Efficient goodness-of-fit tests in multi-dimensional vine copula models

Abstract

We introduce a new goodness-of-fit test for regular vine (R-vine) copula models, a flexible class of multivariate copulas based on a pair-copula construction (PCC). The test arises from the information matrix ratio. The corresponding test statistic is derived and its asymptotic normality is proven. The test’s power is investigated and compared to 14 other goodness-of-fit tests, adapted from the bivariate copula case, in a high dimensional setting. The extensive simulation study shows the excellent performance with respect to size and power as well as the superiority of the information matrix ratio based test against most other goodness-of-fit tests. The best performing tests are applied to a portfolio of stock indices and their related volatility indices validating different R-vine specifications.

keywords:

copula , goodness-of-fit tests , information matrix ratio test , power comparison , R-vine1 Introduction

Analyzing complex correlated data has received considerable attention in the current statistical literature. Among many approaches to modeling correlation structures, copula based models offer a powerful and flexible toolbox to characterize dependence profiles among variables, which have been studied extensively. However, it is unfortunate that there is little progress known in the theory and method concerning a goodness-of-fit (GOF) test, an important aspect of statistical model diagnostics. In fact, most of the published work has been only focused on bivariate copula models (see for example Genest et al., 2009).

Copulas join marginal distributions of a (continuous) random vector with their dependency structure by a joint cumulative distribution function (cdf) . Here is the unique cdf with uniform margins on the unit hypercube (Sklar, 1959). Classical copula classes such as the elliptical or Archimedean copulas are very limited with respect to flexibility in higher dimensions. But they are very powerful and well understood in the bivariate case. Thus Joe (1996) and later Bedford and Cooke (2001, 2002) independently constructed multivariate densities using bivariate copulas. They permit flexibility and feasibility of constructing and computing a relatively large dimensional copula model. In Aas et al. (2009) this process is termed a pair-copula construction (PCC) and the statistical inference is developed for it. Since then the theory of vine copulas arising from the PCC were studied in literature (see for example Czado, 2010; Stöber and Schepsmeier, 2013; Czado et al., 2012; Dißmann et al., 2013).

Along with the break through of vine copula constructions model diagnosis becomes ever so imperative in the application of multi-dimensional vine copulas. Developing efficient GOF tests is now a timely task as already noted in Fermanian (2012), and an important addition to the current literature of vine copulas. In addition, comprehensive comparisons for many of the classical GOF tests are lacking in terms of their relative merits when they are applied to multi-dimensional copulas. So far model verification methods for vine copulas are usually based on the likelihood, or on the Akaike Information Criterion (AIC) or Bayesian Information Criterion (BIC) as classical comparison measures, which take the model complexity into account.

In our goodness-of-fit (GOF) tests we would like to test

| (1) |

where denotes the (vine) copula distribution function and is a class of parametric (vine) copulas with being the parameter space of dimension .

For the elliptical and parametric Archimedean copulas many GOF tests were studied in the literature (Genest et al., 2006, 2009; Berg, 2009; Huang and Prokhorov, 2011). However, a GOF test for vine copula models verifying the chosen pair-copula families has, to our knowledge, only be treated in Schepsmeier (2013). Although, already Aas et al. (2009) suggested a GOF test for vine copulas based on the multivariate probability integral transformation (PIT) of Rosenblatt (1952) given in the appendix, but never investigated its small sample performance. We will show that this test and many other copula GOF tests have little to no power in the high dimensional setting of a vine and thus are not appropriate to be utilized there.

The main contribution of this paper is a new GOF test to perform model verification of vine copula models using hypothesis tests. As in Schepsmeier (2013) it is based on the Bartlett identity () as generally suggested by White (1982). Here is the expected Hessian or variability matrix, and is the expected outer product of the gradient or sensitivity matrix. In contrast to the White test, which relies on the difference between and , our new test is based on the information matrix ratio (IMR), (Zhou et al., 2012).

First, the IMR based test statistic for vine models will be derived and its asymptotic normality under the Bartlett identity will be proven. Secondly, the small sample performance for size and power will be investigated and compared to 14 other GOF tests for vines in a high dimensional setting ( and ). In particular, we will compare to GOF tests based on the

-

1.

difference of Bartlett identity or

-

2.

empirical copula process , with ,

(2) and being the copula with estimated parameter(s) , and/or

-

3.

multivariate PIT.

For the tests based on the multivariate PIT aggregation to univariate test data is facilitated using different aggregation functions. For the univariate test data then standard univariate GOF test statistics such as Anderson-Darling (AD), Cramér-von Mises (CvM) and Kolmogorov-Smirnov (KS) are used. In contrast, the empirical copula process (ECP) based test use the multivariate Cramér-von Mises (mCvM) and multivariate Kolmogorov-Smirnov (mKS) test statistics. The different GOF tests are given in the appendix for the convenience of the reader.

The power study will expose that the information based GOF tests such as the information matrix difference approach of Schepsmeier (2013) and in particular our new IMR based test outperform the other GOF tests in terms of size and power. The PIT based GOF tests reveal little to no power against the considered alternatives. But applying the PIT transformed data to the empirical copula process, as first suggested by Genest et al. (2009), is more promising. Here is replaced by the independence copula in the ECP.

The remainder of this paper is structured as follows: Section 2 gives an introduction on vine copula models. The new proposed IR test is introduced and its test statistics derived in Section 3. Additionally the asymptotic normality of the test statistic is proven. Further GOF tests extended from known copula GOF tests are given in Section 4 for the extensive power comparison study in Section 5 investigating their size and power. An application of an 8-dimensional portfolio of stock indices and their related volatility indices is performed in Section 6 comparing different vine specifications and proposed GOF tests. The final Section 7 summarizes and shows areas of further research.

2 Regular vine copula model

Pair-copula constructions (PCC) are a very flexible way to model multivariate distributions with copulas. The model is based on the decomposition of the -dimensional density into (conditional) bivariate copula densities. Bedford and Cooke (2001, 2002) introduced linked trees , where denotes the set of nodes while represents the set of edges, which helps to organize the vine construction. The following conditions have to be fulfilled to call a sequence of trees a vine:

-

1.

is a tree with nodes and edges .

-

2.

For , is a tree with nodes and edges .

-

3.

If two nodes in tree are joined by an edge, the corresponding edges in must share a common node (proximity condition).

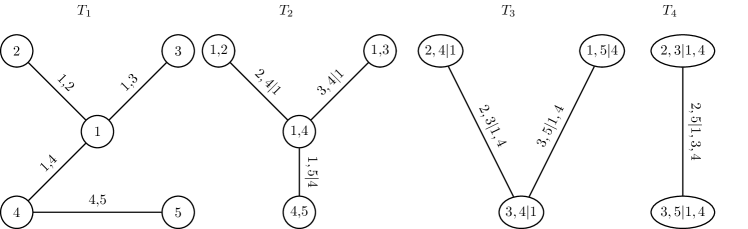

An example of a vine tree sequence is given in Figure 1. Here and forming the unconditional pair-copulas. The conditional pair-copulas are the edges of tree 2-4. The complete construction of the joint density is given in Example 1.

Following the notation of Czado (2010) we define a set of bivariate copula densities corresponding to edges in , for . Here denotes the subvector of determined by the set of indices in . The set is called the conditioning set while the indices and form the conditioned set. Then a -dimensional regular vine copula density can be constructed as

| (3) |

For the copula arguments, the conditional cdfs

and

, Joe (1996) developed a formula derived from the first derivative of the corresponding cdf with respect to the second copula argument, i.e.

| (4) |

Here is an index chosen from the conditioning set, such that is in . In the literature Equation (4) is often called a h-function. It is a recursive function which simplifies the calculation of the density or log-likelihood considerably. See for example Dißmann et al. (2013) for a algorithmic presentation of the log-likelihood of an R-vine. Denoting the pair-copula parameters of with a vine copula model with density given in (3) is abbreviated as . We assume that the copula does not depend on the values , i.e. on the conditioning set without the chosen variable . This is called the simplifying assumption.

Example 1 (5-dim pair-copula construction)

The corresponding copula density to the vine tree sequence given in Figure 1 can be expressed as

| (5) |

There are two special cases of an R-vine tree structure . A line like structure of the trees is called D-vine in which each node has a maximum degree of 2, while a star structure is a canonical vine (C-vine) with a root node of degree . All other nodes have degree 1. Statistical inference methods of D-vines are discussed in Aas et al. (2009). A model selection algorithm as well as the maximum likelihood parameter estimation for C-vines is developed in Czado et al. (2012).

3 Information matrix ratio test

A new approach for a GOF test for vine copulas is the information ratio (IR) test. It is inspired by the paper of Zhou et al. (2012), who propose an IR test for general model misspecification of the variance or covariance structures. Their test is related to the “in-and-out-sample” (IOS) test of Presnell and Boos (2004), which is a likelihood ratio test. Additionally Presnell and Boos (2004) showed that the IOS test statistic can be expressed as a ratio of the expected Hessian and the expected outer product of the gradient. In particular, let be a random vector with copula distribution function . Further let

| (6) |

the expected Hessian matrix of the random (vine) copula log-likelihood function and the expected outer product of the corresponding score function, respectively. Here denotes the derivative with respect to the copula parameter . Now the information matrix ratio (IMR) is defined as

| (7) |

Our test problem is the reformulated general test problem of White (1982):

where is the -dimensional identity matrix. To calculate the corresponding test statistic we follow Schepsmeier (2013) and define the random matrices

| (8) |

using the log-likelihood function of the model with specified vine tree sequence and pair-copulas but unknown parameter . Given an i.i.d. sample from for and the corresponding maximum likelihood estimate based on the sample counter parts are

respectively. The sample equivalents to and are then

| (9) |

Thus, we get as empirical version of (7):

As in Zhou et al. (2012) we define the information ratio (IR) statistic as

| (10) |

where denotes the trace of matrix . To derive the asymptotic normality of the test statistic some conditions have to be set. The first two conditions and guarantee the existence of the gradient and the Hessian matrix.

-

The density function (3) is twice continuous differentiable with respect to .

-

- and are positive definite.

Condition are more technical and are the same as in Presnell and Boos (2004).

-

There exist such that as .

-

The estimator has an approximating influence curve function such that

where as , , and is finite.

-

The real-valued function possesses second order partial derivatives with respect to , and

-

(a)

and are finite.

-

(b)

There exists a function such that for all in a neighborhood of and all , where .

-

(a)

In the following represents the vectorization of the symmetric matrix . Let , then Presnell and Boos (2004) showed that

where is the mean vector and is the asymptotic covariance matrix of . Here is the -dimensional zero vector and is the -dimensional identity matrix. Furthermore, let define the partial derivatives of taken with respect to the components of , i.e.

Theorem 1

Let satisfy the conditions . Further, let hold for the maximum likelihood estimator with . Additionally, the condition has to be satisfied for both and for each . Then the IR test statistic

where is the standard error of the IR test statistic, defined as

Here is the asymptotic covariance matrix arising from the joint asymptotic normality of and defined above. By we denote the -dimensional vector of partial derivatives of taken with respect to the components of and evaluated at their limits in probability, i.e. .

Proof

Since the theoretical asymptotic variance is quite difficult to compute, an empirical version is used in practice. To evaluate the standard error numerically, Zhou et al. (2012) suggest a perturbation resampling approach. Furthermore, Presnell and Boos (2004) state that the convergence to normality is slow and thus they suggest obtaining p-values using a parametric bootstrap under the null hypothesis.

The condition for implies, that the copula density function (3) is four times differentiable with respect to . Furthermore, the first and second moment of the second derivative has to be finite. The vine copula density is four times differentiable if all selected pair-copulas are four times differentiable. These assumptions are satisfied for the elliptical Gauss and Student’s t-copula as well as for the parametric Archimedean copulas in all dimensions.

Let and as in Theorem 1. Then the test

is an asymptotic -level test. Here denotes the quantile of a -distribution.

4 Further goodness-of-fit tests for vine copulas

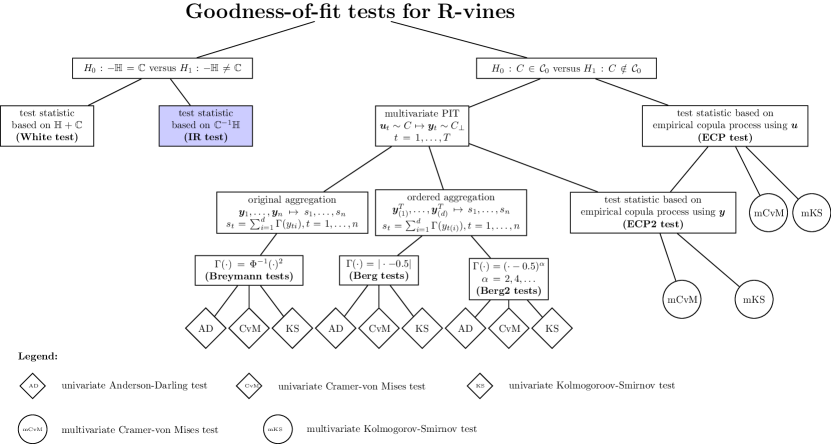

In the recent years many GOF test were suggested for copulas. The most promising ones were investigated in Genest et al. (2009) and Berg (2009). However only the size and power of the elliptical and one-parametric Archimedean copulas for were analyzed. The multivariate case is therefore poorly addressed. For vine copulas little is done. A first test for vine copulas was suggested but not investigated in Aas et al. (2009). Their GOF is based on the multivariate PIT and an aggregation introduced by Breymann et al. (2003). After aggregation standard univariate GOF tests such as the Anderson-Darling (AD), the Cramér-von Mises (CvM) or the Kolmogorov-Smirnov (KS) tests are applied. They are described in more detail in B. We will denote the resulting tests as Breymann.

Similar approaches based on the multivariate PIT are proposed by Berg and Bakken (2007). Beside new aggregation functions forming univariate test data, they perform the aggregation step on the ordered PIT output data instead of . Again standard univariate GOF tests are applied. These approaches will be called Berg and Berg2, respectively.

Berg and Aas (2009) applied a test for against based on the empirical copula process (ECP) to a 4-dimensional vine copula. As the Breymann test, their GOF test is not described in detail or investigated with respect to its power. We will denote this test as ECP. An extension of the ECP-test is the combination of the multivariate PIT approach with the ECP. The general idea is that the transformed data of a multivariate PIT should be “close” to the independence copula Genest et al. (2009). Thus a distance of CvM or KS type between them is considered. This approach is called ECP2.

Schepsmeier (2013) was the first who analyzed the power of a GOF test for vine copulas in detail. His approach is, as our new IR GOF test, based on the information matrix equality and specification test introduced by White (1982). His power studies show, that the convergence to the asymptotic distribution function of the test statistic is very slow. Further, given copula data with sample size smaller than 10000 the test does not reach its nominal level based on asymptotic p-values. But using bootstrapped p-values the test shows very good power behavior. We denote this approach as White.

In the forthcoming sections we will introduce the vine copula test of Schepsmeier (2013), the multivariate PIT based GOF such as the ones of Breymann et al. (2003) and Berg and Bakken (2007), and the two ECP based GOF tests. A first overview of the considered GOF tests is given in Figure 2.

4.1 White’s information matrix test

The GOF test of Schepsmeier (2013) uses White’s information matrix equality and specification test. It is a rank-based test which is asymptotically pivotal, i.e. the asymptotic distribution is independent of model parameters.

Let be a random vector with vine copula log-likelihood . Further let and be defined as in Equation (6) the expected Hessian matrix and the expected outer product of the score function, respectively. Considering the Bartlett identity we can formulate the vine copula misspecification test problem as

| (11) |

Here, denotes the true value of the vine copula parameter vector. Following the notation of Schepsmeier (2013) we denote by the vectorized sum of and defined in (8). Its empirical version is denoted by , where and are defined in (9). Further, we define the expected gradient matrix of the random vector as

Now, under suitable regularity conditions (A1-A10 in White, 1982), assuring that is a continuous measurable function and its derivatives exist, the following is shown. Given a copula model (Huang and Prokhorov, 2011) or a vine copula model (Schepsmeier, 2013), the asymptotic covariance matrix of is given by

Here, is again the maximum likelihood estimate of given i.i.d. samples. For details on the estimation of and we refer to Schepsmeier (2013).

Thus, the test statistic of the White test is

| (12) |

where is the estimated asymptotic variance matrix given observation.

The test statistic follows asymptoticly a distributed random variable with degrees-of-freedom , where is the number of vine copula parameters. But Schepsmeier (2013) showed that even for small dimensions the asymptotic theory does not hold for relative large data sets, for example in 5 dimensions. However for bootstrapped p-values the power is quite satisfying, i.e. the tests has power against false vine copula model specifications. Denoting the quantile of the distribution by the White test rejects the null hypothesis (11) if . In the bootstrapped case the distribution is replaced by the empirical distribution function of the bootstrapped test statistics.

4.2 Rosenblatt’s transform tests

The vine copula GOF test suggested by Aas et al. (2009) is based on the multivariate probability integral transform (PIT) of Rosenblatt (1952) applied to copula data and a given estimated vine copula model . The general multivariate PIT definition and the explicit algorithm for the R-vine copula model is given in A. The PIT output data is assumed to be i.i.d. with for . Now, a common approach in multivariate GOF testing is dimension reduction. Here the aggregation is performed by

| (13) |

with a weighting function .

Breymann et al. (2003) suggest as weight function the squared quantile of the standard normal distribution, i.e. , with denoting the cdf. Finally, they apply a univariate Anderson-Darling test to the univariate test data . The three step procedure is summarized in Figure 3.

Berg and Bakken (2007) point out that the approach of Breymann et al. (2003) has some weaknesses and limitations. The weighting function strongly weights data along the boundaries of the -dimensional unit hypercube. They suggest a generalization and extension of the PIT approach. First, they propose two new weighting functions for the aggregation in (13):

Further, they use the order statistics of the random vector , denoted by with observed values . The calculation of the order statistics PIT can be simplified by using the fact that are i.i.d. random variables and is a Markov chain (David, 1981, Theorem 2.7). Now Theorem 1 of Deheuvels (1984) can be applied and the calculation of the PIT ease to

| (14) |

Now, Berg and Bakken (2007) construct the aggregation as the sum of a product of two weighting functions applied to and , respectively, i.e.

Here and are chosen from the suggested weighting functions including the one of Breymann et al. (2003). Let be the corresponding random aggregation of . If and or vise versa, the asymptotic distribution of follows a distributed random variable (Breymann et al., 2003). In all other cases the asymptotic distribution of is unknown.

The combinations with and for performed very poorly in the simulation setup considered later. Thus we will not include them in the forthcoming power study. Only the weighting functions listed in Table 1 will be investigated. As final test statistics to the test data we apply the univariate Cramér-von Mises (CvM) or Kolmogorov-Smirnov (KS) test, as well as the mentioned univariate Anderson-Darling (AD) test. All three test statistics are given in B for the convenience of the reader.

| Short | Description | |

|---|---|---|

| Breymann | ||

| Berg | ||

| Berg2 | ||

Let and denote the quantile of the univariate AD, CvM or KS test statistic, respectively. Then the test rejects the null hypothesis (1) if or , respectively.

4.3 Empirical copula process tests

A rather different approach is suggested by Genest and Rémillard (2008) for copula GOF testing. They propose to use the difference of the copula distribution function with estimated parameter and the empirical copula (see Equation (2)) given the copula data . This stochastic process is known as the empirical copula process (ECP) and will be used to test (1). For a vine copula model the copula distribution function is not given in closed form. Thus a bootstrapped version has to be used.

Now, the ECP is utilized in a multivariate Cramér-von Mises (mCvM) or multivariate Kolmogorov-Smirnov (mKS) based test statistic. The multivariate distribution functions and in Equation (18) and (19) of B.1 are replaced by their (vine) copula equivalents and , respectively. Thus we consider

To avoid the calculation/approximation of Genest et al. (2009) and other authors propose to use the transformed data of the PIT approach and plug them into the ECP. The idea is to calculate the distance between the empirical copula of the transformed data and the independence copula . Thus, the considered multivariate CvM and KS test statistics are

respectively. Since neither the mCvM nor the mKS test statistic has a known asymptotic distribution function a parametric bootstrap procedure has to be applied to estimate p-values. Thus a computer intensive double bootstrap procedure has to be implemented. As before the test rejects the null hypothesis (1) if or , respectively. Here and are the quantiles of the mCvM and mKS test statistic’s empirical distribution function, respectively. Similar rejection regions are defined for the ECP2 test statistics.

5 Power study

To investigate the power behavior of the proposed GOF tests and to compare them to each other we conduct several Monte Carlo studies of different dimension. The second property of interest is the ability of the test to maintain the nominal level or size, usually chosen at 5%.

If a test has the probability of rejection less than or equal to a small number , called the level of significance, for the hypothesis , then such a test is called a -level test. We speak of rejecting at level . Common values for are 0.05 and 0.01. Since a test of level is also a test of level , the smallest such is called size of the test and is the maximum probability of type I error (Bickel and Doksum, 2007, p.217). The power of a test against the alternative is the probability of rejecting when is true. It is often denoted as .

Given an observed test statistic of the corresponding p-value is defined as

Here represents one of the test statistics (White), (IR), (AD), (CvM or mCvM) and (KS or mKS) introduced in Section 3 and 4.

For a given model consider the random statistic based on an i.i.d. sample of size from model with observed value . Define the random variable which takes on values in . Let denote the distribution function of , then is the actual size of the test at level (nominal size). A test maintains its nominal level if . As estimates of the p-value and the distribution function we use their empirical versions. Therefore generate bootstrap realizations of the test statistic , denoted as , when observations are drawn from model .Then the estimate of is given as

Further, the estimated size at level is defined as Generating i.i.d. data sets of an alternative model in to estimate by we get the power of the test when the alternative holds.

5.1 General simulation setup

For the general simulation setup we follow the procedure of Schepsmeier (2013). Given a vine copula model we test for each proposed GOF test if it has suitable power against an alternative vine copula model , where , as follows:

In all of the forthcoming simulation studies we used replications and the number of observations were chosen to be or . As model dimension we chose and and the critical level is . Possible pair-copula families in the investigated vine copula models are the elliptical Gauss and Student’s t-copula, the Archimedean Clayton, Gumbel, Frank and Joe copula, and their rotated versions. Further, all calculations are performed using the statistical software R111R Development Core Team (2012). R: A language and environment for statistical computing. R Foundation for Statistical Computing, Vienna, Austria. ISBN 3-900051-07-0, URL http://www.R-project.org/. and the R-package VineCopula of Schepsmeier et al. (2012).

5.2 Test specification

In our power study we investigate the size and power behavior of the proposed GOF tests given an R-vine as true model () with respect to the alternatives

-

1.

multivariate Gauss copula,

-

2.

C-vine copula and

-

3.

D-vine copula.

Details on the R-vine structure (Figure 1), the chosen pair-copula families and copula parameters for are given in Table 5 in C. For the 8 dimensional example we refer to Table 6 of C.

The estimated C- and D-vine structures ( and ) are given in Equation (22) and (23) of C, respectively. The structure selection of the D-vine copula is facilitated by solving a traveling salesman algorithm while the root order of the C-vine model follows the heuristic of Czado et al. (2012). The assignment of the pair-copula families in the C- and D-vine uses AIC as suggested and validated in Brechmann (2010). The last alternative copula model is the multivariate Gauss copula, which can be formulated as a vine copula as well (see Czado, 2010). In the Gaussian case the conditional correlation parameters, which form the pair-copula parameters, are equal to the partial correlation parameters. They can be calculated recursively using the entries of the multivariate Gauss copula variance-covariance matrix.

Although all three stated alternatives have different vine structures and pair-copula families we do not know which vine copula model is “closer” to the true R-vine model. A often proposed approach for model comparison is the Kullback and Leibler (1951) information criterion (KLIC). It measures the distance between a true unknown distribution and a specified, but estimated model. In the following definition we follow Vuong (1989). Let be the true (vine) copula density function of a -dimensional random vector . Further, denotes the expected value with respect to this true distribution. The estimated (vine) copula density of is denoted as , where is the estimated model parameter (vector) given samples of . Then, the KLIC between and is defined as

The model with the smallest KLIC is “closest” to the true model. In the plots of the following power study we ordered the alternatives on the x-axis by their KLIC as listed in Table 2, e.g. for we have the order D-vine, C-vine, Gauss.

The approximation of the multidimensional integral is facilitated by Monte Carlo or a numerical integration based on the R package cubature (C code by Steven G. Johnson and R by Balasubramanian Narasimhan, 2011). In the numerical integration copula data, i.e. , or standard normal transformed data, i.e. , are used. We see that it is quite challenging to estimate the KLIC distance in high dimensions.

| d | method | C-vine | D-vine | Gauss |

|---|---|---|---|---|

| 5 | Monte Carlo | 0.65 | 0.64 | 0.72 |

| numerical integration based on copula margins | 0.6211footnotemark: 1 | 0.4511footnotemark: 1 | 0.7111footnotemark: 1 | |

| numerical integration based on normal margins | 0.4811footnotemark: 1 | 0.5111footnotemark: 1 | 0.5011footnotemark: 1 | |

| 8 | Monte Carlo | 1.66 | 0.13 | 0.73 |

| numerical integration based on copula margins | 1.4622footnotemark: 2 | 1.2922footnotemark: 2 | 1.9122footnotemark: 2 | |

| numerical integration based on normal margins | 2.1533footnotemark: 3 | 3.2033footnotemark: 3 | 2.1433footnotemark: 3 |

5.3 Results

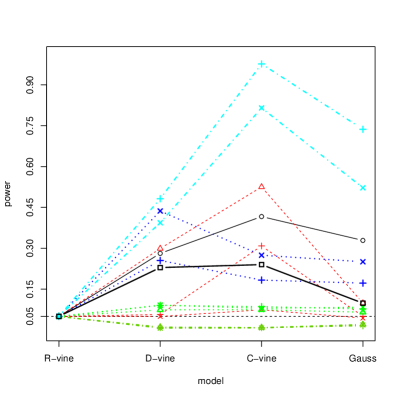

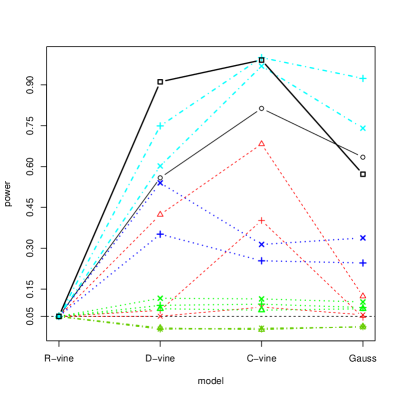

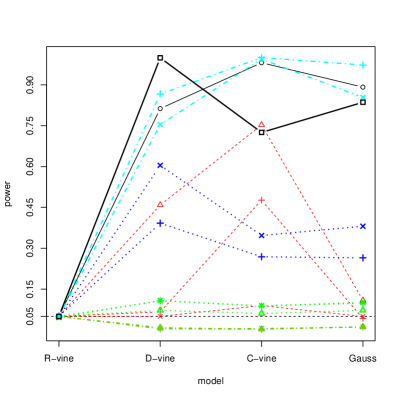

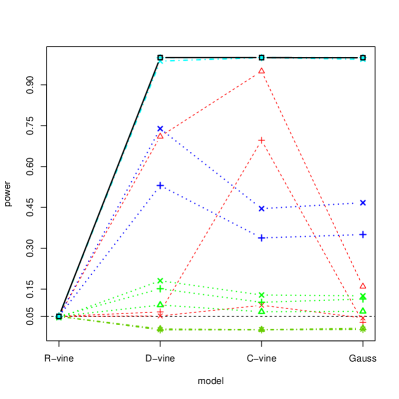

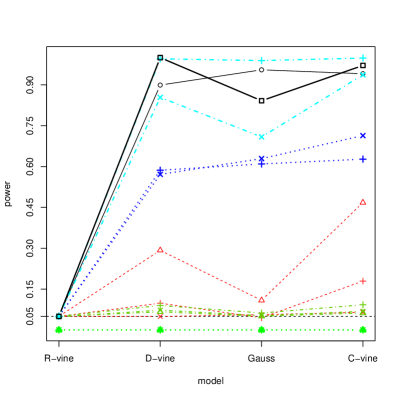

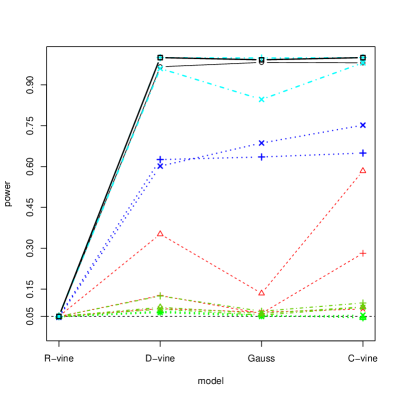

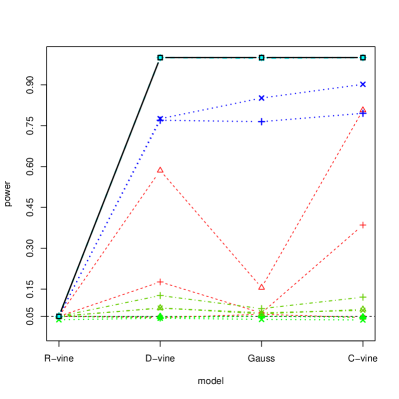

Since all proposed GOF tests have either no asymptotic distribution at all or face substantial numerical problems estimating the asymptotic variance or have shown to have low power in small samples, we only investigate the bootstrapped version of the tests. In the Figures 4 and 5 we illustrate the estimated power of all 15 proposed GOF tests for and , respectively. On the x-axis we have the R-vine as true model and the three alternatives ordered by their KLIC. For the true model the actual size is plotted. A horizontal black dashed line indicates the 5% -level.

Size: All proposed GOF tests maintain their given size independently of the number of sample points for . In the 8-dimensional case the GOF tests based on the Berg approaches do not maintain their nominal size in case of and . All other GOF tests do hold the level and thus control the type I error.

Sample size effects on power: We have increasing power with increasing sample size for the White, IR, ECP, ECP2 and Breymann (in combination with the AD test statistic) GOF test. The tests based on Berg and Berg2 have no or very low power independently of the number of observations. This is also true for the Breymann GOF test in combination with the univariate CvM and KS test statistics. In eight dimensions the number of sample points are important for the IR test since the tests has very small power considering only 500 data points. In five dimensions the effect is not that eye-catching but can be found too. Almost independent from the the number of sample points is the ordering of the test by their power. In all test scenarios the ECP2 test with mCvM test statistic outperforms the others, followed by the IR test, the test based on White and the ECP2 test based on the mKS test statistic. The next GOF tests are the tests based on the ECP and the Breymann transformation with AD test statistic.

Dimension effect on the power: The power of the top four GOF tests (IR, White, ECP and ECP2) are almost independent of the dimension. Only in the case of sample points a clearly increase of power can be observed from to dimensions. For the weaker tests the reverse is true. With increasing dimension the Breymann GOF test decreases in power. The Berg and Berg2 tests are independently of the dimension.

Effect of alternatives on the power: The results with respect to the KLIC are two-fold. For the power increases with increasing KLIC for the most GOF tests except for the Gauss copula in . For it is again the multivariate Gauss copula which is out of line for many of the tests. The exceptions are the ECP tests. For the power of the four “good” tests mentioned before increases with KLIC. Some of them have even a power of 100%. The Breymann test is conspicuous, since the test is working quite well for the C- and D-vine alternative but is relatively poor for the multivariate Gaussian copula independent of the dimension or sample size. While the Breymann tests have much lower power than the four best GOF tests, they still have power to distinguish between the null and alternative models.

Effects of the test functionals on power: For ECP, ECP2 or Breymann tests it appears that CvM based test statistics are more powerful than the KS type test statistics. This is in line with Genest et al. (2009) for bivariate copula GOF tests.

The poor performance of the Breymann, Berg and Berg2 approach was also recognized in the comparison studies of Genest et al. (2009) in the bivariate case and in Berg (2009) for copulas of dimension 2, 4 and 8. The analyzed copulas in Berg (2009) were the Gauss, Student’s t, Clayton, Gumbel and Frank copula. But there the test statistics maintained their nominal level and had some explanatory power.

The bootstrapped p-values or power values stabilize fast for increasing bootstrap replications, for all GOF tests. This happens for 1000-1500 replications, irrespective of sample size or alternative. In many cases the stabilization is even faster.

Beside these last points, no clear hierarchy among the best performing proposed test statistics is recognizable. But some tests perform rather well while others do not even maintain their nominal level. In particular, our new IR test performs quite well in terms of power against false alternatives.

Of cause the computation time for the different proposed GOF tests is also a point of interest for practical applications. Therefore, in Table 3 the computation times in seconds for the different methods run on a Intel(R) Core(TM) i5-2450M CPU @ 2.50GHz computer for are given alongside with a summary of our findings. The computing time of the information matrix based methods White and IR are clearly higher than the other test statistics. Given the complex calculation of the R-vine gradient and Hessian matrix (see Stöber and Schepsmeier, 2013) this is not very surprising.

| White | Breymann | Berg | Berg2 | ECP | ECP2 | IR | |

| main idea | PIT+Aggregation+uniform test | PIT+ECP | |||||

| hold nominal level | + | + | + | + | + | ||

| power against | + | 0 | 0 | + | + | ||

| alternatives | (partly) | (partly) | |||||

| consistentency | + | + | + | ||||

| asymptotic | + | 0 | + | ||||

| distribution | (only for high n) | (proved to be | (not tested) | ||||

| incorrect) | |||||||

| complexity | 0 | + | 0 | + | |||

| (difficult cov. | (3 step procedure) | (2 step | |||||

| matrix) | procedure) | ||||||

| computation time | |||||||

| 3.41 | 0.06 | 0.06 | 0.07 | 0.08 | 0.06 | 1.66 | |

| 58.79 | 0.14 | 0.14 | 0.18 | 0.17 | 0.13 | 30.30 | |

6 Application

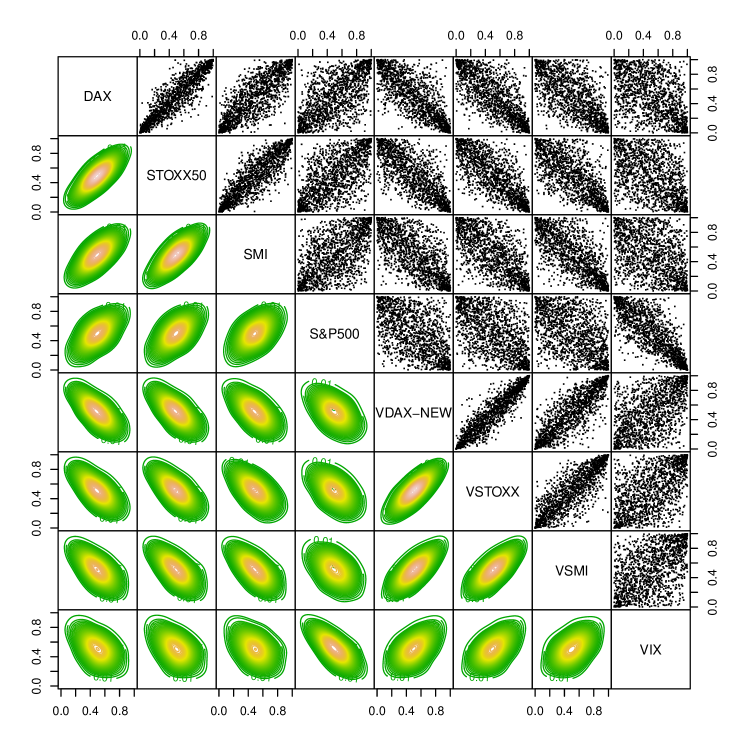

As application we consider a financial data set of four indices and their corresponding volatility indices, namely the German DAX and VDAX-NEW, the European EuroSTOXX50 and VSTOXX, the US S&P500 and VIX, and the Swiss SMI and VSMI. The daily data cover the time horizon of the current financial crisis starting at August, 9th, 2007 when a sharp increase of inter bank interest rates was noticed, until April 30th, 2013, resulting in 1405 data points. For each marginal time series we calculated the log-returns and modeled them with an AR(1)-GARCH(1,1) model using Student’s t innovations. The resulting standardized residuals are transformed using the non-parametric rank transformation (see Genest et al., 1995) to obtain copula data.

The contour and pair plots in Figure 6 reveal the expected elliptical positive dependence behavior among the indices and among the volatility indices. But between the indices and the volatilities a negative dependence can be observed. Furthermore, a slight asymmetric tail dependence is recognizable.

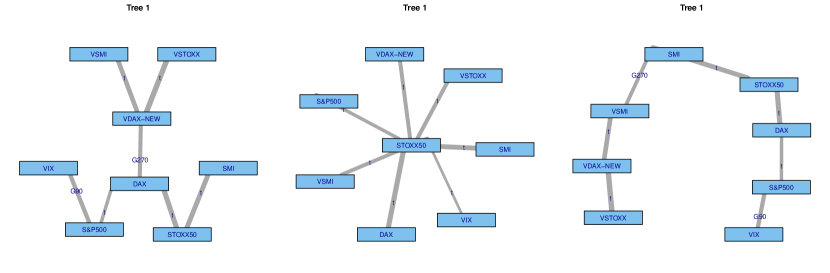

To model the dependence structure we investigated four models. In particular, an R-vine copula model, selected using the maximum spanning tree algorithm by Dißmann et al. (2013), a C-vine copula, selected by the heuristic proposed by Czado et al. (2012), a D-vine copula, selected using a traveling sales man algorithm, and a multivariate Gaussian copula. The corresponding first trees of the vine models are illustrated in Figure 7. For the R-vine copula as well as in the D-vine copula we can see that the indices and the volatilities cluster except for the US ones. The C-vine copula is too restrictive to recognize such groupings. Another interesting point is that the first tree structure of the R-vine is very close to the first tree structure of the D-vine. If we delete the edge “DAX-VDAX-NEW” and add a new edge “VSMI-SMI” in the R-vine we get the D-vine tree structure. Further, we see evidence of asymmetric tail dependence since (rotated) Gumbel copulas are selected.

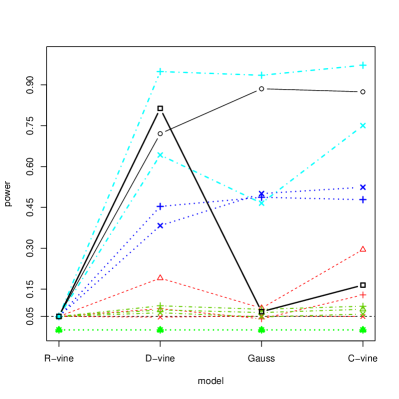

Performing a parametric bootstrap with most of the good performing proposed GOF tests, namely White, IR, ECP (with CvM) and ECP2 (with CvM), confirm that a vine copula model can not be rejected at a 5% significance level (see Table 4). Only the ECP2 approach returns a p-value of 0.01 below the chosen significance level of 0.05 for the estimated C-vine copula, and the White based test a pvalue for the estimated R-vine copula model. The multivariate Gauss copula is rejected by the White, the IR and ECP2 GOF test, while the ECP based test returns a p-value of 0.6. In 3 of 4 GOF tests the highest returned p-value is for the D-vine copula. But note that the size of the p-value or the ordering of the p-values do not give an ordering of the considered models.

As in the simulation study the GOF tests differ in their rejection decision and several GOF tests are needed to get a better picture of the better fitting model. The discrimination between the estimated vine copula models is even harder than in the power study. The MC-estimated KLIC of the R-vine to the C-vine is only 0.15, while the KLIC of the R-vine to the D-vine is even smaller (0.11). Even the multivariate Gauss copula has an estimated small KLIC with 0.31. Additional simulation studies based on the estimated vine copula models for show that the simulated power is quite small for all proposed GOF tests.

In terms of log-likelihood the D-vine is also the best fitting vine copula to the data unless the R-vine has a better AIC and BIC. The significant smaller number of parameters favors the R-vine compared to the D- or C-vine.

The economical interpretation of these findings is, that the assumption of multivariate Gaussian distributed random vectors is not fulfilled in times of financial and economic crises. More flexible models are needed to capture the asymmetric behaviors and tail dependencies. R-vines are able to model these properties as already shown in Brechmann and Czado (2013) or Stöber and Schepsmeier (2013).

| log-lik | #par | AIC | BIC | White | ECP | ECP2 | IR | |||

|---|---|---|---|---|---|---|---|---|---|---|

| CvM | KS | CvM | KS | |||||||

| R-vine | 7652 | 33 | -15238 | -15065 | 0.002 | 0.18 | 0.98 | 0.30 | 0.67 | 0.75 |

| C-vine | 7585 | 42 | -15086 | -14865 | 0.14 | 0.51 | 0.36 | 0.01 | 0.74 | |

| D-vine | 7654 | 41 | -15226 | -15011 | 0.41 | 0.82 | 0.24 | 0.55 | 0.67 | 0.52 |

| Gauss | 7320 | 28 | -14584 | -14445 | 0.60 | 0.28 | ||||

7 Discussion

We introduced a new GOF test for regular vine copula models based on the information matrix ratio. The calculation of the test statistic as well as its asymptotic distribution function showed up to be challenging. But good empirical approximations have been found as shown in an extensive power study. The study revealed good performance of the test in terms of power against false alternatives given simulated p-values. Given sufficient data points the test is even consistent. Furthermore, the new GOF test maintained always its nominal level, controlling the type I error, independently of sample size, dimension or alternative.

Since only Schepsmeier (2013) investigated a GOF test for R-vines so far, further GOF tests extended from the (bivariate) copula case are introduced to facilitate a wider comparison. In particular, 14 other GOF tests were explained and compared in a multi-dimensional setting. The small sample performance for size and power were analyzed for GOF tests based on the difference of the Bartlett identity, the empirical copula process and the multivariate PIT. This paper gives the first comparison study and review of vine copula GOF tests. The new IR test as well as the White test introduced by Schepsmeier (2013) and the ECP2 based tests of Genest et al. (2009) performed very well. They outperformed the tests based on the multivariate PIT. The PIT based tests revealed little power against the considered alternatives. In particular, the new IR GOF test performed best in several cases. Thus, the proposed GOF tests enable statisticians to conduct efficient model diagnostics using hypothesis tests in high dimensional settings.

Of cause further GOF tests already known for copulas can be extended to the vine copula case. But most of them will have crucial problems in higher dimensions. For example the likelihood ratio based GOF test or the Chi-squared type GOF test, both introduced for copulas in Dobrić and Schmid (2005), have to partition the unit hypercube. This will probably result in long computation time in high dimensions as well as the need of sufficient large number of observations. The Kendall’s process based GOF tests suggested by Berg and Aas (2009) need like the ECP based GOF tests a double bootstrap procedure since the Kendall’s process is not trackable for the vine copula. But this approach revealed good results in the comparison study of Genest et al. (2009) for bivariate copulas. Further suggestions for copula GOF tests are for example presented in Fermanian (2012).

A very interesting hybrid approach was suggested by Zhang et al. (2013). Since no GOF test outperforms in all cases a hybrid test is suggested. Given test statistics with sample size and controlling type I error for any given significance level under the null hypothesis the hybrid p-value is defined as

Here denote the p-values of the test statistics . They showed that the power function is bounded from below and if there is at least one test which is consistent, then the hybrid test is consistent. An extension to the vine copula case would be highly welcomed.

By testing the validity of the null hypothesis , where denotes the (vine) copula distribution function and is a class of parametric copulas one has to take the margins into account. As pointed out by Genest et al. (2009) the marginal distribution functions of the random variables can be considered as nuisance parameters. So far we always considered known margins. Thus an extension of the proposed GOF tests to unknown margins has to be considered in the future.

Acknowledgments

The author acknowledge substantial contributions by his colleagues of the research group of Prof. C. Czado at Technische Universität München and the support of the TUM Graduate School’s International School of Applied Mathematics. A special thanks goes to Peter Song for fruitful discussions. Numerical calculations were performed on a Linux cluster supported by DFG grant INST 95/919-1 FUGG.

References

- Aas et al. (2009) Aas, K., Czado, C., Frigessi, A., Bakken, H., 2009. Pair-copula construction of multiple dependence. Insurance: Mathematics and Economics 44, 182–198.

- Anderson and Darling (1954) Anderson, T.W., Darling, D.A., 1954. A test of goodness of fit. Journal of the American Statistical Association 49, 765–769.

- Bedford and Cooke (2001) Bedford, T., Cooke, R., 2001. Probability density decomposition for conditionally dependent random variables modeled by vines. Ann. Math. Artif. Intell. 32, 245–268.

- Bedford and Cooke (2002) Bedford, T., Cooke, R., 2002. Vines - a new graphical model for dependent random variables. Annals of Statistics 30, 1031–1068.

- Berg (2009) Berg, D., 2009. Copula goodness-of-fit testing: An overview and power comparison. The European Journal of Finance 15, 1466–4364.

- Berg and Aas (2009) Berg, D., Aas, K., 2009. Models for construction of multivariate dependence: A comparison study. The European Journal of Finance 15, 639–659.

- Berg and Bakken (2007) Berg, D., Bakken, H., 2007. A copula goodness-of-fit approach based on the conditional probability integral transformation. Http://www.danielberg.no/publications/Btest.pdf.

- Bickel and Doksum (2007) Bickel, P.J., Doksum, K.A., 2007. Mathematical Statistics: Basic Ideas and selected Topics. volume 1. Pearson Prentice Hall, Upper Saddle River. second edition.

- Brechmann (2010) Brechmann, E., 2010. Truncated and simplified regular vines and their applications. Diploma thesis. Center of Mathematical Sciences, Munich University of Technology. Garching bei München.

- Brechmann and Czado (2013) Brechmann, E.C., Czado, C., 2013. Risk management with high-dimensional vine copulas: An analysis of the Euro Stoxx 50. Statistics & Risk Modeling , forthcoming.

- Breymann et al. (2003) Breymann, W., Dias, A., Embrechts, P., 2003. Dependence structures for multivariate high-frequency data in finance. Quantitative Finance 3, 1–14.

- C code by Steven G. Johnson and R by Balasubramanian Narasimhan (2011) C code by Steven G. Johnson and R by Balasubramanian Narasimhan, 2011. cubature: Adaptive multivariate integration over hypercubes. R package version 1.1-1.

- Czado (2010) Czado, C., 2010. Pair-Copula Constructions of Multivariate Copulas, in: Jaworski, P. and Durante, F. and Härdle, W.K. and Rychlik, T (Ed.), Copula Theory and Its Applications, Lecture Notes in Statistics, Springer-Verlag, Berlin Heidelberg. pp. 93–109.

- Czado et al. (2012) Czado, C., Schepsmeier, U., Min, A., 2012. Maximum likelihood estimation of mixed C-vines with application to exchange rates. Statistical Modelling 12, 229–255.

- David (1981) David, H., 1981. Order statistics. Wiley series in probability and mathematical statistics. Applied probability and statistics, Wiley.

- Deheuvels (1984) Deheuvels, P., 1984. The characterization of distributions by order statistics and record values: A unified approach. Journal of Applied Probability 21, 326–334.

- Dißmann et al. (2013) Dißmann, J., Brechmann, E., Czado, C., Kurowicka, D., 2013. Selecting and estimating regular vine copulae and application to financial returns. Computational Statistics and Data Analysis 59, 52 – 69.

- Dobrić and Schmid (2005) Dobrić, J., Schmid, F., 2005. Testing goodness of fit for parametric families of copulas - application to financial data. Communications in Statistics - Simulation and Computation 34, 1053–1068.

- Fermanian (2012) Fermanian, J.D., 2012. An overview of the goodness-of-fit test problem for copulas. ArXiv e-prints 1211.4416.

- Genest et al. (1995) Genest, C., Ghoudi, K., Rivest, L.P., 1995. A semiparametric estimation procedure of dependence parameters in multivariate families of distributions. Biometrika 82, 543–552.

- Genest et al. (2006) Genest, C., Quessy, J.F., Rémillard, B., 2006. Goodness-of-fit Procedures for Copula Model Based on the Probability Integral Transformation. Scandinavian Journal of Statistics 33, 337–366.

- Genest and Rémillard (2008) Genest, C., Rémillard, B., 2008. Validity of the parametric bootstrap for goodness-of-fit testing in semiparametric models. Annales de l’Institut Henri Poincaré - Probabilités et Statistiques 44, 1096–1127.

- Genest et al. (2009) Genest, C., Rémillard, B., Beaudoin, D., 2009. Goodness-of-fit tests for copulas: a review and power study. Insur. Math. Econ. 44, 199–213.

- Huang and Prokhorov (2011) Huang, W., Prokhorov, A., 2011. A goodness-of-fit test for copulas. Submitted to Economic Reviews.

- Joe (1996) Joe, H., 1996. Families of m-variate distributions with given margins and m(m-1)/2 bivariate dependence parameters, in: L. Rüschendorf and B. Schweizer and M. D. Taylor (Ed.), Distributions with Fixed Marginals and Related Topics, Inst. Math. Statist., Hayward, CA. pp. 120–141.

- Kullback and Leibler (1951) Kullback, S., Leibler, R.A., 1951. On Information and Sufficiency. The Annals of Mathematical Statistics 22, 79–86.

- Morales-Nápoles et al. (2010) Morales-Nápoles, O., Cooke, R.M., Kurowicka, D., 2010. About the number of vines and regular vines on n nodes. preprint, personal communication .

- Presnell and Boos (2004) Presnell, B., Boos, D.D., 2004. The ios test for model misspecification. Journal of the American Statistical Association 99, 216–227.

- Rosenblatt (1952) Rosenblatt, M., 1952. Remarks on a Multivariate Transformation. The Annals of Mathematical Statistics 23, 470–472.

- Schepsmeier (2013) Schepsmeier, U., 2013. A goodness-of-fit test for regular vine copula models. Http://arxiv.org/abs/1306.0818.

- Schepsmeier et al. (2012) Schepsmeier, U., Stoeber, J., Brechmann, E.C., 2012. VineCopula: Statistical inference of vine copulas. R package version 1.0.

- Sklar (1959) Sklar, M., 1959. Fonctions de répartition à n dimensions et leurs marges. Publ. Inst. Statist. Univ. Paris 8, 229–231.

- Stöber and Schepsmeier (2013) Stöber, J., Schepsmeier, U., 2013. Estimating standard errors in regular vine copula models. Computational Statistics , 1–29.

- Vuong (1989) Vuong, Q., 1989. Likelihood Ratio Tests for Model Selection and Non-Nested Hypotheses. Econometrica 57, 307–333.

- White (1982) White, H., 1982. Maximum likelihood estimation of misspecified models. Econometrica 50, 1–26.

- Zhang et al. (2013) Zhang, S., Okhrin, O., Zhou, Q.M., Song, P.X.K., 2013. Goodness-of-fit Test For Specification of Semiparametric Copula Dependence Models. Personal communication http://sfb649.wiwi.hu-berlin.de/papers/pdf/SFB649DP2013-041.pdf.

- Zhou et al. (2012) Zhou, Q.M., Song, P.X.K., Thompson, M.E., 2012. Information ratio test for model misspecification in quasi-likelihood inference. Journal of the American Statistical Association 107, 205–213.

Appendix A Rosenblatt’s transform for R-vines

The multivariate probability integral transformation (PIT) of Rosenblatt (1952) transforms the copula data with a given multivariate copula into independent data in , where is the dimension of the data set.

Definition 2 (Rosenblatt’s transform)

Let denote copula data of dimension . Further let be the joint cdf of . Then Rosenblatt’s transformation of , denoted as , is defined as

where is the conditional copula of given .

The data vector is now i.i.d. with . In the context of vine copulas the multivariate PIT is given for the special classes of C- and D-vine in Aas et al. (2009, Algorithm 5 and 6). It is a straight forward application of the Rosenblatt transformation of Definition 2 to the recursive structure of a C- or D-vine copula. Similar, an algorithm for the R-vine can be stated, see Algorithm A. Here we make use of a similar structured algorithm of Dißmann et al. (2013) for calculating the log-likelihood of an R-vine copula.

In order to perform computations for a general R-vine copula model, it is convenient to use matrix notation (see Morales-Nápoles et al., 2010; Dißmann et al., 2013). It stores the edges of an R-vine tree sequence in a lower triangular matrix. For the vine tree sequence of Figure 1 this is given by

| (15) |

As an illustration for how the R-vine matrix is derived from the tree sequence in Figure 1 and vice versa, let us consider the second column of the matrix. Here we have on the diagonal, and as a second entry. The set of remaining entries below is . This corresponds to the edge in of Figure 1. Similarly, the edge corresponds to the first and third entry of the second column given the last entry of this row. So the second column of identifies the edges and 1,4. Here we ordered the conditioned set in ascending order. Further, the diagonal of is sorted in descending order which can always be achieved by reordering the node labels. The elements of are denoted by . From now on, we will assume that all matrices are ”normalized” in this way as this allows to simplify notation. Similar to the R-vine tree sequence identifying matrix , we can store the corresponding copula families and parameters in additional lower triangular matrices.

Further, the conditional distributions and are required for the calculation of the log-likelihood function in an R-vine model. Evaluated at a -dimensional vector of observations , and are the arguments of the copula density corresponding to edge . We will store these values in the matrices

| (16) |

and

| (17) |

respectively, both of dimension . For computational purposes an additional matrix is needed to decide whether the arguments of the pair-copula have to be picked from matrix or . For details we refer to Dißmann et al. (2013).

Algorithm A now calculates the PIT of an R-vine copula model.

The vector stores at the end the transformed PIT variables.

Appendix B Cramér-von Mises, Kolmogorov-Smirnov and Anderson Darling goodness-of-fit test

B.1 Multivariate and univariate Cramér-von Mises and Kolmogorov-Smirnov test

Already in the third century of 1900 two model specification tests were developed by Cramér and von Mises, and by Kolmogorov and Smirnov. Both tests treat the hypothesis that i.i.d. samples of the random vector follow a specified continuous distribution function , i.e.

The general multivariate Cramér-von Mises (mCvM) test statistic for a d-dimensional random vector is defined as

| (18) |

while the multivariate Kolmogorov-Smirnov (mKS) test statistic is

| (19) |

Here

denotes the empirical distribution function corresponds to the i.i.d. sample of .

The univariate cases for the random variable are then denoted by

B.2 Univariate Anderson-Darling test

The Anderson and Darling (1954) test, is a statistical test of whether a given probability distribution fits a given set of data samples. It extends the Cramér-von Mises test statistics by adding more weight in the tails of the distribution in consideration. Although it has a general multivariate definition we introduce only the univariate case, since only the univariate case is needed in Section 4.2. Let be a random variable then the null hypothesis of the Anderson-Darling test is again against the alternative . The general univariate Anderson-Darling (AD) test statistic is defined as

| (20) |

where is a non-negative weighting function. With the weighting function Anderson and Darling (1954) put more weight in the tails since this function is large near and . Setting the weight function to one gets as a special case the Cramér-von Mises test statistic. In the case of uniform margins (20) simplifies to

| (21) |

Appendix C Model specification for the power study

For the vine copula density (see Equation (3)) often a short hand notation is used. For this the pair-copula arguments are omitted and denotes only the conditioned and conditioning set. Thus, for the R-vine given in Example 1 we can write

Similarly the considered C- and D-vine copula can be expressed as

| (22) | ||||

| (23) |

| Tree | |||

|---|---|---|---|

| 1 | Gauss | 0.71 | |

| Gauss | 0.33 | ||

| Clayton | 0.71 | ||

| Gumbel | 0.74 | ||

| 2 | Gumbel | 0.38 | |

| Gumbel | 0.47 | ||

| Gumbel | 0.33 | ||

| 3 | Clayton | 0.35 | |

| Clayton | 0.31 | ||

| 4 | Gauss | 0.13 |

| Tree | Tree | ||||||

|---|---|---|---|---|---|---|---|

| 1 | Joe | 0.41 | 3 | Frank 0.03 | 7 | ||

| Gauss | 0.59 | Gumbel | 0.22 | ||||

| Gauss | 0.59 | Gauss | 0.41 | ||||

| Frank | 0.23 | Gumbel | 0.68 | ||||

| Frank | 0.19 | 4 | Clayton | 0.17 | |||

| Clayton | 0.44 | Gauss | 0.09 | ||||

| Gumbel | 0.64 | Frank | 0.21 | ||||

| 2 | Clayton | 0.58 | Gumbel | 0.57 | |||

| Gumbel | 0.44 | 5 | Joe | 0.25 | |||

| Frank | 0.11 | Gumbel | 0.17 | ||||

| Clayton | 0.53 | Frank | 0.02 | ||||

| Clayton | 0.29 | 6 | Gumbel | 0.31 | |||

| Gauss | 0.53 | Clayton | 0.20 | ||||

| 3 | Gauss | 0.19 | 7 | Frank | 0.03 |