Exact Simulation Pricing with Gamma Processes and Their Extensions

Abstract

Exact path simulation of the underlying state variable is of great practical importance in simulating prices of financial derivatives or their sensitivities when there are no analytical solutions for their pricing formulae. However, in general, the complex dependence structure inherent in most nontrivial stochastic volatility (SV) models makes exact simulation difficult. In this paper, we shall present a nontrivial SV model that parallels the notable Heston SV model in the sense of admitting exact path simulation as studied by Broadie and Kaya. The instantaneous volatility process of the proposed model is driven by a Gamma process. Extensions to the model including superposition of independent instantaneous volatility processes are studied. Numerical results show that the proposed model outperforms the Heston model and two other Lévy driven SV models in terms of model fit to the real option data. The ability to exactly simulate some of the path dependent derivative prices is emphasized. Moreover, this is the first instance where an infinite activity volatility process can be exactly applied in such pricing contexts.

Keywords: Exact Path Simulation, Asset Pricing, Gamma Processes, Generalized Gamma Convolution, Gamma Leveraging

1 Introduction

Financial models for underlying asset price processes are usually specified as stochastic differential equations (SDE) in the asset pricing context. These include the traditional bivariate diffusion SV models, eg Heston (1993) model, and the later popular SV models of Barndorff-Nielsen and Shephard (2001) (BNS hereafter), where the instantaneous volatility processes are modelled by Non Gaussian Ornstein-Uhlenbeck (OU) processes. The BNS models, due to their flexibility and relative simplicity, have steadily gained in popularity and are now well represented in the literature. See for instance the paper by Carr et al. (2003) and monographs of (Cont and Tankov (2003) and Schoutens (2003)).

The exact simulation of such underlying asset price models is of great practical relevance. This is especially true when we can use Monte Carlo simulation to generate an unbiased estimate of the price of a derivative security when there is no analytical solution to its pricing formula. By exact, we exclude such methods as the first order Euler discretization, which as pointed out for instance in Broadie and Kaya (2006) leads to extra bias and slows down the convergence rate of the estimator from to (Duffie and Glynn (1995)), where stands for the total computational budget. In particular, we mean obtaining exact sample paths of the state variables. However, in general, the complex dependence structure inherent in most non-trivial SV models makes this task difficult. A notable exception is the work of Broadie and Kaya (2006) who were able to exactly simulate the paths of the Heston model and its jump-diffusion extensions. Therefore, under the Heston model, the square root convergence rate of the simulation estimator (of eg option price) can be recovered. The Heston model arises by modelling the instantaneous volatility of asset price as a Cox-Ingersoll-Ross (CIR) process whose driving Brownian motion may be correlated with the price process, addressing the possible issue of leverage effect which refers to the phenomenon that volatilities and asset returns are negatively correlated. The simulation techniques used by Broadie and Kaya rely, in part, on the decomposition result of Pitman and Yor (1982) which are quite specific to the CIR process. However, as pointed out in Broadie and Kaya (2006) the sampling procedure which is based on the numerical inversion of a characteristic function is not without difficulties. In particular Glasserman and Kim (2011) proposes an approximation method that circumvents the use of characteristic function and hence, albeit not technically an exact simulation procedure, alleviate some these difficulties.

A natural question is: are there other price processes, which exhibit a great deal of flexibility, that can be exactly sampled? In this work, we shall demonstrate that a class of models within the BNS framework called BNS OU-Gamma SV model and its extensions is in parallel with the case of Broadie and Kaya (2006), allowing exact simulation. However, our exact sampling method is entirely different, and we believe much simpler, as it relies only on the simulation of a finite number of independent Uniform[0,1] and Gamma random variables. Moreover, it is important to mention that, although this is one member of the larger class considered by BNS, we show that, in relation to the Heston model, it is quite comparable, perhaps even better, in terms of model fit to the options market. After all, as we shall see in section 2.1, the Heston model is also a particular instance of a larger bivariate diffusion class.

First, we show that when the background driving Lévy process (BDLP) of the instantaneous volatility process, ie a Non Gaussian OU process, is specified by a Gamma process (with scale), the simulation based pricing method can be exactly implemented not only for financial derivatives that depend only on the marginal distribution of terminal asset price (eg European options), both without and with leverage effect, but also for such path dependent derivatives that depend on the joint distribution of asset prices at finitely many time points (eg Forward Start Options). The technical tool we use for the exact simulation is based on a most recently developed perfect sampling method of Devroye and James (2011) termed the Double CFTP (coupling from the past) method. To be specific, the problem of sampling asset prices under the BNS OU SV model is eventually reduced to that of sampling integrated volatilities (integrals of the instantaneous volatility process over non-overlapped time intervals) possibly along with the corresponding leverage increments which are BDLP increments due to the component of price process that is used to model the leverage effect. Under the BNS OU-Gamma SV model, these quantities are generalized gamma convolution (GGC) variables and admit independent decompositions that facilitate exact simulation. See for instance (Bondesson (1992) and James et al. (2008)) on GGC variables. The Double CFTP method is just designed for the exact simulation of this type of variables. This is the first instance where an infinite activity (infinite jumps over any finite time horizon) Non Gaussian OU process can be exactly applied in such pricing contexts. Notice that the exact simulation of the price model is trivial when the BDLP is compound Poisson which is not our interest here. Otherwise, as it is well known, under the BNS framework, an all purpose approach is to apply the infinite series representation method of Rosiński (1991). However, such issues as truncation of the infinite series representation, the slow convergence rate of the series and no explicit expression of the inverse tail mass function (section 5.2.2 of Schoutens (2003)) in general make the exact simulation difficult for those infinite activity cases. The difficulty arises generally from the nontrivial dependence either between integrated volatility and leverage increment or between integrated volatilities, which as far as we know can only be exactly tackled in the trivial compound case and the OU-Gamma case studied here. Moreover, as we mentioned earlier, in terms of fit of model to the same real option data set, we show in section 7.1 that the BNS OU-Gamma SV model outperforms both the Heston SV model and the other two BNS OU SV models studied by Nicolato and Vernardos (2003).

Second, we provide simulation methods for natural generalizations of the Non Gaussian OU process with Gamma BDLP to the case where the BDLP is a GGC subordinator, ie increasing Lévy process without drift that has a GGC marginal distribution, instead of Gamma process, since GGC subordinators include Gamma processes as special cases. Indeed, as shown in section 6.2, this extension does provide us more distributional flexibilities. This is due to the fact that GGC random variables can be represented as scale mixtures of Gamma random variables and hence have distributions that are quite different from the gamma distribution. In fact such random variables may possess heavy tails. We illustrate some simple examples in section 4.

The independence property that we exploit for the BNS OU-Gamma model is not available for the more general BNS OU-GGC models and hence, in general, we cannot implement an exact simulation procedure. However, in section 4.1 we show that if we modify slightly the framework presented in Barndorff-Nielsen and Shephard (2001) it is possible to obtain exact simulation for non-path based options. We refer to this modification as gamma leveraging. In section 4.3 and 5.2, we discuss highly accurate approximation methods for certain types of path based options.

The rest of this paper is organized as follows: We first give, in section 2, a general introduction to simulation issues related to pricing financial derivatives under both the bivariate diffusion SV model and the SV model of BNS type. In section 3, we demonstrate that a BNS type model, ie BNS OU-Gamma SV model, parallels the diffusion type Heston model in the sense of Broadie and Kaya (2006), admitting exact path simulation. GGC extensions to the OU-Gamma model are made in section 4. Superposition of independent OU instantaneous volatility processes are also considered in both sections 3 and 4. The Double CFTP exact sampling technique is introduced in section 5, where two approximation techniques are also discussed. Section 6 and 7 collect all the relevant numerical results while the algorithm of the exact sampler and some of the theoretical details are given in appendices.

Remark 1

It is well known that due to the presence of Brownian motion, the task of exactly simulating many SV models can be reduced to statements involving the simulation of a joint distribution consisting of an integrated volatility and instantaneous volatility. This is the case for the Heston model, the general BNS OU class of models, among many others. However what is crucial is to be able to develop an efficient method to exactly sample from the complex joint distributions involving the volatility components. So far the only non-trivial case where this has been achieved is the Heston model. Here we show by quite different sampling techniques that this can also be applied to the BNS OU-Gamma model.

Remark 2

This paper aims at devising exact simulation technique for pricing derivatives whose underlying asset follows a nontrivial BNS OU type SV model that parallels the Heston model. On the other hand, semi-closed expression is available for the price of an European option under Heston model (see Heston (1993)) and two other BNS OU type models, ie the case where the Non Gaussian OU volatility process has a Gamma marginal distribution (compound case) and the case where the volatility process has an Inverse Gaussian (IG) marginal (see Nicolato and Vernardos (2003)). These semi-closed price formulae are derived using the inverse Fourier transformation idea that involves corresponding terminal log asset price’s characteristic function, whose exponent consists of only elementary complex functions that facilitate the numerical computation, see Schoutens (2003) pp.87-91 for detailed examples and Carr and Madan (1999) for the computational method Fast Fourier Transformation (FFT). However, under the BNS OU-Gamma/GGC models in this paper, the exponents of characteristic functions consist of nontrivial complex functions (involving even multiple integration of complex functions that need to be evaluated numerically in addition to FFT) that make the implementation of transformation method difficult. See Zhang (2010) pp.93 for the general characteristic function formula for OU-GGC model.

2 Simulating derivative prices under different SV models

We shall consider the problem of pricing a financial derivative with a general discounted payoff function where is the underlying asset price process given by certain price model. Based on the fundamental theorem of asset pricing, the no-arbitrage price of the derivative is given by the expected discounted payoff under the risk neutral measure, ie Whether this expectation can be explicitly evaluated depends on the complexity of both the underlying asset price model and the payoff function . Notice that in the sequel, we shall always assume that we work with the risk neutral measure (or interchangeably, the equivalent martingale measure) unless otherwise stated.

Under such simple models as Black-Scholes (BS) model, the derivative price is usually explicitly and easily evaluated. However, there is strong empirical evidence of stochastic volatility, see for instance (Shephard (1996) and Ghysels et al. (1996)), which reflects the deficiency of BS model in describing the underlying asset prices and hence in pricing financial derivatives, since BS model assumes a constant volatility. SV extensions are made to the BS model to circumvent its shortcomings. Under most of those SV models, the evaluation of the above expectation is much more involved and nontrivial anymore. Monte Carlo simulation method could be the choice whenever the underlying price model or the payoff function is so complicated that analytical evaluation is formidable. The idea is simple, given that we can simulate exactly (if possible) i.i.d. copies of ie then the derivative price, ie can be estimated by the following Monte Carlo average

The estimate converges to the true value as by the law of large numbers.

In order to make the problem considered tractable enough, throughout, we shall only consider two types of derivatives with the following discounted payoff functions

- (i)

(path independent)

- –

eg European Call Option with discounted payoff “”, where is the strike price and is the constant risk-free rate.

- (ii)

(path dependent) for

- –

eg Forward Start Option with discounted payoff “”, where determines the magnitude of floating strike.

It is readily seen that type (ii) derivatives involve underlying asset prices at finitely many time points while type (i) derivatives depend on only the terminal asset price. As we shall see later, this difference matters a lot when we present simulation issues under the BNS OU SV models.

The rest of this section is devoted to a general introduction of two different types of SV models and their simulation issues related to the above pricing problem.

2.1 Bivariate diffusion SV model

A rather general bivariate diffusion type continuous time models for the underlying asset price process are specified under the risk neutral measure by the following SDE’s:

| (1) |

where is the risk free rate, is the dividend yield, is a standard Brownian motion, is the underlying instantaneous volatility process that describes the fluctuation of stock price over time, is another standard Brownian motion that may be correlated with as we shall see later and , , and are positive parameters. The volatility processes given by (1) are called constant elasticity variance (CEV) processes and also used as short-rate model by Chan et al. (1992). When and , (1) reduces to the GARCH diffusion process of Nelson (1990) and the popular CIR process of Cox et al. (1985) respectively. See also Meddahi (2002).

When , we arrive at the popular Heston (1993) SV model. The following is a typical specification for the price and volatility processes under the Heston model:

| (2) |

Here and are two independent standard Brownian motions, are positive parameters with for never hitting zero (staying positive in other words) and is the parameter that characterizes the leverage effect or co-movements between the price and volatility processes. To be precise, is the instantaneous constant correlation between the driving Brownian motion of price process, ie , and that of the volatility process, ie . Suppose that we are at time and the future time is of our concern. Applying stochastic exponential, one can solve for the price of (2):

| (3) |

Simple stochastic integration gives:

| (4) |

Broadie and Kaya (2006) proposed an exact simulation method for sampling from the transition distribution of price process under the Heston model (2), ie , and hence for sampling from the finite dimensional distribution of the price process, ie for . Denote

that is called integrated volatility over time interval . The basic simulation steps of Broadie and Kaya (2006)’s approach can be listed as follows

- Step 1.

Sampling that follows a non-central Chi-squared distribution;

- Step 2.

Sampling ;

- Step 3.

is easily recovered through (4);

- Step 4.

Conditional on all the above quantities, is log-normally distributed.

Broadie and Kaya (2006) realizes that the key difficulty arises in Step 2 and proposes a sampling method that is based on inverting the related characteristic function using FFT. This approach is not without any difficulty; see Glasserman and Kim (2011) for more discussions and an alternative simulation procedure under the Heston model.

Remark 3

In Step 3, we notice that, due to the square root specification of CIR processes, term that appears as leverage effect in (3) can be recovered through (4). This fact facilitates the exact path simulation for Heston model. For other more general specifications (1) of when exact simulation is much more involved and nontrivial. Notice that CIR process is a particular instance of a larger class (1) of instantaneous volatility models.

2.2 BNS OU SV model

Continuous time SV models are not limited to be of the bivariate diffusion type. Barndorff-Nielsen and Shephard (2001) proposes another type of SV model that is termed BNS OU SV model, where the instantaneous volatility process is modeled by a Non Gaussian OU process rather than a diffusion process. The change of measure argument of Nicolato and Vernardos (2003) guarantees that the usual BNS OU SV model of Barndorff-Nielsen and Shephard (2001) with leverage effect can be specified under the risk neutral measure as:

| (5) |

Here is the asset log price, the parameter characterizes the leverage effect and controls the persistent rate of the instantaneous volatility process . Here follows a Non Gaussian OU process driven by a subordinator (Lévy process that has positive increments without drift) . Notice that

Here is the Lévy density of the BDLP . Models in physical measure and equivalent martingale measure can be of the same type if the change of measure is structure preserving. In the sequel, we shall assume the change of measure is structure preserving and work with this risk neutral measure. See Nicolato and Vernardos (2003) for more details on this. Next, we show how simulation works under the BNS OU SV model. We discuss the path independent and dependent cases and their differences under the BNS framework.

Path independent case:

First, for the path independent case, the basic problem is the exact sampling from the distribution of for some . It is easy to see that the distribution of is Normal with mean

| (6) |

and variance conditional on , and From Barndorff-Nielsen and Shephard (2001) (see also Nicolato and Vernardos (2003)) we have that:

| (7) |

Hence the problem reduces to how to produce exact i.i.d. samples of the following random pair

| (8) |

Notice that the first element of (8), ie leverage increment, is from the leverage effect while the second element is due to the integrated volatility (7). The corresponding simulation algorithm is

- Step 1.

Sampling the random pair (8);

- Step 2.

- Step 3.

Sampling Normal with mean and variance to get .

Path dependent case:

Second, for the path dependent case, the basic problem is the exact sampling from the distribution of for . The difference from the path independent case is realized as follows. Generating can be performed the same way as in the path independent case. However, from to and so on, we need to condition on in order to generate and so on. Denote and for The simulation issue for the path dependent case effectively reduces to how to sample exactly from, in addition to the leverage increment of (8), the series specified by the following two dimensional AR(1) equation (see section 5.4.3 of Barndorff-Nielsen and Shephard (2001)):

| (19) |

Here

| (24) |

and s are independent. The simulation algorithm in this case is, for

- Step 1.

Sampling the random pair and noticing that serves also as the leverage increment, ie the first element in (8);

- Step 2.

- Step 3.

Sampling Normal with mean and variance to get .

Remark 4

Although the increment may be the same for both random pairs (8) and (24), notice that they come from different parts of the BNS OU SV model. For (8), the increment comes from the leverage component of the asset price process, while the increment of (24) comes from the BDLP that drives the instantaneous volatility process. They coincide when the leverage component agrees with the BDLP.

In general, sampling exactly from the random pairs (8) and (24) is difficult due to their nontrivial dependence structures, while the case when the BDLP is compound Poisson is trivial. Rosinski’s (1991) infinite series representation method is usually suggested for sampling the stochastic integrals, ie functionals of the BDLP, that appear in the random pairs; see section 2.5 of Barndorff-Nielsen and Shephard (2001). However, as we mentioned earlier, there is difficulty in implementation of this method as indicated in section 5.2.2 of Schoutens (2003), hence the simulation is not exact. To be specific, besides an infinite series representation, Rosinski’s method also involves the evaluation of inverse tail mass function , where the tail mass function is defined as . In particular, under the proposed OU-GGC model, the Lévy density of BDLP is of form , where and the expectation is taken w.r.t. the positive random variable ( being a constant reduces to the OU-Gamma case). Therefore, the tail mass function under OU-GGC model, being non-standard, is written as

whose numerical evaluation is difficult especially when approaches zero since numerical evaluation of such an integral as is an ill-posed problem (see section 4.4, chapter 4 of Press et al. (2007) for more details). Moreover, importantly, the inverse of tail mass function is hence not available and numerical inversion is needed presenting additional challenges to implementing Rosinski’s method under OU-GGC models. We do not proceed along this course as it is beyond the scope of this paper which after all aims at devising an exact simulation method.

3 Exact path simulation of BNS OU-Gamma SV model

In this section, we shall present a parallel of Heston (1993) model within the BNS framework, the BNS OU-Gamma SV model, ie the model (5) with the BDLP being specified as a Gamma process with shape parameter and scale parameter . In general, the distributions and the dependence structure of the two components of random pairs (8) and (24) are nontrivial. But under the BNS OU-Gamma SV model, the two pairs can be explicitly decomposed as follows:

| (25) | |||

| (26) |

Here denotes a random variable and denotes a Dirichlet mean random variable that can be written as the steady solution of the following stochastic equation

where is a random variable, is a variable, and all the variables that appear in the right-hand side of the equation are independent of one another. Furthermore, and are independent, which facilitates the exact simulation. Dirichlet mean random variables are functionals of Dirichlet processes or integrals of functions w.r.t. Dirichlet processes in other words. See James et al. (2008) for a relevant survey and James (2010) for a recent development. A general theory in this regard is provided in Appendix A. The Double CFTP method of Devroye and James (2011) can be applied for the exact sampling of in (25) and (26), see section 5 for more details. It remains to obtain which is straightforward. Therefore, the path simulation of asset price process, ie sampling prices at finitely many time points, can be implemented exactly, hence the simulation pricing of both path independent and dependent derivatives.

To illustrate how derivative prices can be simulated under the BNS OU-Gamma SV model, we take a look at the path independent case while path dependent case follows similarly. We need to produce an i.i.d. random sample of to get a Monte Carlo evaluation of the derivative price. For each , we generate the pair (25), ie and also independently generate from a standard Normal distribution. We get the random samples of by setting

where ,

and

by noticing that under the BNS OU-Gamma SV model. As we discussed at the beginning of section 2, would be an unbiased estimate of the true derivative price with discounted payoff function .

Remark 5

Choosing to be a Gamma process for the BNS OU SV model parallels choosing in (1) under the bivariate diffusion setting. That is, in both cases, in the meantime of tackling the difficult problem of exact simulation from relevant instantaneous/integrated volatilities, one is able to get an exact sample for the leverage effect, see Remark 3 and 4. Table 1 provides a comparison between the Heston model and the BNS OU-Gamma model in terms of distributions of relevant quantities and their exact sampling methods in the path simulation of underlying asset price process in two time points case.

| Heston | BNS OU-Gamma | ||||

| distribution | sampling method | distribution | sampling method | ||

| Path-indep. | Noncentral | with Poisson d.f. | |||

| Broadie and Kaya (2006) | FFT | (25)&(26) | Double CFTP | ||

| Path-dep. | |||||

Note. Involved quantities in the simulation are integrated volatilities, ie and , and the instantaneous volatilities, ie and , where . Path-dep. is for path dependent, Path-indep. is for path independent and d.f. is for degrees of freedom.

3.1 Superposition

Barndorff-Nielsen and Shephard (2001) in section 3 discusses the possibility of generating more flexible dependence structure by the superposition of independent Non Gaussian OU processes, ie weighted sum of independent Non Gaussian OU processes with different persistence rates. Nicolato and Vernardos (2003) in section 6 also points out the possible research direction of investigating the effect of superposition on option pricing. In the following, we shall show that the previous simulation approach works fine with superposition. That is to say, simulation can be performed exactly for both the path independent and dependent cases under the BNS OU-Gamma SV model with superposition.

One typical log price dynamics of a BNS OU-Gamma SV model with superposition, under the risk neutral measure, may be expressed as:

where the superscript of and stands for “superposition”, the instantaneous volatility is given by the sum of independent OU processes, ie for The th OU process is specified as follows:

where ’s are chosen such that and are independent Gamma processes with common shape and scale parameters and such that As long as distributions or where and stands for the corresponding asset price under superposition model, are concerned in pricing financial derivatives, the previous exact simulation strategy readily applies here if we treat each individual the same way as before. Notice that here the right derivative price is written, for instance, as More technical details can be found in section 4.2, where we cast the problem in a more general setting.

4 Extension of OU-Gamma: The OU-GGC Class

A natural extension to the BNS OU-Gamma SV model would be BNS OU-GGC SV model, where we take the BDLP of (5) to be a Generalized Gamma Convolution (GGC) subordinator with shape parameter and scale random variable ie GGC Similar extension can also be made to the superposition case. GGC variables/subordinators can behave quite differently from Gamma ones. We next address this briefly from a density point of view. A Gamma process, ie GGC ( is a positive constant), evaluated at time 1 is a Gamma random variable with density

In the following, we provide two examples of GGC subordinators taken from James (2010). We refer to (James et al. (2008) and James (2010)) for more examples.

Example 1

For , let denote a positive -stable random variable specified by its Laplace transform

Let be an independent copy of In addition, define

The subordinator in section 4.3 of James (2010) is a GGC where

Moreover, ( is a Uniform variable) with density function

See Bertoin et al. (2006) for more information on this example.

Example 2

For a GGC, say , arises from exponentially tilting GGC. The density of is given by:

From the above examples, we can see that GGC variables can even have no first moment as in Example 1 in contrast to the Gamma case, for instance, GGC variables have no first moment for . Importantly, our motivation of making the GGC extension is that, as shown in section 6.2, OU-GGC models can provide more flexibility in generating different kinds of return distributions.

4.1 Path independent case: Gamma Leveraging

As it is usually the case that generalization means loss of certain level of tractability, there is no exception here. Recall that for pricing path independent derivatives, we have to deal with the random pair (8), ie . Nonetheless, unlike the OU-Gamma case, it is difficult to sample exactly the pair (8) due to the nontrivial dependence structure of its two components. Recall also Remark 4 that the necessity of sampling in pair, ie (8), is attributable to the usage of the GGC BDLP to model the leverage effect. In view of this, we would like to introduce an interesting concept called gamma leveraging, which means replacing the GGC BDLP , which appears as the leverage component of the asset log price process in (5), by its extracted Gamma component. To be specific, the log price process of new gamma leveraged BNS (GL-BNS) OU-GGC SV model is rewritten as:

| (27) |

where the superscript of refers to “gamma leveraging”, and is the Gamma component of GGC BDLP , which is made theoretically clear from a Poisson random measure point of view. See Appendix A for details. It then follows that the random pair (8) adjusted to the GL-BNS OU-GGC SV model is rewritten as:

where is the steady solution of

and and are independent. Therefore, exact simulation applies again after the introduction of gamma leveraging. The following Remark 6 shows that we actually lose no essential economic meaning about the “leverage effect” in the gamma leveraged model (27) comparing to the original BNS OU-GGC model, ie (5) with BDLP being given by a GGC subordinator.

Remark 6

Following Barndorff-Nielsen and Shephard (2001), section 4.3, we can compare the leverage effects, which can be empirically measured by correlation between current return and future volatility, under the BNS OU-GGC model ((5) where is GGC) and under the GL-BNS OU-GGC model (27) by comparing covariances:

and

where and are the log returns over intervals of length and is the length of lag. Hence, in this sense, it is evident that there is not much difference in terms of leverage effects between two models.

Remark 7

We can represent a BNS OU-Gamma model as a GL-BNS OU-GGC model by the reparametrization: where and are parameters of leverage effect in GL-BNS OU-GGC model and BNS OU-Gamma model respectively. Notice that for an OU-Gamma model.

4.2 GL-BNS OU-GGC with superposition

A GL-BNS OU-GGC model can also be extended to the case of countable superposition of independent Non Gaussian OU processes. In this case, the log price model under a risk neutral measure may be expressed as:

| (28) |

where superscript of refers to both “gamma leveraging” and “superposition” and is defined similarly as in subsection 3.1. Besides, ’s are independent GGC subordinators with common shape parameter and corresponding scale random variables . Moreover, where is the extracted Gamma component of its corresponding th GGC BDLP Next, we illustrate how path independent derivatives are priced based on this setup.

Let denote the price corresponding to the model (28) and let . Hence one can simulate the relevant expected discounted payoff function:

if one can exactly sample random variables having the conditional distribution of . This can be done as follows. The conditional distribution of is normal with mean

and variance , given and Notice that where each individual integrated volatility can be represented as usual:

Hence the simulation problem reduces to how to produce exact samples from the following random pair:

| (29) |

Proposition 1 in the following characterizes the distribution of the pair (29) that enables one to use the Double CFTP for exact sampling.

Proposition 1

Consider specifications for the pair in (29) where s are independent GGC subordinators. Here are independent variables with distributions Set with Then, for , the joint distribution of (29) is equivalent in distribution to the vector:

where is independent of , which satisfies

where , is a discrete random variable on with , independent of . If the are identically distributed, then .

Proof. By straightforward calculations, the Lévy exponent of

can be expressed as

and this is the same as , concluding the result.

4.3 Path dependent case: Approximations

As we remarked in section 2.2, see Remark 4, in order to simulate path dependent derivative prices, one needs to be able to sample exactly, in addition to the leverage increment of (8), the random pair (24), ie

where the increment of comes from the BDLP , which drives the instantaneous volatility process , rather than the leverage component of the price process. Hence, under the GL-BNS OU-GGC SV model, the Double CFTP method can not be directly applied to the exact path simulation because of the nontrivial dependence between the two elements in (24). Further, the gamma leveraging introduced before cannot help tackling this difficulty in the path dependent case. However, as we shall demonstrate in the following section, several approximation methods perform surprisingly well in handling the above situation.

5 Sampling GGC random variables

As we have already seen that in both the OU-Gamma and OU-GGC models simulation effectively involves the decomposition of a stochastic integral like , where the BDLP is a Gamma process or GGC subordinator. The possible choices in this paper for are: and Under both models, this integral is a GGC random variable with decomposition like where is a variable and is a Dirichlet mean random variable that is, as we mentioned before, the steady solution of a stochastic equation of form:

| (30) |

where is a positive scale random variable. Corresponding to the above three choices of is and respectively, where is the scale variable of GGC BDLP and reduces to the Gamma BDLP case. Moreover, and are independent. The next section discusses the exact sampling method for Dirichlet mean variable In subsection 5.2 we discuss several approximate sampling methods and how the nontrivial dependence structure of the pair (24) is handled by those methods under the GL-BNS OU-GGC models as mentioned earlier in subsection 4.3. The precision of approximation is confirmed by a comparison with the exact Double CFTP method in section 6.

5.1 Exact method: The Double CFTP

The first type of algorithm is an exact sampling method by Devroye and James (2011) which is called the double coupling from the past (Double CFTP). Propp and Wilson (1998a, b) proposed coupling from the past (CFTP) method that is an exact sampling algorithm for the steady state distribution of a Markov chain. In the CFTP, the past time is identified by the first time that every possible state is coalesced into a single state at the current time, and that single state is exactly from the steady state distribution of the Markov Chain, see Devroye and James (2011) for a review of CFTP. By using a doubling trick, Devroye and James (2011) proposed the Double CFTP algorithm which finds the coalescence time and hence generate a sample from the steady state distribution of Markov Chain determined by the equation (30). If is a bounded random variable and then the Double CFTP can be directly applied to sample exactly from the Dirichlet mean random variable . When , we cannot directly adopt the Double CFTP method. Nonetheless, let such that Then can be represented as:

where ’s are independent random variables, ’s are independent Dirichlet mean variables with shape parameters and common scale random variable and, moreover, ’s are independent of ’s. In summary, we can use the Double CFTP method for exact simulation as long as is a bounded random variable. Appendix B summarizes the algorithm.

Remark 8

From Figure 1 in section 6, we notice that the function which maps to the expected stack size is convex. By the property of convex function, we have for and any decomposition such that . Therefore, it is easy to see that the best decomposition for any non-integer is: for where

5.2 Approximation methods

The second type of algorithms are approximation methods based on truncation with both fixed and random number of components. A Dirichlet mean random variable defined through (30) can be represented as:

| (31) |

Here and where are i.i.d. variables equal in distribution to and are i.i.d. variables that have the same distribution as For some , we can approximate by

Firstly, we consider the fixed terms truncation method that is similar as in Ishwaran and James (2001). It assumes that is a fixed number and can be either bounded or unbounded but have to satisfy By simple calculation, we get the error bound in sense as

Secondly, we consider the stopping time approach of Guglielmi et al. (2002). On the one hand, if is bounded by a known constant the approach relies on detecting

which is the first time that equals up to a given machine precision that is approximately 2.22e-016 for IEEE 754 standard double. We implement this number in the following numerical studies. The above stopping rule guarantees the following exact error bound rather than that in sense

See also Muliere and Tardella (1998) for related works. On the other hand, for unbounded cases with , we can easily extend the above stopping time idea as

which guarantees now an error bound as follows

See Murdoch (2000) for the modification of CFTP to deal with unbounded cases. In subsection 6.1, we compare the exact sampling method, ie the Double CFTP method, with approximation methods, showing their surprising high precision.

Remark 9

Based on the summation representation (31) of Dirichlet mean variables, the path simulation under OU-GGC models can be approximately handled as follows. By noticing that the two elements of (24) and the possible leverage increment of (8) have (or equivalently ) variables in common, except that they have different variables, we can first generate copies of variables for both the two elements and the possible leverage increment, and then generate variables respectively to get an approximate sample of the random pair (24) and the possible leverage increment of (8).

Remark 10

Note the infinite series representation of in (31) is based on the sequence having the size biased distribution of a sequence of probabilities with a Poisson Dirichlet law, otherwise known as a stick-breaking sequence; see Ishwaran and James (2001) for pertinent references and background. The well-known fact that the tail of sum of this sequence, decreases at an exponential rate in is key to the good performance of the approximation methods we use.

6 Simulation studies

All the simulation experiments are performed on a laptop PC with an Intel(R) Core(TM)2 Duo CPU P8700 2.53GHz and 1.89RAM. All programs are coded in C programming language with GNU scientific library (GSL) version 1.4 being used for generating random numbers from such standard distributions as Normal, Gamma, Beta and Uniform. See the reference manual of GSL for details about those standard random number generator algorithms and references therein. The C programs are compiled by Microsoft Visual C++ 6.0.

6.1 The Double CFTP vs Approximation methods

For let be a Dirichlet mean variable with shape parameter and scale random variable given by according to our model setting. By simple calculation, the true mean and variance of are given by

Table 2 displays experiment results of the Double CFTP and approximation algorithms with 10,000,000 trials. For approximation algorithms with fixed number of components, we consider All of the algorithms give reasonable results with small error from the true values. It implies that all considered approximation algorithms can be nice alternatives of the Double CFTP algorithm. On the other hand, the exact nature of the Double CFTP provides a reliable benchmark for comparison.

| 0.1 | 0.2 | 0.5 | 1 | 2 | 5 | 10 | |||

|---|---|---|---|---|---|---|---|---|---|

| 0.18393 | |||||||||

| 0.02018 | 0.01850 | 0.01480 | 0.01110 | 0.00740 | 0.00370 | 0.00202 | |||

| Double CFTP | 0.18399 | 0.18389 | 0.18390 | 0.18392 | 0.18398 | 0.18394 | 0.18395 | ||

| 0.02019 | 0.01849 | 0.01479 | 0.01110 | 0.00740 | 0.00370 | 0.00202 | |||

| App. | N=10 | 0.18397 | 0.18391 | 0.18396 | 0.18393 | 0.18391 | 0.18392 | 0.18394 | |

| 0.02017 | 0.01850 | 0.01480 | 0.01109 | 0.00742 | 0.00460 | 0.00592 | |||

| N=50 | 0.18397 | 0.18391 | 0.18396 | 0.18393 | 0.18391 | 0.18392 | 0.18394 | ||

| 0.02017 | 0.01850 | 0.01480 | 0.01109 | 0.00742 | 0.00460 | 0.00592 | |||

| N=100 | 0.18397 | 0.18391 | 0.18396 | 0.18393 | 0.18391 | 0.18394 | 0.18394 | ||

| 0.02017 | 0.01850 | 0.01480 | 0.01109 | 0.00739 | 0.00370 | 0.00202 | |||

| Stopping | 0.18397 | 0.18391 | 0.18396 | 0.18393 | 0.18391 | 0.18394 | 0.18396 | ||

| 0.02017 | 0.01850 | 0.01480 | 0.01109 | 0.00739 | 0.00370 | 0.00202 | |||

| Double CFTP | 76.14446 | 38.07715 | 15.22293 | 7.61515 | 15.23131 | 38.08296 | 76.14860 | ||

| App.-Stopping | 4.74350 | 8.49265 | 19.76969 | 38.69694 | 77.41112 | 217.53297 | 1406.53346 | ||

Note. The true values of the mean and variance of are and respectively. Here is a mean estimate, is a variance estimate, is an estimate of and is an estimate of .

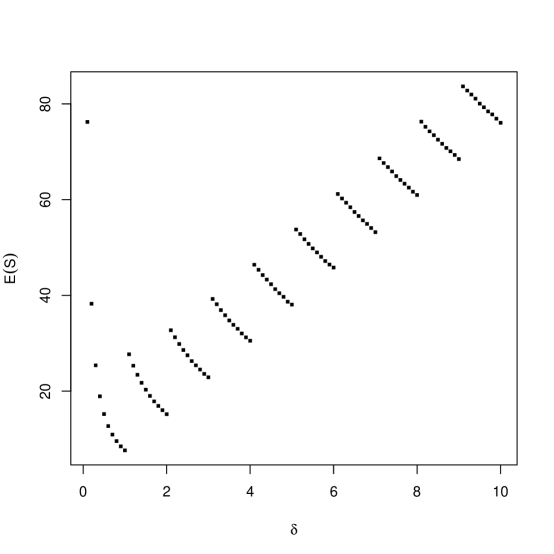

Let be the stack size of the Double CFTP algorithm, see Appendix B. Computation times and consumption of memory heavily depend on for the Double CFTP and for a truncating algorithm with stopping time. The main problem with Double CFTP algorithms is that is not uniformly bounded. It is especially bad when is very small or very large. Figure 1 shows estimates of for . The minimum is achieved when For a truncating algorithm with a stopping time, estimates of keep increasing as is increasing, see also Devroye and James (2011) for more discussions.

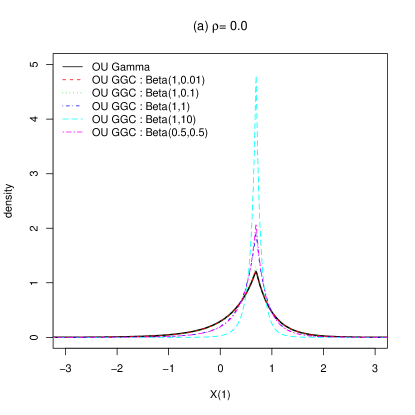

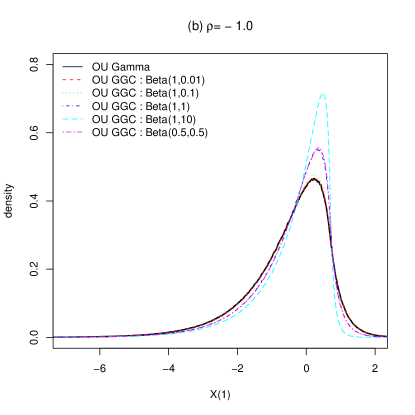

6.2 From BNS OU-Gamma to GL-BNS OU-GGC

In this section we compare the BNS OU-Gamma and GL-BNS OU-GGC models in terms of the flexibility of generating different distributions for the log return, eg , when and For simplicity, we assume that and Under these assumptions, is simplified to

where now and Here is either a Gamma process with shape and scale for the BNS OU-Gamma model or a GGC subordinator with for GL-BNS OU-GGC model. Figure 2 displays the estimated densities of over 10,000,000 trials. Table 3 gives the mean, standard deviation, skewness and kurtosis of over 10,000,000 trials. These simulation results show that the GL-BNS OU-GGC model is a reasonable extension to the BNS OU-Gamma model in terms of distributional flexibility.

| BNS | GL-BNS OU-GGC | ||||||

|---|---|---|---|---|---|---|---|

| OU-Gamma | Beta(1,0.01) | Beta(1,0.1) | Beta(1,1) | Beta(1,10) | Beta(0.5,0.5) | ||

| mean | 0.5090 | 0.5111 | 0.5256 | 0.6011 | 0.6765 | 0.6014 | |

| s.d. | 0.6404 | 0.6367 | 0.6091 | 0.4447 | 0.1846 | 0.4465 | |

| skew. | -1.0415 | -1.0423 | -1.0463 | -1.0125 | -0.6272 | -1.1309 | |

| kurt. | 7.6148 | 7.6475 | 7.8050 | 8.9646 | 10.4274 | 9.7664 | |

| mean | -0.4912 | -0.4883 | -0.4745 | -0.3992 | -0.3229 | -0.3983 | |

| s.d. | 1.1876 | 1.1849 | 1.1709 | 1.0945 | 1.0160 | 1.0955 | |

| skew. | -1.3571 | -1.3576 | -1.3925 | -1.5905 | -1.9043 | -1.6040 | |

| kurt. | 6.4008 | 6.3918 | 6.5259 | 7.3110 | 8.6068 | 7.4114 | |

Note. , and

7 Numerical results on simulation pricing

In this section, we investigate the performance of our proposed models in terms of pricing both the European call options (path independent) and the forward start options (path dependent). The study consists of two parts. First, we calibrate our proposed models to a real option data set that was used by many authors in the literature. Based on the parameter estimation from the calibration procedure, we then demonstrate the capability of those proposed models in pricing some of the path dependent options, eg the forward start options.

We call the price generated by directly taking the Monte Carlo average of payoffs calculated over sample paths of the asset price plain simulation price (PSP), see section 2. In order to improve the efficiency of the exact simulation pricing method, a conditional BS representation of the derivative price can be applied to reduce the Monte Carlo error of the price estimator. See (Hull and White (1987) and Willard (1997)) for the argument of this representation under SV models. The price produced by this latter method is called formula simulation price (FSP). Next we explain how the conditional Monte Carlo method works. We follow the sections 5 and 7 of Broadie and Kaya (2006) and subsection 4.2 of Nicolato and Vernardos (2003).

European Call options

The price of a European call option can be equivalently represented under BNS OU SV models as

where denotes the usual BS price formula, and are the corresponding spot price and volatility and the notation emphasizes that the BS price is conditional on a path of the BDLP Under the BNS OU SV model (5), we have that and Therefore, it is not necessary to condition on the entire path of the BDLP. The call price can just be rewritten as

Under the BNS OU-Gamma model, conditional on we can produce exactly i.i.d. copies of the random pair (25), and hence i.i.d. copies of the BS price inside the expectation. The FSP is therefore written as , in contrast to the PSP given by We denote

for later use.

Forward Start Options

A similar conditional argument can be applied to pricing a forward start option with fair price By the linear homogeneity of the European call price w.r.t. the spot price and the strike, we can rewrite the forward start option price as

where is the conditional BS price as defined in the previous European call option case. Therefore, under the BNS OU-Gamma model, conditional on we can sample exactly i.i.d. copies of random pairs (25) and (26), and hence i.i.d. copies of and also the BS price inside the expectation. The FSP is thus given by in contrast to the PSP given by . See section 7 of Broadie and Kaya (2006) for more details and Kruse and Nögel (2005) for relevant works.

7.1 Model calibration

The data set has 87 call option prices on the S&P 500 Index at the close of the market on 2 November 1993, see (Aït-Sahalia and Lo (1998) and Aït-Sahalia and Lo (2000)) for a detailed description of the data set. On that day, the S&P 500 Index closed at 468.44. The risk-free rate is and the dividend yield is assumed to be zero. This data set has been analyzed by many authors including (Duffie et al. (2000) and Nicolato and Vernardos (2003)).

We compared the BNS OU-Gamma and GL-BNS OU-GGC models both with superposition For the GL-BNS OU-GGC model, we used such that For models with superposition , we give a constraint on the parameter set that to avoid the label-switching problem, ie the unidentifiability of the permutation of ’s, see Diebolt and Robert (1994) for a label-switching problem. Typically, calibration (fit of model to the market data) is a model estimation procedure under the risk neutral measure, which is done by minimizing the mean-square error

where model prices are the simulation estimates of the expected discounted payoffs (the true model prices). Therefore, the MSE that we report here involves a Monte Carlo error, ie the variance of the simulation estimator of the true model price. FSP is used to reduce this Monte Carlo error. For the calibration purpose, the Double CFTP perfect sampler is available for all the above considered models. Usually a grid search method is used to find parameter estimates. However, a grid search over more than 5 dimensional parameter space is almost impossible. Instead of a grid search, we used the simplex algorithm for multidimensional minimization problems (Nelder and Mead (1965)) that is implemented in a GSL version 1.4. It is one of those methods that do not require derivatives and are robust. We use 100,000 trials, ie , to get model prices. This number turns out to be large enough so that the MSE reported here is precise up to at least three decimal places. Table 4 displays the risk-neutral calibrated parameters and MSEs. There is notable improvement of fit with introducing the GGC extension while little improvement can be made by including superposition. In terms of MSE, the OU-Gamma model outperforms the Heston model, by noticing that OU-Gamma model has an MSE of (see second column of Table 4) while the MSE of Heston model is (this can be found from the first column of Table of Duffie et al. (2000)) and the MSE of OU-Gamma model is significantly smaller. As can be seen from the Table 5.1 of Nicolato and Vernardos (2003), BNS models with IG and Gamma marginals give MSEs and respectively, hence OU-Gamma model outperforms these two models as well.

| BNS OU-Gamma | GL-BNS OU-GGC | |||

| super-pos. | ||||

| – 4.88115 | – 4.87261 | – 0.04455 | – 0.04434 | |

| 0.81303 | 0.79608 | 0.80124 | 0.79536 | |

| 0.00981 | 0.00989 | 0.00954 | 0.00971 | |

| 3.61908 | 3.68861 | |||

| 0.10414 | 0.11126 | |||

| 0.00437 | 0.00418 | 0.00414 | 0.00407 | |

| 2.24323 | 2.27276 | 2.68545 | 2.69492 | |

| 0.00006 | 0.00003 | |||

| 0.02755 | 0.01442 | |||

| MSE | 0.00870 | 0.00842 | 0.00778 | 0.00711 |

7.2 Simulating path dependent option prices

In Table 5, we also give the simulation pricing results for forward start options based on parameters estimated from the previous calibrations. For BNS OU-Gamma model, we applied both the exact sampling method and approximation methods for comparison. Estimated prices are similar for both methods. The time needed for the exact method is more than the approximation method under the BNS OU-Gamma model with superposition and the set of estimated parameters. For the GL-BNS OU-GGC model, we can only apply approximation methods. It also gives similar estimated values. The Monte Carlo errors of FSPs are significantly smaller than that of PSPs. It is not surprising that a large amount of time is required in the exact path simulation of OU-Gamma model with superposition since, as we mentioned earlier in section 3.1, the two independent OU processes have to be treated separately in order to generate a price path. However, according to our fitted result in Table 4, the second OU process results in simulating a Dirichlet Mean variable with shape parameter which is time consuming as expected, see section 6.1 and in particular Figure 1. Nonetheless, this is not a problem for the path independent case as in model calibration, where one can always treat the simulation in an aggregate fashion as indicated by Proposition 1 of subsection 4.2. The related Dirichlet Mean variable then has shape parameter with moderate value.

Although we illustrate here the exact simulation pricing of forward start options, other more heavily path dependent derivatives, eg Bermudan options, can also be priced by the proposed exact simulation method as long as the derivatives’ payoff function depends on discretely spaced asset prices at a finite number of times. The computation time is linear in the number of time points when they are equally spaced.

| # of trials | PSP | s.e. | c.t. | FSP | s.e. | c.t. | |||

|---|---|---|---|---|---|---|---|---|---|

| 10,000 | BNS OU-Gamma | Exact | 5.95545 | 0.06524 | 2 | 5.97314 | 0.02963 | 2 | |

| 5.98338 | 0.06593 | 114 | 6.00002 | 0.02973 | 113 | ||||

| App. | 5.98782 | 0.06433 | 2 | 5.99087 | 0.02904 | 2 | |||

| 6.04260 | 0.06412 | 3 | 5.98026 | 0.02934 | 3 | ||||

| GL-BNS OU-GGC | App. | 6.00127 | 0.06489 | 2 | 6.06638 | 0.02890 | 2 | ||

| 5.96249 | 0.06314 | 3 | 5.96251 | 0.02895 | 3 | ||||

| 100,000 | BNS OU-Gamma | Exact | 5.98164 | 0.02127 | 15 | 5.98314 | 0.00941 | 16 | |

| 5.99319 | 0.02145 | 1131 | 6.00002 | 0.00938 | 1123 | ||||

| App. | 6.00002 | 0.02125 | 16 | 5.99100 | 0.00940 | 15 | |||

| 6.00211 | 0.02201 | 29 | 6.00006 | 0.00951 | 28 | ||||

| GL-BNS OU-GGC | App. | 5.99176 | 0.02103 | 17 | 5.98917 | 0.00939 | 17 | ||

| 5.98142 | 0.02192 | 29 | 5.99251 | 0.00941 | 29 | ||||

Note. Fitted model parameters are shown in table 4 and , , year, years. 100 components are used for approximation methods. Here s.e. is standard error and c.t. is computing time (in seconds).

8 Conclusions

In this paper, we devise the exact path simulation method for the nontrivial BNS type OU-Gamma SV models that parallels the result of Broadie and Kaya (2006) for the popular Heston model. Such extensions as superposition of independent OU volatility processes and OU-GGC models to the baseline OU-Gamma models are also studied. The exact simulation technique still applies to pricing path independent derivatives under the larger class of OU-GGC models by introducing the gamma leveraging concept, while approximation method is needed when considering pricing path dependent derivatives. The high precision of the two proposed approximation methods is confirmed by a comparison to the exact Double CFTP method in the numerical study. We then calibrated the proposed OU-Gamma model among others to a well known European option data set that has been studied by many authors in the literature, showing its better performance than the Heston model and two other BNS type models. The models’ capabilities of pricing path dependent options are also illustrated by numerical tests, showing their potential in practical applications.

Appendix A: Independence properties of GGC random variables

Let denote a Poisson random measure on with mean measure

where and is a probability measure. A generalized Gamma convolution subordinator, GGC, is defined as

As a special case, if is a constant , it is just a Gamma process with shape parameter and scale parameter Here

is a Gamma completely random measure on with mean measure That is, for any disjoint subsets of and , and are independent Gamma and Gamma random variables respectively, where

Additionally,

is a Gamma subordinator that is the extracted Gamma component of . For and ,

is a random probability measure which is a Dirichlet process and is independent of . It follows that for any non-negative function ,

Here is a Dirichlet mean variable that is independent of and satisfies

where , and . denotes a uniform distribution on and denotes a beta distribution with mean and variance . Three random variables on the right-hand side, ie , and , are mutually independent. While and are clearly dependent, the distribution of the pair can be expressed as

See for instance James et al. (2008) and James (2010) among others for references.

Appendix B: A compact algorithm of the Double CFTP

The Double CFTP method of Devroye and James (2011) is designed for exact sampling a random variable defined through the following stochastic equation or Markovian map

where all variables on the right-hand side are independent of one another and on both sides have the same distribution. We assume that the density of is bounded from below on by a constant and In the following algorithm, see James and Zhang (2011), are variables and and have the same distributions.

- Backward phase.

For : keep generating and storing until Keep

- Set starting point.

Set

- Forward phase.

For : given previously stored, do the following step: generate , and , and construct Repeat this step until:

or or . Then set

- Output.

Return .

As a special case, is a Dirichlet mean variable when is a variable. Particularly in this paper, the Dirichlet mean variables under consideration are those with for , whose density is for all , and being or (see section 5), which are bounded by , and respectively if . The above algorithm is ready-to-use for simulating relevant Dirichlet mean random numbers by simply setting and

Acknowledgments

We would like to thank Prof. Yacine Aït-Sahalia for providing us the option data set. Dohyun Kim’s research is supported by the Korean Research Foundation Grant funded by the Korean Government (KRF-2008-314-C0046).

References

- Aït-Sahalia and Lo (1998) Aït-Sahalia, Y. and Lo, A. (1998) Nonparametric Estimation of State-Price-Densities Implicit in Financial Asset Prices. Journal of Finance, 53, 499–547.

- Aït-Sahalia and Lo (2000) Aït-Sahalia, Y. and Lo, A. (2000) Nonparametric Risk Management and Implied Risk Aversion. Journal of Econometrics, 94, 9–51.

- Barndorff-Nielsen and Shephard (2001) Barndorff-Nielsen, O. E. and Shephard, N. (1973) Non-Gaussian Ornstein-Uhlenbeck-based models and some of their uses in financial economics. Journal of the Royal Statistical Society B, 63, 167–241.

- Bertoin et al. (2006) Bertoin, J., Fujita, T., Roynette, B. and Yor, M. (2006). On a particular class of self-decomposable random variables: The duration of a Bessel excursion straddling an independent exponential time. Probab. Math. Statist., 26, 315–366.

- Bondesson (1992) Bondesson, L. (1992) Generalized gamma convolutions and related classes of distributions and densities. Lecture Notes in Statistics, 76. Springer-Verlag, New York.

- Broadie and Kaya (2006) Broadie, M. and Kaya, Ö. (2006) Exact simulation of stochastic volatility and other affine jump diffusion processes. Operations Research, 54, 217–231.

- Carr and Madan (1999) Carr, P., Madan, D. B. (1999) Option pricing and the fast fourier transform. Journal of Computational Finance, 2, 61–73.

- Carr et al. (2003) Carr, P., Geman, H., Madan, D. B. and Yor, M. (2003) Stochastic volatility for Lévy processes. Math. Finance, 13, 345–382.

- Chan et al. (1992) Chan, K. C., Karolyi, G. A., Longstaff, F. A. and Sanders, A. B. (1992) An empirical comparison of alternative models of the short-term interest rate. The Journal of Finance, 47, 1209–1227.

- Cont and Tankov (2003) Cont, R. and Tankov, P. (2003) Financial modelling with jump processes. Chapman & Hall/CRC Press.

- Cox et al. (1985) Cox, J. C., Ingersoll, J. E. and Ross, S. A. (1985) A theory of the term structure of interest rates. Econometrica, 53, 385–406.

- Devroye and James (2011) Devroye, L. and James, L.F. (2011) The Double CFTP method. ACM Transactions on Modeling and Computer Simulation, 21(2), 10.1–10.20.

- Diebolt and Robert (1994) Diebolt, J. and Robert, C. (1994) Estimation of finite mixture distributions by Bayesian sampling, J. Royal Statist. Soc. Series B, 56, 363–375.

- Duffie and Glynn (1995) Duffie, D. and Glynn, P. (1995) Efficient Monte Carlo estimation of security prices. Ann. Appl. Probab., 4(5), 897–905.

- Duffie et al. (2000) Duffie, D., Singleton, K. and Pan, J. (2000) Transform analysis and asset pricing for affine jump-diffusions. Econometrica, 68, 1343–1376.

- Heston (1993) Heston, S. L. (1993) A closed-form solution for options with stochastic volatility with applications to bond and currency options. Review of Financial Studies, 13, 585–625.

- Hull and White (1987) Hull, J. and White, A. (1987) The pricing of options on assets with stochastic volatilities. Journal of Finance, 42(2), 281–300.

- Glasserman and Kim (2011) Glasserman, P. and Kim, K. (2011) Gamma expansion of the Heston stochastic volatility model. Finance and Stochastics, 15, 267–296.

- Guglielmi et al. (2002) Guglielmi, A., Holmes, C.C. and Walker, S. G. (2002) Perfect simulation involving functionals of a Dirichlet process. Journal of Computational and Graphical Statistics, 11, 306–310.

- Ghysels et al. (1996) Ghysels, E., Harvey, A. C. and Renault, E. (1996) Stochastic volatility. In Statistical Methods in Finance, Rao, C. R., and Maddala, G. S. (eds), pp. 119–191. North-Holland, Amsterdam.

- Ishwaran and James (2001) Ishwaran, H. and James, L. F. (2001) Gibbs sampling methods for stick-breaking priors. J. Amer. Stat. Assoc., 96, 161–173.

- James (2010) James, L.F. (2010) Dirichlet mean identities and laws of a class of subordinators. Bernoulli, 16, 361–388.

- James et al. (2008) James, L.F., Roynette, B. and Yor, M. (2008) Generalized Gamma Convolutions, Dirichlet means, Thorin measures, with explicit examples. Probab. Surv., 5, 346–415.

- James and Zhang (2011) James, L.F. and Zhang, Z. (2011) Quantile Clocks. Annals of Applied Probability, 21, 1627–1662.

- Kruse and Nögel (2005) Kruse, S. and Nögel, U. (2005) On the Pricing of Forward Starting Options under Stochastic Volatility. Finance Stochastics, 9, 233–250.

- Meddahi (2002) Meddahi, N. (2002) A Theoretical Comparison between Integrated and Realized Volatility. Journal of Applied Econometrics, 17, 479–508.

- Muliere and Tardella (1998) Muliere, P. and Tardella, L. (1998) Approximating distributions of random functionals of Ferguson-Dirichlet priors. Canadian Journal of Statistics, 26, 283–297.

- Murdoch (2000) Murdoch, D. J. (2000) Exact samplling for Bayesian inference: Unbounded state space. In Monte Carlo Methods, Madras, M. (ed), pp. 111 C121. Fields Institute Communications, Vol. 26. American Mathematical Society, Providence, RI.

- Nelder and Mead (1965) Nelder, J. A. and Mead, R. (1965) A simplex method for function minimization. Computer Journal, 7, 308–315.

- Nelson (1990) Nelson, D. (1990) ARCH models as diffusion approximations. Journal of Econometrics, 45, 7–38.

- Nicolato and Vernardos (2003) Nicolato, E. and Vernardos, E. (2003) Option pricing in stochastic volatility models of the Ornstein-Uhlenbeck type. Math. Finance, 12, 27–47.

- Pitman and Yor (1982) Pitman, J. and Yor, M. (1982) A decomposition of Bessel bridges. Z. Wahrscheinlichkeitstheorie verw. Gebiete, 59, 425–457.

- Press et al. (2007) Press, W.H., Teukolsky, S.A., Vetterling, W.T., Flannery, B.P. (2007) Numerical Recipes 3rd Edition: The Art of Scientific Computing. Cambridge University Press.

- Propp and Wilson (1998a) Propp, J. G. and Wilson, D. B. (1998a) Exact sampling with coupled Markov chains and applications to statistical mechanics. Random Structures and Algorithms, 9, 223–252.

- Propp and Wilson (1998b) Propp, J. G. and Wilson, D. B. (1998b) How to get a perfectly random sample from a generic Markov chain and generate a random spanning tree of a directed graph. Journal of Algorithms, 27, 170–217.

- Rosiński (1991) Rosiński, J. (1991) On a class of infinitely divisible processes represented as mixtures of Gaussian processes. In Stable Processes and Related Topics, Cambanis, S., Samorodnitsky, G., and Taqqu, M. S. (eds), pp. 27–41. Birkhäuser, Basel.

- Schoutens (2003) Schoutens, W. (2003) Levy Processes in Finance: Pricing Financial Derivatives. Wiley.

- Shephard (1996) Shephard, N. (1996) Statistical aspects of ARCH and stochastic volatility. In Time Series Models in Econometrics, Finance and Other Fields, Cox, D. R., Barndorff-Nielson, O. E., and Hinkley, D. V. (eds), pp. 1–67. Chapman & Hall, London.

- Willard (1997) Willard, G. A. (1997) Calculating prices and sensitivities for path independent derivative securities in multifactor models. J. Derivatives, 5(1), 45–61.

- Zhang (2010) Zhang, Z. (2010) Inference for continuous time stochastic volatility models: market microstructure from a chronological perspective. Ph.D. thesis, The Hong Kong University of Science and Technology, Department of Information Systems, Business Statistics and Operations Management.