Stationarity against integration in the autoregressive process with polynomial trend

Abstract.

We tackle the stationarity issue of an autoregressive path with a polynomial trend, and we generalize some aspects of the LMC test, the testing procedure of Leybourne and McCabe. First, we show that it is possible to get the asymptotic distribution of the test statistic under the null hypothesis of trend-stationarity as well as under the alternative of nonstationarity, for any polynomial trend of order . Then, we explain the reason why the LMC test, and by extension the KPSS test, does not reject the null hypothesis of trend-stationarity, mistakenly, when the random walk is generated by a unit root located at . We also observe it on simulated data and we correct the procedure. Finally, we describe some useful stochastic processes that appear in our limiting distributions.

Key words and phrases:

LMC test, KPSS test, Unit root, Stationarity testing procedure, Polynomial trend, Stochastic nonstationarity, Random walk, Integrated process, ARIMA process, Donsker’s invariance principle, Continuous mapping theorem.Notations. In all the paper, we define as the lag operator with the convention that . In addition, is the renormalization of any , and designates the indicator function. We will always consider that and that denotes the integer part of . To lighten the notations, we will usually refer to the corresponding vector by removing the implicit subscript on the variable. For example, where is the transpose of .

1. A consistent test for a unit root

We consider the autoregressive process of order on with a polynomial trend of order , driven by a random walk and an additive error. For an observed path of size , we investigate the model given, for all , by

| (1.1) |

where, for all , is an autoregressive polynomial having all its zeroes outside the unit circle, where, for any ,

| (1.2) |

is a random walk starting from , and where and are uncorrelated white noises of variance and , respectively. From now on, white noises are to be interpreted in the strong sense, that is as sequences of independent and identically distributed random variables. For the sake of simplicity, we consider that . We also normalize the known part of the trend, by selecting , to simplify the treatment of the projections, as we will see in the technical proofs. The order of the polynomial trend is , but we will also take account of the case where no trend is introduced in (1.1). We switch from one situation to another by selecting or . Our objective is to establish a testing procedure for

One can observe that (1.1) is a trend-stationary process under the null , since the process is almost surely zero, and an integrated process of order 1 under the alternative . Hence, evaluating against is equivalent to testing stationarity against integration in the stochastic part of the process. In this context, our work is a generalization of the procedure of [Leybourne and McCabe, 1994], shortened LMC test in all the sequel. In their original paper, they propose to make use of the maximum likelihood estimator of on a given path of size and to estimate the trend parameters using a least squares methodology on the residual process. Then, they build a test statistic and establish its behavior under the null hypothesis of stationarity for specific trends (none, constant or linear). Under , they show that the test statistic diverges with rate , and that it is possible to get its correctly renormalized asymptotic distribution. In the simple case where , [Nabeya and Tanaka, 1988] had already investigated the founding principles of this strategy. This restriction seems nevertheless far from the reality of time series since all correlation phenomenon has disappeared. Earlier, [Nyblom and Makelainen, 1983], [Nyblom, 1986] and [Leybourne and McCabe, 1989] had already taken an interest in such test statistics, for closely related models. The procedure of [Kwiatkowski et al., 1992], shortened from now on KPSS test, translates any correlation in the residual process, to avoid any preliminary estimation of and . Their test statistic (described later in Remark 1.2) is shown to reach the same asymptotic distribution but, as a long-run variance has to be estimated instead, there is a truncation at a lag such that to ensure consistency, and the divergence under occurs with rate . One can accordingly expect that the LMC procedure will be more powerful to discriminate , and such observations are made in [Leybourne and McCabe, 1994]. However, the true value of is needed and all flexibility is sacrificed, contrasting with the KPSS procedure. The stationarity of time series being a contemporary issue, it is not surprising to find an abundant literature on empirical studies, anomalies detection or improvements brought to these strategies: let us mention [Saikkonen and Luukkonen, 1993], [Leybourne and McCabe, 1999], [Newbold et al., 2001], or [Müller, 2005], [Harris et al., 2007], [De Jong et al., 2007], [Pelagatti and Sen, 2009] and all associated references, without completeness. First we will show that in the context of the LMC test, it is possible to get the asymptotic distribution of the test statistic under as well as under , for any polynomial trend of order . Then, we will explain, and we will observe it on some straightforward simulated data, the reason why the LMC test – and by extension the KPSS test – does not reject the null hypothesis of trend-stationarity, mistakenly, when the random walk is generated by a unit root located at . We have widely been inspired by the calculation methods of [Phillips, 1987], [Kwiatkowski et al., 1992] and [Leybourne and McCabe, 1994], themselves relying on the Donsker’s invariance principle and the Mann-Wald’s theorem, that we will also recall. Finally, we will describe some useful stochastic processes that appear in our limiting distributions, and we will prove our results.

The case corresponds to a trend-stationary process both under and under , it is consequently not of interest as part of this paper. Combining (1.1) and (1.2), the model under is

| (1.3) |

where the source of the stochastic nonstationarity of is

| (1.4) |

which is the partial sum process of when . First,

where are easily identifiable (e.g. when ) and the process is second-order equivalent in moments to an MA residual, as it is explained in [Kwiatkowski et al., 1992]. We obtain the integrated model given, for all , by

| (1.5) |

where is a white noise of variance depending on the so-called signal-to-noise ratio . For the generating process (1.5), we build a consistent estimator of (see Remark 1.1 below), and we consider the residual process

| (1.6) |

Note that under , , implying that the differentiated process is causal and invertible. On the other hand, under and the process is not invertible.

Remark 1.1.

The consistency of is a crucial issue of the study. Let be the operator defined as

It follows that

where is easily identifiable ( when or ) and is a moving average polynomial of order . Now, let

Clearly, implying that is a causal ARMA process having a potentially nonzero intercept. Under , has unit roots and its last zero is outside the unit circle (since ). Under , has unit roots. In both situations, Theorem 2.1 of [Pötscher, 1991] ensures that a pseudo-MLE is consistent for treating as a Gaussian noise, whereas is easily estimated as intercept of a stationary ARMA process. Nevertheless, only the AR part of the process is of interest for us, and a faster method is worth considering. The causality of implies that there exists a causal representation

such that, according to Chapter 7 of [Brockwell and Davis, 1996], the sample autocovariance function of is a consistent estimator of its autocovariance function . Using a Yule-Walker approach, for all ,

Hence, a consistent estimator of may be obtained via . The selection of will be widely discussed in Section 3.

As a result of the previous remark, it makes sense to estimate under using a least squares methodology in the model given by

| (1.7) |

where is the residual process coming from the estimation of . A second-order residual set is then built via

| (1.8) |

where is the least squares estimator of in the model (1.7). Let the partial sum processes of and be defined as

| (1.9) |

Finally, consider the test statistic

| (1.10) |

Remark 1.2.

The test statistic of the KPSS procedure is very close to . The main difference is that satisfies some weaker assumptions including correlation (see [Kwiatkowski et al., 1992]), leading to and no parameter to estimate. In return, a long-run variance defined as

has to be estimated using a truncation method. The test statistic is

and corresponds to (1.10) when , that is when the long-run variance is estimated as a white noise variance.

We now establish the asymptotic behavior of under . The stochastic processes appearing in our limiting distributions are described in the next section.

Theorem 1.1.

Assume that . Then, for , we have the weak convergence

where is the generalized Brownian bridge of order . In addition, for , we have the weak convergence

where is the standard Wiener process.

In the following theorem, we show that diverges under for with rate and we study the asymptotic behavior of the test statistic correctly renormalized. We also show that it decreases to zero under for .

Theorem 1.2.

Assume that . Then, for and , we have the weak convergence

where is the integrated Brownian bridge of order and is the detrended Wiener process of order . In addition, for , we have the weak convergence

where is the integrated Wiener process of order 1 and is the standard Wiener process. Finally, for ,

The situation where is the cause of a number of complications as we will see in the associated proofs, that is the reason why we limit ourselves to stipulate the convergence of to zero in the general case. However, in the particular case where , we reach the following result.

Proposition 1.1.

Assume that . Then, for and , we have the weak convergence

where and are independent standard Wiener processes.

One can notice that this is the only situation in which and simultaneously play a role in the asymptotic behavior, this explains why we had to make such a decomposition into and . As a matter of fact, under , is the only perturbating process whereas under with , is dominated by . We are pretty convinced, on the basis of a simulation study, that it is possible to find an identifiable limiting distribution for when and . However, we have not reached the explicit expression in this work because of complications due to the phenomenon of compensation in the invariance principles, and calculations very hard to conduct. This could form an objective for a future study.

Remark 1.3.

It is also possible to extend the whole results to the multi-integrated processes under the alternative, such as ARI processes having more than one unit root. In model (1.1), the random walk is now itself generated by a random walk, and so on up to positive unit roots. Then, weak convergences in Theorem 1.2 become

respectively for and . For negative unit roots, we still reach the convergence

Such results may be useful to produce a statistical testing procedure concerning the integration order of the generating process of an observed path and/or to check the true value of .

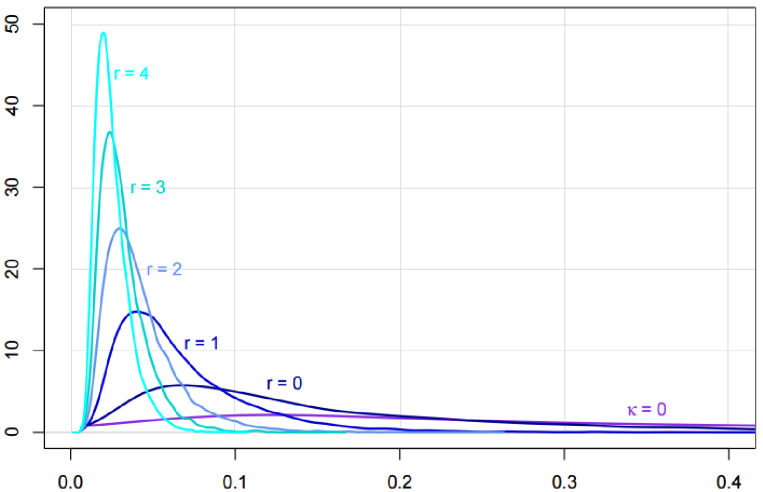

On Figure 1, we have represented the asymptotic distribution of under for , then for and , using Monte-Carlo experiments.

2. Some useful stochastic processes

Throughout the study, we deal with some stochastic processes, built from the standard Wiener process that we are now going to introduce. In all definitions, we consider that .

Definition 2.1 (Integrated Wiener Process).

The process given, for , by

is called a “integrated Wiener process of order ” in the whole paper. By convention, .

For example,

Definition 2.2 (Generalized Brownian Bridge).

The process given, for , by

where is an application from into given by formula (8) in [MacNeill, 1978], is called a “generalized Brownian bridge of order ” in the whole paper.

Definition 2.3 (Integrated Brownian Bridge).

The process given, for , by

is called a “integrated Brownian bridge of order ” in the whole paper. By convention, .

Definition 2.4 (Detrended Wiener Process).

The process given, for , by

is called a “detrended Wiener process of order ” in the whole paper. It is explicitly defined as

where the nonsingular matrix satisfies for all , , and where

| (2.1) |

Let us illustrate these definitions on the standard cases and . According to Definition 2.2 and formula (8) in [MacNeill, 1978], for ,

which is the usual “Brownian bridge”. It follows from Definitions 2.3 and 2.4 that

and that

which is the usual “demeaned Wiener process”. Similarly, for ,

is the “second-level Brownian bridge”, leading to

Finally,

is the standard “detrended Wiener process”.

3. A corrected test adapted to the negative unit root

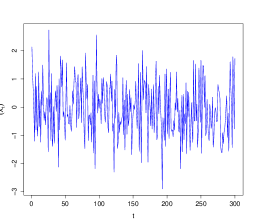

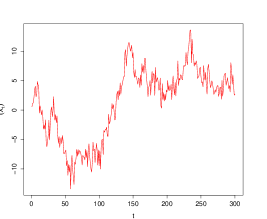

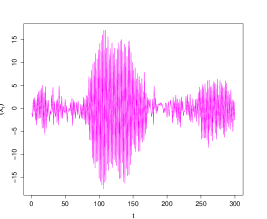

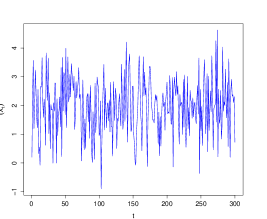

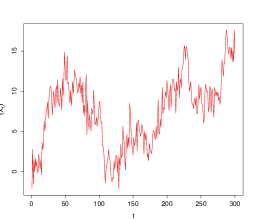

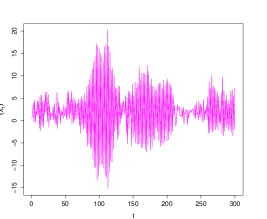

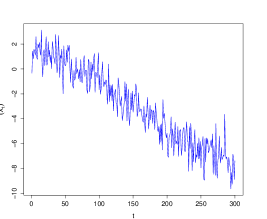

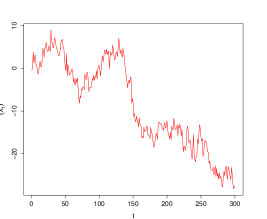

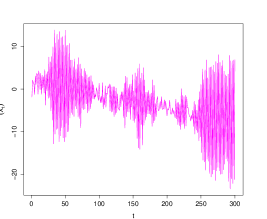

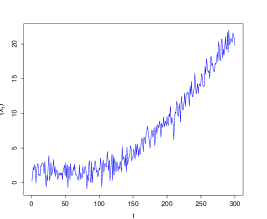

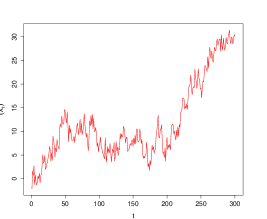

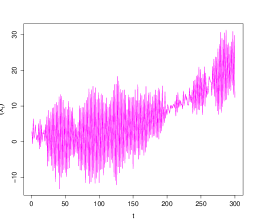

The empirical power of the KPSS and LMC procedures has been widely studied in the literature (see Section 1 for references). For , the improvements that we described in this paper (for any and ) are mainly theoretical. On the other hand, we thought useful to conduct an empirical study for , because in this case it is not only a matter of generalization but also a matter of correction of the existing procedures. To motivate the study, we have represented on Figures 2–5 below some examples of simulations according to (1.3) under , under and under , using the configurations indicated in the captions. Clearly, a visual investigation is required to decide whether or is the most likely alternative, which is a crucial point to stationarize the process. In the whole experiments, the quantiles of the limit distribution of the test statistic under the null, depending on and , have been taken from Table 2 of [MacNeill, 1978].

The first observation is that, due to the alternation generated by , it seems quite intuitive to choose between and to conduct the test. Besides, it is perceptible on the simulations that heteroscedasticity is manifest. Such high-frequency signals (under ) are quite unusual in the econometric field, and yet it remains a nonstationary eventuality that a consistent test needs to handle. In the particular case where , and where and are standard Gaussian white noises, we have conducted simulations, each time testing for stationarity using the KPSS and the LMC procedures. We have obtained the following results (Table 1). On the one hand, we observe that the size of each test is appropriate, since the procedures have been conducted with a significance level . One also observes that each test is consistent under but, as one can notice on Table 1 they are mislead under and do not detect this kind of nonstationarity.

| KPSS | LMC | |

|---|---|---|

| Under | 0.051 | 0.051 |

| Under | 0.989 | 0.998 |

| Under | 0.043 | 0.010 |

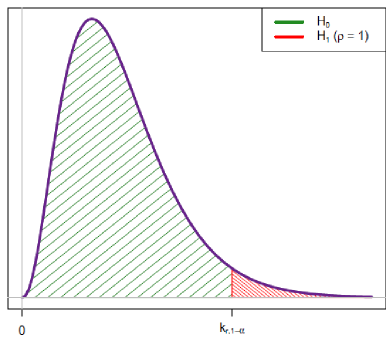

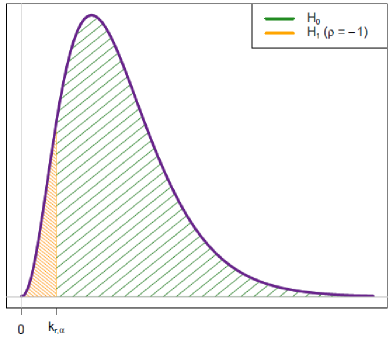

This phenomenon is a direct consequence of Theorem 1.2, in which we have proved that converges to zero when the unit root of the integrated process is located at . To correct this misuse, we suggest to modify the rejecting rules of the usual procedures depending on whether the alternative is or . Let be the –quantile of the limiting distribution of Theorem 1.1 for a given , with the convention that if . Then the corrected test takes the following form,

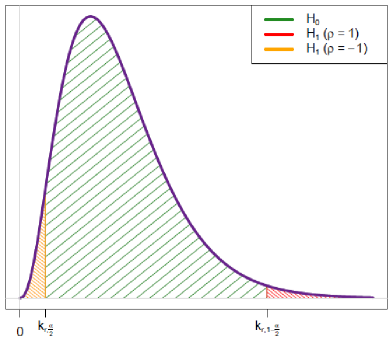

Defined as above, the corrected test is exactly the LMC test for and , the generalization lies in and the correction lies in the whole situations under . In the particular case where , it is even possible to build a two-sided test for stationarity,

which is adapted to test for against . Figure 6 gives an overview of the corresponding rejection areas. However, it is crucial to note that for , it may be problematic to get a consistent estimation of since we cannot stationarize the process without any information on . The two-sided procedure is therefore useful only for , i.e. in the KPSS framework.

The application of the two-sided corrected test to the dataset used to fill Table 1 leads to 97.6 % of rejection of . With no doubt, this is a confirmation that is now correctly treated. The main corollary of the study is that our results should be rigorously driven to the KPSS procedure. Indeed, on the one hand, it is known that the LMC test suffers from size distortion for a stationary but strongly serially correlated process, as pointed out in [Caner and Kilian, 2001] or [Lanne and Saikkonen, 2003] among others, not forgetting that is always difficult to properly evaluate in an ARMA process. On the other hand, the corrected two-sided test could be conducted without choosing beforehand between and as the alternative. Such a test would be fully consistent for testing stationarity of ARMA processes, this is a trail for a future study.

4. Proof of the main results

We are now going to prove our main results. We will consider in all the sequel the design matrix of order defined as

| (4.1) |

The Donsker’s invariance principle and the Mann-Wald’s continuity theorem being the cornerstone of all our reasonings, we found useful to remind them in this section.

Theorem 4.1 (Donsker).

Assume that is a sequence of independent and identically distributed random variables having mean 0 and finite variance . Let and . For a given , let also

Then, as goes to infinity, we have the weak convergence

where is the standard Wiener process.

Theorem 4.2 (Mann-Wald).

Assume that is a sequence of random elements defined on a metric space . Assume that the application , where is also a metric space, has a set of discontinuity points such that . Then, as goes to infinity,

The implication holds for the convergence in distribution, the convergence in probability and the almost sure convergence.

Proof.

The Donsker’s invariance principle is described and proved in Section 8 of [Billingsley, 1999]. The Mann-Wald’s continuity theorem, usually called continuous mapping theorem, is for example introduced in Theorem 2.7 of [Billingsley, 1999] and proved thereafter. ∎

In addition, we need to introduce an invariance principle for the residuals of the regression of a random sequence on a polynomial trend in the case where the disturbance has an integrated component. This is an extension of Theorem 1(d) of [Stock, 1999]. For but with a more general kind of perturbation, one can also find the foundations of this strategy in [Ibragimov and Phillips, 2008].

Lemma 4.1.

Consider, for all , the model

with and . Let be the least squares estimator of and the estimated residual set. Then, we have the weak convergence

where where is the detrended Wiener process of order .

Proof.

Recall that is a random walk of order generated by a white noise sequence of variance , that we can define as

| (4.2) |

where we consider to lighten the calculations that . The least squares estimator of is given by

| (4.3) |

where is the th column of given by (4.1). It follows that

| (4.4) |

in which we define the residual . We start by establishing an invariance principle for . First, Theorem 4.1 is sufficient to get

| (4.5) |

By extension,

| (4.6) |

from Theorem 4.2. Iterating the process, we obtain, for ,

| (4.7) |

Since a.s. from the strong law of large numbers, it follows that also satisfies the invariance principle given by (4.7), for all . For , one can identify the limiting distribution in (4.7) and to and in Assumption 1(a) of [Stock, 1999]. In addition, the th line of given in (4.4) is

| (4.8) |

We are now going to study the rate of convergence of . For all , denote . We can use (4.7) to get

| (4.9) |

By combining (4.8) and (4.9), we find that, for all ,

| (4.10) |

where the limiting distribution is given in (2.1). Moreover, by a direct calculation,

| (4.11) |

where is given in (4.3) and the nonsingular matrix satisfies for all . It follows from (4.4), (4.10) and (4.11) that

| (4.12) |

It only remains to notice that

| (4.13) |

and to combine (4.7) and (4.12) to conclude that, for ,

from Theorem 4.2, where is the limiting value of . For , the latter convergence is given in Theorem 1(d) of [Stock, 1999]. This achieves the proof of Lemma 4.1. ∎

Proof of Theorem 1.1. Denote by the projection matrix and by the identity matrix of order . We start by expressing in terms of to establish an invariance principle such as Theorem 4.1 on given by (1.9). We first consider the general case where . From (1.6) and (1.8), since is the least squares estimator of , a direct calculation shows that, for all ,

| (4.14) |

where is the th component of , and, for , is the th component of with . From Theorem 1 of [MacNeill, 1978], we have the weak convergence

| (4.15) |

In addition, for any and since is causal, equation (1.1) leads to

| (4.16) |

where and . The coefficients of the deterministic trend are identifiable via a tedious but straightforward calculation. It follows from (4.16) that is a stable stationary AR process which also satisfies an invariance principle, as it is stipulated for example in Theorem 1 of [Dedecker and Rio, 2000]. If we define the so-called long-run variance as

which is finite for a stable AR process (see Chapter 3 of [Brockwell and Davis, 1996]), then, for all ,

| (4.17) |

by using again Theorem 1 of [Dedecker and Rio, 2000]. Convergence (4.17) and the consistency of imply that

| (4.18) |

Noticing that in (1.9) is the partial sum process of , it follows that

| (4.19) |

In addition, it is not hard to see that

since can be seen as the residual of the regression of on a polynomial time trend with zero coefficients. The same kind of convergence can be reached for following a similar methodology as in [Phillips and Perron, 1988], since can be seen as the residual of the regression of a weakly stationary process on a polynomial time trend also with zero coefficients. Hence, by the Cauchy-Schwarz’s inequality,

| (4.20) |

where the process is given by (1.9). Finally,

by application of Theorem 4.2. This achieves the proof of Theorem 1.1, using (4.19), (4.20), Slutsky’s lemma and taking , in the case where there is a polynomial trend. On the other hand, for , is the zero matrix and we merely have and in (4.14), for all and . Then, convergence (4.20) follows from the strong law of large numbers and, by Theorem 4.1, the invariance principle (4.19) becomes

| (4.21) |

The end of the proof follows the same reasoning as above.

Proof of Theorem 1.2. We now suppose that , implying that the process has a stochastic nonstationarity generated by the random walk given by (1.4). We first consider the general case . In the same way as for (4.14), we obtain

| (4.22) |

where is the th component of . In addition, for all , is the th component of and is given, for all , by

| (4.23) |

and , with the notations of (4.16). Hence, is second-order equivalent in moments to a stationary ARMA process. From Theorem 1 of [Dedecker and Rio, 2000], it satisfies an invariance principle in which its long-run variance is involved, and the rate is . Then, by Theorem 4.2 and standard calculations, one can see that behaves like since all invariance principles on can also be established on . However as is consistent, it appears that all asymptotic results will only be driven by , and their partial sum processes. First, by Theorem 4.1 in the case where , we have already seen in (4.5) that we have the invariance principle

| (4.24) |

For , one cannot directly apply Theorem 4.1 since is not built from identically distributed random variables. However, convergence (4.24) still holds by using for example Theorem 1 of [Dedecker and Rio, 2000]. Depending on the value of , the end of the proof is totally different. On the one hand, for , from Lemma 4.1 with , we have the weak convergence

| (4.25) |

It follows that

| (4.26) |

by application of Theorem 4.2. Since the leading term of is as it is explained above and using convergence (4.25), we get an invariance principle for the partial sum process in (1.9), given by

| (4.27) |

We can also reach the same convergence by using Theorem 1 of [MacNeill, 1978] combined with convergence (4.6), that is

| (4.28) |

Of course, (4.20) cannot hold under and the asymptotic behavior of will now stem from (4.25). Indeed,

implying that

| (4.29) |

In addition, from (4.27),

The latter convergence together with (4.29) and Theorem 4.2 achieve the first part of the proof, by selecting . On the other hand, for , the summation (4.28) is different due to the phenomenon of compensation. As a matter of fact, it is not hard to see that, for any even and odd integer , respectively, we have

Let be the sequence defined, for an even and all , by

and, for an odd and all , by

Hence, , and all covariances are zero, since and are not correlated. It follows that is a white noise and that it satisfies, by virtue of Theorem 1 of [Dedecker and Rio, 2000], the invariance principle

| (4.30) |

Thus, we obtain the invariance principles

and, by application of Theorem 1 of [MacNeill, 1978],

| (4.31) |

Exploiting the latter convergence and the domination of in (the estimator of remaining consistent), it follows that

| (4.32) |

Let us now restart the reasoning developed in Lemma 4.1, but for and . We recall that, using the notations associated with (4.8), for all ,

First, it is not hard to see that

is a martingale adapted to the natural filtration of , whose increasing process is such that a.s. with obviously

The law of large numbers for scalar martingales (see e.g. [Duflo, 1997]) implies that a.s. Hence,

| (4.33) |

In addition, denote by the partial sum process associated with for . Let also and be the partial sum processes associated with , for the even and odd subscripts, respectively. Explicitly,

and

with and . A direct calculation shows that, for and all ,

| (4.34) |

where we have for all odd and for all even . It is possible, via Theorem 4.1, to establish an invariance principle on the processes and . As a matter of fact,

| (4.35) |

It follows, from Theorem 4.2, that

| (4.36) |

and that

| (4.37) |

since it is not hard to see that and behave like . Moreover, the convergences (4.35) and the definition of directly lead to

| (4.38) |

In addition, the invariance principle (4.9) for and , here corresponding to the one associated with , gives, together with (4.34), (4), (4) and (4.38),

and thus, with the notations above, for all ,

successively using (4.4) and (4.13). By virtue of Theorems 4.1–4.2 and the strong law of large numbers, we deduce, following the same calculations, that the process grows with rate , which achieves the proof for since (4.32) shows that the numerator of also grows with the same rate. Finally, for , the invariance principle (4.25) merely becomes

| (4.39) |

from Theorem 4.1, and the end of the reasoning easily follows as above.

Proof of Proposition 1.1. This proof will be very succinct since all results have been established in the previous reasonings. Indeed, for and , convergence (4.32) becomes

if we split the limiting distribution into two independent components, so as to easily deal with in the sequel. Without any trend fitted, we also have , for all . It follows that, similarly,

We achieve the proof by choosing and by applying Theorem 4.2.

Acknowledgements. The author thanks the anonymous Reviewer for his suggestions and constructive comments which helped to improve substantially the paper.

References

- [Billingsley, 1999] Billingsley, P. (1999). Convergence of probability measures. Wiley Series in Probability and Statistics: Probability and Statistics. John Wiley & Sons Inc., New York, second edition.

- [Brockwell and Davis, 1996] Brockwell, P. J. and Davis, R. A. (1996). Introduction to Time Series and Forecasting. Springer-Verlag, New-York.

- [Caner and Kilian, 2001] Caner, M. and Kilian, L. (2001). Size distortions of tests of the null hypothesis of stationarity: Evidence and implications for the PPP debate. J. Int. Money. Financ., 20:639–657.

- [De Jong et al., 2007] De Jong, R. M., Amsler, C., and Schmidt, P. (2007). A robust version of the KPSS test, based on indicators. J. Econometrics., 137-2:311–333.

- [Dedecker and Rio, 2000] Dedecker, J. and Rio, E. (2000). On the functional central limit theorem for stationary processes. Ann. Inst. Henri Poincar , B., 36-1:1–34.

- [Duflo, 1997] Duflo, M. (1997). Random iterative models, volume 34 of Applications of Mathematics, New York. Springer-Verlag, Berlin.

- [Harris et al., 2007] Harris, D., Leybourne, S. J., and McCabe, B. P. M. (2007). Modified KPSS tests for near integration. Economet. Theor., 23-2:355–363.

- [Ibragimov and Phillips, 2008] Ibragimov, R. and Phillips, P. C. B. (2008). Regression asymptotics using martingale convergence methods. Economet. Theor., 24-4:888–947.

- [Kwiatkowski et al., 1992] Kwiatkowski, D., Phillips, P. C. B., Schmidt, P., and Shin, Y. (1992). Testing the null hypothesis of stationarity against the alternative of a unit root : How sure are we that economic time series have a unit root? J. Econometrics., 54:159–178.

- [Lanne and Saikkonen, 2003] Lanne, M. and Saikkonen, P. (2003). Reducing size distortions of parametric stationarity tests. J. Time Ser. Anal., 24:423–439.

- [Leybourne and McCabe, 1989] Leybourne, S. J. and McCabe, B. P. M. (1989). On the distribution of some test statistics for parameter constancy. Biometrika., 76:167–177.

- [Leybourne and McCabe, 1994] Leybourne, S. J. and McCabe, B. P. M. (1994). A consistent test for a unit root. J. Bus. Econ. Stat., 12-2:157–166.

- [Leybourne and McCabe, 1999] Leybourne, S. J. and McCabe, B. P. M. (1999). Modified stationarity tests with data-dependent model-selection rules. J. Bus. Econ. Stat., 17-2:264–270.

- [MacNeill, 1978] MacNeill, I. B. (1978). Properties of sequences of partial sums of polynomial regression residuals with applications to tests for change of regression at unknown times. Ann. Statis., 6-2:422–433.

- [Müller, 2005] Müller, U. (2005). Size and power of tests of stationarity in highly autocorrelated time series. J. Econometrics., 128-2:195–213.

- [Nabeya and Tanaka, 1988] Nabeya, S. and Tanaka, K. (1988). Asymptotic theory of a test for the constancy of regression coefficients against the random walk alternative. Ann. Statist., 16-1:218–235.

- [Newbold et al., 2001] Newbold, P., Leybourne, S. J., and Wohar, M. E. (2001). Trend-stationarity, difference-stationarity, or neither: further diagnostic tests with an application to U.S. Real GNP, 1875-1993. J. Econ. Bus., 53-1:85–102.

- [Nyblom, 1986] Nyblom, J. (1986). Testing for deterministic linear trend in time series. J. Am. Stat. Assoc., 81:545–549.

- [Nyblom and Makelainen, 1983] Nyblom, J. and Makelainen, T. (1983). Comparisons of tests for the presence of random walk coefficients in a simple linear model. J. Am. Stat. Assoc., 78:856–864.

- [Pelagatti and Sen, 2009] Pelagatti, M. M. and Sen, P. K. (2009). A robust version of the KPSS test based on ranks. Working Papers from Università degli Studi di Milano-Bicocca, Dipartimento di Statistica., No 20090701.

- [Phillips, 1987] Phillips, P. C. B. (1987). Time series regression with a unit root. Econometrica., 55-2:277–301.

- [Phillips and Perron, 1988] Phillips, P. C. B. and Perron, P. (1988). Testing for a unit root in time series regression. Biometrika., 75-2:335–346.

- [Pötscher, 1991] Pötscher, B. M. (1991). Noninvertibility and pseudo-maximum likelihood estimation of misspecified ARMA models. Economet. Theor., 7:435–449.

- [Saikkonen and Luukkonen, 1993] Saikkonen, P. and Luukkonen, R. (1993). Testing for a moving average unit root in autoregressive integrated moving average models. J. Am. Stat. Assoc., 88:596–601.

- [Stock, 1999] Stock, J. (1999). A Class of Tests for Integration and Cointegration. Cointegration, Causality and Forecasting: A Festschrift for Clive W.J. Granger. R. Engle and H. White, Oxford University Press, Oxford.