The fine structure of volatility feedback II:

overnight and intra-day effects

Abstract

We decompose, within an ARCH framework, the daily volatility of stocks into overnight and intra-day contributions. We find, as perhaps expected, that the overnight and intra-day returns behave completely differently. For example, while past intra-day returns affect equally the future intra-day and overnight volatilities, past overnight returns have a weak effect on future intra-day volatilities (except for the very next one) but impact substantially future overnight volatilities. The exogenous component of overnight volatilities is found to be close to zero, which means that the lion’s share of overnight volatility comes from feedback effects. The residual kurtosis of returns is small for intra-day returns but infinite for overnight returns. We provide a plausible interpretation for these findings, and show that our Intra-day/Overnight model significantly outperforms the standard ARCH framework based on daily returns for Out-of-Sample predictions.

1 Introduction

The ARCH (auto-regressive conditional heteroskedastic) framework was introduced in [1] to account for volatility clustering in financial markets and other economic time series. It posits that the current relative price change can be written as the product of a “volatility” component and a certain random variable , of zero mean and unit variance, and that the dynamics of the volatility is self-referential in the sense that it depends on the past returns themselves as:

| (1) |

where is the “baseline” volatility level, that would obtain in the absence of any feedback from the past, and is a kernel that encodes the strength of the influence of past returns. The model is well defined and leads to a stationary time series whenever the feedback is not too strong, i.e. when . A very popular choice, still very much used both in the academic and professional literature, is the so called “GARCH” (Generalized ARCH), that corresponds to an exponential kernel, , with . However, the long-range memory nature of the volatility correlations in financial markets suggests that a power-law kernel is more plausible — a model called “FIGARCH”, see [2, 3] and below.

Now, the ARCH framework implicitly singles out a time scale, namely the time interval over which the returns are defined. For financial applications, this time scale is often chosen to be one day, i.e. the ARCH model is a model for daily returns, defined for example as the relative variation of price between two successive closing prices. However, this choice of a day as the unit of time is often a default imposed by the data itself. A natural question is to know whether other time scales could also play a role in the volatility feedback mechanism. In our companion paper [4], we have studied this question in detail, focusing on time scales larger than (or equal to) the day. We have in fact calibrated the most general model, called “QARCH” [5], that expresses the squared volatility as a quadratic form of past returns, i.e. with a two-lags kernel instead of the “diagonal” regression (1). This encompasses all models where returns defined over arbitrary time intervals could play a role, as well as (realized) correlations between those — see [4] and references therein for more precise statements, and [6, 7, 8, 9] for earlier contributions along these lines.

The main conclusion of our companion paper [4] is that while other time scales play a statistically significant role in the feedback process (interplay between and resulting in non-zero off-diagonal elements ), the dominant effect for daily returns is indeed associated with past daily returns. In a first approximation, a FIGARCH model based on daily returns, with an exponentially truncated power-law kernel , provides a good model for stock returns, with and days. This immediately begs the question: if returns on time scales larger than a day appear to be of lesser importance,333Note a possible source of confusion here since a FIGARCH model obviously involves many time scales. We need to clearly distinguish time lags, as they appear in the kernel , from time scales, that enter in the definition of the returns themselves. what about returns on time scales smaller than a day? For one thing, a trading day is naturally decomposed into trading hours, that define an ‘Open to Close’ (or ‘intra-day’) return, and hours where the market is closed but news accumulates and impacts the price at the opening auction, contributing to the ‘Close to Open’ (or ‘overnight’) return. One may expect that the price dynamics is very different in the two cases, for several reasons. One is that many company announcements are made overnight, that can significantly impact the price. The profile of market participants is also quite different in the two cases: while low-frequency participants might choose to execute large volumes during the auction, higher-frequency participants and market-makers are mostly active intra-day. In any case, it seems reasonable to distinguish two volatility contributions, one coming from intra-day trading, the second one from overnight activity. Similarly, the feedback of past returns should also be disentangled into an intra-day contribution and an overnight contribution. The calibration of an ARCH-like model that distinguishes between intra-day and overnight returns is the aim of the present paper, and is the content of Section 2. We have in fact investigated the role of higher frequency returns as well. For the sake of clarity we will not present this study here, but rather summarize briefly our findings on this point in the conclusion.

The salient conclusions of the present paper are that the intra-day and overnight dynamics are indeed completely different — for example, while the intra-day (Open-to-Close) returns impact both the future intra-day and overnight volatilities in a slowly decaying manner, overnight (Close-to-Open) returns essentially impact the next intra-day but very little the following ones. However, overnight returns have themselves a slowly decaying impact on future overnights. Another notable difference is the statistics of the residual factor , which is nearly Gaussian for intra-day returns, but has an infinite kurtosis for overnight returns. We discuss further the scope of our results in the conclusion Section 4, and relegate several more technical details to appendices.

2 The dynamics of Close-to-Open and Open-to-Close stock returns and volatilities

Although the decomposition of the daily (Close-to-Close) returns into their intra-day and overnight components seems obvious and intuitive, very few attempts have actually been made to model them jointly (see [10, 11]). In fact, some studies even discard overnight returns altogether. In the present section, we define and calibrate an ARCH model that explicitly treats these two contributions separately. We however first need to introduce some precise definitions of the objects that we want to model.

2.1 Definitions, time-line and basic statistics

We consider equidistant time stamps with day. Every day, the prices of traded stocks are quoted from the opening to the closing hour, but we only keep track of the first and last traded prices. For every stock name , is the open price and the close price at date . (In the following, we drop the index when it is not explicitly needed). We introduce the following definitions of the geometric returns, volatilities, and residuals:

| Intra-day return: | (2a) | ||||

| Overnight return: | (2b) | ||||

| Daily return: | (2c) | ||||

The following time-line illustrates the definition of the three types of return:

| (3) |

To facilitate the reading of our tables and figures, intra-day returns are associated with the green color (or light gray) and overnight returns with blue (or dark gray).

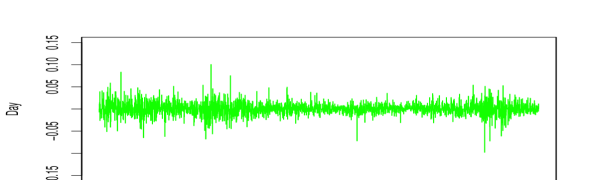

Before introducing any model, we discuss the qualitative statistical differences in the series of Open-Close returns and Close-Open returns . First, one can look at Fig. 1 for a visual impression of the difference: while the intra-day volatility is higher than the overnight volatility, the relative importance of “surprises” (i.e. large positive or negative jumps) is larger for overnight returns. This is confirmed by the numerical values provided in Tab. 1 for the volatility, skewness and kurtosis of the two time series and .

It is also visible on Fig. 1 that periods of high volatilities are common to the two series: two minor ones can be observed in the middle of year 2000 and at the beginning of year 2009, and an important one in the middle of year 2002.

An important quantity is the correlation between intra-day and overnight returns, which can be measured either as (overnight leading intra-day) or as (intra-day leading overnight). The statistical reversion revealed by the measured values of the above correlation coefficients ( and , respectively) is slight enough (compared to the amplitude and reach of the feedback effect) to justify the assumption of i.i.d. residuals. If there were no linear correlations between intra-day and overnight returns, the squared volatilities would be exactly additive, i.e. . Deviations from this simple addition of variance rule are below .

2.2 The model

The standard ARCH model recalled in the introduction, Eq. (1), can be rewritten identically as:

| (4) |

meaning that there is a unique kernel describing the feedback of past intra-day and overnight returns on the current volatility level.

If however one believes that these returns are of fundamentally different nature, one should expand the model in two directions: first, the two volatilities and should have separate dynamics. Second, the kernels describing the feedback of past intra-day and overnight returns should a priori be different. This suggests to write the following generalized model for the intra-day volatility:

| (5) | ||||

where we have added the possibility of a “leverage effect”, i.e. terms linear in past returns that can describe an asymmetry in the impact of negative and positive returns on the volatility. The notation used is, we hope, explicit: for example describes the influence of squared intra-Day past returns on the current intra-Day volatility. Note that the mixed effect of intra-Day and overNight returns requires two distinct kernels, and , depending on which comes first in time. Finally, the time-line shown above explains why the index starts at for past intra-day returns, but at for past overnight returns. We posit a similar expression for the overnight volatility:

| (6) | ||||

The model is therefore fully characterized by two base-line volatilities , four leverage (linear) kernels , eight quadratic kernels , and the statistics of the two residual noises needed to define the returns, as . We derive in Appendix A conditions on the coefficients of the model under which the two volatility processes remain positive at all times. The model as it stands has a large number of parameters; in order to ease the calibration process and gain in stability, we in fact choose to parameterize the dependence of the different kernels with some simple functions, namely an exponentially truncated power-law for and a simple exponential for :

| (7) |

The choice of these functions is not arbitrary, but is suggested by a preliminary calibration of the model using a generalized method of moments (GMM), as explained in the companion paper, see Appendix C.2 in Ref. [4].

As far as the residuals are concerned, we assume them to be i.i.d. centered Student variables of unit variance with respectively and degrees of freedom. Contrarily to many previous studies, we prefer to be agnostic about the kurtosis of the residuals rather than imposing a priori Gaussian residuals. It has been shown that while the ARCH feedback effect accounts for volatility clustering and for some positive kurtosis in the returns, this effect alone is not sufficient to explain the observed heavy tails in the return distribution (see for example [4]). These tails come from true ‘surprises’ (often called jumps), that cannot be anticipated by the predictable part of the volatility, and that can indeed be described by a Student (power-law) distribution of the residuals.

2.3 Dataset

The dataset used to calibrate the model is exactly the same as in our companion paper [4]. It is composed of US stock prices (four points every day: Open, Close, High and Low) for stocks present permanently in the S&P-500 index from Jan. 2000 to Dec. 2009 ( days). For every stock , the daily returns (), intra-day returns () and overnight returns () defined in Eq. (2) are computed using only Open and Close prices at every date . In order to improve the statistical significance of our results, we consider the pool of stocks as a statistical ensemble over which we can average. This means that we assume a universal dynamics for the stocks, a reasonable assumption as we discuss in Appendix B.

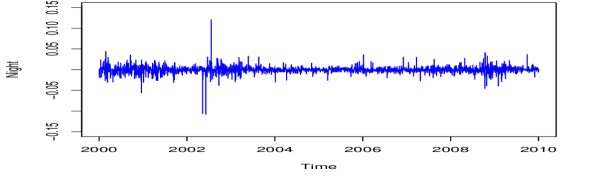

Bare stock returns are “polluted” by several obvious and predictable events associated with the life of the company, such as quarterly announcements. They also reflect low-frequency human activity, such as a weekly cyclical pattern of the volatility, which is interesting in itself (see Fig. 2). These are of course real effects, but the ARCH family of models we investigate here rather focuses on the endogenous self-dynamics on top of such seasonal patterns. For example, the quarterly announcement dates are responsible for returns of typically much larger magnitude (approximately three times larger on average for daily returns) that have a very limited feedback in future volatility.

We therefore want to remove all obvious seasonal effects from the dataset, and go through the following additional steps of data treatment before estimating the model. For every stock , the average over time is denoted , and for each date , the cross-sectional average over stocks is . All the following normalizations apply both (and separately) for intra-day returns and overnight returns.

-

•

The returns series are first centered around their temporal average: In fact, the returns are already nearly empirically centered, since the temporal average is small, see Tab. 1 above.

-

•

We then divide the returns by the cross-sectional dispersion:

This normalization444 If the element is not excluded in the average, the tails of the returns are artificially cut-off: when , is capped at . removes the historical low-frequency patterns of the volatility, for example the weekly pattern discussed above (Fig. 2). In order to predict the “real” volatility with the model, one must however re-integrate these patterns back into the ’s.

-

•

Finally, we normalize stock by stock all the returns by their historical standard deviation: for all stock , for all ,

imposing .

This data treatment allows to consider that the residual volatility of the returns series is independent of the effects we do not aim at modeling, and that the series of all stocks can reasonably be assumed to be homogeneous (i.e. identically distributed), both across stocks and across time. This is necessary in order to calibrate a model that is translational-invariant in time (i.e. only the time lag enters Eqs. (5,6)), and also to enlarge the calibration dataset by averaging the results over all the stocks in the pool — see the discussion in Appendix B.

2.4 Model estimation

Assuming that the distribution of the residuals is a Student law, the log-likelihood per point of the model can be written as ():

| (8) |

where are defined in Eqs. (5,6), are the degrees of freedom of the Student residuals, and denote generically the sets of volatility feedback parameters.

Conditionally on the dataset, we maximize numerically the likelihood of the model, averaged over all dates and all stocks.

Calibration methodology:

As mentioned above, we in fact choose to parameterize the feedback kernels as suggested by the results of the method of moments, i.e. exponentially truncated power-laws for ’s and simple exponentials for ’s. Imposing these simple functional forms allows us to gain stability and readability of the results. However, the functional dependence of the likelihood on the kernel parameters is not guaranteed to be globally concave, as is the case when it is maximized “freely”, i.e. with respect to all individual kernel coefficients and , with . This is why we use a three-step approach:

-

1.

A first set of kernel estimates is obtained by the Generalized Method of Moments (GMM), see [4], and serves as a starting point for the optimization algorithm.

-

2.

We then run a Maximum Likelihood Estimation (MLE) of the unconstrained kernels based on Eq. (8), over parameters for both and , with a moderate value of maximum lag three months. Taking as a starting point the coefficients of step 1 and maximizing with a gradient descent, we obtain a second set of (short-range) kernels.

-

3.

Finally, we perform a MLE estimation of the parametrically constrained kernels with the functional forms (7) for ’s and ’s, which only involves parameters in every set and , with now a large value of the maximum lag two years. Taking as a starting point the functional fits of the kernels obtained at step 2, and maximizing with a gradient descent, we obtain our final set of model coefficients, shown in Tabs. 3,3.

Thanks to step 2, the starting point of step 3 is close enough to the global maximum for the likelihood to be locally concave, and the gradient descent algorithm converges in a few steps. The Hessian matrix of the likelihood is evaluated at the maximum to check that the dependency on all coefficients is indeed concave.

The numerical maximization of the likelihood is thus made on or parameters per kernel, independently of the chosen maximum lag , that can thus be arbitrarily large with little additional computation cost.

Finally, the degrees of freedom of the Student residuals are determined using two separate one-dimensional likelihood maximizations (one for and one for ) and then included as an additional parameter in the MLE of the third step of the calibration. Note that does not vary significantly at the third step, which means that the estimation of the volatility parameters at the second step can indeed be done independently from that of .

This somewhat sophisticated calibration method was tested on simulated data, obtaining very good results.

The special case :

We ran the above calibration protocol on intra-day and overnight volatilities separately.

For the overnight model, this led to a slightly negative value of the baseline volatility (statistically compatible with zero). But of course negative values of are excluded for a stable and positive volatility process. For overnight volatility only, we thus add a step to the calibration protocol, which includes the constraint in the estimation of and (which are the two main contributors to the value of the baseline volatility). For simplicity, we consider here that . We take the results of the preceding calibration as a starting point and freeze all the kernels but and , expressed (in this section only) as follows:

| (9) |

where is fixed by the constraint :

| (10) |

with the ratio of the two initial amplitudes, and the (low) contribution of the fixed ‘cross’ kernels and to . We then maximize the likelihood of the model with respect to the five parameters and , for which a gradient vector and a Hessian matrix of dimension can be deduced from equations (9) and (10). The coefficients and confidence intervals of the kernels and are replaced in Sect. 3.1 by the results of this final step, along with the corresponding value of the overnight baseline volatility, in Sect. 3.3.

For intra-day volatility instead, the results are given just below, in Sect. 3.1.

3 Intra-day vs. overnight: results and discussions

The calibration of our generalized ARCH framework should determine three families of parameters: the feedback kernels and , the statistics of the residuals and finally the “baseline volatilities” . We discuss these three families in turn in the following sections.

3.1 The feedback kernels

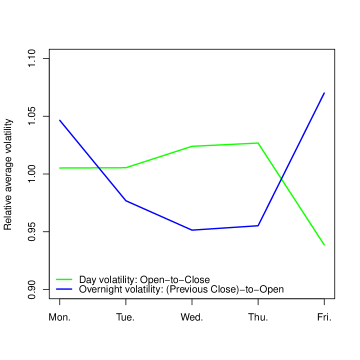

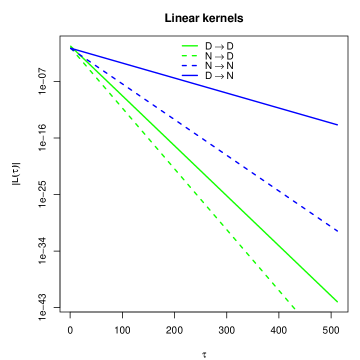

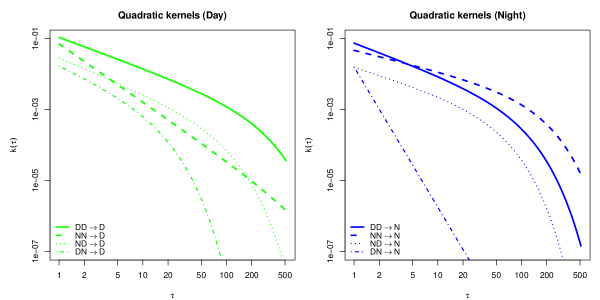

In this section, we give the results of the ML estimation of the regression kernels for a maximum lag : estimates of the parameters are reported in Tabs. 3,3, and the resulting kernels are shown in Fig. 3.

| Kernels | |||||

|---|---|---|---|---|---|

| Kernels | |||||

|---|---|---|---|---|---|

We define the exponential characteristic times and , for which qualitative interpretation is easier than for and . In the case of the quadratic kernels (of type ), represents the lag where the exponential cut-off appears, after which the kernel decays to zero quickly. One should note that in three cases, we have . These correspond to kernels with , which means that the power-law decays quickly by itself. In these cases the identifiability of is more difficult and cut-off times are ill-determined, since the value of only matters in a region where the kernels are already small. The exponential term could be removed from the functional form of equation (7), for these kernels only (the calibration would then modify very slightly the value of the power-law exponent ).

Intra-day volatility:

From Tab. 3 and Fig. 3(a), we see that all intra-day quadratic kernels are positive. However, a clear distinction is observed between intra-day feedback and overnight feedback: while the former is strong and decays slowly ( and days), the latter decays extremely steeply () and is quickly negligible, except for the intra-day immediately following the overnight, where the effect is as strong as that of the previous intra-day. The cross kernels ( or ) are both statistically significant, but are clearly smaller, and decay faster, than the effect.

As far as the leverage effect is concerned, both ’s are found to be negative, as expected, and of similar decay time: days (one week). However, the amplitude for their immediate impact is two times smaller for past overnight returns: versus .

In summary, the most important part of the feedback effect on the intra-day component of the volatility comes from the past intra-days themselves, except for the very last overnight, which also has a strong impact — as intuitively expected, a large return overnight leads to a large immediate reaction of the market as trading resumes. However, this influence is seen to decay very quickly with time. Since a large fraction of company specific news release happen overnight, it is tempting to think that large overnight returns are mostly due to news. Our present finding would then be in line with the general result reported in [12]: volatility tends to relax much faster after a news-induced jump than after endogenous jumps.

Overnight volatility:

In the case of overnight volatility, Tab. 3 and Fig. 3(a) illustrate that the influence of past intra-days and past overnights is similar: , in particular when both are large. The cross kernels now behave quite differently: whereas the behavior of is not very different from that of or (although its initial amplitude is four times smaller), is negative and small, but is hardly significant for . Interestingly, as pointed out above, the equality means that it is the full Close-to-Close return that is involved in the feedback mechanism on the next overnight. What we find here is that this equality very roughly holds, suggesting that, as postulated in standard ARCH approaches, the daily close to close return is the fundamental object that feedbacks on future volatilities. However, this is only approximately true for the overnight volatility, while the intra-day volatility behaves very differently (as already said, for intra-day returns, the largest part of the feedback mechanism comes from past intra-days only, and the very last overnight).

Finally, the leverage kernels behave very much like for the intra-day volatility. In fact, the leverage kernel is very similar to its counterpart, whereas the decay of the kernel is slower ( days, nearly one month).

Stability and positivity:

We checked that these empirically-determined kernels are compatible with a stable and positive volatility process. The first obvious condition is that the system is stable with positive baseline volatilities . The self-consistent equations for the average volatilities read: (neglecting small cross correlations):

| (11) | ||||

| (12) |

This requires that the two eigenvalues of the matrix of the corresponding linear system are less than unity, i.e.

| (13) |

where the hats denote the integrated kernels, schematically . This is indeed verified empirically, the eigenvalues being .

Moreover, for intra-day and overnight volatilities separately, we checked that our calibrated kernels are compatible with the two positivity conditions derived in Appendices A.2,A.3 : the first one referring to the cross kernels and , and the second one to the leverage kernels and . For , the criteria fail for two spurious reasons. Firstly, for lags greater than their exponential cut-offs, the quadratic kernels vanish quicker than the ‘cross’ kernels, which makes the “ by ” criterion fail. Secondly, the criterion cannot be verified for overnight volatility with (for lower values of , using the same functional forms and coefficients for the kernels, rises to a few percents). These two effects can be considered spurious because the long-range contributions have a weak impact on the volatilities and cannot in deed generate negative values, as we checked by simulating the volatility processes with . We thus restricted the range to ( six months) in order to test our results with the two positive volatility criteria (again, see Appendix A). For the ill-determined exponential decay rates , the upper bounds of the confidence intervals are used. The two criteria are then indeed verified for both intra-day and overnight volatilities.

3.2 Distribution of the residuals

As mentioned above, we assume that the residuals (i.e. the returns divided by the volatility predicted by the model) are Student-distributed. This is now common in ARCH/GARCH literature and was again found to be satisfactory in our companion paper [4]. The fact that the are not Gaussian means that there is a residual surprise element in large stock returns, that must be interpreted as true ‘jumps’ in the price series.

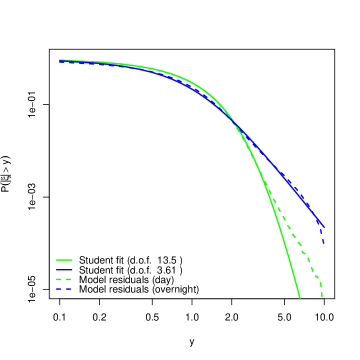

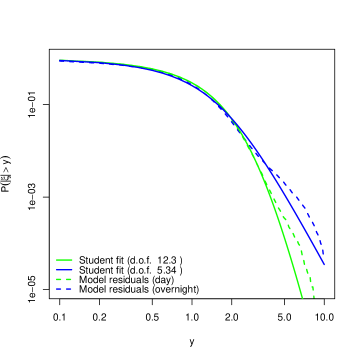

The tail cumulative distribution function (CDF) of the residuals is shown in Fig. 4 for both intra-day and overnight returns, together with Student best fits, obtained with long feedback kernels (). This reveals a clear difference in the statistical properties of and . First, the Student fit is better for overnight residuals than for intra-day residuals, in particular far in the tails. More importantly, the number of degrees of freedom is markedly different for the two types of residuals: indeed, our MLE estimation yields and as reported in Tab. 4, resulting in values of the residual kurtosis and . This result must be compared with the empirical kurtosis of the returns that was measured directly in Sect. 2. The intuitive conclusion is that the large (infinite?) kurtosis of the overnight returns cannot be attributed to fluctuations in the volatility, but rather, as mentioned above, to large jumps related to overnight news. This clear qualitative difference between intra-day and overnight returns is a strong argument justifying the need to treat these effects separately, as proposed in this paper.

We have also studied the evolution of and as a function of the length of the memory of the kernels, see Tab. 4. If longer memory kernels allow to account for more of the dynamics of the volatility, less kurtic residuals should be found for larger ’s. This is indeed what we find, in particular for intra-day returns, for which increases from for to for . The increase is however much more modest for overnight returns. We propose below an interpretation of this fact.

3.3 Baseline volatility

| 21 | 42 | 512 | |

|---|---|---|---|

| 10.7 | 12.6 | 13.5 | |

| 3.49 | 3.58 | 3.61 | |

| 18.1% | 12.8% | 8.5% | |

| 14.0% | 7.3% | 0.0% |

Finally, we want to study the ratio , which can be seen as a measure of the relative importance of the baseline component of the volatility, with respect to the endogenous feedback component.555In fact, the stability criterion for our model reads , which is found to be satisfied by our calibration, albeit marginally for the overnight volatility. The complement gives the relative contribution of the feedback component, given by in the present context.666There is a contribution of the cross terms since intra-day/overnight and overnight/intra-day correlations are not exactly zero, but this contribution is less than one order of magnitude lower than the .

The results for are given in Tab. 4 for and : as mentioned above, a larger explains more of the volatility, therefore reducing the value of both and . While is small () and comparable to the value found for the daily ARCH model studied in the companion paper [4], the baseline contribution is nearly zero for the overnight volatility. We find this result truly remarkable, and counter-intuitive at first sight. Indeed, the baseline component of the volatility is usually associated to exogenous factors, which, as we argued above, should be dominant for since many unexpected pieces of news occur overnight!

Our interpretation of this apparent paradox relies on the highly kurtic nature of the overnight residual, with a small value as reported above. The picture is thus as follows: most overnights are news-less, in which case the overnight volatility is completely fixed by feedback effects, set by the influence of past returns themselves. The overnights in which important news is released, on the other hand, contribute to the tails of the residual , because the large amplitude of these returns could hardly be guessed from the previous amplitude of the returns. Furthermore, the fact that decays very quickly is in agreement with the idea, expressed in [12], that the impact of news (chiefly concentrated overnight) on volatility is short-lived.777This effect was confirmed recently in [13] using a direct method: the relaxation of volatility after large overnight jumps of either sign is very fast, much faster than the relaxation following large intra-day jumps.

In conclusion, we find that most of the predictable part of the overnight volatility is of endogenous origin, but that the contribution of unexpected jumps reveals itself in the highly non-Gaussian statistics of the residuals. The intra-day volatility, on the other hand, has nearly Gaussian residuals but still a very large component of endogenous volatility ().

3.4 In-Sample and Out-of-Sample tests

In order to compare our bivariate Intra-day/Overnight volatility prediction model with the standard ARCH model for daily (close-to-close) volatility, we ran In-Sample (IS) and Out-of-Sample (OS) likelihood computations with both models. Of course, in order to compare models, the same quantities must be predicted. A daily ARCH model that predicts the daily volatility at date can predict intra-day and overnight volatilities as follows:

| (14) |

where is the average over all dates and all stocks, and as in Sect. 2, is the daily (close-to-close) return of date . Similarly, our bivariate intra-day/overnight model that provides predictions for intra-day and overnight volatilities separately can give the following estimation of the daily volatility:

| (15) |

For each of the 6 predictions (of the intra-day, overnight and daily volatilities by the two models separately, bivariate Intra-day/Overnight and standard ARCH), we use the following methodology:

-

•

The pool of stock names is split in two halves, and the model parameters are estimated separately on each half.

-

•

The “per point” log-likelihood (8) is computed for both sets of parameters, once with the same half dataset as used for the calibration (In-Sample), and once with the other half dataset (Out-of-Sample, or “control”). We compute the log-likelihoods for intra-day and overnight volatilities (), and for daily volatility:

Bivariate models : Standard ARCH models : where is computed in the bivariate model (i.e. with six regressors: four quadratic and two linear) and is computed in the standard ARCH model (i.e. with two regressors: one quadratic and one linear), and and are as given by equations (14) and (15).

-

•

The IS log-likelihood of the model is computed as the average of the two In-Sample results, and similarly for the OS log-likelihood . We call and the average likelihood per point (ALpp) of the model IS and OS, expressed as percentages, that are two proxies of the “probability that the sample data were generated by the model”.

We then use the values of and to compare models. For a “good” model, these values must be as high as possible, but they must also be close to each other. As a matter of fact, if is significantly greater than , the model may be over-fitting the data. On the contrary, if is greater than , which seems counter-intuitive, the model may be badly calibrated. The results of this model comparison are given in Tab. 5: the bivariate Intra-day/Overnight model has a higher likelihood than the standard daily ARCH model, both In-Sample (this was to be expected even from pure over-fitting due to additional parameters) and Out-of-Sample (thus outperforming in predicting the “typical” random realization of the returns).

The likelihoods of the predictions obtained with equations (14) and (15) are marked with the exponent in Tab. 5. For these likelihoods, “In-Sample” simply means that the same half of the stock pool was used for the calibration of the model and for the estimation of the likelihood, although different types of returns are considered. Similarly, “Out-of-Sample” likelihoods are estimated on the other half of the stock pool. These values serve as comparison benchmarks between the two models.

| Prediction | ||||||

|---|---|---|---|---|---|---|

| ALpp [%] | ||||||

| Biv. Intra-day/Overnight | ||||||

| Standard ARCH | ||||||

We see that in all cases, the bivariate Intra-day/Overnight significantly outperforms the standard daily ARCH framework, in particular concerning the prediction of the total (Close-Close) volatility.

4 Conclusion and extension

The main message of this study is quite simple, and in fact to some extent expected: overnight and intra-day returns are completely different statistical objects. The ARCH formalism, that allows one to decompose the volatility into an exogenous component and a feedback component, emphasizes this difference. The salient features are:

-

•

While past intra-day returns affect equally both the future intra-day and overnight volatilities, past overnight returns have a weak effect on future intra-day volatilities (except for the very next one) but impact substantially future overnight volatilities.

-

•

The exogenous component of overnight volatilities is found to be close to zero, which means that the lion’s share of overnight volatility comes from feedback effects.

-

•

The residual kurtosis of returns (once the ARCH effects have been factored out) is small for intra-day returns but infinite for overnight returns.

-

•

The bivariate intra-day/overnight model significantly outperforms the standard ARCH framework based on daily returns for Out-of-Sample predictions.

Intuitively, a plausible picture for overnight returns is as follows: most overnights are news-less, in which case the overnight volatility is completely fixed by feedback effects, set by the influence of past returns themselves. Some (rare) overnights witness unexpected news releases, which lead to huge jumps, the amplitude of which could hardly have be guessed from the previous amplitude of the returns. This explains why these exogenous events contribute to residuals with such fat tails that the kurtosis diverge, and not to the baseline volatility that concerns the majority of news-less overnights.

These conclusions hold not only for US stocks: we have performed the same study on European stocks obtaining very close model parameter estimates.888Equities belonging to the Bloomberg European 500 index over the same time span 2000–2009, see Appendix C for detailed results. Notably, the baseline volatilities are found to be and (for intra-day and overnight volatilities, respectively), in line with the figures found on US stocks and the interpretation drawn. The only different qualitative behavior observed on European stocks is the quality of the Student fit for the residuals of the overnight regression: whereas US stocks exhibit a good fit with degrees of freedom (hence infinite kurtosis), European stocks have a fit of poorer quality in the tails and a parameter larger than 4, hence a positive but finite kurtosis.

Having decomposed the Close-Close return into an overnight and an intra-day component, the next obvious step is to decompose the intra-day return into higher frequency bins — say five minutes. We have investigated this problem as well, the results are reported in [14]. In a nutshell, we find that once the ARCH prediction of the intra-day average volatility is factored out, we still identify a causal feedback from past five minute returns onto the volatility of the current bin. This feedback has again a leverage component and a quadratic (ARCH) component. The intra-day leverage kernel is close to an exponential with a decay time of hour. The intra-day ARCH kernel, on the other hand, is still a power law, with an exponent that we find to be close to unity, in agreement with several studies in the literature concerning the intra-day temporal correlations of volatility/activity — see e.g. [15, 16, 17], and, in the context of Hawkes processes, [18, 19]. It would be very interesting to repeat the analysis of the companion paper [4] on five minute returns and check whether there is also a dominance of the diagonal terms of the QARCH kernels over the off-diagonal ones, as we found for daily returns. This would suggest a microscopic interpretation of the ARCH feedback mechanism in terms of a Hawkes process for the trading activity.

Acknowledgements

We thank S. Ciliberti, N. Cosson, L. Dao, C. Emako-Kazianou, S. Hardiman, F. Lillo and M. Potters for useful discussions. P. B. acknowledges financial support from Fondation Natixis (Paris).

References

- [1] Robert F. Engle. Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica: Journal of the Econometric Society, pages 987–1007, 1982.

- [2] Tim Bollerslev, Robert F. Engle, and Daniel B. Nelson. ARCH models, pages 2959–3038. Volume 4 of Engle and McFadden [20], 1994.

- [3] Richard T. Baillie, Tim Bollerslev, and Hans O. Mikkelsen. Fractionally integrated generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 74(1):3–30, 1996.

- [4] Rémy Chicheportiche and Jean-Philippe Bouchaud. The fine-structure of volatility feedback 1: Multi-scale self-reflexivity. Physica A: Statistical Mechanics and its Applications, 2014.

- [5] Enrique Sentana. Quadratic ARCH models. The Review of Economic Studies, 62(4):639, 1995.

- [6] Ulrich A. Müller, Michel M. Dacorogna, Rakhal D. Davé, Richard B. Olsen, Olivier V. Pictet, and Jacob E. von Weizsäcker. Volatilities of different time resolutions — analyzing the dynamics of market components. Journal of Empirical Finance, 4(2):213–239, 1997.

- [7] Gilles Zumbach and Paul Lynch. Heterogeneous volatility cascade in financial markets. Physica A: Statistical Mechanics and its Applications, 298(3-4):521–529, 2001.

- [8] Lisa Borland and Jean-Philippe Bouchaud. On a multi-timescale statistical feedback model for volatility fluctuations. The Journal of Investment Strategies, 1(1):65–104, December 2011.

- [9] Yoash Shapira, Dror Y. Kenett, Ohad Raviv, and Eshel Ben-Jacob. Hidden temporal order unveiled in stock market volatility variance. AIP Advances, 1(2):022127–022127, 2011.

- [10] Giampiero M. Gallo. Modelling the impact of overnight surprises on intra-daily volatility. Australian Economic Papers, 40(4):567–580, 2001.

- [11] Ilias Tsiakas. Overnight information and stochastic volatility: A study of European and US stock exchanges. Journal of Banking & Finance, 32(2):251–268, 2008.

- [12] Armand Joulin, Augustin Lefevre, Daniel Grunberg, and Jean-Philippe Bouchaud. Stock price jumps: News and volume play a minor role. Wilmott Magazine, pages 1–7, September/October 2008.

- [13] Nicolas Cosson. Analysis of realized and implied volatility after stock price jumps. Master’s thesis, Université de Paris VI Pierre et Marie Curie, Jun 2013. Available upon request.

- [14] Pierre Blanc. Modélisation de la volatilité des marchés financiers par une structure ARCH multi-fréquence. Master’s thesis, Université de Paris VI Pierre et Marie Curie, Sep 2012. Available upon request.

- [15] Marc Potters, Rama Cont, and Jean-Philippe Bouchaud. Financial markets as adaptive systems. EPL (Europhysics Letters), 41(3):239, 1998.

- [16] Yanhui Liu, Parameswaran Gopikrishnan, Pierre Cizeau, Martin Meyer, Chung-Kang Peng, and H. Eugene Stanley. Statistical properties of the volatility of price fluctuations. Physical Review E, 60:1390–1400, Aug 1999.

- [17] Fengzhong Wang, Kazuko Yamasaki, Shlomo Havlin, and H. Eugene Stanley. Scaling and memory of intraday volatility return intervals in stock markets. Physical Review E, 73(2):026117, 2006.

- [18] Emmanuel Bacry, Khalil Dayri, and Jean-François Muzy. Non-parametric kernel estimation for symmetric Hawkes processes. Application to high frequency financial data. The European Physical Journal B, 85:1–12, 2012.

- [19] Stephen J. Hardiman, Nicolas Bercot, and Jean-Philippe Bouchaud. Critical reflexivity in financial markets: a Hawkes process analysis. arXiv preprint q-fin.ST/1302.1405, 2013.

- [20] Robert F. Engle and Daniel L. McFadden, editors. Handbook of Econometrics, volume 4. Elsevier/North-Holland, Amsterdam, 1994.

Appendix A Non-negative volatility conditions

In this appendix, we study the mathematical validity of our volatility regression model. The first obvious condition is that the model is stable, which leads to the condition (13) in the text above. This criterion is indeed obeyed by the kernels calibrated on empirical results. Secondly, the volatility must remain positive, which is not a priori guaranteed with multiple kernels associated to signed regressors. We now establish a set of sufficient conditions on the feedback kernels to obtain non-negative volatility processes.

A.1 One correlation feedback kernel, no leverage coefficients

We consider first the simpler model for daily volatility, without linear regression coefficients:

This modification of the standard ARCH model can lead to negative volatilities if (at least) one term in the last sum takes large negative values. This issue can be studied more precisely with the matrix form of the model:

with

and where and coefficients are assumed to be all positive (which is the case empirically). This formula highlights the fact that the volatility remains positive as soon as the symmetric matrix is positive semidefinite. We now determine a sufficient and necessary condition under which has negative eigenvalues. The characteristic polynomial of is

and the eigenvalues of are the zeros of , solutions , i.e. such that

Hence, has at least one negative eigenvalue iff s.t.

and finally,

| (16) |

When the quadratic kernel is positive-semidefinite, remains positive for all . For example, in the standard ARCH model, the inequality is saturated for all by construction, and the condition (16) is satisfied.

The positive-semidefiniteness of , equivalent to

is ensured by the sufficient condition that every term in the development of the quadratic form is positive:

| is positive-semidefinite | |||

Although more stringent a priori, this “ by ” condition resumes, in this particular case, to the necessary and sufficient criterion (16). In the next subsection, we use the same method to obtain a sufficient condition for the semidefiniteness of in the more complicated case with two correlation feedback kernels.

A.2 Two correlation feedback kernels, no leverage coefficients

With an additional feedback function and a coefficient corresponding to the term in the sum, the model is

or , with , defined by

The positive-semidefiniteness of is harder to characterize directly, so we use the “ by ” method to find a criterion for a sufficient condition. For any and any vector , the quadratic form is decomposed as follows:

and clearly, a sufficient condition for the sum to be non-negative is that each term is non-negative:

The last condition is equivalent to a simpler one, with saturating one of the two inequalities: denoting and , is positive-semidefinite if (but not only if), ,

is larger than one, yielding the following a.s. positive volatility criterion:

A.3 With leverage coefficients

We now add leverage terms to the volatility equation:

with

and appropriate vectors . It is easy to show that, assuming a positive-definite ,

| (17) |

Appendix B Universality assumption

To obtain a better convergence of the parameters of the model, the estimates are averaged over a pool of US stocks. The validity of this method lies on the assumption that the model is approximately universal, i.e. that the values of its coefficients do not vary significantly among stocks.

We check that this assumption is relevant by splitting the stock pool in two halves and running the estimation of the model on the two halves independently. We obtain a set of coefficients calibrated on the first half and a set on the second half (each set contains parameters, three for each of the four kernels, two for each of the two kernels, plus ).

If the (normalized) returns series for each stock were realizations of the same process, the differences between the coefficients of the two half stock pools would be explained by statistical noise only. To quantify how close the observed differences are to statistical noise, we run a series of Wald tests and study the obtained p-values. We test against , where , by comparing the statistic

| (18) |

to the quantiles of a variable, where is the sample size for each half stock pool, is the Fisher Information matrix of the model and is the Jacobian matrix of .

For intra-day volatility, the p-value is close to zero if all the coefficients are included, but becomes very high () if we exclude from the test. One can conclude that all the parameters but can be considered universal, with a high significance level of . It is not surprising that at least one coefficient varies slightly among stocks (it would indeed be a huge discovery to find that US stocks can be considered as identically distributed!).

In the case of overnight volatility, we first test the universality of the parameters in and , for which the constraint is included in the estimation. We then test the other parameters for universality. Once again, a few of them (, and ) must be excluded from the tests to obtain acceptable p-values. We then obtain for the first test and for the second.

It is then natural to wonder whether the four coefficients that cannot be considered as statistically universal differ significantly in relative values. That is why we compute a second comparison criterion: for a pair of coefficients estimated on the first and second half stock pools respectively, we compute the relative difference, defined as:

The values of this criterion are summarized in Tabs. 6,7. The first observation is that no relative difference exceeds (except for three of the ill-determined ) which indicates that the signs and orders of magnitude of the coefficients of the model are invariant among stocks. The coefficients for which the relative difference is high but the statistical one is low do not contradict the universality assumption: the ML estimation would need a larger dataset to determine them with precision, and the difference between the two halves can be interpreted as statistical noise.

Three of the four “non-universal” coefficients, , and also show a significant relative difference between the two stock pools (above ). These are thus the only coefficients of the model for which averaging over all stocks is in principle not well-justified, and for which the confidence intervals given in Sect. 3.1 should be larger. However, these variations do not impact the global shapes of the corresponding kernels in a major way, and our qualitative comments on the feedback of past returns on future intra-day and overnight volatilities are still valid.

The results of this section indicate that most coefficients of the model are compatible with the assumption of universality. Although some coefficients do show slight variations, our stock aggregation method (with proper normalization, as presented in Sect. 2.3) is reasonable.

| Kernels | |||

|---|---|---|---|

| 34.4 % | |||

| 77.6 % | |||

| 94.8 % | |||

| Kernels | ||

|---|---|---|

| Kernels | |||

|---|---|---|---|

| 33.0 % | |||

| 30.1 % | 80.0 % | ||

| 35.5 % | 21.0 % | ||

| Kernels | ||

|---|---|---|

| 32.0 % | ||

Appendix C The case of European stocks: results and discussions

In order to verify that our conclusions are global and not specific to US stock markets, we also calibrated our model on European stock returns. The dataset is composed of daily prices for European stocks of the Bloomberg European 500 index, on the same period 2000–2009. The data treatment is exactly the same as before. The following sections analyze and compare the results to those obtained on US stocks.

C.1 The feedback kernels: parameters estimates

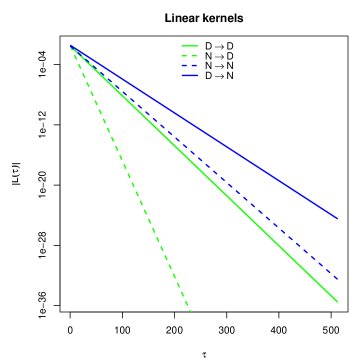

ML estimates of the parameters in the regression kernels (for a maximum lag ) are reported in Tabs. 9,9, and the resulting kernels are shown in Figs. 5(a),5(b).

| Kernels | |||||

|---|---|---|---|---|---|

| Kernels | |||||

|---|---|---|---|---|---|

Intra-day volatility:

From Tab. 9 and Fig. 5(a), we see that all the conclusions drawn previously for the case of US stocks hold for European stocks. The intra-day feedback is stronger and of much longer memory than overnight feedback, which decays very quickly (although more slowly for European stocks, with instead of ). The cross kernels are still clearly smaller than the two quadratic ones, with close to unity.

The leverage effect is similar to the case of US stocks too, although its initial amplitude is approximately equal for past intra-day and overnight returns, whereas past intra-days are stronger than overnights for US stocks.

Overnight volatility:

In the case of overnight volatility, we see from Tab. 9 and Fig. 5(a) that not only do all our previous conclusions still hold in the European case (long memory for both intra-day and overnight feedback, second cross kernel nearly equal to zero), but the coefficients of the model are remarkably close to those of the US calibration.

C.2 Distribution of the residuals

For intra-day returns, the distribution of the residuals is very similar to the case of US stocks. However, for overnight returns, some differences must be pointed out. Firstly, as can be seen on Tab. 10, is significantly higher for European stock () than for US stocks (). As a consequence, the kurtosis of overnight residuals is finite: . The distribution is still highly leptokurtic, but the result is less extreme than for US stocks. Secondly, figure 6 shows that the quality of the Student fit is of lesser quality here. For European stocks, both intra-day and overnight residuals seem to be fitted by a lower value of for far tail events, whereas this only held for intra-day residuals in the US case.

C.3 Baseline volatility

| 512 | |

|---|---|

| 12.3 | |

| 5.34 | |

| 10.0% | |

| 0.0% |

Finally, we compare the ratios of the two stock pools. Here again, the results are very close to our previous calibration: for intra-day volatility, for overnight volatility. Like in the case of US stocks, the calibration procedure yields a slightly negative , so we add an additional step that includes the constraint (for overnight volatility only).

One of our main conclusions for US stocks is that overnight volatility is entirely endogenous, and that the exogeity of overnight returns is contained in the leptokurtic distribution of overnight residuals. This section proves that this is also true for European stocks and suggests that our findings hold quite generally.