Optimization under convexity constraints: are the finite element discretizations consistent ?

Abstract

It is proved in [1] that the problem of minimizing a Dirichlet-like functional of the function discretized with Finite Elements, under the constraint that be convex, cannot converge. Here, we first improve this result by proving that non-convergence is due to the mesh refinment lack of richness, remains local and is true even for any mesh. Then, we investigate the consistency of various natural discretizations ( and ) of second order constraints (subharmonicity and convexity) without discussing the convergence. We also numerically illustrate convergence of a method proposed in the literature that is simpler than existing methods.

Keywords:convexity; finite elements; interpolation; conformal approximation; minimization

subjclass:26B25, 52A41, 65K10, 65N30, 90C25, 91B24

1 INTRODUCTION

This paper is devoted to the numerical discretization of optimization with constraints on the second order derivative, namely problems of the form

| (1) |

where is a functional and is a subset of the set of symmetric matrices. Such problems appear in various contexts, in particular in physics and economics.

Since Newton, the shape of minimal resistance has been a topic of interest. It is called the Newton’s problem and is of the type of (1). With some additional assumptions, it amounts to looking for a concave function that minimizes a nonlinear functional. See for instance the original book [2], the historical survey in [3], more recent theoretical results in [4, 5, 6] or numerical results [7, 8].

The associated problem of discretizing convex functions or bodies

is indeed wider than expected. For instance, the Alexandrov’s

problem (see [9] and [7]), the Cheeger’s

constant [7, 10] and the Newton’s problem

[7, 8] can be numerically studied.

In economics, it suffices to remember that utility functions are concave to see the very wide applicability of these problems. For instance, in [11], the authors are interested in finding the minimum of a convex and quadratic functional over the set of convex functions

| (2) |

where and is a (2,2) symmetric and positive-definite matrix and is given by

| (3) |

So is strictly convex and the set is convex. It is then easy to check that there exists a unique minimizer of over . The regularity of the solutions is studied in [12]. Note that, when and in a domain with nonnegative coordinates, the problem degenerates: an exact convex solution exists, up to an additive constant

| (4) |

that can be fixed if we force to vanish at a point (if ).

In [1], Choné and Le Meur exhibit an obstruction to the

convergence of the mere discretization of this problem through

conformal Finite Element (FE) method on regular meshes. They

also extensively use the explicit solution (4) to illustrate

the lack of convergence when a predicted condition is no more

satisfied. Here “conformal” means that the discretized

function is supposed to satisfy exactly the continuous constraint. As

a consequence of this result, no optimization process that would use

such conformal discretization of both the functional and the

constraint may converge for any solution on these meshes. Yet

approximation theory easily proves convergence of every separate

discretization of these terms.

A possible approach to circumvent the mesh problem is, first, to test whether a sample of values on given points (and not mesh) may be associated to a convex function or body. Then one must construct the associated mesh (so, function dependent !) so as to interpolate. This was done in [13] for FE by Leung and Renka. But such a regularity is too restrictive for us. This article [13] reviews other papers, some of them being commented as false. It proves that the issue is not so simple.

The projection of a given function is addressed in [14] through the saddle-point method. In this article, the authors even weight the convexity constraint to tune the convergence to the solution. The computations appear to be more robust than expected by theory. An attempt of explanation is given in [15].

In [16], the authors describe and implement an algorithm that optimizes not in the set of discretized and convex (i.e. conformal) functions but in the set of the convex functions after discretization (so that they may be non-convex once discretized). More precisely they characterize, for a specific structured set of cartesian points, the image through the discretization of a (continuous) convex function. This yields such a huge number of constraints on the function that it may not be recommended.

In [7], Lachand-Robert and Oudet address the problem of discretizing a convex body. They use the parametric generalization in order to discretize convex functions’ graphs. In the functional, they isolate the dependence on the point , the unit normal at and the signed distance . Although they notice that the three variables are “somehow redundant”, they implement a gradient like method, based on the variation of only . They address both the Alexandrov’s problem, the Cheeger’s sets and the Newton’s problem. This was revisited since in [10] and solved in a very elegant way in [8].

Separately, Aguilera and Morin [17] prove convergence of a Finite Difference (FD) “approximation using positive semidefinite programs and discrete Hessians”. In [18], the same authors prove even convergence of a Finite Element (FE) discretization of the weak Hessian. Since FD are included in FE for convenient meshes, these two articles seem to contradict both [1] and the present article. Indeed, they do not, but we discuss them below (section 5).

In [19], Ekeland and Moreno propose a non-local discretization that relies on the representation of any convex function as the supremum of affine functions (its minorants). So their “discrete” representation of continuous functions is conformal but non-local. The major drawback is that the complexity increases drastically with dimension, due to the nonlocality, but it works.

More recently, two very different means of resolution were proposed. Both are non-conformal in the sense that the discretized solution is not convex. In the first one, Mérigot and Oudet [21] propose to discretize the convexity constraint by under sampling it. More precisely, they prove convergence of their algorithm if the constraint is forced only on a subset of the sampling points. In the second one, Mirebeau [22] proves that for a given grid, he may provide a sequence of sets of (less than four) points on which it suffices to force convexity to ensure convexity at convergence on this given grid. This makes only linear constraints.

There seems to be a convergent opinion through [22], [21], [18] that indeed the number of constraints must be not too large. A deeper discussion of this crucial point is postponed to a forthcoming article.

In [20], the author goes further than [18]. He uses approximation theory, where there is no reason why a function (should it be convex or not) should not be approximable. So as to remain inside this theory, he uses two auxilliary functions that make his solution strictly convex, so that the constraint of convexity may not be saturated. Nevertheless, we are surprised that these functions are not needed in his numerical experiment. It could be due to the fact that the hidden constraints (that will appear below) are filled by the exact solution and so do not trigger any discrepancy. This explains why our results are not contradictory with Oberman’s or Wachsmuth’s.

A totally different tool has emerged since. It consists in using an evolution PDE with a as an initial condition. In [23] (and other articles), the author computes the convex envelope of a graph using such a nonlinear PDE. Later [24] exhibits an evolution PDE, close to the previous, which, starting from a given , is proved to converge to the convexified of . They use stochastic control representation to prove an exponential convergence. This set of evolution PDE is a new idea and very important in optimal transport theory.

The present article deals with two main types of non-convergence

results. On the one hand, the non-convergence in for conformal

Finite Element (FE) is revisited after [1] from a

theoretical point of view. On the other hand, the consistency of

discretized linear optimization over second order constraints is

investigated for various discretizations ( and ) and various

constraints: linear (subharmonicity) or nonlinear (convexity). The

motivation for convexity has been stressed. Subharmonicity is only

studied as an intermediate step toward convexity because it is

linear.

In Section 2, first we restate some already known results, then we prove that non-convergence is purely local and so is true for any mesh. In Section 3, we investigate the consistency of various FE discretizations of our model problem. Section 4 is devoted to the consistency of FE discretizations (strong or weak convexity). We discuss the articles [17, 18] that could seem to contradict [1] in Section 5 and we conclude in Section 6.

2 THEORETICAL RESULTS ON THE FEM

In the present section, we first recall some already known results and make them more explicit.

2.1 Already known results

In [1], various results are proved. Since the goal in the present subsection is to extend this study, we need to remind the reader of these results. We consider an open convex and bounded domain of , but we use only (and and positive) in applications. The Lemma 3 of [1] states:

Lemma 1

A function , in every triangle of ’s mesh, is convex if and only if, for any pair of adjacent triangles

| (5) |

where (resp. ) is the (constant) gradient of inside triangle 1 (resp. 2) and is the unit normal pointing from triangle 1 to 2.

As reminded in [1], convexity of can be defined dually as where means the matrix is positive semi-definite, is a nonnegative test function in and

| (6) |

This definition is weak (in the sense of distributions) but it is also equivalent to a strong one when is sufficiently regular. We will use a weaker definition where the trial and test functions will be in a (finite dimensionnal) subspace of : the set of some FE functions. Last we will report on [18] which uses an even weaker definition where the test functions are in a much smaller subspace than ’s. One can easily check that the weak definition of convexity (with test functions) implies the weaker definition of convexity (with only the basis functions in associated to interior points as test functions) but they are not equivalent.

The proof of Lemma 1 is based on the following formula written for the function :

| (7) |

where the summation is taken over all interior edges of the mesh,

and are two unit vectors, is a

function with compact support in , and

designate the two (constant) gradients of in the two

triangles that share the edge and is the unit normal

from triangle 1 to triangle 2. This formula is right thanks to the

property that the gradient of a continuous function across the edge

has its tangential derivative along the edge continuous. Namely

where is the

unit tangent vector. The proof also relies on the fact that for all unit vector

, the bilinear form is positive semi-definite, whatever

.

Through a proof very similar to the one of Theorem 4 in [1], one may prove a wider Theorem that even applies locally:

Theorem 1

Let be an open and convex subset of and a triangulation of . If there exists an open and convex such that the following property is satisfied in and for the mesh :

| (8) |

then any function convex and will satisfy the following equation in the sense of distributions on :

| (9) |

The proof relies on the fact that if a function is convex, then by Lemma 1, the gradient’s jumps are non-negative. As a consequence, in Formula (7), if is convex, the scalar coefficients are all non-negative. But separately, if condition is satisfied, and so even the non-diagonal terms of the hessian () are sign-constrained !

Notice first that property only depends on the geometry of the mesh and not on any function. Notice then that the property is at given but, if it remains for a sequence of in , then the associated functions given by Theorem 1 satisfy (9) even at the limit in . Yet such a property (9) is (sometimes) contradictory with the property of convexity. For instance , where and , is strictly convex. Yet has no sign prescribed if is only strictly convex. This is the key of the obstruction to the convergence stated in [1]. The next subsection is devoted to discussing the generality of .

2.2 Is property frequent ?

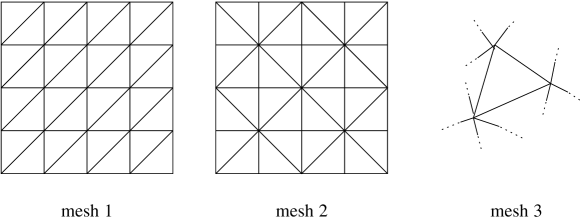

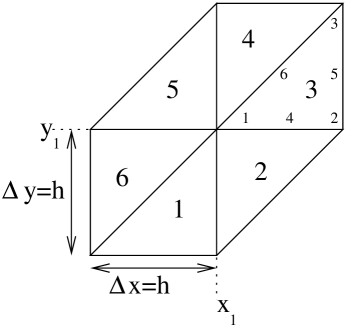

In this subsection, we start from some elementary observations on particular meshes, then we argue on whether such meshes are frequent and state a Theorem. Three types of meshes may be considered that are depicted in Figure 1.

Concerning mesh 1, three different unit normals (up to a multiplicative factor ) exist in all the domain: . If we choose and , the values taken by (with the possible ) are . They are all nonnegative.

Concerning mesh 2, four types of unit normals can be found in all the domain: . If we choose and , the values taken by (with the possible ) are . They are all nonnegative.

Any structured mesh like mesh 1 or 2, if refined while keeping the same structure, will satisfy with the very same and for any . But what can be stated about a more general mesh like mesh 3 ?

We are going to prove the following Theorem.

Theorem 2

Let be an open and convex set of , an open and convex subset and a triangulation of

.

For any given and , there exists such that

is true in and for . Moreover, if the

refinement process does not enrich the edges’ directions of

in , then the property is

true for any in .

Proof of Theorem 2

First, one must notice that the condition is invariant through changing into . So, it does not depend on the choice of the hyperplane’s unit normal.

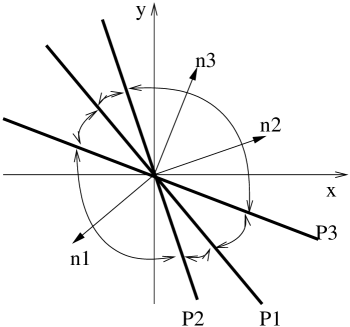

Let us take a very general mesh like mesh 3 for which we may isolate a single triangle. Then, for each of the three unit normals (up to the multiplicative coefficient -1), having is equivalent to having and in the same closed half plane whose normal is . Equivalently, we can take either and on the same side as or on the opposite side. Gathering the conditions associated to each of the three edges, we are led to choosing both and in one of the six half cone that intersects none of the three hyperplanes. Such a configuration is depicted on Figure (2). The three unit normals are drawn and called n, n, n and their associated hyperplanes are called P, P, P. So, one may easily find such a couple for any given triangle.

Even better, whatever might be the finite number of edges for a larger and a given , one sees obviously that such a choice of and is easy since there always exists a finite number of hyperplanes. As a consequence, and can be choosen to be both in any of the cones which partition the whole unit circle. So the property is true even on any given and potentially unstructured mesh of a subdomain of .

Could a refinement process preserve the property for a given couple (), a given and any ?

In case of any general given mesh we have just proved that one may find and , should they suit the property only in . Then, for instance, if the refinement process is such that every triangle in is refined into four homothetic subtriangles, it is obvious that no more edges’ direction will be provided. As a consequence, the very same and will then suit property in for any refined mesh and any . The proof is complete.

In a sense to be defined, the set of refinement processes that enable is open and non-empty. The main question is “Does the refinement process enrich in normals ?”.

2.3 More information on the lack of convergence

In [1], the authors state that the ”conformal method may not converge for some limit function” because the second derivative of the limit is forced to satisfy an unnatural condition. In this subsection, we give a more precise result in and still use our Lemma 1 that enables to identify the convexity of and the non-negativity of its gradients’ jumps (for FE). This enables us to state our main Theorem:

Theorem 3

Let be an open and convex domain in , an open and convex subdomain of and a family of meshes . If the property is satisfied in and for the meshes , then there exists and a convex function such that

This Theorem uses that if Property is satisfied in a domain for a family of meshes , should it be only locally in , there will be two unit vectors such that (9) holds. Given those , there exists a function that may not be the limit in of any sequence of functions both and convex (in a strong definition) on this family of meshes. The improvement of this Theorem with respect to [1] is that the obstruction is local. As a consequence we may apply our obstruction on any mesh and not only regular ones.

We need some more preliminary results and definitions before proving this Theorem 3 concerning FE.

Definition 1

Let be an open subset of , and . For any and two independent unit vectors, there exist two positive numbers such that

For such , one defines:

If , then

. We are going to prove that such a quantity

will be overconstrained by

the mere discretization and the limit will not satisfy the right

sign of the second derivative.

We want now to define an explicit solution depending on some parameters. A well-chosen combination of these parameters will provide a non-approximable function. For instance, let and the problem (2, 3) for a positive definite real matrix be such that:

| (10) |

Then there exists an exact solution thanks to (4):

| (11) |

The function is such that it is zero at the corner of the domain chosen but it can easily be generalized to other domains. Simple computations prove the following formula:

| (12) |

where are the components of . It is then useful to state the following Lemma.

Lemma 2

Let be two given independent unit vectors in . Let and given. Then, there exists such that , and

| (13) |

provided are such that there exists .

Roughly speaking, Lemma 2 states that for any independent , one may find a positive definite matrix such that the associated satisfies the following property on its associated bilinear form:

Proof of Lemma 2

From the formula (12), one sees that it is sufficient to find a positive definite symmetric bilinear form () such that, for independent given, . We will build up from its eigenvalues and eigenvectors.

Let be a unit vector between and (normalized mean for instance). Then let be a unit vector normal to . With the same notations for and in this new basis, and .

Let now be a matrix in the canonical basis with the eigenvectors and the associated positive eigenvalues . Obviously, is positive semi-definite. Then which may be less than given, for an appropriate choice of . Then the are the coefficients of the matrix in the canonical basis as written in (10).

We have now obtained all what is needed to start the following proof.

Proof of Theorem 3.

Since we assume is satisfied in for , this provides a couple of vectors . Theorem 1 enables us to claim that any function satisfies (9) in the sense of distributions in :

| (14) |

for any nonnegative . This property obviously remains for open and convex subdomains of .

Should it be needed, one could decrease and find a subdomain such that for any nonnegative , the function

| (15) |

is nonnegative and in . So the function is eligible for equation (14) whatever . The second derivative of may be computed:

So we have, for any nonnegative :

| (16) |

Separately, given , Lemma 2 enables us to claim there exists a convex quadratic function such that (13) is true for given. Moreover, because of (16), since the open set is of non-zero measure, and is a constant known by (12), we have

As a consequence, for convenient , we are led to

| (17) |

for any nonnegative and convex and . This last inequality contradicts any possible convergence in of a sequence of convex functions in to given by Lemma 2.

The previous Theorem adds one more argument to the need of convenient numerical methods to discretize the constraint of convexity.

3 Consistency of the FEM

The non-convergence of the convexity problem (2, 3) discretized by conformal Finite Elements is proved and numerically illustrated in [1]. It is even proved to apply to non-regular meshes in the subsection 2.3. We give here a very different argument by studying the consistency of various discretizations of convexity.

One could wonder why study consistency. The reason is that when one discretizes convexity (or even its linear form of subharmonicity), there exist meshes and FE on which the discretization is not consistent. As a consequence, any proof of convergence must exclude at least these cases. The fact that the FE-discretized Dirichlet functional and the FE-discretized Hessian matrix converge separately is not sufficient. Already [25] claimed convergence, but was later proved to be wrong in [1].

3.1 Use of the gradients’ jumps for convexity

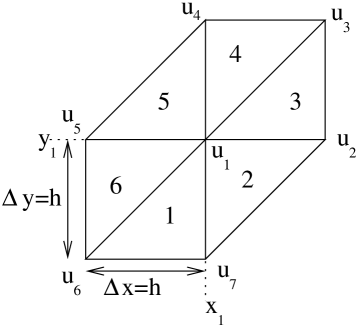

Given a sufficiently smooth function , one may interpolate it in FE as . If the mesh is structured as in Figure 3, should it be local, one may compute the gradients’ jumps accross the edges as functions of the values at the various involved nodes. Then one may compute the series expansion of the sampled values from the exact initial function . The jumps between triangles 1 and 2, 2 and 3 and last 3 and 4 are respectively:

| (18) |

where we denote the partial derivative with respect to and the second order derivative with respect to . When , instead of forcing the solution of a problem to be convex, we force it to some mesh-dependent combination of its second order derivatives to have a sign or another. In addition, this combination is meaningless since for the convex limit function, it may have whatever sign. We will say that such a discretization is not consistent.

We may repeat here that our non-consistency result is not contradictory with the convergence results of [20] (for instance) since these results rely on a regularization that makes the algorithm look for strictly convex functions. Looking in the interior of the set of convex functions, the constraint may not be saturated and so disappears.

Below, we investigate the consistency of various other discretizations.

3.2 Use of a weak version

We use here a weak definition of convexity which is similar to the one of [18], except that their trial basis and test basis functions are different. We use the same trial and test basis. Their method is fully discussed and illustrated in Section 5.

3.2.1 The subharmonicity constraint

Subharmonicity is an interesting property simpler than convexity since it is only linear. A weak definition of subharmonicity () is, for any test function in the discrete basis ( is defined in (6)):

| (19) |

One may then prove the following Proposition:

Proposition 3.1

The weak discretization of the subharmonicity constraint on a mesh like in Figure 3 is consistent:

| (20) |

where is the node at the center of the cell’s group .

The proof is very easy and left to the reader. Indeed, it is only the

discretization of the Laplacian which is known to be consistent and

even convergent !

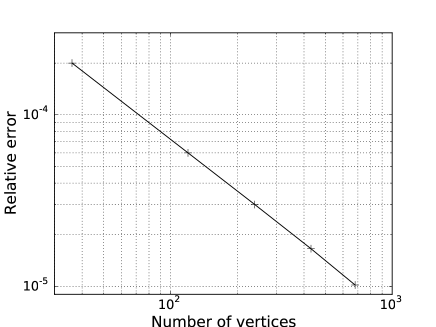

In order to test this discretization, we used the Matlab package optim to minimize the functional , where , over the set of subharmonic functions. The initial condition is . The exact solution of this projection is and its Laplacian vanishes. The convergence with the procedure quadprog of quadratic programming can be seen on Figure 4. It is quite satisfactory.

3.2.2 The convexity constraint

One may give a weak definition of convexity:

| (21) |

for any , basis function of the FEM at the node . One may then prove the following Proposition:

Proposition 3.2

This discretization (21) for the (nonlinear) convexity contraint is consistent. Nevertheless, the numerical treatment of the linear and nonlinear constraints should raise inaccuracies since they are of very different orders of magnitude ( and ). A very natural question would be to investigate its convergence. Such a study is postponed to an other article.

The consistency of the FEM is tested for various meshes. The weak Hessian is reported in Table 1 where one may claim that two meshes are non-consistent with the determinant but all are consistent with the trace (laplacian).

4 Consistency of the FEM

In the present section, we investigate the consistency of various discretizations through FEM of two second order derivative constraints: subharmonicity and convexity.

First, we interpolate a continuous function to a function

in a domain meshed with triangles

as in Figure 5. Here, the index denotes both vertices and

edge midpoints. Then we compute the discretized version of the second

order term constrained to be nonnegative (various versions are

treated) and compute its series expansion. If forcing it to be

nonnegative amounts to forcing the continuous limit function to the

correct constraint, then we claim the discretization is

consistent. Otherwise it is

inconsistent.

For the whole section, we assume the mesh is (at least locally) structured around the point of coordinates . The local numbering of triangles is depicted in Figure 5. The node is localy numbered 1 in every triangle and the local numbering of nodes is depicted in triangle of Figure 5.

4.1 Gradients’ jumps for the convexity constraint

In a way similar to the case, one may prove for functions :

for any interior edge of the mesh, and are two unit normal vectors, is a function with compact support in . By taking localized along the edge , one may state that this definition of convexity (with test functions) implies the non-negativity of the gradients’ jumps.

In order to test the consistency of such a discretization, we compute the gradients’ jumps accross the edges common to triangles and , and and last and . Of course, they are not constant since they are FE. After an exact computation and a series expansion (details left to the reader), one may state the following Proposition.

Proposition 4.1

The discretization of the convexity constraint with the jump of the gradients between triangles and , and , and of a function on a mesh like in Figure 5 gives terms

| (23) |

Such a discretization is non-consistent.

Since for instance between triangles and , changes sign (but remains ), one deduces from (23) that forcing the non-negativity of the gradients’ jump along the whole edge forces the limit function to satisfy the non-natural equality condition !

4.2 Weak version of the second derivative at a vertex

We define the weak (i.e. with trial and test functions) version of the Hessian matrix at vertex as:

| (24) |

where is defined in (6). Strictly speaking, this may not provide a correct weak version of non-negativity since changes sign. Anyway, one may state the following Proposition which proof is left to the reader:

Proposition 4.2

It appears that such a discretization is not even consistent for the linear part of the constraint. More precisely, while one could believe one forces the solution to be subharmonic, indeed, one forces it to be such that ! The full nonlinear convexity constraint on the same vertices may only work worse.

One must notice that the fourth order of the expansion in (25) is meaningful. Indeed, on the one hand the three midpoints quadrature is exact for functions in a triangle. On the other hand the basis function for a vertex vanishes on these midpoints. As a result, the order two term is identically zero. So the first non-zero term is the fourth one and the constraint is of fourth order too.

4.3 Weak version of the second derivative at an edge midpoint

We define the weak version of the second derivative at an edge midpoint (denoted by index ) in a way similar to (24). Indeed, the function in (24) is replaced by the basis function associated to an edge midpoint indexed by .

As in subsection 3.2, the basis functions (of the edge midpoints) are non-negative. So it is a priori an admissible weak formulation of semi-definite positiveness.

4.3.1 The subharmonicity constraint

Let us assume we discretize the constraint by

| (26) |

for all index of an edge midpoint interior to . One may then state a Proposition (which proof is left to the reader):

Proposition 4.3

The discretization of the linear part of the convexity constraint according to (26) on a mesh as in Figure 5 () gives the same series expansion, whether the edge is vertical, horizontal or diagonal:

| (27) |

for any index of an edge midpoint interior to . Such a discretization of an inequality constraint is consistent.

Various questions remain. If we discretize the subharmonicity (or the convexity) constraint only at edge midpoints, is it enough constraints or not ? More generaly, the amount of constraints compared to the amount of degrees of freedom (dof) should be discussed. The relevance of this question seems to be the conclusion of most recent articles like [22, 21, 18].

4.3.2 The convexity constraint

Like in the subharmonic case, we take a weak version of the continuous nonlinear constraint det with (nonnegative) test functions associated to every edge midpoint in the interior. One may then easily prove the following Proposition:

Proposition 4.4

The discretization of the nonlinear part of the convexity constraint on a mesh as in Figure 5 () gives:

| (28) |

for any index of an edge midpoint interior to . Such a discretization of an inequality constraint is consistent.

So the convergence order of the linear constraint is two while the nonlinear one’s is four. Such a discrepancy between the orders of convergence of those two constraints should be managed in numerical simulation using both constraints. At least this discretization is consistent.

5 Discussion on the Aguilera and Morin’s articles

Roughly speaking, the first article [17] proves convergence of the FD discretization of problems like ours. The second [18] proves convergence of the FE discretization of the same problems but the authors imagine the clever trick of using different basis for the trial and the test functions.

5.1 Finite Differences

In [17], Aguilera and Morin deal with FD and “prove convergence under very general conditions, even when the continuous solution is not smooth”. Their proof relies on approximation theory and on a weak definition of convexity, namely the FD approximation of the Hessian matrix is forced to be positive. They stress that their FD-convexity is not equivalent to a continuous convexity. As a consequence, their approximation is not conformal. So there is no contradiction with [1]. In addition, one must notice that the number of constraints is roughly twice the number of interior points. It is large, but grows only linearly with the degrees of freedom. They also provide numerical experiments.

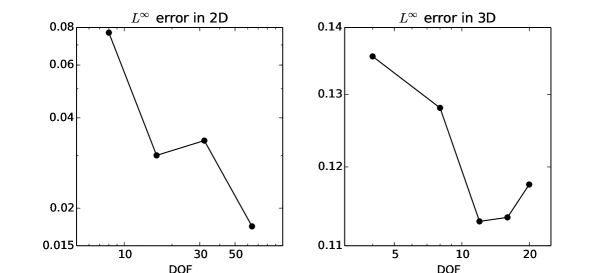

Unfortunately the numerical experiments are not very convincing. Concerning the monopolist problem in 2D, they claim that “the error in the norm is smaller or approximately equal to ” (p. 27). Yet, their Table 1 provides errors that we draw in a loglog scale in the left part of Figure 6. The order of convergence is not clear.

For the monopolist problem in 3D, the authors notice that “the error is not converging to zero with order ” (p. 29). Since they only prove convergence and do not forecast any order, there is no contradiction. But when their Table 2 is drawn in a loglog scale (see Figure 6 right), convergence seems not to be reached yet. Moreover the execution time grows faster than polynomialy both for 2D and 3D monopolist.

As reminded by the authors, FD discretization gives the very same matrices as the FE (both for trial and test functions), on a mesh like our mesh 1 on Figure 1 (except boundary conditions irrelevant here). In this sense, one may claim that their FD discretization is somehow equivalent to a (for trial) - (for test) discretization which was proved to be non-consistent. Indeed, the next article [18] gives one example (Example 3.7 p. 3150) of discretization and a weak definition of convexity (with trial and test functions, so alike FD discretization), where “ does not converge to as ” (p. 3151 and Figure 3.1).

Discussing the way these results on FD are coherent with the results on FE is postponed to a forthcoming article.

5.2 Finite Elements

In [18], Aguilera and Morin prove convergence of the discretization of the full problem: not only the approximation of the Hessian, but also of the functional together.

Especially, they define , interpolation of on a given mesh with respect to the trial functions basis as . They also use a (possibly) different FE basis for the test functions . Then, the discrete Hessian matrix is defined weakly by and FE convexity is defined as:

for all in the test functions basis, where they denote if is positive semi-definite. Notice that the matrix is a rectangle if the trial and test basis do not have the same number of functions !

Then their main result states convergence of the discretization once one assumes at least (p. 3147):

-

C.2

There exists a linear operator with values in the discretization space (the interpolant), an integer , and a constant independent of and such that

-

C.3

The basis test-functions are such that

The condition C.3 merely states that the test functions, that are

supposed to approximate positive functions,

remain nonnegative. So the basis functions are at most or a

subset of .

The condition C.2 is very classical and states that the trial space is . In addition, the proof requires . In other words, the trial functions must at least be .

This is seen by the authors who say they “need to elaborate” on the

condition . On their p. 3150, they notice the FE discretized

Hessian ( and so ) expands into the FD scheme (for one

specific mesh !) at first order and so they refer to their FD article

to conclude that in the case of some specific meshes, their Theorem

“also holds for ” (or FE).

Yet, the very next example they provide is and they “report

numerical evidence supporting the necessity of assuming in

[their] Theorem 3.6” (p. 3150). They stress that “since is

convex, the projection should converge to as , but this is not the case in this example” (p. 3150) and “

does not converge to as ” (p. 3151). They

summarize this result by saying “although there is some sort of

super-convergence for some meshes, for general meshes […] FE-convex

piecewise linear [m=2!] function may not suffice”. Discussing

how this numerical example articulates with [17]

is postponed to a forthcoming article.

All this is even complexified when the authors cope with numerical experiments of FE discretization. As they notice, the FE test functions in the basis are not all nonnegative. So they “considered the usual piecewise linear nodal basis for the vertices” and “the usual quadratic bubbles” for the edges’ midpoints (p. 3152).

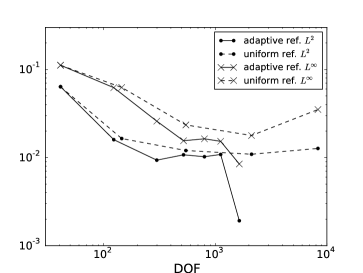

Their table of convergence (Table 5.1) is transformed into loglog graphic in Figure 7. The last simulation with adaptive refinement gives a good point, but the uniform-refinement simulations give non-decreasing errors. Again convergence is not obvious. So as to make this convergence obvious, we illustrate their method in Section 5.4.

5.3 Are [17, 18] contradictory with [1] ?

The answer is no. But it deserves to be explained.

Both [18] and [1] use a dual definition of convexity and have conclusions that could seem to be contradictory. The only difference is that [18] uses different basis for trial and test functions:

while [1] uses the same basis for trial and test functions, both in :

Both discretizations are weak in a sense, but the one of [18] has less test functions than trial functions and so less contraints than the number of Degrees Of Freedom (DOF). Indeed means that the trial basis is rather large (at least ) and condition C.3 that the test basis is at most . The matrix of constraints is rectangle and there are less constraints than the unknowns whereas the discretization of [1] uses the same basis for trial and test and so involves square matrices.

Then, it is not surprising that the problem discretized with the weak

definition in [1] is overconstrained : there are as

many constraints as DOF ! Indeed it appears also from the literature

that the amount of constraints must be not too large. The article

[22] defines a stencil of constraints that is coarser

than the grid and [21] defines a subgrid of points

on which the constraint is applied. Then it seems coherent that the FE

proof of [18] requires more DOF than the

number of constraints. The methods of [20] and similar

works look for functions in the interior of the convex

functions set where the boundary are irrelevant.

Our Proposition 4.2 proved in subsection 3.2 states that if we discretize with FE and use a set of test functions (but then some test functions change sign), then the discretization of the linear part of the constraint is non-consistent. It proves that the proof of convergence of FEM by [18], which fails if the test functions change sign (as in and higher), maynot be improved on that point. So we do believe their theorem is optimal.

If we use the consistency test for some discretizations, we can compute the first non-zero term in the expansion of

for discretizations and report these computations in Table 1 (lower part) on various meshes depicted in Table 1 (upper part). It appears that some discretizations are not consistent with convexity (two on the left) while others are (two on the right).

5.4 Does the FEM converge ?

The convergence is proved in [18] for

() trial functions and test functions with additionnal

assumptions. In order to ensure the numerical convergence, we wrote a

Python code to mesh a square , discretize the

functional (2), and discretize the nonlinear constraints of

inequality (convexity). Then we use the minimize function in

scipy to minimize the functional. The execution time are

meaningless since they rely on the level of precision we ask and we

only want to illustrate convergence.

In a very first step, we look for the solution to (2,3,10), which exact solution is given in (11). It is not surprising that, whatever the mesh, we can get a relative error of . It only justifies that a quadratic function may be approximated by a numerical code without error.

In order to justify convergence, one needs a more complex convex function to find.

5.4.1 Convergence to an exact solution

We choose

and take the functional

which is also, up to a constant, . The function is constrained to be convex and be such that , which makes sense since the function is convex and so regular enough for evaluating at . The solution is convex, but we are going to prove that its interpolate is not convex.

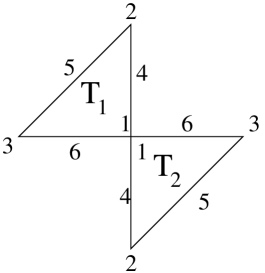

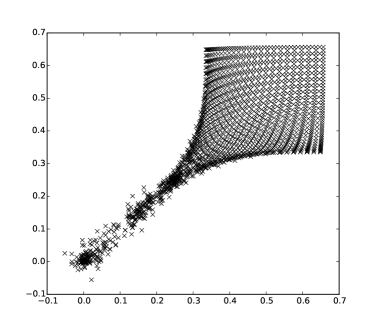

The geometrical argument is that we -interpolate a function of on a mesh like mesh 1 in Figure 1. Let us take the interpolate of on the two triangles depicted in Figure 8, close to the point at the center as before. Let us prove now that the interpolate is strictly convex inside . Along the segment between the point numbered 1 in and the point 5 in , one has:

where is the value of the interpolate at the DOF locally numbered in triangle . These values are the same as those of by definition of the interpolate and enable to write the last equality. It is then easy to check that this function is strictly convex for . The same computations in the triangle gives for

Since both and are strictly convex in their domains and have the same value on three aligned points, the function maynot be convex at least on the segment between the points numbered 5 in and the point numbered 5 in (see Figure 8).

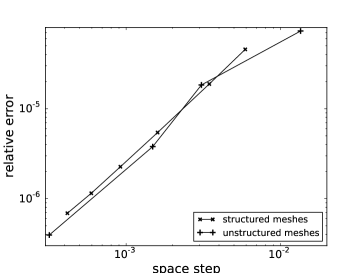

Despite the non-convexity of the interpolate of the exact solution (which is convex), the convergence of the FEM method proposed and proved in [18] is clearly illustrated in Figure 9 where structured and unstructured meshes are used.

The order of convergence seems to be the same on structured and unstructured meshes. It is roughly 1.6.

5.4.2 Can this method be used ?

In order to use this method justified theoretically (in [18]) and numerically (above), we look for a solution to the problem of the monopolist in :

There exists no explicit solution to this problem but some properties of the solution are known (see [11]).

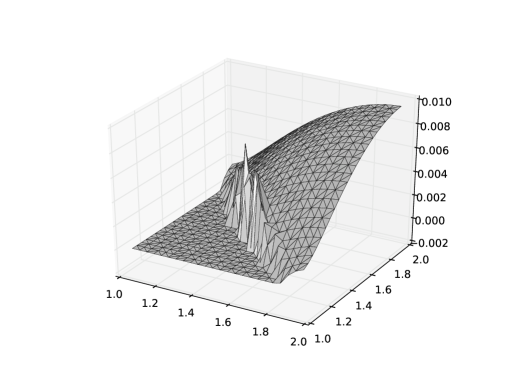

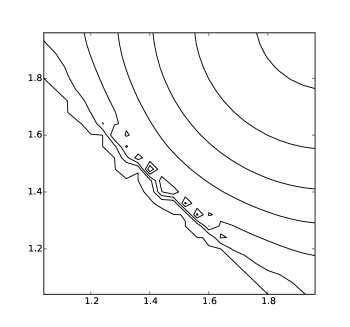

The computed function on a structured mesh , its gradient and its second eigenvalue look similar to the ones computed in [22]. The graph of the full function would be difficult to understand because of the number of DOF. That is why we only use the information from in Figure 10 (left).

So as to display the gradient, one might compute the gradient for associated to an interior point, with a function , and . But since the quadrature uses the three mid-points, it is right only up to functions, and so the integral being over a function is not exact. Yet, since the discretization, which is exact, gives the same graphical result with less points, we consider the Figure with test functions to be acceptable. The result may be seen in Figure 10 (right).

In Figure 11, one may see the second eigenvalue of the Hessian, computed as a function tested on functions and its level sets on the right. The first eigenvalue is not significant because of numerical artifacts. They are computed as the two roots per interior vertex of:

6 CONCLUSION

In this article we prove (Theorem 3) that the discretization of a function that satisfies a strong definition of convexity (with test functions), which is equivalent to the gradients’ jumps positivity (for FE), and so is conformal, leads to an additional constraint on the limit function. While [1] dealt mainly with regular meshes, our result extends explicitely to any mesh. The error of such a discretization of the constraint does not vanish with the space step. We justify that it is localized where the additional constraint on the limit function is not satisfied. The condition for existence of such a counter-example requires information both from the mesh and its refinement but is general.

In addition, among the discretization of with a strong (section 3.1) or weak (section 3.2) definition of convexity, not all are consistent. The definition of consistency is very similar to the one of partial differential equations and it is used above to discriminate likely discretizations and unlikely ones. But this does not guarantee good numerical results even when the discretization is consistent. We also discuss some structured meshes, the discretization of and the use of test functions for convexity (say convexity). we prove they may or maynot be consistent (Table 1).

We also test the gradients’ jumps of functions (strong discretization with test functions in subsection 4.1) and various weak discretizations for and for some test functions (subsections 4.2 and 4.3). Some of them are consistent and some are not.

We also discuss the literature, but let a deeper study of how [17, 18] interact with [1] to a forthcoming article. In a last subsection, we numerically illustrate the convergence of [18]’s FEM where the trial and test basis are different. Even if other methods exist, such as the recent methods using an evolution PDE converging to the convexified function [23, 24], this FEM is maybe one of the simplest. Comparisons of all these methods would be a thrilling challenge.

Acknowledgments

The author thanks G. Carlier for drawing his attention to the problem of subharmonicity approximation.

References

- [1] P. Choné and H.V.J. Le Meur (2001). Non-convergence result for conformal approximation of variational problems subject to a convexity constraint. Numer. Funct. Anal. Optim. 22 no. 5-6:529–547.

- [2] I. Newton (1686). Philosophiae Naturalis Principia Mathematica.

- [3] H.H. Goldstine (1980). A history of the calculus of variations from the 17th to the 19th century Springer-Verlag, Heidelberg.

- [4] G. Buttazzo, V. Ferone and B. Kawohl (1995). Minimum problems over sets of concave functions and related questions. Math. Nachr. 173:71-89.

- [5] T. Lachand-Robert and M.A. Peletier (2001). An Example of Non-convex Minimization and an Application to Newton’s Problem of the Body of Least Resistance, Ann. Inst. H. Poincaré Anal. Non Linéaire 18, no. 2:179–198.

- [6] P.L. Lions (1998). Identification du cône dual des fonctions convexes et applications. (French. English, French summary) [Identification of the dual cone of convex functions and applications] C. R. Acad. Sci. Paris Sér. I Math. 326 no. 12, 1385–1390.

- [7] T. Lachand-Robert and É. Oudet (2005). Minimizing within convex bodies using a convex hull method, SIAM Journal on Control and Optimization Vol. 16 Number 2:368-379.

- [8] G. Wachsmuth (2014). The numerical solution of Newton’s problem of least resistance, Math. Program. Ser. A 147: 331–350.

- [9] G. Carlier (2004). On a theorem of Alexandrov. J. Nonlinear Convex Anal. 5, no. 1:49–58.

- [10] G. Carlier, M. Comte and G. Peyré (2009). Approximation of maximal Cheeger sets by projection, M2AN Math. Model. Numer. Anal. 43(1):139-150.

- [11] J.-C. Rochet and P. Choné (1998). Ironing, sweeping and multidimensionnal screening, Econometrica 66:783-826.

- [12] G. Carlier and T. Lachand-Robert (2001). Regularity of solutions for some variational problems subject to a convexity constraint. Comm. Pure Appl. Math. 54 no. 5:583–594.

- [13] N.K. Leung and R.J. Renka (1999). convexity-preserving interpolation of scattered data. SIAM J. Sci. Comput. 20 , no. 5:1732–1752.

- [14] G. Carlier, T. Lachand-Robert and B. Maury (1999). -projection into the set of convex functions: a saddle-point formulation. CEMRACS 1999 (Orsay), 277–289 (electronic), ESAIM Proc., 10, Soc. Math. Appl. Indust., Paris.

- [15] B. Maury (2003). Version continue de l’algorithme d’Uzawa. (French) [Continuous version of the Uzawa algorithm] C. R. Math. Acad. Sci. Paris 337 , no. 1:31–36.

- [16] G. Carlier, T. Lachand-Robert and B. Maury (2001). A numerical approach to variational problems subject to convexity constraint, Numer. Math. 88, no. 2:299–318.

- [17] N.E. Aguilera and P. Morin (2008). Approximating optimization problems over convex functions, Numer. Math. 111(1):1-34

- [18] N.E. Aguilera and P. Morin (2009). On convex functions and the finite element method, SIAM J. Numer. Anal. 47(4):3139-3157

- [19] I. Ekeland and S. Moreno-Bromberg (2010). An algorithm for computing solutions of variational problems with global convexity constraints, Numer. Math. 115(1):45-69.

- [20] G. Wachsmuth (2017). Conforming Approximation of Convex Functions with the Finite Element Method, submited.

- [21] Q. Mérigot and É. Oudet (2014). Handling convexity-like constraints in variational problems, SIAM J. Numer. Anal., 52 (5):2466–2487.

- [22] J.M. Mirebeau (2015). Adaptive, Anisotropic and Hierarchical cones of Discrete Convex functions, Numer. Math. pp. 1–47.

- [23] A. Oberman (2008). Computing the convex envelope using a nonlinear partial differential equation, Mathematical Models and Methods in Applied Sciences (M3AS), Vol. 18. No 5 759–780.

- [24] G. Carlier and A. Galichon (2012). Exponential convergence for a convexifying equation, ESAIM COCV, 18, no. 3, 611–620.

- [25] B. Kawohl and C. Schwab (1998). Convergent finite elements for a class of nonconvex variationnal problems, IMA Journal of Numerical Analysis 18:133-149.