Least Product Relative Error Estimation

Kani CHEN, Yuanyuan LIN, Zhanfeng WANG and Zhiliang YING

A least product relative error criterion is proposed for multiplicative regression models. It is invariant under scale transformation of the outcome and covariates. In addition, the objective function is smooth and convex, resulting in a simple and uniquely defined estimator of the regression parameter. It is shown that the estimator is asymptotically normal and that the simple plugging-in variance estimation is valid. Simulation results confirm that the proposed method performs well. An application to body fat calculation is presented to illustrate the new method.

Keywords: Linear hypothesis; Multiplicative regression model; Product form; Relative error, Scale invariance; Variance estimation.

1 Introduction

In regression analysis, the least squares (LS) and least absolute deviation (LAD) are the most commonly used criteria based on absolute errors (Stigler, 1981; Portnoy & Koenker, 1997). In some situations, however, criteria based on relative errors that are scale invariant and less sensitive to outliers are more desirable (Narula & Wellington, 1977; Makridakis et al., 1984; Khoshgoftaar et al., 1992; Ye, 2007; Park & Stefanski, 1998; Chen et al., 2010; Zhang & Wang, 2012). Consider the following multiplicative regression model

| (1.1) |

where is the response variable, is the -vector of explanatory variables with the first component being 1 (intercept), is the corresponding -vector of regression parameters with the first component being the intercept and is the error term, which is strictly positive. An additional constraint on needs to be imposed so that the first component of (intercept) becomes identifiable. Model (1.1) is also known as the accelerated failure time (AFT) model in the survival analysis literature.

For the multiplicative regression model (1.1), Chen et al. (2010) gives a convincing argument that a proper criterion should take into account both types of relative errors: one relative to the response and the other relative to the predictor of the response. A criterion with only one type of relative errors often leads to biased estimation. They introduce the least absolute relative error (LARE) estimation for model (1.1) by minimizing

| (1.2) |

the sum of the two types of the relative errors. The LARE estimation enjoys the robustness and scale-free property. However, like the LAD, the LARE criterion function is nonsmooth, and, as a result, the limiting variance of the corresponding estimator involves the density of the error. Furthermore, its computation is slightly more complicated than linear programming.

It would be desirable to develop a criterion function which not only incorporates the relative error terms, but also is smooth and convex. The latter would ensure the numerical uniqueness of the resulting estimator and the consistency of the usual plug-in sandwich-type variance estimation. The main purpose of this paper is to introduce a simple, smooth, convex and interpretable criterion function and to develop a related inference procedure.

The rest of the paper is organized as follows. Section 2 introduces the least product relative error (LPRE) criterion, along with simple inference procedures, including point and variance estimation, hypothesis testing and related large sample properties. Extension of the LPRE to a general class of relative error criteria is given in Section 3. Section 4 contains simulation results and a real example. Some discussion and concluding remarks are given in Section 5.

2 Least product relative error

The least absolute relative error (LARE) criterion (1.2) of Chen et al. (2010) is the result of adding together the two relative error terms. In this paper, we consider multiplying the two relative error terms and propose the following least product relative error (LPRE) criterion

| (2.1) |

Note that the summand can be written as . Thus, it may be viewed as a symmetrized version of the squared relative errors (Park and Stefanski, 1998).

A simple algebraic manipulation leads to the following alternative expression

| (2.2) |

from which we can see major advantages. First, the criterion function is infinitely differentiable. Second, it is strictly convex since the exponential function is strictly convex. As a result, finding the minimizer is equivalent to finding the root of its first derivative. The usual asymptotic properties can therefore be derived by a local quadratic expansion and standard inference methods for M-estimation are applicable.

2.1 Estimation

We now deal with parameter estimation and develop the corresponding theory. Our estimator for will be denoted by and defined as the minimizer of (2.1) or, equivalently, (2.2). The strict convexity of (2.2) entails that the minimizer, if it exists, must be unique. Assume the design matrix is nonsingular. This is a minimum condition for the purpose of identifiability. Then, is strictly convex, and, as , , implying . It follows that as . And the following theorem holds.

Theorem 1. If is nonsingular, then exists and is unique.

Remark 1. The nonsingularity of is also a necessary and sufficient condition for the least squares estimator to be unique.

We next establish asymptotic properties for under suitable regularity conditions. For notational simplicity, we assume that , , are independent and identically distributed. It allows for heteroskedasticity in that it does not require the error term to be independent of the explanatory variable . We will use the following conditions for the development of the asymptotic theory.

Condition C1. There exists such that .

Condition C1*. There exists such that .

Condition C2. The expected design matrix, , is positive definite.

Condition C3. The error terms satisfy .

Condition C1 is almost minimal for the criterion function (4) to have a finite expectation in a neighborhood of the true parameter . It also ensures that the limit of (4) is twice differentiable with respect to and that the differentiation and expectation is interchangeable. Condition C2 ensures that the design matrix is nonsingular, a minimal requirement for the regression parameter to be identifiable. Under C1 and C2, the limiting criterion function is strictly convex in a neighborhood of . Condition C3 is equivalent to that the derivative of the criterion function at has mean 0, again a minimal condition for the resulting estimator to be asymptotically unbiased. The strict convexity and the asymptotic unbiasedness ensure that the estimator is consistent. Condition C1* is simply a stronger version of C1 for the asymptotic normality to hold.

Theorem 2. Under Conditions C1, C2 and C3, is strongly consistent.

Proof. Under C1, C2 and C3, one can show that converges to in a small neighborhood of and that both are convex. Thus, by Rockafellar (1970, Theorem 10.8), , the minimizer of , converges to , the minimizer of .

The next theorem establishes the asymptotic normality and the validity of the plug-in variance estimation. Let and . Define their plug-in estimators and

Theorem 3. Under Conditions C1*, C2 and C3, is asymptotically normal with mean and covariance matrix , which is consistently estimated by .

Proof. Since is consistent, by the Taylor expansion,

where and lies in between the true parameter and the LPRE estimate . The desired results follow from the law of large numbers and the central limit theorem.

It can be shown that when the error has density

| (2.3) |

where is the normalizing constant, becomes the Fisher information. It then follows that is asymptotically efficient.

2.2 Hypothesis testing

We now turn to hypothesis testing. Although the asymptotic theory developed in the preceding subsection can be used to construct Wald-type testing statistics, we will focus on an approach that is based directly on the LPRE criterion. For simplicity, we assume homogeneous errors, i.e. is independent of and consider the following null hypothesis

| (2.4) |

where and , are -vectors that are linearly independent and lie in the linear space spanned by the column vectors of the design matrix .

Let

| (2.5) |

Through the usual quadratic expansion, we can arrive at an asymptotic ANOVA-type decomposition. The asymptotic normality can then be applied to show that, under the null hypothesis, converges in distribution to , where and is the central chi-squared distribution with degree of freedom. The constant can be estimated consistently by . Therefore we can use as the testing statistic with as the cut-off point, where is a given nominal significance level.

3 General relative error criteria

A general relative error (GRE) criterion can be constructed:

| (3.1) |

where is a bivariate function satisfying certain regularity conditions. Taking , it becomes the LARE criterion function (Chen et al., 2010) while , it becomes the LPRE of the preceding section. One may also consider (Ye, 2007). Note that all three criteria here are symmetric functions. A possible non-symmetric one could be , where we pay more attention to the relative error of and more heavily penalize large value of compared to .

The derivative of with respect to is defined as

Its expectation becomes 0 when

| (3.2) |

Let be a minimizer of the criterion function (3.1). It follows that, under (3.2), is asymptotically unbiased. In fact we have the following result concerning the limiting distribution of .

Theorem 4. Under (3.2) and additional regularity conditions concerning the nonsingularity of the design matrix and finite moment condition on the error, is asymptotically normal with mean and covariance matrix where , and constant satisfies, as ,

The proof of Theorem 4 is similar to that of Theorem 1 in Chen et al. (2010) and is omitted. In general, the asymptotic variance of , the minimizer of , may involve the density function of the error. To avoid density estimation, an approximation based on random weighting can be applied. If the error has a density function as follows:

| (3.3) |

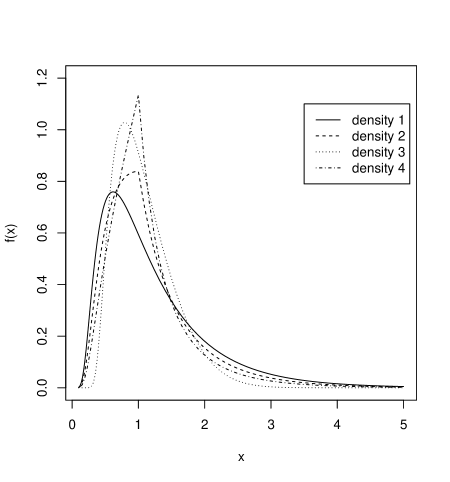

where is a normalizing constant, then the estimator is asymptotically efficient. Density in (3.3) belongs to a class of inverse transformation invariant density, meaning that if a random variable is distributed with density , then is equal in distribution to . Figure 1 shows densities of some particular choices of function . One can see that the error distribution with which the product criterion is efficient has heavier tails than others, indicating that the product criterion is more robust in practical application.

INSERT FIGURE 1 HERE

Based on general relative error criterion (3.1), a general test statistic to test hypothesis (2.4) can be constructed as

| (3.4) |

Especially, when the error terms follow the distribution described in (3.3), is identical to the log-likelihood ratio test statistic. The following theorem demonstrates the asymptotic distribution of .

Theorem 5. Under the hypothesis (2.4) and additional regularity conditions,

as , where refers to the chi-square distribution with degrees of freedom.

The proof of Theorem 5 is similar to that of Theorem 1 in Chen et al. (2008) and is also omitted. In general, the asymptotic distribution of may involve the density of the errors. The plug-in method involving density estimation can be inaccurate and computationally troublesome. In this case, a random weighting method, as used by Chen et al. (2008) and Wang et al. (2009), can be applied.

4 Numerical studies

4.1 Simulation studies

Simulation studies are conducted to compare the finite sample performance of the proposed LPRE, the LARE, the LS and the LAD. The data are generated from the model

| (4.1) |

where and are two independent covariates following the standard normal distribution and . We consider five error distributions: the distribution with which the LARE estimator is efficient; the distribution with which the LPRE estimator is efficient; the exponential of the uniform distribution on ; the log-standard normal distribution; and the uniform distribution on with chosen such that . Note that the first four error distributions are such that is distributed same as . The sample size is . The variance estimation for the LARE and the LAD is based on random weighting with resampling size , while the variance estimation for the LPRE and the LS is based on the plug-in rule. The LS and LAD estimates are obtained by minimizing and , respectively. The simulation results are based on 1000 replications.

INSERT TABLES 1, 2, 3 HERE

It is seen from Table 1 that the LPRE performs considerably better than the LARE, the LS and the LAD when is uniformly distributed on . With log-normal error distribution, the LPRE performs as well as the LARE and is comparable to the LS. With the uniform error distribution, the LPRE performs slightly better than the LS, and much better than the LARE and the LAD. The variance estimation of the LPRE gives accurate coverage probability in the study.

The performance of the proposed test statistic is evaluated with the product relative error criterion. We consider two null hypotheses and . Tables 2 and 3 present the empirical significance levels and powers with when follows the distributions with which the LPRE and the LARE are respectively efficient, the log-uniform distribution on and the log-standard normal distribution. It is seen that the empirical significance levels are close to the nominal levels, suggesting that is adequate. Under and nominal level 0.05, the power increases from 0.05 to 1.0 as varies from 0.0 to 0.4. In other words, the power increases as the parameters move away from the null hypothesis, a common phenomenon in hypothesis testing.

4.2 Application

We apply the proposed method to analysis of the body fat data. The data contain various body measurement indices related with percentage of body fat for 252 men, which are available at http://lib.stat.cmu.edu/datasets/ bodyfat; see Penrose et al. (1985). We select 12 explanatory variables: age (), height4/weight2 () and 10 other body circumference indexes (neck, chest, abdomen, hip, thigh, knee, ankle, biceps, forearm and wrist, denoted by , ). We note that is a transform of the well-known body mass index (BMI) defined as the ratio of weight to height2. The sample size is 251. The response variable is the percentage of body fat. We delete one observation with and fit the model

| (4.2) |

where , denote the normalized explanatory variables.

To evaluate the performance of different methods, the dataset is partitioned into two parts. The first part with 200 observations is used to fit model (4.2), and the rest 51 observations are used to evaluate the prediction power. The results are shown in Tables 4 and 5.

INSERT TABLES 4 and 5 HERE

The -value is calculated by , where is the estimate of , is the estimated standard deviation for , and is the cumulative distribution function for the standard normal distribution. The variance estimation of the LPRE and the LS are obtained by the plug-in rule, while that for LARE and LAD are obtained by random weighting resampling. Table 4 shows that the four methods identify some common variables (with -value 0.05), such as age, 1/BMI and abdomen circumference. It makes sense that the percentage of body fat increases as age, BMI and abdomen circumference become large. However, the biceps circumference is identified only by the LPRE, indicating the percentage of body fat increases as the biceps circumference becomes larger.

The prediction accuracy based on the four methods estimation is measured by four different median indices: median of absolute prediction errors (MPE), median of product relative prediction errors (MPPE), median of additive relative prediction errors (MAPE) and median of squared prediction errors (MSPE), where , . Table 5 shows that the LPRE has the smallest MPE, MPPE, MAPE and MSPE among the LPRE, the LARE, the LS and the LAD.

5 Concluding remarks

In our view, in the realm of criteria based on relative errors, the LPRE proposed in this paper has the best potential to be the basic and primary choice, just like the least squares in the realm of criteria based on absolution errors. The proposed LPRE represents a substantial improvement over that of Chen et al. (2010) both theoretically and computationally, particularly in terms of the simplicity of inference. Extensions can be made to cover analysis of censored data and high dimensional data. Moveover, we present a more general GRE method and tests of linear hypotheses based on relative errors, which is not studied in Chen et al. (2010) and other relevant literature. The LPRE criterion may have broad applications in financial and survival data analysis.

References

-

Chen, K., Guo, S., Lin, Y., and Ying, Z. (2010). Least absolute relative error estimation. J. Am. Statist. Assoc. 105, 1104–1112.

-

Chen, K., Ying, Z., Zhang, H., and Zhao, L. (2008). Analysis of least absolute deviation. Biometrika 95, 107–122.

-

Gauss, C. F. (1809). Theoria Motus Corporum Coelestium. Perthes, Hamburg. Translation reprinted as Theory of the Motions of the Heavenly Bodies Moving about the Sun in Conic Sections. Dover, New York, 1963.

-

Khoshgoftaar, T. M., Bhattacharyya, B. B., and Richardson, G. D. (1992). Predicting software errors, during development, using nonlinear regression models: a comparative study. IEEE Transactions on Reliability 41, 390–395.

-

Knight, K. (1998). Limiting distribution for regression estimators under general conditions. Ann. Statist. 26, 755–770.

-

Makridakis, S., Andersen, A., Carbone, R., Fildes, R., Hibon, M., Lewandowski, R., Newton, J., Parzen, E., and Winkler, R. (1984). The Forecasting Accuracy of Major Time Series Methods. New York: Wiley.

-

Narula, S. C., and Wellington, J. F. (1977). Prediction, linear regression and the minimum sum of relative errors. Technometrics 19, 185–190.

-

Park, H., and Stefanski, L. A. (1998). Relative-error prediction. Statist.Prob. Letters 40, 227–236.

-

Penrose, K. W., Nelson, A. G. and Fisher, A. G. (1985). Generalized body composition prediction equation for men using simple measurement techniques (abstract). Medicine and Science in Sports and Exercise 17, 189–189.

-

Pollard, D. (1991). Asymptotics for least absolute deviations regression estimators. Econometric Theory 7, 186–199.

-

Portnoy, S., and Koenker, R. (1997). The Gaussian hare and the Laplacian tortoise: computability of squared-error versus absolute-error estimators (with discussion). Statist. Sci. 12, 279–300.

-

Rockafellar, R. T. (1970). Convex analysis. Princeton University Press, Princeton, N.J.

-

Scheff, H. (1959). The analysis of variance. New York: John Wiley.

-

Stigler, S. M. (1981). Gauss and the invention of least squares. Ann. Statist. 9, 465–474.

-

Wang, Z., Wu, Y. and Zhao, L. (2009). Approximation by randomly weighting method for linear hypothesis testing in censored regression model. Sci. in China Series A: Mathematics 52, 561–576.

-

Ye, J. (2007). Price models and the value relevance of accounting information. Technical report.

-

Zhang, Q. and Wang, Q. (2012). Local least absolute relative error estimating approach for partially linear multiplicative model. Statist. Sinica Preprint.

| density1: | ||||

| density2: | ||||

| density3: | ||||

| density4: |

Table 1. Comparison among various approaches with

| (-2,2) | ||||||

| LPRE | BIAS | 0.007 0.004 0.009 | 0.001 0.001 0.004 | 0.002 0.001 0.001 | 0.004 0.005 0.004 | 0.002 0.000 0.001 |

| SE | 0.037 0.037 0.037 | 0.067 0.067 0.067 | 0.074 0.075 0.076 | 0.045 0.045 0.045 | 0.023 0.023 0.023 | |

| SEE | 0.036 0.036 0.036 | 0.067 0.067 0.067 | 0.075 0.075 0.075 | 0.045 0.045 0.045 | 0.023 0.023 0.023 | |

| CP | 0.943 0.942 0.955 | 0.952 0.952 0.952 | 0.948 0.949 0.945 | 0.945 0.956 0.947 | 0.948 0.950 0.950 | |

| LARE | BIAS | 0.001 0.002 0.001 | 0.001 0.002 0.000 | 0.004 0.004 0.002 | 0.001 0.001 0.001 | 0.044 0.000 0.001 |

| SE | 0.032 0.033 0.034 | 0.077 0.075 0.073 | 0.076 0.073 0.076 | 0.047 0.048 0.047 | 0.035 0.034 0.034 | |

| SEE | 0.033 0.034 0.034 | 0.075 0.075 0.075 | 0.073 0.072 0.072 | 0.047 0.047 0.047 | 0.032 0.032 0.033 | |

| CP | 0.945 0.944 0.951 | 0.944 0.943 0.959 | 0.926 0.928 0.931 | 0.936 0.927 0.934 | 0.942 0.943 0.943 | |

| LS | BIAS | 0.001 0.002 0.001 | 0.001 0.002 0.000 | 0.004 0.003 0.002 | 0.004 0.005 0.005 | 0.004 0.005 0.001 |

| SE | 0.035 0.035 0.037 | 0.083 0.081 0.078 | 0.071 0.069 0.072 | 0.047 0.047 0.047 | 0.025 0.025 0.025 | |

| SEE | 0.035 0.035 0.035 | 0.081 0.080 0.080 | 0.070 0.069 0.070 | 0.045 0.045 0.045 | 0.025 0.026 0.026 | |

| CP | 0.945 0.952 0.926 | 0.948 0.937 0.951 | 0.950 0.939 0.935 | 0.939 0.941 0.950 | 0.945 0.946 0.947 | |

| LAD | BIAS | 0.001 0.002 0.001 | 0.001 0.004 0.001 | 0.004 0.003 0.001 | 0.009 0.008 0.010 | 0.053 0.001 0.002 |

| SE | 0.033 0.034 0.034 | 0.143 0.140 0.135 | 0.090 0.085 0.090 | 0.061 0.060 0.058 | 0.037 0.037 0.036 | |

| SEE | 0.036 0.038 0.038 | 0.145 0.144 0.144 | 0.093 0.094 0.094 | 0.063 0.062 0.062 | 0.040 0.040 0.039 | |

| CP | 0.938 0.915 0.921 | 0.897 0.868 0.888 | 0.917 0.907 0.906 | 0.899 0.887 0.906 | 0.900 0.902 0.901 | |

| ; | ||||||

| . | ||||||

Table 2. Type I error and power with the null hypothesis

| (-2,2) | ||||||||

| (1.0, 1.0, 0.0) | 0.053 | 0.015 | 0.049 | 0.009 | 0.057 | 0.013 | 0.053 | 0.006 |

| (1.0, 1.0, 0.1) | 0.338 | 0.157 | 0.280 | 0.120 | 0.593 | 0.350 | 0.772 | 0.569 |

| (1.0, 1.0, 0.2) | 0.823 | 0.637 | 0.745 | 0.555 | 0.987 | 0.965 | 0.999 | 0.997 |

| (1.0, 1.0, 0.3) | 0.984 | 0.955 | 0.980 | 0.921 | 1 | 1 | 1 | 1 |

| (1.0, 1.0, 0.4) | 1 | 0.999 | 0.998 | 0.991 | 1 | 1 | 1 | 1 |

| represents the nominal significance level. | ||||||||

Table 3. Type I error and power with the null hypothesis

| (-2,2) | ||||||||

|---|---|---|---|---|---|---|---|---|

| (1.0, 0.0, 0.0) | 0.045 | 0.013 | 0.057 | 0.015 | 0.048 | 0.008 | 0.058 | 0.008 |

| (1.0, 0.1, 0.0) | 0.270 | 0.103 | 0.222 | 0.084 | 0.524 | 0.281 | 0.683 | 0.463 |

| (1.0, 0.1, 0.1) | 0.462 | 0.258 | 0.391 | 0.214 | 0.809 | 0.607 | 0.941 | 0.828 |

| (1.0, 0.2, 0.0) | 0.773 | 0.568 | 0.663 | 0.455 | 0.984 | 0.933 | 0.997 | 0.990 |

| (1.0, 0.2, 0.2) | 0.965 | 0.900 | 0.914 | 0.810 | 1 | 1 | 1 | 1 |

Table 4. Analysis of the body fat data with LPRE, LARE, LS and LAD

| LPRE | LARE | LS | LAD | ||||||||

| Est | -value | Est | -value | Est | -value | Est | -value | ||||

| 2.823 (0.026) | 0.000 | 2.851 (0.027) | 0.000 | 2.835 (0.022) | 0.000 | 2.883 (0.029) | 0.000 | ||||

| 0.085 (0.038) | 0.013 | 0.052 (0.027) | 0.027 | 0.072 (0.031) | 0.011 | 0.055 (0.038) | 0.074 | ||||

| -0.155 (0.068) | 0.011 | -0.205 (0.073) | 0.002 | -0.156 (0.056) | 0.003 | -0.211 (0.088) | 0.008 | ||||

| -0.103 (0.052) | 0.024 | -0.064 (0.044) | 0.073 | -0.102 (0.043) | 0.009 | -0.064 (0.047) | 0.087 | ||||

| -0.167 (0.076) | 0.014 | -0.168 (0.063) | 0.004 | -0.134 (0.063) | 0.017 | -0.093 (0.081) | 0.125 | ||||

| 0.582 (0.091) | 0.000 | 0.547 (0.084) | 0.000 | 0.558 (0.075) | 0.000 | 0.501 (0.105) | 0.000 | ||||

| -0.231 (0.085) | 0.003 | -0.200 (0.069) | 0.002 | -0.217 (0.07) | 0.001 | -0.235 (0.079) | 0.001 | ||||

| 0.105 (0.077) | 0.086 | 0.047 (0.055) | 0.196 | 0.090 (0.063) | 0.076 | 0.064 (0.073) | 0.190 | ||||

| 0.026 (0.054) | 0.315 | 0.003 (0.038) | 0.469 | 0.020 (0.044) | 0.327 | -0.011 (0.048) | 0.409 | ||||

| -0.009 (0.036) | 0.401 | -0.018 (0.037) | 0.313 | -0.005 (0.029) | 0.437 | -0.002 (0.032) | 0.475 | ||||

| 0.081 (0.049) | 0.049 | 0.034 (0.049) | 0.244 | 0.051 (0.041) | 0.106 | 0.008 (0.056) | 0.443 | ||||

| 0.033 (0.040) | 0.205 | 0.035 (0.034) | 0.152 | 0.033 (0.033) | 0.157 | 0.028 (0.042) | 0.252 | ||||

| -0.088 (0.047) | 0.031 | -0.084 (0.036) | 0.010 | -0.088 (0.039) | 0.012 | -0.095 (0.044) | 0.015 | ||||

| Est,parameter estimate. The estimated standard deviations are given in the parentheses. | |||||||||||

Table 5. Comparisons of median prediction errors with LPRE, LARE, LS and LAD

| LPRE | LARE | LS | LAD | |

|---|---|---|---|---|

| MPE | 3.679 | 3.957 | 3.861 | 3.933 |

| MPPE | 0.039 | 0.046 | 0.043 | 0.041 |

| MPAE | 0.401 | 0.433 | 0.418 | 0.410 |

| MSPE | 13.537 | 15.660 | 14.907 | 15.468 |