On the numerical solution of some nonlinear stochastic differential equations using the semi-discrete method

Abstract.

In this paper we are interested in the numerical solution of stochastic differential equations with non negative solutions. Our goal is to construct explicit numerical schemes that preserve positivity, even for super linear stochastic differential equations. It is well known that the usual Euler scheme diverges on super linear problems and the Tamed-Euler method does not preserve positivity. In that direction, we use the Semi-Discrete method that the first author has proposed in two previous papers. We propose a new numerical scheme for a class of stochastic differential equations which are super linear with non negative solution. In this class of stochastic differential equations belongs the Heston -model that appears in financial mathematics, for which we prove through numerical experiments the “optimal” order of strong convergence at least of the Semi-Discrete method.

Key words and phrases:

Semi-Discrete method, super-linear drift and diffusion, Holder continuous, model, order of convergence.AMS subject classification: 65C30, 65C20, 60H10

1. Introduction.

Throughout, let and be a complete probability space, meaning that the filtration satisfies the usual conditions, i.e. is right continuous and includes all null sets. Let be a one dimensional Wiener process adapted to the filtration Consider the following stochastic differential equation (SDE),

| (1.1) |

where the coefficients are measurable functions such that (1.1) has a unique strong solution and is independent of all , a.s. SDE (1.1) has non autonomous coefficients, i.e. depend explicitly on

To be more precise, we assume the existence of a predictable stochastic process such that ([25, Definition 2.1]),

and

The drift coefficient is the infinitesimal mean of the process and the diffusion coefficient is the infinitesimal variance of the process SDEs of the form (1.1) have rarely explicit solutions, thus numerical approximations are necessary for simulations of the paths or for approximation of functionals of the form where can be for example in the area of finance, the discounted payoff of European type derivative.

We are interested in strong approximations (mean-square) of (1.1), in the case of super or sub linear drift and diffusion coefficients. This kind of numerical schemes have applications in many areas, such as simulating scenarios, filtering, visualizing stochastic dynamics (see for instance [17, Section 4] and references therein), have theoretical interest (they provide fundamental insight for weak-sense schemes) and generally do not involve simulations over long-time periods or of a significant number of trajectories.

We present some models that are not linear both in the drift and diffusion coefficient:

-

•

The following linear drift model had been initially proposed for the dynamics of the inflation rate in ([6, Relation 50]) and has taken its name, CIR, by the initials of the authors in the aforementioned paper. It is used in the field of finance as a description of the stochastic volatility procedure in the Heston model ([13]), but also belongs to the fundamental family of SDEs that approximate Markov jump processes ([8]). The CIR model is described by the following SDE,

(1.2) where is independent of all a.s. and the parameters are positive. Parameter is the level of the interest rate where the drift is zero, meaning that when is below the drift is positive, whereas in the other case is negative. As grows, the range of the positive drift becomes wider. Parameter defines the slope of the drift. The condition is necessary for the stationarity of the process When is negative, the main term of the slope, is positive and given the diffusion the process blows up. The condition implied by the Feller test ([9, Case (ii),p.173]) is necessary and sufficient for the process not to reach the boundary zero in finite time.

-

•

The model ([14]) or the inverse square root process ([1]), that is used for modeling stochastic volatility,

(1.3) where is independent of , a.s. and . The conditions and are necessary and sufficient for the stationarity of the process and such that zero and infinity is not attainable in finite time ([1, Appendix A]).

-

•

The constant elasticity of variance model ([5]), which is used for pricing assets,

(1.4) where is independent of , a.s., and . SDE (1.4) has a unique strong solution if and only if and takes values in The case corresponds to CIR model (1.2), whereas corresponds to a Brownian motion, i.e. the famous Black-Scholes model ([3]).

-

•

Superlinear models, i.e. models of the form (1.1) where one of the coefficients is superlinear, i.e. when we have that

(1.5) or

(1.6) where

For some of the aforementioned problems there are methods of simulation ([4], [28]). However, if a full sample path of the SDE has to be simulated or the SDEs under study are a part of a bigger system of SDEs, then numerical schemes are in general more effective.

Problems like (1.2), (1.3) and (1.4) are meant for non-negative values, since they represent rates or pricing values. Thus “good” numerical schemes preserve positivity ([2], [20]). The explicit Euler scheme has not that property, since its increments are conditional Gaussian. For example, the transition probability of the Euler scheme in case of (1.2) reads as

thus, even in the first step there is an event of negative values with positive probability. We refer to ([22]), between other papers, that considers Euler type schemes, modifications of them to overcome the above drawback, and the importance of positivity. Thus, for the same problem, the truncated Euler scheme ([7]) has been proposed, as well as a modification of it, ([15]), where in a step the numerical scheme can leave but is forced to come back in the next steps.

One more drawback, that appears in case of superlinear problems (1.5) or (1.6), like (1.3), is that the moments of the scheme may explode ([19, Theorem 1]). A method that overcomes this drawback is the Tamed-Euler method, ([17, Relation 4]) and reads: and

| (1.7) |

for every and all (1.7) is explicit, does not explode and converges strongly to the exact solution of SDE (1.1), i.e.,

| (1.8) |

for some where are continuous versions of (1.7) through linear interpolation. It still does not preserve positivity.

For the aforementioned reasons there is an interest in the construction of numerical schemes to simulate the corresponding SDEs, that have the desired properties. An attempt to this direction has been made by the first author in ([11], [12]) suggesting the Semi-Discrete method (where, briefly saying, we discretize a part of the SDE). Using this method in ([11]) the author produced a new numerical scheme (but not unique in this situation) for the first aforementioned problem and proves the strong convergence of the scheme in mean square sense. Later on, in ([12]), the author generalizes the idea of the Semi-Discrete method and uses this generalization to approximate a class of super linear problems, suggesting a new numerical scheme that preserves positivity in that case, proving again the strong convergence in the mean square sense.

A basic feature of the Semi-Discrete method is that it is explicit, compared to other interesting, but implicit methods ([27],[26]), and converges strongly in the mean square sense to the exact solution of the original SDE. Moreover, the Semi-Discrete method preserves positivity ([11, Section 3]) and it does not explode in some super-linear problems ([12, Section 3]). The purpose of this paper is to generalize further the method to include non-autonomous coefficients, in (1.1) and cover cases like that of the Heston -model.

2. The setting and the main result.

Assumption A Let be such that where satisfy the following conditions for any such that where the constant depends on and denotes the maximum of

Let the equidistant partition and We propose the following Semi-Discrete numerical scheme

| (2.1) |

where we assume that for every (2.1) has a unique strong solution and a.s. In order to compare with the exact solution which is a continuous time process, we consider the following interpolation process of the Semi-Discrete approximation, in a compact form,

| (2.2) |

where when The first and third variable in denote the discretized part of the original SDE. We observe from (2.2) that in order to solve for , we have to solve an SDE and not an algebraic equation, thus in this context, we cannot reproduce implicit schemes, but we can reproduce the Euler scheme if we choose and

The numerical scheme (2.2) converges to the true solution of SDE (1.1) and this is stated in the following, which is our main result.

Theorem 2.1.

In ([12]) the case with no square root term is treated, thus Theorem 2.1 is a generalization of ([12, Theorem 1]). Section 3 provides all the necessary and finally the proof of Theorem 2.1. Section 4 gives applications to super linear drift and diffusion problems with non negative solution, one of which includes the Heston -model. Section 5 shows experimentally the order of convergence of the SD method applied to the Heston -model. The Semi-Discrete scheme is strongly convergent in the mean square sense and preserves positivity of the solution.

3. Proof of Theorem 2.1.

We denote the indicator function of a set by The constant may vary from line to line and it may depend apart from on other quantities, like time for example, which are all constant, in the sense that we don’t let them grow to infinity.

3.1. Error bound for the explicit Semi-Discrete scheme

Lemma 3.1.

Let the assumption of Theorem 2.1 hold. Let and set the stopping time Then the following estimate holds

| (3.1) |

where does not depend on implying as

Proof of Lemma 3.1.

Let integer such that It holds that

where we have used Cauchy-Schwarz inequality and Assumption A for the function 111By the fact that we want the problem (1.1) to be well posed and by the conditions on and we get that are bounded on bounded intervals. Taking expectations in the above inequality gives

where in the first step we have used Doob’s martingale inequality ([21, Theorem 1.3.8]) on the diffusion term, in the second step Assumption A for the function Thus,

which justifies the notation, (see for example [30]). ∎

3.2. Convergence of the Semi-Discrete scheme in

Proposition 3.2.

Let the assumptions of Theorem 2.1 hold. Let and set the stopping time Then we have

| (3.2) |

for any where

and does not depend on It holds that

Proof of Proposition 3.2.

Let the non increasing sequence with and We introduce the following sequence of smooth approximations of (method of Yamada and Watanabe, [31])

where the existence of the continuous function with and support in is justified by The following relations hold for with

We have that

| (3.3) |

Applying Ito’s formula to the sequence we get

where in the second step we have used Assumption A for the functions and the properties of and

Taking expectations in the above inequality yields

where we have used Lemma 3.1 and the fact that .222The function belongs to the space of real valued measurable adapted processes such that thus ([25, Theorem 1.5.8]) implies . Thus (3.3) becomes

where in the last step we have used the Gronwall inequality ([10, Relation 7]) and Taking the supremum over all gives (3.2). ∎

3.3. Convergence of the Semi-Discrete scheme in

Set the stopping time for some big enough. We have that

| (3.4) | |||||

where in the second step we have applied Young inequality,

for and in the third step we have used the elementary inequality with and comes from the moment bound assumption. It holds that

thus (3.4) becomes

| (3.5) |

We estimate the difference It holds that

where in the second step we have used Cauchy-Schwarz inequality and Assumption A for and

Taking the supremum over all and then expectations we have

| (3.6) | |||||

where in the last step we have used Holder’s inequality and Doob’s martingale inequality with since is an valued martingale that belongs to It holds that

where we have used Assumption A for Relation (3.6) becomes

where we have used Lemma 3.1 and Jensen’s inequality for the concave function The integrand of the last term is bounded, from Proposition 3.2, by

where Application of the Gronwall inequality implies

Note that, given the quantity can be arbitrarily small by choosing big enough and small enough Relation (3.5) becomes,

Given any we may first choose such that then choose such that then and finally such that concluding as required to verify (2.3).

4. Superlinear examples.

4.1. Example I

We study the numerical approximation of the following SDE,

| (4.1) |

where is a locally Lipschitz and bounded function with locally Lipschitz constant bounding constant , is independent of all for some and a.s., , are positive and bounded functions with Model (4.1) has super linear drift and diffusion coefficients.

We propose the following Semi-Discrete numerical scheme

| (4.2) |

where for and a.s., or in a more compact form,

| (4.3) |

where when The linear SDE (4.3) has a solution which, by use of Ito’s formula, has the explicit form

| (4.4) |

where

Proposition 4.1.

4.1.1. Proof of Proposition 4.1

In order to prove Proposition 4.1 we need to verify the assumptions of Theorem 2.1. Let

We verify Assumption A for Let such that We have that

thus, Assumption A holds for with

We verify Assumption A for Let such that We have that

where we have used the fact that the function is Holder continuous and Thus, Assumption A holds for .

4.1.2. Moment bound for original SDE

Lemma 4.2.

In the previous setting it holds that a.s.

Proof of Lemma 4.2.

Set the stopping time for some with the convention that Application of Ito’s formula on implies,

where

Taking expectations in the above inequality and using the fact that 333The function belongs to the space thus ([25, Theorem 1.5.8]) implies . we get that

where we have used Gronwall inequality with independent of We have that

| (4.6) |

Lemma 4.3.

In the previous setting it holds that

for some and any

Proof of Lemma 4.3.

In the case of ’s outside a finite ball of radius with and we have that

where the last inequality is valid for all such that Thus is bounded for all since when we have that is finite and say Since is positive, application of ([25, Theorem 2.4.1]) implies

for any and all . Using Ito’s formula on with (in order to use Doob’s martingale inequality later) we have that

where Taking the supremum and then expectations in the above inequality we get

where in the last step we have used Doob’s martingale inequality to the diffusion term 444The function belongs to the family thus ([25, Theorem 1.5.8]) implies i.e. . and Gronwall inequality. ∎

4.1.3. Moment bound for Semi-Discrete approximation

Lemma 4.4.

In the previous setting it holds that

for some and for any

Proof of Lemma 4.4.

Set the stopping time for some with the convention that Application of Ito’s formula on with implies,

where the last inequality is valid for and

Taking expectations and using that we get

Application of the Gronwall inequality implies

We have that

thus taking expectations in the above inequality and using the estimated upper bound for we arrive at

and taking limits in both sides as we get that

Fix . The sequence is nondecreasing in since is increasing in and as and as thus the monotone convergence theorem implies

| (4.7) |

for any Following the same lines as in Lemma 4.3, i.e. using again Ito’s formula on , taking the supremum and then using Doob’s martingale inequality on the diffusion term we obtain the desired result. Note that in this last step we need . ∎

Remark 4.5.

-

(i)

Proposition 4.1 implies that our explicit numerical scheme converges in the mean square sense. Moreover, by (4.4) we get that our numerical scheme preserves positivity, which is a desirable modelling property ([2], [20]). Example (4.1) covers the model (1.3), in the case where are constant, and super-linear problems both in drift and diffusion.

-

(ii)

Moreover, note that in the analysis that we followed, we did not discretize the coefficients . In general, by Theorem 2.1, we are free to discretize any of the functions at any degree. Thus, we can fully discretize every meaning that (4.2) will become

(4.8) or semi-discretize every

(4.9) where The only difference in that situation is that we require, to be locally Lipschitz in both variables.

-

(iii)

One more point of discussion is the dependence on that we can assume on the coefficients ’s. Specifically, we consider the more general SDE

(4.10) Then, assuming that it admits a unique strong solution, our method seems to work. In the example discussed here, an extra condition on the ’s would be of the form

-

(iv)

We illustrate our method in the case Then the diffusion term takes positive and negative values and thus method ([29]) does not work since it requires in order to use the Lamperti-type transformation, as well as Milstein method ([16]) since for the same reason their Assumption 2.7 is violated. The only method that we know and can be used for this situation is the Tamed-Euler method ([18], [17]) but the drawback is that it does not preserve positivity.

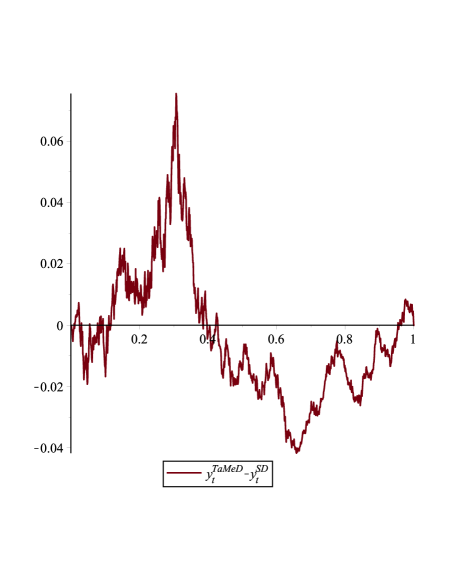

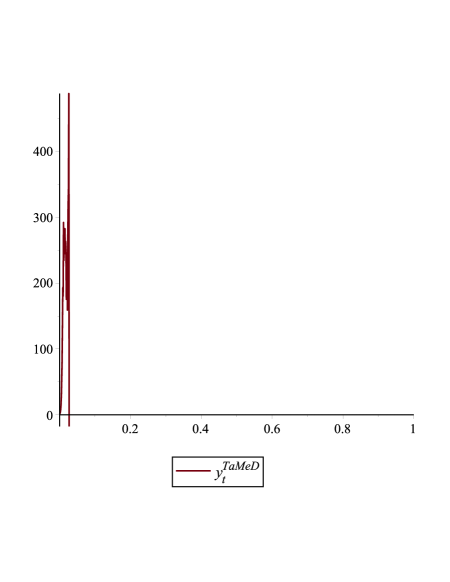

Below, we compare our scheme, in the case where are constant, with Tamed-Euler method in ([17]) and see in Figure 1 that for “good” data the two methods are close. Choosing different data, we see that Tamed-Euler (1.7) takes negative values, even in the first step. In particular we see, that by altering the parameters we get the results presented in Table 1 and shown in Figure 2. Note that if the Tamed-Euler takes a negative value, it explodes in the next step, because of the term while taking the value zero in a step results in zero terms for all the following steps.

Set of Parameters Time of first Value of negative step step 1 27 Table 1. Negative values of Tamed-Euler scheme (1.7) for Heston model. Figure 1. Difference between the Semi-Discrete scheme and Tamed-Euler scheme (1.7) for .

Figure 2. Tamed-Euler method (1.7) does not preserve positivity, .

4.2. Example II

Consider the following stochastic differential equation (SDE),

| (4.11) |

where is independent of all for some and a.s., are positive and bounded functions with and

Lemma 4.6.

[Positivity of ] In the previous setting it holds that a.s.

Proof of Lemma 4.6.

Set the stopping time for some with the convention that Application of Ito’s formula on implies,

where

Taking expectations in the above inequality and using the fact that 555The function belongs to the space thus ([25, Theorem 1.5.8]) implies . we get that

where we have used Gronwall inequality with independent of We have that

| (4.12) |

The following Lemma shows uniform bounds of moments of

Lemma 4.7.

In the previous setting it holds that

for some and any

Proof of Lemma 4.7.

We follow the same lines as in the proof of Lemma 4.3. In particular, we first get the bound

where the last inequality is valid for all such that which implies

for any and all . Using Ito’s formula on with (in order to use Doob’s martingale inequality later) we have that

where Taking the supremum and then expectations in the above inequality we get

where in the last step we have used Doob’s martingale inequality to the diffusion term 666The function belongs to the family thus ([25, Theorem 1.5.8]) implies i.e. . and Gronwall inequality. ∎

Model (4.11) has super linear drift and diffusion coefficients. We study the numerical approximation of (4.11). We propose the following Semi-Discrete numerical scheme for the transformed process of (4.11),

| (4.13) |

where for and a.s., where

| (4.14) |

or in a more compact form,

| (4.15) |

where when The linear SDE (4.15) has a solution which, by use of Ito’s formula, has the explicit form

| (4.16) |

where

The transformation of (4.11). Application of Ito’s formula to the function implies

where are given by (4.14).

In order to use Proposition 4.1 we have to verify that

Since we immediately have and Moreover

and is easy to see that

Proposition 4.8.

In the previous setting, the following convergence to the true solution of (4.11) in the mean square sense holds,

| (4.18) |

Proof of Proposition 4.8

4.2.1. Convergence result

We use the following inequality implied by the mean value theorem

thus we get that

Set the stopping time for some big enough. Taking the supremum and then expectations in the above inequality yields,

where in the second step we have applied Young inequality,

for and

It holds that

where is the maximum of the bounding moment constants of and Moreover, we have that,

where we have used again Young inequality. When we have that thus it suffices to bound the moments of and Note that by Lemma 4.3 the uniform bound for the moment of holds when and by Lemma 4.4 the uniform bound for the moment of is valid for any thus for 888We also have to ensure that Lemma 4.7 holds, thus we have to choose such that or equivalently we have to choose such that whose existence is ensured by the condition we get that for some In the case it suffices to bound the moments of and Again by Lemma 4.3 the uniform bound for the moment of holds when and by Lemma 4.4 the uniform bound for the moment of is valid for any thus for 999We also have to ensure that Lemma 4.7 holds, thus we have to choose such that or equivalently we have to choose such that whose existence is ensured by the condition we get that for some Thus, by Footnotes 8 and 9 and the condition or equivalently we get the bound where is a constant depending on Collecting all the estimates together,

Given any we may first choose such that then choose such that and finally such that which is justified by Proposition 4.1 to get that as required to verify (4.18).

4.3. Example III

Consider the following stochastic differential equation (SDE),

| (4.19) |

where is a locally Lipschitz and bounded function with locally Lipschitz constant bounding constant is independent of all for every and a.s., are positive and bounded functions and is odd with where The above conditions on the parameters imply the uniform bound of as shown in the following result.

Lemma 4.10.

[Moment bound for original SDE] In the previous setting it holds that

for some and every

Proof of Lemma 4.10.

In the case of ’s outside a finite ball of radius with and when we have that

where the the last inequality is valid for all and we have used and that is odd. Thus is bounded for all since when we have that is finite and say Application of ([25, Theorem 2.4.1]) implies

for any and all . Using Ito’s formula on we have that

where we have used that is odd and Taking the supremum and then expectations in the above inequality we get

where in the last step we have used Doob’s martingale inequality to the diffusion term 101010The function belongs to the family thus ([25, Theorem 1.5.8]) implies i.e. . and Gronwall inequality. ∎

Model (4.19) has super linear drift and diffusion coefficients. We study the numerical approximation of (4.19). We propose the following Semi-Discrete numerical scheme for (4.19)

| (4.20) |

where for and a.s., or in a more compact form,

| (4.21) |

where when The linear SDE (4.21) has a solution which, by use of Ito’s formula, has the explicit form ([23, Chapter 4.4, relation(4.10)])

| (4.22) |

where

Proposition 4.11.

The following convergence to the true solution of (4.19) in the mean square sense holds,

| (4.23) |

4.3.1. Proof of Proposition 4.11

In order to prove Proposition 4.11 we just need to verify the assumptions of Theorem 2.1. Let

We verify Assumption A for The conditions on the parameters imply that Let such that We have that

where we have applied the mean value theorem for the function , thus Assumption A holds for with

We verify Assumption A for Since we have that is locally Holder continuous in i.e.

| (4.24) |

Let such that We have that

where we have used (4.24) and Thus, Assumption A holds for .

Lemma 4.12.

[Positivity of ] In the previous setting it holds that a.s.

Proof of Lemma 4.12.

Set the stopping time for some with the convention that Application of Ito’s formula on implies,

Taking absolute values in the above equality and then expectations and using Jensen inequality and then Ito’s isometry on the diffusion term, we get

where is as in Lemma 4.10 and Now we proceed as in Lemmata 4.2 and 4.6, to get first that and then conclude that i.e. a.s. ∎

Lemma 4.13.

[Moment bound for Semi-Discrete approximation] In the previous setting it holds that

for some and for every

Proof of Lemma 4.13.

Set the stopping time for some with the convention that Application of Ito’s formula on implies,

where we have used that the last inequality is valid for the constant is independent of and Taking expectations and using that we get

where in the second step we have applied Gronwall inequality. We have that

thus taking expectations in the above inequality and using the estimated upper bound for we arrive at

and taking limits in both sides as we get that

Fix . The sequence is nondecreasing in since is increasing in and as and as thus the monotone convergence theorem implies

| (4.25) |

for any Following the same lines as in Lemma 4.10, i.e. using again Ito’s formula on , taking the supremum and then using Doob’s martingale inequality on the diffusion term we obtain the desired result. ∎

5. Numerical Experiments.

We study the numerical approximation of the following SDE,

| (5.1) |

where is independent of all for some and a.s., , are positive constants with Model (5.1) has super linear drift and diffusion coefficients.

In Proposition 4.1 we have shown that the following Semi-Discrete numerical scheme111111The existence and uniqueness of is shown in Appendix A. (in a more general setting with time-varying coefficients)

| (5.2) |

where for and a.s., or in a more compact form,

| (5.3) |

where when converges to the true solution of (5.1) in the mean square sense, that is

| (5.4) |

Relation (5.4) does not show the order of convergence. We aim to show experimentally the order.

The linear SDE (5.3) has a solution which, by use of Ito’s formula, has the explicit form

| (5.5) |

where The Semi-Discrete numerical scheme preserves positivity, which is a desirable modeling property.

In order to estimate the endpoint error where is the exact solution of (5.1) and is the Semi-Discrete approximation (5.5) we follow a standard procedure ([24, Section 3.3]). We compute batches of simulation paths. Each batch is estimated by

and the Monte Carlo estimator of the error

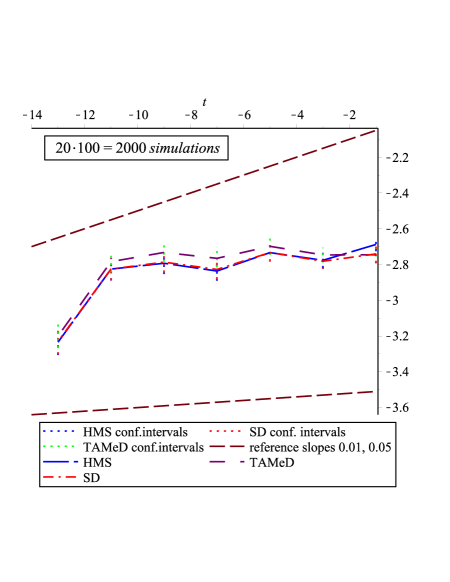

requires Monte Carlo sample paths. When the batch size averages they can be considered as Gaussian. A confidence interval for the error is of the form

We simulate paths121212We simulate with GHz Intel Pentium, GB of RAM in Maple Software. The effort made is just for the purpose of the order of convergence and not for the efficiency of the computer code-time.. The choice for is considered in ([24, p.118]). We should not forget to change the student t-test quantile when we change the number of batches or the significance level For example for the confidence intervals we have

| t-test quantile | |||||||

|---|---|---|---|---|---|---|---|

We discretize with a number of steps in power of The iterative SD-procedure reads

for where are the increments of the Brownian motion.

We want to compare our results with two other methods. The first is an implicit Milstein scheme proposed in ([16, Section 2.2]), which takes the form

and the second is a tamed Euler-Maruyama scheme proposed in ([17, Relation 4]), which reads

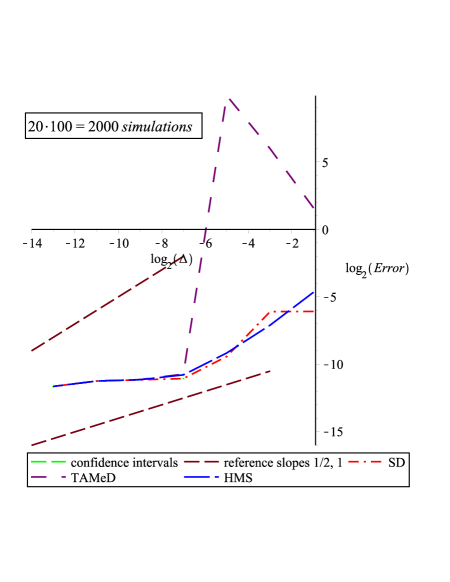

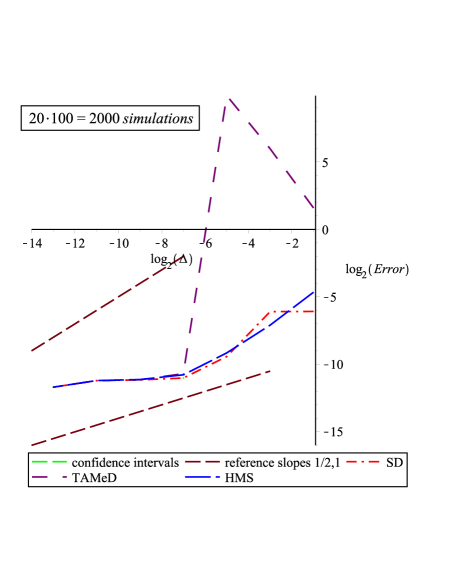

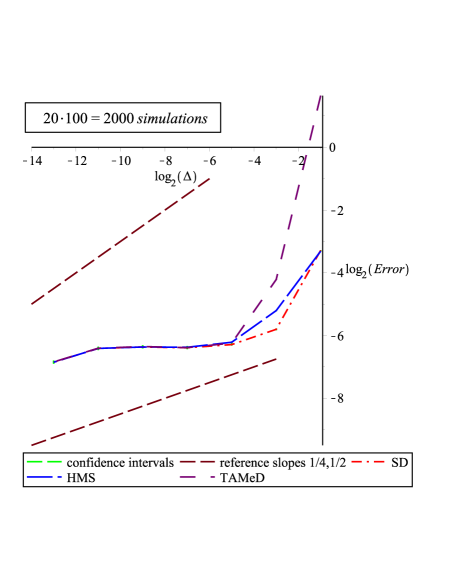

As a reference solution, we take in the first experiment the value of at as in the numerical experiment in ([16, Section 4.1]), and in the second experiment at since we have shown by (5.4) that it strongly converges to the exact solution. We plot in a scale and error bars represent confidence intervals. The results are shown in Figures 3 and 4 and Tables 3 and 4.

| Step | SD-Error | HMS-Error | TAMeD-Error |

|---|---|---|---|

| Step | SD-Error | HMS-Error | TAMeD-Error |

|---|---|---|---|

The following points of discussion are worth mentioning.

-

•

The SD method and the HMS method are very close, with SD performing slightly better, except only for the step size The same situation appears in both cases, i.e. independently of the choice of the exact solution, which is a positive feature of SD.

-

•

A linear regression with the method of least squares fit, in the case one considers only the first four points with steps produced values consistent with the strong order of convergence equal to for both SD and HMS methods, whereas considering all the seven points, values close to Tables 5 and 6 present the exact values of order of convergence. We see that the order of convergence of SD for problem (5.1) is at least

Number of points order of SD order of HMS Table 5. Order of convergence of SD and HMS approximation of (5.1) with HMS exact solution with digits of accuracy. Number of points order of SD order of HMS Table 6. Order of convergence of SD and HMS approximation of (5.1) with SD exact solution with digits of accuracy. -

•

The confidence intervals are of such an order that indicates that we donnot need to increase the number of batches All the above calculations are made evaluating with digits. The results of doubling the number of digits to are shown in the following Tables 7 and 8, that indicate that there is no significant difference of the situation.

Step SD-Error HMS-Error TAMeD-Error Table 7. Error and step size of SD,HMS and TAMeD approximation of (5.1) with HMS exact solution with digits of accuracy. Number of points order of SD order of HMS Table 8. Order of convergence of SD and HMS approximation of (5.1) with HMS exact solution with digits of accuracy. -

•

For small it may happen that the global error will begin to increase as is further decreased ([24, p.97]). This effect is due to the roundoff error which influences the calculated global error. In practice, that implies the existence of a minimum step size for each initial value problem, below which the accuracy of the approximations through a specific method cannot be improved.

-

•

Convergence of a numerical scheme does not alone guarantee its practical value ([24, p.129]). It may be numerical UNSTABLE. Moreover, in practice, the computer time consumed to provide a desired level of accuracy, is of great importance. As mentioned in Footnote 12, we donnot claim that SD method performs well in that aspect, because of the exponential calculations involved. However, it seems that it can reach accuracy up to digits, as fast as the HMS method.

-

•

We would like to see how things become, by altering the parameter SD method, seems to work, with the theoretical proof shown in Section 4.1, when is over What happens below that range? HMS method works for over Moreover, as noted in Remark 4.5(iv), our method can cover more general cases, in contrast to HMS, by introducing the function in the diffusion part, or/and by assuming random coefficients

In the following Figure 5 we present the situation when we change the parameters of SDE (5.1) in such a way that we are closer to the theoretical acceptable range ( by lowering to ).

Figure 5. SD, HMS, and TAMeD method applied to SDE (5.1) with HMS exact solution and parameters with digits of accuracy.

The rate of convergence drops to a half for both SD and HMS method and TAMeD seems to perform better than before. To be more precise we present in the table 9 the exact numbers.

Number of points order of SD order of HMS Table 9. Order of convergence of SD and HMS approximation of (5.1) with HMS exact solution with digits of accuracy when In Figure 6 we present the case with

Figure 6. SD, HMS, and TAMeD method applied to SDE (5.1) with HMS exact solution and parameters with digits of accuracy.

The rate of convergence drops dramatically for all methods. Moreover the TAMeD performs even better, close to SD and HMS. To be more precise we present in the table 10 the exact numbers.

Number of points order of SD order of HMS order of TAMeD Table 10. Order of convergence of SD and HMS approximation of (5.1) with HMS exact solution with digits of accuracy when -

•

Regarding the TAMeD method, a major drawback is that it does not preserve positivity. However, we remark that even though the errors of the TAMeD approximation are quite big, for big step sizes,131313In the plots these errors donnot seem so big, because of the scale. The tables though show this anomaly. all methods behave quite close for small ’s and even closer for bigger as we lower the parameter close to its critical value.

References

- [1] Ahn, D-H., Gao, B. (1999). A parametric nonlinear model of term structure dynamics. The Review of Financial Studies. 12, 721-762.

- [2] Appleby, J.A.D., Guzowska, M., Kelly C., Rodkina, A. (2010). Preserving positivity in solutions of discretised stochastic differential equations. Applied Mathematics and Computation. 217,(2) 763-774.

- [3] Black, F., Scholes, M. (1973). The pricing of options and corporate liabilities. Journal of Political Economy 81, 637-659.

- [4] Broadie, M., Kaya, O. (2006). Exact simulation of stochastic volatility and other affine jump diffusion processes. Oper. Res. 54, 217-231.

- [5] Cox, J.C. (1975). Notes on option pricing I: Constant elasticity of variance diffusions. Working paper, Stanford University.

- [6] Cox, J.C., Ingersoll, J.E., Ross, S.A. (1985). A theory of the term structure of interest rates. Econometrica 53, 385-407.

- [7] Deelstra, G., Delbaen, F. (1998). Convergence of discretized stochastic (interest rate) processes with stochastic drift term. Appl Stochastic Models Data Anal. 14, 77-84.

- [8] Either S., Kurtz, T. (1986). Markov Processes: Characterization and Convergences. John Wiley Sons, New York.

- [9] Feller, W. (1951). Two singular diffusion problems. Annals of Mathematics 54, 173-182.

- [10] Gronwall, T.H. (1919). Note on the derivatives with respect to a parameter of the solutions of a system of differential equations. Annals of Mathematics 20, 292-296.

- [11] Halidias, N. (2012). Semi-discrete approximations for stochastic differential equations and applications. International Journal of Computer Mathematics , 1-15.

- [12] Halidias, N. (2013). A novel approach to construct numerical methods for stochastic differential equations. Numer Algor.

- [13] Heston, S.L. (1993). A closed form solution for options with stochastic volatility, with applications to bonds and currency options. Rev. Financial Stud. 6, 327-343.

- [14] Heston, S.L. (1997). A simple new formula for options with stochastic volatility. Course notes of Washington University in St. Louis, Missouri.

- [15] Higham, D.J., Mao, X. (2005). Convergence of Monte-Carlo simulations involving the mean-reverting square root process. J. Comp. Fin. 8, 35-62.

- [16] Higham, D.J., Mao, X., Szpruch, L. (2013). Convergence, Non-negativity and Stability of a New Milstein Scheme with Applications to Finance. Discrete and Continuous Dynamical System Series B. 18, 1-18.

- [17] Hutzenhaler, M., Jentzen, A. (2012). Numerical approximations of stochastic differential equations with non-globally Lipschitz continuous coefficients. preprint.

- [18] Hutzenhaler, M., Jentzen, A., Kloeden, P. (2012). Strong convergence of an explicit numerical method for sdes with non-globally Lipschitz continuous coefficients. Ann. Appl. Prob.22 (2012), no. 4, 1611-1641.

- [19] Hutzenhaler, M., Jentzen, A., Kloeden, P. (2011). Strong and weak divergence in finite time of Euler’s method for stochastic differential equations with non-globally Lipschitz coefficients. Proc. Roy. Soc. London A 467, no. 2130, 1563-1576.

- [20] Kahl, C., Gunther, M., Rosberg, T. (2008). Structure preserving stochastic integration schemes in interest rate derivative modeling. Applied Numerical Mathematics. 58,(3) 284 - 295.

- [21] Karatzas, I., Shreve, S.E. (1988). Brownian motion and stochastic calculus. Springer-Verlag New York.

- [22] Kloeden, P., Neuenkirch, A. (2012). Convergence of numerical methods for stochastic differential equations in mathematical finance. preprint.

- [23] Kloeden, P., Platen, E. (1995). Numerical solution of stochastic differential equations. Vol 23, Stochastic Modelling and Applied Probability. Springer-Verlag Berlin. corrected 2nd printing

- [24] Kloeden, P., Platen, E., Schurz, H. (2003). Numerical solution of stochastic differential equations through computer experiments. Springer-Verlag Berlin. corrected 3rd printing

- [25] Mao, X. (1997). Stochastic Differential Equations and Applications. Horwood Publishing.

- [26] Mao, X., Szpruch, L. (2013a). Strong convergence and stability of implicit numerical methods for stochastic differential equations with non-globally Lipschitz continuous coefficients. J. Comput. Appl. Math. 238, 14-28.

- [27] Mao, X., Szpruch, L. (2013b). Strong convergence rates for backward Euler-Maruyama method for non-linear dissipative-type stochastic differential equations with super-linear diffusion coefficients. Stochastics. 85, 144-171.

- [28] Marakov, R., Glew, D. (2010). Exact simulation of Bessel diffusions. Monte Carlo Methods Appl. 16, no. 3-4, 283-306.

- [29] Neuenkirch, A., Szpruch, L. (2012). First order strong approximations of scalar SDEs with values in a domain. preprint.

- [30] Olver, F.W.J. (1997). Asymptotics and special functions. AKP classics, Wellesley, Mass.

- [31] Yamada, T., Watanabe, S. (1971). On the uniqueness of solutions of stochastic differential equations. J. Math. Kyoto Univ. 11, 155-167.

Appendix A Existence and uniqueness of for Heston model

A.1. Uniqueness of solution of

Let be two solutions of SDE (5.3) with same initial condition, i.e. with By Lemma 4.4 they both belong to the space of measurable adapted processes such that

Set the stopping times and for some big enough and consider the stopping times for Take and It holds that

where in the second step Cauchy-Schwarz inequality, in the third step the elementary inequality for the appropriate ’s and Assumption A for in the last step the fact that when and the equality in the initial conditions and

Taking the supremum over all and then expectations we have

| (A.1) | |||||

where we have used Doob’s maximal inequality with since is an valued martingale that belongs to Moreover, we have that

where we have used Assumption A for thus relation (A.1) becomes

which by use of Gronwall’s inequality gives

| (A.2) |

Following the same arguments we can show that

for every integer 141414For just use the same ideas as for and the other cases follow exactly the same way using in every step the result of the previous step. Thus, if we drop the index from the stopping times with the meaning that and for some big enough and consider the stopping time we have that

Hence, for all a.s. which proves that the solution of SDE (5.3), and in general of SDE (2.1) when it exists, is unique.

A.2. Existence of solution of

We will show the existence of the solution of SDE (5.2) for and the same procedure can be followed to show the existence of the solution of SDE (5.2) for every integer i.e. the existence of the solution of SDE (5.3). Application of Ito’s formula to for implies

Now take the exponential of both sides of (4.4) with in the case to verify that (5.5) is indeed a solution of SDE (5.2) for