Bayesian estimation of a sparse precision matrix

Abstract

We consider the problem of estimating a sparse precision matrix of a multivariate Gaussian distribution, including the case where the dimension is large. Gaussian graphical models provide an important tool in describing conditional independence through presence or absence of the edges in the underlying graph. A popular non-Bayesian method of estimating a graphical structure is given by the graphical lasso. In this paper, we consider a Bayesian approach to the problem. We use priors which put a mixture of a point mass at zero and certain absolutely continuous distribution on off-diagonal elements of the precision matrix. Hence the resulting posterior distribution can be used for graphical structure learning. The posterior convergence rate of the precision matrix is obtained. The posterior distribution on the model space is extremely cumbersome to compute. We propose a fast computational method for approximating the posterior probabilities of various graphs using the Laplace approximation approach by expanding the posterior density around the posterior mode, which is the graphical lasso by our choice of the prior distribution. We also provide estimates of the accuracy in the approximation.

Keywords : Graphical Lasso; Graphical models; Laplace approximation; Posterior convergence; Precision matrix.

1 Introduction

Statistical inference on large covariance or precision matrix (inverse of covariance matrix) is a topic of growing interest in recent times. Often the dimension grows with the sample size and even can be bigger than . Data of this type are frequently encountered in fMRI, spectroscopy, gene array expressions and so on. Estimation of the covariance or precision matrix is of special interest because of their importance in methods like principal component analysis (PCA), linear discriminant analysis (LDA), etc. In cases where , the sample covariance matrix is necessarily singular, and hence an estimator of the precision matrix cannot be obtained by inverting it. Therefore we need to resort to other techniques for handling the high-dimensional problems.

Regularization methods for estimation of the sample covariance or precision matrix have been proposed and studied in recent literature for high-dimensional problems. These include banding, thresholding, tapering and penalization based methods; for example, see Ledoit and Wolf, (2004); Huang et al., (2006); Yuan and Lin, (2007); Bickel and Levina, 2008a ; Bickel and Levina, 2008b ; Karoui, (2008); Friedman et al., (2008); Rothman et al., (2008); Lam and Fan, (2009); Rothman et al., (2009); Cai et al., (2010, 2011). The primary goal of these regularization based methods is to impose a sparsity structure in the matrix. Most of these methods are applicable to situations where there is a natural ordering in the underlying variables, for example in data from time series, spatial data, etc., so that variables which are far off from each other have smaller correlations or partial correlations. In high-dimensional situations for data arising from genetics or econometrics, a natural ordering of the underlying variables may not always be readily available and hence estimation methods which are invariant to the ordering of the variables are desirable.

For estimation of a sparse inverse covariance matrix, graphical models (Lauritzen,, 1996) provide an excellent tool, as the conditional dependence between the component variables is captured an undirected graph; see Dobra et al., (2004); Meinshausen and Bühlmann, (2006); Yuan and Lin, (2007); Friedman et al., (2008). There are several methods in the frequentist literature for the estimation of the precision matrix through graphical models. These methods include minimization of the penalized log-likelihood of the data with a lasso type penalty on the elements of the precision matrix. Several algorithms have been developed in the literature to solve the above optimization problem, including coordinate descent based algorithm for the lasso, which is popularly known as the graphical lasso (Meinshausen and Bühlmann,, 2006; Friedman et al.,, 2008; Banerjee et al.,, 2008; Yuan and Lin,, 2007; Guo et al.,, 2011; Witten et al.,, 2011). Other methods include the Sparse Permutation Invariant Covariance Estimator (SPICE) (Rothman et al.,, 2008).

Frequentist behavior of Bayesian methods in the context of high dimensional covariance matrix estimation have been studied only by a few authors. Ghosal, (2000) studied asymptotic normality of posterior distributions for exponential families, which include the normal model with unknown covariance matrix, when the dimension , but restricting to . Recently, Pati et al., (2012) considered sparse Bayesian factor models for dimensionality reduction in high dimensional problems and showed consistency in the -operator norm (also known as the spectral norm) by using a point mass mixture prior on the factor loadings, assuming such a factor model representation of the true covariance matrix.

Bayesian methods for inference using graphical models have also been developed, as in Roverato, (2000); Atay-Kayis and Massam, (2005); Letac and Massam, (2007). A conjugate family of priors, known as the -Wishart prior (Roverato,, 2000) have been developed for incomplete decomposable graphs. The equivalent prior on the covariance matrix is termed as the hyper inverse Wishart distribution in Dawid and Lauritzen, (1993). Letac and Massam, (2007) introduced a more general family of conjugate priors for the precision matrix, known as the -Wishart family of distributions, which also has the conjugacy property. The properties of this family of distributions, including expressions for the Bayes estimators were further explored in Rajaratnam et al., (2008). Recently Banerjee and Ghosal, (2013) studied posterior convergence rates for a -Wishart prior inducing a banding structure, where the true precision matrix need not have the banding structure.

Wang, (2012) developed a Bayesian version of the graphical lasso, putting Laplace priors on the off-diagonal elements of the precision matrix and exponential priors on the diagonals. Similar in lines with the Bayesian lasso (Park and Casella,, 2008), the posterior mode in this case coincides with the graphical lasso estimate. A block Gibbs sampler is also developed for sampling from the resulting posterior. However, the Bayesian graphical lasso does not introduce any sparsity in the graphical structure because of the absence of a point mass at zero in the prior distribution for the off-diagonal elements. On the other hand, if point masses are introduced, the resulting posterior distribution on the structure of the graph becomes extremely difficult to compute based on the traditional reversible jump Markov chain Monte Carlo method.

In this paper, we derive posterior convergence rates for the Bayesian graphical lasso prior in terms of the Frobenius norm under appropriate sparsity conditions. For computing the posterior distribution, we propose a Laplace approximation based method to compute the posterior probability of different graphical structures. Such Laplace approximations based methods have been developed for variable selection in regression models; for example, see Yuan and Lin, (2005); Curtis et al., (2014). The lasso type penalty on the elements lead to non-differentiability of the integrand, when the graphical lasso sets an off-diagonal entry to zero, but the model includes that off-diagonal entry as a free variable. We shall call such models non-regular following the terminology used by Yuan and Lin, (2005) for variable selection in linear regression models. We show that the posterior probability of non-regular models are substantially smaller than their regular counterparts and hence in comparison may be ignored from consideration. We also estimate the error in the Laplace approximation for regular models.

The paper is organized as follows. In the next section, we introduce notations and discuss preliminaries on graphical models required for the other sections of the paper. In Section 3, we state model assumptions and specify the prior distribution on the underlying parameters, derive the form of the posterior and obtain the posterior convergence rate using the general theory developed in Ghosal et al., (2000). In Section 4, we develop the approximation of the posterior probabilities for different graphical models and discuss the issue of non-regular graphical models. We also show that the error in approximation of the posterior probabilities using the Laplace approximation is asymptotically negligible under appropriate conditions. A simulation study is performed in the Section 5 followed by a real data example in Section 6. Proofs of main results and additional lemmas are included in the Appendix.

2 Notations and preliminaries

An undirected graph comprises of a non-empty set of vertices indexing the components of a -dimensional random vector along with an edge-set defined by . Let be , where the precision matrix is such that implies . We then say that follows a Gaussian graphical model (GGM) with respect to the graph . Since the absence of an edge between and implies conditional independence of and given , a GGM serve as an excellent tool in representing the sparsity structure in the precision matrix. Following the notation in Letac and Massam, (2007), the canonical parameter is restricted to , where is the cone of positive definite symmetric matrices of order having zero entry corresponding to each missing edge in . We also denote the linear space of symmetric matrices of order by , and to be the cone of positive definite matrices of order . Corresponding to each GGM , we define the set .

By (respectively, ), we mean that is bounded (respectively, as ). For a random sequence , (respectively, ) means that for some constant (respectively, for all ). For numerical sequences and , by (or, we mean that , while by we mean that . By we mean that . The indicator function is denoted by . Vectors are represented in bold lowercase English or Greek letters with the components of a vector by the corresponding non-bold letters, that is, for , . For a vector , we define the following vector norms: , . Matrices are denoted in bold uppercase English or Greek letters, like , where stands for the th entry of . The identity matrix of order will be denoted by . If is a symmetric matrix, let stand for its eigenvalues and let the trace of be denoted by . Viewing as a vector in , we define and -norms on matrices as

Note that , the Frobenius norm. Viewing an operator from to , where , we can also define, We refer to the norm as the -operator norm. This gives the -operator norm of as

For symmetric matrices, . For symmetric matrices and of order , we have the following:

| (2.1) |

stands for the unique positive definite square root of a positive definite matrix . For two matrices and , we say that (respectively, ) if is nonnegative definite (respectively, positive definite). Thus for a positive definite matrix , where stands for the zero matrix. We denote sets in non-bold uppercase English letters. The cardinality of a set , that is, the number of elements in is denoted by . We define the symmetric matrix .

The Hellinger distance between two probability densities and is given by .

For a subset of a metric space , denote the -covering number of with respect to , that is, the minimum number of -balls of size is needed to cover .

3 Model, prior and posterior concentration

Consider independent random samples from , where is nonsingular and the precision matrix is sparse. The problem is to estimate and to learn the underlying graphical structure. We denote the natural unbiased estimator of by .

The graphical lasso produces sparse solutions for the precision matrix, in similar lines to that of the lasso in case of linear regression. The graphical lasso estimator minimizes two times the penalized negative log-likelihood

| (3.1) |

over the class of positive definite matrices, and acts as the penalty parameter. Rothman et al., (2008) derived frequentist convergence rates of the penalized estimator under some sparsity assumptions on the true precision matrix. More specifically, consider the following class of positive definite matrices of order :

| (3.2) |

Though Rothman et al., (2008) considered penalizing only the off-diagonal elements of , some modification of the proof of their result leads to the same convergence rate for the graphical lasso estimator, obtained by additionally penalizing the diagonal elements. Let us denote as the graphical lasso estimator based on a sample of size from a -dimensional Gaussian distribution with precision matrix , where is given by (3.2). Then, it follows from Theorem 1 in Rothman et al., (2008) that the rate of convergence of is . By the triangle inequality,

Also, the triangle inequality and sub-multiplicative property for matrix operator norms gives,

Thus, we get,

Now, we have, by assumption, and it follows from Theorem 1 in Rothman et al., (2008) that as . Noting that , we get,

| (3.3) |

In the Bayesian context, Wang, (2012) introduced the graphical lasso prior, which uses exponential distributions on diagonal elements and Laplace density on off-diagonal elements, all independently of each other, and finally imposes a positive definiteness constraint. The graphical lasso prior has a drawback that it puts absolutely continuous priors on the elements of the precision matrix, and hence the posterior probabilities of the event is always exactly zero.

Wang, (2012) also mentioned an extension of the graphical lasso by putting an additional level of prior on the underlying graphical model structure using point mass priors on the events corresponding to the absence of an edge in the edge-set , although did not develop the method. We put point-mass prior on the events to make posterior inference about the sparse structure of the underlying graphical model. Define to be a vector of edge-inclusion indicator, that is,

| (3.4) |

Similar to the Bayesian graphical lasso prior, given the underlying graphical structure, we put a Laplace prior on the non-zero off-diagonal elements of the precision matrix and for the diagonal elements we have a exponential prior, overall maintaining the positive definiteness of the parameter. Then the joint prior density on is given by,

| (3.5) |

We propose two different priors on the graphical structure indicator . The edge indicators are considered to be independent and identically distributed (i.i.d) Bernoulli random variables, and conditioned to the restriction that the model size does not exceed . For some , the prior distribution on is assumed to satisfy

| (3.6) |

This prior is similar to that used by Castillo and van der Vaart, (2012), which chooses the model size first according to a distribution with a similar tail decay and then subsets are selected randomly with equal probability. We can also specify the individual priors on the same as above, but now truncating the model size to some fixed , where is chosen so as to satisfy the metric entropy condition required for posterior convergence.

Thus, in the first situation, the prior on the graphical structure indicator , given , is given by,

| (3.7) |

leading to

| (3.8) |

In the second case, the prior on is simply given by

| (3.9) |

Smaller values of prefer graphical models with fewer number of edges, hence inducing more sparsity in the precision matrix.

Due to the positive definiteness constraint on the parameter , the normalizing constant corresponding posterior distribution of the graphical model becomes intractable and hence was not explored in Wang, (2012). One possible solution is to employ a reversible jump Markov chain Monte Carlo (RJMCMC) algorithm, which jumps from models of varying dimensions to evaluate the posterior probabilities. As there are as many as possible models, the posterior model probabilities estimated by RJMCMC visits are extremely unreliable. We consider a radically different approach to posterior computation based on Laplace approximations, elaborated in the next section.

Under the above prior specifications, the joint posterior distribution of and given the data is given by

| (3.10) | |||||

Thus,

| (3.11) |

where

| (3.12) | |||||

The following result gives posterior convergence rate as . We assume that the true model is sparse, as given by the class of positive definite matrices in (3.2).

Theorem 3.1.

4 Posterior Computation

The marginal posterior density of the graphical structure indicator can be obtained by integrating out elements of the precision matrix in the joint posterior density in (3.10), to get

| (4.1) |

where

| (4.2) |

Note that is minimized at , the graphical lasso estimate corresponding to the penalty parameter . The marginal posterior of is, however, intractable. We give an approximate method for the posterior probability computations of various models using Laplace approximation. The Laplace approximation requires expanding the integrand in (4.1) around the maximum, which in this case, coincides with the graphical lasso solution.

4.1 Approximating model posterior probabilities

Define , where is the graphical lasso solution corresponding to the underlying graphical model structure and penalty parameter . Then,

| (4.3) |

where is

| (4.4) |

Clearly is minimized at by the definition of , so the first derivative of vanishes at , provided that it is differentiable at . Define the matrix , where

| (4.5) |

Using standard matrix calculus (for example, see Section 15.9 of Harville, (2008)), we can find that the Hessian of is the matrix , whose th entry for is given by

| (4.6) |

Thus the Laplace approximation to the posterior probability is given by

| (4.7) |

The approximation in (4.7) is meaningful only if all the graphical lasso estimates of the off-diagonal elements corresponding to the graph generated by are non-zero; otherwise the derivative of does not exist. A similar situation arises in the context of regression models; see Yuan and Lin, (2005) and Curtis et al., (2014). In the next section, we show that such “non-regular models” can essentially be ignored for the purpose of posterior probability evaluation.

4.2 Ignorability of non-regular models

As discussed in the previous section, the objective function of the graphical lasso problem is not differentiable if the graphical lasso solution is zero for at least one pair . These models are referred to as non-regular models. This essentially means that given a fixed graphical structure index , the graphical lasso solution is for at least one . Let us assume, for notational simplicity, that the first elements of are 1 and the rest are 0. Also, among those 1’s, the last of them have corresponding graphical lasso solution equal to zero. For such a non-regular model, we argue that the submodel , with first 1’s and rest 0’s, provides the same graphical lasso solution for the non-zero elements as the bigger model . This means that for such that , the graphical lasso solution corresponding to , given by is identical with that corresponding to , given by . We refer to such a submodel as the regular submodel of the non-regular model .

Lemma 4.1.

For a submodel of as defined above, the graphical lasso solution corresponding to the two models are identical.

We give a proof of the above lemma in the appendix. For notational convenience, let us denote the precision matrix corresponding to the structure indicator by , and corresponding matrix is defined by . We denote the graphical lasso solution in the non-regular model and the corresponding regular submodel by . The ratio of the posterior model probabilities of the two model is given by,

| (4.8) |

The following result shows the ignorability of the non-regular models.

Theorem 4.2.

Proof.

Using (3.14), we have,

Now, note that for such that , we have,

Hence, using Lemma A.2, we get

| (4.9) | |||||

The last inequality follows from the fact that if the prior as in (3.8) is used, then since . For the other prior as in (3.9), the inequality follows trivially as it involves the ratio of two indicator variables only.

For , the above ratio is less than . This completes the proof. ∎

The above result is particularly important in the sense that we can focus on the regular models only, ignoring the non-regular ones especially if is chosen to be small. While approximating the posterior probabilities of the regular models, we re-normalize the values considering the regular models only.

4.3 Error in Laplace approximation

The approximation in the posterior probability of the graphical model is based on a Taylor series expansion of the function around the graphical lasso solution . Let , and denote the vectorized version of , but excluding entries corresponding to the missing edges in the underlying graphical model. Thus is a vector of dimension corresponding to the graphical structure indicator . If the graphical model is -sparse, that is, there are edges present in the graph, then . The following result gives the bound on the remainder term of the Taylor series expansion under the above assumptions.

Lemma 4.3.

Consider a graphical model with variables such that the graph is -sparse. Then, with probability tending to 1, the remainder term in the expansion of the function as defined in (4.2), around the graphical lasso solution , is bounded by , where .

This result can be used to find a bound for the error in Laplace approximation of the posterior probabilities of the graphical model structures. The following result gives the condition for which the error in approximation is asymptotically negligible.

Theorem 4.4.

The error in Laplace approximation of the posterior probability of a graphical model structure is asymptotically negligible if , where is the posterior convergence rate, that is, the error in the Laplace approximation tends to zero if .

The proof of the above result depends on several additional results, including Lemma 4.3 involving the bound on the remainder term in the Taylor series expansion of . We give a proof of the above result along with these additional results in the appendix.

5 Simulation results

We perform a simulation study to assess the performance of the Bayesian method for graphical structure learning. We use 4 different models for our simulations, and we specify these models in terms of the elements of the covariance matrix or the precision matrix , as follows:

-

1.

Model 1: AR(1) model, .

-

2.

Model 2: AR(2) model, .

-

3.

Model 3: Star model, where every node is connected to the first node, and , and otherwise.

-

4.

Model 4: Circle model, .

Corresponding to each model, we generate samples of size and dimension . The penalty parameter for the graphical lasso algorithm is chosen to be 0.5 and the value of appearing in the prior of the graphical structure indicator to be 0.4. We run 100 replications for each of the models and find the median probability model for each replication. To assess the performance of the median probability model (denoted by ‘MPP’), we compute the specificity, sensitivity and Matthews Correlation Coefficient (MCC) averaged across the replications as defined below and also compute the same for the graphical lasso (denoted by ‘GL’). The results are presented in Table 1.

| (5.1) |

where TP, TN, FP and FN respectively denote the true positives, true negatives, false positives and false negatives in the selected model, which in our case is the median probability model.

| MPP | GL | MPP | GL | |||||||||||||

| Model | SP | SE | MCC | SP | SE | MCC | SP | SE | MCC | SP | SE | MCC | ||||

| 30 | 0.977 | 0.941 | 0.831 | 0.961 | 0.983 | 0.784 | 0.986 | 0.996 | 0.907 | 0.969 | 1.000 | 0.823 | ||||

| (0.003) | (0.019) | (0.015) | (0.003) | (0.010) | (0.013) | (0.002) | (0.003) | (0.014) | (0.002) | (0.000) | (0.013) | |||||

| AR(1) | 50 | 0.987 | 0.953 | 0.841 | 0.977 | 0.986 | 0.785 | 0.991 | 0.992 | 0.903 | 0.980 | 1.000 | 0.823 | |||

| (0.002) | (0.013) | (0.010) | (0.001) | (0.004) | (0.010) | (0.001) | (0.004) | (0.008) | (0.001) | (0.000) | (0.006) | |||||

| 100 | 0.992 | 0.967 | 0.837 | 0.989 | 0.991 | 0.804 | 0.994 | 0.995 | 0.890 | 0.991 | 0.999 | 0.827 | ||||

| (0.001) | (0.008) | (0.007) | (0.001) | (0.003) | (0.006) | (0.001) | (0.002) | (0.008) | (0.001) | (0.001) | (0.006) | |||||

| 30 | 0.975 | 0.470 | 0.546 | 0.964 | 0.535 | 0.558 | 0.987 | 0.495 | 0.617 | 0.982 | 0.517 | 0.610 | ||||

| (0.003) | (0.014) | (0.013) | (0.002) | (0.013) | (0.012) | (0.002) | (0.008) | (0.008) | (0.002) | (0.009) | (0.007) | |||||

| AR(2) | 50 | 0.983 | 0.462 | 0.541 | 0.971 | 0.508 | 0.522 | 0.993 | 0.489 | 0.629 | 0.987 | 0.534 | 0.622 | |||

| (0.001) | (0.013) | (0.011) | (0.002) | (0.010) | (0.009) | (0.001) | (0.005) | (0.007) | (0.001) | (0.001) | (0.006) | |||||

| 100 | 0.989 | 0.470 | 0.537 | 0.980 | 0.531 | 0.514 | 0.995 | 0.484 | 0.624 | 0.993 | 0.529 | 0.624 | ||||

| (0.001) | (0.006) | (0.006) | (0.001) | (0.007) | (0.007) | (0.001) | (0.006) | (0.004) | (0.001) | (0.009) | (0.005) | |||||

| 30 | 0.947 | 0.289 | 0.228 | 0.937 | 0.310 | 0.224 | 0.995 | 0.210 | 0.378 | 0.993 | 0.252 | 0.402 | ||||

| (0.004) | (0.038) | (0.036) | (0.003) | (0.043) | (0.036) | (0.001) | (0.032) | (0.041) | (0.001) | (0.036) | (0.038) | |||||

| Star | 50 | 0.945 | 0.492 | 0.332 | 0.934 | 0.514 | 0.317 | 0.993 | 0.475 | 0.585 | 0.990 | 0.514 | 0.577 | |||

| (0.003) | (0.034) | (0.025) | (0.003) | (0.035) | (0.023) | (0.000) | (0.034) | (0.024) | (0.001) | (0.032) | (0.022) | |||||

| 100 | 0.939 | 1.000 | 0.485 | 0.927 | 1.000 | 0.452 | 0.988 | 1.000 | 0.792 | 0.984 | 1.000 | 0.748 | ||||

| (0.002) | (0.000) | (0.007) | (0.002) | (0.000) | (0.005) | (0.000) | (0.000) | (0.008) | (0.001) | (0.000) | (0.007) | |||||

| 30 | 0.733 | 1.000 | 0.399 | 0.694 | 1.000 | 0.369 | 0.719 | 1.000 | 0.388 | 0.674 | 1.000 | 0.354 | ||||

| (0.004) | (0.000) | (0.003) | (0.006) | (0.000) | (0.004) | (0.005) | (0.000) | (0.004) | (0.004) | (0.000) | (0.003) | |||||

| Circle | 50 | 0.831 | 1.000 | 0.409 | 0.822 | 1.000 | 0.398 | 0.833 | 1.000 | 0.411 | 0.814 | 1.000 | 0.390 | |||

| (0.003) | (0.000) | (0.003) | (0.002) | (0.000) | (0.003) | (0.002) | (0.000) | (0.003) | (0.002) | (0.000) | (0.002) | |||||

| 100 | 0.891 | 1.000 | 0.378 | 0.894 | 1.000 | 0.383 | 0.903 | 1.000 | 0.399 | 0.902 | 1.000 | 0.397 | ||||

| (0.001) | (0.000) | (0.002) | (0.001) | (0.000) | (0.002) | (0.008) | (0.000) | (0.002) | (0.001) | (0.000) | (0.002) | |||||

6 Illustration with real data

In this section we illustrate the Bayesian graphical structure learning method with the stock price data from Yahoo! Finance. Description of the data set can be found in Liu et al., (2009) and available in the huge package on CRAN (Zhao et al.,, 2012) as stockdata. The data set consists of closing prices of stocks that were consistently included in the S&P 500 index in the time period January 1, 2003 to January 1, 2008 for a total of 1258 days. The stocks are also categorized into 10 Global Industry Classification Standard (GICS) sectors, namely, “Health Care”, “Materials”, “Industrials”, “Consumer Staples”, “Consumer Discretionary”, “Utilities”, “Information Technology”, “Financials”, “Energy”, “Telecommunication Services”.

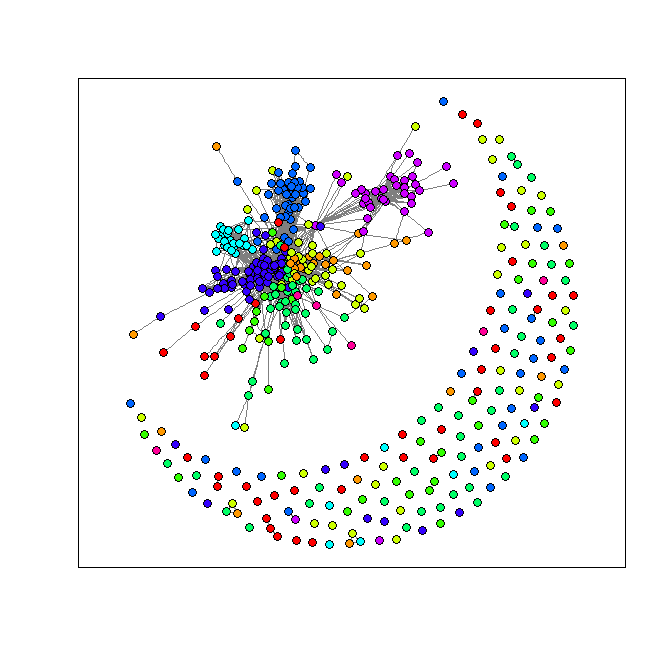

Denoting as the closing stock price for the th stock on day , we construct the data matrix with entries . For analysis, we construct the data matrix by standardizing , so that each stock has mean zero and standard deviation one. We find the median probability model as selected by the Bayesian graphical structure learning method. The corresponding graphical structure is displayed in Figure 1. The vertices of the graph are colored corresponding to the different GICS sectors. We find that stocks from the same sectors tend to be related with other members from that category, and generally not related across different sectors, though there are some connections, which may be due to some other possible latent factors affecting all of them. The grouping of the stocks corresponding to their sectors is expected, implying that the stock prices for a particular sector are conditionally independent of those of other sectors.

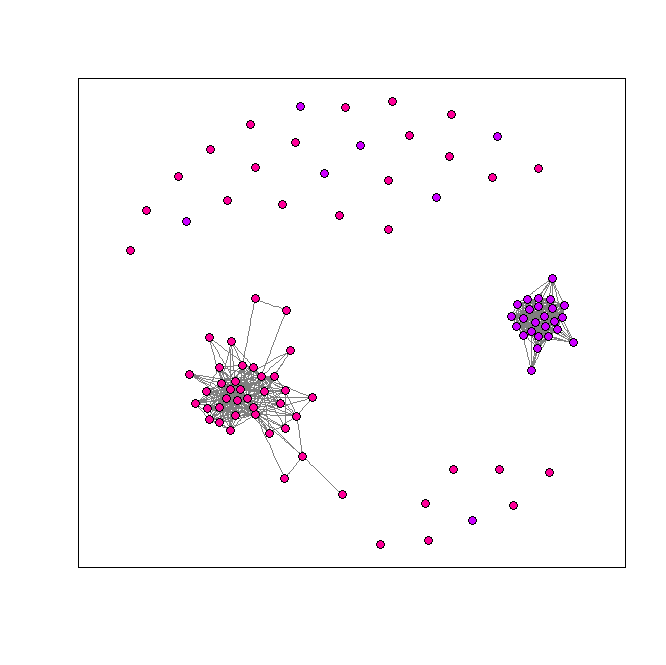

We also individually study data pertaining to some of the specific sectors to have a closer look at the strength of the groupings where perturbations due to latent factors is least expected. For this, we consider the sectors “Utilities” and “Information Technology”. The graphical structure is displayed in Figure 2. The stock prices for the two sectors clearly separate as desired.

Appendix A Proofs

We now give a proof of the result on posterior convergence rate of the precision matrix.

Proof of Theorem 3.1.

In order to establish the rates of convergence of the posterior distribution, we first need to check the prior concentration rate, that is,

| (A.1) |

where . Note that, for and a symmetric matrix , we have,

| (A.2) |

We use the above result to find the expressions for and . Denoting the eigenvalues of the matrix by , using and (A.2), we get,

| (A.3) | |||||

Now, , and from an argument in Lemma A.1 it implies that if , then . Hence we can expand in the powers of to get

| (A.4) |

Also,

Thus,

| (A.5) |

Now, using the assumptions on the true precision matrix and the matrix norm relations given by (2.1), we have,

| (A.6) | |||||

Hence, equations (A.5) and (A.6), along with (2.1) give,

The components of are not independently distributed, but a truncation applies because of the positive definite restriction. However, as the true lies in the set of positive definite matrices which is open, the truncation can only increase concentration in a small ball centered at the truth, so we can pretend componentwise independence for the purpose of lower bounding the above prior probability. This gives

| (A.7) |

The prior concentration rate condition thus gives,

| (A.8) |

so as to get

Next, we need to construct tests for against the alternative . Let denote the joint density of the observations and let be the prior. From the results of Birgé, (1984) and Le Cam, (1986), we know that for a probability measure and any convex set of probability measures, there exists tests such that

| (A.9) |

where

Let , where is the constant appearing in Lemma A.1 and . We claim that for any in the convex hull of . To see this, represent as

| (A.10) |

where is an arbitrary probability measure on -ball around in terms of Frobenius distance. Then, for any , by Lemma A.1 and the convexity of the squared Hellinger distance,

| (A.11) |

This implies that by the triangle inequality. Thus, by (A.9), we can find tests for vs. such that the error probabilities are bounded by .

In order to get a test for vs. with similar error probability, we also need to cover the alternative with balls of size and satisfy the metric entropy condition

| (A.12) |

where is the distance on induced by on , is a constant and is a suitable subset of , called a sieve, such that is exponentially small. For a graph with vertices, consider the sieve to be the space of all densities such that the graph corresponding to has maximum number of edges and each off-diagonal entry of is at most . Then the metric entropy condition is given by

| (A.13) |

where we choose to ensure that , for some constants and , and that can be made as large as we want by making larger. Thus the best solution of (A.13) leads to the relation

| (A.14) |

which is satisfied if we choose , large. Also, for this choice of , we have,

| (A.15) |

where can be made as large as possible by making large. For the bound on the prior probability of the complement of the above sieve, we have, using the condition on prior (3.8),

| (A.16) |

For the prior (3.9), the first term in (A.16) is exactly zero, and for the prior (3.8), from equation (A.15),

| (A.17) |

where is a constant which can be made as large as we please by making larger. Note that under the condition , the requirement is satisfied as . Hence as found above is the desired posterior convergence rate. ∎

The following lemma establishes a norm equivalence necessary for finding posterior convergence rate and metric entropy calculations.

Lemma A.1.

If is the density of , then for all ,

-

(i)

, when ,

-

(ii)

,

for some universal constant .

Proof.

Let be the eigenvalues of the matrix . Half squared Hellinger distance between and is given by

| (A.18) |

and the Frobenius norm of the difference between and is given by, from (2.1),

| (A.19) | |||||

First we show that either or implies for all for sufficiently small . This is necessary to expand in powers of . Let us consider the case . Then,

| (A.20) | |||||

Now let . This implies . Rearranging the terms, we get, . Since every term in the product exceeds 1, we have,

| (A.21) |

The above equation, upon squaring and rearrangement of terms, gives, for all ,

| (A.22) |

Note that equation (A.21) gives that . Hence, the above equation implies that . Choose so that we get for all .

Now, let us assume that , for some . This implies, from equation (A.18),

Now, using Taylor’s series expansion. Then, from the above equation after rearrangement of the terms, we get, , so that,

| (A.23) |

Now, equation (A.19) gives that . Choosing , the first inequality follows.

To show the other way round, assume that . Then,

| (A.24) | |||||

Thus, if , then for some . ∎

We now give a proof of the result on the graphical lasso solutions being identical in case of a regular submodel for a non-regular model.

Proof of Lemma 4.1.

The graphical lasso solution for the model , given by satisfies, by the Karush-Kuhn-Tucker (KKT) condition; see, for example, Boyd and Vandenberghe, (2004), Witten et al., (2011));

| (A.25) |

where is a matrix with elements

| (A.26) |

For a non-regular model , consider the non-zero elements of the graphical lasso solution. Corresponding to the submodel of , we construct a matrix such that,

| (A.27) |

Then, satisfies the KKT condition corresponding to the model , and hence is a graphical lasso solution for . But the construction of the above solution gives that . This completes the proof. ∎

The following lemma is essential in proving the ignorability of the non-regular models for posterior probability evaluation.

Lemma A.2.

Consider a non-regular model with the corresponding regular submodel , having identical graphical lasso estimate given by . For as defined in Section 4.2, for fixed values of , we have,

| (A.28) |

Proof.

Consider maximization of the function

| (A.29) |

with respect to the elements where . Differentiating the above function for a particular value of gives,

| (A.30) |

The maximizer satisfies . Now consider the function as defined earlier. The derivative of with respect to satisfies

| (A.31) |

and,

| (A.32) |

The above two conditions give,

If the first derivative of is continuous at , then, we have . This immediately implies the result stated in the lemma. ∎

We now prove the result on the bound of the remainder term in the Taylor series expansion of the function . The proof requires other additional results which are also stated and proved below.

Proof of Lemma 4.3.

The Taylor series expansion of gives,

| (A.33) |

where is the remainder term in the expansion. Using the integral form of the remainder, we have,

| (A.34) |

Subtracting (A.34) from (A.33) gives,

| (A.35) | |||||

The above bound involves the maximum of the absolute differences between the elements of the Hessian matrices computed at two different values and . We first show that, with probability tending to one,

| (A.36) |

Using the matrix norm relations in (2.1), we get,

| (A.37) | |||||

with probability tending to 1, using (3.3). Thus, noting that , we prove the result in equation (A.36).

For any symmetric matrix of order , we note that has the form where , and s are some elements of . This can be derived easily by writing out the elements of the product of the matrices involved and noting that matrices like have non-zero entries at only two places corresponding to . Hence the elements of have the form , where ’s and ’s are some elements of and respectively. Then, using equation (A.36), we get, with probability tending to one,

| (A.38) |

Since this holds true for any arbitrary element of , using (3.3) and (A.38), we get that with probability tending to one,

| (A.39) |

where and are suitable constants.

We now prove the result on the error in Laplace approximation of the posterior probabilities of graphical model structures.

Proof of Theorem 4.4.

Using the Taylor series expansion of as in (A.33), we can write the posterior probability of the graphical structure indicator given the data as in equation (4.1) to be proportional to

| (A.40) |

We denote by for notational simplicity. Using (3.14), we get

| (A.41) |

Also, for , . Thus, the upper and lower bounds of the integral are given by

Note that,

| (A.43) |

if and the minimum eigenvalue of is bounded away from zero, which we prove in Lemma A.3 below. Hence, the bounds can be simplified to

| (A.44) |

Using the above bounds, the ratio of the actual integral to the approximate integral has upper and lower bounds given by

| (A.45) | |||||

The above expression is bounded between . Using Lemma A.3 below, , and hence the above bound on the ratio goes to 1 if , so that the error in Laplace approximation is asymptotically small.

∎

We now prove the result that the eigenvalues of the Hessian are bounded away from zero.

Lemma A.3.

Given a graphical model with model indicator , the minimum eigenvalue of the Hessian corresponding to the function , evaluated at , is bounded away from zero.

Proof.

The Hessian of the function corresponding to the full model with free elements has the form . The Hessian evaluated at the graphical lasso solution corresponding to the graphical model with model indicator is a principal minor of . Hence it suffices to prove that the minimum eigenvalue of is bounded away from zero. Note that, . Thus, using (3.3), . ∎

References

- Atay-Kayis and Massam, (2005) Atay-Kayis, A. and Massam, H. (2005). A Monte-Carlo method for computing the marginal likelihood in nondecomposable Gaussian graphical models. Biometrika, 92(2):317–335.

- Banerjee et al., (2008) Banerjee, O., El Ghaoui, L., and d’Aspremont, A. (2008). Model selection through sparse maximum likelihood estimation for multivariate Gaussian or binary data. J. Mach. Learn. Res., 9:485–516.

- Banerjee and Ghosal, (2013) Banerjee, S. and Ghosal, S. (2013). Posterior convergence rates for estimating large precision matrices using Graphical models.

- (4) Bickel, P. and Levina, E. (2008a). Covariance regularization by thresholding. Ann. Statist., 36(6):2577–2604.

- (5) Bickel, P. and Levina, E. (2008b). Regularized estimation of large covariance matrices. Ann. Statist., 36(1):199–227.

- Birgé, (1984) Birgé, L. (1984). Sur un théorème de minimax et son application aux tests. Probab. Math. Statist., 3:259–282.

- Boyd and Vandenberghe, (2004) Boyd, S. P. and Vandenberghe, L. (2004). Convex Optimization. Cambridge university press.

- Cai et al., (2011) Cai, T., Liu, W., and Luo, X. (2011). A constrained -minimization approach to sparse precision matrix estimation. J. Amer. Statist. Assoc., 106(494):594–607.

- Cai et al., (2010) Cai, T., Zhang, C., and Zhou, H. (2010). Optimal rates of convergence for covariance matrix estimation. Ann. Statist., 38(4):2118–2144.

- Castillo and van der Vaart, (2012) Castillo, I. and van der Vaart, A. (2012). Needles and straw in a haystack: Posterior concentration for possibly sparse sequences. Ann. Statist., 40(4):2069–2101.

- Curtis et al., (2014) Curtis, S. M., Banerjee, S., and Ghosal, S. (2014). Fast Bayesian model assessment for nonparametric additive regression. Comput. Statist. Data Anal., 71:347–358.

- Dawid and Lauritzen, (1993) Dawid, A. and Lauritzen, S. (1993). Hyper Markov laws in the statistical analysis of decomposable graphical models. Ann. Statist., 21(3):1272–1317.

- Dobra et al., (2004) Dobra, A., Hans, C., Jones, B., Nevins, J., Yao, G., and West, M. (2004). Sparse graphical models for exploring gene expression data. J. Multivariate Anal., 90(1):196–212.

- Friedman et al., (2008) Friedman, J., Hastie, T., and Tibshirani, R. (2008). Sparse inverse covariance estimation with the graphical lasso. Biostatistics, 9(3):432–441.

- Ghosal, (2000) Ghosal, S. (2000). Asymptotic normality of posterior distributions for exponential families when the number of parameters tends to infinity. J. Multivariate Anal., 74(1):49–68.

- Ghosal et al., (2000) Ghosal, S., Ghosh, J. K., and Van Der Vaart, A. W. (2000). Convergence rates of posterior distributions. Ann. Statist., 28(2):500–531.

- Guo et al., (2011) Guo, J., Levina, E., Michailidis, G., and Zhu, J. (2011). Joint estimation of multiple graphical models. Biometrika, 98(1):1–15.

- Harville, (2008) Harville, D. A. (2008). Matrix Algebra from a Statistician’s Perspective. Springer.

- Huang et al., (2006) Huang, J., Liu, N., Pourahmadi, M., and Liu, L. (2006). Covariance matrix selection and estimation via penalised normal likelihood. Biometrika, 93(1):85–98.

- Karoui, (2008) Karoui, N. (2008). Operator norm consistent estimation of large-dimensional sparse covariance matrices. Ann. Statist., 36(6):2717–2756.

- Lam and Fan, (2009) Lam, C. and Fan, J. (2009). Sparsistency and rates of convergence in large covariance matrix estimation. Ann. Statist., 37(6B):4254.

- Lauritzen, (1996) Lauritzen, S. (1996). Graphical Models, volume 17. Oxford University Press, USA.

- Le Cam, (1986) Le Cam, L. (1986). Asymptotic Methods in Statistical Decision Theory. Springer, New York.

- Ledoit and Wolf, (2004) Ledoit, O. and Wolf, M. (2004). A well-conditioned estimator for large-dimensional covariance matrices. J. Multivariate Anal., 88(2):365–411.

- Letac and Massam, (2007) Letac, G. and Massam, H. (2007). Wishart distributions for decomposable graphs. Ann. Statist., 35(3):1278–1323.

- Liu et al., (2009) Liu, H., Lafferty, J., and Wasserman, L. (2009). The nonparanormal: Semiparametric estimation of high dimensional undirected graphs. J. Mach. Learn. Res., 10:2295–2328.

- Meinshausen and Bühlmann, (2006) Meinshausen, N. and Bühlmann, P. (2006). High-dimensional graphs and variable selection with the lasso. Ann. Statist., 34(3):1436–1462.

- Park and Casella, (2008) Park, T. and Casella, G. (2008). The Bayesian Lasso. J. Amer. Statist. Assoc., 103(482):681–686.

- Pati et al., (2012) Pati, D., Bhattacharya, A., Pillai, N., and Dunson, D. (2012). Posterior contraction in sparse Bayesian factor models for massive covariance matrices. arXiv Preprint 1206.3627v2.

- Rajaratnam et al., (2008) Rajaratnam, B., Massam, H., and Carvalho, C. (2008). Flexible covariance estimation in graphical Gaussian models. Ann. Statist., 36(6):2818–2849.

- Rothman et al., (2008) Rothman, A., Bickel, P., Levina, E., and Zhu, J. (2008). Sparse permutation invariant covariance estimation. Electron. J. Statist., 2:494–515.

- Rothman et al., (2009) Rothman, A., Levina, E., and Zhu, J. (2009). Generalized thresholding of large covariance matrices. J. Amer. Statist. Assoc., 104(485):177–186.

- Roverato, (2000) Roverato, A. (2000). Cholesky decomposition of a hyper inverse Wishart matrix. Biometrika, 87(1):99–112.

- Wang, (2012) Wang, H. (2012). Bayesian graphical lasso models and efficient posterior computation. Bayesian Analysis, 7(4):867–886.

- Witten et al., (2011) Witten, D. M., Friedman, J. H., and Simon, N. (2011). New insights and faster computations for the graphical lasso. J. Comput. Graph. Statist., 20(4):892–900.

- Yuan and Lin, (2005) Yuan, M. and Lin, Y. (2005). Efficient empirical bayes variable selection and estimation in linear models. J. Amer. Statist. Assoc., 100(472).

- Yuan and Lin, (2007) Yuan, M. and Lin, Y. (2007). Model selection and estimation in the Gaussian graphical model. Biometrika, 94(1):19–35.

- Zhao et al., (2012) Zhao, T., Liu, H., Roeder, K., Lafferty, J., and Wasserman, L. (2012). The huge package for High-dimensional Undirected Graph Estimation in R. J. Mach. Learn. Res., 98888:1059–1062.