red

Bayesian Optimization With Censored Response Data

Abstract

Bayesian optimization (BO) aims to minimize a given blackbox function using a model that is updated whenever new evidence about the function becomes available. Here, we address the problem of BO under partially right-censored response data, where in some evaluations we only obtain a lower bound on the function value. The ability to handle such response data allows us to adaptively censor costly function evaluations in minimization problems where the cost of a function evaluation corresponds to the function value. One important application giving rise to such censored data is the runtime-minimizing variant of the algorithm configuration problem: finding settings of a given parametric algorithm that minimize the runtime required for solving problem instances from a given distribution. We demonstrate that terminating slow algorithm runs prematurely and handling the resulting right-censored observations can substantially improve the state of the art in model-based algorithm configuration.

1 Introduction

Right-censored data—data for which only a lower bound on a measurement is available—occurs in several applications. For example, if a patient drops out of a clinical study (for a reason other than death), we know only a lower bound on her survival time. In some cases, one can actively decide to censor certain data points in order to save time or other resources; for example, if a drug variant is unsuccessful in curing a disease by the time a known drug is successful, one may decide to stop the trial with and instead invest the resources to test a new variant . Here, we describe how to integrate such censored observations into Bayesian optimization (BO). BO aims to find the minimum of a blackbox function —a potentially noisy function that is not available in closed form, but can be queried at arbitrary input values. BO proceeds in two phases: (1) constructing a model of using the observed function values; and (2) using the model to select the input for the next query.

We extend the standard formulation of blackbox function minimization to include a cost function that measures the cost of obtaining the function value for a given input. The budget for minimizing is now given as a limit on the cumulative cost of function evaluations (in contrast to the traditional number of allowed function evaluations). We call the resulting blackbox function minimization variant cost-varying. In this paper, we focus on problems with the following cost monotonicity property.

Definition 1

A cost-varying blackbox function minimization problem is cost monotonic if

For example, a function may describe how quickly different drug variants cure a disease, or how quickly plants reach a desired size given different fertilizer variants; in these examples, it takes exactly time to determine , i.e., . When terminating the function evaluation prematurely after a censoring threshold , the cost is only , but the resulting censored data point is also less informative: we only obtain a lower bound . Cost monotonicity also applies to minimization objectives other than time, such as energy consumption, communication overhead, or strictly monotonic functions of these.

The application domain motivating our research is the following algorithm configuration (AC) problem. We are given a parameterized algorithm , a distribution of problem instances , and a performance metric capturing ’s performance with parameter settings on instances . Let denote the expected performance of with setting (where the expectation is over instances drawn from ; in the case of randomized algorithms, it would also be over random seeds). If we are given only samples from distribution , then simplifies to . The problem is then to find a parameter setting of that solves . Automated procedures (i.e., algorithms) for solving AC have recently led to substantial improvements of the state of the art in a wide variety of problem domains, including SAT-based formal verification [11], mixed integer programming [12], and automated planning [7]. Traditional AC methods are based on heuristic search [19, 8, 1, 16, 2] and racing algorithms [3, 4], but recently the BO method SMAC [14] has been shown to compare favourably to these approaches.

A particularly important performance metric in the AC domain is algorithm A’s runtime for solving problem instance given settings . Minimizing this metric within a given time budget is a cost monotonic problem (since it yields ). Algorithm runs can also be terminated prematurely, yielding a cheaper lower bound on . As shown in the following, by exploiting this cost monotonicity, we can substantially improve the state of the art in model-based algorithm configuration.

2 Regression Models Under Censoring

Our training data is , where is a parameter setting, is an observation, and is a censoring indicator such that if and if . Various types of models can handle such censored data. In Gaussian processes (GPs)—the most widely used tool for Bayesian optimization—one could use approximations to handle the resulting non-Gaussian observation likelihoods; for example, [6] described a Laplace approximation for handling right-censored data. Here, we use random forests (RFs) [5], which have been shown to yield better predictive performance for the high-dimensional and predominantly discrete inputs typical of algorithm configuration [17]. Following [14], we define the predictive distribution of a RF model for input as , where and are the empirical mean and variance of predictions of across the trees in . RFs have previously been adapted to handle censored data [21, 10], but the classical methods yield non-parametric Kaplan-Meier estimators that do not lend themselves to Bayesian optimization since they are undefined beyond the largest uncensored data point.

We introduce a simple EM-type algorithm for filling in censored values.111This document is an extended version of our workshop paper that originally introduced this algorithm [13]. We denote the probability density function and the cumulative density function of a standard Normal distribution by and , respectively. Let be an input for which we observed a censored value . Given a Gaussian predictive distribution of , the truncated Gaussian distribution is defined by the probability density function

| (3) |

Our algorithm is inspired by the EM algorithm of Schmee and Hahn [20]. Applied to an RF model as its base model, that algorithm would first fit an initial RF using only uncensored data and then iterate between the following steps:

-

E.

For each tree in the RF and each s.t. : ;

-

M.

Refit the RF using as the basis for tree .

While the mean of is the best single value to impute, this algorithm yields overly confident predictions. To preserve our uncertainty about the true value of , we change Step 1 to:

-

E.

For each tree in the RF and each s.t. : .

More precisely, we draw all required samples for a censored data point at once, using stratifying sampling. When constructing the random forest, we take bootstrap samples of all data points for each tree, regardless of their censoring status; this leads to zero, one, or multiple copies of each censored data point per tree. We keep track of the combined number of copies for each data point and obtain these samples as quantiles of the cumulative distribution. Algorithm 1 summarizes this process in pseudocode. Lines 1–1 assign a bootstrap sample of the original data to each tree, and line 1 initializes the random forest on the uncensored data. Then, the algorithm iterates imputing values for the censored data points (lines 1–1) and re-fitting trees on both uncensored data points and the individual trees’ imputed values for censored data points (lines 1–1).222For software engineering reasons, our actual implementation fits the first random forest using a bootstrap sample different from the one used for the remainder of the iterations. As an implementation detail, to avoid potentially large outlying predictions above a known maximal runtime (in our experiments, seconds), we ensure that the mean imputed value does not exceed .333In Schmee & Hahn’s algorithm, this simply means imputing . In our sampling version, it amounts to keeping track of the mean of the imputed samples for each censored data point and subtracting from each sample for data point if .

Compared to imputing the mean as in a straight-forward adaptation of Schmee & Hahn’s algorithm, our modified version takes our prior uncertainty into account when computing the posterior predictive distribution, thereby avoiding overly confident predictions. We also emulate drawing joint samples for the censored data points (with all imputed values being similarly lucky/unlucky) in order to preserve the predictive uncertainty in the mean of multiple censored values. In lines 1–1 of Algorithm 1, this is done by assigning the lower quantiles of the predictive distribution to trees with lower index (to yield consistent underpredictions) and higher quantiles to the ones with higher index (to yield consistent overpredictions). Using this mechanism preserves our predictive uncertainty even in the mean of imputed samples, while drawing each sample independently would reduce this uncertainty by a factor of .

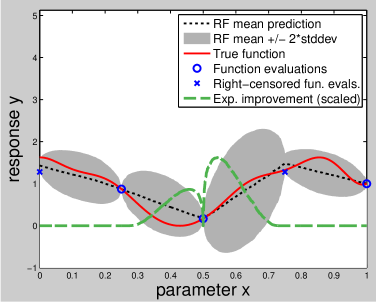

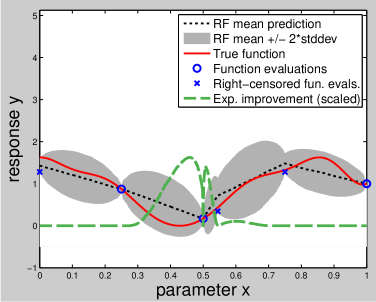

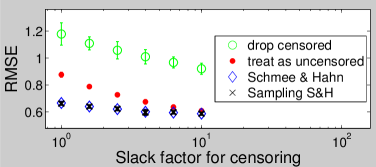

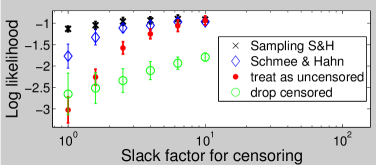

Predictive distributions from our sampling-based EM algorithm are visualized for a simple function in Figure 1(a); note that the predictive variance at censored data points does not collapse to zero (as it would when using Schmee & Hahn’s original procedure with a random forest model).444Note that our RF’s predictive mean converges to a linear interpolation between data points with a sufficient number of trees, and that its variance grows with the distance from observed data points. (Like the classical approach for building regression trees, at each node we select an interval from which to select a split point to greedily minimize the weighted within-node variance of the node’s children. Instead of selecting this point as , we sample it uniformly at random from . This yields linear interpolation in the limit.) As shown in Figure 2, both Schmee & Hahn’s procedure and our sampling version yield substantially lower error than either dropping censored data points or treating them as uncensored. By preserving predictive uncertainty for the censored data points, our sampling method yields the highest log likelihoods.

3 Bayesian Optimization Under Censoring

In order to minimize a blackbox function , Bayesian optimization iteratively evaluates at some query point, updates a model of , and uses that model to decide which query point to evaluate next. One standard method for trading off exploration and exploitation in Bayesian optimization is to select the next query point to maximize the expected positive improvement over the minimal function value seen so far. Let and denote the mean and variance predicted by our model for input , and define . Then, one can obtain (see, e.g., [18]) the closed-form expression

| (4) |

where and denote the probability density function and cumulative distribution function of a standard normal distribution, respectively. As usual, we maximize this criterion across the input space to select the next setting to evaluate. This Bayesian optimization process does not change when we allow some evaluations of to be right-censored; the only difference is that our model has to be able to handle such censored data. Algorithm 2 gives the pseudocode of Bayesian optimization for this case of partial right censoring.

In the variant of this problem we face, we can also pick the censoring threshold for a each query point, up to which we are willing to evaluate the function, and above which we will accept a censored sample. There is no obvious best choice of : increasing it yields more informative but also more costly data. Here, we heuristically set to a multiplicative factor (the “slack factor”) times .555Our approach here is inspired by the “adaptive capping” method used by the algorithm configuration procedure ParamILS [16]; indeed, we recover that method when the slack factor is 1. We allow for slack factors greater than 1 because they can improve model fits, albeit at the expense of more costly data acquisition. Figure 1 visualizes the first two steps of the resulting Bayesian optimization procedure for the minimization of a given blackbox function, starting from an initial Latin hypercube design.

We now return to algorithm configuration (AC), the problem motivating our research. AC differs from standard problems attacked by Bayesian Optimization (BO) in some important ways: most importantly, categorical input dimensions are common (due to algorithm parameters with finite, non-ordered domains); inputs tend to be high dimensional; the optimization objective is a marginal over instances (in the BO literature, this particular problem has, e.g., been addressed by [22, 9]); the objective varies exponentially (good settings perform orders of magnitude better than poor ones), and the overhead of fitting and using models has to be taken into account since it is part of the time budget available for AC. The model-based AC method SMAC addresses these issues, including several modifications of standard BO methods to achieve state-of-the-art performance for AC (for details, see [15, 14]). Here, we improve SMAC further by setting censoring thresholds as described above and building models under the resulting censored data as described in Section 2.

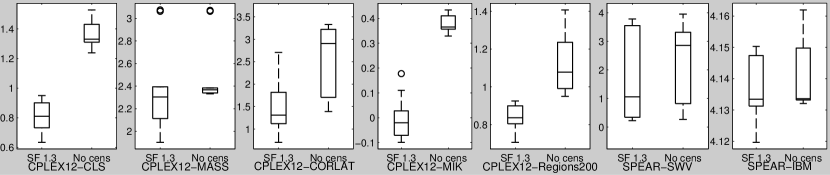

We compared our modified version of SMAC to the original version on a range of challenging real-world configuration scenarios: optimizing the 76 parameters of the commercial mixed integer solver CPLEX on five different sets of problem instances (obtained from [12]), and the 26 parameters of the industrial SAT solver SPEAR on two sets of problem instances from formal verification (obtained from [11]). Each SMAC run was allowed 2 days and the maximum censoring time for each CPLEX/SPEAR run was 10 000 seconds. Algorithm configuration scenarios with such high maximum runtimes have been identified as a challenge for SMAC [14], and we demonstrate here that our adaptive censoring technique substantially improved its performance for these scenarios.

| Scenario | Unit | Median of mean runtimes on test set | |||||

|---|---|---|---|---|---|---|---|

| SF 1 | SF 1.1 | SF 1.3 | SF 1.5 | SF 2 | No censoring | ||

| CPLEX12-CLS | [] | ||||||

| CPLEX12-MASS | [] | ||||||

| CPLEX12-CORLAT | [] | ||||||

| CPLEX12-MIK | [] | ||||||

| CPLEX12-Regions200 | [] | ||||||

| SPEAR-SWV | [] | ||||||

| SPEAR-IBM | [] | ||||||

We performed 10 configuration runs for each of 7 problem domains and each of 6 versions of SMAC (no censoring, and censoring with 5 different slack factors). At the end of each configuration run, we recorded SMAC’s best found configuration and computed the run’s test performance as that configuration’s mean runtime on a test set of instances disjoint from the training set, but sampled from the same distribution.

Figure 3 and Table 1 show that our modified version of SMAC with censoring substantially outperformed the original SMAC version without capping. Our modified version gave better results in all 7 cases (with statistical significance achieved in 4 of these), with the improvements in median test performance reaching up to a factor of 126 (SPEAR-SWV).

4 Conclusion

We have demonstrated that censored data can be integrated effectively into Bayesian optimization (BO). We proposed a simple EM algorithm for handling censored data in random forests and adaptively selected censoring thresholds for new data points at small multiples above the best seen function values. In an application to the problem of algorithm configuration, we achieved substantial speedups of the state-of-the-art procedure SMAC. In future work, we would like to apply censoring in BO with Gaussian processes, actively select the censoring threshold to yield the most information per time spent, and evaluate the effectiveness of BO with censoring in further domains.

Acknowledgments

We would like to thank our summer coop student Jonathan Shen for many useful discussions and for assistance in cleaning up the Matlab source code of SMAC used for our experiments. Thanks also to Steve Ramage for porting SMAC to Java afterwards and improving its usability, as well as for feedback on an earlier version of this report.

References

- [1] B. Adenso-Diaz and M. Laguna. Fine-tuning of algorithms using fractional experimental design and local search. Operations Research, 54(1):99–114, Jan–Feb 2006.

- [2] C. Ansotegui, M. Sellmann, and K. Tierney. A gender-based genetic algorithm for the automatic configuration of solvers. In Proc. of CP-09, pages 142–157, 2009.

- [3] M. Birattari, T. Stützle, L. Paquete, and K. Varrentrapp. A racing algorithm for configuring metaheuristics. In Proc. of GECCO-02, pages 11–18, 2002.

- [4] M. Birattari, Z. Yuan, P. Balaprakash, and T. Stützle. F-race and iterated F-race: An overview. In Empirical Methods for the Analysis of Optimization Algorithms, pages 310–336. Springer, Berlin, Germany, 2010.

- [5] L. Breiman. Random forests. Machine Learning, 45(1):5–32, 2001.

- [6] E. Ertin. Gaussian process models for censored sensor readings. In Proceedings of the IEEE Statistical Signal Processing Workshop 2007 (SSP’07), pages 665–669, 2007.

- [7] C. Fawcett, M. Helmert, H. H. Hoos, E. Karpas, G. Röger, and J. Seipp. FD-Autotune: Domain-specific configuration using fast-downward. In Proc. of the ICAPS workshop on planning and learning (PAL 2011), pages 13–20, 2011.

- [8] J. Gratch and G. Dejong. Composer: A probabilistic solution to the utility problem in speed-up learning. In Proc. of AAAI-92, pages 235–240, 1992.

- [9] P. Groot, A. Birlutiu, and T. Heskes. Bayesian Monte Carlo for the global optimization of expensive functions. In Proc. of ECAI 2010, pages 249–254, 2010.

- [10] T. Hothorn, B. Lausen, A. Benner, and M Radespiel-Tröger. Bagging survival trees. Statistics in Medicine, 23:77 91, 2004.

- [11] F. Hutter, D. Babić, H. H. Hoos, and A. J. Hu. Boosting verification by automatic tuning of decision procedures. In Proc. of FMCAD’07, pages 27–34, Washington, DC, USA, 2007.

- [12] F. Hutter, H. H. Hoos, and K. Leyton-Brown. Automated configuration of mixed integer programming solvers. In Proc. of CPAIOR-10, pages 186 –202, 2010.

- [13] F. Hutter, H. H. Hoos, and K. Leyton-Brown. Bayesian optimization with censored response data. In NIPS workshop on Bayesian Optimization, Sequential Experimental Design, and Bandits, 2011. Published online.

- [14] F. Hutter, H. H. Hoos, and K. Leyton-Brown. Sequential model-based optimization for general algorithm configuration. In Proc. of LION-5, pages 507–523, 2011.

- [15] F. Hutter, H. H. Hoos, K. Leyton-Brown, and K. P. Murphy. Time-bounded sequential parameter optimization. In Proc. of LION-4, 2010.

- [16] F. Hutter, H. H. Hoos, K. Leyton-Brown, and T. Stützle. ParamILS: An automatic algorithm configuration framework. Journal of Artificial Intelligence Research, 36:267–306, October 2009.

- [17] F. Hutter, L. Xu, H. H. Hoos, and K. Leyton-Brown. Algorithm runtime prediction: Methods & evaluation. Artificial Intelligence, 2012. To appear.

- [18] D. R. Jones, M. Schonlau, and W. J. Welch. Efficient global optimization of expensive black box functions. Journal of Global Optimization, 13:455–492, 1998.

- [19] S. Minton, M. D. Johnston, A. B. Philips, and P. Laird. Minimizing conflicts: A heuristic repair method for constraint-satisfaction and scheduling problems. AIJ, 58(1):161–205, 1992.

- [20] J. Schmee and G. J. Hahn. A simple method for regression analysis with censored data. Technometrics, 21(4):417–432, 1979.

- [21] M. R. Segal. Regression trees for censored data. Biometrics, 44(1):35–47, March 1988.

- [22] B. J. Williams, T. J. Santner, and W. I. Notz. Sequential design of computer experiments to minimize integrated response functions. Statistica Sinica, 10:1133–1152, 2000.