Feedback Detection for Live Predictors

Abstract

A predictor that is deployed in a live production system may perturb the features it uses to make predictions. Such a feedback loop can occur, for example, when a model that predicts a certain type of behavior ends up causing the behavior it predicts, thus creating a self-fulfilling prophecy. In this paper we analyze predictor feedback detection as a causal inference problem, and introduce a local randomization scheme that can be used to detect non-linear feedback in real-world problems. We conduct a pilot study for our proposed methodology using a predictive system currently deployed as a part of a search engine.

1 Introduction

When statistical predictors are deployed in a live production environment, feedback loops can become a concern. Predictive models are usually tuned using training data that has not been influenced by the predictor itself; thus, most real-world predictors cannot account for the effect they themselves have on their environment. Consider the following caricatured example: A search engine wants to train a simple classifier that predicts whether a search result is “newsy” or not, meaning that the search result is relevant for people who want to read the news. This classifier is trained on historical data, and learns that high click-through rate (CTR) has a positive association with “newsiness.” Problems may arise if the search engine deploys the classifier, and starts featuring search results that are predicted to be newsy for some queries: promoting the search result may lead to a higher CTR, which in turn leads to higher newsiness predictions, which makes the result be featured even more.

If we knew beforehand all the channels through which predictor feedback can occur, then detecting feedback would not be too difficult. For example, in the context of the above example, if we knew that feedback could only occur through some changes to the search result page that were directly triggered by our model, then we could estimate feedback by running small experiments where we turn off these triggering rules. However, in large industrial systems where networks of classifiers all feed into each other, we can no longer hope to understand a priori all the ways in which feedback may occur. We need a method that lets us detect feedback from sources we might not have even known to exist.

This paper proposes a simple method for detecting feedback loops from unknown sources in live systems. Our method relies on artificially inserting a small amount of noise into the predictions made by a model, and then measuring the effect of this noise on future predictions made by the model. If future model predictions change when we add artificial noise, then our system has feedback.

To understand how random noise can enable us to detect feedback, suppose that we have a model with predictions in which tomorrow’s prediction has a linear feedback dependence on today’s prediction : if we increase by , then increases by for some . Intuitively, we should be able to fit this slope by perturbing with a small amount of noise and then regressing the new against the noise; the reason least squares should work here is that the noise is independent of all other variables by construction. The main contribution of this paper is to turn this simple estimation idea into a general procedure that can be used to detect feedback in realistic problems where the feedback has non-linearities and jumps.

Counterfactuals and Causal Inference

Feedback detection is a problem in causal inference. A model suffers from feedback if the predictions it makes today affect the predictions it will make tomorrow. We are thus interested in discovering a causal relationship between today’s and tomorrow’s predictions; simply detecting a correlation is not enough. The distinction between causal and associational inference is acute in the case of feedback: today’s and tomorrow’s predictions are almost always strongly correlated, but this correlation by no means implies any causal relationship.

In order to discover causal relationships between consecutive predictions, we need to use some form of randomized experimentation. In our case, we add a small amount of random noise to our predictions. Because the noise is fully artificial, we can reasonably ask counterfactual questions of the type: “How would tomorrow’s predictions have changed if we added more/less noise to the predictions today?” The noise acts as an independent instrument that lets us detect feedback. We frame our analysis in terms of a potential outcomes model that asks how the world would have changed had we altered a treatment; in our case, the treatment is the random noise we add to our predictions. This formalism, often called the Rubin causal model [1], is regularly used for understanding causal inference [2, 3, 4]. Causal models are useful for studying the behavior of live predictive systems on the internet, as shown by, e.g., the recent work of Bottou et al. [5] and Chan et al. [6].

Outline and Contributions

In order to define a rigorous feedback detection procedure, we need to have a precise notion of what we mean by feedback. Our first contribution is thus to provide such a model by defining statistical feedback in terms of a potential outcomes model (Section 2). Given this feedback model, we propose a local noising scheme that can be used to fit feedback functions with non-linearities and jumps (Section 4). Before presenting general version of our approach, however, we begin by discussing the linear case in Section 3 to elucidate the mathematics of feedback detection: as we will show, the problem of linear feedback detection using local perturbations reduces to linear regression. Finally, in Section 5 we conduct a pilot study based on a predictive model currently deployed as a part of a search engine.

2 Feedback Detection for Statistical Predictors

Suppose that we have a model that makes predictions in time periods for examples . The predictive model itself is taken as given; our goal is to understand feedback effects between consecutive pairs of predictions and . We define statistical feedback in terms of counterfactual reasoning: we want to know what would have happened to had been different. We use potential outcomes notation [7] to distinguish between counterfactuals: let be the predictions our model would have made at time if we had published as our time- prediction. In practice we only get to observe for a single ; all other values of are counterfactual. We also consider , the prediction our model would have made at time if the model never made any of its predictions public and so did not have the chance to affect its environment. With this notation, we define feedback as

| (1) |

i.e., the difference between the predictions our model actually made and the predictions it would have made had it not had the chance to affect its environment by broadcasting predictions in the past. Thus, statistical feedback is a difference in potential outcomes.

An additive feedback model

In order to get a handle on feedback as defined above, we assume that feedback enters the model additively: where is a feedback function, and is the prediction published at time . In other words, we assume that the predictions made by our model at time are the sum of the prediction the model would have made if there were no feedback, plus a feedback term that only depends on the previous prediction made by the model. Our goal is to estimate the feedback function .

Artificial noising for feedback detection

The relationship between and can be influenced by many things, such as trends, mean reversion, random fluctuations, as well as feedback. In order to isolate the effect of feedback, we need to add some noise to the system to create a situation that resembles a randomized experiment. Ideally, we might hope to sometimes turn our predictive system off in order to get estimates of . However, predictive models are often deeply integrated into large software systems, and it may not be clear what the correct system behavior would be if we turned the predictor off. To side-step this concern, we randomize our system by adding artificial noise to predictions: at time , instead of deploying the prediction , we deploy , where is artificial noise drawn from some distribution . Because the noise is independent from everything else, it puts us in a randomized experimental setup that allows us to detect feedback as a causal effect. If the time prediction is affected by , then our system must have feedback because the only way can influence is through the interaction between our model predictions and the surrounding environment at time .

Local average treatment effect

In practice, we want the noise to be small enough that it does not disturb the regular operation of the predictive model too much. Thus, our experimental setup allows us to measure feedback as a local average treatment effect [4], where the artificial noise acts as a continuous treatment. Provided our additive model holds, we can then piece together these local treatment effects into a single global feedback function .

3 Linear Feedback

We begin with an analysis of linear feedback problems; the linear setup allows us to convey the main insights with less technical overhead. We discuss the non-linear case in Section 4. Suppose that we have some natural process and a predictive model of the form . (Suppose for notational convenience that includes the constant, and the intercept term is folded into .) For our purposes, is fixed and known; for example, may have been set by training on historical data. At some point, we ship a system that starts broadcasting the predictions , and there is a concern that the act of broadcasting the may perturb the underlying process. Our goal is to detect any such feedback. Following earlier notation we write for the time variables perturbed by feedback, and for the counterparts we would have observed without any feedback.

In this setup, any effect of on is feedback. A simple way to constrain this relationship is using a linear model . In other words, we assume that is perturbed by an amount that scales linearly with . Given this simple model, we find that:

| (2) |

and so with ; is the feedback function we want to fit.

We cannot work with (2) directly, because is not observed. In order to get around this problem, we add artificial noise to our predictions: at time , we publish predictions instead of the raw predictions . As argued in Section 2, this method lets us detect feedback because can only depend on through a feedback mechanism, and so any relationship between and must be a symptom of feedback.

A Simple Regression Approach

With the linear feedback model (2), the effect of on is This relationship suggests that we should be able to recover by regressing against the added noise . The following result confirms this intuition.

Theorem 1.

Suppose that (2) holds, and that we add noise to our time predictions. If we estimate using linear least squares

| (3) |

where and is the number of examples to which we applied our predictor.

Theorem 1 gives us a baseline understanding for the difficulty of the feedback detection problem: the precision of our feedback estimates scales as the ratio of the artificial noise to natural noise . Note that the proof of Theorem 1 assumes that we only used predictions from a single time period to fit feedback, and that the raw predictions are all independent. If we relax these assumptions we get a regression problem with correlated errors, and need to be more careful with technical conditions.

Efficiency and Conditioning

The simple regression model (3) treats the term as noise. This is quite wasteful: if we know we usually have a fairly good idea of what should be, and not using this information needlessly inflates the noise. Suppose that we knew the function111In practice we do not know , but we can estimate it; see Section 4.

| (4) |

Then, we could write our feedback model as

| (5) |

where is a known offset. Extracting this offset improves the precision of our estimate for .

Theorem 2.

Under the conditions of Theorem 1 suppose that the function from (4) is known and that the are all independent of each other conditional on . Then, given the information available at time , the estimate

| (6) | ||||

| (7) |

Moreover, if the variance of does not depend on , then is the best linear unbiased estimator of .

Theorem 2 extends the general result from above that the precision with which we can estimate feedback scales as the ratio of artificial noise to natural noise. The reason why is more efficient than is that we managed to condition away some of the natural noise, and reduced the variance of our estimate for by

| (8) |

In other words, the variance reduction we get from directly matches the amount of variability we can explain away by conditioning. The estimator (6) is not practical as stated, because it requires knowledge of the unknown function and is restricted to the case of linear feedback. In the next section, we generalize this estimator into one that does not require prior knowledge of and can handle non-linear feedback.

4 Fitting Non-Linear Feedback

Suppose now that we have the same setup as in the previous section, except that now feedback has a non-linear dependence on the prediction: for some arbitrary function . For example, in the case of a linear predictive model , this kind of feedback could arise if we have feature feedback the feedback function then becomes . When we add noise to the above predictions, we only affect the feedback term :

| (9) |

Thus, by adding artificial noise , we are able to cancel out the nuisance terms, and isolate the feedback function that we want to estimate. We cannot use (9) in practice, though, as we can only observe one of or in reality; the other one is counterfactual. We can get around this problem by conditioning on as in Section 3. Let

| (10) | ||||

is a term that captures trend effects that are not due to feedback. The denotes convolution:

| (11) |

Using the conditional mean function we can write our expression of interest as

| (12) |

where . If we have a good idea of what is, the left-hand side can be measured, as it only depends on and . Meanwhile, conditional on , the first two terms on the right-hand side only depend on , while is independent of and mean-zero. The upshot is that we can treat (12) as a regression problem where is noise. In practice, we estimate from an auxiliary problem where we regress against .

A Pragmatic Approach

There are many possible approaches to solving the non-parametric system of equations (12) for , e.g., [8], Chapter 5. Here, we take a pragmatic approach, and constrain ourselves to solutions of the form and , where and are predetermined basis expansions. This approach transforms our problem into an ordinary least-squares problem, and works well in terms of producing reasonable feedback estimates in real-world problems (see Section 5). If this relation in fact holds for some values and , the result below shows that we can recover by least-squares.

Theorem 3.

Suppose that and are defined as above, and that we have an unbiased estimator of with variance Then, if we fit by least squares using (12) as described in Appendix A, the resulting estimate is unbiased and has variance

| (13) |

where the design matrices and are defined as

| (14) |

and is a diagonal matrix with .

In the case where our spline model is misspecified, we can obtain a similar result using methods due to Huber [9] and White [10]. In practice, we can treat as known since fitting is usually easier than fitting : estimating is just a smoothing problem whereas estimating requires fitting differences. If we also treat the errors in (12) as roughly homoscedatic, (13) reduces to

| (15) |

This simplified form again shows that the precision of our estimate of scales roughly as the ratio of the variance of the artificial noise to the variance of the natural noise.

Our Method in Practice

For convenience, we summarize the steps needed to implement our method here: (1) At time , compute model predictions and draw noise terms for some noise distribution . Deploy predictions in the live system. (2) Fit a non-parametric least-squares regression of to learn the function . We use the R formula notation, where means that we want to learn a function that predicts . (3) Set up the non-parametric least-squares regression problem

| (16) |

where the goal is to learn . Here, is the density of , and denotes convolution. In Appendix A we show how to carry out these steps using standard R libraries.

The resulting function is our estimate of feedback: If we make a prediction at time , then our time prediction will be boosted by . The above equation only depends on , , and , which are all quantities that can be observed in the context of an experiment with noised predictions. Note that as we only fit using the differences in (16), the intercept of is not identifiable. We fix the intercept (rather arbitrarily) by setting the average fitted feedback over all training examples to 0; we do not include an intercept term in the basis .

Choice of Noising Distribution

Adding noise to deployed predictions often has a cost that may depend on the shape of the noise distribution . A good choice of should reflect this cost. For example, if the practical cost of adding noise only depends on the largest amount of noise we ever add, then it may be a good idea to draw uniformly at random from for some . In our experiments, we draw noise from a Gaussian distribution .

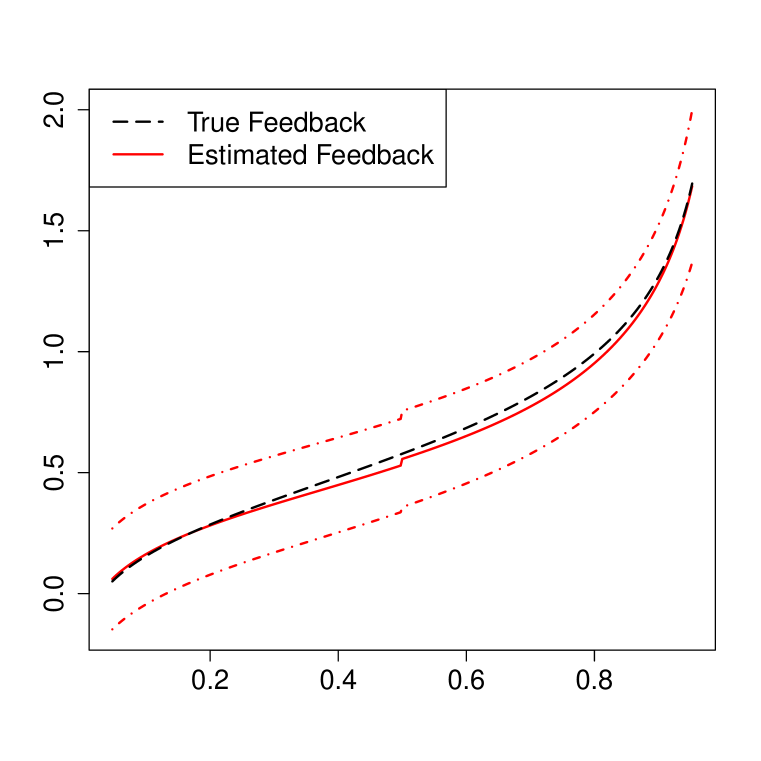

5 A Pilot Study

The original motivation for this research was to develop a methodology for detecting feedback in real-world systems. Here, we present results from a pilot study, where we added signal to historical data that we believe should emulate actual feedback. The reason for monitoring feedback on this system is that our system was about to be more closely integrated with other predictive systems, and there was a concern that the integration could induce bad feedback loops. Having a reliable method for detecting feedback would provide us with an early warning system during the integration.

The predictive model in question is a logistic regression classifier. We added feedback to historical data collected from log files according to half a dozen rules of the form “if is high and , then increase by a random amount”; here is the time- prediction deployed by our system (in log-odds space) and is some feature with a positive coefficient. These feedback generation rules do not obey the additive assumption. Thus our model is misspecified in the sense that there is no function such that a current prediction increased the log-odds of the next prediction by , and so this example can be taken as a stretch case for our method.

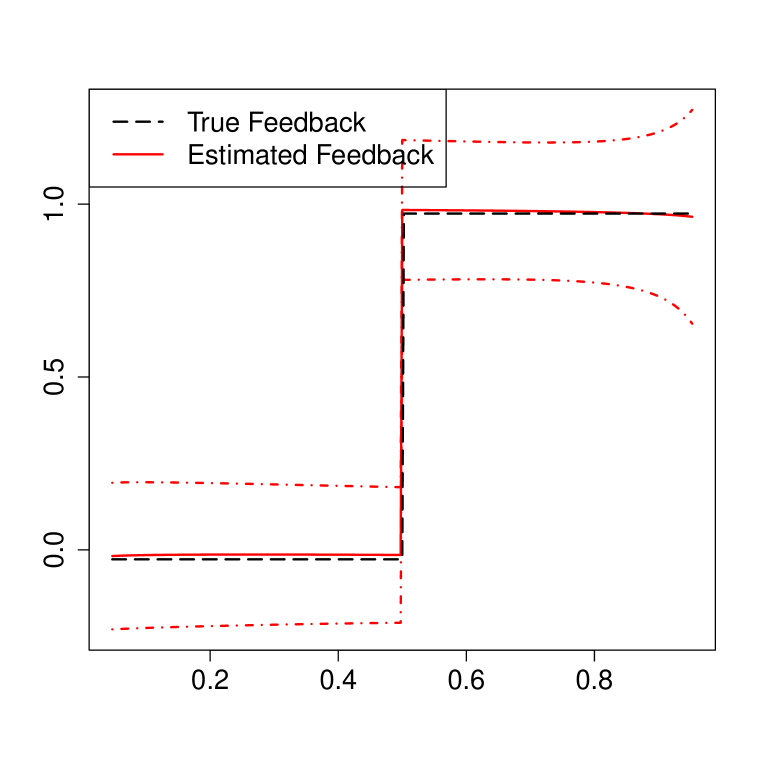

Our dataset had on the order of 100,000 data points, half of which were used for fitting the model itself and half of which were used for feedback simulation. We generated data for 5 simulated time periods, adding noise with at each step, and fit feedback using a spline basis discussed in Appendix B. The “true feedback” curve was obtained by fitting a spline regression to the additive feedback model by looking at the unobservable ; we used a natural spline with knots evenly spread out on in log-odds space plus a jump at 0.

For our classifier of interest, we have fairly strong reasons to believe that the feedback function may have a jump at zero, but probably shouldn’t have any other big jumps. Assuming that we know a priori where to look for jumps does not seem to be too big a problem for the practical applications we have considered. Results for feedback detection are shown in Figure 1. Although the fit is not perfect, we appear to have successfully detected the shape of feedback. The error bars for estimated feedback were obtained using a non-parametric bootstrap [11] for which we resampled pairs of (current, next) predictions.

This simulation suggests that our method can be used to accurately detect feedback on scales that may affect real-world systems. Knowing that we can detect feedback is reassuring from an engineering point of view. On a practical level, the feedback curve shown in Figure 1 may not be too big a concern yet: the average feedback is well within the noise level of the classifier. But in large-scale systems the ways in which a model interacts with its environment is always changing, and it is entirely plausible that some innocuous-looking change in the future would increase the amount of feedback. Our methodology provides us with a way to continuously monitor how feedback is affected by changes to the system, and can alert us to changes that cause problems. In Appendix B, we show some simulations with a wider range of effect sizes.

6 Conclusion

In this paper, we proposed a randomization scheme that can be used to detect feedback in real-world predictive systems. Our method involves adding noise to the predictions made by the system; this noise puts us in a randomized experimental setup that lets us measure feedback as a causal effect. In general, the scale of the artificial noise required to detect feedback is smaller than the scale of the natural predictor noise; thus, we can deploy our feedback detection method without disturbing our system of interest too much. The method does not require us to make hypotheses about the mechanism through which feedback may propagate, and so it can be used to continuously monitor predictive systems and alert us if any changes to the system lead to an increase in feedback.

Related Work

The interaction between models and the systems they attempt to describe has been extensively studied across many fields. Models can have different kinds of feedback effects on their environments. At one extreme of the spectrum, models can become self-fulfilling prophecies: for example, models that predict economic growth may in fact cause economic growth by instilling market confidence [12, 13]. At the other end, models may distort the phenomena they seek to describe and therefore become invalid. A classical example of this is a concern that any metric used to regulate financial risk may become invalid as soon as it is widely used, because actors in the financial market may attempt to game the metric to avoid regulation [14]. However, much of the work on model feedback in fields like finance, education, or macro-economic theory has focused on negative results: there is an emphasis on understanding when feedback can happen and promoting awareness about how feedback can interact with policy decisions, but there does not appear to be much focus on actually fitting feedback. One notable exception is a paper by Akaike [15], who showed how to fit cross-component feedback in a system with many components; however, he did not add artificial noise to the system, and so was unable to detect feedback of a single component on itself.

Acknowledgments

The authors are grateful to Alex Blocker, Randall Lewis, and Brad Efron for helpful suggestions and interesting conversations. S. W. is supported by a B. C. and E. J. Eaves Stanford Graduate Fellowship.

References

- [1] Paul W Holland. Statistics and causal inference. Journal of the American Statistical Association, 81(396):945–960, 1986.

- [2] Joshua D Angrist, Guido W Imbens, and Donald B Rubin. Identification of causal effects using instrumental variables. Journal of the American Statistical Association, 91(434):444–455, 1996.

- [3] Bradley Efron and David Feldman. Compliance as an explanatory variable in clinical trials. Journal of the American Statistical Association, 86(413):9–17, 1991.

- [4] Guido W Imbens and Joshua D Angrist. Identification and estimation of local average treatment effects. Econometrica, 62(2):467–475, 1994.

- [5] Léon Bottou, Jonas Peters, Joaquin Quiñonero-Candela, Denis X Charles, D Max Chickering, Elon Portugaly, Dipankar Ray, Patrice Simard, and Ed Snelson. Counterfactual reasoning and learning systems: The example of computational advertising. Journal of Machine Learning Research, 14:3207–3260, 2013.

- [6] David Chan, Rong Ge, Ori Gershony, Tim Hesterberg, and Diane Lambert. Evaluating online ad campaigns in a pipeline: Causal models at scale. In Proceedings of the 16th ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 7–16. ACM, 2010.

- [7] Donald B Rubin. Causal inference using potential outcomes. Journal of the American Statistical Association, 100(469):322–331, 2005.

- [8] Trevor Hastie, Robert Tibshirani, and Jerome Friedman. The Elements of Statistical Learning. Springer New York, second edition, 2009.

- [9] Peter J Huber. The behavior of maximum likelihood estimates under nonstandard conditions. In Proceedings of the Fifth Berkeley Symposium on Mathematical Statistics and Probability, pages 221–233, 1967.

- [10] Halbert White. A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity. Econometrica: Journal of the Econometric Society, 48(4):817–838, 1980.

- [11] Bradley Efron and Robert Tibshirani. An Introduction to the Bootstrap. CRC press, 1993.

- [12] Robert K Merton. The self-fulfilling prophecy. The Antioch Review, 8(2):193–210, 1948.

- [13] Fabrizio Ferraro, Jeffrey Pfeffer, and Robert I Sutton. Economics language and assumptions: How theories can become self-fulfilling. Academy of Management Review, 30(1):8–24, 2005.

- [14] Jón Danıelsson. The emperor has no clothes: Limits to risk modelling. Journal of Banking & Finance, 26(7):1273–1296, 2002.

- [15] Hirotugu Akaike. On the use of a linear model for the identification of feedback systems. Annals of the Institute of Statistical Mathematics, 20(1):425–439, 1968.

- [16] Theodoros Evgeniou, Massimiliano Pontil, and Tomaso Poggio. Regularization networks and support vector machines. Advances in Computational Mathematics, 13(1):1–50, 2000.

- [17] Federico Girosi, Michael Jones, and Tomaso Poggio. Regularization theory and neural networks architectures. Neural Computation, 7(2):219–269, 1995.

- [18] Peter J Green and Bernard W Silverman. Nonparametric Regression and Generalized Linear Models: A Roughness Penalty Approach. Chapman & Hall London, 1994.

- [19] Trevor Hastie and Robert Tibshirani. Generalized Additive Models. CRC Press, 1990.

- [20] Grace Wahba. Spline Models for Observational Data. Siam, 1990.

- [21] Stefanie Biedermann, Holger Dette, and David C Woods. Optimal design for additive partially nonlinear models. Biometrika, 98(2):449–458, 2011.

- [22] Werner G Müller. Optimal design for local fitting. Journal of statistical planning and inference, 55(3):389–397, 1996.

- [23] William J Studden and D J VanArman. Admissible designs for polynomial spline regression. The Annals of Mathematical Statistics, 40(5):1557–1569, 1969.

- [24] Erich Leo Lehmann and George Casella. Theory of Point Estimation. Springer, second edition, 1998.

Appendix A Fitting Non-Linear Feedback by Ordinary Least Squares Regression

Carrying out the fitting procedure outlined in Section A is straight-forward using standard R functions if we are willing to construct and using pre-specified basis expansions

| (17) |

Recall that cannot have an intercept, as it would not be identifiable. We first need to construct the design matrices

| (18) |

from (14). Constructing just involves choosing a basis function; however, evaluating

| (19) |

for each row of can be computationally intensive if we are not careful. In particular, evaluating by numerical integration separately for each can be painfully slow. A more efficient way to compute is to evaluate over a grid of -values in a single pass using the fast Fourier transform (e.g., by using convolve in R), and then to linearly interpolate the result onto the real line (e.g., using approxfun).

Once we have computed these design matrices, we can estimate and by solving the linear regression problems

| (20) |

and

| (21) |

where is just a vector with entries . Notice that this whole procedure only requires knowledge of , , and the noised new predictions ; we never reference the counterfactual predictions or unobservable predictions .

In practice, most of the errors in our procedure come from the difference equation (21) and not from the conditional mean regression (20). Thus, when our model is well-specified and the additivity assumption holds, we can get good estimates for the accuracy of by looking at the parametric standard error estimates provided by lm from fitting (21); this is what we did for the simulations presented in Figure 2. In case of model misspecification, however, parametric confidence intervals can break down and it is better to use non-parametric methods such as the bootstrap. We used a non-parametric bootstrap for the logs simulation presented in Section 5.

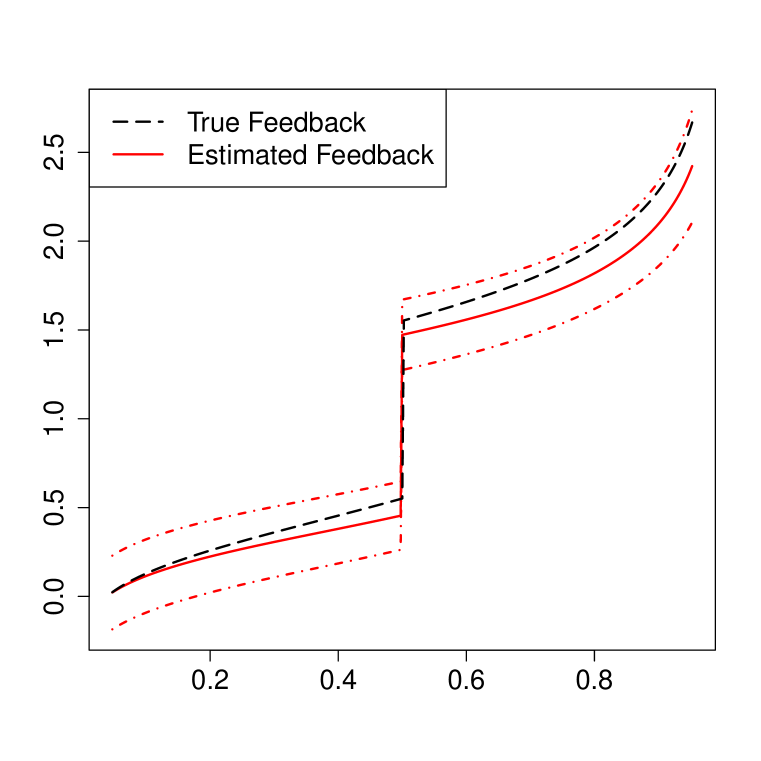

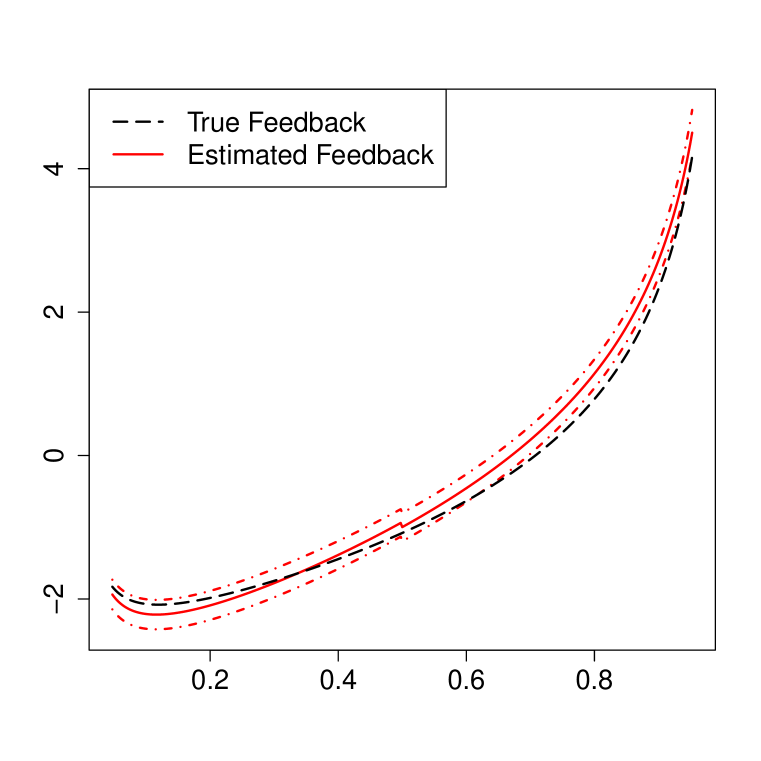

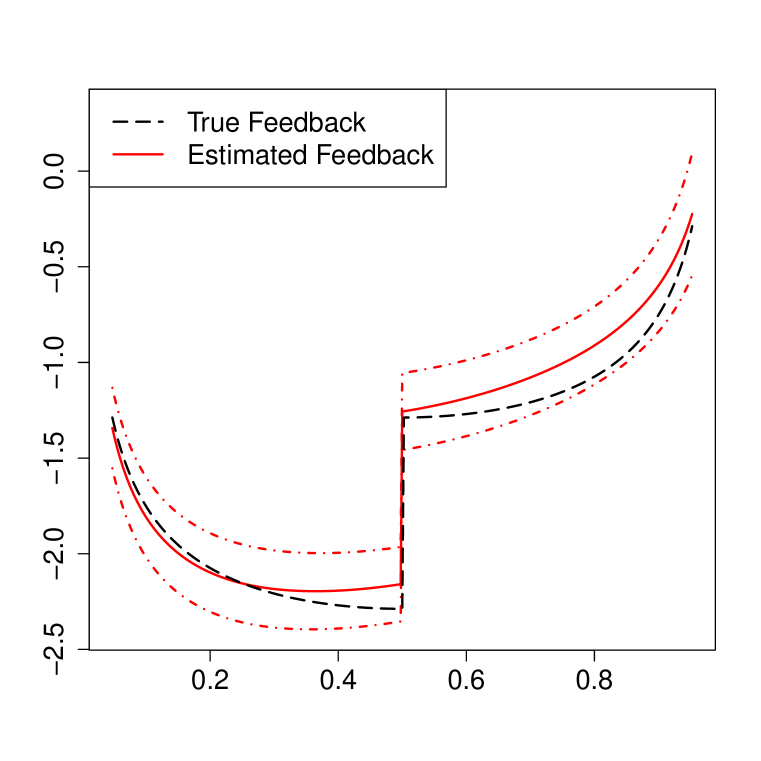

Appendix B Simulation Experiments

Here, we present a collection of simulation experiments, the results of which are given in Figure 2. These examples are all logistic regression examples with additive feedback in log-odds space. In the plots, the -axis shows feedback in log-odds space, whereas the -axis shows deployed predictions in probability space.

The simulations all had (old prediction, new prediction) pairs. The predictions had natural noise with standard error , i.e., the pair was centered at and distributed as . We added Gaussian noise with to the deployed predictions. In order to mimic real datasets, we made our simulation highly imbalanced: There were many strong predictions for the negative class with , but less so for the positive class. This is why our model performed better near than near .

We fit both the trend and the feedback function as the sum of a natural spline with degrees of freedom and knots spread evenly over , and a jump at zero log-odds (i.e., ). The dashed lines show the different feedback functions used in each example.

As emphasized earlier, the intercept of the feedback function is not identifiable from our experiments. We fixed the intercept by setting the average fitted feedback over all training examples to 0. Since all our training sets were heavily imbalanced, this effectively amounted to setting feedback to 0 at . The plots that do not hit the (0, 0) point are missing a sharp spike at the left-most end; the plot ends at .

Appendix C Extensions and Further Work

In this section, we discuss some possible extensions to the work presented in this paper.

C.1 Feedback Removal

If we detect feedback in a real-world system, we can try to identify the root causes of the feedback and fix the problem by removing the feedback loop. That being said, a natural follow-up question to our research is whether we can automatically remove feedback. In the context of the linear feedback model (2), we incur an expected squared-error loss of

from completely ignoring the feedback problem. Meanwhile, if we use the maximum likelihood estimate to correct feedback, we suffer a loss

where the first term comes from our errors in estimating and the second comes from the extra noise we needed to inject into the system in order to detect the feedback.

An interesting topic for further research would be to find how to optimally set the scale of the artificial noise under various utility assumptions, and to understand the potential failure modes of feedback removal under model misspecification. In order to remove feedback, we would also need to have some way of dealing with the intercept term.

C.2 Covariate-Dependent Feedback

Our analysis was presented in the context of the additive feedback model

In practice, however, we may want to let feedback depend on some other covariates

for example, we may want to slice feedback by geographic region. One particularly interesting but challenging extension would be to make feedback depend on the unperturbed prediction :

For example, if is a prediction for how good a search result is, we might assume that search results that are actually good have a different feedback response from those that are terrible . The challenge here is that is unobserved, and so we need to have it act on via proxies. Developing a formalism that lets depend on in a useful way while allowing for consistent estimation seems like a promising pathway for further work.

C.3 Penalized Regression

The key technical challenge in implementing our method for feedback detection is solving the spline equation (12). In Section 4 we proposed a pragmatic approach that enabled us to get good feedback estimates in many examples. However, it should be possible to devise more general methods for fitting . The equation (12) is linear in , and so any strictly convex penalty function over some convex subset of real valued functions on leads to a well-defined estimator through the convex optimization problem

| (22) | ||||

In the context of smoothing splines, a popular choice is to use

and make be the set on which this integral is well-defined. There is an extensive literature on non-parametric regression problems constrained by smoothness penalties [16, 17, 18, 19, 20]; presumably, similar approaches should also give us smoothing spline solutions to (12).

C.4 Deterministic Designs

Finally, in this paper, we have focused on detecting feedback by adding random noise to raw model predictions. It would be interesting to see whether we can improve the efficiency of our procedure by optimizing the noise choice more closely and using a deterministic design. The problem of finding optimal designs for spline-type problems has been studied by several authors [21, 22, 23].

Appendix D Proofs

Proof of Theorem 1.

Because is fully artificial noise, we know a-priori that and are independent. Thus, we can treat as a homoscedastic noise term for our regression, and (3) follows immediately from standard results for ordinary least squares regression. ∎

Proof of Theorem 2.

The are independent of the , and so (7) follows from an argument analogous to the one that led to (3). If the are still homoscedastic after conditioning on then, because the are mean-zero by construction, the fact that is the best linear unbiased estimator of follows directly from an application of the Gauss-Markov theorem where we treat as fixed and as random, see[24], p. 184. ∎