New measure of multifractality and its application in finances

Abstract

We provide an alternative method for analysis of multifractal properties of time series. The new approach takes into account the behavior of the whole multifractal profile of the generalized Hurst exponent for all moment orders , not limited only to the edge values of describing in MFDFA scaling properties of smallest and largest fluctuations in signal. The meaning of this new measure is clarified and its properties are investigated for synthetic multifractal data as well as for real signals from stock markets. We show that the proposed new measure is free of problems one can meet in real nonstationary signals, while searching their multifractal signatures.

Keywords: multifractality, spurious multifractality, finite size effects, multifractal detrended analysis, multifractal bias, scaling, time series analysis, new multifractal measure, generalized Hurst exponent

PACS:

05.45.Tp, 89.75.Da, 05.40.-a, 89.65.Gh,89.75.-k

1 Introduction

The multifractal detrended fluctuation analysis (MFDFA) [1] became in last ten years the major technique used for studying the multifractal properties in complex systems and in time series. More then 500 papers discusses MFDFA issues in variety of problems related with complexity (see, e.g., [2]–[18]). The central role in MFDFA is played by the -th moment of fluctuation function () defined as [1]

| (1) |

for , and

| (2) |

for , where

| (3) |

and () are data in series, is the size of window box in which detrending is performed, while is the polynomial trend subtracted for -th data in -th window box ().

The observed scaling law

| (4) |

is crucial within MFDFA to estimate the multifractal properties of a signal given by the profile of generalized Hurst exponents . The strength of multifractality present in data is usually studied as a spread

| (5) |

of some edge values of generalized Hurst exponent calculated at the fixed negative () and positive () moments respectively ().

In the case of stationary series, is proven to be a monotonically decreasing function and therefore [19]. However, many examples shown recently in literature for synthetic data [20, 21] as well as for realistic signals [18, 24] reveal that multifractal properties may lay far outside this simplest scenario and the spread , defined as the difference of generalized Hurst exponents calculated for small negative and large positive fluctuation moments, is not indicative in these cases.

A non-monotonic behavior of profile is observed for instance in nonstationary data what leads to twisted multifractal spectrum [18] if the Hölder description of multifractality is adopted with a help of Legendre transform [22, 23]. In the case of nonstationary data with periodicity, white or color noise added (see, e.g., [20, 21]) one may see domains where is either increasing or decreasing with , local maxima in are formed or even suggesting that big fluctuations may appear more often than small ones. It is contrary to observations in stationary data [19] where it should be the other way round. There are examples of realistic time series where the multifractal profile, despite small and insignificant spread, significantly expands in the central part for moment orders . One finds such behavior for instance for nonlinearly transformed financial data containing extreme events (see, e.g., [24]). The similar spread may correspond also to significantly different characteristics of the profile in the center for .

The above results convince that a traditional measurement of multifractality within MFDFA, based entirely on the spread may be misleading. Therefore we propose in this article an alternative measure of multifractal properties which takes into account the behavior of the multifractal profile as a whole for all -th order moments, not limited only to the edge values found at .

2 Introducing new measure

As pointed above, the new measure should be sensitive to behavior of the whole profile in the wide range of moments () and should not neglect the multiscaling properties within this range of ’s, contrary to the standard measure based on the spread alone which takes into account just the edge values of the generalized Hurst exponents .

In the simplest case of multifractal data with the abandoned effects of so called multifractal bias, generally discussed in [25], a natural extension of can be defined as a cumulated distance between the multifractal profile and the main Hurst exponent value for considered series.

One may write then a new measure in the integral form

| (6) |

It turns out that has an interesting interpretation of the scaling exponent in the new power law linking the geometric mean of detrended -th order fluctuations of the signal for all values with the size of the time window. Indeed, consider the normalized detrended -th moment of fluctuation defined as follows

| (7) |

where is the standard deviation of detrended fluctuation () in time window of length . Using the power law from Eq.(4) we may write the relationship

| (8) |

where is some function generally dependent on but independent on . Hence, using definition from Eq.(6)

| (9) |

Replacing by and by , where , the first integral in RHS of Eq.(9) can be approximated by a discrete sum

| (10) |

Comparing Eqs(9) and (10), one gets in the continuous limit

| (11) |

The latter relation builds after simple rearrangement the postulated power law

| (12) |

Note that the standard spread of generalized Hurst exponents values used in MFDFA to determine the multifractal content can also be interpreted in the above context as the scaling exponent in the power law

| (13) |

which links together with the ratio of the smallest () and the biggest () detrended deformed fluctuations. Hence, the scaling in Eq.(12) related with geometric mean of all detrended fluctuations , can be regarded as the modification of MFDFA method we call GMFDFA (geometric mean MFDFA).

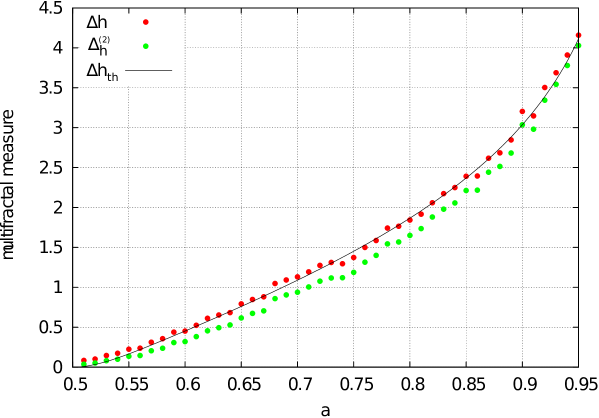

We will test the behavior of the new measure analyzing first the synthetic multifractal signals with apriori well known multiscaling properties. They were generated from the binomial random cascade algorithm [26] for the almost complete range of parameter describing the richness of multifractal content in synthetic signal () with a step . Fig. 1 shows the plot of analytical expectation in this model obtained from the relation [27]

| (14) |

and compared with two numerical findings, respectively for the standard and ”new” measure, calculated for from numerical simulation of profile. These plots prove that in a case of synthetic data new measure of multifractal content is qualitatively and quantitatively indistinguishable from the standard measure based on the spread of the edges .

The simple recipe for the new measure will have to be modified if so called multifractal bias effects are to be included in analysis [24, 25, 28]. Let us recall here main issues connected with such multifractal bias. It is defined as the continuous set of profiles calculated for a given system or signal, which do not correspond to multifractal properties of this system at some confidence level, despite . Such bias can be seen particularly in short signals where accidental fluctuations, not related with multifractal properties, contribute to fluctuation function and dominate over fluctuations having their origin in multifractal properties of the signal due to small statistics of short data. It raises the edge of the multifractal spread. On the other hand, the influence of large fluctuations in short data set can be suppressed since MFDFA algorithm may treat such fluctuations as longer trends and eliminate them. In both cases the observed spread is increased comparing with the corresponding value obtained for much longer data and grows with persistency in signal [25]. Another source of multifractal bias are nonlinear transformations performed on data which introduce always additional registered multifractal effect.

The level of multifractal bias in series can be calculated or simulated with a number of semi-analytic formulas provided in [25]. Note that deliberately we do not mix this bias effect here with so called spurious multifractality [20] caused by various external contaminations in signal or nonstationarities coming, e.g., from the influence of noise present in data.

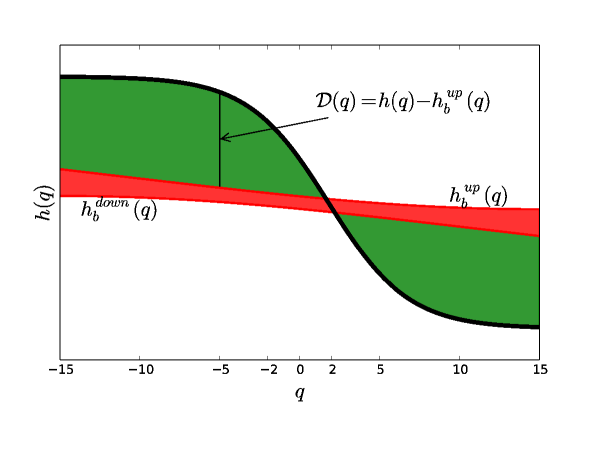

When taking multifractal bias into account, one has to generalize the formula in Eq.(6), replacing in there by the corresponding multifractal bias thresholds at the assumed confidence level ( throughout this article). Here are respectively the upper () and the lower () edge of the bias area (ribbon) explained in Fig. 2 (and shown also in Figs. 3,5–7). Simultaneously, profile in Eq. (6) has to be replaced by the observed (registered) values of the multifractal profile coming from direct application of Eq.(4) in MFDFA.

Let us define a distance function as

| (15) |

The modified measure in the case of multifractal bias present in signal can be taken as the average distance

| (16) |

and is presented as a green area in Fig. 2.

A new measure of multifractality generalizes the multifractal spread in such a way, that it can be used for particular profiles even if the standard measure could not be applied (e.g., when or ). One always gets describing multiscaling properties in a system for the whole range of fluctuation moments. The result means that the observed multifractal profile entirely lies in a biased ribbon domain for all moment orders and hence there are no expected real multifractal effects even if .

Note, however, that the maximum value of at which the new measure is calculated can not be too high, since then the contribution to the profile with high volatility may be dominated by domains where .

3 Application to synthetic and real time series

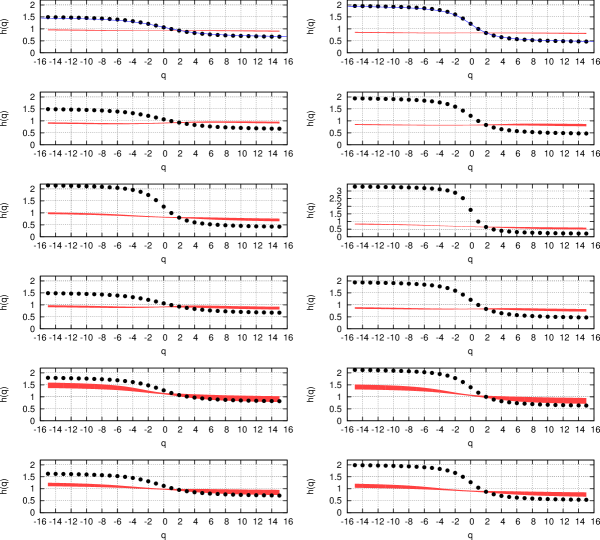

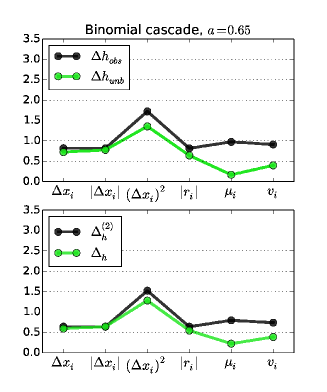

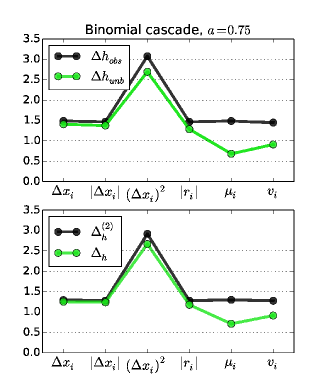

In order to present the qualities of proposed measure let us start with analysis of synthetic signals obtained from binomial cascade model, additionally, taking into account the multifractal bias. The calculated multifractal profiles , together with ribbon-like areas representing the multifractal bias are gathered in Fig. 3 for two values of cascade parameter and (). The values obtained for three measures applied to examples from Fig. 3: observed (biased) spread , unbiased spread and proposed measure are presented in Fig. 4. The actual values of multifractal measures corresponding to this figure are collected in Table. 1. Note, that in the traditional measurement of the multifractal spread (see Fig. 2), when and we have the following relations in terms of the edge values:

| (17) |

| (18) |

where are the observed (biased) edge values of the multifractal profile and are increments above (below) the multifractal bias level. The latter ones are assumed to be null if the edges satisfy .

Therefore, one gets

| (19) |

where is the bias level and is the unbiased spread of generalized Hurst exponents.

In case of synthetic multifractals, the new measure gives results similar to unbiased multifractal spread as seen from tabularized values in Table 1. Both measures ( and ) subtract the influence of finite size (FSE) and nonlinear transformation effects.

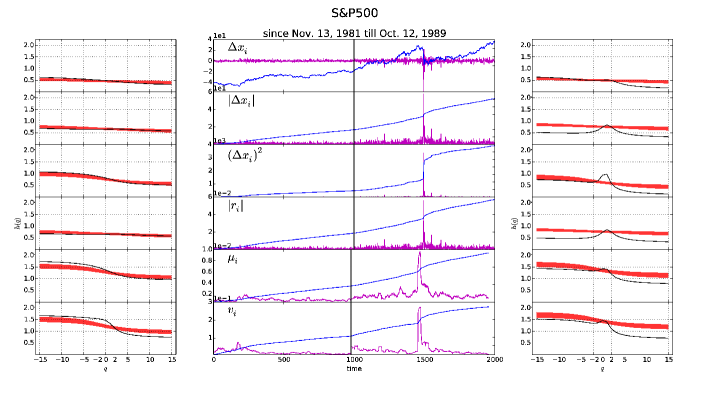

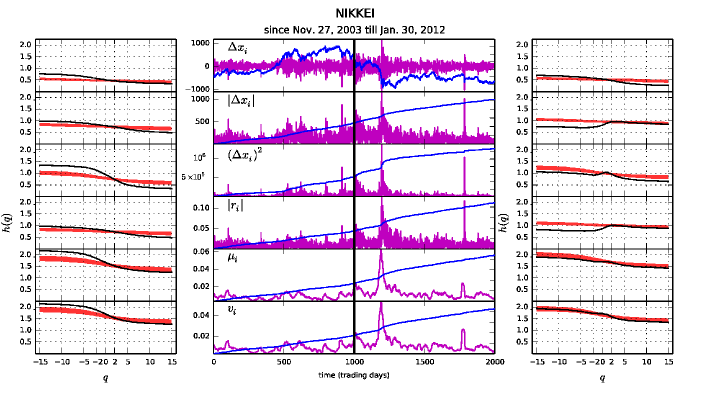

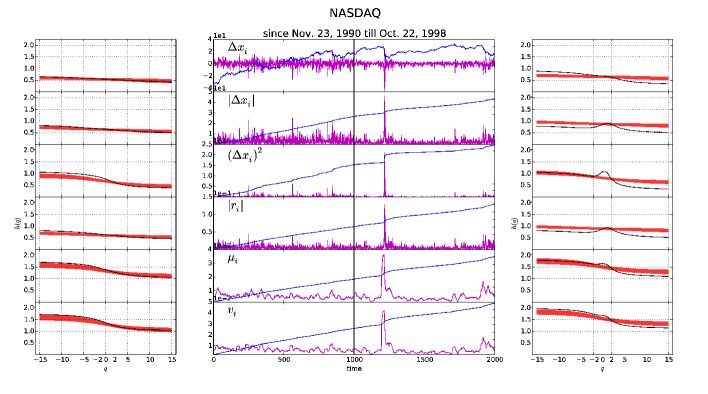

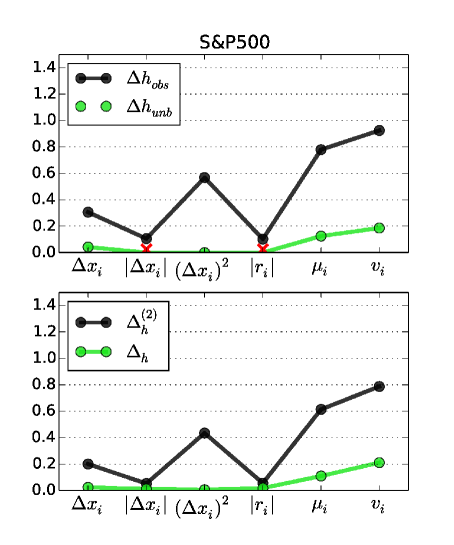

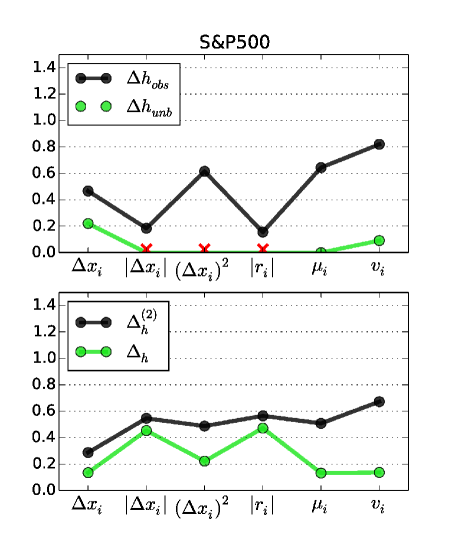

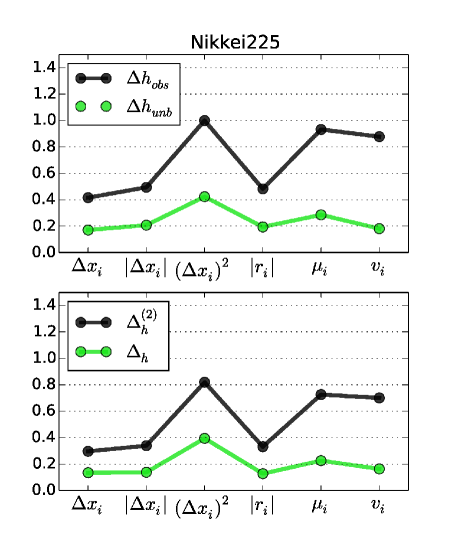

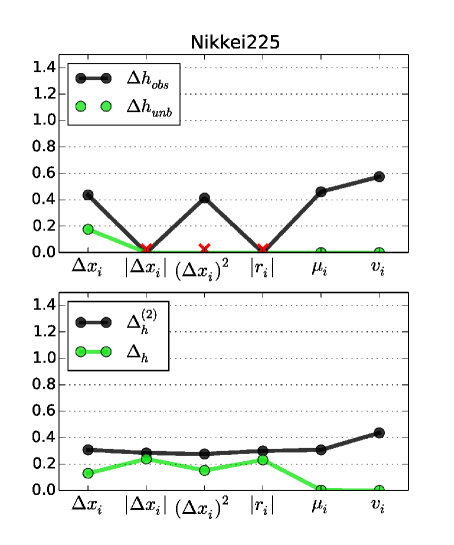

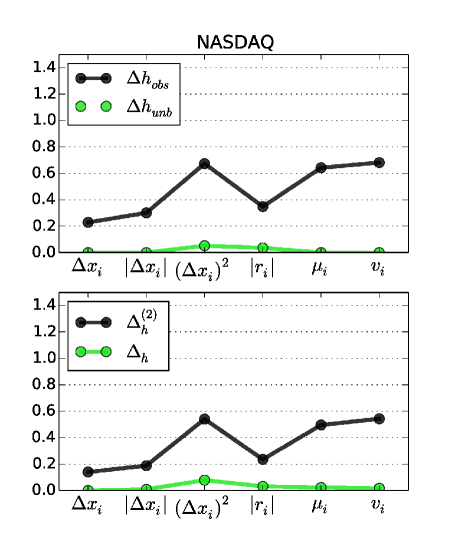

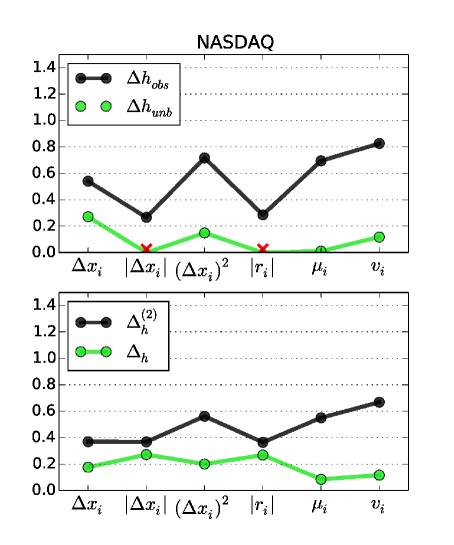

However, when a real complex system data are considered significant difference between new and standard measure can be observed. We present an evolution of three stock exchange indices: S&P500, Nikkei225 and NASDAQ in Figs. 5, 6 and 7 in two adjacent time windows. Investigated examples are chosen in such a way, that each right hand side window contains an extreme event, that is: ”Black Monday” of 19. October 1987 for S&P500, fall crash in 2008 for Nikkei225 and the crash of 30. August 1995 for NASDAQ, while the left hand side window corresponds to proceeding ”quiet” period on the stock market. All data are investigated for primary price increments and their nonlinear transformations: absolute price increments , quadratic increments , absolute returns and moving volatilities , , where and transaction days. The properties of multifractal profiles and multifractal bias coming from FSE and nonlinear transformation effects (red ribbon-like area) are presented in the first and last column in each figure. The quantitative comparison of multifractal measures based on and exponents calculated from these plots are collected in Tables 2–4 and plotted in Figs. 8–10.

Clear differences in multifractal features are visible between quiet and more dynamical periods (differences in shapes of profiles), which makes them excellent candidates to confront the qualities of three measures , and the proposed one . No qualitative difference between both periods is visible for primary data of Nikkei225 index, when the standard measure is applied. S&P500 and NASDAQ behave the other way round – one observes richer multifractal structure for them in dynamical period. For nonlinear transformations a strong non-monotonicity is mostly visible in dynamical period of all considered market indices leading in some cases ( and for Nikkei225) to inversed behavior, where (here ). Thus and the traditional measure is not indicative in such cases. The unbiased measure for and of dynamical period for S&P500, Nikkei225 and NASDAQ and just in case of Nikkei225 index causes also interpretation problems (). The above problematic situations are marked as cross-points in Figs. 8, 9, 10. Unexpectedly, moving volatile transformations and for dynamical period of Nikkei225 index, show complete lack of unbiased multifractal effects contrary to other considered indices.

The new measure (see bottom panel in Figs. 8, 9, 10) maintains validity of conclusions stated about multifractal features found in traditional manner for primary series . But simultaneously, all prior problems with interpretation of multifractal properties of transformed data disappear. The interesting results are seen for two leading world indices S&P500 and NASDAQ, particularly in dynamical zones. The standard measure could not provide any quantitative result to be compared with the corresponding behavior in ”quiet” zone (see Figs. 8–10, top panels). The new measure makes it possible (see Figs. 8–10, bottom panels). Moreover, one clearly notices that the index and its nonlinear transformations exhibit much richer multifractal content in a dynamical periods, then in the ”quiet” zone. Nikkei index is an exception, but also here a comparison between multifractal behaviors in two domains is possible only within the newly introduced measure (see Fig. 9).

4 Conclusions

This paper proposed the new method of measuring multifractal features in time series. The method is based on global analysis of generalized Hurst exponents . In the simplest case, when multifractal bias is not considered, the new measure is defined as cumulated distance of the generalized Hurst exponents from the main Hurst exponent , since is the only scaling exponent value one can refer to in monofractal case. The generalisation to the case with multifractal bias from FSE and nonlinear transformations was also provided.

An example of synthetically generated multifractals with binomial cascades shows, that the new measure reproduces the standard spread of multifractal profile , both before and after transformation. However, when multifractal bias is taken into account, the new measure seems to be much more resistant to disturbances coming from different sources.

We have presented the examples of real signals drawn from financial markets. These examples prove, that the new technique of measuring multi-scaling features in time series is useful, especially in very dynamical periods of complex system evolution, when simpler predecessor () ceases to work properly (see transformations , , in right panels of Figs. 8 and 9 and transformations , in right panel of Fig. 10). Obtained results seem to confirm, that whenever standard methods of detecting multifractality within MFDFA face problems, the newly proposed approach based on the scaling law from Eq. (12) detects it successfully.

| 0.82 | 0.82 | 1.72 | 0.82 | 0.98 | 0.91 | 1.49 | 1.47 | 3.08 | 1.43 | 1.49 | 1.45 | |

| 0.73 | 0.78 | 1.36 | 0.64 | 0.17 | 0.40 | 1.41 | 1.38 | 2.69 | 1.29 | 0.68 | 0.91 | |

| 0.61 | 0.68 | 1.49 | 0.66 | 0.76 | 0.69 | 1.27 | 1.31 | 2.86 | 1.26 | 1.26 | 1.26 | |

| 0.60 | 0.68 | 1.28 | 0.60 | 0.16 | 0.35 | 1.26 | 1.30 | 2.66 | 1.24 | 0.41 | 0.56 | |

| ”quiet” period | dynamical period | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.31 | 0.11 | 0.57 | 0.10 | 0.78 | 0.92 | 0.47 | 0.18 | 0.62 | 0.16 | 0.64 | 0.82 | |

| 0.04 | 0.00 | 0.13 | 0.19 | 0.22 | 0.00 | 0.09 | ||||||

| 0.20 | 0.05 | 0.43 | 0.06 | 0.61 | 0.79 | 0.29 | 0.55 | 0.49 | 0.56 | 0.51 | 0.67 | |

| 0.02 | 0.01 | 0.01 | 0.02 | 0.11 | 0.21 | 0.13 | 0.45 | 0.22 | 0.47 | 0.13 | 0.14 | |

| ”quiet” period | dynamical period | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.42 | 0.49 | 1.00 | 0.48 | 0.93 | 0.88 | 0.44 | 0.41 | 0.46 | 0.58 | |||

| 0.17 | 0.21 | 0.42 | 0.19 | 0.29 | 0.18 | 0.18 | 0.00 | 0.00 | ||||

| 0.30 | 0.34 | 0.82 | 0.33 | 0.73 | 0.70 | 0.31 | 0.28 | 0.28 | 0.30 | 0.31 | 0.44 | |

| 0.13 | 0.14 | 0.39 | 0.13 | 0.23 | 0.16 | 0.13 | 0.24 | 0.15 | 0.23 | 0.00 | 0.00 | |

| ”quiet” period | dynamical period | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.23 | 0.30 | 0.67 | 0.35 | 0.64 | 0.68 | 0.54 | 0.27 | 0.72 | 0.29 | 0.69 | 0.83 | |

| 0.00 | 0.00 | 0.05 | 0.04 | 0.00 | 0.00 | 0.27 | 0.15 | 0.01 | 0.12 | |||

| 0.14 | 0.19 | 0.54 | 0.24 | 0.50 | 0.54 | 0.37 | 0.37 | 0.56 | 0.36 | 0.55 | 0.67 | |

| 0.00 | 0.01 | 0.08 | 0.03 | 0.02 | 0.02 | 0.18 | 0.27 | 0.20 | 0.27 | 0.08 | 0.12 | |

References

- [1] J. W. Kantelhardt, S. A. Zschiegner, E. Koscielny-Bunde, S. Havlin, A. Bunde, H. E. Stanley, Physica A 316 (2002) 87

- [2] L. Telesca, V. Lapenna, M. Macchiato, Physica A 354 (2005) 629

- [3] L. Telesca, V. Lapenna, Tectonophysics 423 (2006) 115

- [4] M. S. Movahed, F. Ghasemi, S. Rahvar, M. R. R. Tabar, Phys. Rev. E 84 (2011) 021103

- [5] P. H. Figueiredo, E. Nogueira Jr., M. A. Moret, S. Coutinho, Physica A 389 (2010) 2090

- [6] S. Dutta, J. Stat. Mech. 12 (2010) P12021

- [7] I. T. Pedron, Journal of Physics: Conference Series 246 (2010) 012034

- [8] F. Liao, Y.-K. Jan, Jour. of Rehab. Res. and Develop. 48 (2011) 787

- [9] G. R. Jafari, P. Pedram, L. Hedayatifar, J. Stat. Mech. (2007) P04012

- [10] P. Oświȩcimka, J. Kwapień, I. Celińska, S. Drożdż , R. Rak, arXiv:1106.2902v1 [physics.data-an]

- [11] F. A. Hirpa, M. Gebremichael, T. M. Over, Water Resour. Res. 46 (2010) W12529

- [12] K. Matia, Y. Ashkenazy, and H. E. Stanley, Europhys. Lett. 61 (2003) 422

- [13] P. Oświȩcimka, J. Kwapień, and S. Drożdż, Physica A 347 (2005) 626

- [14] J. Kwapień, P. Oświȩcimka , and S. Drożdż, Physica A 350 (2005) 466

- [15] J. Jiang, K. Ma, and X. Cai, Physica A 378 (2007) 399

- [16] K. E. Lee and J. W. Lee, Physica A 383 (2007) 65

- [17] G. Lim, S. Kim, H. Lee, K. Kim, and D.-I. Lee, Physica A 386 (2007) 259

- [18] Ł. Czarnecki, D. Grech, Act. Phys. Pol. A 117 (2010) 4

- [19] J. W. Kantelhardt, arXiv:0804.0747v1 [physics.data-an] (2008)

- [20] J. Ludescher, M. I. Bogachev, J. W. Kantelhardt, A. Y. Schumann, A. Bunde, Physica A 390 (2011) 2480.

- [21] D. Gulich, L. Zunino, Physica A 391 (2012) 4100

- [22] J. Feder, Fractals, New York, Plenum Press (1988).

- [23] H.-O. Peitgen, H. Jürgens, D. Saupe, Chaos and Fractals, nd ed. Springer (2004).

- [24] D. Grech and G. Pamuła, Acta Phys. Pol. A 121 (2012) B-34

- [25] D. Grech, G. Pamuła, Physica A 392 (2013) (in print)

- [26] C. Meneveau, K. R. Sreenivasan, Phys. Rev. Lett. 59, (1987) 1424

- [27] A.-L. Barabasi, T. Vicsek, Multifractality of self-affine fractals, Phys. Rev. A 44, (1991) 2730.

- [28] D. Grech, G. Pamuła, arXiv:1307.2014 [physics.data-an]