Differentiablity of excessive functions of one-dimensional diffusions and the principle of smooth fit

Abstract

The principle of smooth fit is probably the most used tool to find solutions to optimal stopping problems of one-dimensional diffusions. It is important, e.g., in financial mathematical applications to understand in which kind of models and problems smooth fit can fail. In this paper we connect - in case of one-dimensional diffusions - the validity of smooth fit and the differentiability of excessive functions. The basic tool to derive the results is the representation theory of excessive functions; in particular, the Riesz and Martin representations. It is seen that the differentiability may not hold in case the speed measure of the diffusion or the representing measure of the excessive function has atoms.

As an example, we study optimal stopping of sticky Brownian motion. It is known that the validity of the smooth fit in this case depends on the value of the discounting parameter (when the other parameters are fixed). We decompose the size of the jump in the derivative of the value function into two factors. The first one is due to the atom of the representing measure and the second one due to the atom of the speed measure.

Dedicated to the memory of a dear friend and colleague

Professor Esko Valkeila

(1951-2012)

Key words: Riesz representation, Martin representation,

Green function, optimal stopping, smooth

fit, sticky Brownian motion.

2010 mathematics subject classification: primary 60J60, 60G40, secondary 31C05.

1 Introduction

Let be a one-dimensional diffusion process in the sense of Itô and McKean [15] living on an interval , i.e., is a time-homogeneous strong Markov process with continuous sample paths. As usual, the notations and are used for the probability measure and the expectation operator, respectively, associated with when initiated from . The life time of is defined as and we set for , where is a fictitious state – the so called cemetery state. Recall that a measurable function is called -excessive, if for all the following two conditions hold:

| (1) | |||

| (2) |

where, by convention, An alternative and equivalent definition is obtained by replacing (1) and (2) by

| (3) | |||

| (4) |

We refer to Dynkin [11] Vol. II for results on excessive functions in general and in particular for one-dimensional diffusions. For excessive functions in the framework of the potential theory of Markov processes, see Blumenthal and Getoor [2] and Chung and Walsh [5]. Excessive functions being descendants of superharmonic functions have, hence, deep roots in the classical potential theory and constitute also fundamental concept in the theory of Markov processes.

Our main motivation for the present study comes, however, from the theory of optimal stopping where excessive functions play a crucial role. Indeed, given a continuous non-negative (reward) function the optimal stopping problem with the underlying process is to find a (value) function and an (optimal) stopping time such that

| (5) |

where denotes the set of all stopping times with respect to the filtration generated by The fundamental result due to Snell and Dynkin (see Shiryayev [28] and Peskir and Shiryayev [24] for details and references), is that is the smallest -excessive function dominating and an optimal stopping time is given by

where is the so called stopping region. Therefore, a good knowledge of excessive functions is a key to a deeper understanding of optimal stopping.

Although our focus is on applications in optimal stopping we wish to point out that excessive functions can also be used, e.g., to condition and/or to kill a process in some particular desirable way. Such conditionings of the underlying process are called excessive transforms or Doob’s -transforms due to Doob’s pioneering work [9]. We refer also to McKean [18], Dynkin [12], and Meyer et al. [19] for early seminal papers. The theory of -transforms in a general setting is discussed in Chung and Walsh [5] Chapter 11. Moreover, a fairly recent problem arising from financial mathematics is to construct for a given process a martingale having the same distribution as at a fixed time or at a random time, see, e.g., Cox et al. [6], Hirsch et al [14], Ekström et al. [13] and Noble [21] and references therein. In particular, Klimmek [16] exploits explicitly -transforms to find the solution of the problem for a random (exponential) time.

These and other applications in mind – and also per se – we offer in this paper firstly a discussion on continuity and differentiablity properties of excessive functions of one-dimensional diffusions and secondly applications to optimal stopping with an example. Our approach utilizes the Riesz and Martin representations which are valid in their strongest and most explicit forms for one-dimensional regular diffusions.

In the next section we give the Riesz and Martin representations with needed prerequisities and also present some examples. An immediate implication of the Riesz representation is then the continuity of excessive functions, see Proposition 2.8. The continuity is implicitly stated already in Salminen [26]. In Dayanik and Karatzas [8] and in Peskir and Shiryayev [24] the continuity is proved for a special class of excessive functions, that is, for value functions in optimal stopping problems. Their proofs utilize the properties of the value functions and the concavity, as in Dynkin and Yuschkevitch [10]. The advantage of the present approach is that it yields the result with full generality. We also shortly list - for general interest - some other basic potential theoretical and related results for one-dimensional regular diffusions. In particular, it is seen that all additive functionals are continuous. This is also pointed out in [3] p. 28 but with a slightly different explanation.

In the third section the differentiability properties of excessive functions are investigated. The Riesz representation allows us to derive conditions for differentiablity with respect to any increasing continuous function see Theorem 3.1. This extends the result in [26] where differentiability with respect to the scale function is studied. We also represent the jump of the derivative of an excessive function as the sum of two terms: the first one is induced by the representing measure and the second one by the speed measure.

These results are then used in the fourth section to study the principle of smooth fit in optimal stopping of one-dimensional diffusions. Our contribution hereby is to demonstrate – using the results in Section 3 – that the proof of the condition for the smooth fit with respect to the scale as presented in [26] can be rewritten – changing mainly only the notation – to a proof of the condition for the smooth fit in the ordinary sense as given in Peskir [23] and Samee [27], see also [24, p. 160] (e.g. when studying the case where the scale function is not differentiable at the stopping point). We conclude by analyzing the smooth fit property in an optimal stopping problem where the underlying process is a sticky Brownian motion. It is known, see Crocce and Mordecki [7], that if the optimal stopping point is the sticky point then the smooth fit typically fails. Our results enhance the understanding of this phenomenon by giving an explicit form for the jump of the derivative of the value function in this case.

2 Riesz and Martin representations

We start with by introducing more notation and recalling some basic facts. Let and denote the left and the right, respectively, end point of which is an interval of any kind. Recall that is the state space of . The notations and are used for the speed measure and the scale function, respectively. Moreover, let denote the generalized differential operator associated with and the first hitting time of , that is,

We assume that is regular (cf. Dynkin [11] Vol. II p.121), that is,

| (6) |

in other words, no matter where starts there is a positive probability to hit any point in This means that a regular diffusions do not have absorbing points and exit points and entrance points are not included in Moreover, a consequence of the regularity is that there does not exist non-empty polar sets (for this notion, see [2, p. 79] ).

Remark 2.1.

The above definition of regularity differs from another often used definition in which (6) is assumed to hold for all and (see, e.g., Revuz and Yor [25] p. 300). According to this latter definition we could have a regular diffusion with and and absorbing. As demonstrated below in Example 2.9 such a diffusion has discontinuous excessive functions – the case we want to exclude.

As showed in Itô and McKean [15, p. 124] the Laplace transform of can be expressed for as

where and are continuous, positive, increasing and decreasing, respectively, solutions of the generalized differential equation

| (7) |

Imposing appropriate boundary conditions determine and uniquely up to a multiplicative constant. The Wronskian - a constant - is defined as

where the superscripts + and - denote the right and left derivatives with respect to the scale function, i.e., for or

cf. (19) and (20) below and recall that the scale function of a diffusion is continuous. It is well-known (see [15, p. 150] ) that

| (8) |

serves as a resolvent kernel (also called the Green function) of i.e., for any Borel subset of

Using Theorem 12.4 in Dynkin [11] it is fairly straightforward to check that for every fixed the function is -excessive (see [26, p. 89] ). Since is symmetric it follows that is self-dual with respect to the speed measure, that is

| (9) |

where

with and bounded Borel measurable functions satisfying appropriate integrability condtions. For the concept of duality and related topics, see Kunita and Watanabe [17], Blumenthal and Getoor [2] and Chung and Walsh [5]. We wish to apply the Riesz representation theorem, see [2, p. 272], and remark that the assumptions for its validity as presented in [2] Chapter VI (see also [17, Theorem 2 p. 505]) are satisfied. An important assumption is that has a dual process which is standard in the sense of the definition in ibid. p. 45. Clearly, is standard and since is self dual the needed assumption is fulfilled. Notice also that (2.1) and (2.2) in [2, p. 265-266] hold.

Theorem 2.2.

(The Riesz representation) Let and an -excessive function of the regular one-dimensional diffusion . It is assumed that is locally integrable with respect to Then there exist an -harmonic function and a Radon measure on such that can be represented uniquely as

| (10) |

Remark 2.3.

(i) The Riesz representation holds also for when is transient. The Green function when has a similar structure as in case but now the corresponding functions and express the hitting probabilities instead of the Laplace transforms of the hitting distributions. In Section 3 we discuss shortly the special case in which the diffusion is not killed inside the state space (ii) The assumption on the local integrability is superfluous in case of one-dimensional diffusions. Indeed, assuming that the -excessive function choose a point such that From (3) we have

| (11) |

The local integrability of follows now easily from the explicit form of and the continuity of and . (iii) The -harmonicity of means that for all compact subset of it holds

| (12) |

where

The Riesz representation does not give much information on the harmonic function associated with a given excessive function. However, in the Martin boundary theory an integral representation is derived also for the harmonic functions. We refer to [17] and [5] for the general theory of Martin boundaries for Markov processes. In the next theorem we state the Martin representation for one-dimensional regular diffusions and, moreover, present the explicit form of the representing measure extracted from [26]. We refer also to [1] and [4] for applications of the Martin boundary theory in optimal stopping.

Theorem 2.4.

(The Martin representation) Let be an -excessive function of the one-dimensional diffusion and a point such that Then can be represented uniquely as

| (13) |

where is a probability measure on characterized via

| (14) | ||||

| (15) |

Conversely, given a probability measure on and then the right hand side of (13) when putting defines an -excessive function.

Remark 2.5.

The expression on the right hand side of (13) is well defined since and are positive on Notice that the probability measure is defined on the closure of also in case and/or In fact, is the so called Martin compactification of

Combining (13) with (10) yields a characterization of the -excessive functions in the Riesz representation. This together with other relationships between the two representations are discussed in the next

Corollary 2.6.

Let and be as in Theorem 2.2. Then there exist and such that The Riesz and the Martin representing measures of are connected via the identity

| (16) |

where is a Borel subset of Moreover, has the unique representation

| (17) |

where

with and

Next example highlights the difference of the Riesz and Martin representations via the fact that and/or could be potentials, that is, not -harmonic.

Example 2.7.

Let be a Brownian motion reflected at 0 and killed at 1. Hence, and it is readily checked that we may take

Notice that and which, in fact, are the appropriate boundary conditions to characterize and respectively. For this process, is -harmonic but is not. Standard computations show that both and satisfy the -harmonicity condition (12) for intervals of the form However, when the condition fails for Indeed, putting we have

Consequently, the Riesz representation of does not have the - harmonic part and, hence,

It follows by the uniqueness of the representing measure that is a multiple of the Dirac measure at 0.

Next we prove the continuity of excessive functions which is an important stepping stone to the differentiability studied in Section 3.

Proposition 2.8.

For a one-dimensional regular diffusion all -excessive functions are continuous.

Proof.

Let be an -excessive function. Substituting the explicit form of the Green kernel in the representation (17) yields

from which evoking the continuity of and it easily follows that

∎

Example 2.9.

To stress the importance of the regularity as defined in (6) we give an example showing that if an end point of I is absorbing then there exist discontinuous excessive functions. Let denote a Brownian motion on absorbed at 0 and consider the function

Since for all we have for

and, for ,

Clearly, also (2) holds. Consequently, is a discontinuous excessive function.

We conclude this subsection by pointing out some important properties of one-dimensional diffusions which can be deduced from the potential theoretical generalities using the explicit form of the Green kernel and the continuity of the excessive functions: () Firstly, since is self dual and for all the function is bounded and continuous it follows from (4.11) p. 290 in [2] that every point in is regular, i.e.,

| (18) |

where

Consequently, by ibid. (3.13) p. 216, posseses at every point a local time () Secondly, again due to the self duality together with the continuity of the sample paths, it holds that all additive functionals of are continuous, see ibid. p. 289. In particular, is a.s. continuous. () Thirdly, recall that an excessive function is called regular for if is continuous on (see ibid. p. 287-288). Hence, from Proposition 2.8 it follows via the continuity of the sample paths that all (finite) excessive functions for are regular.

3 Differentiability

For an increasing continuous function and an arbitrary -excessive function we introduce the one sided derivatives of with respect to :

| (19) | ||||

| (20) |

for every for which the limits on the right hand sides exist and are finite. We say that is -differentiable at if

Our basic result gives conditions for the -differentiability of an arbitrary -excessive function . Recall from the Riesz representation that there exists a Radon measure such that (10) holds.

Theorem 3.1.

Let and be as above and assume that functions and are for -differentiable at a point . Then the left and the right -derivative of exist at and satisfy

| (21) |

Moreover, is -differentiable at if and only if .

Proof.

Since functions and are assumed to be -differentiable at we may, without loss of generality, take in (17), and, hence, has the representation

Since and are increasing and decreasing, respectively, it holds

Evoking that is a measure and and are assumed to be -differentiable at we obtain

Consequently,

It follows that has the right -derivative given by

| (23) |

Analogous calculations yield for the left -derivative

| (24) |

Hence, we have

| (25) | ||||

and this completes the proof. ∎

Remark 3.2.

Choosing equal to the scale function yields (3.7) Corollary in [26]. In fact, the idea of the proof is the same as in [26]. However, therein the proof is based explicitly on the Martin representation. Notice that taking in (3) yields

| (26) |

which differs from the formula in the proof of (3.7) Corollary in [26] due to the different normalizations of the representing measure in the Riesz and Martin representations. Notice also that taking gives, of course, a condition for the differentiablity in the usual sense.

We study next the differentiablity of 0-excessive functions. Hence, it is assumed that is transient and, moreover, that the killing measure is identically zero. Then with probability 1. As stated in Remark 1 after Theorem 2.2 the Riesz representation holds also for the 0-excessive functions. In fact, in [2] only the case with is discussed in detail. The differentiablity of 0-excessive functions can be analyzed similarly as was done in Theorem 3.1 for -excessive functions. Therefore, we formulate the result as a corollary. For simplicity, it is assumed that the boundary condition at a regular boundary point is killing. Then the Green function can be written as (see [15, p. 130], and [3, p. 20])

| (27) |

Corollary 3.3.

Let be a transient diffusion as introduced above and a 0-excessive function of . Assume that the scale function of is differentiable at a given point Then has the left and the right derivative at and it holds

| (28) |

Moreover, is differentiable at if and only if .

Proof.

Consider formula (17) in case and Since and are assumed to be killing boundaries we have

Consequently, we may assume, without loss of generality, that in the representation of in (17) Hence,

| (29) |

The cases and can be handled similarly; we leave the details to the reader. Formula (3) corresponds (22) and the proof can be continued similarly as was done after (22) but taking ∎

The basic assumption in Theorem 3.1 is that and are -differentiable. In case this assumption typically fails at points which are atoms of the speed measure, i.e., (so called sticky points), and at such points, see [15, p. 129], [25, p. 308] (notice that there is a misprint in the formula in the middle of page 309; the term on the right hand side should be without factor 2) and [3, p.18],

| (30) |

and

| (31) |

Next theorem extends formula (26) for diffusions having sticky points.

Theorem 3.4.

Let be an -excessive function of the diffusion Then it holds

| (32) |

where denotes the right (left) derivative with respect to the scale function.

Proof.

Due to (30) and (31) we may assume without loss of generality that has the Riesz representation

| (33) |

By similar calculations as in the proof of Theorem 3.1 taking therein we obtain (cf. (23) and (24))

| (34) |

and

| (35) |

Subtracting (34) from(35) yields

| (36) | ||||

Using (30), (31) and noticing that

Identity (3) can be written as follows

by (33), and the proof is complete. ∎

4 Application to optimal stopping

4.1 Smooth fit

Probably the most used method to solve optimal stopping problems (with infinite horizon) for one-dimensional diffusions is based on the principle of smooth fit. This principle says that the value function as defined in (5) meets the reward function smoothly at the boundary points of the stopping region i.e., at the boundary points in case exists. The idea of the method is to guess the form of and to find its boundary points using the continuity and the differentiablity of the proposed value function. After this, a verification theorem (see, e.g., Øksendal [22, p. 215 Theorem 10.4.1]) is needed to show that the proposed value is indeed the right one.

In [26] a criterion for the validity of the smooth fit (with respect to the scale function) is derived. This criterion can extracted from Theorem 4.1 below by choosing equal to the scale function. A condition for the smooth fit with respect to “usual” differentiation is obtained by taking to be the identity mapping. The criterion holds also for (transient case with general killing measure). We formulate the result for a left boundary point of obviously there is a similar result for a right boundary point.

Theorem 4.1.

Let be a left boundary point of i.e., and for some positive and Let be a continuous and increasing function and assume that the reward function and the functions and are -differentiable at Then the value function in (5) is -differentiable at and the smooth fit with respect to holds:

| (37) |

Proof.

Specializing to transient diffusions without killing inside the state space and applying Corollary 3.3 yields the following result which is the contents of Theorem 2.3 in [23], see also [24] section 9.1.

Corollary 4.2.

Let be a transient diffusion as introduced in Corollary 3.3. Let be a point such that If the reward function and the scale function are differentiable at then the smooth fit holds at :

| (38) |

4.2 Example: Sticky Brownian motion

In this section we study an optimal stopping problem when the underlying process is a sticky Brownian motion with drift . We let denote this process and, by definition, we take it to be sticky at 0. The speed measure and the scale function of are given for by

respectively, where denotes the Dirac measure at 0 and the stickyness parameter is positive. In case, put i.e., is in natural scale. The infinitesimal operator associated with (see Ito and Mckean [15, p. 111-112]) is given for by

and defined by continuity at 0, that is, The domain is taken to be

Notice that in our case and, hence, for instance,

To find the fundamental solutions and associated with recall that the unique positive (up to a multiplicative constants) increasing and decreasing solutions the ODE

are given by

respectively, where Consequently, we should find constants and such that

and

are continuous (at 0) and, moreover, satisfy the condition (cf. (30) and (31))

| (39) |

Straightforward calculations show that

| (40) |

and

| (41) |

where We remark that these expressions coincide in case with the formulas in [3, p. 123].

We study now the OSP as given in (5) with

| (42) |

where is the sticky Brownian motion introduced above.

Proposition 4.3.

In case the problem is equivalent with the corresponding problem for ordinary Brownian motion with drift. The smooth fit holds and the optimal stopping time is

Proof.

The value function of the problem is the smallest 0-excessive majorant of the reward function. Recall that the Green function in case and there is no killing inside is determined by linear combinations of the scale function (see (27) for a example). Since the scale functions of and the ordinary Brownian motion with drift are equal it follows from the Martin representation that the classes of -excessive functions for these processes are identical. Consequently, in the considered OSPs the value functions and the optimal stopping times are equal. The solution of the latter problem was found already by Taylor [29], see also, e.g., [20], [28, p. 124-5], and [26], and, herefrom, it is clearly seen that the smooth fit holds. ∎

Remark 4.4.

Another explanation/proof of Proposition 4.3 is that making a state sticky in BM does not change the probabilities of hitting points. Since in case it does not "cost to wait" the problems with or without the sticky point have the same solutions.

We specialize now to case It is proved in [7] for that the smooth fit does not hold when the discounting parameter is in the interval where and We wish to study this phenomenon via the representing measure of the value function. Consider the following functions defined for

and

Notice that these functions are multiples of expressions in (14) and (15), of the Martin representing measure if on the RHS we use instead of It is straightforward to check the following properties of and :

-

(s1) is decreasing for

-

(s2)

-

(s3)

-

(t1) is increasing for

-

(t2)

-

(t3)

Let denote the unique solution (if it exists) of the equation for ; in case there is no solution we put Let and define

and

| (43) |

where From the properties of and it is seen that these definitions induce a Borel measure on Using the definition of the Wronskian we obtain

Therefore, setting makes a probability measure. Notice also that

and

The probability measure yields via the representation formula (13) the -excessive function

| (47) |

In this context we call the Martin representing measure of Clearly, the function does not depend on We conclude with the following

Proposition 4.5.

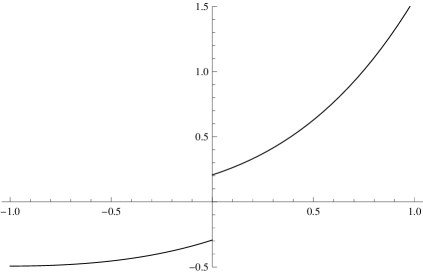

The function is the value function of OSP (42), i.e., is the smallest -excessive majorant of The optimal stopping time is In particular, for with and it holds that

| (48) |

and the Riesz representing measure has an atom at 0:

| (49) |

In case, the smooth fit holds and If the smooth fit fails and

Proof.

By the construction, the function is -excessive. To prove that is a majorant of is straightforward and elementary from the explicit expressions. For a more sophisticated proof, notice that on the function is increasing since on (and for if ). Consequently, for

Assume next that there exists an -excessive majorant smaller than . Consider first the case where the equation has a unique root on We let, as above, denote this root. Since is assumed to be an -excessive majorant of smaller than it holds that for Consequently, the Martin representing measures of and are equal on and given by (14) and (15). However, because the representing measure of does not put mass on Hence, the representing measures of and are equal and so, by the uniqueness of the Martin representation, In case does not have a zero on the Martin representing measure of has an atom at given by

| (50) |

where is a non-negative constant given explicitly in (53). Since the representing measures of and are equal on and it is assumed that we must have

and

Consider now the Martin representations of and for

and

respectively. We show that, in fact, for all contradicting the assumption that is smaller than Indeed, for

Using that and it is seen that for

| (51) |

is equivalent with

Since is decreasing (51) holds if

| (52) |

Observing that

it is seen that (52) is true if for all

and to check this is elementary from (40) and (41) or follows directly from the monotonicity. This completes the proof that is the smallest -excessive majorant of .

References

- [1] L. H. R. Alvarez and P. Salminen. Optimal stopping of linear diffusions: A synthesis (under preperation).

- [2] R.M. Blumenthal and R.K. Getoor. Markov Processes and Potential Theory. Academic Press, New York, London, 1968.

- [3] A.N. Borodin and P. Salminen. Handbook of Brownian Motion – Facts and Formulae, 2nd edition. Birkhäuser, Basel, Boston, Berlin, 2002.

- [4] S. Christensen and A. Irle. A harmonic function technique for the optimal stopping of diffusions. Stochastics, 83(4-6):347–363, 2011.

- [5] K.L. Chung and J.B. Walsh. Markov processes, Brownian motion, and time symmetry, 2nd edition. Springer-Verlag, Berlin, Heidelberg, New York, 2005.

- [6] A.M.G. Cox, D. Hobson, and J. Oblój. Time-homogeneous diffusions with a given marginal at a random time. ESAIM Probab. Stat., 15:S11–S24, 2011.

- [7] F. Crocce and E. Mordecki. Explicit solutions of one-sided optimal stopping problems for one-dimensional diffusions. Stochastics An International Journal of Probability and Stochastic Processes, 86(3):491–509, 2014.

- [8] S. Dayanik and I. Karatzas. On the optimal stopping problem for one-dimensional diffusions. Stochastic Process. Appl., 107(2):173–212, 2003.

- [9] J.L. Doob. Conditional Brownian motion and the boundary limits of harmonic functions. Bull. Soc. Math. France, 85:431–458, 1957.

- [10] E. B. Dynkin and A. A. Yushkevich. Markov Processes: Theory and Problems. Plenum Press, New York, 1969.

- [11] E.B. Dynkin. Markov Processes, Vol. I and II. Springer-Verlag, Berlin, Göttingen, Heidelberg, 1965.

- [12] E.B. Dynkin. The space of exits of a Markov process. Russ. Math. Surv., 24(4):89–157, 1969.

- [13] E. Ekström, D. Hobson, S. Janson, and J. Tysk. Can time homogenous diffusions produce any distribution ? Probab. Theory Relat. Fields, 155:493–520, 2013.

- [14] F. Hirsh, C. Profeta, B. Roynette, and M. Yor. Peacocks and Associated Martingales, with Explicit Constructions. Bocconi University Press; Springer-Verlag Italia, Milano, 2011.

- [15] K. Itô and H.P. McKean. Diffusion Processes and Their Sample Paths. Springer-Verlag, Berlin, Heidelberg, 1974.

- [16] M. Klimmek. The Wronskian parametrizes the class of diffusions with a given distribution at a random time. Electron. Commun. Probab., 17:50, 1–8, 2012.

- [17] H. Kunita and T. Watanabe. Markov processes and Martin boundaries I. Illinois J. Math., 9:485–526, 1965.

- [18] H. McKean. Excursions of a non-singular diffusion. Z. Wahrscheinlichkeitstheorie verw. Gebiete, 1:230–239, 1963.

- [19] P.A. Meyer, R.T. Smythe, and J.B. Walsh. Birth and death of Markov processes. In Proc. Sixth Berkeley Symposium III, pages 295–305. Univ. of California Press, 1971.

- [20] A.G. Mucci. Existence and explicit determination of optimal stopping times. Stochastic Process. Appl., 8:33–58, 1978.

- [21] J. Noble. Time homogeneous diffusions with a given marginal at a deterministic time. Stochastic Process. Appl., 123:675–718, 2013.

- [22] B. Øksendal. Stochastic Differential Equations. An introduction with applications. Universitext. Springer-Verlag, Berlin, 6th edition, 2003.

- [23] G. Peskir. Principle of smooth fit and diffusions with angles. Stochastics, 79(3-4):293–302, 2007.

- [24] G. Peskir and A.N. Shiryaev. Optimal Stopping and Free-Boundary Problems. Lectures in Mathematics ETH Zürich. Birkhäuser Verlag, Basel, 2006.

- [25] D. Revuz and M. Yor. Continuous Martingales and Brownian Motion. Springer-Verlag, Berlin, third edition, 1999.

- [26] P. Salminen. Optimal stopping of one-dimensional diffusions. Math. Nachr., 124:85–101, 1985.

- [27] F. Samee. On the principle of smooth fit for killed diffusions. Electron. Commun. Probab., 15:89–98, 2010.

- [28] A. N. Shiryaev. Optimal Stopping Rules. Springer-Verlag, Berlin, 1978.

- [29] H.M. Taylor. Optimal stopping in a Markov process. Ann. Math. Stat., 39:1333–1344, 1968.