Queues and risk processes with dependencies

E.S. Badila111 Supported by Project 613.001.017 of the Netherlands Organisation for Scientific Research (NWO)

Email addresses: e.s.badila@tue.nl, o.j.boxma@tue.nl, resing@win.tue.nl., O.J. Boxma and J.A.C. Resing

Abstract: We study the generalization of the queue obtained by relaxing the assumption of independence between inter-arrival times and service requirements. The analysis is carried out for the class of multivariate matrix exponential distributions introduced in [12]. In this setting, we obtain the steady state waiting time distribution and we show that the classical relation between the steady state waiting time and the workload distributions remains valid when the independence assumption is relaxed. We also prove duality results with the ruin functions in an ordinary and a delayed ruin process. These extend several known dualities between queueing and risk models in the independent case. Finally we show that there exist stochastic order relations between the waiting times under various instances of correlation.

Keywords: G/G/1 queue, dependence, waiting time, workload, stochastic ordering, duality, ruin probability, insurance risk, Value at Risk.

2000 Mathematics Subject Classification. Primary 60K25, 91B30.

1. Introduction

In this paper we study a single server queue with the special feature that the service requirement of each arriving customer is correlated with the subsequent inter-arrival time. Dependence between service and inter-arrival times arises naturally in a number of applications. If one has some control over the arrival process to the server, then one might, e.g., wait a relatively long (short) time with dispatching a new job to the server, if the previous job was relatively big (small). In fact, we shall see in Section 5 that a positive correlation between the service requirement and the subsequent inter-arrival time reduces the waiting times, whereas negative correlation increases waiting times. The increase/decrease is in the sense of convex ordering (cf. [28], Ch. 1).

In studying the single server queue , it is usually assumed that all inter-arrival times and service requirements are independent. An important exception is the class of queues with Batch Markovian Arrival Process, , see for example Lucantoni [26] and references therein. The queue provides a framework to model dependence between successive interarrival times. In [19] it is also used to study an queue in which service requirements depend on the previous inter-arrival times; see [14] for a different approach to the latter form of dependence, which does not use the MAP machinery. An important paper regarding dependence between inter-arrival and service requirements is the one by Adan and Kulkarni [1]. They consider a single server queue with Markov-dependent inter-arrival and service requirements: a service requirement and subsequent inter-arrival time have a bivariate distribution that depends on an underlying Markov chain which jumps at customer arrival epochs. The inter-arrival times in [1] are exponentially distributed, with rate when the Markov chain jumps to state .

It should be observed that the analysis of a queue with some dependence structure between a service requirement and the subsequent inter-arrival time is intrinsically easier than that of a queue with some dependence structure between and the next . The reason is that and only appear as a difference in the Lindley recursion for the waiting time of the arriving customer. In a sense, the study of the waiting time distribution in the queue reduces to the study of a random walk with steps . Still, there are not many examples known of joint distributions of that allow a detailed exact analysis. One of the exceptions is provided in [16], where a threshold-type dependence between and is shown to be analytically tractable.

In the present study, we shall consider a very general class of bivariate distributions of , which allows us to obtain detailed, explicit, results for the steady-state waiting time and workload distribution. The dependence structure under consideration is modelled by a class of bivariate matrix-exponential distributions (Bladt and Nielsen [12]) in which the joint Laplace-Stieltjes transform of the claim size and the inter-claim time is a rational function.

While this paper was under preparation, Hansjoerg Albrecher kindly pointed out to us that Constantinescu et al. [20] were obtaining results similar to ours for a generalization of the Sparre Andersen insurance risk model. The classical Sparre Andersen model considers the development of the capital of an insurance company that earns premium at a fixed rate and that receives claims with a stochastic size at stochastic inter-arrival times – all the input variables being independent. In contrast, Constantinescu et al. [20] allow a claim size to depend on the previous inter-claim time, in a similar way as an inter-arrival time depends on the previous service requirement in our queueing model. One can establish a duality relation between the insurance risk model of [20] and our model (cf. Section 4), and this duality relation in particular implies that the probability of ruin of the insurance company, with initial capital , equals the probability that the steady-state waiting time in the corresponding queueing model exceeds . Our approach is based on Wiener-Hopf factorization; Constantinescu et al. [20] use a completely different approach, based on operator theory methods. We shall explore the relation between the queueing and insurance risk models with dependence in more detail, which will allow us to also obtain the so-called delayed ruin probability in the model of [20], viz., the ruin probability when time is not a claim arrival epoch but an arbitrary epoch, the claim arrival process being in stationarity.

Already having discussed the queueing literature with dependence between inter-arrival and service requirement, let us now turn to the insurance risk literature with dependence between inter-claim time and claim size. In recent years, this has been a hot topic in risk theory. Albrecher and Boxma [2] derive exact formulas for the ruin probability in a Cramér-Lundberg model with a threshold-type dependence between a claim size and the next inter-claim time. In [3] a much more general semi-Markovian risk model is being considered, which bears some resemblance to the queueing model in [1]. Kwan and Yang [25] consider a specific threshold-type dependence of claim size on previous inter-claim time; in [4] this is put in the larger framework of Markov Additive Processes. Another specific dependence structure between claim size and previous inter-claim time is treated in Boudreault et al. [15]. Asymptotic results were obtained in Albrecher and Kantor [5], where the relation between the dependence structure and the Lundberg exponent is studied. Also Albrecher and Teugels [6] give asymptotic results for the finite and infinite horizon ruin probabilities when the current claim size and the previous inter-claim time are dependent according to an arbitrary copula structure.

The main contributions of the paper are the following. (i) We provide an exact analysis of the waiting time distribution in a queue with correlation between a service requirement and the subsequent interarrival time , and having a multivariate matrix-exponential distribution. (ii) We prove that the simple relation which holds between steady-state workload and waiting time distributions in the ordinary queue remains valid in the case of correlated and . (iii) We consider the dual Sparre Andersen insurance risk model with correlation between inter-claim time and subsequent claim size, and in particular we show that the Takács relation (cf. [21], Corollary 4.5.4) between the ordinary ruin probability and the delayed ruin probability remains valid. (iv) Finally, we show that, in comparison with the classical set-up without dependence, positive and negative correlation respectively decreases and increases the waiting times in the sense of convex ordering. We also illustrate with numerical results the influence of dependence on the expected values of the waiting times but also on the -percentiles of the ruin functions (VaR’s).

The paper is organized as follows. Section 2 contains a detailed model description, which in particular includes a description of the class of bivariate distributions under consideration. It also presents the waiting time analysis. The relation between the steady-state waiting time and workload distributions is exposed in Section 3. Section 4 is devoted to the dual insurance risk model. In Section 5 we consider several examples of bivariate distributions of and . For these examples, we present numerical results on the mean and tail of the waiting time distribution (and, by duality, on the ruin probability), which exhibit the effect of (positive or negative) correlation on waiting time and ruin probability, together with stochastic ordering results and by consequence, ordering between the waiting times.

2. Model Description and Analysis of the waiting time

We study a generalization of the classical model, where we allow for an arbitrary correlation between the service requirement of the customer and the inter-arrival time between the and customer. As a key performance measure in this model, we first consider the waiting time process in an initially empty system. In Section 3, we prove that the steady-state waiting time is related to the steady-state workload in a similar way as in the independent case.

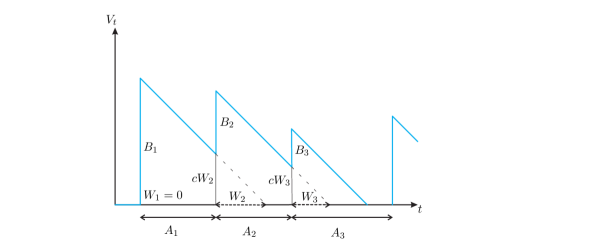

Let be the service requirement of the customer, the inter-arrival time between the and the customer, and the server’s speed. We assume that are i.i.d. sequences of random vectors. This implies that the arrival process of customers is renewal and that the quantities are i.i.d. However, within a pair, and are dependent, hence the service requirement and the subsequent inter-arrival time are correlated. We denote by a generic pair made up of a service requirement and the subsequent inter-arrival time. In Figure 1 we display the workload process and the waiting time process ; here denotes work in the system at time , and denotes the waiting time of the arriving customer. The waiting time process satisfies the Lindley recursion:

Under the stability condition , converges in distribution to a proper random variable and we can write:

| (1) |

The dependence structure:

We model the dependence structure using the class of multivariate matrix-exponential distributions (MVME), which was introduced by Bladt and Nielsen [12]. This class contains other known classes of distributions with interesting probabilistic interpretations, like the multivariate phase-type distributions studied in Assaf et al. [11] and further in Kulkarni [24]. We will further discuss this class in Section 5 where we also give examples which admit a probabilistic interpretation. Below we cite Definition 4.1 of Bladt and Nielsen [12]:

Definition 1.

A non-negative random vector is said to have a bivariate matrix-exponential distribution if the joint Laplace-Stieltjes transform (LST) is a rational function in , i.e. it can be written as , where and are polynomial functions in and .

As a consequence of this defining property, the transform of the difference is also a rational function. For simplicity, let us denote . We rewrite identity (1) in terms of Laplace-Stieltjes transforms. After some straightforward computations, one obtains:

| (2) |

Using the rationality of the transform of , we can rewrite (2):

where is the function on the right-hand side of (2), which is analytic in and continuous in . Also, since by definition, is analytic in and continuous in .

Using Wiener-Hopf factorization, we now obtain the LST of the steady-state waiting time distribution:

Theorem 1.

For having a bivariate matrix exponential distribution, the LST of the steady state waiting time is given by

| (3) |

where are the zeros of in and are its poles in .

Proof.

Let be the number of zeros of in . We move these to the right-hand side of the identity above:

| (4) |

where , the product being over the zeros of with ; and . Now the left-hand side of (4) is analytic in , the right-hand side remains analytic in ; therefore by analytic continuation, the left-hand side is an entire function.

We use a version of Liouville’s theorem A.2 (see Appendix), which states that an entire function with asymptotic behavior must be a polynomial of degree at most .

Liouville’s theorem implies that the left-hand side of (4) is a polynomial of degree . Therefore we can write

| (5) |

Since has zeros only in , must have all the zeros of from because otherwise would have a pole in which is not possible.

Now all boils down to showing that and have the same number of zeros (i.e. ) in . Rouché’s theorem A.1 in the Appendix seems to be the right tool for this, and in Lemma A.1 in the Appendix we show that indeed in .

Since must have these zeros of as its own, and at the same time from above, this determines up to a constant: , where , being the zeros of with (this also includes the zero at ). After replacing and reducing the factors in Formula (5), we obtain the following formula for :

| (6) |

Setting determines the constant: , hence (3) follows. ∎

Remark 1.

The PASTA property does not hold, and hence the distribution of the steady-state workload differs in principle from , the steady-state workload as seen by an arriving customer. In particular, we have Actually, we find the atom at zero of if we take in (3), with the additional remark that the numerator has the same number of factors as the denominator, which follows from Rouché’s theorem:

| (7) |

On the other hand, from first principles we have, with , for the steady-state probability of an empty system:

The factorization used in the proof of identity (3) can be also used to obtain the transform of , the steady state idle period of the system.

Corollary 1.

The transform of the idle period is given by

with being the zeroes of in and its poles in

Proof.

Conditional on , , so we may write

The transform already appears on the right-hand side of (2), hence the transform of the idle period can be rewritten as

| (8) |

Remark 2.

Alternatively we can use Formula (6.20) in Cohen [17], p.21, which makes use of the regenerative structure of the workload process w.r.t. the busy cycles of the queue. It can be shown that the formula remains valid even in the dependent case. The connection with (8) is then , the mean number of customers served during a busy cycle.

In the next section we show that similar arguments involving regeneration as the ones employed in [17], can be extended in our setting to give the relation between the steady-state workload and waiting time distributions.

3. The steady-state workload

In this section we consider the steady-state workload in the queueing model with correlation between service requirement and subsequent inter-arrival time . We shall prove that the known relation between the steady-state workload and waiting time for the single server queue with independent service requirement and inter-arrival time ([8], p. 274, [17], p. 19/20, or [18], p. 296/297) remains valid. For this purpose we adapt the proof in [17], which is based on the fact that the workload process regenerates at the beginning of each busy cycle. The LST of the workload and waiting time distributions can then be written as stochastic mean values of the LST over one full busy cycle.

Theorem 2.

The steady-state workload and the waiting time are related in the following way:

| (9) |

with and the marginal distribution of a residual service requirement, viz.,

Remark that only the marginal distribution of the residual service requirement appears in the above, not the joint distribution of and .

Proof.

Let 0 be the beginning of a busy period and be its length. Following Cohen[17], within this busy period, we may write (cf. Figure 1):

where is the workload at time , is the number of arrivals in and is the last arrival epoch before . The following identities hold path-wise:

| (10) |

Here is the number of customers served during a busy period. The key observation is that the following relation holds even when and are dependent:

There is no expectation taken so integration is carried out as usual, all these being path-wise identities. Formula (10) now becomes

We make use of the following identities for the waiting time during a busy period:

For , ; and , hence

| (11) |

All derivations up to this point are path-wise manipulations, hence insensitive to correlations between and . Remark that is independent of but also of the r.v. . So if we take expectations in (11)

So that

| (12) |

A key remark is that the workload process is still regenerative with respect to the renewal sequence given by the epochs at which busy periods begin. Under the stability condition, the mean cycle length of the workload process is finite, hence the stochastic mean value results still hold in this case (cf. Cohen[17], Thm. 4.1) and we have the identities:

and

We can now use these identities together with (12) and , so we may write

Note that by definition, , with the i.i.d. sequence such that is the service requirement of the customer in a busy cycle. Hence Wald’s identity gives , and using in addition , , we can rewrite the above as

This can immediately be inverted to give the desired relation (9).∎

4. Duality between the insurance and queueing processes

It is well known that there are duality relations between the classical queue and the corresponding classical Sparre Andersen insurance risk model, with independence between service requirements (respectively claim sizes) and inter-arrival times. In this case ‘corresponding’ means: the same inter-arrival distributions, the service requirement distribution equals the claim size distribution, the service rate is the same as the premium rate. There are two versions of the duality result (cf. Asmussen and Albrecher [9], p. 45, 161):

| (13) |

| (14) |

Here is the tail of the amount of work as seen by an arriving customer in equilibrium, and is the tail of the steady-state workload in the queue. is the ruin probability in the Sparre Andersen model, when at time the capital is and a new inter-arrival time begins, i.e., is an arrival epoch. is the ruin probability when the risk process is started in stationarity, i.e., is independent of the process itself. In this case the time elapsed until the first claim arrives has a residual distribution. We will call the ordinary ruin probability and the delayed ruin probability.

We pose and answer three questions in this section, for the dependencies under consideration

(between service requirement and subsequent inter-arrival time, respectively between inter-claim time and subsequent claim size):

(1) Does the duality relation (13) still hold?

(2) Does the duality relation (14) still hold?

(3) Does the relation between steady-state workload and waiting time from Theorem 2 translate

to a relation between delayed ruin probability and ordinary ruin probability, just as it does in the independent case (cf. p. 69 of Grandell

[22])?

The answer to question (1) is immediately seen to be positive, as shown in Asmussen and Albrecher [9] p.45, because this relation uses only the random walk structure of the risk/queueing process embedded at arrival epochs, which is preserved in the model we study ( and only appear in the random walk via the difference ). The Laplace transform of the ruin probability now immediately follows from the waiting time LST in Theorem 1, by observing that the relation becomes in terms of transforms: . Hence we have:

Corollary 2.

The Laplace transform of , equals

Notice that, as mentioned in the Introduction, this result was also obtained in Constantinescu et al. [20], using operator theory.

We shall prove that the answer to question (3) is also affirmative. In combination with the duality relation (13), this implies that the answer to question (2) is also affirmative: the duality relation (14) still holds in the dependent case.

For the purpose of studying the relation between the ordinary and the delayed ruin functions below, we assume that the pair (A,B) has a joint density, .

Let and be the survival functions for the ordinary risk process and for its stationary version, respectively. In addition, denote by the initial capital, and let be the arrival rate of claims.

Theorem 3.

The relation between the survival functions for the two versions of the ruin process is

Let us make some remarks about this formula before proving it.

Remark 3.

In the stationary version of the ruin process, the first claim arrival happens after a time distributed as the residual inter-arrival time. Because of the correlation between claim sizes and their inter-arrival times, the claim size that corresponds to the residual arrival time will have a distinguished distribution; therefore let us denote the first pair by . Regarding the density function, it can be shown that (see Lemma A.3)

| (15) |

Remark 4.

The double integral that appears in the last term from Theorem 3 above:

equals the marginal tail of a claim size, . If we replace this in the relation from Theorem 3, we obtain the same formula as in Grandell[22] p.69:

| (16) |

This is also known as Takács’ formula (see [21], Corollary 4.5.4). (16) shows that only the marginal residual service requirement appears in this relation between and , even if we have the correlation between a pair .

By using the fact that , as , together with dominated convergence, to argue that it is allowed to interchange limit and integration, one can easily show that . Now observe that Relation (16) between delayed and ordinary survival function is the precise counterpart/equivalent of relation (9) between the workload and waiting time distributions.

Proof of Theorem 3.

We follow the derivation that Grandell[22] (p. 69, see also p.5) has given for the case when and are independent. Starting with the stationary risk process, we condition on the arrival time of the first claim, together with its size:

Using (15) we obtain:

By changing the order of integration between variables and , we have:

We use the change of variable :

| (17) |

Let us take the derivative of . In Lemma A.2 in the Appendix we argue that this is allowed.

Here we replaced the first term in the right-hand side by virtue of the renewal equation for the ordinary survival probability. We can now integrate between and :

| (18) |

Let us focus on the last term from (18), to be called . Integration over yields, with the density of the service requirement distribution :

5. Examples and Numerical results

In this section we present examples of dependence structures which are tractable and have a probabilistic interpretation. We also numerically illustrate the effect of correlations on the waiting time distribution/ruin probability. Throughout the section we take for simplicity .

A comprehensive survey of multivariate matrix-exponential distributions (MVME) can be found in Bladt and Nielsen [12]. As a special subclass of these, Kulkarni [24] introduced multivariate phase-type (MPH) distributions (see also Assaf et al. [11]). In the bivariate case, these are defined as follows: Consider a continuous-time Markov chain , with finite state space , with an absorbing state , and generator matrix

together with a reward matrix , for , . Assume that as long as we stay in state , we earn at rate vector . We look at the bivariate distribution of the random vector , where the marginals of this vector are defined to be the total accumulated rewards until absorption:

with the time to absorption. Remark that can be rewritten as

| (21) |

being the number of jumps until absorption of the embedded discrete-time Markov chain and the holding time in state . The ’s are independent exponentials with rates . The dependence structure between and is thus given by the underlying continuous-time Markov chain . That this is indeed a subclass of MVME, follows from [12], Theorem 4.1.

As a special case of Kulkarni’s bivariate-phase type distributions, one can obtain a fairly large class of distributions by a partial decoupling of the bivariate phase-type: For the discrete-time Markov chain , and for a fixed , let be independent, having exponential distributions with rates and , respectively. Without loss of generality we can consider , and set

The difference with Formula (21) is that now the dependence structure is given only by the common underlying discrete-time Markov chain . Furthermore, if we assume the jump rates to be the same in each state, i.e. exp, exp, then the number of jumps before absorption is a sufficient statistic for the joint distribution of . More precisely, conditional on , and are independent Erlang, Erlang respectively.

Remark 5.

This dependence structure can be realized as in the description of Kulkarni’s class. More precisely, we obtain the partial decoupling by doubling all states of the underlying Markov Process: replace each transient state with , and allow only the corresponding component of to increase while in state (formally, put , and similarly , ). Extend the transition matrix of the Markov Chain such that after visiting state , it always jumps to state and thereafter jumps according to the original transition matrix.

If we denote by the initial distribution of , by the transient component of its transition matrix, and by the vector of exit probabilities, then by conditioning on we obtain the following result as a probabilistic alternative to Theorem 3.2 in Bladt&Nielsen [12]:

Lemma 1.

-

a)

The Laplace-Stieltjes transform of is:

-

b)

The transform of the difference , is a rational function of the form , with and polynomial functions such that .

Proof: see Appendix.

Examples:

. Kibble and Moran’s bivariate Gamma distribution (Kotz et al. [23]) can be realized as above. Consider the state space . Assume the Markov Chain starts in and jumps from to w.p. or stays in state w.p. . Furthermore, assume the same rates for the holding times in every state: exp, exp, for , . Hence this distribution is the fold convolution of Kibble and Moran’s bivariate exponential with itself (cf. [23]), where this bivariate exponential distribution can be represented as

with having a geometric distribution. In the insurance risk setting, the analysis for this example has been done in Ambagaspitiya [7] and also in Constantinescu et al. [20] using operator theory. The Laplace transform of the ordinary ruin probability is given by

with the pole of order of such that .

. Cheriyan and Ramabhadran’s bivariate Gamma is another example of Kulkarni’s bivariate phase-type. This was also analyzed in Ambagaspitiya [7] in the insurance risk setting.

For nonnegative integers , consider the state space , with the set of transient states partitioned as: with , , . The chain starts in state 1 and jumps from state to . The jump rates are while in state , . The reward rates in state are for ; for , and , for . Then the bivariate total accumulated reward has a distribution of the form

where are mutually independent Erlang, .

. In the class of MVME, it is possible to achieve negative correlation as well. Consider to be a discrete random variable with finite support: , for some positive integer. Negative correlation can be achieved if we consider the following mixture of Erlang distributions:

For more examples of negatively correlated phase-type distributions, we refer to [13].

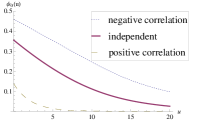

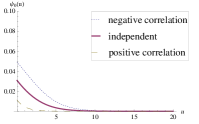

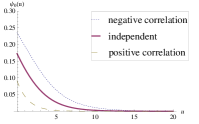

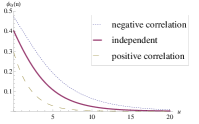

Stochastic ordering results. We compare the tails of the waiting times for the mixed Erlang distributions in the following scenarios: the negatively correlated one from Example 3 versus the positively correlated case

and the corresponding independent pair obtained by sampling twice from the distribution of ; i.e. for and i.i.d. copies of

Here is taken to have finite support, as in Example 3 above.

Denote respectively by , and , the differences in the three scenarios above. In Theorem 4 below we show that under a mild assumption on the distribution of , there exists convex ordering between the random variables , and . For two r.v.’s and , means, by definition, that for any arbitrary convex function ,

| (22) |

For more about the notion of convex order and other related stochastic orderings, we refer the reader to [28], Ch. 1. Before we give the result, let us recall a useful criterion (cf.[28], Prop. 1.5.1):

Proposition 1 (Karlin & Novikoff’s cut criterion).

For , r.v.’s with c.d.f.’s and respectively, and finite first moments, assume that , and that there exists an such that , for and for . Then .

Theorem 4.

| (23) |

Moreover, if has a symmetric distribution, , then we also have

| (24) |

Proof.

Let and respectively be Erlang and Erlang distributed random variables independent of each other, for ; also denote .

We will first prove ordering, that is the functional inequality (22) is restricted to increasing convex functions . This together with the fact that the expected values of , and are the same implies ordering (see [28], Thm. 1.3.1, p.9).

Take to be any convex and increasing function. Firstly, we prove (23), that is, we must show that , or equivalently,

Let us put for simplicity , so we can rewrite the above as

| (25) |

Note that (25) is an association type of inequality, similar to Cebishev’s inequality (see [10], Lemma 2.3 and the references therein). Using that the form a probability distribution, we can further rewrite (25)

| (26) |

Remark that there is an equal number of terms on the two sides of (26) because we sum over indices that lie respectively above and below the main diagonal of the tableaux . We are done as soon as we show that the inequality holds for a one-to-one correspondence between these indices; more precisely, for the correspondence , , we will prove that

| (27) |

that is, (26) holds term by term, and remark that the coefficients and cancel against each other. Put and denote

Obviously, is increasing and convex, because is. Consider the decomposition of and as sums of independent r.v.’s , and with , Erlang distributed of order and rates and , respectively. By conditioning on and , we can write

Similarly, we obtain and , so that (27) becomes

| (28) |

All boils down to proving (28). In order to achieve this, let be a r.v. with a Bernoulli(1/2) distribution and let be two arbitrary positive constants. Consider the following r.v.’s

We have the following identities in distribution

with being the Dirac measure at . Now it follows easily from the cut criterion in Proposition 1 above that . Hence, in particular, we can choose as a test function to obtain

Because is a Bernoulli(1/2), the inequality above becomes

Finally, taking the double mixture over and according to the distributions of and respectively, shows that (28) is true, and this proves (23).

and upon regrouping terms it becomes

This is the analogue of (26). Again, it suffices to prove the term by term inequalities similar to (27). The symmetry axis in this case is the second diagonal of the tableaux. This means that the correspondence is , so the analogue of (27) that we prove is, for fixed,

| (29) |

In (29) we dropped the coefficients and because these are equal since is assumed to have a symmetric distribution. If we set , from this point on the analysis is essentially the same. Consider the analogue of ,

then becomes

This is precisely (28) with replaced by , and since was taken to be an arbitrary increasing convex function, the proof is complete.∎

Remark 6.

The requirement for to have a symmetric distribution may be too strong in general. Some assumption on the distribution of is necessary but only for the ordering . For example, if we let and (Dirac mass in 1) then is the difference of two independent Erlang-1, whereas is an Erlang-1 minus an Erlang-2 so is -dominated in this case.

The above proof of the inequality between and does not require the finiteness of the support of ; discrete phase type is also a possible case in which the sums that appear in the proof become series. There are no convergence problems and we are allowed to change summation order as well, due to probabilistic interpretations. Of course there are restrictions if we look for negative correlation when has infinite support. More about this possibility can be found in Bladt and Nielsen [13] on negatively correlated exponentials.

Proposition 2.

Let , , and , be the steady-state waiting times, that correspond to the increments of the random walk distributed as , , and , respectively. Then we have convex ordering between the waiting times in the three scenarios

Proof.

From the definition of convex ordering, is the same as , and similarly is the same as . Therefore the external monotonicity result from Daley and Stoyan [28] (Thm. 5.2.1, p.80) implies that the steady state workloads are convex ordered in the three scenarios, according to the increments of the random walk. This can also be seen in the numerical tables and the plots below.∎

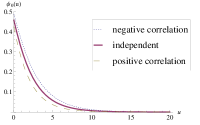

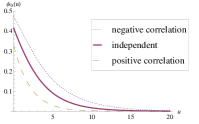

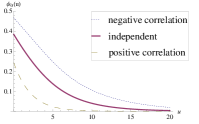

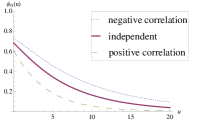

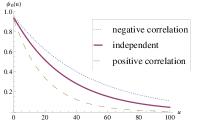

In Table 1 below, we keep fixed, say , and we vary . In Table 2 we vary the load coefficient and we keep the mixing distribution uniform on (i.e., ). The tables contain the mean waiting times, their atoms at zero and , the 95 quantile of the survival function/waiting time (i.e., is the value of the initial capital for which ). The plots of the tails of the ruin functions are in Figure 2 and Figure 3 below.

| 2 | 0.86 | 1.11 | 1.36 | 0.57 | 0.54 | 0.51 | 4.36 | 5.31 | 6.25 |

|---|---|---|---|---|---|---|---|---|---|

| 4 | 0.68 | 1.37 | 2.11 | 0.67 | 0.58 | 0.52 | 3.93 | 6.78 | 9.48 |

| 7 | 0.51 | 1.78 | 3.22 | 0.75 | 0.61 | 0.53 | 3.39 | 9.09 | 14.35 |

| 14 | 0.31 | 2.79 | 5.82 | 0.85 | 0.64 | 0.540 | 2.33 | 14.58 | 25.74 |

| .05 | 0.01 | 0.07 | 0.15 | 0.988 | 0.96 | 0.95 | 0 | 0 | 0 |

| .25 | 0.12 | 0.47 | 0.88 | 0.90 | 0.82 | 0.76 | 0.85 | 3.54 | 5.72 |

| .5 | 0.62 | 1.50 | 2.48 | 0.70 | 0.59 | 0.52 | 3.74 | 7.54 | 11.1 |

| .75 | 2.48 | 4.77 | 7.15 | 0.39 | 0.32 | 0.27 | 10.14 | 17.81 | 25.5 |

| .95 | 18.4 | 31.4 | 44.48 | 0.08 | 0.066 | 0.056 | 58.26 | 97.89 | 137.58 |

APPENDIX

Theorem A.1 (, [29], p.116).

If two functions and are analytic inside and on a closed contour , and on , then and have the same number of zeros inside .

Theorem A.2 (, [29], p.85).

If is analytic for all finite values of , and as ,

then is a polynomial of order .

We can now formulate and prove the following lemma.

Lemma A.1.

Let and be the numerator and the denominator of . Then and have the same number of zeros in .

Proof.

Via Rouch’s theorem, we first prove that on a suitably chosen contour in the complex plane. The fact that and that the transform is rational (so it is also analytic on a strip in ) suggests that we consider the following contour made up from the extended semi-circle

together with the vertical line segment

We show that on this contour, for sufficiently small.

First on : as . We can assume , else there is nothing to prove. This means for sufficiently large.

In order to prove the inequality on the line segment , we use the stability condition: . So for sufficiently small, . Then on we have:

Hence on the whole contour. These being polynomials, Rouch’s theorem A.1 ensures that and have the same number of zeros inside , and since was arbitrarily small, this also holds on , where is the interior of . Finally, letting , proves the assertion. ∎

Proof of Lemma 1.

a) We can write the joint Laplace-Stieltjes transform by conditioning on :

If we set , we can recognize the probability generating function of at , call it .

has a discrete phase-type distribution with representation (Neuts [27]), such that is non-singular (here is the identity matrix), and the probability vector is supported on the transient states. Thus

for , , . If we now focus on this generating function, we have the following (Asmussen [8] Prop. 4.1, p.83):

and we have proved part

b) To see why is a rational function, rewrite the inverse :

Remark that the denominator is a polynomial of order (the number of transient states) in , because appears only on the diagonal of the matrix . is the algebraic complement of (also known as matrix of cofactors). Its entries are of the form , where is the matrix obtained by deleting row and column of . These are polynomials in of order (because of the deleted rows and columns in the entries, the degree of the determinants of these sub-blocks as polynomials in is always smaller than the dimension of the matrix ) and hence so is the bilinear form , which is the numerator of . ∎

Lemma A.2.

in (17) is differentiable.

Proof.

Let Using the triangle inequality, we have the following upper bound

Let us denote by and the first and the second term that appear above, respectively. If we use the fact that , we find the upper bounds on and :

and similarly,

So if we denote ,

and clearly the upper bound is integrable as a function of . By virtue of dominated convergence

∎

Lemma A.3.

Under the conditions from Remark 3, the density of the pair is

Proof.

Consider the augmented pair which by definition has density

where acts as the normalizing factor: Let be a standard uniform r.v., independent of both and . Then , therefore conditional on , is uniformly distributed over the interval , so we may write in terms of density functions

∎

Acknowledgment. The authors are indebted to Hansjoerg Albrecher, Søren Asmussen, Zinoviy Landsman, and Tomasz Rolski for valuable discussions and useful references.

References

- [1] I.J.B.F. Adan and V. Kulkarni. Single-server queue with Markov-dependent inter-arrival and service times. Queueing Systems, 45:113–134, 2003.

- [2] H. Albrecher and O.J. Boxma. A ruin model with dependence between claim sizes and claim intervals. Insurance: Mathematics and Economics, 35:245–254, 2004.

- [3] H. Albrecher and O.J. Boxma. On the discounted penalty function in a Markov-dependent risk model. Insurance: Mathematics and Economics, 37:650–672, 2005.

- [4] H. Albrecher, O.J. Boxma and J. Ivanovs. On simple ruin expressions in dependent Sparre Andersen risk models. Eurandom Report 2012-024, 2012; to appear in J. Appl. Probab.

- [5] H. Albrecher and J. Kantor. Simulation of ruin probabilities for risk processes of Markovian type. Monte Carlo Methods and Applications, 8(2):111–127, 2002.

- [6] H. Albrecher and J.L. Teugels. Exponential behavior in the presence of dependence in risk theory. Journal of Applied Probability, 43(1):257–273, 2006.

- [7] R.S. Ambagaspitiya. Ultimate ruin probability in the Sparre Andersen model with dependent claim sizes and claim occurrence times. Insurance: Mathematics and Economics, 44(3):464–472, 2009.

- [8] S. Asmussen. Applied Probability and Queues. Springer, 2nd edition, 2003.

- [9] S. Asmussen and H. Albrecher. Ruin Probabilities. World Scientific Publ. Cy., Singapore, 2010.

- [10] S. Asmussen, A. Frey, T. Rolski and V. Schmidt. Does Markov-modulation increase the risk? ASTIN Bull, (25):49–66, 1995.

- [11] D. Assaf, N. A. Langberg, T. Savits, and M. Shaked. Multivariate phase-type distributions. Operations Research, 32(3):688–701, 1984.

- [12] M. Bladt and B.F. Nielsen. Multivariate matrix-exponential distributions. Stochastic Models, 26(1):1–26, 2010.

- [13] M. Bladt and B.F. Nielsen. On the construction of bivariate exponential distributions with an arbitrary correlation coefficient. Stochastic Models, 26(2):295–308, 2010.

- [14] S.C. Borst, O.J. Boxma and M.B. Combé. An queue with dependence between interarrival and service times. Stochastic Models, 9:341–371, 1993.

- [15] M. Boudreault, H. Cossette, D. Landriault and E. Marceau. On a risk model with dependence between interclaim arrivals and claim sizes. Scand. Actuar. J., 5:265–285, 2006.

- [16] O.J. Boxma and D. Perry. A queueing model with dependence between service and interarrival times. European J. Oper. Res., 128:611–624, 2001.

- [17] J.W. Cohen. On Regenerative Processes in Queueing Theory. Springer-Verlag, 1976.

- [18] J.W. Cohen. The Single Server Queue. North Holland, 1982.

- [19] M.B. Combé and O.J. Boxma. BMAP modelling of a correlated queue. In: Network Performance Modeling and Simulation, eds. J. Walrand, K. Bagchi and G.W. Zobrist (1998), pp. 177–196.

- [20] C. Constantinescu, D. Kortschak, and V. Maume-Deschamps. Ruin probabilities in models with a Markov chain dependence structure. To appear in Scand. Actuar. J.

- [21] P. Franken, D. König, U. Arndt and V. Schmidt. Queues and Point Processes John Wiley & Sons, Chichester, 1983.

- [22] J. Grandell. Aspects of Risk Theory. Springer-Verlag, 1992.

- [23] S. Kotz, N. Balakrishnan, and N.L. Johnson. Continuous Multivariate Distributions, volume 1. John Wiley & Sons Inc., 2000.

- [24] V.G. Kulkarni. A new class of multivariate phase type distributions. Operations Research, 37(1):151–158, 1989.

- [25] I.K.M. Kwan and H. Yang. Ruin probability in a threshold insurance risk model. Belg. Actuar. Bull., 7:41–49, 2007.

- [26] D.M. Lucantoni. New results on the single-server queue with a batch Markovian arrival process. Stochastic Models, 7: 1–46, 1991.

- [27] M.F. Neuts. Matrix-Geometric Solutions in Stochastic Models: An Algorithmic Approach. Dover Publications, 1991.

- [28] D. Stoyan. Comparison Methods for Queues and Other Stochastic Models. John Wiley & Sons Ltd., 1983.

- [29] E.C. Titchmarsh. The Theory of Functions. Oxford University Press, 2nd edition, 1939.