A Lyapunov Optimization Approach to Repeated Stochastic Games

Abstract

This paper considers a time-varying game with players. Every time slot, players observe their own random events and then take a control action. The events and control actions affect the individual utilities earned by each player. The goal is to maximize a concave function of time average utilities subject to equilibrium constraints. Specifically, participating players are provided access to a common source of randomness from which they can optimally correlate their decisions. The equilibrium constraints incentivize participation by ensuring that players cannot earn more utility if they choose not to participate. This form of equilibrium is similar to the notions of Nash equilibrium and correlated equilibrium, but is simpler to attain. A Lyapunov method is developed that solves the problem in an online max-weight fashion by selecting actions based on a set of time-varying weights. The algorithm does not require knowledge of the event probabilities and has polynomial convergence time. A similar method can be used to compute a standard correlated equilibrium, albeit with increased complexity.

I Introduction

Consider a repeated game with players and one game manager. The game is played over an infinite sequence of time slots . Every slot there is a random event vector . The game manager observes the full vector , while each player observes only the component . The value represents information known only to the manager. After the slot event is observed, the game manager sends a message to each player . Based on this message, the players choose a control action . The random event and the collection of all control actions for slot determine individual utilities for each player . Each player is interested in maximizing the time average of its own utility process. The game manager is interested in providing messages that lead to a fair allocation of time average utilities across players.

Specifically, let be the time average of . The fairness of an achieved vector of time average utilities is defined by a concave fairness function . The goal is to devise strategies that maximize subject to certain game-theoretic equilibrium constraints. For example, suppose the fairness function is a sum of logarithms:

This corresponds to proportional fair utility maximization, a concept often studied in the context of communication networks [2]. Another natural concave fairness function is:

for some given constant . This fairness function assigns no added value when the average utility of one player exceeds that of another.

Let be the message vector provided by the game manager on slot . The value is an element of the set and represents the action the manager would like player to take. A player is said to participate if she always chooses the suggestion of the manager, that is, if for all . At the beginning of the game, each player makes a participation agreement. Participating players receive the messages , while non-participating players do not.

This paper considers the class of algorithms that deliver message vectors as a stationary and randomized function of the observed . Assuming that all players participate, this induces a conditional probability distribution on the actions, given the current . The conditional distribution is defined as a coarse correlated equilibrium (CCE) if it yields a time average utility vector with the following property [3]: For each player , the average utility is at least as large as the maximum time average utility this player could achieve if she did not participate (assuming the actions of all other players do not change). Overall, the goal is to maximize subject to the CCE constraints.

I-A Contributions and related work

The notion of coarse correlated equilibrium (CCE) was introduced in [3] in the static case where there is no event process . The CCE definition is similar to a correlated equilibrium (CE) [4][5][6]. The difference is as follows: A correlated equilibrium (CE) is more stringent and requires the utility achieved by each player to be at least as large as the utility she could achieve if she did not participate but if she still knew the messages on every slot. It is known that both CCE and CE constraints can be written as linear programs. Adaptive methods that converge to a CE for static games are developed in [7][8][9]. The concept of Nash equilibrium (NE) is more stringent still: The NE constraint requires all players to act independently and without the aid of a message process [10][6]. Unfortunately, the problem of computing a Nash equilibrium is nonconvex.

This paper uses the NE, CE, and CCE concepts in the context of a stochastic game with random events . The optimal action associated with a particular event can depend on whether or not the event is rare. This paper develops an online algorithm that is influenced by the event probabilities, but does not require knowledge of these probabilities. The algorithm uses the Lyapunov optimization theory of [11][12] and is of the max-weight type. Specifically, every slot , the game manager observes the realization and chooses a suggestion vector by greedily minimizing a drift-plus-penalty expression. Such Lyapunov methods are used extensively in the context of queueing networks [13][14] (see also related methods in [15][16][17]). This is perhaps the first use of such techniques in a game-theoretic setting.

One reason the solution of this paper can have a simple structure is that the random event process is assumed to be independent of the prior control actions. Specifically, while the components are allowed to be arbitrarily correlated across , the vector is assumed to be independent and identically distributed (i.i.d.) over slots. Prior work on stochastic games considers more complex problems where is influenced by the control action of slot , including work in [18] which studies correlated equilibria in this context. This typically involves Markov decision theory and has high complexity. Specifically, if is the set of all possible values of , and if is the (finite) size of this set, then complexity is typically at least as large as .

In contrast, while the current paper treats a stochastic problem with more limited structure, the resulting solution is simple and grows as . Specifically, the algorithm uses a number of virtual queues that is linear in , rather than exponential in , resulting in polynomial bounds on convergence time. Furthermore, the number of virtual queues grows only linearly in the size of each set . This improves on the original conference version of this paper [1], which required a number of virtual queues that was exponential in the size of . The exponential-to-polynomial improvement is done by equivalently modeling the constraints via a grouping of conditional expectations given an observed random event.

II Static games

This section introduces the problem in the static case without random processes . The different forms of equilibrium are defined and compared through a simple example. The general stochastic problem is treated in Section III.

Suppose there are players, where is an integer larger than 1. Each player has an action space , assumed to be a finite set. The game operates in slotted time . Every slot , each player chooses an action . Let be the vector of control actions on slot . The utility earned by player on slot is a real-valued function of :

The utility functions can be different for each player . Define . Consider starting with a particular vector and modifying it by changing a single entry from to some other action . This new vector is represented by the notation . Define as the set of all vectors , being the set product of over all .

The three different forms of equilibrium considered in this section are defined by probability mass functions for . It is assumed throughout that:

-

•

for all .

-

•

.

If actions are chosen independently every slot according to the same probability mass function , the law of large numbers ensures that, with probability 1, the time average utility of each player is:

II-A Nash equilibrium (NE)

II-B Correlated equilibrium (CE)

The standard concept of correlated equilibrium from [4][5] can be motivated by a game manager that provides suggested actions every slot , where player only sees , player only sees , and so on. Assume the suggestion vector is independent and identically distributed (i.i.d.) over slots with some probability mass function . Assume all players participate, so that every slot their chosen actions match the suggestions. The probability mass function is a correlated equilibrium (CE) if:

| (3) |

These constraints imply that no player can gain a larger average utility by individually deviating from the suggestions of the game manager [5]. This can be understood as follows: Fix an and an such that . Divide both sides of the above inequality by . Then:

-

•

The left-hand-side is the conditional expected utility of player , given that all players participate and that player sees suggestion on the current slot.

-

•

The right-hand-side is the conditional expected utility of player , given that she sees on the current slot, that all other players participate, and that player chooses action instead of (so player does not participate).

The correlated equilibrium constraints are linear in the variables. Define as the number of actions in set . The number of linear constraints specified by (3) is then:

| (4) |

II-C Coarse correlated equilibrium (CCE)

The definition of correlated equilibrium assumes that non-participating players still receive the suggestions from the game manager. As the suggestion for player may be correlated with the suggestions of other players , this can give a non-participating player a great deal of information about the likelihood of actions from other players. The following simple modification assumes that non-participating players do not receive any suggestions from the game manager. A probability mass function is a coarse correlated equilibrium (CCE) if it satisfies the constraints (2). Note that the product form constraints (1) are not required. This CCE definition was introduced in [3]. Similar to the CE case, these CCE constraints imply that no player can increase her average utility by individually deviating from the suggestions of the game manager.

The CCE constraints (2) are linear in the values. The number of CCE constraints is:

This number is typically much less than the number of constraints required for a CE, specified in (4). Assuming that for each player (so that each player has at least 2 action options), the number of CCE constraints is always less than or equal to the number of CE constraints, with equality if and only if for all players .

II-D A superset result

The assumption that all sets are finite make the game a finite game. Fix a finite game and define , , and as the set of all probability mass functions that define a (mixed strategy) Nash equilibrium, a correlated equilibrium, and a coarse correlated equilibrium, respectively. It is known that every such finite game has at least one mixed strategy Nash equilibrium, and so is nonempty [19][10]. Furthermore, it is known that any NE is also a CE, and any CE is also a CCE, so that [4][5][3]:

| (5) |

Furthermore, the sets and are closed, bounded, and convex [4][5][3].

II-E A simple example

Consider a game where player has three control options and player has two control options:

The utility functions and are specified in the table of Fig. 1, where player 1 actions are listed by row and player 2 actions are listed by column.

There are six possible action vectors . Define the mass function by values , , , , , associated with each of the six possibilities, as shown in Fig. 1.

The eight CE constraints for this problem are:

| player 1 sees : | ||||

| player 1 sees : | ||||

| player 1 sees : | ||||

| player 1 sees : | ||||

| player 1 sees : | ||||

| player 1 sees : | ||||

| player 2 sees : | ||||

| player 2 sees : |

It can be shown that there is a single probability mass function that satisfies all of these CE constraints:

This is also the only NE. The average utility vector associated with this mass function is .

In contrast, the five CCE constraints for this problem are:

| player 1 chooses : | ||||

| player 1 chooses : | ||||

| player 1 chooses : | ||||

| player 2 chooses : | ||||

| player 2 chooses : | ||||

There are an infinite number of probability mass functions that satisfy these CCE constraints. Three different ones are given in the table of Fig. 2, labeled distribution 1, distribution 2, and distribution 3. Distribution 1 corresponds to the CE and NE distribution.

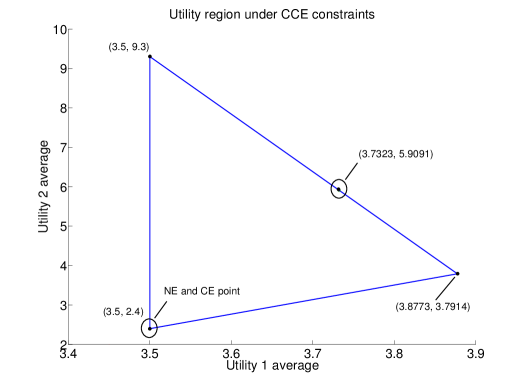

The set of all utility vectors achievable under CCE constraints is the triangular region shown in Fig. 3. The three vertices of the triangle correspond to the three distributions in Fig. 2, and are:

The point is the lower left vertex of the triangle and corresponds to the CE (and NE) distribution. It is clear that both players can significantly increase their utility by changing from CE constraints to CCE constraints. This illustrates the following general principle: All players benefit if non-participants are denied access to the suggestions of the game manager. This principle is justified by (5).

II-F Utility optimization with equilibrium constraints

There are typically many probability distributions that satisfy the CCE constraints. The goal is to find one that leads to an optimal vector of average utilities. Optimality is determined by a concave fairness function, as defined below.

For convenience, assume all utility functions are nonnegative. Define as an upper bound on the utility for each player , so that:

Define as a continuous and concave function that maps the set to the real numbers. This is called the fairness function. The game manager chooses a probability mass function with the goal of maximizing subject to CCE constraints:

| Maximize: | (6) | ||||

| Subject to: | (7) | ||||

| (8) | |||||

| (9) | |||||

| CCE constraints (2) are satisfied | (10) |

III Stochastic games

Let be a vector of random events for slot . Each component takes values in some finite set , for . Define . The vector process is assumed to be independent and identically distributed (i.i.d.) over slots with probability mass function:

where the notation “” means “defined to be equal to.” On each slot , the components of the vector can be arbitrarily correlated.

At the beginning of each slot , each player observes its own random event . The game manager observes the full vector , including the additional information . It then sends a suggested action to each participating player . Assume , where is the finite set of actions available to player . Each player chooses an action . Participating players always choose . Non-participating players do not receive and choose using knowledge of only and of events that occurred before slot .

Let be the action vector. The utility earned by each player on slot is a function of and :

For convenience, assume utility functions are nonnegative with maximum values for , so that:

III-A Discussion of game structures

This model can be used to treat various game structures. For example, the scenario where all players have full information can be treated by defining for all . This is useful in games related to economic markets, where can represent a commonly known vector of current prices. Alternatively, one can imagine a game with a single random event process that is known to the game manager but unknown to all players. For example, consider a game defined over a wireless multiple access system. Wireless users are players in the game, and the access point is the game manager. In this example, can represent a vector of current channel conditions known only to the access point. Such games can be treated by setting to a default constant value for all and all slots .

III-B Pure strategies and the virtual static game

Assume all players participate, so that for all . For each , denote the sizes of sets and by and , respectively. Define a pure strategy function for player as a function that maps to the set . There are such functions. Define:

Enumerate the pure strategy functions for player and represent them by for . Define:

Each vector can be used to specify a profile of pure strategies used by each player. For each and each , define:

| (11) |

In the special case when the action of each player on slot is defined by pure strategy , the action vector is . The average utility earned by player on such a slot is defined:

| (12) |

The stochastic game can be treated as a virtual static game as follows: The virtual static game also has players. The virtual action space of each player is viewed as the set of pure strategies . Every slot , each player selects a pure strategy . The virtual utility functions are given by the functions .

The virtual static game is still a finite game. Hence, the NE, CE, and CCE definitions for static games can be used here. In particular, let be a probability mass function over the finite set of strategy profiles . Then:

-

•

(NE for virtual static game) is a NE for the virtual static game if it has the product form:

(13) where , and if:

(14) -

•

(CE for virtual static game) is a CE for the virtual static game if:

(15) -

•

(CCE for virtual static game) is a CCE for the virtual static game if it satisfies (14).

A given probability mass function defined over generates a conditional probability mass function defined over all and :

| (16) |

where is an indicator function that is 1 if , and is 0 else. However, not all functions can be generated in this way.111The conference version of this paper [1] contained an incorrect statement suggesting that all distributions can be generated by distributions according to (16) (Lemma 1 from page 5 of [1]). While this is true in the case when can be an arbitrary function of the full vector, it does not hold for strategy functions with the structure (11). The author regrets the misleading statement in [1]. Fortunately, that incorrect statement was never used, and so it did not affect any of the results in [1].

For example, the right-hand-side of (16) does not depend on . In contrast, a game manager might want to select as a function of the full random event vector .

If (16) holds, a game manager with no knowledge of the random event vector could produce suggestions according to by randomly selecting a strategy vector with probability , and then broadcasting component to each player . Thus, the NE, CE, and CCE conditions in (13)-(15) for the virtual static game can be viewed as information restricted (IR) notions of equilibrium for the stochastic game. Formally, define a probability mass function to be an IR-NE if it satisfies (13)-(14), an IR-CE if it satisfies (15), and an IR-CCE if it satisfies (14).

Lemma 1

Proof:

III-C General equilibrium for the stochastic game

Let be a conditional probability mass function defined over , . It is assumed throughout that:

| (18) | |||||

| (19) |

General equilibria for the stochastic game can be defined in terms of . The conference version of this paper [1] does this by specifying constraints for each pure strategy , similar to the virtual static game constraints (14) and (15). Unfortunately, this requires a number of constraints that is exponential in the size of the sets . The following alternative definition is equivalent to that given in [1], yet uses only a polynomial number of constraints. For the case of NE and CCE, it does so by introducing additional variables for each and each . Intuitively, represents the largest conditional expected utility achievable by player , given that she does not participate and that she observes .

-

•

(NE for the stochastic game) is a NE for the stochastic game if it has the product form (17) and if there are real numbers such that:

(20) and

(21) -

•

(CE for the stochastic game) is a CE for the stochastic game if there are real numbers such that:

(22) and

(23) - •

The next lemma shows that every information restricted equilibrium generates a general equilibrium .

Lemma 2

Suppose and satisfy (16). Then:

(c) If is a NE for the virtual static game, then is a NE for the stochastic game.

Proof:

See Appendix A. ∎

One may wonder if the constraints (20)-(21) can be stated more simply by removing the variables. Indeed, one may wonder if (20)-(21) are equivalent to:

for all , , . This is not generally the case. Indeed, the above constraints are more restrictive and imply that the conditional expected utility of player , given she observes , is greater than or equal to the conditional expectation this player could achieve given and given that she does not participate. On the other hand, the constraints (20)-(21) allow a violation of this property for a given . Such a violation does not imply that player could improve beyond the utility associated with participating. That is because that act of not participating may itself decrease the achievable average utility in certain states by an amount that cannot be recovered by changing strategies on other states. This is a subtlety that does not arise in the static game context without the processes.

Define , , as the set of all conditional probability mass functions that are NE, CE, and CCE, respectively, for the stochastic game.

Lemma 3

For a general stochastic game as defined above:

(a) The set is nonempty.

(b) .

(c) Sets and are closed, bounded, and convex.

Proof:

The virtual static game is finite and hence has at least one mixed strategy NE [19][10]. Let be the corresponding conditional mass function defined by (16). Then is a NE for the stochastic game (by Lemma 2c), and so is nonempty. This proves part (a).

To prove (c), note that is the intersection of the set of all that satisfy the (closed, bounded, and convex) probability simplex constraints (18)-(19) and the set of all that satisfy the linear constraints (20)-(21). Similarly, is the intersection of all that satisfy (18)-(19) with all that satisfy the linear constraints (22)-(23).

To prove that , suppose that is a CE. Then it satisfies the CE constraints (22)-(23) for some values . Define:222More precisely, the values are defined to be in the special case when .

These values satisfy . Summing (23) over and applying the above definition of proves that (20)-(21) hold. The proof that is given in Appendix B. ∎

III-D Complexity comparison

The CCE for the virtual static game is defined by the constraints (14). There is one such constraint for each and each , where is the number of pure strategies for player . Thus, the number of constraints is:

This grows exponentially in the size of the sets . Thus, even though these constraints are linear, computation of a CCE for the virtual static game can be very complex.

The CCE constraints for the stochastic game are given in (20)-(21). There are constraints in (20). For (21), there is one such constraint for each , each , and each , for a total of:

This is linear in the sizes of the and sets. Thus, the general CCE constraints (20)-(21) provide a significant complexity reduction. A similar “exponential-to-polynomial” complexity reduction holds for the CE definition when comparing the constraints in (15) to those in (22)-(23).

III-E Unilateral changes cannot increase utility

The stochastic NE, CE, and CCE definitions above have the following property: Assuming actions are chosen according to an equilibrium mass function , a given player cannot improve her utility by unilaterally deviating from these actions. This is formalized in the lemmas below.

First note that if is chosen according to a mass function , then for all :

Now fix . For all , let be a random function that maps a point to a randomly chosen point according to some distribution that depends on . It is assumed that for a given slot , is conditionally independent of and given . The expected utility on slot associated with unilaterally changing action to action is:

where the expectation on the right-hand-side is with respect to the distribution of .

Proof:

Suppose satisfies (20)-(21). Fix . Fix a random function , and define:

Multiplying (21) by and summing over gives:

Summing both sides over and using (20) gives the expression (24).

Now suppose (24) holds for all and all randomized functions . Fix . For each deterministically define as the element that maximizes the right-hand-side of (21) over all . Likewise, define by:

assuming the denominator is nonzero (else, define ). Then (21) holds by construction. Further, inequality (20) holds because it is equivalent to (24) for the given function. ∎

The next lemma extends the random function to , so that its distribution depends on both and :

Lemma 5

is a CE for the stochastic game if and only if:

for all and all randomized functions .

Proof:

The proof is similar to that of Lemma 4 and is omitted for brevity. ∎

III-F Optimization objective

As before, define as a continuous and concave function that maps to the set of real numbers. The goal is to choose messages according to a conditional probability mass function that solves the problem below:

| Maximize: | (25) | ||||

| Subject to: | (26) | ||||

| CCE constraints (20)-(21) are satisfied | (27) | ||||

| (28) | |||||

| (29) |

This is a convex program in the unknowns . The next section presents an online solution that does not require knowledge of the probabilities .

IV Lyapunov optimization

For a real-valued stochastic process defined over slots , define:

Recall that for each player and each slot . For , , and , define:

where is an indicator function that is 1 if , and 0 else. The value is zero if , and else it is the utility player would receive on slot if it uses action (assuming are the actions of others).

A reformulation of (25)-(29) that does not require the decisions to use the same conditional distribution every slot is as follows: Every slot , the game manager observes and chooses an action vector and variables to solve:

| Maximize: | |||

| (30) | |||

| Subject to: | |||

| (31) | |||

| (32) | |||

| (33) | |||

| (34) |

The constraints (31) correspond to (20), and the constraints (32) correspond to (21). Such time average problems can be solved by stationary and randomized algorithms [11]. Specifically, if and are optimal variables for problem (25)-(29), then the following is an optimal solution to (30)-(34): Every slot , observe and independently choose according to the conditional mass function , and choose . Conversely, any solution to (30)-(34) has the following property: For any , there is a positive integer such that for any , time average expectations over produce conditional probability mass functions that are within of satisfying all constraints and achieving the optimal objective function value of problem (25)-(29). Specifically:

IV-A Transformation via Jensen’s inequality

Using the auxiliary variable technique of [11], the problem (30)-(34), which seeks to maximize a nonlinear function of a time average, can be transformed into a maximization of the time average of a nonlinear function. To this end, let be an auxiliary vector that the game manager chooses on slot , assumed to satisfy for all and all . Define:

Jensen’s inequality implies that for all slots :

| (36) |

Now consider the following problem: Every slot the game manager observes and chooses an action vector , variables , and an auxiliary vector to solve:

| Maximize: | |||

| (37) | |||

| Subject to: | |||

| (38) | |||

| (39) | |||

| (40) | |||

| (41) | |||

| (42) | |||

| (43) |

The problems (30)-(34) and (37)-(43) are equivalent. To see this, let and be the optimal objective values for problems (30)-(34) and (37)-(43), respectively. Let and be optimal stationary and randomized decisions that solve (30)-(34), and let be the corresponding expected utilities for player . Then:

The decisions and can be used, together with for all and all , to satisfy all constraints of the new problem (37)-(43) with (possibly sub-optimal) objective function value . Because this is not necessarily optimal for the new problem, one has .

On the other hand, let , , and be decisions that solve the new problem (37)-(43). Then these same decisions satisfy all constraints of the problem (30)-(34) and thus yield an objective function value no more than , so that:

| (44) | |||||

| (45) | |||||

| (46) |

where (44) follows by (38) together with continuity of , (45) follows by Jensen’s inequality (36), and (46) follows because the decisions are optimal for the new problem. It follows that . In particular, any solution to (37)-(43) also solves (30)-(34).

IV-B The drift-plus-penalty algorithm

For the constraints (39), for each define a virtual queue with update equation:

The above looks like a slotted time queueing equation with arrival process and service process . The intuition is that if a control algorithm is constructed that makes these queues mean rate stable, so that:

then constraint (39) is satisfied [11]. This queueing update can be simplified using the identity:

Hence:

| (47) |

Likwewise, to enforce the constraint (40), for each , , , define a virtual queue with update equation:

| (48) |

Finally, for the constraints (38), for each define a virtual queue with update equation:

| (49) |

Define the function:

This is called a Lyapunov function. Define , called the Lyapunov drift on slot . The drift-plus-penalty algorithm is defined by choosing control actions greedily every slot to minimize a bound on the drift-plus-penalty expression . Here, is the “penalty” and is a nonnegative constant that affects a tradeoff between convergence time and proximity to the optimal solution.

Lemma 6

For all slots one has:

| (50) |

where:

Proof:

Greedily minimizing the right-hand-side of (50) every slot leads to the following algorithm: Every slot , the game manager observes the queues , , and the current . Then:

-

•

Auxiliary variables : The game manager chooses as the solution to:

Maximize: Subject to: (51) -

•

Auxiliary variables : For each and , choose to minimize:

-

•

Suggested actions: Choose to minimize:

The manager then sends suggested actions to each (participating) player .

- •

This is an online algorithm that does not require knowledge of the probabilities .

IV-C A closer look at the algorithm

The selection in the above algorithm reduces to the following: Every slot , observe and the queues. Then for each and , choose:

The decisions reduce to the following: Every slot , observe and the queues. Then choose to minimize:

Finally, consider the case when the fairness function is a separable sum of individual concave functions:

Then the decisions reduce to separately choosing for each as the value in the interval that maximizes . For example, if , then:

where is defined:

IV-D Performance analysis

For simplicity, assume all virtual queues are initially empty, so that . Define as the optimal value of the objective function for (25)-(29). By equivalence of the transformations, is also the optimal value for problem (37)-(43). Define as the vector of all virtual queues , , , and define .

Theorem 1

If and the above algorithm is implemented using a fixed value , then:

(a) For all slots one has:

(c) For all slots the virtual queue sizes satisfy:

where is the maximum possible value for , being the maximum of over for all .333In the special case when is entrywise nondecreasing, then .

Proof:

Fix a time slot . Given the existing queue values , , and the observed , the algorithm makes decisions , , to minimize the right-hand-side of (50). Thus:

| (52) |

for any alternative decisions , , that satisfy (42)-(43), and where:

Now consider alternative decisions defined by the optimal solution to problem (25)-(29). Specifically, choose to be conditionally independent of current queue states, given the observed , according to the probability distribution that solves (25)-(29). Choose , where are the optimal values for the solution to (25)-(29). Finally, define , being the expected utility of player under the optimal distribution , and note that:

Choose for all . Then (20)-(21) imply:

| (53) | |||||

| (54) | |||||

| (55) | |||||

| (56) |

Taking expectations of (52) and substituting (53)-(56) gives:

The above inequality holds for all . Fix a slot . Summing the above over slots and using gives:

| (57) |

Rearranging (57) and using the definition of gives:

Using Jensen’s inequality and proves part (a).

Again rearranging (57) gives:

Using the fact that , dividing by , and taking square roots proves part (c). Part (b) follows immediately from part (c).

∎

Define . Theorem 1 shows that average utility is within of optimality. Part (c) of the theorem implies that constraint violation is within after time . If a Slater condition holds, this convergence time is improved to [11]. Similar bounds can be shown for infinite horizon time averages (rather than time average expectations) [20].

IV-E Discussion

The online algorithm ensures the constraints (39)-(40) are satisfied. This shows that average utility of each player is greater than or equal to the achievable utility if the player were to constantly use the best pure strategy. The best pure strategy of player is the one that uses the optimal action as a function of the observed . This corresponds to the constraints in (20)-(21). If an algorithm makes random decisions independently every slot according to a conditional probability mass function , then constraints (39)-(40) imply player cannot do better under any alternative decisions, possibly those that mix pure strategies with different mixing probabilities every slot. A subtlety is that the online algorithm does not make stationary and randomized decisions. Thus, it is not clear if a player with knowledge of the algorithm could improve average utility by making alternative decisions that do not correspond to a pure strategy. Of course, the online algorithm yields time averages that correspond to a desired . Thus, a potential fix is to run the online algorithm in the background and make decisions according to the time averages that emerge.

V Simplification under a special case

Consider the special case when there is a single random event process that is known only to the game manager. Thus, there are no random event processes for any player . This can be treated in the framework of the previous section by formally defining the sets to consist of a single element 0, so that for all slots and all players . However, this special case can be treated more simply by removing the auxiliary variables . Indeed, for all and all , define:

| Maximize: | |||

| (58) | |||

| Subject to: | |||

| (59) | |||

| (60) | |||

| (61) | |||

| (62) |

The above constraints are different from (37)-(43) because the variables have been removed, the constraint (40) has been removed, and the constraint (39) has been modified to (60).

Since the constraint (59) is identical to constraint (38), it is enforced by the same virtual queue with update equation given in (49). However, the constraint (60) is enforced by the following new constraint for all and :

| (63) |

The resulting algorithm is as follows: Every slot , the game manager observes the queues and the current . Then:

-

•

Auxiliary variables : Choose as before (that is, according to (51)).

-

•

Suggested actions: Choose to minimize:

- •

In this special case when no player observes any random events, the set of pure strategies for each player coincides with the set of actions . Thus, this algorithm is the same as that given in the conference version of this paper [1], where it is shown to give performance similar to that of Theorem 1.

VI Conclusions

This paper considered a simple game structure for repeated stochastic games. Every slot a random vector is generated by nature. Players observe different components of this vector and then choose individual actions with the help of a game manager. A coarse correlated equilibrium (CCE) for this stochastic game was defined to ensure that participating players earn at least as much utility as they could earn by individually deviating (and hence receiving no help from the manager). The paper considered optimizing a concave function of the vector of time average utilities (called a fairness function), subject to the CCE constraints. Lyapunov optimization was used to solve the problem over time, without requiring knowledge of the probabilities for the process. Similar techniques can be used to enforce correlated equilibrium (CE) constraints.

Appendix A — Proof of Lemma 2

Suppose and satisfy (16). The following identities are useful. For all one has:

| (64) |

This can be proven by substituting (16) into the left-hand-side of (64) and using (12). Likewise, for any and any pure strategy function for player (where ), one has:

| (65) |

Proof:

(Lemma 2a) Suppose satisfies the constraints (20)-(21). Fix . Substituting (64) into the left-hand-side of (20) gives:

| (66) |

Now fix an index . For each , define . Substituting this into (21) gives:

Summing the above over all and using (65) gives:

Combining the above with (66) proves that the constraints (14) hold.

Now Suppose satisfies the constraints (14). For each and , define the function as the action that maximizes:

Define as the corresponding maximum divided by . Then constraints (21) hold by construction. Now let be the index for the pure strategy of player that selects actions according to the function . Then:

| (67) |

Summing the above over all gives:

| (68) | |||

| (69) | |||

| (70) |

where (68) follows from (65), (69) follows from (14), and (70) follows from (64). Thus, the constraints (20) hold. ∎

VII Appendix B — Proof that

Suppose that is a NE for the stochastic game, so that it has the product form (17) and satisfies the constraints (20)-(21). Suppose is not a CE for the stochastic game, so that constraints (22)-(23) are not satisfied. The goal is to reach a contradiction.

Since the constraints (22)-(23) are not satisfied, by Lemma 5 it follows that there exists a player and a randomized function for which:

| (71) |

Because the product form property (17) holds, one has:

| (72) |

Now consider the following alternative strategy for player , based only on knowledge of its observed (without knowledge of ): Define the random action that observes , independently generates a random element according to the conditional distribution , and then defines . This policy uses the conditional distribution associated with the actual value, but does not require knowledge of this actual value. Define as the expected utility of player under this alternative randomized strategy :

By (72), is the same as the right-hand-side of (71), and so . On the other hand, since is a NE for the stochastic game, Lemma 4 ensures that no such alternative randomized strategy can improve the average utility of player , so that . This is the desired contradiction.

References

- [1] M. J. Neely. A Lyapunov optimization approach to repeated stochastic games. Proc. Allerton Conference on Communication, Control, and Computing, Oct. 2013.

- [2] F. Kelly. Charging and rate control for elastic traffic. European Transactions on Telecommunications, vol. 8, no. 1 pp. 33-37, Jan.-Feb. 1997.

- [3] H. Moulin and J. P. Vial. Strategically zero-sum games: The class of games whose completely mixed equilibria cannot be improved upon. International Journal of Game Theory, vol. 7, no. 3/4, pp. 201-221, 1978.

- [4] R. Aumann. Subjectivity and correlation in randomized strategies. Journal of Mathematical Economics, vol. 1, pp. 67-96, 1974.

- [5] R. Aumann. Correlated equilibrium as an expression of bayesian rationality. Econometrica, vol. 55, pp. 1-18, 1987.

- [6] M. J. Osborne and A. Rubinstein. A Course in Game Theory. MIT Press, Cambridge, MA, 1994.

- [7] D. P. Foster and R. V. Vohra. Calibrated learning and correlated equilibrium. Games and Economic Behavior, vol. 21, pp. 40-55, 1997.

- [8] S. Hart and A. Mas-Colell. A simple adaptive procedure leading to correlated equilibrium. Econometrica, vol. 68, no. 5, pp. 1127-1150, Sept. 2000.

- [9] D. Fudenberg and D. K. Levine. Conditional universal consistency. Games and Economic Behavior, vol. 29, no. 1-2, pp. 104-130, Oct. 1999.

- [10] J. F. Nash. Non-cooperative games. Annals of Mathematics, vol. 54, pp. 286-295, 1951.

- [11] M. J. Neely. Stochastic Network Optimization with Application to Communication and Queueing Systems. Morgan & Claypool, 2010.

- [12] L. Georgiadis, M. J. Neely, and L. Tassiulas. Resource allocation and cross-layer control in wireless networks. Foundations and Trends in Networking, vol. 1, no. 1, pp. 1-149, 2006.

- [13] L. Tassiulas and A. Ephremides. Dynamic server allocation to parallel queues with randomly varying connectivity. IEEE Transactions on Information Theory, vol. 39, no. 2, pp. 466-478, March 1993.

- [14] M. J. Neely, E. Modiano, and C. Li. Fairness and optimal stochastic control for heterogeneous networks. IEEE/ACM Transactions on Networking, vol. 16, no. 2, pp. 396-409, April 2008.

- [15] A. Eryilmaz and R. Srikant. Fair resource allocation in wireless networks using queue-length-based scheduling and congestion control. IEEE/ACM Transactions on Networking, vol. 15, no. 6, pp. 1333-1344, Dec. 2007.

- [16] A. Stolyar. Greedy primal-dual algorithm for dynamic resource allocation in complex networks. Queueing Systems, vol. 54, no. 3, pp. 203-220, 2006.

- [17] X. Lin, N. B. Shroff, and R. Srikant. A tutorial on cross-layer optimization in wireless networks. IEEE Journal on Selected Areas in Communications, Special Issue on Nonlinear Optimization of Communication Systems, vol. 14, no. 8, Aug. 2006.

- [18] E. Solan and N. Vieille. Correlated equilibrium in stochastic games. Games and Economic Behavior, vol. 38, pp. 362-399, 2002.

- [19] J. F. Nash. Equilibrium points in -person games. Proceedings of the National Academy of Sciences of the United States of America, vol. 36, pp. 48-49, 1950.

- [20] M. J. Neely. Stability and probability 1 convergence for queueing networks via Lyapunov optimization. Journal of Applied Mathematics, vol. 2012, doi:10.1155/2012/831909, 2012.