include an additional instrumental state to obtain a linear observation equation and set in our notation , , :

| (41) | |||||

| (42) | |||||

| (43) | |||||

| (44) | |||||

where , conform to . Thus (41-44) conform with the generic state space model (1-2) with and . In the computations, we fix to 0.05 to maintain some variation in state . We rely on a Maple script, called before each run of the filter, to compute the second order approximation. As is not used for prediction at time , it suffices to use the bivariate continuous resampling algorithm sketched in Appendix B for .

The structural parameters , , are kept fixed in simulation and estimation with values equal to those considered in Schmitt-Grohe and Uribe (2004) and the deprecation of capital is kept at . A simulated data set () is generated with the remaining parameters at , and is subsequently subject to simulated maximum likelihood analysis using the PSPF.

| log-like | log-like | |||||||

|---|---|---|---|---|---|---|---|---|

| 1.89 | -2.73 | -2.13 | 128.11 | 1.89 | -2.73 | -2.13 | 128.17 | |

| <0.01 | ||||||||

| (0.32) | (0.18) | (0.09) | (0.33) | (0.19) | (0.09) | |||

| <0.01 | <0.01 | <0.01 | <0.01 | |||||

Table 6 provides parameter estimates and statistical standard deviations, along with corresponding standard deviations due to MC error across 50 independent replications of the experiments. A typical computing time is 160 seconds to maximize a simulated log-likelihood for using our C++ implementation and 4 EM iterations distributed on 4 kernels of the 2010 laptop used. We consider two different swarm sizes, and , to assess the robustness of the results, and find only very small differences except for the obvious decreases in MC uncertainties for the larger swarm.

Malik and Pitt (2011) fit the same model using their (non-adapted) continuous particle filtering method, but their routine required “20000 particles to obtain robust results” for a somewhat shorter data set. They do not report MC standard deviations or the values of structural parameters they used, and therefore a direct comparison is difficult. However, it is clear that the PSPF requires one order of magnitude fewer particles to obtain robust results, which is very likely to justify the computational overhead of the PSPF.

As a further comparison we also implemented SIR and ASIR filters with and without augmentation of the state, namely targeting either (41-44) or (42-43) along with observation equation . The parameters are kept fixed at values given in Table 6. Firstly we find that the filters fares almost identically with and without state augmentation, which suggest that state augmentation comes at a small cost for this model. Secondly, ASIR based on fares much poorer than the standard SIR filter, which indicates that the simple generic importance density implied by this version of the ASIR has too thin tails and therefore more model specific adaptation is in order. Finally, for the SIR with (without) state augmentation we obtain a mean log-likelihood estimate reading 124.63 (124.61) and MC standard error in the log-likelihood estimate reading 0.38 (0.34) for across 100 replications. Therefore the SIR MC standard errors are of the same order as the PSPF while using 4-8 times as many particles.

We also observe that the log-likelihoods associated with the SIR are lower than the corresponding for PSPF, which indicate that the bias introduced by the PSPF is more material here than for the previous example. There are several explanations for this, with the most prominent being that filtering distribution is less constrained by the observation likelihood relative to the previous example, as in this case. This effect enables bias to build up over time. In addition, we observe that the kernel smoothing step of the PSPF introduces synthetic noise in the degenerate state transition (42) and thereby implicitly making the model more flexible, which may be contributing to the higher log-likelihood.

6 Discussion

In this paper we explore the pre-smoothed update and the resulting particle filter with a special emphasis on smoothing parameter selection. Through simulation experiments and real data studies, the pre-smoothed particle filter is shown to perform very well. In particular, we have shown that the somewhat heuristic choice of one time period as the criterion for choosing smoothing parameters also leads a competitive filter for many periods, both in terms of log-likelihood evaluation and filtering.

The PSPF borrows ideas from a number of sources, including the filter of Alspach and Sorenson (1972) and the subsequent literature, but differ in the use of a resampling step. In Alspach and Sorenson (1972) the mixture approximation of the posterior is propagated through the system, allowing a non-uniform distribution of the weights to evolve. The exact updating of finite Gaussian mixtures when the observation noise is additively Gaussian is due to Kotecha and Djuric (2003). More general Pre-smoothed filters employing MISE-based smoothing parameter criteria that are capable of handling more general observation equations via a rejection sampling algorithm are discussed by Le Gland et al. (1998); Hürzeler and Künsch (1998); Musso et al. (2001); Le Gland and Oudjane (2004); Crisan and Miguez (2014). Shrunk kernel estimates in particle filters with constant smoothing parameter were proposed by Liu and West (2001). The dynamic smoothing parameter selection that we advocate is most closely related to that of Flury and Shephard (2009), but their application was to a post-smoothed filter. The effect smoothing parameter choice in pre-smoothed filters is also considered in Le Gland and Oudjane (2004) and Crisan and Miguez (2014), but they target posterior simulation performance rather than likelihood performance. The PSPF also borrows ideas from particle-based high-dimensional ( large) data assimilation methods such as the Ensemble Kalman Filter (Evensen, 2003; Rezaie and Eidsvik, 2012) in that Gaussian updating formulas are used, but our focuses on potential applications and precision are very different.

A major advantage of the proposed particle filtering approach is that it is very easy to adapt to new models. The PSPF is not based on importance sampling, and therefore the need for problem-specific importance densities, and the potential for unbounded weight variance (Geweke, 1989), is mitigated. Provided an implementation of the PS update and smoothing parameter selection (C++ and MATLAB source code is available from the first author upon request), a user is only responsible for providing routines for simulating the state equation and specifying the observation equation. Implementation of the PS-update is also trivial when using a high-level language such as MATLAB. Our implementation in MATLAB used in section 4.2 amounts to a few dozen lines when using built in functions for minimizing and fitting prior .

One potential direction of further research is to assess the effect of the choice of pilots , . In the present work, we have focused on parametric pilots that lead to simple expressions for , and that require the least possible computational effort. However, any choices of finite Gaussian mixture pilots, including fully non-parametric pilots (see e.g. Wand and Jones, 1994) with Gaussian kernels, would lead to (more complicated) closed form expressions for . It would therefore be interesting to investigate whether adding more components to the pilots would lead to substantially better results when the cost of more complicated computation associated with such an approach are taken into account.

References

- Aït-Sahalia (1999) Aït-Sahalia, Y. (1999). Transition densities for interest rate and other nonlinear diffusions. Journal of Finance 54(4), 1361–1395.

- Alspach and Sorenson (1972) Alspach, D. and H. Sorenson (1972). Nonlinear bayesian estimation using gaussian sum approximations. Automatic Control, IEEE Transactions on 17(4), 439 – 448.

- Amisano and Tristani (2010) Amisano, G. and O. Tristani (2010). Euro area inflation persistence in an estimated nonlinear dsge model. Journal of Economic Dynamics and Control 34(10), 1837 – 1858.

- Andreasen (2011) Andreasen, M. M. (2011). Non-linear dsge models and the optimized central difference particle filter. Journal of Economic Dynamics and Control 35(10), 1671 – 1695.

- Andrieu et al. (2010) Andrieu, C., A. Doucet, and R. Holenstein (2010). Particle markov chain monte carlo methods. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 72(3), 269–342.

- Cappe et al. (2007) Cappe, O., S. Godsill, and E. Moulines (2007). An overview of existing methods and recent advances in sequential monte carlo. Proceedings of the IEEE 95(5), 899 –924.

- Chan et al. (1992) Chan, K. C., G. A. Karolyi, F. A. Longstaff, and A. B. Sanders (1992). An empirical comparison of alternative models of the short-term interest rate. The Journal of Finance 47(3), pp. 1209–1227.

- Chopin et al. (2013) Chopin, N., P. E. Jacob, and O. Papaspiliopoulos (2013). Smc2: an efficient algorithm for sequential analysis of state space models. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 75(3), 397–426.

- Chorin and Tu (2009) Chorin, A. J. and X. Tu (2009). Implicit sampling for particle filters. Proceedings of the National Academy of Sciences 106(41), 17249–17254.

- Crisan and Miguez (2014) Crisan, D. and J. Miguez (2014). Particle-kernel estimation of the filter density in state-space models. Bernoulli 20(4), 1879–1929.

- DeJong et al. (2013) DeJong, D. N., R. Liesenfeld, G. V. Moura, J.-F. Richard, and H. Dharmarajan (2013). Efficient likelihood evaluation of state-space representations. The Review of Economic Studies 80(2), 538–567.

- Del Moral (2004) Del Moral, P. (2004). Feynman-Kac Formulae. Springer.

- Del Moral et al. (2011) Del Moral, P., A. Doucet, and S. Singh (2011). Uniform stability of a particle approximation of the optimal filter derivative.

- Doucet et al. (2001) Doucet, A., N. de Freitas, and N. Gordon (2001). Sequential Monte Carlo Methods in Practice. Springer.

- Evensen (2003) Evensen, G. (2003). The ensemble kalman filter: theoretical formulation and practical implementation. Ocean Dynamics 53, 343–367.

- Fernandez-Villaverde and Rubio-Ramirez (2007) Fernandez-Villaverde, J. and J. F. Rubio-Ramirez (2007). Estimating macroeconomic models: A likelihood approach. Review of Economic Studies 74(4), 1059–1087.

- Flury and Shephard (2009) Flury, T. and N. Shephard (2009). Learning and filtering via simulation: smoothly jittered particle filters. University of Oxford, Department of Economics Discussion Paper Series.

- Flury and Shephard (2011) Flury, T. and N. Shephard (2011). Bayesian inference based only on simulated likelihood: Particle filter analysis of dynamic economic models. Econometric Theory 27(Special Issue 05), 933–956.

- Geweke (1989) Geweke, J. (1989). Bayesian inference in econometric models using monte carlo integration. Econometrica 57(6), pp. 1317–1339.

- Gordon et al. (1993) Gordon, N., D. Salmond, and A. Smith (1993). Novel approach to nonlinear/non-gaussian bayesian state estimation. Radar and Signal Processing, IEE Proceedings F 140(2), 107 –113.

- Hürzeler and Künsch (1998) Hürzeler, M. and H. R. Künsch (1998). Monte carlo approximations for general state-space models. Journal of Computational and Graphical Statistics 7(2), pp. 175–193.

- Iwashita and Siotani (1994) Iwashita, T. and M. Siotani (1994). Asymptotic distributions of functions of a sample covariance matrix under the elliptical distribution. The Canadian Journal of Statistics / La Revue Canadienne de Statistique 22(2), pp. 273–283.

- Jones (1991) Jones, M. (1991). On correcting for variance inflation in kernel density estimation. Computational Statistics and Data Analysis 11(1), 3 – 15.

- Kantas et al. (2009) Kantas, N., A. Doucet, S. S. Singh, and J. M. Maciejowski (2009). An overview of sequential monte carlo methods for parameter estimation in general state-space models. In 15th IFAC Symposium on System Identification, Volume 15.

- King et al. (1988) King, R. G., C. I. Plosser, and S. T. Rebelo (1988). Production, growth and business cycles: I. the basic neoclassical model. Journal of Monetary Economics 21(2), 195 – 232.

- Kitagawa (1996) Kitagawa, G. (1996). Monte carlo filter and smoother for non-gaussian nonlinear state space models. Journal of Computational and Graphical Statistics 5(1), pp. 1–25.

- Kotecha and Djuric (2003) Kotecha, J. and P. Djuric (2003). Gaussian sum particle filtering. Signal Processing, IEEE Transactions on 51(10), 2602 – 2612.

- Le Gland et al. (1998) Le Gland, F., C. Musso, and N. Oudjane (1998). An analysis of regularized interacting particle methods in nonlinear filtering. In M. K. Jiri Rojicek, Marketa Valeckova and K. Warwick (Eds.), Preprints of the 3rd IEEE European Workshop on Computer-Intensive Methods in Control and Signal Processing, pp. 167–174.

- Le Gland and Oudjane (2004) Le Gland, F. and N. Oudjane (2004). Stability and uniform approximation of nonlinear filters using the hilbert metric and application to particle filters. The Annals of Applied Probability 14(1), 144–187.

- Liu and West (2001) Liu, J. and M. West (2001). Combined parameter and state estimation in simulation-based filtering. In A. Doucet, N. de Freitas, and N. Gordon (Eds.), Sequential Monte Carlo Methods in Practice. Springer-Verlag.

- Liu and Chen (1998) Liu, J. S. and R. Chen (1998). Sequential Monte Carlo methods for dynamic systems. Journal of the American Statistical Association 93, 1032–1044.

- Malik and Pitt (2011) Malik, S. and M. K. Pitt (2011). Particle filters for continuous likelihood evaluation and maximisation. Journal of Econometrics 165(2), 190 – 209.

- McLachlan and Peel (2000) McLachlan, G. and D. Peel (2000). Finite mixture models. Wiley New York.

- Musso et al. (2001) Musso, C., N. Oudjane, and F. Legland (2001). Improving regularized particle filters. In A. Doucet, N. de Freitas, and N. Gordon (Eds.), Sequential Monte Carlo Methods in Practice. New York, Number 12 in Statistics for Engineering and Information Science, pp. 247–271. Springer-Verlag.

- Pitt and Shephard (1999) Pitt, M. and N. Shephard (1999). Filtering via simulation: auxiliary particle filter. Journal of the American Statistical Association 446, 590–599.

- Pitt (2002) Pitt, M. K. (2002). Smooth particle filters for likelihood evaluation and maximisation. Working Paper. University of Warwick, Department of Economics.

- Polson et al. (2008) Polson, N. G., J. R. Stroud, and P. Müller (2008). Practical filtering with sequential parameter learning. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 70(2), 413–428.

- Poyiadjis et al. (2011) Poyiadjis, G., A. Doucet, and S. S. Singh (2011). Particle approximations of the score and observed information matrix in state space models with application to parameter estimation. Biometrika 98(1), 65–80.

- Press et al. (2007) Press, W. H., S. A. Teukolsky, W. T. Vetterling, and B. P. Flannery (2007). Numerical Recipes 3rd Edition: The Art of Scientific Computing. Cambridge University Press.

- Rezaie and Eidsvik (2012) Rezaie, J. and J. Eidsvik (2012). Shrinked (1-) ensemble kalman filter and gaussian mixture filter. Computational Geosciences 16, 837–852.

- Rubin (1987) Rubin, D. B. (1987). The calculation of posterior distributions by data augmentation: Comment: A noniterative sampling/importance resampling alternative to the data augmentation algorithm for creating a few imputations when fractions of missing information are modest: The sir algorithm. Journal of the American Statistical Association 82(398), pp. 543–546.

- Schmitt-Grohe and Uribe (2004) Schmitt-Grohe, S. and M. Uribe (2004). Solving dynamic general equilibrium models using a second-order approximation to the policy function. Journal of Economic Dynamics and Control 28(4), 755 – 775.

- Shephard and Pitt (1997) Shephard, N. and M. K. Pitt (1997). Likelihood analysis of non-gaussian measurement time series. Biometrika 84, 653–667.

- Silvermann (1986) Silvermann, B. W. (1986). Density Estimation for Statistics and Data Analysis. New York: Chapman and Hall.

- Stordal et al. (2011) Stordal, A., H. Karlsen, G. Nævdal, H. Skaug, and B. Valles (2011). Bridging the ensemble kalman filter and particle filters: the adaptive gaussian mixture filter. Computational Geosciences 15, 293–305.

- Wand (1994) Wand, M. P. (1994). Fast computation of multivariate kernel estimators. Journal of Computational and Graphical Statistics 3(4), pp. 433–445.

- Wand and Jones (1994) Wand, M. P. and M. C. Jones (1994). Kernel Smoothing. Chapman and Hall, London.

- West (1993) West, M. (1993). Approximating posterior distributions by mixture. Journal of the Royal Statistical Society. Series B (Methodological) 55(2), pp. 409–422.

Appendix A Calculations related to the practical MSE

Appendix B Continuous resampling details

This section details algorithms for continuous (with respect to parameters) sampling from a finite Gaussian mixture when the variance of each of the component is equal. Both algorithms assume that the uniform random numbers applied are the same for each run of the algorithm.

B.1 Continuous resampling for

In the case where the state is univariate, we have found that our preferred re-sampling step consist of the following

-

•

Grid: Compute mean and standard deviation of the FGM representation of and initiate a -point regular grid containing say the mean 8 standard deviations. Typical values of are 512 or 1024.

-

•

PDF: Noticing that the variance in each component in is equal, the PDF may be computed using fast Fourier transform methods as explained thoroughly in Silvermann (1986), section 3.5 (with the modification that each particle weight is now and not ).

-

•

CDF: Compute the cumulative distribution function (CDF) of the approximate probability density function using a mid-point rule for each grid point.

-

•

Fast inversion: Sample based on stratified uniforms using the CDF-inversion algorithm provided in Appendix A.3 of Malik and Pitt (2011).

The total operation count of this algorithm is and thus is linear complexity in the number of particles retained also for continuous sampling.

B.2 Continuous resampling for

Also for , it is possible to use fast Fourier transforms to compute the posterior PDF at fine grid (say ) by doing the smoothing in the Fourier domain. Our implementation rely on the following steps

-

•

Sample first dimension: Sample from using algorithm for (the marginal is easily recovered from the finite Gaussian mixture representation of ).

-

•

Joint PDF: Compute at a fine grid using 2-dimensional fast Fourier transform methods and linear binning (see Wand (1994) for details).

-

•

Conditional CDFs: Compute the CDF of for each grid point in the -dimension from the joint PDF using a mid-point rule.

-

•

Sample : For each , sample using inversion sampling based on a linear interpolation of the -CDFs adjacent to .

The computational complexity is

,

i.e. linear in the number of particles.