An optimal three-way stable and monotonic spectrum of bounds on quantiles:

a spectrum of coherent measures of financial risk and economic inequality

Abstract

A certain spectrum of upper bounds on the tail probability , with and being the best possible exponential upper bound on , is shown to be stable and monotonic in , , and , where is a real number and is a random variable. The bounds are optimal values in certain minimization problems. The corresponding spectrum of upper bounds on the -quantile of is shown as well to be stable and monotonic in , , and , with equal the largest -quantile of . In fact, and are nondecreasing in with respect to the stochastic dominance of any order . It is shown that for small enough values of the quantile bounds are close enough to the true quantiles provided that the right tail of the distribution of is light enough and regular enough, depending on . Moreover, it is shown that the quantile bounds possess the crucial property of the subadditivity in if , as well as the positive homogeneity and translation invariance properties, and thus constitute a continuous spectrum of so-called coherent measures of risk. A number of other useful properties of the bounds and are established. In particular, it is shown that, quite similarly to the bounds on the tail probabilities, the quantile bounds are the optimal values in certain minimization problems. This allows for a comparatively easy incorporation of the bounds and into more specialized optimization problems, with additional restrictions, say on the distribution of the random variable . It is shown that the mentioned minimization problems for which and are the optimal values are in a certain sense dual to each other; in the special case this corresponds to the bilinear Legendre–Fenchel duality. In finance, the -quantile is known as the value-at-risk (VaR), whereas the value of is known as the conditional value-at-risk (CVaR) and also as the expected shortfall (ES), average value-at-risk (AVaR), and expected tail loss (ETL). Also in the present paper, a short proof of the well-known Rockafellar–Uryasev–Pflug theorem that VaR is a minimizer in the Rockafellar–Uryasev variational representation of CVaR is provided. More generally, the minimizers in the variational representation of are described in detail for any . A generalization of the Cillo–Delquie necessary and sufficient condition for the so-called mean-risk (M-R) to be nondecreasing with respect to the stochastic dominance of order is presented, with a short proof. Moreover, a necessary and sufficient condition for the M-R measure to be coherent is given. It is shown that the quantile bounds can be used as measures of economic inequality. The spectrum parameter may be considered an index of sensitivity: the greater is the value of , the greater is the sensitivity of the function to risk/inequality. The problems of effective computation of and are considered.

Bounds on quantiles

Iosif Pinelis

Department of Mathematical Sciences

Michigan Technological University

Houghton, Michigan 49931, USA

E-mail: \printead[ipinelis@mtu.edu]e1

keywordAMSAMS 2010 subject classifications:

[class=AMS] \kwd[Primary ]52A41 \kwd60E15 \kwd26A51 \kwd26B25 \kwd91B30 \kwd91B82 \kwd[; secondary ]60E15 \kwd90C25 \kwd90C26 \kwd49J45 \kwd49J55 \kwd49K30 \kwd49K40 \kwd39B62

probability inequalities \kwdextremal problems \kwdtail probabilities \kwdquantiles \kwdcoherent measures of risk \kwdmeasures of economic inequality \kwdvalue-at-risk (VaR) \kwdconditional value-at-risk (CVaR) \kwdexpected shortfall (ES) \kwdaverage value-at-risk (AVaR) \kwdexpected tail loss (ETL) \kwdmean-risk (M-R) \kwdGini’s mean difference \kwdstochastic dominance \kwdstochastic orders

chapter

subsubsection

1 An optimal three-way stable and three-way monotonic spectrum of upper bounds on tail probabilities

Consider the family of functions given by the formula

| (1.1) |

for all . Here, as usual, denotes the indicator function, and for all real .

Obviously, the function is nonnegative and nondecreasing for each , and it is also continuous for each . Moreover, it is easy to see that, for each ,

| (1.2) |

Next, let us use the functions as generalized moment functions and thus introduce the generalized moments

| (1.3) |

Here and in what follows, unless otherwise specified, is any random variable (r.v.), , , and . Since , the expectation in (1.3) is always defined, but may take the value . It may be noted that in the particular case one has

| (1.4) |

which does not actually depend on .

Now one can introduce the expressions

| (1.5) |

By (1.2), and are nondecreasing in . In particular,

| (1.6) |

It will be shown later (see Proposition 1.4) that also largely inherits the property of of being continuous in .

The definition (1.5) can be rewritten as

| (1.7) |

where

| (1.8) | ||||

| and | ||||

| (1.9) | ||||

here and subsequently, we also use the conventions and for all . The alternative representation (1.7) of follows because (i) for , (ii) , and (iii) .

In view of (1.7), one can see (cf. [38, Corollary 2.3]) that, for each , is the optimal (that is, least possible) upper bound on the tail probability given the generalized moments for all , where

| (1.10) |

In fact (cf. e.g. [43, Proposition 3.3]), the bound remains optimal given the larger class of generalized moments for all functions , where

| (1.11) |

denotes the set of all nonnegative Borel measures on , and, as usual, stands for the set of all real-valued functions on . By [39, Proposition 1(ii)] and [43, Proposition 3.4],

| (1.12) |

This provides the other way to come to the mentioned conclusion that

| (1.13) |

By [40, Proposition 1.1], the class of generalized moment functions can be characterized as follows in the case when is a natural number: for any , one has if and only if has finite derivatives on such that is convex on and for . Also, by [43, Proposition 3.4], if and only if is infinitely differentiable on , and on and for all .

Thus, the greater the value of , the narrower and easier to deal with is the class and the smoother are the functions comprising . However, the greater the value of , the farther away is the bound from the true tail probability .

Of the bounds , the loosest and easiest one to get is , the so-called exponential upper bound on the tail probability . It is used very widely, in particular when is the sum of independent r.v.’s , in which case one can rely on the factorization . A bound very similar to was introduced in [16] in the case when the sum of independent bounded r.v.’s; see also [36, 15, 37]. For any , the bound is a special case of a more general bound given in [38, Corollary 2.3]; see also [38, Theorem 2.5]. For some of the further developments in this direction see [39, 7, 8, 41, 42, 9, 43]. The papers mentioned in this paragraph used the representation (1.7) of , rather than the new representation (1.5). The new representation appears, not only of more unifying form, but also more convenient as far as such properties of as the monotonicity in and the continuity in and in are concerned; cf. (1.2) and the proofs of Propositions 1.4 and 1.5; those proofs, as well as proofs of most of the other statements in this paper, are given in Appendix A. Yet another advantage of the representation (1.5) is that, for , the function inherits the convexity property of , which facilitates the minimization of in , as needed to find by (1.5); relevant details on the remaining “difficult case” can be found in Section 3.1.

On the other hand, the “old” representation (1.7) of is more instrumental in establishing the mentioned connection with the classes of generalized moment functions; in proving part (iii) of Proposition 1.2; and in discovering and proving Theorem 2.3.

***

Some of the more elementary properties of are presented in

Proposition 1.1.

-

(i)

is nonincreasing in .

-

(ii)

If and , then for all .

-

(iii)

If and for all real , then for all .

-

(iv)

If and , then as and as , so that for all .

-

(v)

If and for some real , then as and as , so that for all .

In view of Proposition 1.1, it will be henceforth assumed by default that the tail bounds – as well as the quantile bounds , to be introduced in Section 2, and also the corresponding expressions , , , and as in (1.3), (1.9), (2.9), and (3.15) – are defined and considered only for r.v.’s (unless indicated otherwise), where

is the set of all real-valued r.v.’s on a given probability space (implicit in this paper), and

| (1.14) |

Observe that the set is a convex cone: for any and any and in , the r.v.’s and are in . Indeed, the conclusion that for any and is obvious. Concerning the conclusion that for any and in , use the inequalities if , Minkowski’s inequality if , and Hölder’s inequality for any positive and such that . Here, as usual, , the -norm of a r.v. – which is actually a norm if and only if . Also, it is obvious that the cone contains all real constants.

It follows from Proposition 1.1 and (1.6) that

| is nonincreasing in , with and . | (1.15) |

Here, as usual, an denote the right and left limits of at .

One can say more in this respect. To do that, introduce

| (1.16) |

Here, as usual, denotes the support set of (the distribution of the r.v.) ; speaking somewhat loosely, is the maximum value taken by the r.v. , and is the probability with which this value is taken. It is of course possible that , in which case necessarily , since the r.v. was assumed to be real-valued.

Introduce also

| (1.17) |

where

| (1.18) |

Recall that, according to the standard convention, for any subset of , if and only if .

Now one can state

Proposition 1.2.

-

(i)

For all one has

-

(ii)

For all one has .

-

(iii)

The function is continuous and convex if ; we use the conventions and for all real ; concerning the continuity of functions with values in the set , we use the natural topology on this set. Also, the function is continuous and convex, with the convention .

-

(iv)

If then the function is continuous.

-

(v)

The function is left-continuous.

-

(vi)

is nondecreasing in , and for all .

-

(vii)

If then ; even for , it is of course possible that , in which case for all real .

-

(viii)

, and if and only if .

-

(ix)

.

-

(x)

for all .

-

(xi)

If then is strictly decreasing in .

This proposition will be useful when establishing continuity properties of the quantile bounds considered in Section 2. For , parts (i), (iv), (vii), (x), and (xi) of Proposition 1.2 are contained in [43, Proposition 3.2].

One may also note here that, by (1.15) and part (v) of Proposition 1.2, the function may be regarded as the tail function of some r.v. : for all real .

Example 1.3.

Some parts of Propositions 1.1 and 1.2 are illustrated in the following picture with graphs of the function for various values of in the important case when the r.v. takes only two values. Then, by the translation invariance property stated below in Theorem 1.6, without loss of generality (w.l.o.g.) . Thus, , where and are positive real numbers and is a r.v. with the uniquely determined zero-mean distribution on the set .

![[Uncaptioned image]](/html/1310.6025/assets/x1.png)

Explicit expressions for were given in [43, Section 3, Example] in the cases and . In the case , one can see that equals for , for , and for , with and . Graphs are shown here on the left, with and , for values of equal (black), (blue), (green), (orange), and (red). In particular, here .

Proposition 1.4.

is continuous in in the following sense: Suppose that is any sequence in converging to , with and ; then .

Let us now turn to the question of stability of with respect to (the distribution of) . First here, recall that one of a number of mutually equivalent definitions of the convergence in distribution, , of a sequence of r.v.’s to a r.v. is the following: for all real such that .

We shall also need the following uniform integrability condition:

| if , | (1.19) | ||

| (1.20) |

Proposition 1.5.

Note that in the case the convergence (1.21) may fail to hold, not only for , but for all real such that .

***

Let us now discuss matters of monotonicity of in , with respect to various orders on the mentioned set of all real-valued r.v.’s . Using the family of function classes , defined by (1.11), one can introduce a family of stochastic orders, say , on the set by the formula

where and and are in . To avoid using the term “order” with two different meanings in one phrase, let us refer to the relation as the stochastic dominance of order , rather than the stochastic order of order . In view of (1.11), it is clear that

| (1.22) |

so that, in the case when for some natural number , the order coincides with the “-increasing-convex” order as defined e.g. in [56, page 206]. In particular,

| (1.23) | ||||

where denotes the usual stochastic dominance of order , and

| (1.24) | ||||

so that coincides with the usual stochastic dominance of order . Also,

| iff for some r.v.’s and which are copies in distribution of and , | (1.25) |

respectively.

By (1.12), the orders are graded in the sense that

| if for some , then for all . | (1.26) |

A stochastic order, which is a “mirror image” of the order , but only for nonnegative r.v.’s, was presented by Fishburn in [20]; note [20, Theorem 2] on the relation with a “bounded” version of this order, previously introduced and studied in [18]. Denoting the corresponding Fishburn [20] order by , one has

| (1.27) |

for nonnegative r.v.’s and . However, as shown in this paper (recall Proposition 1.1) the condition of the nonnegativity of the r.v.’s is not essential; without it, one can either deal with infinite expected values or, alternatively, require that they be finite. The case when is an integer was considered, in a different form, in [5].

One may also consider the order defined by the condition that if and only if and are nonnegative r.v.’s and for all , where ,

| (1.28) | ||||

| (1.29) |

with as in (2.3), and the integral in (1.28) is understood as the Lebesgue integral with respect to the nonnegative Borel measure on defined by the condition that for all ; cf. [29, 31]. Note that . For nonnegative r.v.’s, the order coincides with the order if ; again see [29, 31]. Even for nonnegative r.v.’s, it seems unclear how the orders and relate to each other for positive real ; see e.g. the discussion following Proposition 1 in [29] and Note 1 on page 100 in [33].

The following theorem summarizes some of the properties of the tail probability bounds established above and also adds a few simple properties of these bounds.

Theorem 1.6.

The following properties of the tail probability bounds are valid.

- Model-independence:

-

depends on the r.v. only through the distribution of .

- Monotonicity in :

-

is nondecreasing with respect to the stochastic dominance of order : for any r.v. such that , one has . Therefore, is nondecreasing with respect to the stochastic dominance of any order ; in particular, for any r.v. such that , one has .

- Monotonicity in :

-

is nondecreasing in .

- Monotonicity in :

-

is nonincreasing in .

- Values:

-

takes only values in the interval .

- -concavity in :

-

is convex in if , and is concave in if .

- Stability in :

-

is continuous in at any point – except the point when .

- Stability in :

-

Suppose that a sequence is as in Proposition 1.4. Then .

- Stability in :

-

Suppose that and a sequence is as in Proposition 1.5. Then .

- Translation invariance:

-

for all real .

- Consistency:

-

for all real ; that is, if the r.v. is the constant , then all the tail probability bounds precisely equal the true tail probability .

- Positive homogeneity:

-

for all real .

A property similar to the model-independence was called “neutrality” in [57, page 97].

2 An optimal three-way stable and three-way monotonic spectrum of upper bounds on quantiles

Take any

| (2.1) |

and introduce the generalized inverse (with respect to ) of the bound by the formula

| (2.2) |

where is as in (1.18). In particular, in view of the equality in (1.6),

| (2.3) |

which is a -quantile of (the distribution of) the r.v. ; actually, is the largest one in the set of all -quantiles of .

It follows immediately from (2.2), (1.13), and (2.3) that

| is an upper bound on the quantile , and | (2.4) | |||

| is nondecreasing in . |

Thus, one has a monotonic spectrum of upper bounds, , on the quantile , ranging from the tightest bound, , to the loosest one, , which latter is based on the exponential bound on . Also, it is obvious from (2.2) that

| is nonincreasing in . | (2.5) |

Proposition 2.1.

Recall the definitions of and in (1.16) and (1.17). The following statements are true.

-

(i)

.

-

(ii)

If then .

-

(iii)

.

-

(iv)

.

-

(v)

If , then the function

(2.6) is the unique inverse to the continuous strictly decreasing function

(2.7) So, the function (2.6) too is continuous and strictly decreasing.

-

(vi)

If , then for any one has .

-

(vii)

If , then .

Example 2.2.

![[Uncaptioned image]](/html/1310.6025/assets/x2.png)

Some parts of Proposition 2.1 are illustrated in the picture here on the left, with graphs for a r.v. as in Example 1.3, with the same and , and the same values of , equal (black), (blue), (green), (orange), and (red). One may compare this picture with the one in Example 1.3, having in mind that the function is a generalized inverse to the function .

The definition (2.2) of is rather complicated, in view of the definition (1.5) of . So, the following theorem will be useful, as it provides a more direct expression of ; at that, one may again recall (2.3), concerning the case .

Theorem 2.3.

Proof of Theorem 2.3.

Note that the case of Theorem 2.3 is a special case of [46, Proposition 1.5], and the above proof of Theorem 2.3 is similar to that of [46, Proposition 1.5]. Correspondingly, the duality presented in the above proof of Theorem 2.3 is a generalization of the bilinear Legendre–Fenchel duality considered in [46].

Theorem 2.4.

The following properties of the quantile bounds are valid.

- Model-independence:

-

depends on the r.v. only through the distribution of .

- Monotonicity in :

-

is nondecreasing with respect to the stochastic dominance of order : for any r.v. such that , one has . Therefore, is nondecreasing with respect to the stochastic dominance of any order ; in particular, for any r.v. such that , one has .

- Monotonicity in :

-

is nondecreasing in .

- Monotonicity in :

-

is nonincreasing in , and is strictly decreasing in if .

- Finiteness:

-

takes only (finite) real values.

- Concavity in or in :

-

is concave in if , and is concave in .

- Stability in :

-

is continuous in if .

- Stability in :

-

Suppose that and a sequence is as in Proposition 1.5. Then .

- Stability in :

-

Suppose that and a sequence is as in Proposition 1.4. Then .

- Translation invariance:

-

for all real .

- Consistency:

-

for all real ; that is, if the r.v. is the constant , then all the quantile bounds equal .

- Sensitivity:

-

Suppose here that . If at that , then for all ; if, moreover, , then .

- Positive homogeneity:

-

for all real .

- Subadditivity:

-

is subadditive in if ; that is, for any other r.v. (defined on the same probability space as ) one has

- Convexity:

-

is convex in if ; that is, for any other r.v. (defined on the same probability space as ) and any one has

The inequality , in other notations, was mentioned (without proof) in [50]; of course, this inequality is a particular, and important, case of the monotonicity of in . That is nondecreasing with respect to the stochastic dominance of order was shown (using other notations) in [13] in the case .

The following strict monotonicity property complements the monotonicity property of in stated in Theorem 2.4.

Proposition 2.5.

Suppose that a r.v. is stochastically strictly greater than (which may be written as ; cf. (1.23)) in the sense that and for any there is some such that . Then if .

This proposition will be useful in the proof of Proposition 2.6 below.

Given the positive homogeneity, it is clear that the subadditivity and convexity properties of easily follow from each other. In the statements in Theorem 2.4 on these two mutually equivalent properties, it was assumed that . One may ask whether this restriction is essential. The answer to this question is “yes”:

Proposition 2.6.

There are r.v.’s and such that for all and all one has , so that is not subadditive (and, equivalently, not convex) in .

It is well known (see e.g. [3, 35, 53]) that is not subadditive in ; it could therefore have been expected that will not be subadditive in if is close enough to . In a quite strong and specific sense, Proposition 2.6 justifies such expectations.

***

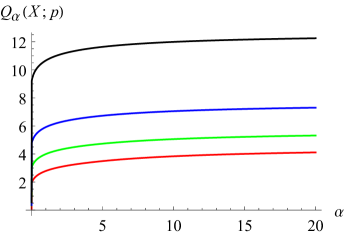

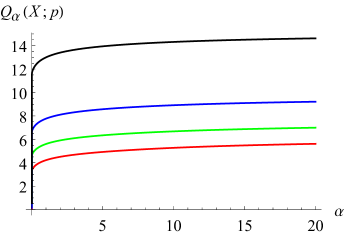

In Figure 1, the graphs of the quantile bounds as functions of are given for (a) (left panel) and (b) (right panel), for the case when has the Gamma distribution with the scale parameter equal and values , , , and of the shape parameter (say ) – shown respectively in colors red, green, blue, and black.

These graphs illustrate the general monotonicity properties of in , , and stated in Theorem 2.4; recall here that the Gamma distribution is (i) stochastically increasing with respect to the shape parameter and (ii) close to normality for large values of . It is also seen that varies rather little in , so that the quantile bounds are not too far from the corresponding true quantiles ; cf. the somewhat similar observation made in [37, Theorem 2.8.].

In fact, it can be shown that for small values of the quantile bounds are relatively close to the true quantiles whenever the right tail of the distribution of is light enough (depending on ) and regular enough. One possible formalization of this general thesis is provided by Proposition 2.7 below, which is based on [38, Theorem 4.2 and Remark 4.3]. We shall need pertinent definitions from that paper.

Take any . Given a positive function on , let us say that is like if there is a positive twice differentiable function on such that

| (2.11) |

as usual, we write if . For any real , the second relation in (2.11) can be rewritten as

| (2.11a) |

which successively implies , , , and hence

| (2.11b) |

In particular, given any , , and ,

| if , then is like . |

Also, given any and in , , and ,

| if or , then is like . |

Moreover, if is like , then for all one has as .

Proposition 2.7.

-

(i)

If the r.v. is bounded from above – that is, , then

(2.12) -

(ii)

If is like for some , then , , and

(2.13) where

(2.14) and is the Gamma function, given by the formula for .

![[Uncaptioned image]](/html/1310.6025/assets/x5.png)

Graphs are shown here on the left: for (red), (orange), (green), (blue), (purple), and (black). It is seen that, if the (right) tail of the distribution of is very heavy – that is, if is comparatively small, then even for the quantile bound is much greater (for small ) than the true quantile . However, if the tail is not very heavy – that is, if is not so small, then the graph of is very flat – that is, varies little with (if is small).

Concerning the relevance of the condition in the asymptotic relations (2.12) and (2.13) in Proposition 2.7, note that small values of are of particular importance in financial practice. Indeed, values of commonly used with the so-called value-at-risk (VaR) measure – equal to the quantile , where is the amount of financial loss – are 1% and 5% for one-day and two-week horizons, respectively [34].

As for the condition that be bounded from above in part (i) of Proposition 2.7, it is obviously fulfilled, in particular, whenever the r.v. takes only finitely many values, as is assumed e.g. in [3].

By (2.11b), if is like for some r.v. and some real , then necessarily – which is in accordance with the assumption made above concerning (2.11).

Usual statistical families of continuous distributions, including the normal, log-normal, gamma, beta, Student, and Pareto families, are covered by Proposition 2.7. More specifically, part (i) of Proposition 2.7 applies to the beta family of distributions, including the uniform distribution. Part (ii) of Proposition 2.7 applies (with ) to the normal, log-normal, and gamma families, including the exponential family; the Student family (with , where is the number of degrees of freedom); and Pareto family (with , assuming that for some and in and all real ). However, note that under the condition that is like , as in part (ii) of Proposition 2.7, (2.13) is guaranteed to hold only for . Also, in the case when is like for some , (2.13) cannot possibly hold for any – because then, by part (ii) of Proposition 1.1, (1.13), and (2.2), . So, the general tendency is that, the lighter the right tail of the distribution of , the wider is the range of values of for which (2.13) holds. Moreover, it appears that, the lighter the right tail of the distribution of , the closer is the constant in (2.13) to and, more generally, the closer is the quantile bound to the true quantile .

One can also show, using [38, Remark 3.13] or [40, Remark 1.4], that (2.13) will hold – with and hence – for all and usual statistical families of discrete distributions, including the Poisson, geometric, and, more generally negative binomial families – because the right tails of those distributions are light enough. On the other hand, (2.12) will hold for any distributions with a bounded support, including the binomial and hypergeometric distributions.

***

3 Computation of the tail probability and quantile bounds

3.1 Computation of

The computation of in the case is straightforward, in view of the equality in (1.6). If , then the value of is easily found by part (i) of Proposition 1.2. So, in the rest of this subsection it may be assumed that and .

In the case when , using (1.5), the inequality

| (3.1) |

the condition , and dominated convergence, one sees that is continuous in and right-continuous in at (assuming the definition (1.3) for as well), and hence

| (3.2) |

Similarly, using in place of (3.1) the inequality whenever , one can show that is continuous in (recall (1.14)) and right-continuous in at , so that (3.2) holds for as well – provided that . Moreover, by the Fatou lemma for the convergence in distribution [10, Theorem 5.3], is lower-semicontinuous in at even if . It then follows by the convexity of in that is left-continuous in at whenever ; at that, the natural topology on the set is used, as it is of course possible that .

Since , one can find some such that (of course, necessarily ); so, one can introduce

| (3.3) |

Then, by (1.3), if and , and if . So, for all one has provided that , and hence

| (3.4) |

Therefore and because , the minimization of in in (3.4) in order to compute the value of can be done effectively if , because in this case is convex in . At that, the positive-part moments , which express for in accordance with (1.3), can be efficiently computed using formulas in [44]; cf. e.g. [43, Section 3.2.3]. Of course, for specific kinds of distributions of the r.v. , more explicit expressions for the positive-part moments can be used.

In the remaining case, when , the function cannot in general be “convexified” by any monotonic transformations in the domain and/or range of this function, and the set of minimizing values of does not even have to be connected, in the following rather strong sense:

Proposition 3.1.

For any , , and , there is a r.v. (taking three distinct values) such that and the infimum in (1.5) is attained at precisely two distinct values of .

Proposition 3.1 is illustrated by

Example 3.2.

![[Uncaptioned image]](/html/1310.6025/assets/x6.png)

Let be a r.v. taking values with probabilities ; then . Also let and , so that , and then let be as in (3.3) with , so that here . Then the minimum of over all real equals and is attained at each of the two points, and , and only at these two points. The graph is shown here on the left.

Nonetheless, effective minimization of in in (3.4) is possible even in the case , say by the interval method. Indeed, take any and write

where (cf. (1.3))

Just as is continuous in , so are and . It is also clear that is nondecreasing and is nonincreasing in .

So, as soon as the minimizing values of are bracketed as in (3.4), one can partition the finite interval into a large number of small subintervals with . For each such subinterval,

so that, by the continuity of in ,

as , uniformly over all subintervals of the interval . Thus, one can effectively bracket the value with any degree of accuracy; this same approach will work, and perhaps may be sometimes useful, for as well.

3.2 Computation of

Proposition 3.3.

(Quantile bounds: Attainment and bracketing).

-

(i)

If then in (2.8) is attained at some and hence

(3.5) moreover, for any

necessarily

(3.6) where

(3.7) (3.8) - (ii)

For instance, in the case when , , and has the Gamma distribution with the shape and scale parameters equal to and , respectively, Proposition 3.3 yields (using ) and .

When , the quantile bound is simply the quantile , which can be effectively computed by formula (2.3), since the tail probability is monotone in . Next, as was noted in the proof of Theorem 2.4, is convex in when , which provides for an effective computation of by formula (2.8).

Therefore, it remains to consider the computation – again by formula (2.8) – of for . In such a case, as in Subsection 3.1, one can use an interval method. As soon as the minimizing values of are bracketed as in (3.6), one can partition the finite interval into a large number of small subintervals with . For each such subinterval,

so that, by the continuity of in ,

as , uniformly over all subintervals of the interval . Thus, one can effectively bracket the value ; this same approach will work, and perhaps may be useful, for as well.

***

If then, by part (ii) of Proposition 3.6 and part (i) of Proposition 3.3, the set is a singleton one; that is, there is exactly one minimizer of . If then is convex, but not strictly convex, in , and the set of all minimizers of in coincides with the set of all -quantiles of , as mentioned at the conclusion of the derivation of the identity (3.10). Thus, if , then the set may in general be, depending on and the distribution of , a nonzero-length closed interval. Finally, if then, in general, the set does not have to be connected:

Proposition 3.4.

For any , , and , there is a r.v. (taking three distinct values) such that and the infimum in (2.8) is attained at precisely two distinct values of .

Proposition 3.4 follows immediately from Proposition 3.1, by the duality (2.10) and the change-of-variables identity for , used to establish (1.7)–(1.9). At that, is one of the two minimizers of in Proposition 3.1 if and only if is one of the two minimizers of in Proposition 3.4.

Proposition 3.1 is illustrated by the following example, which is obtained from Example 3.2 by the same duality (2.10).

Example 3.5.

![[Uncaptioned image]](/html/1310.6025/assets/x7.png)

As in Example 3.2, let and let be a r.v. taking values with probabilities . Also let . Then the minimum of over all real equals and is attained at each of the two points, and , and only at these two points. The graph is shown here on the left. The minimizing values of here, and , are related with the minimizing values of in Example 3.2, and , by the mentioned formula (here with and ).

***

In the case , an expression of can be given in terms of the true -quantile :

| (3.10) |

That the expression for in (2.8) coincides with the one in (3.10) was proved in [52, Theorem 1] for absolutely continous r.v.’s and in [35, page 273] and [53, Theorem 10] in general. For the readers’ convenience, let us present here the following brief proof of (3.10). For all real and one has

It follows that the right derivative of the convex function at any point is , which, by (2.3), is if and if . Hence, is a minimizer in of , and thus (3.10) follows by (2.8). It is also seen now that any -quantile of is a minimizer in of as well, and is the largest of these minimizers.

As was shown in [53], the expression for in (3.10) can be rewritten as a conditional expectation:

| (3.11) |

where is any r.v. which independent of and uniformly distributed on the interval , , and is any real number in the interval such that

such a number always exists. Thus, the r.v. is used to split the possible atom of the distribution of at the quantile point in order to make the randomized tail probability exactly equal to . Of course, in the absence of such an atom, one can simply write

| (3.12) |

However, as pointed out in [52, 53], a variational formula such as (2.8) has a distinct advantage over such ostensibly explicit formulas as (3.10) and (3.11), since (2.8) allows for incorporation into specialized optimization problems, with additional restrictions, say on the distribution of ; cf. e.g. [52, Theorem 2].

Nonetheless, let us obtain an extension of the representation (3.10), valid for all . In accordance with [43, Proposition 3.2], consider

| (3.13) |

The following proposition will be useful.

Proposition 3.6.

-

(i)

If then is convex in .

-

(ii)

If then is strictly convex in .

-

(iii)

is strictly convex in unless for some .

Suppose at this point that . By part (i) of Proposition 3.3 (stated in Section 3), the minimum-attainment set

| (3.14) |

is nonempty and bounded. Also, this set is closed, by the continuity of in . Therefore, the definition

| (3.15) |

makes sense, and

| (3.16) |

thus, is the largest value of minimizing . Moreover, in the case when this largest minimizer is

| (3.17) |

the largest -quantile of , as stated at the end of the paragraph containing (3.10) and its proof. Thus, indeed the representation (3.10) is extended to all :

| (3.18) |

Further properties of are presented in

Proposition 3.7.

Suppose that . Then the following statements are true.

-

(i)

Computation of :

-

(a)

If then , where is as in (1.16).

-

(b)

Suppose here that and . Then , where is the only root of the equation and, again for ,

(3.19) Moreover,

(3.20) Furthermore, for all one has , and also as (assuming that for some ); in addition, for all .

-

(a)

-

(ii)

is nonincreasing in and for . Moreover, if then is strictly decreasing in and continuous in ; at that, and .

-

(iii)

is nonincreasing in in the sense that if and ; in particular,

(3.21) if . More specifically, if , , and , then ; if , , and , then . Moreover, if and , then .

-

(iv)

is consistent: for all .

-

(v)

is positive-homogeneous: for all .

-

(vi)

is translation-invariant: for all .

-

(vii)

is partially monotonic: if for some ; also, for any .

-

(viii)

However, for any and any , is not monotonic in all .

-

(ix)

Consequently, for any and any , is not subadditive or convex in all .

By (3.21), is a lower bound on the true -quantile of . Therefore and in view of part (i) of Proposition 3.7, may be referred to as the lower -quantile of the r.v. .

Example 3.8.

![[Uncaptioned image]](/html/1310.6025/assets/x8.png)

***

One may conclude this section by an obvious but oftentimes rather useful observation that – even when a minimizing value of or in formulas (1.5), (1.7), or (2.8) is not identified quite perfectly – one still obtains, by those formulas, an upper bound on or and hence on the true tail probability or the true quantile , respectively.

4 Implications for risk control/inequality modeling in finance/economics

In financial literature – see e.g. [35, 53, 24], the quantile bounds and are known as the value-at-risk and conditional value-at-risk, denoted as and , respectively:

| (4.1) |

here, is interpreted as a priori uncertain potential loss. The value of is also known as the expected shortfall (ES) [2], average value-at-risk (AVaR) [47], and expected tail loss (ETL) [26]. As indicated in [53], at least in the case when there is no atom at the quantile point , the quantile bound is also called the “mean shortfall” [28], whereas the difference is referred to as “mean excess loss” [17, 6].

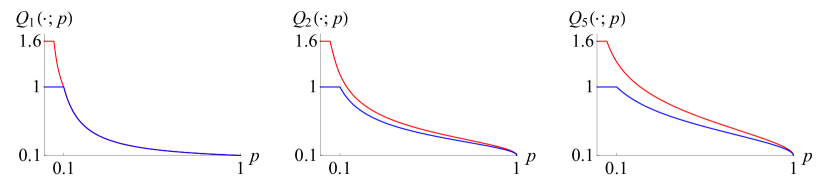

Greater values of correspond to greater sensitivity to risk; cf. e.g. [19]. For instance, let and denote the potential losses corresponding to two different investments portfolios. Suppose that there are mutually exclusive events and and real numbers and such that (i) , (ii) the loss of either portfolio is if the event does not occur, (iii) the loss of the -portfolio is if the event occurs, and (iv) the loss of the -portfolio is if the event occurs, and it is if the event occurs. Thus, the r.v. takes values and with probabilities and , and the r.v. takes values , , and with probabilities , , and , respectively. So, , that is, the expected losses of the two portfolios are the same. Clearly, the distribution of is less dispersed than that of , both intuitively and also in the formal sense that for all . Therefore, everyone will probably say that the -portfolio is riskier than the -portfolio. However, for any it is easy to see, by (2.3), that and hence, in view of (3.10), . Using also the continuity of in , as stated in Theorem 2.4, one concludes that the risk value of the riskier -portfolio is the same as that of the less risky -portfolio for all . Such indifference (which may also be referred to as insensitivity to risk) may generally be considered “an unwanted characteristic” [23, pages 36, 48].

Let us now show that, in contrast with the risk measure , the value of is sensitive to risk for all and all ; that is, for all such and and for the losses and as above, . Indeed, take any . By (1.16) and (3.13), , , , , and . If then, by part (ii) of Proposition 2.1, . If now then, by (3.20), . Also, by strict version of Jensen’s inequality and the strict convexity of in , for all . So, by (3.18) and (2.8), . Thus, it is checked that for all and all .

The above example is illustrated in Figure 2, for and . It is seen that the sensitivity of the measure to risk (reflected especially by the gap between the red and blue lines for ) increases from the zero sensitivity when to an everywhere positive sensitivity when to an everywhere greater positive sensitivity when .

***

Based on an extensive and penetrating discussion of methods of measurement of market and nonmarket risks, Artzner et al [3] concluded that, for a risk measure to be effective in risk regulation and management, it has to be coherent, in the sense that it possess the translation invariance, subadditivity, positive homogeneity, and monotonicity properties. In general, a risk measure, say , is a mapping of a linear space of real-valued r.v.’s on a given probability space into . The probability space (say ) was assumed to be finite in [3]. More generally, one could allow to be infinite, and then it is natural to allow to take values as well. In [3], the r.v.’s (say ) in the argument of the risk measure were called risks but at the same time interpreted as “the investor’s future net worth”. Then the translation invariance was defined in [3] as the identity for all r.v.’s and real numbers , where is a positive real number, interpreted as the rate of return. We shall, however, follow Pflug [35], who considers a risk measure (say ) as a function of the potential cost/loss, say , and then defines the translation invariance of , quite conventionally, as the identity for all r.v.’s and real numbers . The approaches in [3] and [35] are equivalent to each other, and the correspondence between them can be given by the formulas , , and . The positive homogeneity as defined in [3] can be stated as the identity for all r.v.’s and real numbers .

Corollary 4.1.

For each , the quantile bound is a coherent risk measure.

This follows immediately from Theorem 2.4.

The usually least trivial of the four properties characterizing the coherence is the subadditivity of a risk measure – which, in the presence of the positive homogeneity, is equivalent to the convexity, as was pointed out earlier in this paper. As is well known and also discussed above, the value-at-risk measure is translation invariant, positive homogeneous, and monotone (in ), but it fails to be subadditive. Quoting [53, page 1458]: “The coherence of [] is a formidable advantage not shared by any other widely applicable measure of risk yet proposed.” Corollary 4.1 above addresses this problem by providing an entire infinite family of coherent risk measures, indexed by , including just as one member of the family.

Theorem 2.4 also provides additional monotonicity and other useful properties of the spectrum of risk measures . The terminology we use to name some of these properties differs from the corresponding terminology used in [3]. Namely, what we referred to as the “sensitivity” in Theorem 2.4 corresponds to the “relevance” in [3]. Also, in the present paper the “model-independence” means that the risk measure depends on the potential loss only through the distribution of the loss, rather than on the way to model the “states of nature”, on which the loss may depend. In contrast, in [3] a measure of risk is considered “model-free” if it does not depend, not only on modeling the “states of nature”, but, to a possibly large extent, on the distribution of the loss. The “model-independence” property is called “law-invariance” in [21, Section 12.1.2], where the consistency property was referred to as “constancy”. An example of such a “model-free” risk measure is given by the Securities and Exchange Commission (SEC) rules, described e.g. in [3, Subsection 3.2]; this measure of risk depends only on the set of all possible representations of the investment portfolio in question as a portfolio of long call spreads, that is, pairs of the form (a long call, a short call). If a measure of risk is not “model-free”, then it is called “model-dependent” in [3].

***

Yitzhaki [58] utilized the Gini mean difference – which had prior to that been mainly used as a measure of economic inequality – to construct, somewhat implicitly, a measure of risk; this approach was further developed in [14, 11]. If (say) a r.v. is thought of as the income of randomly selected person in a certain state, then the Gini mean difference can be defined by the formula

where is an independent copy of and is a measurable function, usually assumed to be nonnegative and such that ; clearly, given the function , the Gini mean difference depends only on the distribution of the r.v. . So, if is considered, for any , as the measure of inequality between two individuals with incomes and such that , then the Gini mean difference is the mean -inequality in income between two individuals selected at random (and with replacement, thus independently of each other). The most standard choice for is the identity function , so that for all . Based on the measure-of-inequality , one can define the risk measure

| (4.2) |

where now the r.v. is interpreted as the uncertain loss on a given investment, with the term then possibly interpreted as a measure of the uncertainty. Clearly, when there is no uncertainty, so that the loss is in fact a nonrandom real constant, then the measure of the uncertainty is , assuming that . If (that is, is normally distributed with mean and standard deviation ) and for some positive constant , then , a linear combination of the mean and the standard deviation, so that in such a case we find ourselves in the realm of the Markowitz mean-variance risk-assessment framework.

It is assumed that is defined when both expected values in the last expression in (4.2) are defined and are not infinite values of opposite signs – so that these two expected values could be added, as needed in (4.2).

It is clear that is translation-invariant. Moreover, is convex in if the function is convex and nondecreasing. Further, if for some positive constant , then is also positive-homogeneous.

It was shown in [58], under an additional technical condition, that is nondecreasing in with respect to the stochastic dominance of order if . Namely, the result obtained in [58] is that if and the distribution functions and of and are such that changes sign only finitely many times on , then . A more general result was obtained in [14], which can be stated as follows: in the case when the function is differentiable, is nondecreasing in with respect to the stochastic dominance of order if and only if . Cf. also [11]. The proof in [14] was rather long and involved; in addition, it used a previously obtained result of [27]. Here we are going to give (in Appendix A) a very short, direct, and simple proof of the more general

Proposition 4.2.

The risk measure is nondecreasing in with respect to the stochastic dominance of order if and only if the function is -Lipschitz: for all and in .

In Proposition 4.2, it is not assumed that or that . Of course, if is differentiable, then the -Lipschitz condition is equivalent to the condition in [14].

The risk measure was called mean-risk (M-R) in [11].

It follows from [14] or Proposition 4.2 above that the risk measure is coherent for any . In fact, based on Proposition 4.2, one can rather easily show more:

Proposition 4.3.

The risk measure is coherent if and only if for some .

It is possible to indicate a relation – albeit rather indirect – of the risk measure , defined in (4.2), with the quantile bounds . Indeed, introduce

| (4.3) |

assuming exists in . By (2.8)–(2.9), is another majorant of , obtained by using in (2.8) as a surrogate of the minimizing value of .

The term in (4.3) is somewhat similar to the Gini mean-difference term , at least when and (the distribution of) the r.v. is symmetric about its mean.

Moreover, if the distribution of is symmetric and stable with index , then with .

One may want to compare the two considered kinds of coherent measures of risk/inequality, for and for and . It appears that the latter measure is more flexible, as it depends on two parameters ( and ) rather than one just one parameter (). Moreover, as Proposition 2.7 shows, rather generally retains a more or less close relation with the quantile – which, recall, is the widely used value-at-risk (VaR). On the other hand, recall here that, in contrast with the VaR, is coherent for . However, both of these kinds of coherent measures appear useful, each in its own manner, representing two different ways to express risk/inequality.

Formulas (4.2) and (4.3) can be considered special instances of the general relation between risk measures and measures of inequality established in [54]. Let be a convex cone of real-valued r.v. with a finite mean such that contains all real constants.

Largely following [54], let us say a coherent real-valued risk measure is strictly expectation-bounded if for all . (Note that here the r.v. represents the loss, whereas in [54] it represents the gain; accordingly, in this paper corresponds to in [54]; also, in [54] the cone was taken to be the space .) In view of Theorem 2.4 and part (vii) of Proposition 2.1, it follows that is a coherent and strictly expectation-bounded risk measure if . Also (cf. [54, Definition 1 and Proposition 1]), let us say that a mapping is a deviation measure if is subadditive, positive-homogeneous, and nonnegative with if and only if for some real constant ; here is any r.v. in . Next (cf. [54, Definition 2]), let us say that a deviation measure is upper-range dominated if for all . Then (cf. [54, Theorem 2]), the formulas

| (4.4) |

provide a one-to-one correspondence between all coherent strictly expectation-bounded risk measures and all upper-range dominated deviation measures .

In particular, it follows that the risk measure , defined by formula (4.3), is coherent for all and all . It also follows that is a deviation measure. As was noted, is a majorant of . In contrast with , in general will not have such a close hereditary relation with the true quantile as e.g. the ones given in Proposition 2.7. For instance, if is like then, by (2.13)–(2.14), for each , whereas for all real . On the other hand, in distinction with the definition (4.3) of , the expression (2.8) for requires minimization in ; however, that minimization will add comparatively little to the complexity of the problem of minimizing subject to a usually large number of restrictions on the distribution of ; cf. again e.g. [52, Theorem 2].

One may also consider the following modification of , which is still a majorant of , but is closer (than is) to the true quantile – at least when is close enough to (recall part (ii) of Proposition 3.7):

| (4.5) |

cf. (2.8).

The risk measure is coherent and strictly expectation-bounded given the condition , which will be assumed in this paragraph. The proof of the translation invariance, positive homogeneity, and subadditivity properties of is almost the same as the proof of these properties of , listed in Theorem 2.4. Then, to prove the monotonicity of (with respect to the order ), it is enough, in view of the subadditivity of and as in the proof of [54, Theorem 2], to show that implies , which obtains indeed, because and if . Finally, is strictly expectation-bounded, because it majorizes , which is strictly expectation-bounded, as noted.

***

Recalling (1.28) and following [31, 32, 33], one may also consider as a measure of risk. Here one will need the following semigroup identity, given in [31, (8a)] (cf. e.g. [38, Remark 3.7]):

| (4.6) |

whenever . The following proposition is well known.

Proposition 4.4.

If the r.v. is nonnegative then

| (4.7) |

where is the Lorenz curve function, given by the formula

| (4.8) |

Indeed, the first equality in (4.7) is the special case of the identity (4.6) with and , and the second equality in (4.7) follows by [30, part (i) of Theorem 3.1], identity (2.8) for , and the second identity in (4.1). Cf. [25, Theorem 2] and [4, 29].

Using (4.6) with , in place of , and in place of together with Proposition 4.4, one has

| (4.9) |

for any . Since is a coherent risk measure, it now follows that, as noted in [32], is a coherent risk measure as well, again for ; by (4.7), this conclusion will hold for . However, one should remember that the expression was defined only when the r.v. is nonnegative (and otherwise some of the crucial considerations above will not hold). Thus, the risk measure is defined only if almost surely.

In view of (4.9), this risk measure is a mixture of the coherent risk measures and thus a member of the general class of the so-called spectral risk measures [1], which are precisely the mixtures, over the values , of the risk measures ; thus, all spectral risk measures are automatically coherent. However, in general such measures will lack such an important variational representation as the one given by formula (2.8) for the risk measure . Of course, for any “mixing” nonnegative Borel measure on the interval and the corresponding spectral risk measure

one can write

| (4.10) |

in view of (4.1) and (2.8)–(2.9). However, in contrast with (2.8), the minimization (in ) in (4.10) needs in general to be done for each of the infinitely many values of . If the r.v. takes only finitely many values, then the expression of in (4.10) can be rewritten as a finite sum, so that the minimization in will be needed only for finitely many values of ; cf. e.g. the optimization problem on page 8 in [32].

On the other hand, one can of course consider arbitrary mixtures in and/or of the risk measures . Such mixtures will automatically be coherent. Also, all mixtures of the measures in will be nondecreasing in , and all mixtures of in will be nonincreasing in .

Deviation measures such as the ones studied in [54] and discussed in the paragraph containing (4.4) can be used as measures of economic inequality if the r.v. models, say, the random income/wealth – defined as the income/wealth of an (economic) unit chosen at random from a population of such units. Then, according to the one-to-one correspondence given by (4.4), coherent risk measures translate into deviation measures , and vice versa.

However, the risk measures themselves can be used to express certain aspects of economic inequality directly, without translation into deviation measures. For instance, if stands for the random wealth then the statement formalizes the common kind of expression “the wealthiest 1% own 30% of all wealth”, provided that the wealthiest 1% can be adequately defined, say as follows: there is a threshold wealth value such that the number of units with wealth greather than or equal to is , where is the number of units in the entire population. Then (cf. (3.12)) , whence indeed . Similar in spirit expressions of economic inequality in terms of can be provided for all . For instance, suppose now that stands for the annual income of a randomly selected household, whereas is a particular annual household income level in question. Then, in view of (2.8)–(2.9), the inequality means that for any (potential) annual household income level less than the maximum annual household income level in the population, the conditional -mean of the excess of the random income over is no less than times the excess of the income level over . Of course, the conditional -mean is increasing in . Thus, using the measure of economic inequality with a greater value of means treating high values of the economic variable in a more progressive/sensitive manner. One may also note here that the above interpretation of the inequality is a “synthetic” statement in the sense that is provides information concerning all values of potential interest of the threshold annual household income level .

Not only the upper bounds on the quantile , but also the upper bounds on the tail probability may be considered measures of risk/inequality. Indeed, if is interpreted as the potential loss, then the tail probability corresponds to the classical safety-first (SF) risk measure; see e.g. [55, 22].

Using variational formulas – of which formulas (1.5), (1.7), and (2.8) are examples – to define or compute measures of risk is not peculiar to the present paper. Indeed, as mentioned previously, the special case of (2.8) with is the well-known variational representation (3.10) of , obtained in [52, 35, 53]. The risk measure given by the SEC rules [3, Subsection 3.2], also mentioned before, is another example where the calculations are done, in effect, according to a certain minimization formula, which is somewhat implicit and complicated in that case.

One can now list some of the advantages of the risk/inequality measures and :

-

•

and are three-way monotonic and three-way stable – in , , and .

-

•

The monotonicity in is graded continuously in , resulting in various, controllable degrees of sensitivity of and to financial risk/economic inequality.

-

•

is the tail-function of a certain probability distribution.

-

•

is a -percentile of that probability distribution.

-

•

For small enough values of the quantile bounds are close enough to the corresponding true quantiles provided that the right tail of the distribution of is light enough and regular enough, depending on .

-

•

and are solutions to mutually dual optimizations problems, which can be comparatively easily incorporated into more specialized optimization problems, with additional restrictions, say on the distribution of the random variable .

-

•

and are effectively computable.

-

•

Even when the corresponding minimizer is not identified quite perfectly – one still obtains an upper bound on the risk/inequality measures or .

- •

-

•

The quantile bounds with constitute a spectrum of coherent measures of financial risk and economic inequality.

-

•

The r.v.’s of which the measures and are taken are allowed to take values of both signs. In particular, if, in a context of economic inequality, is interpreted as the net amount of assets belonging to a randomly chosen economic unit, then a negative value of corresponds to a unit with more liabilities than paid-for assets. Similarly, if denotes the loss on a financial investment, then a negative value of will obtain when there actually is a net gain.

Some of these advantages, and especially their totality, appear to be unique to the bounds proposed here.

Appendix A Proofs

Proof of Proposition 1.1.

Parts (ii) and (iii) follow by (1.7)–(1.9). Indeed, for all real and if , and for all real and if for all real .

Concerning part (iv) of Proposition 1.1, assume indeed that and . Then, for any , (1.7)–(1.9) imply as . On the other hand, obviously for all real . So, indeed, as .

Thus, part (iv) of Proposition 1.1 is proved.

The proof of part (v) is rather similar to that of part (iv). Assume indeed that and for some real . Then as . Since for all real , one indeed has as .

As for the proof of the statement that as for , it is the same as the corresponding proof for .

Thus, part (v) of Proposition 1.1 is proved as well. ∎

Proof of Proposition 1.2.

(i) Let us first verify part (i). For , this follows immediately from the equality in (1.6) and the definitions in (1.16).

Take then any . Take indeed any .

If and , then ; so, by (1.3), the condition , and dominated convergence, . The case is similar: .

(iii) Concerning part (iii) of Proposition 1.2, consider first the case . Then, by (1.7), the function

| (A.1) |

is the pointwise supremum, in , of the family of continuous convex functions . So, the function (A.1) is convex. It is also finite on the interval , by part (ii) of Proposition 1.2. So, the function (A.1) is continuous on . Moreover, this function is lower-semicontinuous and nondecreasing, and hence continuous at the point , in the case when . Thus, the function (A.1) is continuous on the entire set , with respect to the natural topologies on and .

The case is considered quite similarly. Here, instead of (A.1), one works with the function

| (A.2) |

which is the pointwise supremum, in real such that , of the family of continuous convex (in fact, affine) functions . (Actually, the values of the latter family of functions are all real, for such that , whereas all the values of the function (A.2) are in ; however, here we take the union, , of the sets and as an interval which is guaranteed to contain all possible values of all the convex functions under consideration.) Here we also use the standard conventions and ; concerning the continuity of functions with values in the set , we use the natural topology on this set.

(iv) Let us now turn to part (iv) of Proposition 1.2. Consider first the case . Then, since the map is continuous, it follows by part (iii) of Proposition 1.2 that is indeed continuous in and left-continuous in at if . The case is quite similar; here, instead of the map , one should use the continuous map .

(v) That the function is left-continuous follows immediately from parts (iv) and (i) if , and from the equality in (1.6) if .

(vi) That is nondecreasing in follows immediately from the definition of in (1.17) and (1.13). That follows because, by (1.15), as .

On the other hand, if then for all in a right neighborhood of – because the right derivative of in at is ; therefore, , and so, again by (1.13), for all .

Let us show that if and only if . By the definition of in (1.17) and (1.15), for all . So, by part (v) of Proposition 1.2 and the inequality in part (vi) of Proposition 1.2,

| (A.3) |

If now , then by the definition of in (1.16); so, by part (i) of Proposition 1.2 and (A.3), , which proves the implication . Vice versa, suppose that . Then necessarily . Moreover, by part (i) of Proposition 1.1 and part (i) of Proposition 1.2, for all one has , so that and hence . Now the conclusion follows by the already established inequality .

(ix) By the definition of in (1.17) and part (i) of Proposition 1.1, the set is an interval with endpoints and . So, by the inequality in part (vi) of Proposition 1.2, . Thus, to verify part (ix) of Proposition 1.2, it is enough to show that . If then this follows immediately from the definition of in (1.18) as a subset of , and if then the same conclusion follows by (A.3).

(x) Part (x) of Proposition 1.2 follows immediately from part (ix) of Proposition 1.2 and the inequality , which latter in turn follows by (1.15).

(xi) Consider first the case . By part(i) of Proposition 1.1 and (1.15), the function (A.1) is nondecreasing, from the value at . It is easy to see that these conditions, together with the convexity of the function (A.1), imply that this function is strictly increasing on the set . In view of part (ii) of Proposition 1.2, this implies that the function is strictly decreasing on the set , which is the same as , by part (ix) of Proposition 1.2. The conclusion in part (xi) of Proposition 1.2 for now follows by its part (iv). The case is quite similar, where one uses, instead of (A.1), the function (A.2), whose limit at is . ∎

Proof of Proposition 1.4.

Let and a sequence be indeed as in Proposition 1.4. If then the desired conclusion follows immediately from part (i) of Proposition 1.2. Therefore, assume in the rest of the proof of Proposition 1.4 that

| (A.4) |

Then (3.4) takes place and, by (3.3), is continuous in . So,

| (A.5) |

and

| (A.6) |

Also, by (1.3), (1.2), the inequality (3.1) for , the condition , and dominated convergence,

| (A.7) |

Hence, by (1.5), for all , whence, again by (1.5),

| (A.8) |

If then for any and such that one has

| (A.9) |

this follows because

If now then (say, by cutting off an initial segment of the sequence ) one may assume that , and then, by (A.9) with in place of , the sequence is equicontinuous in , uniformly in . Therefore, by (A.5) and the Arzelà–Ascoli theorem, the convergence in (A.7) is uniform in and hence the conclusion follows by (A.6) – in the case when .

Quite similarly, the same conclusion holds if ; that is, is left-continuous in at the point provided that .

Proof of Proposition 1.5.

This is somewhat similar to the proof of Proposition 1.4. One difference here is the use of the uniform integrability condition, which, in view of (1.3), (3.1), and the condition , implies (see e.g. [10, Theorem 5.4]) that for all

| (A.10) |

here, in the case when and , one should also use the Fatou lemma for the convergence in distribution [10, Theorem 5.3], according to which one always has , even without the uniform integrability condition. In this entire proof, it is indeed assumed that .

Using the same ingredients, it is easy to check part (ii) of Proposition 1.5 as well. Indeed, assuming that and using also (1.6), one has

which yields (1.21) for . Also, implies ; see e.g. [10, Theorem 2.1]. So, if , then and hence (1.21) holds for , by the first sentence of part (ii) of Proposition 1.5.

It remains to prove part (i) of Proposition 1.5 assuming (A.4). The reasoning here is quite similar to the corresponding reasoning in the proof of Proposition 1.4, starting with (A.4). Here, instead of the continuity of in , one should use the convergence , which holds provided that is chosen to be such that . Concerning the use of inequality (A.9), note that (i) the uniform integrability condition implies that is bounded in and (ii) the convergence in distribution implies that as . Proposition 1.5 is now completely proved. ∎

Proof of Theorem 1.6.

The model-independence is obvious from the definition (1.5). The monotonicity in follows immediately from (1.22), (1.10), and (1.7)–(1.9). The monotonicity in was already given in (1.13). The monotonicity in is part (i) of Proposition 1.1. That takes on only values in the interval follows immediately from (1.15). The -concavity in and stability in follow immediately from parts (iii) and (i) of Proposition 1.2. The stability in and the stability in are Propositions 1.4 and 1.5, respectively. The translation invariance, consistency, and positive homogeneity follow immediately from the definition (1.5). ∎

Proof of Proposition 2.1.

(ii) Suppose here indeed that . Then for any one has , by part (i) of Proposition 1.2, whence, by (1.18), . On the other hand, for any one has , by part (i) of Proposition 1.1 and part (i) of Proposition 1.2, whence . So, , and the conclusion now follows by the definition of in (2.2).

(iii) If then the inequality in part (iii) of Proposition 2.1 is trivial. If and , then and hence by (2.2). Now part (iii) of Proposition 2.1 follows from its part (ii).

(iv) Take any . Then . Moreover, for all one has . Therefore and because the set is an interval with endpoints and , it follows that . Thus, for any given and for all small enough one has and hence, by the already established part (iii) of Proposition 2.1, . This means that part (iv) of Proposition 2.1 is proved for . To complete the proof of this part, it remains to refer to the monotonicity of in stated in (2.4) and, again, to part (iii) of Proposition 2.1.

(v) Assume indeed that . By part (viii) of Proposition 1.2, the case is equivalent to , and in that case both mappings (2.6) and (2.7) are empty, so that part (v) of Proposition 2.1 is trivial. So, assume that and, equivalently, . The function is continuous and strictly decreasing, by parts (iv) and (xi) of Proposition 1.2. At that, by parts (iv) and (i) of Proposition 1.2 if , and by (1.15) and (1.16) if . Also, by the condition and parts (iv) and (x) of Proposition 1.2 if , and by (1.15) if . Therefore, the continuous and strictly decreasing function maps onto , and so, formula (2.7) is correct, and there is a unique inverse function, say , to the function (2.7); moreover, this inverse function is continuous and strictly decreasing. It remains to show that for all . Take indeed any . Since the function is inverse to (2.7) and strictly decreasing, , for , and for . So, by part (i) of Proposition 1.1, for and for . Now the conclusion that for all follows by (2.2).

(vi) Assume indeed that and take indeed any . If then the conclusion in part (vi) of Proposition 2.1 is trivial, in view of (2.1). So, w.l.o.g. and hence , by (1.18) and part (ix) of Proposition 1.2. Let now for brevity, so that and, by the already verified part (iii) of Proposition 2.1, . Therefore, . So, by part (v) of Proposition 2.1 and parts (iv) and (i) of Proposition 1.2,

| (A.12) |

which yields the conclusion in the case when . If now then and, by part (v) of Proposition 2.1, and , so that the conclusion follows by (A.12) in this case as well.

Proof of Theorem 2.4.

The model-independence, monotonicity in , monotonicity in , translation invariance, consistency, and positive homogeneity properties of follow immediately from (2.2) and the corresponding properties of stated in Theorem 1.6.

Concerning the monotonicity of in : that is nondecreasing in follows immediately from (2.3) for and from (2.8) and (2.9) for . That is strictly decreasing in if follows immediately from part (v) of Proposition 2.1 and the verified below statement on the stability in : is continuous in if .

The concavity of in in the case when follows by (2.8), since is affine (and hence concave) in . Similarly, the concavity of in follows by (2.8), since is affine in .

The stability of in can be deduced from Proposition 2.1. Alternatively, the same follows from the already established finiteness and concavity of in or (cf. the proof of [53, Proposition 13]), because any finite concave function on an open interval of the real line is continuous, whereas the mappings and are homeomorphisms.

Concerning the stability of in , take any real . Then the convergence holds, by Proposition 1.5. So, in view of (1.18), if then eventually (that is, for all large enough ) . Hence, by (2.2), for each real such that eventually one has . It follows that On the other hand, by part (vi) of Proposition 2.1, for any one has and hence eventually , which yields and hence . It follows that . Recalling now the established inequality , one completes the verification of the stability of in .

The stability of in is proved quite similarly, only using Proposition 1.4 in place of Proposition 1.5. Here the stipulation is not needed.

Consider now the sensitivity property.

First, suppose that .

Then, for all real , the derivative of in is less than

, where .

The inequality can be rewritten as the true inequality for the convex function , where .

So, the derivative is negative and hence decreases in (here, to include , we also used the continuity of in , which follows by the condition and

dominated convergence). On the other hand, if then . Also, by (2.9) if the condition holds. Recalling again the continuity of in , one completes the verification of the sensitivity property – in the case .

The sensitivity property in the case follows by (3.10). Indeed, (3.10) yields if , and

by the condition if ;

moreover, one has and hence if and .

On the other hand, by (2.3), implies .

Thus, the sensitivity property in the case is verified is well.

This and the already established monotonicity of in implies the sensitivity property whenever .

As far as this property is concerned, it remains to verify it when – assuming that . The sets and are intervals with the right endpoint .

The condition means that .

By the right continuity of in ,

the set contains the closure of the set .

So, and hence , by (2.3).

Thus, the sensitivity property is fully verified.

In the presence of the positive homogeneity, the subadditivity property is easy to see to be equivalent to the convexity; cf. e.g. [51, Theorem 4.7].

Therefore, it remains to verify the convexity property.

Assume indeed that .

If at that , then the function is a norm and hence convex; moreover, this function is nondecreasing on the set of all nonnegative r.v.’s. On the other hand, the function is nonnegative and convex. It follows by (2.9) that

is convex in the pair .

So, to complete the verification of the convexity property of in the case , it remains to refer to the well-known and easily established fact that, if is convex in , then is convex in ; cf. e.g. [51, Theorem 5.7].

The subadditivity and hence

convexity of in in the remaining case

can now be obtained

by the already established stability in .

It can also be deduced

from [49, Lemma B.2] (cf. [48, Lemma 2.1]) or

from by the main result in [46], in view of the inequality

given in the course of the discussion following

[46, Corollary 2.2] therein.

However, a direct proof, similar to the one above for , can be based on the observation that is convex in the pair .

Since is obviously linear in , the convexity of in means precisely that

for any natural number , any r.v.’s , any positive real numbers , and any positive real numbers with , one has the inequality

, where

and ; but the latter inequality can be rewritten as an instance of Hölder’s inequality:

, where and (so that ).

(In particular, it follows that is convex in , which is useful when is computed by formula (2.8).)

The proof of Theorem 2.4 is now complete. ∎

Proof of Proposition 2.5.

Consider first the case . Let r.v.’s and be in the default domain of definition, , of the functional . The condition and the left continuity of the function imply that for any there are some and such that for all . On the other hand, by the Fubini theorem, for all . Recalling also that and are in , one has for all . By Proposition 3.3, for some . So, . (Note that the proof of Proposition 3.3, given later in this appendix, does not use Proposition 2.5 – so that there is no vicious circle here.)

Proof of Proposition 2.6.

Suppose that indeed . Let and be independent r.v.’s, each with the Pareto density function given by the formula , so that for all . Then, by the condition , the condition (assumed by default in this paper and, in particular, in Proposition 2.5) holds; this is the only place in the proof of Proposition 2.6 where the condition is used. Also, then it is not hard to see that for all one has and hence, by the definition of the relation given in Proposition 2.5,

Using now Proposition 2.5 together with the positive homogeneity property stated in Theorem 2.4, one concludes that if .

It remains to consider the case . Note that the function is decreasing strictly and continuously from to . So, in view of (2.3), the function is the inverse to the function . Similarly, the function is the inverse to the strictly decreasing continuous function . Since for all , it follows that and thus the inequality holds for as well. ∎

Proof of Proposition 2.7.

(i) The equalities in (2.12) follow immediately from part (iv) of Proposition 2.1. The condition in (2.12) follows from the condition – because, by the definition of in (1.16), one always has . Thus, part (i) of Proposition 2.7 is verified.

(ii) Take any and suppose that indeed is like . Then, in view of (2.11) and because the function was supposed to be positive on , one observes that for all large enough real . Therefore and because is nondecreasing in , in fact for all real . In particular, it now follows that indeed . Moreover, recalling the definition (1.18) of and the equality in (1.6), one sees that for any real and all in the (nonempty) right neighborhood of , one has ; therefore and because, by the definition (2.2) of , the set is an interval with endpoints and , one concludes that for all . Thus, for ; that the same limit relation holds for any now follows immediately by the monotonicity of in , as stated in (2.4).

To complete the proof of Proposition 2.7, it remains to verify (2.13). First here, consider the case , so that . For brevity, let

Then

| (A.13) |

the latter asymptotic relation is an extension of, and proved quite similarly to, the asymptotic relation (2.11b). Introduce also

Let indeed , as in (2.13). Then

| (A.14) |

Because the set is an interval with endpoints and , one has and , whence

| (A.15) |

On the other hand, by [38] (see Corollary 2.3, duality relation (4), Theorem 4.2, and Remark 4.3 there),

| (A.16) |

note that the condition “ is like ” in part (ii) of Proposition 2.7 corresponds to the condition “ as for some which is like ” in [38, Remark 4.3], because the notion “like ” is defined in the present paper slightly differently from [38]. Combining (A.15) and (A.16), one has

| (A.17) |

here and elsewhere, or, equivalently, means, by definition, that for some nonnegative function . Also, (A.15) with can be written as

Comparing this with (A.17) and recalling (A.13), one sees that

Therefore and because of (A.14),

so that . Quite similarly, , which shows that indeed (2.13) holds – in the case .

Proof of Proposition 3.1.

Take indeed any and . Note that there are real numbers , , and such that

| (A.18) |

Indeed, if , , and , where , then all of the conditions in (A.18) will be satisfied, possibly except the condition , which latter will be then equivalent to the condition . However, this condition can be satisfied by letting be small enough – because .

If now , , and satisfy (A.18), then there is a r.v. taking values , , and with probabilities , , and , respectively. Let indeed be such a r.v. Then for all

| (A.19) |

Moreover, by the condition , the function is strictly concave on each of the intervals , , and . So, the minimum of in equals and is attained precisely at two distinct positive values of . Thus, in the case , Proposition 3.1 follows by (A.19). The case of a general immediately reduces to that of by using the shifted r.v. in place of . ∎

Proof of Proposition 3.3.

Consider first part (i) of the proposition. For any real one has . On the other hand, by (3.8), for all real one has , whence provided that also . Thus, if either or . This, together with the continuity of in , completes the proof of part (i) of Proposition 3.3.

Concerning part (ii) of the proposition, consider first

Case 1: . Take then any real such that and then any real such that ; note that , since . Then for any real one has and hence

| (A.20) |

provided that

the latter inequality is in fact equivalent to the strict inequality in (A.20); recall here also that and , whence . Taking now into account that is lower semi-continuous in (by Fatou’s lemma) and as , one concludes that

which completes the consideration of Case 1 for part (ii) of the proposition. It remains to consider

Case 2: . Note that is translation invariant in the sense that for all and . Therefore, without loss of generality , so that a.s. and for all real . Now, by dominated convergence, and , whence

| (A.21) |