Optimal sparse volatility matrix estimation for high-dimensional Itô processes with measurement errors

Abstract

Stochastic processes are often used to model complex scientific problems in fields ranging from biology and finance to engineering and physical science. This paper investigates rate-optimal estimation of the volatility matrix of a high-dimensional Itô process observed with measurement errors at discrete time points. The minimax rate of convergence is established for estimating sparse volatility matrices. By combining the multi-scale and threshold approaches we construct a volatility matrix estimator to achieve the optimal convergence rate. The minimax lower bound is derived by considering a subclass of Itô processes for which the minimax lower bound is obtained through a novel equivalent model of covariance matrix estimation for independent but nonidentically distributed observations and through a delicate construction of the least favorable parameters. In addition, a simulation study was conducted to test the finite sample performance of the optimal estimator, and the simulation results were found to support the established asymptotic theory.

doi:

10.1214/13-AOS1128keywords:

[class=AMS]keywords:

, and t1Supported in part by NSF Grants DMS-10-5635 and DMS-12-65203. t2Supported in part by NSF Career Award DMS-0645676 and NSF FRG Grant DMS-08-54975.

1 Introduction

Modern scientific studies in fields ranging from biology and finance to engineering and physical science often need to model complex dynamic systems where it is essential to incorporate internally or externally originating random fluctuations in the systems [Aït-Sahalia, Mykland and Zhang (2005), Mueschke and Andrews (2006) and Whitmore (1995)]. Continuous-time diffusion processes, or more generally, Itô processes, are frequently employed to model such complex dynamic systems. Data collected in the studies are treated as the processes observed at discrete time points with possible noise contamination. For example, the prices of financial assets are usually modeled by Itô processes, and the price data observed at high-frequencies are contaminated by market microstructure noise. In this paper we investigate estimation of the volatilities of the Itô processes based on noisy data.

Several volatility estimation methods have been developed in the past several years. For estimating a univariate integrated volatility, popular estimators include two-scale realized volatility [Zhang, Mykland and Aït-Sahalia (2005)], multi-scale realized volatility [Zhang (2006) and Fan and Wang (2007)], realized kernel volatility [Barndorff-Nielsen et al. (2008)] and pre-averaging based realized volatility [Jacod et al. (2009)]. For estimating a bivariate integrated co-volatility, common methods are the previous-tick approach [Zhang (2011)], the refresh-time scheme and realized kernel volatility [Barndorff-Nielsen et al. (2011)], the generalized synchronization scheme [Aït-Sahalia, Fan and Xiu (2010)] and the pre-averaging approach [Christensen, Kinnebrock and Podolskij (2010)]. Optimal volatility and co-volatility estimation has been investigated in the parametric or nonparametric setting [Aït-Sahalia, Mykland and Zhang (2005), Bibinger and Reiß (2011), Gloter and Jacod (2001a, 2001b), Reiß (2011) and Xiu (2010)]. These works are for estimating scalar volatilities or volatility matrices of small size. Wang and Zou (2010) and Tao et al. (2011) studied the problem of estimating a large sparse volatility matrix based on noisy high-frequency financial data. Fan, Li and Yu (2012) employed a large volatility matrix estimator based on high-frequency data for portfolio allocation. The large volatility matrix estimation is a high-dimensional extension of the univariate case. It can be also considered as a generalization of large covariance matrix estimation for i.i.d. data to volatility matrix estimation for dependent data with measurement errors. Despite recent progress on volatility matrix estimation, there has been remarkably little fundamental theoretical study on optimal estimation of large volatility matrices. Consistent estimation of large matrices based on high-dimensional data usually requires some sparsity, and the sparsity may naturally result from appropriate formulation of some low-dimensional structures in the high-dimensional data. For example, in large volatility matrix estimation with high-frequency financial data sparsity means that a relatively small number of market factors play a dominate role in driving volatility movements and capturing the market risk. In this paper we establish the optimal rate of convergence for large volatility matrix estimation under various matrix norms over a wide range of classes of sparse volatility matrices. We expect that our work will stimulate further theoretical and methodological research as well as more application orientated study on large volatility matrix estimation.

Specifically we consider the problem of estimating the sparse integrated volatility matrix for a -dimensional Itô process observed with additive noises at equally spaced discrete time points. The minimax upper bound is obtained by constructing a new procedure through a combination of the multi-scale and threshold approaches and by studying its risk properties. We first construct a multi-scale volatility matrix estimator and show that its elements obey subGaussian tails with a convergence rate . Then we threshold the constructed estimator to obtain a threshold volatility matrix estimator and derive its convergence rate. The upper bound depends on and through .

A key step in obtaining the optimal rate of convergence is the derivation of the minimax lower bound for the high-dimensional Itô process with measurement errors. We succeed in establishing the risk lower bound in three steps. First we select a particular subclass of Itô processes with a zero drift and a constant volatility matrix so that the volatility matrix estimation problem becomes a covariance matrix estimation problem where the observed data are dependent and have measurement errors; second, take a special transformation of the observations to convert the problem into a new covariance matrix estimation problem where the observed data have no measurement errors and are independent but not identically distributed, with covariance matrices equal to the constant volatility matrix plus an identity matrix multiplying by a shrinking factor depending on the sample size ; third, adopt the minimax lower bound technique developed in Cai and Zhou (2012) for sparse covariance matrix estimation based on i.i.d. data to establish a minimax lower bound for independent but nonidentically distributed observations. The minimax lower bound matches the upper bound obtained by the new procedure up to a constant factor, and thus the upper bound is rate-optimal.

The volatility matrix estimation is closely related to large covariance matrix estimation which received lots of attentions recently in the literature. While the covariance matrix plays a key role in statistical analysis, its classic estimation procedures, like the sample covariance matrix estimator, may behave very poorly when the matrix size is comparable to or exceeds the sample size. To overcome the curse of dimensionality, various regularization techniques have been developed for estimation of large covariance matrices in recent years. Wu and Pourahmadi (2003) explored nonparametric estimation of large covariance matrices by local stationarity. Ledoit and Wolf (2004) proposed to boost diagonal elements and downgrade off-diagonal elements of the sample covariance matrix estimator. Huang et al. (2006) used a penalized likelihood method to estimate large covariance matrices. Yuan and Lin (2007) considered large covariance matrix estimation in a Gaussian graph model. Bickel and Levina (2008a, 2008b) developed regularization methods by banding or thresholding the sample covariance matrix estimator when the matrix size is comparable to the sample size. El Karoui (2008) employed a graph model approach to characterize sparsity and investigated consistent estimation of large covariance matrices. Fan, Fan and Lv (2008) utilized factor models for estimating large covariance matrices. Johnstone and Lu (2009) studied consistent estimation of leading principal components in principal component analysis. Lam and Fan (2009) established sparsistency and convergence rates for large covariance matrix estimation. Cai, Zhang and Zhou (2010) and Cai and Zhou (2012) studied minimax estimation of covariance matrices when both sample size and matrix size are allowed to go to infinity and derived optimal convergence rates for estimating decaying or sparse covariance matrices.

The rest of the paper proceeds as follows. Section 2 presents the model and the data and constructs volatility matrix estimators. Section 3 establishes the asymptotic theory under sparsity for the constructed matrix estimators as both sample size and matrix size go to infinity. Section 4 derives the minimax lower bound for estimating a large sparse volatility matrix and shows that the threshold volatility matrix estimator asymptotically achieves the minimax lower bound. Thus combining results in Sections 3 and 4 together, we establish the optimality for large sparse volatility matrix estimation. Section 5 features a simulation study to illustrate the finite sample performances of the volatility matrix estimators. To facilitate the reading we relegate all proofs to Section 6 and two Appendix sections, where we first provide the main proofs of the theorems in Section 6 and then collect additional technical proofs in the two appendices.

2 Volatility matrix estimation

2.1 The model set-up

Suppose that is an Itô process following the model

| (1) |

where stochastic processes , , and are defined on a filtered probability space with filtration satisfying the usual conditions, is a -dimensional standard Brownian motion with respect to , is a -dimensional drift vector, is a by matrix, and and are assumed to be predictable processes with respect to .

We assume that the continuous-time process is observed with measurement errors only at equally spaced discrete time points; that is, the observed discrete data obey

| (2) |

where are noises with mean zero.

Let be the volatility matrix of . We are interested in estimating the following integrated volatility matrix of ,

based on noisy discrete data , , .

2.2 Estimator

Let be an integer and be the largest integer . We divide time points into nonoverlap groups , . Denote by the number of time points in . Obviously, the value of is either or . For , we write the th time point in as , . With each , we define the volatility matrix estimator

Here in (2.2), to account for noises in data , we use to subsample the data and define . To reduce the noise effect we average volatility matrix estimators to define one-scale volatility matrix estimator

| (4) |

Let for some positive constant , and , . We use each to define a one-scale volatility matrix estimator and then combine them together to form a multi-scale volatility matrix estimator

| (5) |

where

| (6) |

which satisfy

The one-scale matrix estimator in (4) was studied in Wang and Zou (2010), and the multi-scale scheme (5)–(6) in the univariate case was investigated in Zhang (2006).

We threshold to obtain our final volatility matrix estimator

| (7) |

where is a threshold value to be specified in Theorem 2.

In the estimation construction we use only time scales corresponding to of order to form increments and averages. In Section 3 we will demonstrate that the data at these scales contain essential information for estimating and show that is asymptotically an optimal estimator of .

3 Asymptotic theoryfor volatility matrix estimators

First we fix notation for our asymptotic analysis. Let be a -dimensional vector and be a by matrix, and define their norms

For the case of matrix, the norm is called the matrix spectral norm. is equal to the square root of the largest eigenvalue of ,

| (8) |

and

| (9) |

For symmetric , (8)–(9) imply that , and is equal to the largest absolute eigenvalue of .

Second we state some technical conditions for the asymptotic analysis. {longlist}[A3.]

Assume for some constants and , and that and in models (1)–(2) are independent. Suppose that , , is a strictly stationary -dependent multivariate time series with mean zero and , where is a fixed integer, and is a finite positive constant. Assume further that are subGaussian in the sense that there exist constants and such that for all and with ,

| (10) |

Assume that there exist positive constants and such that

Further we assume with probability one for ,

| (11) |

Assume that is sparse in the sense that

| (12) |

where is a positive random variable with finite second moment, , and is a deterministic function with slow growth in such as .

Condition A1 allows noises to have cross sectional correlations as well as cross temporal correlations. In particular we may have any contemporaneous correlations between and as well as lagged serial auto-correlations for individual noise and lagged serial cross-correlations between and with lags up to . As in covariance matrix estimation, the subGaussianity (10) is essentially required to obtain an optimal convergence rate depending on through . It is obvious that independent normal noises satisfy these assumptions. The constraint is needed to obtain a high-dimensional minimax lower bound; otherwise the problem will be similar to usual asymptotics with large but fixed ; is to ensure the existence of a consistent estimator of . Condition A2 is to impose proper assumptions on the drift and volatility of the Itô process so that we can obtain subGaussian tails for the quadratic forms of , which together with the subGaussianity (10) are used to derive subGaussian tails for the elements of the volatility matrix estimator . Condition A3 is a common sparsity assumption required for consistently estimating large matrices [Bickel and Levina (2008b), Cai and Zhou (2012), and Johnstone and Lu (2009)].

The following two theorems establish asymptotic theory for the estimators and defined by (5) and (7), respectively.

Theorem 1

Remark 1.

Theorem 1 establishes subGaussian tails for the elements of the matrix estimator . It is known that, when univariate or bivariate continuous Itô processes are observed with measurement errors at discrete time points, the optimal convergence rates for estimating a univariate integrated volatility or a bivariate integrated co-volatility are [Gloter and Jacod (2001a, 2001b), Reiß (2011), and Xiu (2010)]. The factor in the exponent of the tail probability bound on the right-hand side of (13) indicates a convergence rate for , which matches the optimal convergence rate for the univariate integrated volatility estimation. This is in contrast to sub-optimal convergence rate results in the literature where a convergence rate was obtained; see, for example, Fan, Li and Yu (2012), Wang and Zou (2010), Zhang, Mykland and Aït-Sahalia (2005), and Zheng and Li (2011).

Theorem 2

For the threshold estimator in (7) we choose threshold with any fixed constant , where is the constant in the exponent of the tail probability bound on the right-hand side of (13). Denote by the set of distributions of , , , from models (1)–(2) satisfying conditions A1–A3. Then as ,

where is a constant free of and .

Remark 2.

For sparse covariance matrix estimation, Cai and Zhou (2012) has shown that the threshold estimator in Bickel and Levina (2008b) is rate-optimal, and the optimal convergence rate depends on and through . The convergence rate obtained in Theorem 2 depends on the sample size and the matrix size through . Note that is the optimal convergence rate for estimating a univariate integrated volatility or a bivariate integrated co-volatility based on noisy data. Since our estimation problem is a generalization of covariance matrix estimation for i.i.d. data to volatility matrix estimation for an Itô process with measurement errors on one hand and a high-dimensional extension of univariate volatility estimation on the other hand, it is interesting to see that the convergence rate in Theorem 2 is a natural blend of convergence rates in the two cases. Also as Theorem 2 implies that the maximum of the eigenvalue differences between and is bounded by . Thus if the eigenvalues of all exceed , asymptotically the eigenvalues of are positive, and is a positive definite matrix. In particular, if goes to zero as and go to infinity, and is positive definite and well conditioned, then is asymptotically positive definite and well conditioned. In Section 4 we will establish the minimax lower bound for estimating and show that the convergence rate in Theorem 2 is optimal.

4 Optimal convergence rate

This section establishes the minimax lower bound for estimating under models (1)–(2) and shows that asymptotically achieves the lower bound and thus is optimal. We state the minimax lower bound for estimating with under the matrix spectral norm as follows.

Theorem 3

Remark 3.

Note that the lower bound convergence rate in Theorem 3 matches the convergence rate of the estimator obtained in Theorem 2. Combining Theorems 2 and 3 together we conclude that the optimal convergence rate is , and the estimator in (7) achieves the optimal convergence rate. Moreover, such optimal estimation results hold for any matrix norm with . Indeed, it can be shown that under the conditions of Theorems 2 and 3, we have that as and go to infinity,

| (17) | |||

where and are constants in Theorems 2 and 3, respectively, is the threshold estimator given by (7) with the threshold value specified in Theorem 2 and the infimum is taken over all estimators based on the data , , , from models (1)–(2).

Remark 4.

Condition (15) is a technical condition that we need to establish the minimax lower bound. It is compatible with conditions A1 and A3 regarding the constraint on and as well as the slow growth of in the sparsity condition (12).

Models (1)–(2) are complicated nonparametric models, and the observations from the models are dependent and have subGaussian measurement errors. To derive the minimax lower bound for models (1)–(2), we find a special subclass of the models to attain the minimax lower bound of the models. Such an approach is often referred to as the method of hardest subproblem. Since generally a minimax problem has lower bound no larger than any of its subproblems, the mentioned special subclass corresponds to the hardest subproblem and is referred to as the least favorable submodel. We will show in Sections 4.1 and 4.2 that the least favorable submodel for models (1)–(2) can be taken as i.i.d. Gaussian measurement errors and process with zero drift and constant volatilities. To establish the minimax lower bound for the least favorable submodel, luckily we are able to find a nice trick in Section 4.1 that transforms the minimax lower bound problem for the least favorable submodel into a new covariance matrix estimation problem with independent but nonidentically distributed observations. Cai and Zhou (2012) have developed an approach combining both Le Cam’s method and Assouad’s lemma, which are two popular methods to establish minimax lower bounds, to derive the minimax lower bound for estimating a large sparse covariance matrix based on i.i.d. observations. We adopt the approach in Cai and Zhou (2012) to derive the minimax lower bound for the new covariance matrix estimation problem with independent but nonidentically distributed observations, which is stated in Theorem 4 of Section 4.2. The derived minimax lower bound in Theorem 4 corresponds to the least favorable submodel and thus is the minimax lower bound for models (1)–(2). Therefore, we prove Theorem 3.

4.1 Model transformation

We take a subclass of models (1)–(2) as follows. For the Itô processes we let and be a constant matrix ; for the noises we let , , , be i.i.d. random variables with distribution, where is specified in condition A1. Then , and the sparsity condition (12) becomes

| (18) |

where and is given by (12).

Let , and . Then models (1)–(2) become

| (19) |

and . As are dependent, we take differences in (19) and obtain

| (20) |

here . For matrix , its elements are independent at different rows but correlated at the same rows. At the th row, elements , , have covariance matrix , where is a tridiagonal matrix with along diagonal entries, next to diagonal entries and elsewhere. is a Toeplitz matrix [Wilkinson (1988)] that can be diagonalized as follows:

| (21) |

where are eigenvalues with expressions

| (22) |

and is an orthogonal matrix formed by the eigenvectors of . Using (21) we transform the th row of the matrix by , and obtain

For , let

Then as diagonalizes , are independent, with ; because are i.i.d. normal random variables with mean zero and variance , and is orthogonal, are i.i.d. standard normal random variables.

Put (20) in a matrix form and right multiply by on both sides to obtain

Denote by , and the column vectors of the matrices , and , respectively. Then the above matrix equation is equivalent to

| (23) |

where and .

From (23) we have that the data transformed random vectors are independent with , where with .

4.2 Lower bound

We convert the minimax lower bound problem stated in Theorem 3 into a much simpler problem of estimating based on the observations from model (23), where are constant matrices satisfying (18) and for some constant . We denote the new minimax estimation problem by , and the theorem below derives its minimax lower bound.

Theorem 4

Remark 5.

As we discussed in Remarks 1 and 2 in Section 3, due to noise contamination, the optimal convergence rate depends on sample size through , instead of for covariance matrix estimation. For the univariate case, discrete sine transform was used to construct a realized volatility estimator [Aït-Sahalia, Mykland and Zhang (2005) and Curci and Corsi (2012)] and reveal some intrinsic insight into how the convergence rate is obtained [Munk and Schmidt-Hieber (2010)]. The similar insight for the high-dimensional case can be seen from the transformation in Section 4.1, which converts model (20) with noisy data into model (23) where the independent random vector follows a multivariate normal distribution with mean zero and covariance matrix , . The transformation via orthogonal matrix , which diagonalizes Toeplitz matrix and is equal to normalized by [see Salkuyeh (2006)], corresponds to a discrete sine transform, with (23) in frequency domain and corresponding to the discrete sine transform of the data at frequency . By comparing the order of , we derive that only at those frequencies with up to , the transformed data are informative for estimating , and we use these number of to estimate and obtain convergence rate. In fact, we have seen the phenomenon in Section 2.1 where the scales used in the construction of in (5) correspond to , with both and of order .

5 A simulation study

A simulation study was conducted to compare the finite sample performances of the MSRVM estimator in (5) and the threshold MSRVM estimator in (7) with those of the ARVM estimator and the threshold ARVM estimator introduced in Wang and Zou (2010). We generated at discrete time points , , from model (1) with by the Euler scheme, where univariate standard Brownian motions were stimulated by the normalized partial sums of independent standard normal random variables, was taken to be a Cholesky decomposition of

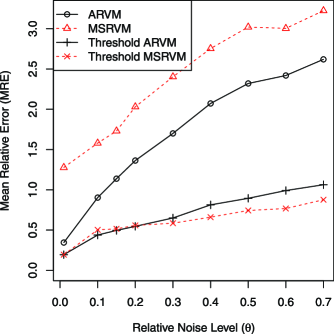

was independently generated from a uniform distribution on , , , were independently drawn from a geometric Ornstein–Uhlenbeck process satisfying and are independent one-dimensional standard Brownian motions that are independent of in model (1). We computed by the average of . We simulated noises independently from a normal distribution with mean 0 and standard deviation , , where is the relative noise level ranging from to . Finally data were obtained by adding the simulated to the generated according to model (2). Using the simulated data we computed the MSRVM estimator and the threshold MSRVM estimator as well as the ARVM estimator and the threshold ARVM estimator. In the simulation study we took and . We repeated the whole simulation procedure times. For a given matrix estimator , a relative matrix spectral norm error was used to measure its performance. We evaluated the mean relative matrix spectral norm error (MRE) by the average of the relative matrix spectral norm errors over the repetitions. As in Wang and Zou (2010) we selected tuning parameters like threshold of the estimators by minimizing the respective MREs.

Figure 1 is the plots of MRE versus relative noise level for the MSRVM, ARVM, threshold MSRVM and threshold ARVM estimators. The basic findings are that while the MREs of the threshold MSRVM and threshold ARVM estimators are comparable at low relative noise levels, the threshold MSRVM estimator has smaller MRE than the threshold ARVM estimator at high relative noise levels; regardless of relative noise levels, the threshold MSRVM and threshold ARVM estimators have significantly smaller MREs than the MSRVM and ARVM estimators. The simulation results support the theoretical conclusions that the threshold procedure is needed for constructing consistent estimators of , and the threshold MSRVM estimator is asymptotically optimal, while the threshold ARVM estimator is suboptimal.

We point out that it is important to have a data-driven choice of tuning parameters for volatility matrix estimator defined in (7). This is largely an open issue. We briefly describe an approach for developing a data-dependent selection of the tuning parameters as follows. For data observed from models (1)–(2), we may divide the whole data time interval into subintervals , and partition data into subsamples , , over the corresponding time periods. To estimate integrated volatility over the th period, according to the procedure described in Section 2.2, we use the th subsample to construct volatility matrix estimator, which is denoted by to emphasize its dependence on and , where denotes the length of , is a threshold value and is an integer that specifies scales used in the volatility matrix estimator given by (7). We predict one period ahead volatility matrix estimator by current period volatility matrix estimator and compute the predication error. We minimize the sum of the spectral norms of the predication errors to select and . For example, we often have high-frequency financial data over many days, and it is natural to use data in each day to estimate the integrated volatility matrix over the corresponding day. We predict one day ahead daily volatility matrix estimator by current daily volatility matrix estimator and compute the predication error. The tuning parameters are then selected by minimizing the sum of the spectral norms of the prediction errors.

6 Proofs

Denote by ’s generic constants whose values are free of and and may change from appearance to appearance. Let and be the maximum and minimum of and , respectively. For two sequences and we write if there exist positive constants and free of and such that . Without loss of generality we take in the construction of given by (5) in Section 2.2.

6.1 Proofs of Theorems 1 and 2

Let

which are random vectors corresponding to the data, the Itô process and the noises at the time point , , , and . Note that we choose index to specify that the analyses are associated with the study of here and below. We decompose defined in (4) as follows:

and thus from (5) we obtain the corresponding decomposition for ,

where the and terms are associated with the process only, the and terms are related to the noises only and the terms denoted by , , and depend on both and .

Now we may heuristically explain the basic ideas for proving Theorems 1 and 2 as follows. With the expression (6.1) we prove the tail probability result for in Theorem 1 by establishing tail probabilities for these and terms in the following three propositions whose proofs will be given in Appendix I.

Proposition 5

Under the assumptions of Theorem 1, we have for and positive in a neighbor of ,

Proposition 6

Under the assumptions of Theorem 1, we have for and positive in a neighbor of ,

Proposition 7

Under the assumptions of Theorem 1, we have for and positive in a neighbor of ,

Because are quadratic forms in the process only, we derive their tail probability in Proposition 5 from the boundedness of the drift and volatility in condition A2; as are quadratic forms in the noises only, we establish the tail probability of in Proposition 7 from the subGaussianity of imposed by condition A1; and are bilinear forms in and , thus we obtain the tail probabilities for and in Proposition 6 from the subGaussian tails of and as well as the independence between and given by condition A1. Since is the matrix estimator obtained by thresholding , we use the tail probability result in Theorem 1 and the sparsity of to analyze and control its matrix norm for proving Theorem 2.

Proof of Theorem 2 Define

As the matrix norm of a symmetric matrix is bounded by its -norm, then

| (27) |

We can bound as follows:

where the second inequality is due to the fact that the sparsity of implies

which are the respective bounds on the number of those entries on each row with absolute values larger than or equal to and the sum of those absolute entries on each row with magnitudes less than ; see Lemma 1 in Wang and Zou (2010). The rest of the proof is to show that , a negligible term. Indeed, the threshold rule indicates that if and if , thus

For term , we have

where the third inequality is from Theorem 1, and the last inequality is due to with .

On the other hand, we can bound term as follows:

where the third inequality is due to Hölder’s inequality, the fourth inequality is from Theorem 1 and

| (28) |

and the last inequality is due to the fact that with .

To complete the proof we need to show (28). As in Zhang, Mykland and Aït-Sahalia (2005), we adjust to account for the noise variances. Let

| (29) |

and define

| (30) |

which are the average realized volatility matrix (ARVM) estimators where the convergence rates for any finite moments of are derived in Wang and Zou [(2010), Theorem 1]. Applying Theorem 1 of Wang and Zou (2010) to the fourth moment of , we have for and ,

| (31) | |||

From (5), (6) and (30) together with simple algebraic manipulations we can express by as follows:

and thus

| (32) |

6.2 Proofs of Theorems 3 and 4

Section 4.1 shows that Theorem 3 is a consequence of Theorem 4. The proof of Theorem 4 is similar to but much more involved than the proof of Theorem 2 in Cai and Zhou (2012) which considered only i.i.d. observations. It contains four major steps. In the first step we construct in detail a finite subset of the parameter space in the minimax problem such that the difficulty of estimation over is essentially the same as that of estimation over , where is the class of constant matrices satisfying (18) and for constant . The second step applies the lower bound argument in Cai and Zhou [(2012), Lemma 3] to the carefully constructed parameter set . In the third step we calculate the factor defined in (6.2) below and the total variation affinity between two average of products of independent but nonidentically distributed multivariate normals. The final step combines together the results in steps 2 and 3 to obtain the minimax lower bound.

Step 1: Construct parameter set . Set , where denotes the smallest integer greater than or equal to , and let be the collection of all row vectors such that for and or for under the constraint (to be specified later). Each element is treated as an matrix with the th row of equal to . Let . Define to be the set of all elements in such that each column sum is less than or equal to . For each and each , define a symmetric matrix by making the th row of equal to , th column equal to and the rest of the entries . Then each component of can be uniquely associated with a matrix . Define , and let be fixed (the exact value of will be chosen later). For each with and , we associate with a volatility matrix by

| (33) |

For simplicity we assume that in the definition of the parameter space for the minimax problem ; otherwise we replace in (33) by with a small constant . Finally we define to be a collection of covariance matrices as

| (34) |

Note that each matrix has value along the main diagonal and contains an submatrix, say, , at the upper right corner, at the lower left corner and elsewhere; each row of the submatrix is either identically (if the corresponding value is ) or has exactly nonzero elements with value .

Now we specify the values of and :

| (35) |

where is a fixed small constant that we require

| (36) |

and

| (37) |

where satisfies

| (38) |

since

Note that and satisfy ,

| (39) |

and consequently every is diagonally dominant and positive definite, and . Thus we have .

Step 2: Apply the general lower bound argument. Let be independent with

where , , and we denote the joint distribution by . Applying Lemma 3 in Cai and Zhou (2012) to the parameter space , we have

| (40) |

where we use to denote the total variation of ,

and

| (42) |

where and .

Step 3: Bound the affinity and per comparison loss. We need to bound the two factors and in (40). A lower bound for is given by the following proposition whose proof is the same as that of Lemma 5 in Cai and Zhou (2012).

Proposition 8

For defined in equation (6.2) we have

A lower bound for is provided by the proposition below. Since its proof is long and very much involved, the proof details are collected in Appendix II.

Proposition 9

Let be independent with , , with and denote the joint distribution by . For and , define as in (42). Then there exists a constant such that

uniformly over .

6.3 Proof of (3) for optimal convergence rate under general matrix norm

The Riesz–Thorin interpolation theorem [Thorin (1948)] implies for ,

| (43) |

Set and , then (43 ) yields for . When is symmetric, (8) shows that . Then immediately we have , which means that for a symmetric matrix estimator, an upper bound under the matrix norm is also an upper bound under the general matrix norm. Thus, as is symmetric, Theorem 2 indicates that for ,

Now consider the lower bound under the general matrix norm for . We will show

where denotes any matrix estimators of , and any symmetric matrix estimators of . (6.3) indicates that it is enough to consider estimators of symmetric matrices.

For symmetric , (9) shows that . For , , by duality we have . Also since is always between and , applying (43) we obtain that . This means that within the class of symmetric matrix estimators, a lower bound under the matrix norm is also a lower bound under the general matrix norm. Thus (6.3) and Theorem 3 together imply that for ,

To complete the proof we need to prove (6.3). The first inequality of (6.3) is obvious. For a given matrix estimator we project it onto the parameter space of the minimax problem by minimizing the matrix norm of over all in the parameter space. Denote its projection by . Since the parameter space consists of symmetric matrices, is symmetric. Hence

where the second inequality is from the triangle inequality and the third one follows from the definition of . Since the above inequality holds for every , we have

which is equivalent to the second inequality of (6.3).

Appendix I Proofs of Propositions 5–7

I.1 Proof of Proposition 5

The definition of in (6.1) shows

and

With the above expression for we obtain that for and ,

where the third inequality is from Lemma 10 below and the last inequality is due to the fact that and the maximum distance between consecutive grids in is bounded by .

Lemma 10

Under model (1) and condition A2, for any sequence satisfying , we have for and small ,

Let and . Then is a stochastic integral with respect to and has the same quadratic variation as . Let . With and we have

with quadratic variation . Also have quadratic variations

Define

Then

is a continuous-time martingale and has quadratic variation

and hence Lévy’s martingale characterization of Brownian motion shows that is a one-dimensional Brownian motion; see Karatzas and Shreve [(1991), Theorem 3.16]. We can apply Lemma 3 in Fan, Li and Yu (2012) to each and obtain for ,

| (47) | |||

Similarly for , we define

Then

are continuous-time martingales with quadratic variations

and hence Lévy’s martingale characterization of Brownian motion implies that are one-dimensional Brownian motions. We can apply Lemma 3 in Fan, Li and Yu (2012) to each of and and obtain for ,

| (48) | |||

Note that

and thus

Combining (I.1) and above inequality we conclude

| (49) | |||

On the other hand,

| (50) | |||

From condition A2 we have that and are bounded by , and thus

| (51) |

Applications of Hölder’s inequality lead to

| (52) | |||

| (53) | |||

From (I.1) we have

| (54) | |||

where the last inequality is due to the bounds obtained from (I.1) and (51)–(I.1) for the four respective probability terms. We handle the last two terms on the right-hand side of (I.1) as follows. If [or equivalently ], using condition A2 (which implies and ) and (I.1), we get

| (55) | |||

which is bounded by , if , which is true provided that

| (56) |

Putting together (I.1) and the probability bound from (I.1)–(56), we conclude that if

| (57) | |||

From condition A2 we have and

Then (I.1) and above inequality imply that if

| (58) |

This proves the lemma with and for satisfies (58).

If (58) is not satisfied, we have

Then the tail probability bound in the lemma obeys

and we easily show the probability inequality in the lemma by choosing and , where and satisfy .

Finally taking and we establish the tail probability, regardless whether satisfies (58) or not, and complete the proof.

I.2 Proof of Proposition 6

As the proofs for and are similar, we give arguments only for . Lemma 11 below establishes the tail probability for . Using the expression of in terms of given by (6.1) and applying Lemma 11, we obtain

where .

Lemma 11

Under the assumptions of Theorem 1, we have for and ,

Simple algebraic manipulations show

The lemma is proved if we establish tail probabilities for both and . Due to similarity, we give the arguments only for . Since and are independent, conditional on the whole path of , is the weighted sum of . Hence,

| (59) | |||

where the inequality is due to the subGaussianity of defined in (10), is the variance of , is given by (6.1) with an expression

and

From the definition of and conditions A1–A2, we have , and on . Thus for small we have

On the other hand, from (I.1) (in the proof of Proposition 5) we have

and thus

Finally substituting (I.2) and (I.2) into (I.2) we obtain

I.3 Proof of Proposition 7

Denote by the correlation between and . From the expression of in terms of given by (6.1) we obtain that is bounded by

Lemma 12

Under the assumptions of Theorem 1, we have for ,

From the definition of in (6.1), we have

and

| (62) |

Note that , and

Hence,

| (63) | |||

To prove the lemma we need to derive the four tail probabilities on the right-hand side of (I.3). Below we will establish the tail probabilities for and by using large deviation results for the case of -dependent random variables in Saulis and Statulevičius (1991). Because of similarity, we give arguments only for the tail probabilities of and .

First for , from the definition of in (6) we have

| (64) |

where . The -dependence of in condition A1 indicates that , , are -dependent, is the average of , , and Lemma 14 below calculates and . Also for any integer ,

where the first inequality is from the Cauchy–Schwarz inequality, and the second inequality is from the subGaussian tails of and , which imply that their -moments are bounded by . Applying Theorem 4.30 in Saulis and Statulevičius (1991) to -dependent random variables we obtain

| (65) |

Plugging (65) with into (I.3) we establish the tail probability for

As , , are serially -dependent, that is, for any integers and , and integer sets and , and are independent if every integer in differs by more than from any integer in . Since for large enough, if integers and differ by more than , for two integer sets and , every element in one integer set must be more than apart from any element in the other integer set. Then and are independent, and thus , , are serially -dependent. Also for any integer ,

where the first inequality is from the Cauchy–Schwarz inequality, and the second inequality is from the subGaussian tails of and . Applying theorem 4.16 in Saulis and Statulevičius (1991) we derive a bound on the th cumulant of , and then using Lemmas 2.3 and 2.4 in Saulis and Statulevičius (1991) we establish the tail probability for as follows:

| (67) |

Since and have the same tail probabilities as and given by (I.3) and (67), respectively, combining them with (I.3) we conclude

Lemma 13

Under the assumptions of Theorem 1, we have for ,

| (68) |

First consider term:

Due to similarity, we show the tail probabilities only for and . Lemma 14 below calculates the mean and variances of and . Since and have, respectively, the same structures as and used in the proof Lemma 12, the arguments for establishing the tail probabilities for and can be used to derive the tail probability bounds for and . Consequently we obtain that

| (69) |

As has the same structure as , similarly we can establish a tail probability for as follows:

| (70) |

Since

Lemma 14

Under the assumptions of Theorem 1 and for large enough so that , we have

Because , and are independent, so

For and , we have

With the -dependence of , we directly compute the variances of and as follows:

We evaluate the variance of as follows:

where the inequality is from the fact that the -dependence of implies zero expectations of for lags larger than .

Similarly, we have

where the inequality is from the fact that the -dependence of implies zero expectations of for lags larger than .

Appendix II Proof of Proposition 9

We break the proof into a few major technical lemmas which are proved in Sections II.2–II.3. Without loss of generality we consider only the case and prove that there exists a constant such that .

The following lemma turns the problem of bounding the total variation affinity into a chi-square distance calculation. Denote the projection of to by and to by . More generally, for a subset , we define a projection of to a subset of by . A particularly useful example of set is for which we use . and are defined similarly. We define the set . For , , and , let

and which depends actually on the value of , not values of , and for the parameter space constructed in Section 6.2. Define the mixture distribution

| (71) |

In other words, is the mixture distribution over all with varying over all possible values while all other components of remain fixed. Define

Lemma 15

If there is a constant such that

| (72) |

then .

We can prove Lemma 15 using the same arguments as the proof of Lemma 8 in Cai and Zhou (2012). To complete the proof of Proposition 9 we need to verify only equation (72).

II.1 Technical lemmas for proving equation (72)

From the definition of in equation (71) and with and , implies is a product of multivariate normal distributions each with a covariance matrix,

| (73) |

where is uniquely determined by with

Let be the number of columns of with column sum equal to and . Since , the total number of s in the upper triangular matrix, we have , which implies . From equations (71) and with and , is an average of number of products of multivariate normal distributions each with covariance matrix of the following form:

| (74) |

where with nonzero elements of equal to and the submatrix is the same as the one for given in (73). Note that the indices and are dropped from and to simplify the notation.

With Lemma 15 in place, it remains to establish equation (72) in order to prove Proposition 9. The following lemma is useful for calculating the cross product terms in the chi-square distance between Gaussian mixtures. The proof of the lemma is straightforward and is thus omitted.

Lemma 16

Let be the density function of for and , respectively. Then

Let , or , be two covariance matrices of the form (74). Note that , or , differs from each other only in the first row/column. Then , or , has a very simple structure. The nonzero elements only appear in the first row/column, and in total there are nonzero elements. This property immediately implies the following lemma which makes the problem of studying the determinant in Lemma 16 relatively easy.

Lemma 17

Let , and , be matrices of the form (74). Define to be the number of overlapping ’s between and on the first row, and

There are index subsets and in with and such that

and the matrix has rank with two identical nonzero eigenvalues when .

Let

| (75) |

where is defined in (73) and determined by , and and have the first row and , respectively. We drop the indices , and from to simplify the notation. Define

It is a subset of in which the element can pick both and as the first row to form parameters in . From Lemma 16 the left-hand side of equation (72) can be written as

| (76) | |||

where is defined in step 1.

Lemma 18

II.2 Proof of equation (72)

We are now ready to establish equation (72) using Lemma 18. It follows from equation (77) in Lemma 18 that

Recall that is the number of overlapping ’s between and on the first row. It is easy to see that has the hypergeometric distribution with

| (79) | |||

Equations (78) and (II.2) imply

where the third inequality is from (38), the fifth inequality is due to (37) and the last inequality is obtained by setting .

II.3 Proof of Lemma 18

Now we are ready to establish equation (78). For simplicity we will write matrix norm as below. It is important to observe that due to the simple structure of . Let be an eigenvalue of . It is easy to see that

since and from equation (39).

Since

| (84) |

we write

where

| (86) |

Define

| (87) |

From equations (II.3) and (84)–(87) we have

The above result and (83) indicate that the proof of Lemma 18 is complete if we show

| (88) | |||

where and depend on the values of and . We dropped the indices , and from to simplify the notation.

Let . Let be the number of columns of with column sum at least for which two rows cannot freely take value or in this column. Then we have . Without loss of generality we assume that . Since , the total number of s in the upper triangular matrix by the construction of the parameter set, we thus have , which immediately implies . Thus we have for every nonnegative integer ,

from equation (II.2), which immediately implies

| (89) | |||

Note that (38) implies

and thus we can bound the first term on the right-hand side of (II.3),

where the second inequality is from (36) and (37). We will show that the second term on the right-hand side of (II.3) is negligible and hence establish (II.3). Indeed, since we have just shown that

the second term on the right-hand side of (II.3) is bounded by

where the second equality is from the fact that (15) and (35) together with indicate

and then

References

- Aït-Sahalia, Fan and Xiu (2010) {barticle}[mr] \bauthor\bsnmAït-Sahalia, \bfnmYacine\binitsY., \bauthor\bsnmFan, \bfnmJianqing\binitsJ. and \bauthor\bsnmXiu, \bfnmDacheng\binitsD. (\byear2010). \btitleHigh-frequency covariance estimates with noisy and asynchronous financial data. \bjournalJ. Amer. Statist. Assoc. \bvolume105 \bpages1504–1517. \biddoi=10.1198/jasa.2010.tm10163, issn=0162-1459, mr=2796567 \bptokimsref \endbibitem

- Aït-Sahalia, Mykland and Zhang (2005) {barticle}[auto:STB—2013/06/05—13:45:01] \bauthor\bsnmAït-Sahalia, \bfnmY.\binitsY., \bauthor\bsnmMykland, \bfnmP. A.\binitsP. A. and \bauthor\bsnmZhang, \bfnmL.\binitsL. (\byear2005). \btitleHow often to sample a continuous-time process in the presence of market microstructure noise. \bjournalReview of Financial Studies \bvolume18 \bpages351–416. \bptokimsref \endbibitem

- Barndorff-Nielsen et al. (2008) {barticle}[mr] \bauthor\bsnmBarndorff-Nielsen, \bfnmOle E.\binitsO. E., \bauthor\bsnmHansen, \bfnmPeter Reinhard\binitsP. R., \bauthor\bsnmLunde, \bfnmAsger\binitsA. and \bauthor\bsnmShephard, \bfnmNeil\binitsN. (\byear2008). \btitleDesigning realized kernels to measure the ex post variation of equity prices in the presence of noise. \bjournalEconometrica \bvolume76 \bpages1481–1536. \biddoi=10.3982/ECTA6495, issn=0012-9682, mr=2468558 \bptokimsref \endbibitem

- Barndorff-Nielsen et al. (2011) {barticle}[mr] \bauthor\bsnmBarndorff-Nielsen, \bfnmOle E.\binitsO. E., \bauthor\bsnmHansen, \bfnmPeter Reinhard\binitsP. R., \bauthor\bsnmLunde, \bfnmAsger\binitsA. and \bauthor\bsnmShephard, \bfnmNeil\binitsN. (\byear2011). \btitleMultivariate realised kernels: Consistent positive semi-definite estimators of the covariation of equity prices with noise and non-synchronous trading. \bjournalJ. Econometrics \bvolume162 \bpages149–169. \biddoi=10.1016/j.jeconom.2010.07.009, issn=0304-4076, mr=2795610 \bptokimsref \endbibitem

- Bibinger and Reiß (2011) {bmisc}[mr] \bauthor\bsnmBibinger, \bfnmMarkus\binitsM. and \bauthor\bsnmReiß, \bfnmM.\binitsM (\byear2011). \bhowpublishedSpectral estimation of covolatility from noisy observations using local weights. Preprint, Humboldt-Universität zu Berlin. \bptokimsref \endbibitem

- Bickel and Levina (2008a) {barticle}[mr] \bauthor\bsnmBickel, \bfnmPeter J.\binitsP. J. and \bauthor\bsnmLevina, \bfnmElizaveta\binitsE. (\byear2008a). \btitleRegularized estimation of large covariance matrices. \bjournalAnn. Statist. \bvolume36 \bpages199–227. \biddoi=10.1214/009053607000000758, issn=0090-5364, mr=2387969 \bptokimsref \endbibitem

- Bickel and Levina (2008b) {barticle}[mr] \bauthor\bsnmBickel, \bfnmPeter J.\binitsP. J. and \bauthor\bsnmLevina, \bfnmElizaveta\binitsE. (\byear2008b). \btitleCovariance regularization by thresholding. \bjournalAnn. Statist. \bvolume36 \bpages2577–2604. \biddoi=10.1214/08-AOS600, issn=0090-5364, mr=2485008 \bptokimsref \endbibitem

- Cai, Zhang and Zhou (2010) {barticle}[mr] \bauthor\bsnmCai, \bfnmT. Tony\binitsT. T., \bauthor\bsnmZhang, \bfnmCun-Hui\binitsC.-H. and \bauthor\bsnmZhou, \bfnmHarrison H.\binitsH. H. (\byear2010). \btitleOptimal rates of convergence for covariance matrix estimation. \bjournalAnn. Statist. \bvolume38 \bpages2118–2144. \biddoi=10.1214/09-AOS752, issn=0090-5364, mr=2676885 \bptokimsref \endbibitem

- Cai and Zhou (2012) {barticle}[auto:STB—2013/06/05—13:45:01] \bauthor\bsnmCai, \bfnmT.\binitsT. and \bauthor\bsnmZhou, \bfnmH.\binitsH. (\byear2012). \btitleOptimal rates of convergence for sparse covariance matrix estimation. \bjournalAnn. Statist. \bvolume40 \bpages2389–2420. \bptokimsref \endbibitem

- Callen, Govindaraj and Xu (2000) {barticle}[mr] \bauthor\bsnmCallen, \bfnmJeffrey\binitsJ., \bauthor\bsnmGovindaraj, \bfnmSuresh\binitsS. and \bauthor\bsnmXu, \bfnmLin\binitsL. (\byear2000). \btitleLarge time and small noise asymptotic results for mean reverting diffusion processes with applications. \bjournalEconom. Theory \bvolume16 \bpages401–419. \biddoi=10.1007/PL00004090, issn=0938-2259, mr=1778742 \bptokimsref \endbibitem

- Christensen, Kinnebrock and Podolskij (2010) {barticle}[mr] \bauthor\bsnmChristensen, \bfnmKim\binitsK., \bauthor\bsnmKinnebrock, \bfnmSilja\binitsS. and \bauthor\bsnmPodolskij, \bfnmMark\binitsM. (\byear2010). \btitlePre-averaging estimators of the ex-post covariance matrix in noisy diffusion models with non-synchronous data. \bjournalJ. Econometrics \bvolume159 \bpages116–133. \biddoi=10.1016/j.jeconom.2010.05.001, issn=0304-4076, mr=2720847 \bptokimsref \endbibitem

- Curci and Corsi (2012) {barticle}[mr] \bauthor\bsnmCurci, \bfnmGiuseppe\binitsG. and \bauthor\bsnmCorsi, \bfnmFulvio\binitsF. (\byear2012). \btitleDiscrete sine transform for multi-scale realized volatility measures. \bjournalQuant. Finance \bvolume12 \bpages263–279. \biddoi=10.1080/14697688.2010.490561, issn=1469-7688, mr=2881619 \bptokimsref \endbibitem

- El Karoui (2008) {barticle}[mr] \bauthor\bsnmEl Karoui, \bfnmNoureddine\binitsN. (\byear2008). \btitleOperator norm consistent estimation of large-dimensional sparse covariance matrices. \bjournalAnn. Statist. \bvolume36 \bpages2717–2756. \biddoi=10.1214/07-AOS559, issn=0090-5364, mr=2485011 \bptokimsref \endbibitem

- Fan, Fan and Lv (2008) {barticle}[mr] \bauthor\bsnmFan, \bfnmJianqing\binitsJ., \bauthor\bsnmFan, \bfnmYingying\binitsY. and \bauthor\bsnmLv, \bfnmJinchi\binitsJ. (\byear2008). \btitleHigh dimensional covariance matrix estimation using a factor model. \bjournalJ. Econometrics \bvolume147 \bpages186–197. \biddoi=10.1016/j.jeconom.2008.09.017, issn=0304-4076, mr=2472991 \bptokimsref \endbibitem

- Fan, Li and Yu (2012) {barticle}[mr] \bauthor\bsnmFan, \bfnmJianqing\binitsJ., \bauthor\bsnmLi, \bfnmYingying\binitsY. and \bauthor\bsnmYu, \bfnmKe\binitsK. (\byear2012). \btitleVast volatility matrix estimation using high-frequency data for portfolio selection. \bjournalJ. Amer. Statist. Assoc. \bvolume107 \bpages412–428. \biddoi=10.1080/01621459.2012.656041, issn=0162-1459, mr=2949370 \bptokimsref \endbibitem

- Fan and Wang (2007) {barticle}[mr] \bauthor\bsnmFan, \bfnmJianqing\binitsJ. and \bauthor\bsnmWang, \bfnmYazhen\binitsY. (\byear2007). \btitleMulti-scale jump and volatility analysis for high-frequency financial data. \bjournalJ. Amer. Statist. Assoc. \bvolume102 \bpages1349–1362. \biddoi=10.1198/016214507000001067, issn=0162-1459, mr=2372538 \bptokimsref \endbibitem

- Gloter and Jacod (2001a) {barticle}[mr] \bauthor\bsnmGloter, \bfnmArnaud\binitsA. and \bauthor\bsnmJacod, \bfnmJean\binitsJ. (\byear2001a). \btitleDiffusions with measurement errors. I. Local asymptotic normality. \bjournalESAIM Probab. Stat. \bvolume5 \bpages225–242 (electronic). \biddoi=10.1051/ps:2001110, issn=1292-8100, mr=1875672 \bptokimsref \endbibitem

- Gloter and Jacod (2001b) {barticle}[mr] \bauthor\bsnmGloter, \bfnmArnaud\binitsA. and \bauthor\bsnmJacod, \bfnmJean\binitsJ. (\byear2001b). \btitleDiffusions with measurement errors. II. Optimal estimators. \bjournalESAIM Probab. Stat. \bvolume5 \bpages243-260. \bptokimsref \endbibitem

- Huang et al. (2006) {barticle}[mr] \bauthor\bsnmHuang, \bfnmJianhua Z.\binitsJ. Z., \bauthor\bsnmLiu, \bfnmNaiping\binitsN., \bauthor\bsnmPourahmadi, \bfnmMohsen\binitsM. and \bauthor\bsnmLiu, \bfnmLinxu\binitsL. (\byear2006). \btitleCovariance matrix selection and estimation via penalised normal likelihood. \bjournalBiometrika \bvolume93 \bpages85–98. \biddoi=10.1093/biomet/93.1.85, issn=0006-3444, mr=2277742 \bptokimsref \endbibitem

- Jacod et al. (2009) {barticle}[mr] \bauthor\bsnmJacod, \bfnmJean\binitsJ., \bauthor\bsnmLi, \bfnmYingying\binitsY., \bauthor\bsnmMykland, \bfnmPer A.\binitsP. A., \bauthor\bsnmPodolskij, \bfnmMark\binitsM. and \bauthor\bsnmVetter, \bfnmMathias\binitsM. (\byear2009). \btitleMicrostructure noise in the continuous case: The pre-averaging approach. \bjournalStochastic Process. Appl. \bvolume119 \bpages2249–2276. \biddoi=10.1016/j.spa.2008.11.004, issn=0304-4149, mr=2531091 \bptokimsref \endbibitem

- Johnstone and Lu (2009) {barticle}[mr] \bauthor\bsnmJohnstone, \bfnmIain M.\binitsI. M. and \bauthor\bsnmLu, \bfnmArthur Yu\binitsA. Y. (\byear2009). \btitleOn consistency and sparsity for principal components analysis in high dimensions. \bjournalJ. Amer. Statist. Assoc. \bvolume104 \bpages682–693. \biddoi=10.1198/jasa.2009.0121, issn=0162-1459, mr=2751448 \bptnotecheck related\bptokimsref \endbibitem

- Karatzas and Shreve (1991) {bbook}[mr] \bauthor\bsnmKaratzas, \bfnmIoannis\binitsI. and \bauthor\bsnmShreve, \bfnmSteven E.\binitsS. E. (\byear1991). \btitleBrownian Motion and Stochastic Calculus, \bedition2nd ed. \bseriesGraduate Texts in Mathematics \bvolume113. \bpublisherSpringer, \blocationNew York. \biddoi=10.1007/978-1-4612-0949-2, mr=1121940 \bptokimsref \endbibitem

- Lam and Fan (2009) {barticle}[mr] \bauthor\bsnmLam, \bfnmClifford\binitsC. and \bauthor\bsnmFan, \bfnmJianqing\binitsJ. (\byear2009). \btitleSparsistency and rates of convergence in large covariance matrix estimation. \bjournalAnn. Statist. \bvolume37 \bpages4254–4278. \biddoi=10.1214/09-AOS720, issn=0090-5364, mr=2572459 \bptokimsref \endbibitem

- Ledoit and Wolf (2004) {barticle}[mr] \bauthor\bsnmLedoit, \bfnmOlivier\binitsO. and \bauthor\bsnmWolf, \bfnmMichael\binitsM. (\byear2004). \btitleA well-conditioned estimator for large-dimensional covariance matrices. \bjournalJ. Multivariate Anal. \bvolume88 \bpages365–411. \biddoi=10.1016/S0047-259X(03)00096-4, issn=0047-259X, mr=2026339 \bptokimsref \endbibitem

- Mueschke and Andrews (2006) {barticle}[auto:STB—2013/06/05—13:45:01] \bauthor\bsnmMueschke, \bfnmN. J.\binitsN. J. and \bauthor\bsnmAndrews, \bfnmM. J.\binitsM. J. (\byear2006). \btitleInvestigation of scalar measurement error in diffusion and mixing processes. \bjournalExperiments in Fluids \bvolume40 \bpages165–175. \bptokimsref \endbibitem

- Munk and Schmidt-Hieber (2010) {bincollection}[mr] \bauthor\bsnmMunk, \bfnmAxel\binitsA. and \bauthor\bsnmSchmidt-Hieber, \bfnmJohannes\binitsJ. (\byear2010). \btitleLower bounds for volatility estimation in microstructure noise models. In \bbooktitleBorrowing Strength: Theory Powering Applications—A Festschrift for Lawrence D. Brown. \bseriesInst. Math. Stat. Collect. \bvolume6 \bpages43–55. \bpublisherIMS, \blocationBeachwood, OH. \bidmr=2798510 \bptokimsref \endbibitem

- Reiß (2011) {barticle}[mr] \bauthor\bsnmReiß, \bfnmMarkus\binitsM. (\byear2011). \btitleAsymptotic equivalence for inference on the volatility from noisy observations. \bjournalAnn. Statist. \bvolume39 \bpages772–802. \biddoi=10.1214/10-AOS855, issn=0090-5364, mr=2816338 \bptokimsref \endbibitem

- Salkuyeh (2006) {barticle}[mr] \bauthor\bsnmSalkuyeh, \bfnmDavod Khojasteh\binitsD. K. (\byear2006). \btitlePositive integer powers of the tridiagonal Toeplitz matrices. \bjournalInt. Math. Forum \bvolume1 \bpages1061–1065. \bidissn=1312-7594, mr=2256665 \bptokimsref \endbibitem

- Saulis and Statulevičius (1991) {bbook}[mr] \bauthor\bsnmSaulis, \bfnmL.\binitsL. and \bauthor\bsnmStatulevičius, \bfnmV. A.\binitsV. A. (\byear1991). \btitleLimit Theorems for Large Deviations. \bseriesMathematics and Its Applications (Soviet Series) \bvolume73. \bpublisherKluwer Academic, \blocationDordrecht. \biddoi=10.1007/978-94-011-3530-6, mr=1171883 \bptokimsref \endbibitem

- Tao et al. (2011) {barticle}[mr] \bauthor\bsnmTao, \bfnmMinjing\binitsM., \bauthor\bsnmWang, \bfnmYazhen\binitsY., \bauthor\bsnmYao, \bfnmQiwei\binitsQ. and \bauthor\bsnmZou, \bfnmJian\binitsJ. (\byear2011). \btitleLarge volatility matrix inference via combining low-frequency and high-frequency approaches. \bjournalJ. Amer. Statist. Assoc. \bvolume106 \bpages1025–1040. \biddoi=10.1198/jasa.2011.tm10276, issn=0162-1459, mr=2894761 \bptokimsref \endbibitem

- Thorin (1948) {barticle}[mr] \bauthor\bsnmThorin, \bfnmG. O.\binitsG. O. (\byear1948). \btitleConvexity theorems generalizing those of M. Riesz and Hadamard with some applications. \bjournalMedd. Lunds Univ. Mat. Sem. \bvolume9 \bpages1–58. \bidmr=0025529 \bptokimsref \endbibitem

- Wang and Zou (2010) {barticle}[mr] \bauthor\bsnmWang, \bfnmYazhen\binitsY. and \bauthor\bsnmZou, \bfnmJian\binitsJ. (\byear2010). \btitleVast volatility matrix estimation for high-frequency financial data. \bjournalAnn. Statist. \bvolume38 \bpages943–978. \biddoi=10.1214/09-AOS730, issn=0090-5364, mr=2604708 \bptokimsref \endbibitem

- Whitmore (1995) {barticle}[pbm] \bauthor\bsnmWhitmore, \bfnmG. A.\binitsG. A. (\byear1995). \btitleEstimating degradation by a Wiener diffusion process subject to measurement error. \bjournalLifetime Data Anal. \bvolume1 \bpages307–319. \bidissn=1380-7870, pmid=9385107 \bptokimsref \endbibitem

- Wilkinson (1988) {bbook}[mr] \bauthor\bsnmWilkinson, \bfnmJ. H.\binitsJ. H. (\byear1988). \btitleThe Algebraic Eigenvalue Problem. \bpublisherOxford Univ. Press, \blocationNew York. \bidmr=0950175 \bptokimsref \endbibitem

- Wu and Pourahmadi (2003) {barticle}[mr] \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. and \bauthor\bsnmPourahmadi, \bfnmMohsen\binitsM. (\byear2003). \btitleNonparametric estimation of large covariance matrices of longitudinal data. \bjournalBiometrika \bvolume90 \bpages831–844. \biddoi=10.1093/biomet/90.4.831, issn=0006-3444, mr=2024760 \bptokimsref \endbibitem

- Xiu (2010) {barticle}[mr] \bauthor\bsnmXiu, \bfnmDacheng\binitsD. (\byear2010). \btitleQuasi-maximum likelihood estimation of volatility with high frequency data. \bjournalJ. Econometrics \bvolume159 \bpages235–250. \biddoi=10.1016/j.jeconom.2010.07.002, issn=0304-4076, mr=2720855 \bptokimsref \endbibitem

- Yuan and Lin (2007) {barticle}[mr] \bauthor\bsnmYuan, \bfnmMing\binitsM. and \bauthor\bsnmLin, \bfnmYi\binitsY. (\byear2007). \btitleModel selection and estimation in the Gaussian graphical model. \bjournalBiometrika \bvolume94 \bpages19–35. \biddoi=10.1093/biomet/asm018, issn=0006-3444, mr=2367824 \bptokimsref \endbibitem

- Zhang (2006) {barticle}[mr] \bauthor\bsnmZhang, \bfnmLan\binitsL. (\byear2006). \btitleEfficient estimation of stochastic volatility using noisy observations: A multi-scale approach. \bjournalBernoulli \bvolume12 \bpages1019–1043. \biddoi=10.3150/bj/1165269149, issn=1350-7265, mr=2274854 \bptokimsref \endbibitem

- Zhang (2011) {barticle}[mr] \bauthor\bsnmZhang, \bfnmLan\binitsL. (\byear2011). \btitleEstimating covariation: Epps effect, microstructure noise. \bjournalJ. Econometrics \bvolume160 \bpages33–47. \biddoi=10.1016/j.jeconom.2010.03.012, issn=0304-4076, mr=2745865 \bptokimsref \endbibitem

- Zhang, Mykland and Aït-Sahalia (2005) {barticle}[mr] \bauthor\bsnmZhang, \bfnmLan\binitsL., \bauthor\bsnmMykland, \bfnmPer A.\binitsP. A. and \bauthor\bsnmAït-Sahalia, \bfnmYacine\binitsY. (\byear2005). \btitleA tale of two time scales: Determining integrated volatility with noisy high-frequency data. \bjournalJ. Amer. Statist. Assoc. \bvolume100 \bpages1394–1411. \biddoi=10.1198/016214505000000169, issn=0162-1459, mr=2236450 \bptokimsref \endbibitem

- Zheng and Li (2011) {barticle}[mr] \bauthor\bsnmZheng, \bfnmXinghua\binitsX. and \bauthor\bsnmLi, \bfnmYingying\binitsY. (\byear2011). \btitleOn the estimation of integrated covariance matrices of high dimensional diffusion processes. \bjournalAnn. Statist. \bvolume39 \bpages3121–3151. \biddoi=10.1214/11-AOS939, issn=0090-5364, mr=3012403 \bptokimsref \endbibitem