A stochastic model for speculative bubbles

Abstract

This paper aims to provide a simple modelling of speculative bubbles and derive some quantitative properties of its dynamical evolution. Starting from a description of individual speculative behaviours, we build and study a second order Markov process, which after simple transformations can be viewed as a turning two-dimensional Gaussian process. Then, our main problem is to obtain some bounds for the persistence rate relative to the return time to a given price. In our main results, we prove with both spectral and probabilistic methods that this rate is almost proportional to the turning frequency of the model and provide some explicit bounds. In the continuity of this result, we build some estimators of and of the pseudo-period of the prices. At last, we end the paper by a proof of the quasi-stationary distribution of the process, as well as the existence of its persistence rate.

Keywords: Speculative bubble; Persistence rate; Gaussian Process; Diffusion Bridge; Statistics of processes.

MSC2010: Primary: 60J70, 35H10, 60G15, 35P15.

1 Introduction

The evolution of prices in markets such as real estate is a popular subject of investigation. The purpose of this paper is to propose a stochastic model which, at the same time, is simple enough to be studied mathematically and accounts for periodicity phenomena induced by speculation.

One commonly talks of financial bubble when, due to speculation of traders or owners, an asset price exceeds an asset fundamental value. These owners then expect to resell the asset at an even higher price in the future. There exist a lot of famous historical examples such as the Dutch Tulip Mania (1634-1637), the Mississippi bubble (1718-1720) or the ”Roaring ’20s that preceded the 1929” crash. We refer to [13] for a general remainder on historical bubbles. Through some more recent events, one can observe that this phenomena is certainly actual. Think for instance to the Internet bubble which bursted in March 2000 after having led astronomical heights and lost more than 75% of its value, and to the housing bubble encountered in the United States (2000-2010) or in European countries (Spain, Ireland, France …) (see [16] or [12]).

A huge litterature exists on speculative bubbles and it seems nearly impossible to quote all the related numerous previous works. We point out that our goal here is not to detail a general model flexible enough to take into account several complex economic realities. However, our approach is to propose a very simple tractable model from a mathematical point of view: the natural equilibrium price is assumed to be all along our temporal evolution, we do not consider any inflation nor credit crunch [10] and there is no regulating effect of any federal bank [3]. At last, the processes introduced in the paper will be supposed time-homogeneous.

According to Shiller [16] (see also [14]), the mechanism of creation of speculative bubbles is the following: ”If asset prices start to rise strongly, the success of some investors attracts public attention that fuels the spread of the enthusiasm for the market: (often, less sophisticated) investors enter the market and bid up prices. This ”irrational exuberance” heightens expectations of further price increases, as investors extrapolate recent price action far into the future. The markets meteoric rise is typically justified in the popular culture by some superficially plausible ”new era” theory that validates the abandonment of traditional valuation metrics. But the bubble carries the seeds of its own destruction; if prices begin to sag, pessimism can take hold, causing some investors to exit the market. Downward price motion begets expectations of further downward motion, and so on, until the bottom is eventually reached.”

In the previous citation, two phenomenas are exhibited: on the one hand, the investors have a tendency to follow the forecasting rule which consists in deciding that the price will increase if it has (strongly) increased in the past. On the other hand, the actions of the investors have certainly a self-reinforcing effect. In this paper, we assume more or less that the dynamics of the market is dictated by these two phenomenas. However, we (necessarily) assume that there is also a general mean-reverting force and there exists randomness in the decisions of the investors. Then, our model is obtained as the limit of the mean dynamics of all the investors when the number of these investors tends to infinity (see next paragraph for more details).

Let us also precise that our setting corresponds to the so-called rational bubbles under symmetric information paradigm described in [4, 18] for instance. In our framework, we are interested in the periodic pattern commonly encountered in such speculative markets, which is of primarily interest as pointed by [9]. We establish that these periodic phenomena are related to a persistence problem which is also an important field of interest from an economic point of view [4, 5]. Note that our model is also simple enough to imagine statistical inference procedures for the estimation of several key parameters. Hence, even if our work comes from a probabilistic motivation, it also opens the way of statistical procedures to test bubble formation. This last statistical point is shortly discussed in the end of our paper and seems challenging for future works (some numerical results show that the standard likelihood estimation does not seem well suited to approach the unknown parameters in such a model).

At last, it is generally empirically observed that the bubbles bursts are fasten than bubbles formations. Our model can be generalized to more complex settings where such burst’s and formation’s timing could be different using a mixture of memory weights with (see next paragraph for more details).

1.1 Modeling of speculation

Let us designate by the temporal evolution of the relative price of a commodity with respect to

another one. For instance it can be the difference between the price of the mean square meter of real estate in a particular town

and the price of the ounce of gold or the mean salary of a month of work.

Let the units be chosen

so that, in the mean over a long time period, this relative price is zero.

We assume that three mechanisms are at work for the evolution of :

- Economic reality plays the role of a restoring force, trying to draw back toward zero.

At least as a first approximation, it is natural to assume that this force is linear, whose rate will be denoted .

- Speculation is reinforcing a tendency observed for some times in the past.

We make the hypothesis that the weight of past

influences is decreasing exponentially fast in time, with rate .

The typical length the observation time window will be given by .

- Uncertainty is modeled by a Brownian motion of volatility , which is a traditional assumption for randomness

coming from a lot of small unpredictable and independent perturbations, due to the functional central limit theorem.

Putting together these three leverages, we end up with a law of evolution of described by the stochastic differential equation

| (1) |

assuming for instance that initially, . Because of the presence of the Brownian motion in the r.h.s., the trajectories of are not differentiable with respect to the time parameter . But for the purpose of a heuristic interpretation, let us pretend they are, so we can consider . Assume furthermore that the “origin” of time was chosen so that before it, was zero, namely, in the above economic interpretation, the two commodities had their prices tied up at their relative equilibrium point before time 0. This enables us to define for any . The middle term of the r.h.s. of (1) can then be rewritten as

| (2) | |||||

where is distributed as an exponential variable of parameter and where stands for the expectation with respect to (i.e. not with respect to the randomness underlying , the corresponding expectation will be denoted ). Thus has a drift taking into account its past tendencies , but very old ones are almost forgotten, due to the exponential weight. Indeed, since , tendencies older than a time of order don’t contribute much.

The equation (1) can be seen as the limit evolution of the means of (relative) prices predicted by a large number of speculative agents. Assume that each agent has his own idea of the evolution of the prices, designated by . The mean process is defined by

For simplicity, we assume as above that all these processes were also defined for negative times and that

At any time , each agent has access to the whole past history of the mean prices (say, which is published a particular institute or website). But to handle this wealth of information, agent has chosen, once for all, a time window length and he computes the ratio in order to decide what is the present tendency of the prices. Then he interferes that this tendency contributes to the infinitesimal evolution of his estimate of prices via the term , speculating that what has increased (respectively decreased) will keep on increasing (resp. decreasing). Nevertheless, as everyone, he also undergoes the strength of the economic reality with rate , which adds a term to his previsions. Furthermore, he cannot escape vagaries of life, good or bad, which disturb his evaluations with the infinitesimal increment , where is a standard Brownian motion. The factor may seem strange at first view, but it accounts for the fact that the consequences of random events are amplified by a large population. Alternately, it could be argued that decompose into , where , for , are independent Brownian motions standing respectively for the random perturbations induced by on (including a self-influence ). It follows that

and we deduce that

Let us assume that all the , for , and all the , for are independent. A first consequence is that the process defined by

is a standard Brownian motion.

Next, under the hypothesis that all the , have the same law as a random variable , we get by the law of

large numbers, that almost surely,

where stands for the expectation with respect to only. Thus letting go to infinity, ends up satisfying the same evolution equation as , if the law of is such that

| (3) |

almost surely with respect the trajectory .

Contrary to the first guess which could be made, should not be distributed according to an exponential law of parameter :

Lemma 1

For any continuous semi-martingale with for , (3) is satisfied if is distributed as a gamma law of shape 2 and scale , namely if

Proof

By continuity of , it is sufficient to check the almost sure equality of (3) for any fixed . Then denote , for , so that

The fact that is a semi-martingale enables to integrate by parts and we find

Remark 2 Conversely, for the process defined by (1) and for , the validity of (3) implies (under an integrability assumption) that the law of is the gamma distribution . Actually, denote by the distribution of and assume that . Then, by the previous result, (3) reads

| (4) |

Now, let . Since the above equality holds almost surely, it follows from Girsanov Theorem (see [15], Chapter 8), that we can replace by times a Brownian motion (and next by linearity take ). Then, the main argument is the support Theorem (see [17]), which yields in particular that for every positive and , for every -function such that on ,

| (5) |

Let be such a function. By (4) and (5), we obtain that for every positive ,

and it follows that for every -function with on ,

| (6) |

the result being available for all positive . Denoting and for all , we get that for all and all function with ,

namely

and and coincide on . Since this is true for all , we get that and coincide on . Because they are both probability measures, they cannot differ only on , so .

In fact this proof can be extended to any continuous semi-martingale whose martingale part is non-degenerate.

The law has the same rate of exponential decrease of the queues at infinity as the exponential distribution of in (2). The most notable difference between these two distributions is their behavior near zero: it is much less probable to sample a small values under than under . Furthermore, is a little more concentrated around its mean than around its mean , their respective relative standard deviations being 1/2 and 1. These features are compatible with the previous modeling: the chance is small that an agent looks shortly in the past to get an idea of the present tendency of and the dispersion of the lengths of the windows used by the agents may not be very important. These behaviors would be amplified, if instead of , we had chosen a gamma distribution of shape and scale , with , for the law of . The limit evolution in this situation is dictated by the stochastic differential equation in given by

(starting again from ), where is the function defined by

(curiously, the r.h.s. coincides with the probability that a Poisson random variable of parameter belongs to ).

For , we recover (1) and .

The stochastic process is clearly not Markovian, but we will see in the sequel that it is a Markov process of order 2:

it is sufficient to add another real component to to get a Markov process.

It can be shown more generally that is a Markov process of order : real components must be added

to make it a Markov process. While this observation provides opportunities of better modelings, the investigation

of for (as well as the extension to non-integer values of ) is deferred to a future paper.

Here we will concentrate on the properties of , but before presenting the results obtained,

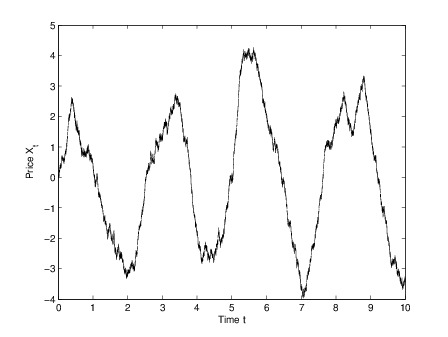

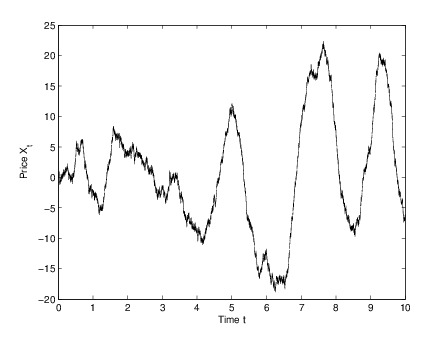

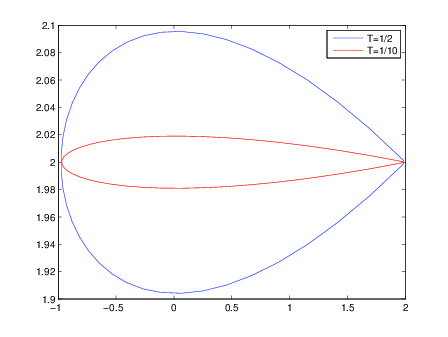

let us give some simulations of in Figure 1.

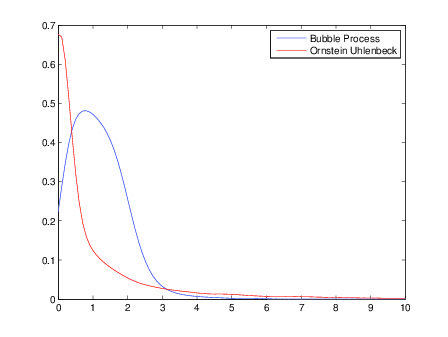

A periodic structure appears, as that observed in practice in the forming of speculative bubbles. The process shows some regularity in returning to its equilibrium position, trend which seems to be only slightly perturbed by the noise. The variety of the trajectories is apparently less rich than that experienced by traditional Ornstein-Ulhenbeck processes, suggesting a concentration of the trajectory laws around some periodic patterns. Figure 2 shows the density of the return time of the process to its equilibrium price . These results have been obtained using a large number of Monte-Carlo simulations. One may remark in Figure 2 that the tail of the return time to equilibrium state is much smaller for our bubble process than the one of the O-U. process with the same invariant measure on the coordinate and with the same amount of injected randomness (namely through a standard Brownian motion). The purpose of this paper is to quantify these behaviors.

1.2 Results

As already mentioned, the process whose evolution is driven by (1) is not Markovian. Nevertheless, it is not so far away from being Markovian: consider the process defined by

The process (where ∗ stands for the transpose operation) is then Markovian and its evolution is dictated by the simple 2-dimensional stochastic differential equation

| (7) |

starting from and where

| and | (12) |

The linearity of (7) and the fact that the initial condition is deterministic imply that at any time the distribution of is Gaussian. As it will be checked in next section, this distribution converges for large time toward , a normal distribution of mean 0 and whose variance matrix is positive definite. Since the Markov process is Feller, is an invariant probability measure for . It is in fact the only one, because the generator associated to the evolution equation (7) and given by

| (13) |

is hypoelliptic (also implying that is positive definite).

The study of the convergence to equilibrium of

begins with the spectral resolution of . Three situations occur:

If , admits two real eigenvalues, .

If , is similar to the Jordan matrix associated to the eigenvalue .

If , admits two conjugate complex eigenvalues, .

But in all cases, let be the largest real part of the eigenvalues, namely

| (14) |

This quantity is the exponential rate of convergence of , the law of , toward , in the sense: for , measure the discrepancy between and through

| (15) |

Since was our primary object of interest, let us also denote by and the first marginal distributions of and respectively.

Proposition 3

We have

These convergences can be extended to other measures of discrepancy, such as the square root of the relative entropy, or to initial distributions of more general than the Dirac measure at 0, at least under the assumption that . Thus if we look at for large , it has almost forgotten that it started from 0 and its law is close to the Gaussian distribution , up to an error .

Nevertheless, the periodicity features we are looking for appear only for , as it can be guessed from the existence of non-real eigenvalues, which suggests as period, where

| (16) |

In the regime where , we have : a lot of periods has to alternate before stationarity is approached. This phenomenon is often encountered in the study of ergodic Markov processes which are far from being reversible, e.g. a diffusion on a circle with a strong constant drift (for instance turning clockwise).

In order to quantify this behavior, we are interested in the return time to zero for , which is of primary interest in the economic interpretation given at the beginning of the introduction (on the contrary to the relaxation time to equilibrium, which seems very far away in the future):

| (17) |

Of course it is no longer relevant to assume that and instead we assume that .

In practice, appears through a temporal shift: we are at time which is such that and we are wondering

when in the future will return to its equilibrium position 0.

Up to the knowledge of , the time left before this return has the same law as if is initialized with

the value .

The next result shows that up to universal factors, the exponential rate of concentration of is given by , confirming that

when , the return to zero happens much before the process reaches equilibrium.

Theorem 4

For any , , and , we have

Furthermore, if , there exists a quantity (which in addition to and , depends on the parameters ) such that

More generally, to any initial distribution on , we can associate a quantity such that

Surprisingly, we found the lower bound more difficult to obtain than the upper bound, while in reversible situations it is often the opposite which is experienced.

Remark 5 In the first appendix it will be shown that a quasi-stationary probability and a corresponding rate can be associated to : the support of is the closure of and under , is distributed as an exponential random variable of parameter :

| (18) |

In the sequel, the quantity will be called the persistence rate of . It can be seen as the smallest eigenvalue (in modulus) of the underlying Markov generator with a Dirichlet condition on the boundary of the domain , when it is interpreted as acting on , where is the restriction of on . The above theorem then provides lower and upper bounds on , essentially proportional to : at least for ,

| (19) |

According to figure 2, starting from other initial distributions on , the law of will no longer be exponential, nevertheless we believe that for any , the following limit takes place

The difficulty in obtaining this convergence stems from the non-reversibility of the process under consideration. In the literature, it is the reversible and elliptic situations which are the most thoroughly investigated. For a general reference on quasi-stationarity, see e.g. the book [6] of Collet, Martínez and San Martín, as well as the bibliography therein.

The previous result provides a good picture for large values of , but is there a precursor sign that will be much shorter than expected? Indeed we cannot miss it, because in this situation of a precocious return to zero, the system has a strong tendency to first explode!

To give a rigorous meaning of this statement, we need to introduce the bridges associated to .

For and , denote by the law of the process evolving according to (7),

conditioned by the event . Note that there is no difficulty to condition by this negligible set, because

the process starting from is Gaussian and the law of is non-degenerate.

For fixed and small, we are interested in the behavior of , the process defined by

Let us define the trajectory by

| (22) |

where and .

Theorem 6

For fixed , as goes to , converges in probability (under ) toward the deterministic trajectory , with respect to the uniform norm on .

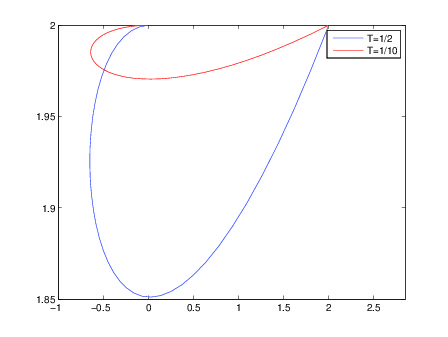

In particular, if are such that , and , the bridge relying to for small explodes as . From the definition of given in (22), we can see that the explosion is in the -direction, toward or , depending on the sign of , as it is illustrated by the pictures of Figure 3.

Remark 7 Note that the sharp behavior of the bridge when leads in Section 4 to a probabilistic proof of a lower-bound for (see Proposition 35). The interest of this alternative proof is that the approach is maybe more intuitive. However, we have not been able to provide some explicit constants following this method.

The paper is constructed on the following plan. In next section we present the preliminaries on , especially its Gaussian features which enable to obtain Proposition 3. We will also see how to parametrize the process under a simpler form. The exit time defined in (17) is investigated in Section 3, where Theorem 4 is obtained. Section 4 is devoted to the study of bridges and to the proof of Theorem 6. At last, we shortly discuss in Section 5 on a numerical and statistical estimation problems related to the estimation of .

2 Preliminaries and simplifications

This section contains some basic results about the Ornstein-Uhlenbeck diffusion described by (7) and whose coefficients are given by (12).

2.1 Gaussian computations

Our main goal here is to prove Proposition 3.

We begin by checking that the process is Gaussian. Indeed, considering the process defined by

we get that

It follows that

since we assumed that . It appears on this expression that for any , the law of is a Gaussian distribution of mean 0 and variance matrix given by

| (24) | |||||

For , the eigenvalues of have negative real parts, so that the above rhs converges as goes to infinity toward a symmetric positive definite matrix . As announced in the introduction, the Gaussian distribution of mean 0 and variance is then an invariant measure for the evolution (7). It is a consequence of the fact that the underlying semi-group is Fellerian (i.e. it preserves the space of bounded continuous functions), as it can be seen from (2.1), where depends continuously on , for any fixed . Note furthermore that the above computations show that for any initial law of , the law of converges toward for large , because converges almost surely toward 0. It follows that is the unique invariant measure associated to (7). To obtain more explicit expressions for the above variances, we need the spectral decomposition of . The characteristic polynomial of being , we immediately obtain the results presented in the beginning of Subsection 1.2 about the eigenvalues of . Let us treat in detail the case , which is the most interesting for us: there are two conjugate eigenvalues, , where (see (14)) and is defined in (16).

Lemma 8

If , there exist two angles and such that for any ,

where

Passing to the limit as , we get and we deduce more precisely that

Proof

From the first line of the matrix , we deduce that an eigenvector associated to is . So writing

| and |

we have that , where

In view of (24), we need to compute for any ,

where ∗ is now the conjugate transpose operation. A direct computation leads to

where and . So we get that

Integrating this expression with respect to , we obtain, first for any ,

and next, recalling that ,

Thus it appears that

where the last term is the sinusoidal matrix defined by

Note that (this can also be deduced from ). To recover the matrices given in the statement of the lemma, we remark that and , so there exist angles such that

| and |

Since , we have and the first announced results follow at once. Concerning the more explicit computation of , just take into account that

| and | ||||

| and |

and expand the matrix

Remark 9 In particular, it appears that for large time , converges in law toward the centered Gaussian distribution of variance .

We will need another basic ingredient, valid in any dimension, about the functional defined in (15).

Lemma 10

Let and be two Gaussian distributions in , , of mean 0 and respective variance matrices and , assumed to be positive definite. If is positive definite, we have

where and otherwise.

Proof

From the above assumptions, we have

Thus the function belongs to (property itself equivalent to the finiteness of ), if and only if the symmetric matrix is positive definite. In this case, we have

where we used that . It remains to note that

Still in the case , we can now proceed to the

Proof of Proposition 3

In view of Lemma 8, we want to apply Lemma 10 with and , for . This amounts to take , matrix converging to zero exponentially fast as goes to . It follows that for large enough, is positive definite and we get

Taking into account that the matrices are bounded uniformly over , an expansion for large gives

(where stands for the Hilbert-Schmidt norm, i.e. the square root of the sum of the squares of the entries of the matrix). We will be able to conclude to

| (35) |

if we can show that

| (36) |

(since it is clear that ). Taking advantage of the fact that is a symmetric and positive definite matrix, we consider for , , which is also a symmetric matrix. Since , this quantity is nonnegative and can only vanish if , or equivalently , is the null matrix. This never happens, because the first entry of , namely , is positive. The continuity and the periodicity of the mapping enables to check the validity of (36) and next of (35).

The corresponding result for the first marginal (the law of ) is obtained in the same way. Indeed, from Lemma 8, for any , is the real Gaussian law of mean 0 and variance , where

with the angles and described in the proof of Lemma 8. In particular is the real Gaussian law of mean 0 and variance . Lemma 10 applied with leads at once to

The remaining situations and can be treated in the same way. In view of the previous arguments, it is sufficient to check that it is possible to write

where is defined in (14) and where the family is such that

for any chosen norm on the space of real matrices, due to their mutual equivalence. The obtention of the family also relies on the spectral decomposition of , with converging for large times if and exploding like if .

2.2 Simplifications with the view to Theorem 4

Let us begin this subsection by emphasizing two important properties of Theorem 4:

The result does not depend on the variance coefficient .

The exponent is proportional to which denotes the mean angular speed of the deterministic

system .

These properties can be understood through some linear and scaling transformations of the process .

More precisely, these transformations will be used in the sequel to reduce the problem to the study of a process with

mean constant angular speed and a normalized diffusion component.

We choose to first give the idea in a general case and then, apply it to our model.

Let with complex eigenvalues given by where and . Let us consider the two-dimensional Gaussian differential system given by

| (37) |

where and is a standard two dimensional Brownian motion. For such a process, the precise transformation is given in Proposition 12. This proposition is based on the following lemma.

Lemma 11

Let with complex eigenvalues given by where and . There exists such that

where

| (38) |

Furthermore, for every , given by is an admissible choice.

Proof

Set . The eigenvalues of are so that . For any , set . The matrix is clearly invertible and using that , one obtains that . The result follows.

Proposition 12

Let be a solution to (37) where with complex eigenvalues given by (with and ). For any and , set . The process is a solution to

| (39) |

where is a standard two-dimensional Brownian motion.

Proof

First, set . Owing to the preceding lemma, is a solution to

For any , set . Setting (which is a Brownian motion), one checks that

We now apply this proposition to our problem.

Corollary 13

Let be a solution to (7) and assume that . Set . Let and set with . Then for any , the process defined by is a solution to

| (40) |

where is a standard two-dimensional Brownian motion. In particular, if and , then is a solution to

| (41) |

where is now a standard one-dimensional Brownian motion.

Remark 14 In the second part, of the corollary, one remarks that one chooses in order that the transformed process has only a (normalized) diffusive component on the second coordinate.

Furthermore, if has for initial deterministic condition, then starts from the point . The images of and by are particularly important for our purposes, since they enable to see that the half-plane for is transformed into the half-plane for . Note that in the setting , the latter half-plane is quite similar to the former one, since .

Proof

We recall that is a solution to

and is defined in (40). When , the eigenvalues of are given by

For any , set with

Applying the previous proposition, we deduce that for any , is a solution to

where is a standard two-dimensional Brownian motion. For the second part, it remains to choose and so that

| (42) |

If , then

| (43) |

One deduces that condition (42) (or more precisely the fact that ) implies . Setting , we have

Condition (42) is then satisfied when .

3 Dirichlet eigenvalues estimates

This section is devoted to the proof of Theorem 4. More precisely, the aim is to obtain successively upper and lower bounds for where . In fact, some of the results will be stated for exit times of more general domains. For a given (open) domain of , we will thus denote by

3.1 Upper-bound for the exit time of an angular sector

3.1.1 The case

In this part, we focus on the particular stopping time of Theorem 4 which corresponds to the exit time of . We have the following result:

Proposition 15

Let be a solution to (7) with . Then, for every such that ,

Proof

Set . The function being a solution to , we deduce in particular that

Since , the roots of the characteristic equation associated with the previous equation are: where . As a consequence, there exists and such that

Reminding that , we deduce that . Thus, at time ,

But and is Gaussian and has a symmetric distribution. Thus, we deduce from what precedes that

which in turn implies that

| (44) |

Thus, we have a upper-bound at time which does not depend on the initial value . As a consequence, we can use a Markov argument. More precisely, owing to the Markov property and to (44), we have for every integer :

An iteration of this property yields

It follows that

This concludes the proof.

3.1.2 Extension to general angular sectors

We now consider an angular sector defined as

| (45) |

where and . The set can also be written with . Note that for the sake of simplicity, we only consider angular sectors which are included in . The results below can be extended to any angular sectors for which the angular size is lower than . For such domains, we first give a result when the model has a constant (mean) angular speed even if such a result does not apply to the solutions of (7) for sake of completeness. This is the purpose of Lemma 16 below.

Concerning now our initial motivation, we also derive an extension of Proposition 15 for any general angular sector, and this result is stated in Proposition 17.

Lemma 16

Let be a solution of

where , , and is a two-dimensional Brownian motion. Let be defined by (45) where and . Then, for any ,

with and

Proof

Let and define , is a solution of

We deduce that

where and . This implies that the angular rate of is constant and is equal to . Thus, it follows that for every starting point ,

One can then find a line passing through and dividing into two half-planes and such that is included in and . Owing to the symmetry of a one-dimensional centered Gaussian distribution, we have

One finally deduces that for every ,

and thus that

The end of the proof is then identical to that of Proposition 15.

We now consider our initial bubble process which is solution of Equation (7). We have the following result.

Proposition 17

Remark 18 Taking and , we retrieve Proposition 15 since then corresponds to the half-plane . Note that contrary to Lemma 16, the exponential rate is not directly proportional to . More precisely, due to the non constant angular speed, and depend on . For the particular domain of Proposition 15 this dependence does not appear since, even if the the angular rate is not constant, the time to do a U-turn is still proportional to .

Proof

By Corollary 13, for any of , (where ) is a solution of

where is a constant real matrix (whose exact expression is not so important) and where . In the new basis ,

Setting , we deduce from Equation (43) that

In such a case

so that

Thus, we deduce from Lemma 16 that

where for a given domain , and , . The result follows.

3.2 Lower-bound

3.2.1 General tool

In this second part, our aim is to obtain the lower-bound part of Theorem 4, in particular we want to derive a upper-bound on:

The results of this section are based on the following (classical) proposition.

Proposition 19

Let be a -valued Markov process with infinitesimal generator and initial distribution . Let be an (open) domain of and assume that . Let . Then, if there exists a bounded function and such that

| (46) |

then, . As a consequence,

Proof

Owing to the Dynkin formula, we have for every

where is a local martingale. Owing to a localization argument and to Fatou’s Lemma, we deduce that

Suppose that . Then, using the dominated convergence theorem and the fact that , we have

whereas the fact that implies that the right-hand term is uniformly lower-bounded by which is (strictly) positive. This yields a contradiction. Thus, . The second assertion then classically follows from the equality

The end of Section 3.2 is devoted to the construction of a function satisfying (46). In fact, for this part, the degeneracy of the process described by Equation (7) implies a significant amount of difficulties. That is why we propose in the next subsection to first focus on the elliptic case which can be handled more easily. Some of the ideas developed in this framework will then be extended to the initial hypoelliptic setting.

3.2.2 The elliptic case

By Corollary 13, we know that we can reduce the problem to the study of a process solution to (41). In this part we focus on its elliptic counterpart: we consider a two dimensional process solution of the following stochastic differential equation

| (47) |

where is a real number and is a standard two-dimensional Brownian motion.

We define .

In order to build a suitable function satisfying (46) with and relatively to the infinitesimal generator associated to (47), we first switch to polar coordinates: Proposition 41 (stated in the second appendix) shows that is given on by

| (48) |

To justify the approach developed below, let us forget formally the derivatives with respect to by fixing and by considering unknown angular functions . The problem of finding and such that (46) holds (with ) reduces to solve the second order ordinary differential equation

with . The solutions are given by exponential functions where are the complex roots of the quadratic characteristic equation associated to the linear ODE given above. One can easily check that and the boundary conditions imply in particular to choose such that otherwise the function cannot remain positive on . This is possible if and only if and the solutions of this simplified spectral problem are then proportional to the function defined by

The previous construction cannot really be extended to the exact initial problem . Nevertheless, this suggests to search potential solutions to the problem under the following form

| (49) |

where is a -function which must be non-positive (due to the boundedness condition in Proposition 19). The action of the generator described in (48) is given as follows (the proof is postponed to the second appendix).

Proposition 20

In order to apply Proposition 19, the problem is now reduced to find a non-positive angular function such that is lower-bounded on . The previous computation shows that we mainly need to satisfy the following constraint

An admissible value of for the spectral inequality will then be obtained by

Note that this implies in particular that

A solution of the problem is given in the next proposition.

Proposition 21

Remark 22 Note that by the scaling and linear transformations previously described, this result can be transferred to general elliptic two-dimensional Ornstein-Uhlenbeck evolutions whose linear drift is given via a matrix admitting complex conjugate eigenvalues (and whose trajectories have thus a tendency to turn around ).

The function is a -function but only a piecewise -function. However, since these functions still belong to the domain of , the conclusions of Proposition 19 still hold. Also note that if we now switch to cartesian coordinates, the counterpart of has the following (nice) form:

Proof

(i) First, assume that and consider the function stated in the former statement. One checks that is a piecewise -function on . Note that we can use this function since Itô’s formula is still available in this case. Furthermore, we check that

| (51) |

so that is non-negative on . As well, easy computations yield:

| (52) |

It follows that is lower-bounded by and the result follows when . The extension to the case is obvious using that is a non-negative function.

(ii) This statement follows from Proposition 19, since is and piecewise .

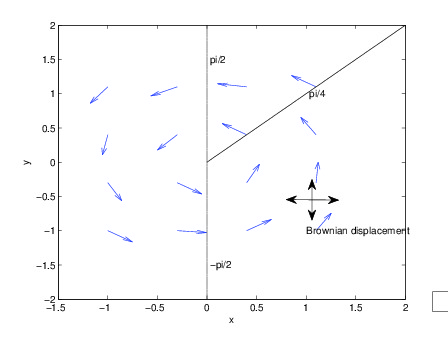

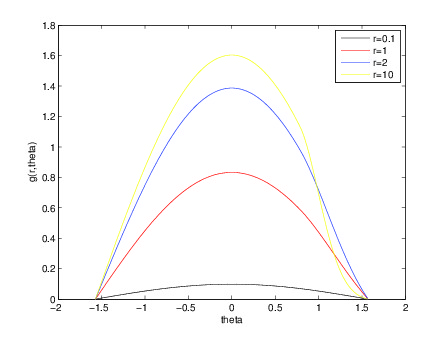

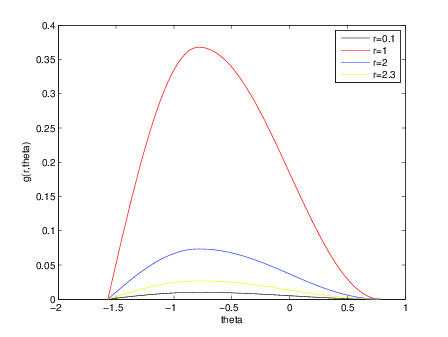

Remark 23 Figure 4 represents the partition of the state space (seen as in the second picture) for the construction of the function (and ) as well as the function for several values of . We should understand the function as follows: must be large when the dynamical system is suspected to take long time to exit the set from . Conversely, it should be small in the region where the vector field of the underlying determinist dynamical system push the trajectories out of . As pointed out by Figure 4, we do not need to consider sub-domain of : the action of the Brownian motion is elliptic and we can always build some trajectories starting from any point of and staying an arbitrarily long time in . Note that when is small, the starting point is near the origin, whatever the value of is and hence, the function is small (see the right side of Figure 4).

3.2.3 The hypoelliptic case

We now come back to the study of the lower-bound of Theorem 4. This result is proved in Proposition 29 stated below. We know from Corollary 13 that up to linear changes of variables in time and space, the initial dynamic may be reduced to the simplified stochastic evolution described by Equation (41). Again let us write down the corresponding infinitesimal generator in polar coordinates (see Proposition 41 given in the second appendix):

| (53) |

with . As mentioned before, we would like to use a strategy similar to the one considered in the elliptic case. However, the hypoelliptic problem is more involved. Roughly speaking, the degeneracy of the diffusive component implies that in the neighbourhood of , the paths of the solutions to (41) can not be strongly slowed down by the action of the Brownian motion (see Remark 3.2.2 and the study on Brownian bridges below). In other words, we are not able (and it seems indeed impossible) to build a function such that the function defined in the previous subsection is lower-bounded. Thus, the idea is to reduce the domain to a smaller angular sector included in where the diffusive action of the Brownian motion is more likely to keep the process in .

Consequently, we consider a more general class of functions (which must be calibrated in the sequel) and define

| (54) |

where is a positive integer and and are some sufficiently smooth functions. Now should be bounded above by a negative constant for to have a chance to be bounded. The new function will be chosen in order that is positive in the interior of the angular sector and vanishes on the boundary of . We first describe the effect of on such a function (the computations are deferred to the second appendix).

Proposition 24

We now need to find an (open) angular sector , a positive integer , some functions and such that

-

1.

on , , on ,

-

2.

and are non-negative on ,

-

3.

is lower-bounded.

-

4.

is bounded above by a negative constant.

This is the purpose of the next proposition.

Proposition 25

Let .

(i) Let be defined by (54) with ,

| (55) |

and . Then, for every and with ,

(ii) As a consequence, for any open half-plane such that , for any probability measure on such that , we have

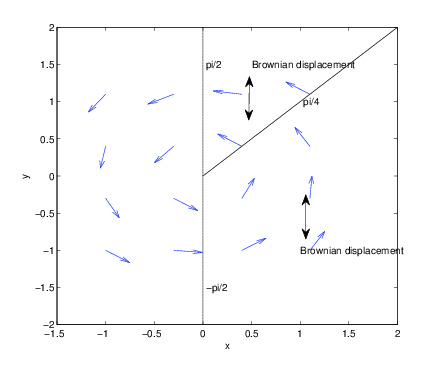

Remark 26 The vector field corresponding to the drift part of the stochastic evolution under study, as well as the most favorable positions (which are expected to be the points where is large) for the starting point in order to keep the process in for large times are illustrated in Figure 5. As pointed out above, the angular sector is now avoided to keep the process in the half-plane . Moreover, the right side of Figure 5 shows that excessive values of (too large or too small ones) are also prohibited: small values are unfavourable since it corresponds to starting positions very close to the origin (and naturally close to the axis ). Large values of are also disadvantageous owing to the large norm of the drift vector field against which the Brownian motion has to fight to keep the process in .

Proof

With the proposed choices of and , one checks that

so that is non-negative. Since is constant and is non-negative, the fact that is non-negative is obvious. Thus, it remains to focus on . In fact, easy computations show that on whereas

The conclusion of the first assertion follows.

(ii) By Proposition 19 and what precedes, for any probability measure on such that ,

| (56) |

Now, consider the general case. Let be a probability such that . Then, for every , for every finite stopping time ,

Thus,

and it follows from the Markov property that

If we assume for a moment that is such that

| (57) |

then,

where is the probability measure defined for every bounded measurable function by

By (56) and the (strict) positivity of , we obtain that

Thus, it remains to prove (57). It is certainly enough to show that for every , there exists a deterministic positive such that

The idea is to build some “good” controlled trajectories: let and denote by the solution of the controlled system

starting from . The classical Support Theorem (see [17]) can be applied since the coefficients of the diffusion are Lipschitz continuous. This implies that (57) is true as soon as there exists such a for which the solution belongs to and such that belongs to . Such a controlled trajectory can be built through the following lemma.

Lemma 27

Let and set and ().

(i) Let with . Then, for every , there exists a controlled trajectory starting from and a positive such that , and .

(ii) Let with and consider the solution to the free dynamical system ( the controlled trajectory with ) starting from . Then, there exists such that and such that with . Furthermore, writing (with and ), this property holds with and .

Remark 28 Note that this lemma will be also used in the proof of Proposition 35 (see Step 3). This is the reason why its statements are a little sharper than what we need for the proof of the previous proposition.

Proof

(i) Without loss of generality, we only prove the result when . The idea is to build such that the derivative of the second component is large enough. More precisely, for every ,

is certainly an equation of a controlled trajectory (by setting ). Furthermore, denoting by its starting point, we have

First, let us choose large enough in order that for all , and , such that and for all . A simple study of the derivative of yields

Thus, for every , there exists large enough such that . Using that for any and , and setting , we obtain that

Since is a continuous function such that as , it follows that for every , there exists such that .

(ii) The result is obvious since the solution to the free dynamical system satisfies

We are now able to prove the lower-bound of Theorem 4.

Proposition 29

Let be a solution of (7) with and let . Then, for every probability measure on such that ,

Remark 30 Since ,

This corresponds to the bound given in Theorem 4. However, the reader can remark that the above result yields some sharper bounds. In particular, when tends to , tends to .

Proof

Let such that . Owing to the symmetry of the Brownian motion, one can check that

where , and .

Second, set and with .

By Corollary 13, there exists such that is a solution of

(41). Denote respectively by and by , the coordinates in the canonical basis and in the basis . Computing , one checks that in the new basis, the set corresponds to the half-plane defined by

Furthermore, from the very definition of , we have

In particular, so that for any probability on such that ,

where satisfies . Now, when , one checks that so that contains the set of Proposition 25 (written in polar coordinates). Applying the second item of this proposition with , we finally obtain

4 Bridges at small times and persistence rate

In this section, we study the diffusion bridge associated to our dynamical system. We then use it to establish some lower-bounds for (where ).

4.1 Explosion of bridges at small times

Our objective here is to prove Theorem 6 and to discuss some related results.

Since we are mainly to take advantage of the Gaussian features of the problem, we could have worked directly with the process whose evolution is given by (7). Nevertheless the computations presented in Subsection 2.1 suggest that it is more advisable to first consider the simplifications made in Subsection 2.2. So we begin by considering the two-dimensional Ornstein-Uhlenbeck process whose evolution is dictated by

| (60) |

where and is a standard real Brownian motion. Let us assume furthermore that the initial condition of is a deterministic point . The arguments of Subsection 2.1 show that is Gaussian and more precisely we have:

Lemma 31

For any , is distributed as a Gaussian law of mean and variance , with

Proof

Let us denote

| and |

From the beginning of Subsection 2.1, we get that for any , on one hand

and on the other hand, the validity of (24). We compute that for any ,

The announced expressions for the entries of follow from immediate integrations. For instance for , we have

For , let us denote by the law of knowing that . With the notations of the above lemma we have

Using Bayes’ formula, we get that for and , the law of conditioned by (and still by ) admits a density proportional to where . It is a non-degenerate Gaussian law, let (resp. ) be its mean vector (resp. its covariance matrix), formula (69) below will show that the covariance matrix does not depend on and . We furthermore define

where and . The next result contains all the required technicalities we will need.

Proposition 32

For all and , we have

Proof

To simplify notations, for , we denote , and . With the notations of Lemma 31, the vector and the matrix are such that for any ,

where is a normalizing term which is independent of . It follows that

| (68) | |||||

| (69) |

where for any ,

All these expressions depend on and the announced convergences will be obtained by expanding them for small . Indeed, simple computations show that for , as ,

where , for , stands for a quantity bounded by , uniformly over and for small enough. It follows that

Using furthermore that for , we have and that

we deduce that

Thus from (69), we get that for ,

with

Recalling that , it appears that , so we obtain

| (79) |

The second convergence announced in the proposition follows at once. To deduce the first one, we begin by checking that for ,

In conjunction with (79), we get

In these expression, the -entries explode as , it explains the renormalisation by considered in the above proposition for and resulting convergence.

Remark 33 Note that when (namely if and are on the same vertical line), it is simpler for the underlying vertical Brownian motion to put them in relation. Hence, the second component of is equal to . In this case, we thus expect the second component of to be convergent when . Pushing further the previous developments yields

| (84) |

and

| (85) |

Combined with the computations of the end of the previous proof, we deduce that if , then no renormalisation is needed for the mean vector and we get

In particular even in the case when , the asymptotical bridge doesn’t stay still (except if ), since

Similarly to the notational conventions endorsed in the introduction, for and , let be the law of the process evolving according to (60), conditioned by the event and consider the process defined by

Under this process is Gaussian and Proposition 32 enables to see that for fixed , as goes to , converges in probability (under ) toward the deterministic trajectory , with respect to the uniform norm on ). Indeed, would even have been sufficient for this behavior. Using the linear space-time transformation described in Subsection 2.2, this result can be retranscripted under the form of Theorem 6.

Remark 34 Following Remark 4.1, if and are such that , then the process , defined by

converges in probability (under ) toward the deterministic trajectory , with respect to the uniform norm on ), where

Using the linear space-time transformation described in Subsection 2.2, this result can also rewritten in the original setting of the Introduction.

4.2 A probabilistic proof of a persistence rate upper-bound

The previous developments on the diffusion bridge associated to (60) enable us to retrieve a lower-bound of , for defined in (17).

Proposition 35

(i) Let be a solution of (60) with . For , let . Then, for any positive , there exists a constant such that for any satisfying and any , one can find a constant (which depends on as well as on the parameters and ) such that

(ii) Let be a solution of (7). There exists such that if , we have for every

where and is a constant which depends on , , and .

Remark 36 It is possible to be more precise, the same proof showing that for all , one can find a corresponding such that (i) is satisfied if , and if is replaced by (the constant has then also to depend on and ). It follows that in (ii) the condition can be replaced by with the price that (and ) must depend on . But we believe that even these results are not optimal (e.g. one could hope for the condition in (ii)), so we won’t detail them. Proposition 35 is just an illustration of how the bridges could be used further.

Proof

(i) The proof is divided into three steps. In the first one, we show that we can build a subset

of

for which any bridge associated to (60), starting and ending in (at a time which will be chosen small) stays in with a high probability. Then, in the second one, we use a Markov-type argument close to the one used in the proof of Proposition 15 to obtain the announced result when the starting point of is in . Finally,

we extend the result to any initial point in .

Step 1. Lower-bound for for a particular . Let and belong to . Denote respectively by and the first and second coordinate of . First, owing to Proposition 32 (and to the more precise developments stated in its proof) and to (84) and (85), one checks that

| (89) |

and

| (90) |

where and satisfy: there exists and a positive constant such that for every , for any and and for any (due to the uniformity of in (84) and (85) with respect to in a compact set of ).

Second, by Theorem V.5.3 of [1] (applied with and ), there exists a universal constant such that

where By Proposition 32, for every , as . Note that this convergence is uniform in and since the covariance matrix does not depend of them. By (79), it appears that the convergence is also uniform in and a little sharper study of the dependence of in yields in fact that for every ,

Applying the previous inequality with , we deduce that there exists such that for every , for every and every ,

We shall now build a box (where and are positive numbers) for which there exists a positive such that when , the mean stays at a distance greater than of the boundary of . Checking that for a point of , the distance from to the boundary is equal to , we thus need to find , and in order that

| (91) | |||||

Note that , and will depend on but not on and satisfying . Using (89) and (90), we obtain that there exists such that for every , for every and every

| (92) |

Equation (92) shows that (91) is fulfilled as soon as

Taking into account that and , the above inequality is satisfied if

| (93) |

relation which no longer depends on . We can now set for instance and and choose small enough so that (93) is satisfied. As a consequence, the subset of is such that for every and verifying , we have

| (94) |

Step 2. Lower-bound for when . We consider a time and a subset of (depending only on ) for which (94) holds. For every , we have

By the Markov property,

where

and is the conditional law (under ) of on . Owing to (94) and to the fact that the support of is included in , we get

Note that for , the transition density is positive and continuous with respect to . It follows that the coefficient is positive by compactness of . Furthermore it is uniform over satisfying the conditions of Proposition 35 (but a priori depends on , as and do). Then, since for all ,

where , we deduce from an induction that for every ,

where (depending only on ).

Step 3. Lower-bound for when . The idea of this step is identical to that of the proof of Proposition 25(ii). More precisely, to extend the lower-bound obtained above to any (up to a constant which depends to ), it is enough to build a controlled trajectory such that belongs to and such that for every .

Owing to Lemma 27, it is enough to consider the case . We treat successively the cases and .

If , the idea is to join a point of a path of the free dynamical system which passes through . More precisely, by Lemma 27, we know that the solution to the free dynamical system starting from passes through at time and that is a curve included in . It remains to join a point of (without leaving out ). This can be done applying Lemma 27 with .

Suppose now that . The construction is slightly different in the cases and (by the assumptions of Proposition

35,

the

situation is excluded). If , we join by crossing the segment with a controlled trajectory. Set . This trajectory can be viewed as the solution starting from of

with . Hence, this is a controlled trajectory which clearly crosses in a finite time. Finally, if , we join a point using Lemma 27. If , we are reduced to the first considered case. So we can assume that and we join the point by crossing the segment with a controlled trajectory (more precisely, is a controlled trajectory). This ends the proof of .

By Corollary 13, there exists such that is a solution of (41). Remind that and for a subset of , set . Similarly to the proof of Proposition 29, one checks that for every ,

where , , and belongs to . The result follows by applying the first part of this proposition with . Indeed, the assumption amounts to . For the other condition, , taking into account that , it is sufficient that , namely and note that .

5 Simulations and statistical considerations

In this section, we shortly focus on some statistical problems related to the estimation of the real parameters which govern the trajectories solutions of (1). We denote the unknown underlying parameters and aim at developing some statistical estimation methods of these parameters. We are also interested in the average time for the process to return to the equilibrium price. When is small, it can be shown that such an average time is close to (see the results of [11] and [2] for small noise asymptotics of random dynamical system) where is the period of the deterministic process associated to the model:

| (95) |

With a slight abuse of language, will be then called pseudo-period of the process.

It is natural to wonder if it is efficient to first estimate and then, to plug these estimates in the analytical formula given above. We describe in the next paragraph how one can use the maximum likelihood estimator to approximate . Then, a short simulation study exhibit rather different behaviours of the estimator of the pseudo-period derived from the values plugged into (95). When is small, we compare such an estimation with a more natural estimator derived from hitting times of the level and show that in some cases, this last estimation can perform better for the recovery of . In our short study, we will assume that the process starts from its equilibrium, that is . This assumption slightly simplifies the MLE derived below.

5.1 Maximum likelihood estimator for parameters and

Statistical settings

In this paragraph, we first detail the computation of the MLE of the real parameters denoted when one observes the whole trajectory of the price between and . This is of course an idealization and a dramatical simplification of the true statistical problem since in practical situations, we can only handle some values of in a discreted observation grid .

Even if the relative size of compared to the time length of observation is of first interest for some real statistical applications, we simplify this short study and consider only continuous observation times. We leave this important question of the statistical balance between and to a future work. In such a situation, it is easy to recover the parameter by considering the normalized quadratic variation of the trajectory .

Hence, in the sequel, we only consider the problem of the estimation of and and we assume the knowledge of (we fix it to for sake of convenience).

Change of measure formula

In order to estimate , we can only handle the process since depends on the unobserved parameter through the relation

For any choice of , we consider the two processes defined by

| (96) |

and

In Equation (96), depends on the increments . A simple integration by part yields the equivalent expression:

The fact that follows from the definition of the process . Thus, satisfies

Now, we can apply the Girsanov formula: if we denote by the law of the process, we then obtain the change of measure formula:

Maximum likelihood

Given any trajectory , we can then define , the log-likelihood of the parameters as follows:

The expression above can be modified using an integration by part. We then obtain the ”robust” formulation:

| (97) | |||||

The maximum likelihood estimator is then formally defined by

For any , is a concave function and thus the optimal value of given any is

Hence, is obtained by maximizing . Unfortunately, we did not find any explicit formula regarding the relation . Hence, to estimate , we use an exhaustive numerical search of the optimal value of and we obtain .

5.2 Estimation of the mean pseudo-period with hitting times strategy

It may be possible to estimate using the maximum likelihood estimators defined above with and plug them in the relation (95) (which is supposed to be true only for with a vanishing noise level)

Of course, the ability of this estimator to well approximate highly depends on the asymptotic behaviour of . We will discuss on several statistical questions related to this study in the next section.

We can also compare with a more nature way to estimate the mean return time all along the trajectories by considering the sequence of crossing times of level of . In this view, let us consider , and define a skeleton chain associated to the trajectory . The sequences and are initialized with:

and recursively built as follows:

When is small, we can now define a quite natural estimator of the mean pseudo-period using this construction. If we set , we set

5.3 Statistical performances and open problems

To establish the numerical performances of and , we use the following statistical setting: several trajectories defined on are observed on some discrete times . The observation time are equally sampled with a constant step size such that . We are interested in the behaviour of our two estimators in the two distinct asymptotic settings:

-

•

High resolution sampling scheme

-

•

Long time observation .

For our purpose, the threshold is defined empirically after several runs of the estimator. It should be carefully chosen since is the parameter which enables to distinguish real crossings of from the natural volatility of the model carried out by the brownian noise. Thus, the calibration of should be related to the noise level contained in . In our simulation, we have chosen . We use for each estimator Monte-Carlo simulations to obtain the repartition of and around .

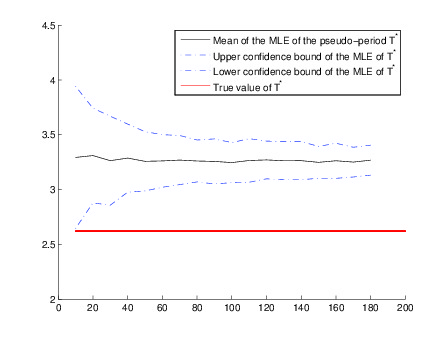

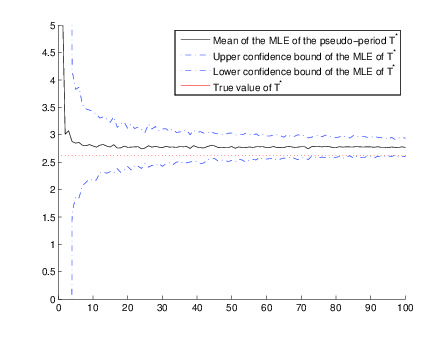

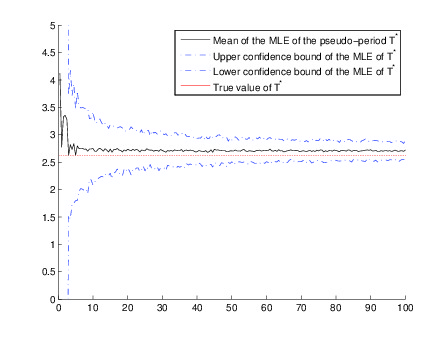

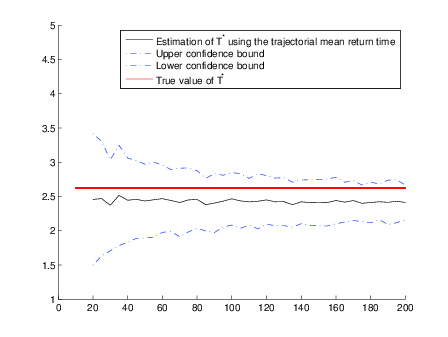

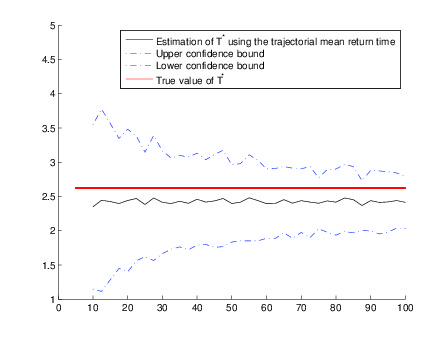

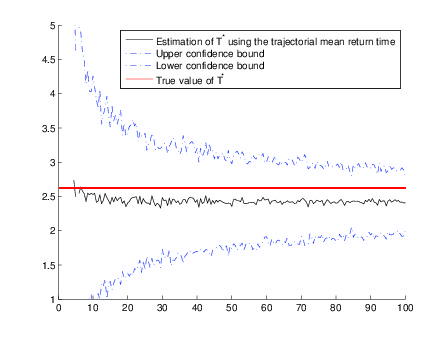

Moreover, we use a discretized version of the stochastic differential equation with several step size. We show in Figure 6 the performances of for several size of discretization step as well as the performances of in Figure 7.

One may instantaneously remark that the step size has an important influence on the ability of to recover although this parameter does not seem so important for the estimator . Simulations show that the smaller , the smaller the bias of . Moreover, the variance of the estimator is mainly determined by the length of simulation (time ). Hence, for a fixed step size of simulation, Figures 6 and 7 demonstrate that it seems better to use to infer . When one may let , the maximum likelihood estimator seems more convenient.

We shortly describe several problems of interest which concern the estimation of . First, the influence of as well as the influence of needs to be understood for the estimation of using the MLE. This question may be faced with a careful understanding of the natural score function defined by the log-likelihood . Our simulations tend to show that a special asymptotic behaviour of ( should be considered to obtain optimal estimations.

Second, the size of the threshold in the definition of has not been theoretically investigated, although it has a great influence on the ability of to nicely recover . Hence, there should also exist a precise asymptotic regime of which may permit to obtain statistical reconstruction properties. Such a last result should be derived from a careful inspection of the local times spent by around the level (to fix ) as well as the concentration rate of the hitting times which may be obtained using Theorem 4.

At last, the link between and the expected time needed for to return to its equilibrium price is still mysterious. We only identify this link in the small noise asymptotics and even though such a relation seems to be true in more general situations for , a theoretical proof is missing.

These three questions are far beyond the scope of this study, and we let them open for future works.

6 Conclusion

In this paper a model of speculative bubble evolution was proposed. The dynamics has to be at least of second order, to have a chance to display a weak periodic behavior typical of this kind of phenomena. This second order is induced by the way the process under consideration weights its past evolution to infer its future behavior (increase/decrease in the close past favoring an immediate tendency to follow the same trend). Dynamics of all orders (including non-integer ones) could be obtained in the same fashion, by modifying the weights. At the “microscopic level”, the latter are related to the distribution of the backward time windows used by a multitude of agents in order to speculate on the future evolution.

But we restricted ourselves to second order dynamics: it is the simplest one and in some sense it mimics Newtonian mecanics, which are also of second order, the forces impacting directly on the acceleration. A main difference is the noise entering our modeling, which is required to maintain some stability of the system under study. Nevertheless and informally, this analogy with the physics law of motion enables to unmask some misleading arguments used by the real estate agencies and the mass media: they mainly explain the evolution of prices by making an inventory of the forces in the housing market, such as loan interest rates, the growth of population, etc. (all these factors, as well as opposite leverages, are summed up in our parameter ), forgetting the order of the evolution equation (induced by the parameter ). Transposed in the astronomy field, it would amount to make the observation that the main interaction between the Sun and the Earth goes through gravitation, so that we should conclude that our planet would soon end up in the Sun. Luckily, we are essentially saved by the second order of the kinetics law which enables the Earth to turn around the Sun!

We have also assumed that the repelling force to the equilibrium level is linear and traduced in (1) by the dritf term at any time . This drift term mimics an economic repelling force which may be non-linear. Nevertheless, our linearization may be considered as a first order valid approximation at least near the equilibrium state .

From the mathematical point of view, our main interest was in the return time to the equilibrium “price” and we have shown that it is more concentrated than the relaxation to the equilibrium distribution of the prices. This feature explains the bubble/almost periodic aspect of the typical trajectories. We have obtained some lower and upper bounds of this concentration rate in Theorem 4. Even if there is still a gap of order around ten between our lower and upper bounds, numerous simulations (not shown in this paper) using the Fleming-Viot’s type algorithm described in [7] lead to the conjecture that .

One failing of our framework is that the parameters , and were assumed to be time-independent, hypothesis which is certainly wrong in practice. Our model should apply only to a few periods and a finer modeling would take into account the time-inhomogeneity of , and . Such an extension remains Gaussian, but its investigation is out of the scope of this paper.

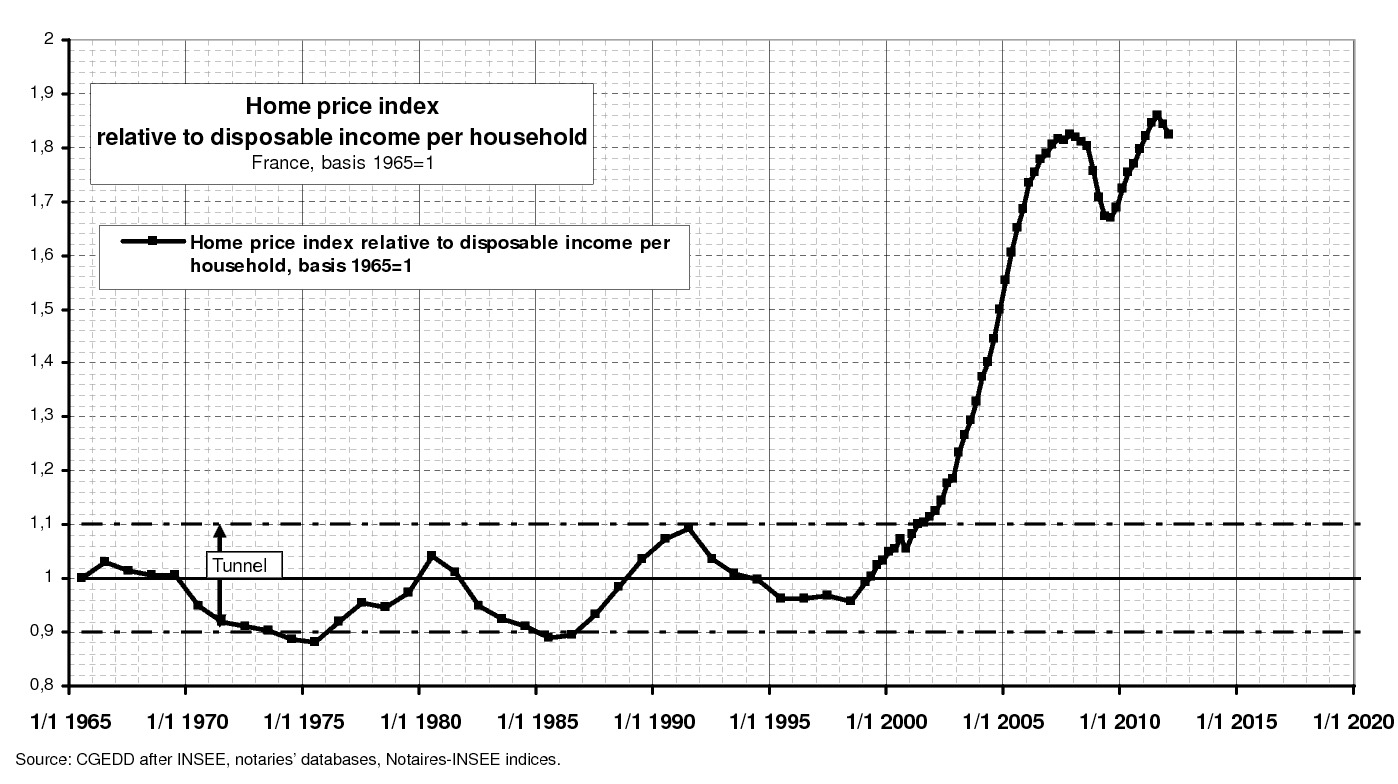

Nevertheless and heuristically, let us just consider the example of the home price index relative to disposable income per household in France from 1995 to 2013 shown in Figure 8. Consider for the logarithm of the quantity displayed in this picture, since it is a ratio and not a difference as wanted in the introduction. If we assume that the modeling of speculation presented in Section 1.1 can be applied to this case, it seems that the coefficients , and valid for the epoch 1965-1998 are not the same as those for 1998-2013. For simplicity, let us make the hypothesis that did not change (the resolution is too coarse to check that) and call , and , the respective values of and . That can be explained by the fact that the conditions were more favorable for buying in the second epoch, especially due to low interest rates. Furthermore one can argue that the advent of Internet has probably modified the extend to which the agents have access to the past evolution of the prices, both in short and long terms. So its effect on is not a priori clear (recall that should be proportional to the mean length of the backward time window). To get a rough idea, we can proceed as follows. Let , and . Figure 8 suggests that between and there were 3 periods under the coefficients , and and that between and there was one quarter of a period under the coefficients , and (except if the equilibrium price has itself changed and that the evolution between 2006 and 2012 is interpreted as one period and half of a new epoch). It follows that and should respectively be proportional to and . Since we do not plan to be very precise, let us make the assumption that and that , so that , and

where

To deduce another equation, let us believe that an ergodic theorem takes place very rapidly (permitted by the non reversibility of the process). Thus according to Remark 2.1, we would get

(more carefully, an empirical variance should be computed), and it follows that

where

can be computed numerically on Figure 8. We deduce that

Numerically, we obtain that , so it would seem that the advent of Internet has led people to rather use more recent trend of the housing market to make their speculation.

At last, using the lower bound obtained in Theorem 4, we may postulate that the probability that the index price hits the equilibrium level (see Figure 8) before year 2017 (which corresponds to an average annual loss of around ) is at least . We can thus wonder if the famous kiss landing generally announced by estate agents may not more probably end in a crash …

Appendix A On the persistence rate

Our goal here is to prove the existence of the quasi-stationary distribution and its persistence rate, as alluded to in Remark 1.2. It is based on general considerations relegated in this appendix because they do not lead to explicit estimates such as (19), which are more important from a practical point of view than the mere existence of . Furthermore, these a priori bounds will be useful in the development to follow.

Recall that and let be its boundary. We are interested in , the realization on of the differential operator given by (13) with Dirichlet boundary condition on . From a probabilist point of view, it is constructed in the following way. For any , let be a diffusion process whose evolution is dictated by and whose initial condition is . Starting from , can be obtained by solving the stochastic differential equation (7) with coefficients given by (12). Let be the stopping time defined by (17), namely

For any , any and any measurable and bounded function defined on , consider

| (98) |

Recall that is the invariant Gaussian probability measure of and denote by its restriction to . Then can be extended into a contraction operator on . Indeed, let be the full operator associated to : any and any measurable and bounded function defined on , we have

| (99) |

Since is invariant for , for any measurable and bounded function defined on (which can also be seen as a function on by assuming that it vanishes outside ), we get by Cauchy-Schwarz inequality,

This bound enables to extend as a contraction on . The Markov property implies that is a semi-group, which is easily seen to be continuous in . The operator is then defined as the generator of this semi-group (in the Hille-Yoshida sense): its domain is the dense subspace of consisting of functions such that converges in as goes to and the limit is by definition.

The spectrum of admits a smallest element (in modulus) . It is a positive real number and the main objective of this appendix is to justify the assertions made in Remark 1.2. We begin by being more precise about the existence of :

Proposition 37

There exists a number and two functions , which are positive on , such that

where is operator adjoint of in .

Essentially, this result is a consequence of the Krein-Rutman theorem (which is an infinite version of the Perron-Frobenius theorem, see for instance the paper [8] of Du) and the fact that the eigenfunctions belong to instead of comes from the hyperboundedness of the underlying Dirichlet semi-group.

The rigorous proof relies on a simple technical lemma about the kernels of the operators for . To check their existence, we first come back to for a given : from the computations of Section 2, this operator is indeed given by a kernel

where

| (100) |

with

It follows easily from (98) and (99) that the same is true for : there exists a function such that

and satisfying

| (101) |

More refined arguments based on the hypoellipticity of enable to see that the mapping is continuous and positive on . We can now state a simple but crucial observation:

Lemma 38

For any , there exists a time such that

Proof

From (101), it is sufficient to prove that

and this can be obtained without difficulty from (100) and from the explicit computations of of and of presented in Section 2.

We can now come to the

Proof of Proposition 37

We begin by applying Lemma 38 with to find some such that for we have

which implies that is of Hilbert-Schmidt class and thus a compact operator. Note furthermore that the spectral radius of is positive for all . Indeed, this feature can be deduced from the second bound of Theorem 4, which implies that for all , . Thus we are in position to apply Krein-Rutman theorem (see Theorems 1.1 and 1.2 of Du [8], where the abstract Banach space should be and the cone should consist of the nonnegative elements of ): if is the spectrum radius of , then there exists a positive function such that . This property characterizes and (up to a constant factor): if is a positive real and if is a positive function such that then is and is proportional to . This suggests to consider the renormalization , so that is uniquely determined (being positive). From the previous property, we deduce that for all and all , and . Indeed, it is sufficient to note that

We deduce that for any , and : write with and note that and similarly . Let us define . Since and is included in the domain of , we have . Furthermore from the general Hille-Yoshida theory we have in ,

Thus considering of the form with going to zero, we deduce that

It remains to set . Since is the spectral norm of the contraction operator , it appears that . The first bound of Theorem 4 enables to check that : from Cauchy-Schwarz inequality, we get that for all and all ,

it follows that

So the norm operator of satisfies

| (102) |

which itself is strictly less than 1 for large enough. Up to the choice of such a in the above arguments, we conclude that .

Let us now check that , since a priori we only know that . This is due to the hyperboundedness of . Let be given and a corresponding such that the conclusion of Lemma 38 is satisfied. Let be given. Cauchy-Schwarz and Hölder inequalities imply that for all and all ,

Integrating this bound with respect to , it follows that

namely send continuously into . If furthermore is of the form with , we get from that belongs to .

The same arguments are also valid for the adjoint semigroup . Its elements for admit the kernels where

We end up with the same quantity , since for any the operators and have the same spectral radius.

Let be the probability measure on which admits as density with respect to . Next result shows the validity of (18):

Proposition 39

The probability measure is a quasi-stationary distribution for and under , is distributed as an exponential law of parameter .

Proof

Let a test function be given. We compute that for all ,

By integration it follows that

at least for , but by usual approximation procedures, this can be extended to any which is measurable and bounded (or nonnegative). This means that is a quasi-stationary distribution for with rate . In particular with , we get

which amounts to being distributed as an exponential law of parameter under .

The bounds (19) are now easy to deduce. Indeed recalling the definition of in terms of given in the proof of Proposition 37 (and the fact that can be chosen arbitrary large), we get from the first bound of Theorem 4 that .

The second bound of Theorem 4 applied with gives that .

Remark 40 Is the unique quasi-stationary probability measure associated to ? A priori one has to be careful since this is wrong for the usual one-dimensional Ornstein-Uhlenbeck process with respect to a half-line. Nevertheless we believe there is uniqueness in our situation, because it is easy for the underlying process to get out of uniformly over the starting point (as shown by the first bound of Theorem 4) and this should be a sufficient condition (in the spirit of Section 7.7 of the book [6] of Collet, Martínez and San Martín, which unfortunately only treat the case of one-dimensional diffusions). At least from the uniqueness statement included in Krein-Rutman theorem (cf. again Theorem 1.2 of Du [8]), we deduce that is the unique quasi-stationary measure admitting a density with respect to which is in . By hyperboundedness of , the latter condition can be relaxed by only requiring that the density belongs to .

Appendix B Computations in polar coordinates

For the sake of completeness, we give below a series of elementary but tedious computations which are omitted in Section 3. We start with the proof of (48) and (53)

Proposition 41

Proof

First, write . Using that