A Tractable State-Space Model for Symmetric Positive-Definite Matrices

Abstract

Bayesian analysis of state-space models includes computing the posterior distribution of the system’s parameters as well as filtering, smoothing, and predicting the system’s latent states. When the latent states wander around there are several well-known modeling components and computational tools that may be profitably combined to achieve these tasks. However, there are scenarios, like tracking an object in a video or tracking a covariance matrix of financial assets returns, when the latent states are restricted to a curve within and these models and tools do not immediately apply. Within this constrained setting, most work has focused on filtering and less attention has been paid to the other aspects of Bayesian state-space inference, which tend to be more challenging. To that end, we present a state-space model whose latent states take values on the manifold of symmetric positive-definite matrices and for which one may easily compute the posterior distribution of the latent states and the system’s parameters, in addition to filtered distributions and one-step ahead predictions. Deploying the model within the context of finance, we show how one can use realized covariance matrices as data to predict latent time-varying covariance matrices. This approach out-performs factor stochastic volatility.

Keywords: backward sample, covariance, dynamic, forward filter

1 Introduction

A state-space model is often characterized by an observation density for the responses and a transition density for the latent states . Usually, the latent states can take on any value in ; however, there are times when the states or the responses are constrained to a manifold embedded in . For instance, econometricians and statisticians have devised symmetric positive-definite matrix-valued statistics that can be interpreted as noisy observations of the conditional covariance matrix of a vector of daily asset returns. In that case, it is reasonable to consider a state-space model that has covariance matrix-valued responses (the statistics) and covariance matrix-valued latent quantities (the time-varying covariance matrices).

Unfortunately, devising state-space models on curved spaces (like the set of covariance matrices) that lend themselves to Bayesian analysis is not easy. Just writing down the observation and transition densities can be difficult in this setting, since one must define distributions on curved spaces. Asking that these densities then lead to some recognizable posterior distribution for the latent states and the system’s parameters compounds the problem. Filtering is slightly less daunting, since one can appeal to sequential methods. (Filtering or forward filtering refers to iteratively deriving the filtered distributions where is the data and represents the system’s parameters.) Approximate methods can also flounder. For instance, when and exist in planar spaces, it is common to write down observation and evolution equations and only specify the first and second moments of the evolution innovations and observation errors, which leads to tractable methods for filtering. However, the notions of mean and variance do not translate automatically to curved spaces and hence even this density-less approach runs into trouble.

Despite these difficulties, it is still of interest to develop state-space models for the set of covariance matrices and other curved spaces, since such data exists. In addition to the financial application described previously, time-varying covariance matrices arise in computer vision (Porikli et al., 2006), and time varying linear subspaces arise in subspace tracking (Srivastava and Klassen, 2004). Some work has explored forward filtering such data. Tyagi and Davis (2008) develop a Kalman-like filter (Kalman, 1960) for symmetric positive-definite matrices while Hauberg et al. (2013) develop an algorithm similar to the unscented Kalman filter (Julier and Uhlmann, 1997) for geodesically complete manifolds. Several collaborations have made use of particle filters: Srivastava and Klassen (2004) for the Grassmann manifold, Tompkins and Wolfe (2007) for the Steifel manifold, Kwon and Park (2010) for the affine group, and Choi and Christensen (2011) for the special Euclidean group.

None of these approaches have produced a state-space model amenable to fully Bayesian inference—inference in which one can compute both the conditional and marginalized versions of the filtered, smoothed, and predictive distributions (where the conditioning and marginalizing is with respect to ) in addition to the joint posterior distribution of the latent states and the system’s parameters. (Smoothing refers to computing the distribution of past states while predicting refers to computing the distribution of future states.) One attempt in that direction, Prado and West (2010) (p. 273), partially address these issues for dynamic covariance matrices, but informally and with less flexibility than the forthcoming.

We fully address these issues for a state-space model with symmetric positive-definite or positive semi-definite rank- observations and symmetric positive-definite latent states. (Let denote the set of order , rank , symmetric positive semi-definite matrices and let denote the set of order , symmetric positive-definite matrices.) The model builds on the work of Uhlig (1997), who showed how to construct a state-space model with observations and hidden states and how, using this model, one can forward filter in closed form. We extend his approach to observations of arbitrary rank and show how to forward filter, how to backward sample, and how to marginalize the hidden states to estimate the system’s parameters, all without appealing to fanciful MCMC schemes. (Backward sampling refers to taking a joint sample of the posterior distribution of the latent states using the conditional distributions .) The model’s estimates and one-step ahead predictions are exponentially weighted moving averages (also known as geometrically weighted moving averages). Exponentially weighted moving averages are known to provide simple and robust estimates and forecasts in many settings (Brown, 1959).

1.1 A comment on the original motivation

Our interest in covariance-valued state-space models arose from studying the realized covariance statistic, which within the context of finance, roughly speaking, can be thought of as a good estimate of the covariance matrix of a collection of daily asset returns. (The daily period is somewhat arbitrary; one may pick any reasonably “large” period.) We had been exploring the performance of factor stochastic volatility models, along the lines of Aguilar and West (2000), which use daily returns, versus exponentially weighted moving averages of realized covariance matrices and found that exponentially smoothing realized covariance matrices out-performed the more complicated factor stochastic volatility models. (Exponential smoothing refers to iteratively calculating a geometrically weighted average of observations and some initialization parameter.) As Bayesians, we wanted to find a model-based approach that is capable of producing similar results and the following fits within that role. To that end, as shown in Section 3, this simple model, used in conjunction with realized covariances, provides better one-step ahead predictions of daily covariance matrices than factor stochastic volatility (which only uses daily returns).

However, the specificity of this original application distracts from the larger problem of devising state-space models on the set of covariance matrices or on curved spaces more generally. As noted previously, it is difficult to devise tractable state-space models in this setting. It is within this more general problem that we find the model most notable.

2 A Covariance Matrix-Valued State-Space Model

The model herein is closely related to several models found in the Bayesian literature, all of which have their origin in variance discounting techniques (Quintana and West, 1987; West and Harrison, 1997). Uhlig (1997) provided a rigorous justification for variance discounting, showing that it is a form of Bayesian filtering for covariance matrices, and our model can be seen as a direct extension of Uhlig’s work. (Shephard (1994) constructs a similar model, but only for the univariate case.) The model of Prado and West (2010) (p. 273) is similar to ours, though less flexible.

Uhlig (1997) considers observations, , , that are conditionally normal given the hidden states , which take values in . We will henceforth write vectors in bold lower case and matrices in bold upper case. In particular, assuming , his model is

where is an integer and is the multivariate beta distribution, which is defined in Section 5. This model possesses closed form formulas for forward filtering that only requires knowing the outer product ; thus, one may arrive at equivalent estimates of the latent states by letting and using the observation distribution

where is the order Wishart distribution with degree of freedom and scale matrix as defined in Section 5. We show that one can extend this model for of any rank:

| (UE) |

where and is an integer less than or is a real number greater than . (When is an integer less than , has rank .) Many of the mathematical ideas needed to motivate Model UE (for Uhlig extension) can be found in a sister paper (Uhlig, 1994) to the Uhlig (1997) paper, and Uhlig could have written down the above model given those results; though, he was focused specifically on the rank-deficient case, and the rank-1 case in particular, as his 1997 work shows. We contribute to this discourse by constructing the model in a fashion that makes sense for observations of all ranks, show that one may backward sample to generate a joint draw of the hidden states, and demonstrate that one may marginalize the hidden states to estimate the system’s parameters , , and .

Model UE has a slightly different form and significantly more flexibility than the model of Prado and West (2010) (see p. 273), which is essentially

As noted by Prado and West, is constrained “to maintain a valid model, since we require either or be integral [and less than ]. The former constraint implies that cannot be too small, defined by the limiting value.” If is integral, then . Thus, one cannot pick from a range of for , when must be an integer, which means there are only allowed values of for , the limiting value when is sufficiently large. When is large this is a severe restriction. Further, for , produces the smallest possible value of ; thus, cannot be below unless . (We have replaced Prado and West’s by and their by .) The parameter is important since it controls how much the model smooths observations when forming estimates and one-step ahead predictions; thus the constraints on are highly undesirable. In contrast, our model lets take on any value.

Given Model UE, we can derive several useful propositions. The proofs of these propositions, which synthesize and add to results from Uhlig (1994), Muirhead (1982) Díaz-García and Jáimez (1997), are technical, and hence we defer their presentation to Section 5. Presently, we focus on the closed form formulas that one may make use of when forward filtering, backward sampling, predicting one step into the future, and estimating , , and .

First, some notation: inductively define the collection of data for with where is some covariance matrix. Let the prior for be where is the Wishart distribution with degrees of freedom and scale matrix . (See Definition 4 for details.) In the following, we implicitly condition on the parameters , , and .

Proposition 1 (Forward Filtering).

Suppose . After observing , the updated distribution is

where

Evolving one step leads to

Proposition 2 (Backward Sampling).

The joint density of can be decomposed as

(with respect to the product measure on the -fold product of embedded in with Lebesgue measure) where the distribution of is a shifted Wishart distribution

Proposition 3 (Marginalization).

The joint density of of is given by

with respect to the differential form where is as found in Definition 4 for either the rank-deficient or full-rank cases, depending on the rank of . (Differential forms, otherwise known as -forms, are vector fields that may be used to simplify multivariate analysis. In particular, one may define densities with respect to differential forms. Mikusiński and Taylor (2002) provide a good introduction to differential forms while Muirhead (1982) shows how to use them for statistics.) The density is

with respect to in the rank-deficient case and is

with respect to in the full-rank case, where , and with like above.

Examining the one-step ahead forecasts of elucidates how the model smooths. Invoking the law of iterated expectations, one finds that . Since is an inverse Wishart distribution, its expectation is proportional to . Solving the recursion for from Fact 1 shows that

| (1) |

Thus, the forecast of will be a scaled, geometrically weighted average of the previous observations. If, further, one enforces the constraint

| (2) |

then taking a step from to does not change its harmonic average, that is . It also implies that the one-step ahead point forecast of is

| (3) |

Hence in the constrained case, the one-step ahead forecast is the geometrically weighted average of past observations. For a geometrically weighted average, the most recent observations are given more weight as decreases. It has been known for some time that such averages provide decent one-step ahead forecasts (Brown, 1959).

3 Example: Covariance Forecasting

As noted initially, Model UE is an extension of the one proposed by Uhlig (1997). For the original model, when , one might consider observing a vector of heteroskedastic asset returns where the precision matrix changes at each time step. The extended model allows the precision matrix to change less often than the frequency with which the returns are observed. For instance, one may be interested in estimating the variance of the daily returns, assuming that the variance only changes from day to day, using multiple observations taken from within the day.

To that end, suppose the vector of intraday stock prices evolves as geometric Brownian motion so that on day the -vector of log prices is

at time , where the fraction of the trading day that has elapsed, is an -dimensional Brownian motion, and . In practice, is essentially zero, so we will ignore that term. Further, suppose one has viewed the vector of prices at equispaced times throughout the day so that Then and is distributed as . Letting where computes the upper Cholesky decomposition and , we recover Model UE exactly. Of course, in reality, returns are not normally distributed; they are heavy tailed and there are diurnal patterns within the day. Nonetheless, the realized covariance literature, which we discuss in more detail in Section A, suggests that taking to be an estimate of the daily variance is a reasonable thing to do; though to suppose that the error is Wishart is a strong assumption. More dubious is the choice of the evolution equation for ; a point we discuss further in Section 4. But the evolution equation for does provide a likelihood that accommodates closed form forward filtering and backward sampling formulas, and possesses only a few parameters, which makes it a relatively cheap model to employ.

The one mild challenge when applying the model is estimating . However, it is possible to “cheat” and not actually estimate at all. Consider (1) and ponder the following two observations. First, is a geometrically weighted sum in . Second, the least important term in the sum is . Thus, one can reasonably ignore if is large enough. To that end, we suggest setting aside the first observations and using where to learn , , and using Proposition 3 and the prior . It may seem costly to disregard the first observations, but since there are so few parameters to estimate this is unlikely to be a problem—the remaining data will suffice.

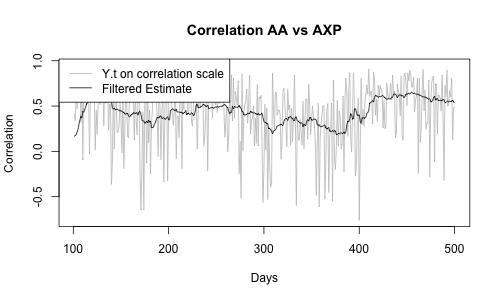

On the left is the log posterior of calculated using and constraint (2). The black line is the log posterior in , which has a mode at corresponding to . The grey line is as a function of . On the right are the values of and the estimate for on the correlation scale. A truncated time series was used to provide a clear picture.

This is the process used to generate Figure 1 (with and ). The data set follows the stocks that comprised the Dow Jones Industrial Average in October, 2010. Eleven intraday observations were taken every trading day for almost four years to produce 927 daily, rank-10 observations . Since the observations are rank-deficient, we know that . (In the full-rank case, we will estimate .) We constrain using (2) so that the only unknown is . Given an improper flat prior for , the posterior mode is , implying that , a not unusual value for exponential smoothing. Once is set, one can filter forward, backward sample, and generate one-step ahead predictions in closed form. The right side of Figure 1 shows the filtered covariance between Alcoa Aluminum and American Express on the correlation scale.

However, one need not take such a literal interpretation of the model. Instead of trying to justify its use on first principles, one may simply treat it as a covariance-valued state-space model, which we do presently. As noted in the introduction and elaborated on in Section A, realized covariance matrices are good estimates of the daily covariance matrix of a vector of financial asset returns. Since realized covariance matrices are good estimates it is natural to try to use them for prediction. The statistics themselves place very few restrictions on the distribution of asset prices and their construction is non-parametric. In other words, the construction of a realized covariance matrix (at least the construction we use) says little about the evolution of the latent daily covariance matrices.

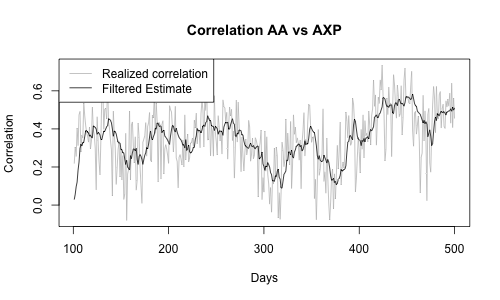

On the left is the log posterior of calculated using and constraint (2). The black line is the level set of the log posterior as a function of , which has a mode at corresponding to . The grey line is the level set of as a function of . On the right are the values of and the estimate for on the correlation scale.

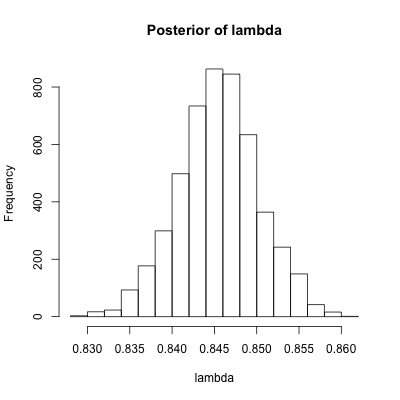

But we do not need to know the exact evolution of the latent daily covariance matrices to employ Model UE to make short-term predictions. To that end, we may treat realized covariance matrices as -valued data that track the latent daily covariances . We construct these realized statistics using the same stocks over the same time period as above, but using all of the intraday data, which results in full-rank observations (see Section B for details). We follow the same basic procedure as above to estimate and , and implicitly by constraint (2). Selecting an improper flat prior for and yields the log-posterior found in Figure 2. The posterior mode is at implying . The gray lines in Figure 2 correspond level sets of in and . As seen in the figure, the uncertainty in is primarily in the direction of the steepest ascent of . One can use Proposition 3 and the method of generating to construct a random walk Metropolis sampler as well. Doing that we find the posterior mean to be , which implies an essentially identical . A histogram of the posterior of is in Figure 3, showing that, though the the direction of greatest variation in corresponds to changes in , the subsequent posterior standard deviation of is small.

Recall, our original motivation for studying -valued state-space models was the observation that exponentially smoothing realized covariance matrices generates better one-step ahead predictions than factor stochastic volatility. In those initial experiments, we used cross-validation to pick the smoothing parameter . Figure 3 shows that one arrives at the same conclusion under two different measures of performance using Model UE and the method described previously to pick . The mesures are described in the caption to Figure 3. To summarize: it is better to use our simple -valued state-space model with realized covariance matrices to make short term predictions than it is to use factor stochastic volatility with only daily returns.

Though we pick a point estimate of the system’s parameters above and then fix that value to make predictions, one can operate in a fully Bayesian manner when computing one-step ahead predictions as well as filtered distributions and the posterior distribution of the latent states. In particular, one can sample the posterior distribution , , and then use those posterior samples to draw from or using forward filtering or to draw from using forward filtering and backward sampling to get the corresponding joint distributions , , and .

Model

MVP

PLLH

FSV 1

0.01021

94910

FSV 2

0.00992

95155

UE

0.00929

96781

MVP: lower is better

PLLH: higher is better

Model

MVP

PLLH

FSV 1

0.01021

94910

FSV 2

0.00992

95155

UE

0.00929

96781

MVP: lower is better

PLLH: higher is better

On the left: the posterior of calculated using , constraint (2), and posterior samples of . On the right: the performance of Model UE versus factor stochastic volatility using 1 and 2 factors. “MVP” stands for minimum variance portfolios and “PLLH” stands for predictive log-likelihood. For all of the models, a sequence of one-step ahead predictions of the latent covariance matrices was generated. For Model UE, we set to be the posterior mode found from the data , as described in Section 3, to generate the one-step ahead predictions. For factor stochastic volatility, we picked the point estimate to be an approximation of the mean of where and is the vector of open to close log-returns on day . For the MVP column, the one-step ahead predictions were used to generate minimum variance portfolios for . The column reports the empirical standard deviation of the subsequent portfolios. Lower standard deviation is better. For the PLLH column, the one-step ahead predictions were used to calculate the predictive log-likelihood where is a multivariate Gaussian kernel. A higher predictive log-likelihood is better. Model UE does better on both counts.

4 Discussion

Employing exponentially weighted moving averages to generate short-term forecasts is not new. These methods were popular at least as far back as the first half of the 20th century (Brown, 1959). In light of this, it may seem that Model UE is rather unglamorous. But this is only because we have explicitly identified how the model uses past observations to make predictions. In fact, many models of time-varying variance behave similarly. For instance, GARCH (Bollerslev, 1986) does exponential smoothing with mean reversion to predict the variance using square returns. Stochastic volatility (Taylor, 1982) does exponential smoothing with mean reversion to predict the log variance using log square returns. Models that include a leverage effect do exponential smoothing so that the amount of smoothing depends on the direction of the returns. Thus, it should not be surprising or uninteresting when a state-space model generates predictions with exponential smoothing or some variation thereof.

This helps explains why a simple model (UE) with high-quality observations can generate better short-term predictions than a complicated model (factor stochastic volatility) with low-quality data. First, both models, in one way or another, are doing something similar to exponential smoothing. Second, the true covariance process seems to revert quite slowly. Thus, there will not be much difference between a one-step ahead forecast that lacks mean reversion (Model UE) and a one-step ahead forecast that includes mean reversion (factor stochastic volatility). Since the prediction mechanisms are similar, the model that uses a “higher resolution” snapshot of the latent covariance matrices has the advantage. Of course, these observations only apply when using factor stochastic volatility with daily returns. It may be the case that one can use intraday information along with some specialized knowledge about the structure of market fluctuations (like factor stochastic volatility) to generate better estimates and predictions.

Despite Model UE’s short-term forecasting success, it does have some faults. First, the evolution of can be rather degenerate. In the one-dimensional case, when is not a martingale, either almost surely converges to zero or almost surely diverges. (The discussion before Proposition 8 expands upon this point.) Presumably, the multivariate case suffers from something similar and, clearly, this does not reflect the dynamics we want to capture. Second, its -step ahead predictions do not revert to some mean, which is what one would expect when modeling a stationary process. In fact, the first point suggests that things are worse than that: the -step ahead predictive distributions may degenerate. Consequently, the model will perform poorly as the horizon of the prediction increases.

Thus, to the larger question, “How does one construct rich, tractable state-space models on curved spaces,” we only gave a partial answer, showing how to create a tractable model—one in which the densities of interest may be computed and sampled. In essence, descriptive richness was sacrificed for tractability. One might proceed in the opposite direction by endowing the latent process with rich dynamics initially. For instance, one may transform a positive-definite matrix into an unconstrained planar coordinate system using the factorization , where is upper triangular, is diagonal, and is the matrix exponential, and then model the dynamics in the planar coordinates . But, in that case, one must deal with a potentially inconvenient distribution in the coordinates for forward filtering or backward sampling. Comparing the benefits of each approach within the context of Bayesian state-space inference is left to future work.

5 Technical Details

Much of the calculus one needs can be found Uhlig (1994) or Muirhead (1982). We synthesize those results here. We are not aware of results in either regarding backward sampling or marginalization.

First, some notation: Assume , . Let denote the set of positive semi-definite symmetric matrices of rank and order . When , we drop from the notation so that denotes the set of positive-definite symmetric matrices of order . For symmetric matrices and , let denote . For let

If is real and we write then we implicitly mean . We will use to denote the determinant of a matrix and to denote the identity. We at times follow Muirhead (1982) and define densities with respect to differential forms (also known as -forms or differential -forms). Mikusiński and Taylor (2002) is a good introduction to calculus on manifolds. The handouts of Edelman (2005) provide a more succinct introduction.

Definition 4 (Wishart distribution).

A positive semi-definite symmetric matrix-valued random variable has Wishart distribution for and if

When , the density for the Wishart distribution is

(Muirhead, 1982) with respect to the volume element

When and is rank deficient, the density is

with respect to the volume element

where , is a matrix of orthonormal columns of order , and with decreasing positive entries (Uhlig, 1994, Thm. 6). The notation is shorthand for a differential -form from the Steifel manifold embedded in where (Muirhead, 1982, p. 63). One can extend the definition of the Wishart distribution to real values of for -valued random variables by defining to have the full rank density defined above.

Definition 5 (the bijection ).

Assume and . A single bijection provides the key to both the evolution of in Model UE and to the definition of the beta distribution. In particular, let take to by letting be the Cholesky factorization of and letting

Conversely, let take to by letting be the Cholesky decomposition of and

One can see that is the inverse of since and .

Definition 6 (beta distribution).

The following theorem synthesizes results from Uhlig (1994), Muirhead (1982), and Díaz-García and Jáimez (1997).

Theorem 7.

Proof.

Forward Filtering.

Suppose we start at time with data , so that the joint distributions of and is characterized by

which looks like (5). Theorem 7 shows that the bijection takes to

which is (4) after applying the transformation summarized by

| (6) |

The transformation includes the evolution equation in (UE) since . It also yields . Conjugate updating then yields where . ∎

The reader may notice that the choice of distribution for is precisely the one that facilitates forward filtering. In particular, assuming that has an acceptable distribution to start, then will have an acceptable distribution to update, so that will have a distribution that lets us play the game all over again. However, we cannot easily write down the distribution of for anything but or . To see why, assume that we start at time with data and evolve to just like above. Now consider moving from to without updating:

The distribution of is but the distribution of is . We cannot apply Theorem 7 at this point because there is a mismatch in the degrees of freedom of and the parameters of —we need not degrees of freedom! Thus, the distribution of is unknown.

Despite not knowing its distribution, one can show that the evolution of is rather degenerate. To see this, consider the one dimensional case, in which

Following Shephard (1994), transforming this equation by the logarithm yields

where and . Let . When , the law of large numbers says that for almost every path there is some such that for . That is, the paths diverge. Hence, when , the paths of either converge to or diverge. The same phenomenon can be seen when numerically simulating data in the multivariate case. This makes generating synthetic data difficult since can quickly become numerically singular. It also implies that the predictive distributions are unruly.

Proposition 8.

Assume and are as in Theorem 7 and let . Then the conditional distribution of is

| (7) |

Proof.

Let and be as in Theorem 7 and let . Let be the rank of . Fix and define a change of variables by . Jointly, has a density with respect to the differential form where is a -form where :

where the index of corresponds to the vectorized (by column) upper triangular portion of . Under , the pull back of is

thus,

where, again, the index corresponds to the vectorized upper triangular portion. Let be the density of with respect to the differential form . Under , the differential form corresponding to the density of ,

becomes

on the manifold

We know that is the differential form corresponding to the distribution of , hence describes the conditional distribution of . Doing another change of variables shows that is a shifted Wishart distribution, that is

∎

Backward Sampling.

The Markovian structure of the model ensures that we can decompose the joint density of the latent states given (and , , ) as

(The density is taken with respect to product measure on the -fold product of embedded in with Lebesgue measure). Applying Proposition 8 with as , as , and as , we find that the distribution of is

∎

Marginalization.

First, by conditioning we can express the density as

with respect to the differential form where is as in Definition 4.

Thus, we just need to derive the distribution of . Assume that and that either is an integer or is real-valued. Suppose that and where . Then the density for is

in the rank-deficient case and is

in the full-rank case, with respect to the differential form is as found in Definition 4 for either the rank-deficient or full-rank cases respectively.

We will only prove the rank-deficient case, since the full-rank case is essentially identical. Consider the joint density :

(where , is a diagonal matrix with decreasing entries, and is in the Steifel manifold ) with respect to , which is

. The latter terms are the kernel for a Wishart distribution in . Integrating the kernel with respect to yields

Hence the density of is

with respect to . Factoring the in the denominator gives us

∎

Appendix A Realized Covariance Matrices

Realized covariance matrices are symmetric positive-definite estimates of the daily quadratic variation of a multidimensional continuous-time stochastic process. Within the context of financial time series, there is both theoretical and empirical evidence to suggest that a realized covariance matrix can be interpreted as an estimate of the covariance matrix of the open to close log returns.

Imagine that the market in which the assets are traded is open 24 hours a day and that we are interested in estimating the covariance matrix of daily log returns. Following Barndorff-Nielsen and Shephard (2002), let be the -vector of log prices where is measured in days and suppose that it is a Gaussian process of the form

where is an -dimensional Brownian motion and is a continuous, deterministic, symmetric positive definite process such that the square of is integrable. Then the day vector of log returns is distributed as

where . The quadratic covariation matrix (quadratic variation henceforth) measures the cumulative local (co)-fluctuations of the sample paths:

where the limit holds for any sequence of partitions of the form and . It is always the case, even when is a stochastic process correlated with , that

(See Proposition 2.10 in Karatzas and Shreve (1991).) Thus, in the Gaussian process case, the variance of is related to the quadratic variation by

If the assets under consideration are traded frequently, then the day- partition of trading times has near zero so that

where the summation is over , is a good estimate of . This is the realized covariance.

The same logic proceeds when is stochastic process that is independent of the Brownian motion. In that case, the only major change is

that is the log returns are a mixture of normals, so that

Since is a good estimate of regardless of , so long as the assets are traded often enough, one still has a good estimate of the daily conditional variance despite the fact that is random. The nice thing about quadratic variation is that it is well-defined for any process that is a semimartingale (Jacod and Shiryaev, 2003, Thm. 4.47). In that sense, it is a completely non-parametric statistic; though the derivations above do not necessarily hold once is correlated with the underlying Brownian motion. Empirical work has shown that can be used to estimate and forecast the variance of the daily returns in the univariate case (Andersen et al., 2001; Koopman et al., 2005) and the covariance matrix of the vector of daily returns in the multivariate case Liu (2009).

We treat the realized covariances (or rather a different, related approximation to called realized kernels) as the noisy observations in Section 3 and then infer , , and to generate filtered estimates and one-step ahead predictions of the latent covariance matrices . Barndorff-Nielsen et al. (2011) describe how to construct the matrix valued data and we follow their general approach to produce symmetric positive-definite valued data for 927 trading days and 30 assets. Details of the construction and the data can be found in Section B.

Appendix B Construction of Realized Kernel and Data

The data set follows the thirty stocks found in Table 1, which comprised the Dow Jones Industrial Average as of October, 2010. The raw data consists of intraday tick-by-tick trading prices from 9:30 AM to 4:00 PM provided by the Trades and Quotes (TAQ) database through Wharton Research Data Services111Wharton Research Data Services (WRDS) was used in preparing this paper. This service and the data available thereon constitute valuable intellectual property and trade secrets of WRDS and/or its third-party suppliers. . The data set runs from February 27, 2007 to October 29, 2010 providing a total of 927 trading days.

| Alcoa (AA) | American Express (AXP) | Boeing (BA) | Bank of America (BAC) | Caterpillar (CAT) |

| Cisco (CSCO)* | Chevron (CVX) | Du Pont (DD) | Disney (DIS) | General Electric (GE) |

| Home Depot (HD) | Hewlett-Packard (HPQ) | IBM (IBM) | Intel (INTC)* | Johnson & Johnson (JNJ) |

| JP Morgan (JPM) | Kraft (KFT) | Coca-Cola (KO) | McDonald’s (MCD) | 3M (MMM) |

| Merk (MRK) | Microsoft (MSFT)* | Phizer (PFE) | Proctor & Gamble (PG) | AT&T (T) |

| Traveler’s (TRV) | United Technologies (UTX) | Verizon (VZ) | Walmart (WMT) | Exxon Mobil (XOM) |

The asterisk denotes companies whose primary exchange is the NASDAQ. All other companies trade primarily on the NYSE.

Our construction of the realized kernels is based upon Barndorff-Nielsen et al. (2009, 2011). Warning: we re-use the letters and , but now they refer to vector-valued continuous-time processes! Barndorff-Nielsen et al.’s model, which takes into account market microstructure noise, is

where are the times at which the -dimensional vector of log stock prices, , are observed, is the latent log stock price, and are errors introduced by market microstructure. The challenge is to construct estimates of the quadratic variation of with the noisy data . They do this using a kernel approach,

where

with and for . The kernel is a weight function and lives within a certain class of functions. While this provides a convenient formula for calculating realized kernels, the choice of weight function and proper bandwidth requires some nuance. Barndorff-Nielsen et al. (2011) discuss both issues. We follow their suggestions, using the Parzen kernel for the weight function and picking as the average of the collection of bandwidths one calculates for each asset individually. Before addressing either of those issues one must address the practical problem of cleansing and synchronizing the data.

- Clean the data

-

: The data was cleaned using the following rules.

-

•

Retrieve prices from only one exchange. For most companies we used the NYSE, but for Cisco, Intel, and Microsoft we used FINRA’s Alternative Display Facility.

-

•

If there are several trades with the same time stamp, which is accurate up to seconds, then the median price across all such trades is taken to be the price at that time.

-

•

Discard a trade when the price is zero.

-

•

Discard a trade when the correction code is not zero.

-

•

Discard a trade when the condition code is a letter other than ‘E’ or ‘F’.

-

•

- Synchronize Prices

-

: Regarding synchronization, prices of different assets are not updated at the same instant in time. To make use of the statistical theory for constructing the realized measures one must decide how to “align” prices in time so that they appear to be updated simultaneously. Barndorff-Nielsen et al. suggest constructing a set of refresh times which corresponds to a “last most recently updated approach.” The first refresh time is the first time at which all asset prices have been updated. The subsequent refresh times are inductively defined so that is the first time at which all assets prices have been updated since . After cleansing and refreshing the data, one is left with the collection from which the realized kernels will be calculated.

- Jitter End Points

-

: For their asymptotic results to hold Barndorff-Nielsen et al. suggest jittering the first and last observations . We do this by taking the average of the first two observations and relabeling the resulting quantity as the first observation and taking the average of the last two observations and labeling the resulting quantity as the last observation.

- Calculate Bandwidths

-

:

We follow Barndorff-Nielsen et al. (2009) when calculating each individually using the time series before it has been synchronized or jittered. Fix and suppress it from the notation—we are only considering a single asset. In particular, for asset the bandwidth is estimated as

where for the Parzen kernel, is the number of observations, and

is the realized variance sampled on a 20 minute grid. is an estimate of the variance of and is given by

The quantity is the sum of square increments taken at a high frequency.

and is the number of observations elements in . For each time series we choose , which is the average number of ticks on that day per two minute period (Barndorff-Nielsen et al., 2009).

References

- Aguilar and West [2000] O. Aguilar and M. West. Bayesian dynamic factor models and portfolio allocation. Journal of Business and Economic Statistics, 18(3):338–357, July 2000.

- Andersen et al. [2001] T. G. Andersen, T. Bollerslev, F. X. Diebold, and H. Ebens. The distribution of realized stock return volatility. Journal of Financial Econometrics, 61:43–76, 2001.

- Barndorff-Nielsen and Shephard [2002] O. E. Barndorff-Nielsen and N. Shephard. Econometric analysis of realized volatility and its use in estimating stochastic volatility. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 64(2):253–280, 2002.

- Barndorff-Nielsen et al. [2009] O. E. Barndorff-Nielsen, P. R. Hansen, A. Lunde, and N. Shephard. Realized kernels in practice: Trades and quotes. Econometrics Journal, 12(3):C1–C32, 2009.

- Barndorff-Nielsen et al. [2011] O. E. Barndorff-Nielsen, P. R. Hansen, A. Lunde, and N. Shephard. Multivariate realized kernels: Consistent positive semi-definite estimators of the covariation of equity prices with noise and non-synchronous trading. Journal of Econometrics, 162:149–169, 2011.

- Bollerslev [1986] T. Bollerslev. Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31:307–327, 1986.

- Brown [1959] R. G. Brown. Statistical Forecasting for Inventory Control. McGraw-Hill, 1959.

- Choi and Christensen [2011] C. Choi and H. I. Christensen. Robust 3d visual tracking using particle filters on the SE(3) group. In IEEE International Conference on Robotics and Automation, pages 4384–4390, 2011.

- Díaz-García and Jáimez [1997] J. A. Díaz-García and R. G. Jáimez. Proof of the conjectures of H. Uhlig on the singular multivariate beta and the Jacobian of a certain matrix transformation. The Annals of Statistics, 25:2018–2023, 1997.

- Edelman [2005] A. Edelman. The mathematics and applications of (finite) random matrices, 2005. URL http://web.mit.edu/18.325/www/handouts.html. See handouts 1-4.

- Hauberg et al. [2013] S. Hauberg, F. Lauze, and K. S. Pedersen. Unscented Kalman filtering on Riemannian manifolds. J Math Imaging Vis, 46:103–120, 2013.

- Jacod and Shiryaev [2003] J. Jacod and A. N. Shiryaev. Limit Theorems For Stochastic Processes. Springer, 2003.

- Julier and Uhlmann [1997] S. J. Julier and J. K. Uhlmann. New extensions of the Kalman filter to nonlinear systems. In Signal Processing, Sensor Fusion, and Target Recognition VI, volume 3068, 1997.

- Kalman [1960] R. E. Kalman. A new approach to linear filtering and prediction problems. Journal of Basic Engineering, 82 (Series D):35–45, 1960.

- Karatzas and Shreve [1991] I. Karatzas and S. E. Shreve. Brownian Motion and Stochastic Calculus. Springer, 1991.

- Koopman et al. [2005] S. J. Koopman, B. Jungbackera, and E. Hol. Forecasting daily variability of the S&P 100 stock index using historical, realised and implied volatility measurements. Journal of Empirical Finance, 12:445–475, 2005.

- Kwon and Park [2010] J. Kwon and F. C. Park. Visual tracking via particle filtering on the affine group. The International Journal of Robotics Research, 29:198–217, 2010.

- Liu [2009] Q. Liu. On portfolio optimization: How and when do we benefit from high-frequency data? Journal of Applied Econometrics, 24:560–582, 2009.

- Mikusiński and Taylor [2002] P. Mikusiński and M. D. Taylor. An Introduction to Multivariate Analysis. Birkhäuser, 2002.

- Muirhead [1982] R. J. Muirhead. Aspects of Multivariate Statistical Theory. Wiley, 1982.

- Porikli et al. [2006] F. Porikli, O. Tuzel, and P. Meer. Covariance tracking using model update based on Lie algebra. In Computer Vision and Pattern Recognition, pages 728 – 735, 2006.

- Prado and West [2010] R. Prado and M. West. Time Series: Modeling, Computation, and Inference, chapter Multivariate DLMs and Covariance Models, pages 263–319. Chapman & Hall/CRC, 2010.

- Quintana and West [1987] J. M. Quintana and M. West. An analysis of international exchange rates using multivariate DLMs. The Statistician, 36:275–281, 1987.

- Shephard [1994] N. Shephard. Local scale models: State space alternative to integrated GARCH processes. Journal of Econometrics, 60:181–202, 1994.

- Srivastava and Klassen [2004] A. Srivastava and E. Klassen. Bayesian and geometric subspace tracking. Advances in Applied Probability, 36(1):43–56, 2004.

- Taylor [1982] S. J. Taylor. Financial Returns Modelled by the Product of Two Stochastic Processes–a Study of Daily Sugar Prices 1961-1979, pages 203–226. Amersterdam: North-Holland., 1982.

- Tompkins and Wolfe [2007] F. Tompkins and P. J. Wolfe. Bayesian filtering on the Stiefel manifold. In Computational Advances in Multi-Sensor Adaptive Processing, pages 261 – 264, 2007.

- Tyagi and Davis [2008] A. Tyagi and J. W. Davis. A recursive filter for linear systems on Riemannian manifolds. In IEEE Conference on Computer Vision and Pattern Recognition, 2008.

- Uhlig [1994] H. Uhlig. On singular Wishart and singular multivariate beta distributions. The Annals of Statistics, 22(1):395–495, 1994.

- Uhlig [1997] H. Uhlig. Bayesian vector autoregressions with stochastic volatility. Econometrica, 65(1):59–73, Jan. 1997.

- West and Harrison [1997] M. West and J. Harrison. Bayesian Forecasting and Dynamic Models. Springer Verlag, 1997.