Primal and Dual Approximation Algorithms for Convex Vector Optimization Problems

Abstract

Two approximation algorithms for solving convex vector optimization problems (CVOPs) are provided. Both algorithms solve the CVOP and its geometric dual problem simultaneously. The first algorithm is an extension of Benson’s outer approximation algorithm, and the second one is a dual variant of it. Both algorithms provide an inner as well as an outer approximation of the (upper and lower) images. Only one scalar convex program has to be solved in each iteration. We allow objective and constraint functions that are not necessarily differentiable, allow solid pointed polyhedral ordering cones, and relate the approximations to an appropriate -solution concept. Numerical examples are provided.

Keywords: Vector optimization, multiple objective optimization, convex programming, duality, algorithms, outer approximation.

MSC 2010 Classification: 90C29, 90C25, 90-08, 91G99

1 Introduction

A variety of methods have been developed in the last decades to solve or approximately solve vector optimization problems. As in scalar optimization, only special problem classes are tractable. One of the most studied classes consists of linear vector optimization problems (LVOPs). There are many solution methods for LVOPs in the literature, see e.g. the survey paper by Ehrgott and Wiecek [8] and the references therein. The multi-objective simplex method, for instance, evaluates the set of all efficient solutions in the variable space (or decision space). Interactive methods, for instance, compute a sequence of efficient solutions depending on the decision maker’s preferences. Benson [2] proposed an outer approximation algorithm in order to generate the set of all efficient values in the objective space. He motivates this method by observing that typically the dimension of the objective space is much smaller than the dimension of the variable space, decision makers tend to choose a solution based on objective values rather than variable values, and often many efficient solutions are mapped to a single efficient point in the objective space. A solution concept for LVOPs which takes into account these ideas has been introduced in [18]. Several variants of Benson’s algorithm for LVOPs have been developed, see e.g. [23, 24, 18, 6], having in common that at least two LPs need to be solved in each iteration. Independently in [11] and [4], an improved variant for LVOPs has been proposed where only one LP has to be solved in each iteration.

Convex vector optimization problems (CVOPs) are more difficult to solve than LVOPs. There are methods which deal with CVOPs, and specific subclasses of it. We refer the reader to the survey paper by Ruzika and Wiecek [22] for a classification of approximation methods for a CVOP. Recently, Ehrgott, Shao, and Schöbel [7] developed a Benson type algorithm for bounded CVOPs, motivated by the same arguments as given above for LVOPs. They extended Benson’s algorithm to approximate the set of all efficient values in the objective space from LVOPs to CVOPs. In this paper, we generalize and simplify this approximation algorithm and we introduce a dual variant of it. To be more detailed, compared to [7], we

-

(i)

allow objective and constraint functions that are not necessarily differentiable (provided certain non-differentiable scalar problems can be solved),

-

(ii)

allow more general ordering cones,

-

(iii)

use a different measure for the approximation error (as in [11]), which allows the algorithms to be applicable to a larger class of problems,

-

(iv)

obtain at no additional cost a finer approximation by including suitable points in the primal and dual inner approximations throughout the algorithm,

-

(v)

reduce the overall cost by simplifying the algorithm in the sense that only one convex optimization problem has to be solved in each iteration instead of two,

-

(vi)

relate the approximation to an -solution concept involving infimum attainment,

-

(vii)

present additionally a dual algorithm that provides an alternative approximation/ -solution.

This paper is structured as follows. Section 2 is dedicated to basic concepts and notation. In Section 3, the convex vector optimization problem, its geometric dual, and solution concepts are introduced. Furthermore, the geometric duality results for CVOPs are stated and explained. In Section 4, an extension of Benson’s algorithm for CVOPs and a dual variant of the algorithm are provided. Numerical examples are given in Section 5.

2 Preliminaries

For a set , we denote by , , , , , respectively the interior, closure, boundary, convex hull and the conic hull of . A polyhedral convex set can be defined as the intersection of finitely many half spaces, that is,

| (1) |

for some , , and . Every non-empty polyhedral convex set can also be written as

| (2) |

where , each is a point, and each is a direction of . Note that is called a direction of if . The set of points together with the set of directions are called the generators of the polyhedral convex set . Representation (2) of A is called the V-representation (or generator representation) whereas representation (1) of A by half-spaces is called H-representation (or inequality representation). A subset of a convex set is called an exposed face of if there exists a supporting hyperplane to , with .

A convex cone is said to be solid, if it has a non-empty interior; pointed if it does not contain any line; and non-trivial if . A non-trivial convex pointed cone C defines a partial ordering on : if and only if . Let be a non-trivial convex pointed cone and a convex set. A function is said to be -convex if holds for all , , see e.g. [20, Definition 6.1]. A point is called -minimal element of A if . If the cone is solid, then a point is called weakly -minimal element if . The set of all (weakly) -minimal elements of is denoted by . The set of (weakly) -maximal elements is defined by . The (positive) dual cone of is the set .

3 Convex Vector Optimization

3.1 Problem Setting and Solution Concepts

A convex vector optimization problem (CVOP) with polyhedral ordering cone is to

| (P) |

where , and are non-trivial pointed convex ordering cones with nonempty interior, is a convex set, the vector-valued objective function is -convex, and the constraint function is -convex (see e.g. [20]). Note that the feasible set of (P) is convex. Throughout we assume that (P) is feasible, i.e., . The image of the feasible set is defined as . The set

| (3) |

is called the upper image of (P) (or upper closed extended image of (P), see [13]). Clearly, is convex and closed.

Definition 3.1.

(P) is said to be bounded if for some .

The following definition describes a solution concept for complete-lattice-valued optimization problems which was introduced in [15]. It applies to the special case of vector optimization (to be understood in a set-valued framework). The solution concept consists of two components, minimality and infimum attainment. Here we consider the special case based on the complete lattice with respect to the ordering , see e.g. [10], which stays in the background in order to keep the notation simple.

In [18] this concept was adapted to linear vector optimization problems, where one is interested in solutions which consist of only finitely many minimizers. In the unbounded case, this requires to work with both points and directions in . For a (bounded) CVOP, the requirement that a solution consists of only finitely many minimizers is not adequate, since it is not possible in general to represent the upper image by finitely many points (and directions). However, a finite representation is possible in case of approximate solutions. To this end, we extend the idea of (finitely generated) -solutions of LVOPs, which was introduced in Remark in [11], to the setting of bounded CVOPs. An infimizer has to be replaced by a finite -infimizer. As we only consider bounded problems here, we do not need to deal with directions. It is remarkable that an -solution provides both an inner and an outer polyhedral approximation of the upper image by finitely many minimizers. Throughout this paper let be fixed.

Definition 3.3.

Note that if is a finite (weak) -solution, we have the following inner and outer approximation of the upper image

3.2 Geometric Duality

Geometric duality for vector optimization problems has first been introduced for LVOPs in [14]. The idea behind geometric duality in the linear case is to consider a dual problem with a lower image being dual to the upper image in the sense of duality of convex polyhedra. Recently, Heyde [13] extended geometric duality to the case of CVOPs.

We next define the geometric dual problem of (P). Recall that is fixed. Further, we fix such that the vectors are linearly independent. Using the nonsingular matrix , we define

for . For arbitrary we immediately obtain the useful statement

| (5) |

The geometric dual of (P) is given by

| (D) |

where the objective function is

and the ordering cone is .

Similar to the upper image for the primal problem (P), we define the lower image for (D) as , where is the feasible region of (D). The lower image can be written as

Proposition 3.5.

Let and . If (P) has a finite optimal value , then is -maximal in and .

Proof.

Since , we have . We obtain and is -maximal in since does not depend on . The remaining statements are obvious. ∎

Remark 3.6.

Another possibility is to define the dual objective function as

By this variant the special structure of the feasible set is taken into account. As this definition leads to the same lower image , very similar results can be obtained.

The lower image is a closed convex set. To show convexity, let , , and set . Then, , as is convex. It holds as we have

Taking into account [13, Proposition 5.5 and Remark 2] we see that is closed (since it can be expressed as for some function , cf. [13]).

In [13] it was proven that there is a one-to-one correspondence between the set of -maximal exposed faces of , and the set of all weakly -minimal exposed faces of . Recall that the -maximal elements of are defined as elements of the set . For we define:

The duality map is constructed as

The following geometric duality theorem states that is a duality map between and .

Theorem 3.7 ([13, Theorem 5.6]).

is an inclusion reversing one-to-one mapping between the set of all -maximal exposed faces of and the set of all weakly -minimal exposed faces of . The inverse map is given by

Similar to Definition 3.2 and following the pattern of the linear case in [11, 18], we introduce a solution concept for the dual problem (D).

Definition 3.8.

As for the primal problem, we also consider an -solution of (D) consisting of only finitely many maximizers. This concept is an extension of -solutions for LVOPs introduced in [11, Remark 4.10] to the convex setting.

Definition 3.9.

Note that if is a finite -solution of (D), one obtains the following inner and outer polyhedral approximation of the lower image

We next show that an approximation of the upper image of (P) can be used to obtain an approximation of the lower image of (D) and vise versa. We have the following duality relations, which will be used to prove the correctness of the algorithms, see Theorems 4.9 and 4.14 below.

Proposition 3.10.

Let be a closed and convex set such that and let be defined by

| (7) |

Then,

| (8) |

Proof.

The inclusion is obvious. Assume that the inclusion does not hold. Then there exists such that for all . By usual separation arguments, we get with . Since we can assume . Setting , we get . For all , we have , i.e., . But , a contradiction. ∎

Proposition 3.11.

Proof.

The inclusion is obvious. Assume the inclusion does not hold. Then, there exists with for all . Applying a separation argument, we obtain with . Using the assumption , we get . Set and let such that . For we have

Without loss of generality we can assume that . Setting , we have for all which implies . But, , a contradiction. ∎

4 Algorithms for CVOPs

Let us consider the convex vector optimization problem (P) with polyhedral ordering cones and . Then, we can assume without loss of generality that , which means that is component-wise convex. Indeed, whenever is polyhedral, the feasible set can be written as , where are the generating vectors of the dual cone of , and is defined by for . Moreover, is -convex if and only if is -convex.

In addition to the assumptions made in the problem formulation of (P) in the beginning of Section 3.1, we will assume the following throughout the rest of the paper.

Assumption 4.1.

Let the following hold true.

-

(a)

The feasible region is a compact subset of .

-

(b)

has non-empty interior.

-

(c)

The objective function is continuous.

-

(d)

The ordering cone is polyhedral, and .

Assumption 4.1 implies that problem (P) is bounded. Indeed, as is compact and is continuous, is compact, in particular, bounded. Thus, there exists and such that the open ball around with radius contains . Furthermore, as , there exists such that . Now one can check that satisfies .

Another consequence of Assumption 4.1 is that is closed, i.e. the upper image as defined in (3) can be expressed as . Assumption 4.1 guaranties the existence of solutions and finite -solutions to (P).

Proof.

This is a consequence of the vectorial Weierstrass Theorem ([15, Theorem 6.2] or [18, Theorem 2.40]). A solution in the sense of Definition 3.2 corresponds to a ‘mild convexity solution’ in [18, Definition 2.48], see [18, Propositions 1.58, 1.59]. The vectorial Weierstrass Theorem [18, Theorem 2.40] implies the existence of a ‘solution’ in the sense of [18, Definition 2.20], obviously being a ‘mild solution’ in the sense of [18, Definition 2.41] and being a ‘mild convexity solution’ by [18, Corollary 2.51]. ∎

Proof.

As already mentioned in the proof of Proposition 4.2, there exists a ‘solution’ in the sense of [18, Definition 2.41], that is, is the set of all minimizers for (P) and we have . For arbitrary fixed , is an open cover of , which is a compact set by Assumptions 4.1. Hence there is a finite subcover and is a finite -solution. ∎

4.1 Primal Algorithm

Benson’s algorithm has been extended to approximate the upper image of a convex vector optimization problem in [7]. In this section, we will generalize and simplify this algorithm as detailed in the introduction. The algorithm can be explained as follows. Start with an initial outer approximation of and compute iteratively a sequence of better outer approximations.

The first step in the iteration is to compute the vertices of . During the algorithm, whenever is updated, it is given by an H-representation. To convert an H-representation into a V-representation (and vise versa) one uses vertex enumeration, see e.g. [3]. For a vertex of , a point on the boundary of the upper image, which is in ‘minimum distance’ to , is determined. Note that for some , and . We add all those to a set , where has to be initialized appropriately. This set will be shown to be a finite weak -solution to (P) at termination. If the minimum distance is less than or equal to an error level , which is determined by the user, the algorithm proceeds to check another vertex of in a similar way. If the minimum distance is greater than the error level , a cutting plane, i.e., a supporting hyperplane of the upper image at the point and its corresponding halfspace containing the upper image are calculated. The new approximation is obtained as . The algorithm continues in the same manner, until all vertices of the current approximation are in ‘-distance’ to the upper image. The details of the algorithm are explained below.

To compute , let be the matrix, whose columns are the generating vectors of the dual cone of the ordering cone and let be normalized in the sense that for all (recall that is fixed). Denote () the optimal solutions of (P), which always exist by Assumptions 4.1 (a) and (c). Define the halfspace

Note that belongs to the feasible set of (D) since and , compare (5). We have , which implies

| (9) |

It is easy to check that for all , contains the upper image (‘weak duality’). We define the initial outer approximation as the intersection of these halfspaces, that is,

| (10) |

Since is pointed and (P) is bounded, contains no lines. By [21, Corollary 18.5.3] we conclude that has at least one vertex. Vertex enumeration yields the set of all vertices.

We will use the following convex program which depends on a parameter vector , which typically does not belong to ,

| (P) |

The second part of constraints can be expressed as . Hence, the Lagrangian

| (11) |

yields the dual problem

which can be equivalently expressed as

| (D) |

where is the matrix whose columns are the generating vectors of the cone .

The following propositions will be used later to prove the correctness of the algorithm.

Proposition 4.4.

Proof.

is compact by Assumption 4.1 (a). The set is closed as is continuous by Assumption 4.1 (c). Thus the feasible set for (P) is compact, which implies the existence of an optimal solution of (P). By Assumption 4.1 (b) there exists with . Since , we have . Taking large enough, we obtain . Hence, satisfies Slater’s condition. Convex programming duality implies the existence of a solution of (D) and coincidence of the optimal values. ∎

Proposition 4.5.

Proof.

Suppose is not a weak minimizer of (P), i.e., for some . We have for some and there exists such that , hence

Multiplying by the matrix whose columns are the generating vectors of , we get , which implies that is feasible for (P) but generates a smaller value than the optimal value , a contradiction.

To show that , first note that . Since is given by as , we have , i.e., and thus . Suppose that . Then (see e.g. [18, Corollary 1.48 (iii)] for the last equation). There exists with , i.e., there is with . This means that is feasible for (P) and has a smaller value than the optimal value , a contradiction. ∎

Proposition 4.6.

Proof.

As is feasible for (D), we have and . By (5), we obtain . Hence is a maximizer of (D) by Proposition 3.5 and the fact that (P) has an optimal solution by Assumption 4.1. It remains to show (12). Since is a saddle point of the Lagrangian in (11), and taking into account that , we get

This yields (12) if we can show that

But, if is considered to be a parameter, is an optimal solution for (D) and the desired statement follows from strong duality between (P) and (D). ∎

The next step is to show that a supporting hyperplane of at can be found using an optimal solution of (D).

Proposition 4.7.

Proof.

Proposition 4.8.

For , let be a finite (weak) -solution of (P), and define . Then, is an inner -approximation of the lower image , that is, .

Similarly, let be a finite -solution of (D), and define . Then, is an inner -approximation of the upper image , that is, .

Proof.

Theorem 4.9.

Proof.

By Assumption 4.1, each problem (P) in line 1 has an optimal solution . By Propositions 3.4 and 3.5, is a weak minimizer of (P) and is a maximizer of (D). Thus, the sets and are initialized by weak minimizers of (P) and maximizers of (D), respectively. As noticed after (10), has at least one vertex. Thus, the set in line 7 is nonempty. By Proposition 4.4, optimal solutions to (P) and (D) exist. By Proposition 4.5 a weak minimizer of (P) is added to in line 11. Proposition 4.6 ensures that a maximizer of (D) is added to in line 11. By Proposition 4.7, we know that defined in lines 6 and 13 satisfies . This ensures that holds throughout the algorithm. By the same argument as used for , we know that has at least one vertex. If the optional break in line 14 is in use, the inner loop (lines 8-16) is left if , and the current outer approximation is updated by setting . For the case without the optional break, see Remark 4.10 below. The algorithm stops if for all the vertices of the current outer approximation . Let us assume this is the case after iterations. We have

| (13) |

Indeed, the first inclusion follows from Proposition 4.7 and the second inclusion follows from the construction of the set , see (9), (10) and lines 13 and 18.

Note that in general, produces a finer outer approximation of the upper image than , see (13). The reason is that, in contrast to , is not necessarily updated in each iteration.

Remark 4.10.

The ‘break’ in line 14 of Algorithm 1 is optional. The algorithm with the break updates the outer approximation right after it detects a vertex with . The algorithm without the break goes over all the vertices of the current outer approximation before updating it. In general, one expects a larger number of vertex enumerations for the first variant (with break), and more optimization problems to solve for the second one (without break).

Remark 4.11 (Alternative Algorithm 1).

We will now discuss a modification of Algorithm 1. It produces -approximations of and as well, but with fewer vertices. Thus, the approximations are coarser. This alternative consists of three modifications.

First, set in line 3 of Algorithm 1. Second, replace lines 11-15 of Algorithm 1 with the alternative lines given below. Then, is only added to the set if there is no cut, while the dual counterpart is only added to if there is a cut. Third, line 21 of Algorithm 1 can be skipped and the vertices of can be returned as the final outer -approximation of . Note that the first two modifications imply , which makes line 21 superfluous.

Under these three modifications, one still finds a finite weak -solution to (P), and a finite -solution to (D); but, in general, and have less elements compared to the original version of Algorithm 1, so the approximation is coarser. This variant is used in [7]. We propose Algorithm 1 as it yields a finer approximation at no additional cost.

4.2 Dual Algorithm

A dual variant of Benson’s algorithm for LVOPs based on geometric duality [14] has been introduced in [6]. An extension which approximately solves dual LVOPs was established in [24]. The main idea is to construct approximating polyhedra of the lower image of the geometric dual problem (D) analogous to Algorithm 1. Geometric duality is used to recover approximations of the upper image of the primal problem (P).

We employ the same idea in order to construct a dual variant of an approximation algorithm for CVOPs. The algorithm starts with an initial outer approximation of and computes iteratively a sequence of smaller outer approximations. As in the primal algorithm, the vertices of are found using vertex enumeration. Each vertex is added to the set , which will be shown to be a finite -solution to (D). Then, we check the ‘distance’ between and the boundary of the lower image. If it is greater than , a point , and a supporting hyperplane to at are determined. The approximation for the next iteration is updated as the intersection of and the corresponding halfspace containing the lower image. The algorithm continues in the same manner until all vertices of the current approximation are in ‘ distance’ to the lower image. After this, it returns a finite weak -solution of (P), a finite -solution of (D), as well as outer and inner approximations to the upper image (and to the lower image , by duality).

The feasible region of (D) obviously provides an outer approximation of . All supporting hyperplanes of are vertical, that is, they have a normal vector with .

Recall that Assumption 4.1 was assumed to hold in this section, which leads to the existence of optimal solutions of (P) and (D) for every . Both convex programs play an important role in the following.

Proposition 4.12.

Let , , and be the optimal objective value for (P). Then,

Proof.

This follows directly from the definition of . ∎

Proposition 4.13.

Let , , and be an optimal solution to problem (P). Then is a non-vertical supporting hyperplane to at .

Proof.

By Proposition 3.5, . We have , as and imply . Since is an affine function but does not depend on , is a non-vertical hyperplane. For any , we have , where the last inequality follows from the definition of . ∎

The initial outer approximation is obtained by solving (P) for

| (14) |

where are the generating vectors of such that . By Proposition 3.4, an optimal solution of (P) is a weak minimizer of (P). We have and by (5). By Proposition 3.5, is a maximizer for (D) and , where denotes the optimal value of (P). By Proposition 4.13, is a non-vertical supporting hyperplane to . The initial outer approximation is

| (15) |

As contains no lines, it has at least one vertex. We now state the dual algorithm.

Theorem 4.14.

Proof.

By Assumption 4.1, (P) has a solution for every . Note that we have by construction. This ensures that in line 1 and in line 8 belong to . Hence, by Proposition 3.4, consists of a weak minimizers of (P) only. We know that , contains no lines and, therefore, it has at least one vertex. Every vertex of in line 8 belongs to . By Proposition 3.5, is a maximizer to (D) with . Proposition 4.13 yields that is a supporting hyperplane of at . Hence, we have for all . The condition in line 11 just excludes some of the ’s to prevent that multiple elements are added to which yield the same objective value .

Assume the algorithm stops after iterations. The vertices of the outer approximation of satisfy , where is the optimal objective value of (P) for .

We next show that is a finite -solution to (D). We know that is nonempty and consists of maximizers for (D) only. It remains to show that is a finite -supremizer, i.e., (6) holds. As shown above, we have . By construction, every vertex of belongs to and we have . By , we obtain .

Finally, we prove that is a finite weak -solution to (P). We already know that is nonempty and finite, and it consists of weak minimizers for (P) only. It remains to show that is a finite -infimizer for (P), i.e., (4) holds. Setting , we have

Using Proposition 3.10, we conclude

By Proposition 4.8, . Altogether we have . ∎

Remark 4.15 (Alternative Algorithm 2).

Using similar arguments as in Remark 4.11 for Algorithm 1, we obtain an alternative variant of Algorithm 2. It is possible to replace lines 10-17 of Algorithm 2 by the alternative lines given below. In addition, one can initialize as the empty set in line 3. Line 23 can be skipped as the vertices of a coarser outer -approximation of are also given by .

4.3 Remarks

1. Algorithms 1 and 2 provide finite -solutions to (D), but only a finite ‘weak’ -solution to (P). The reason can be found in Propositions 3.4, and 4.5. Recall that for LVOPs in case of the situation is different: One can easily find a finite solution to (P). Since is polyhedral, the vertices that generate are considered, and any vertex of is -minimal, see [11].

2. Algorithms 1 and 2 return vertices of inner and outer approximations of . However, both inner and outer approximations of and can be obtained from the -solution concept: If is a finite weak -solution to (P) and is the matrix of generating vectors of , then is a V-representation of an inner approximation of and is an H-representation of an outer approximation of . If is a finite -solution to (D), then is a V-representation of an inner approximation of , and is an H-representation of an outer approximation of .

3. All algorithms in this paper still work correctly if Assumption 4.1 (a) is replaced by the requirement that optimal solutions of (P) and (P) exist for those parameter vectors and that occur during an algorithm is applied to a problem instance. This follows from the fact that compactness was only used to prove existence of the scalar problems. Note that (P) being bounded was not explicitly used in any proof. However, (P) being bounded is equivalent to (P) being bounded for every , which is necessary but not sufficient for the existence of a solution to (P). Problems with non-compact feasible set are solved in Examples 5.3 and 5.4 below.

4. This last remark concerns finiteness of the algorithms presented here. Even though there exists a finite -solution to (P) for any error level by Proposition 4.3, and a finite weak -solution to (P) is found if the algorithm terminates, it is still an open problem to show that the algorithms are finite. If the optional break command in Algorithm 1 is disabled, every vertex of the current approximation of is checked before updating the next approximation. Thus, decreases in each iteration of Algorithm 1. If one stops the algorithms at the iteration, a finite weak - solution to (P) is returned. In order to show that the algorithm is finite, one would need to show that . The situation in Algorithm 2 is similar.

5 Examples and numerical results

We provide four examples in this section. The first one illustrates how the algorithms work. The second example is [7, Example 6.2], an example with non-differentiable constraint function. This problem can be solved by the algorithms in this paper, where we use a solver which is able to solve some special non-differential scalar problems. The third example has three objectives and is related to generalization (iii) in the introduction. The last example has a four dimensional outcome space and shows that the algorithms provided here can be used for the calculation of set-valued convex risk measures. The corresponding vector optimization problems naturally have ordering cones being strictly larger and having more generating vectors than , which was one motivation to extend the algorithms to arbitrary solid convex polyhedral ordering cones.

We provide some computational data for each example with a corresponding table. The second column of the table shows the variant of the algorithm, where ‘break/no break’ corresponds to the optional breaks in line 14 of Algorithm 1, and line 16 of Algorithm 2. The next two columns show the number of scalar optimization problems ( opt.) solved, and the number of vertex enumerations ( vert. enum.) used during the algorithms. We provide the number of elements in the solution sets , found by Algorithms 1 and 2, as well as the number of the elements of the solution sets , found by the alternative versions given by Remarks 4.11 and 4.15. CPU time is measured in seconds. We used MATLAB to implement the algorithms, and we employ CVX, a package for specifying and solving convex programs, as a solver ([5, 9]). We ignore the approximation error of the solver, because it is typically much smaller than the we fix in the algorithms.

Example 5.1.

Consider the following problem

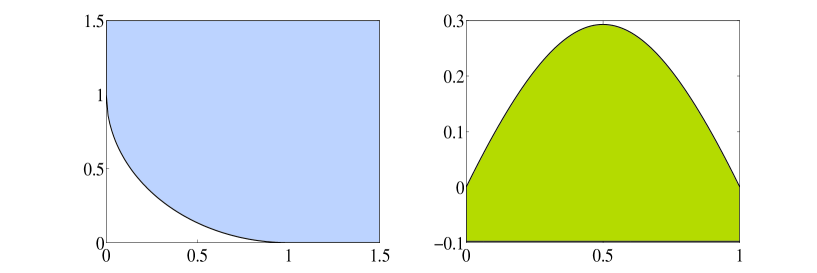

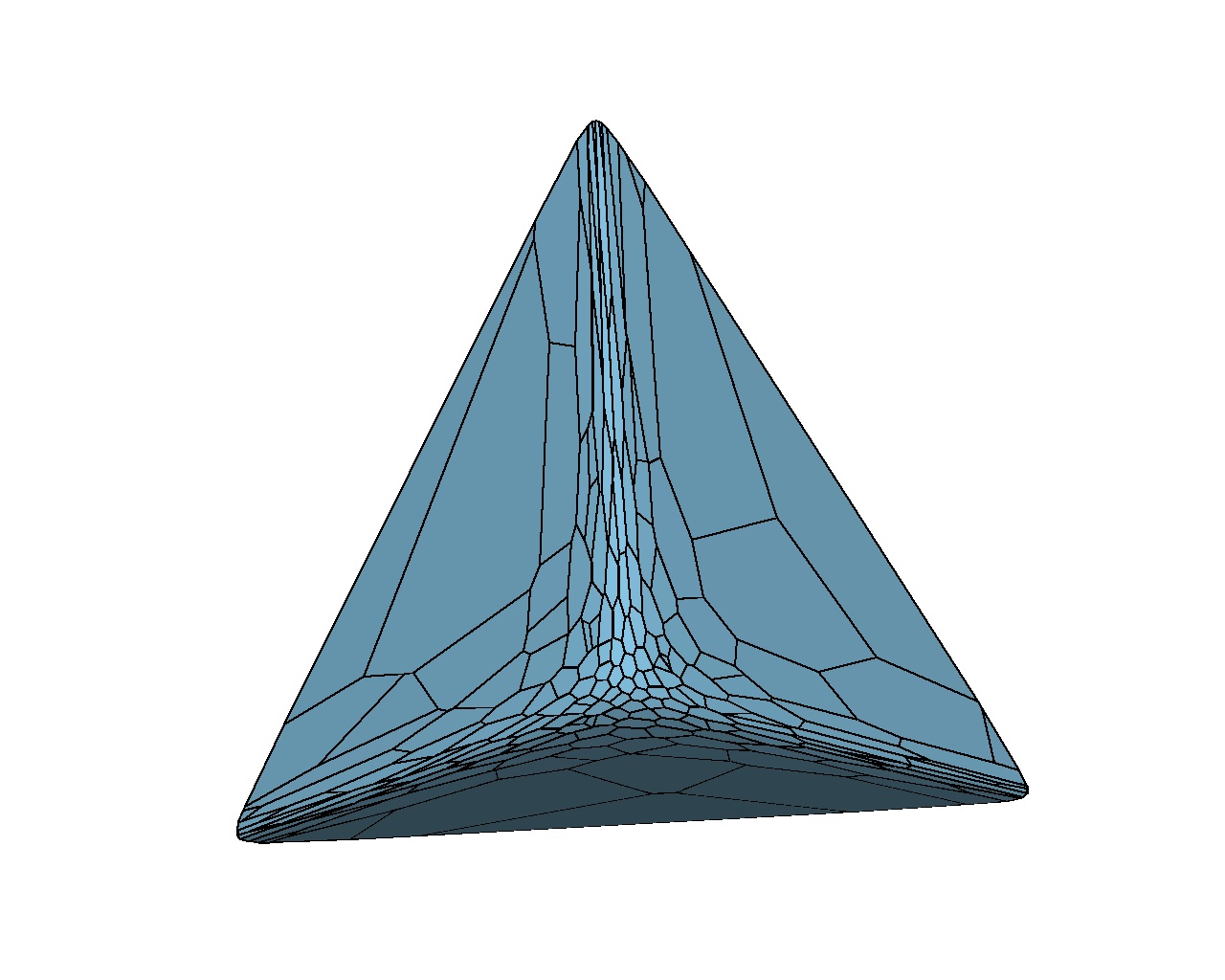

We set . The corresponding upper image and the lower image can be seen in Figure 1.

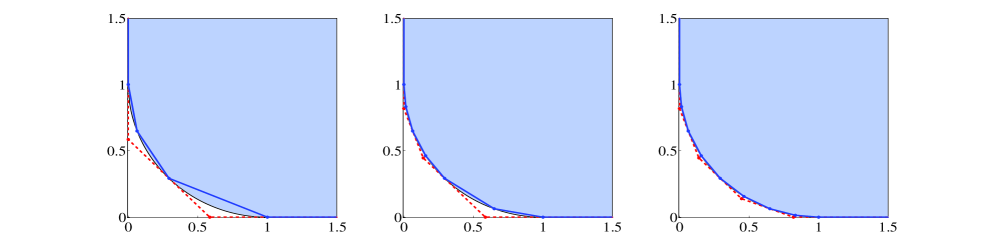

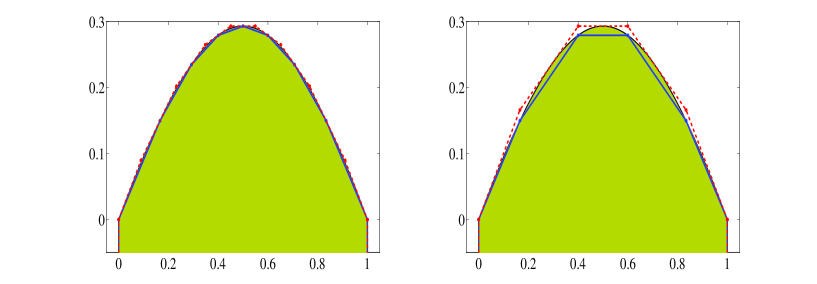

Algorithm 1 starts with . We set the approximation error and use the optional break in line 14. Figure 2 shows the inner and outer approximations for the upper image after the first three iterations . Remember that the current outer approximation is . The current inner approximation is , where denotes the ‘solution’ set at the end of iteration step .

After the third iteration (), Algorithm 1 stops. It returns vertices of an inner approximation given by , which coincide in this example with the finite weak -solution to (P):

The vertices of the final outer approximation are calculated in line of Algorithm 1, see left picture in Figure 3. If one uses the alternative version of the algorithm explained by Remark 4.11, then the inner and outer approximation would only have four vertices, see right picture in Figure 3, and a finite weak -solution to (P) is calculated as

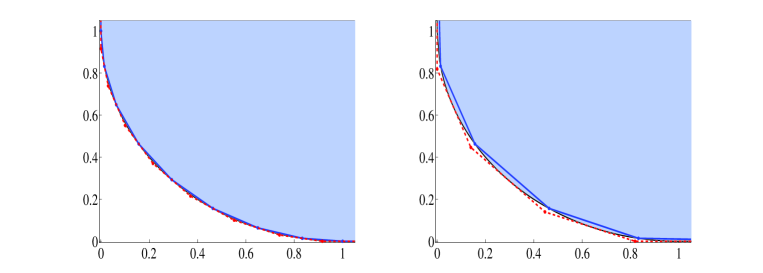

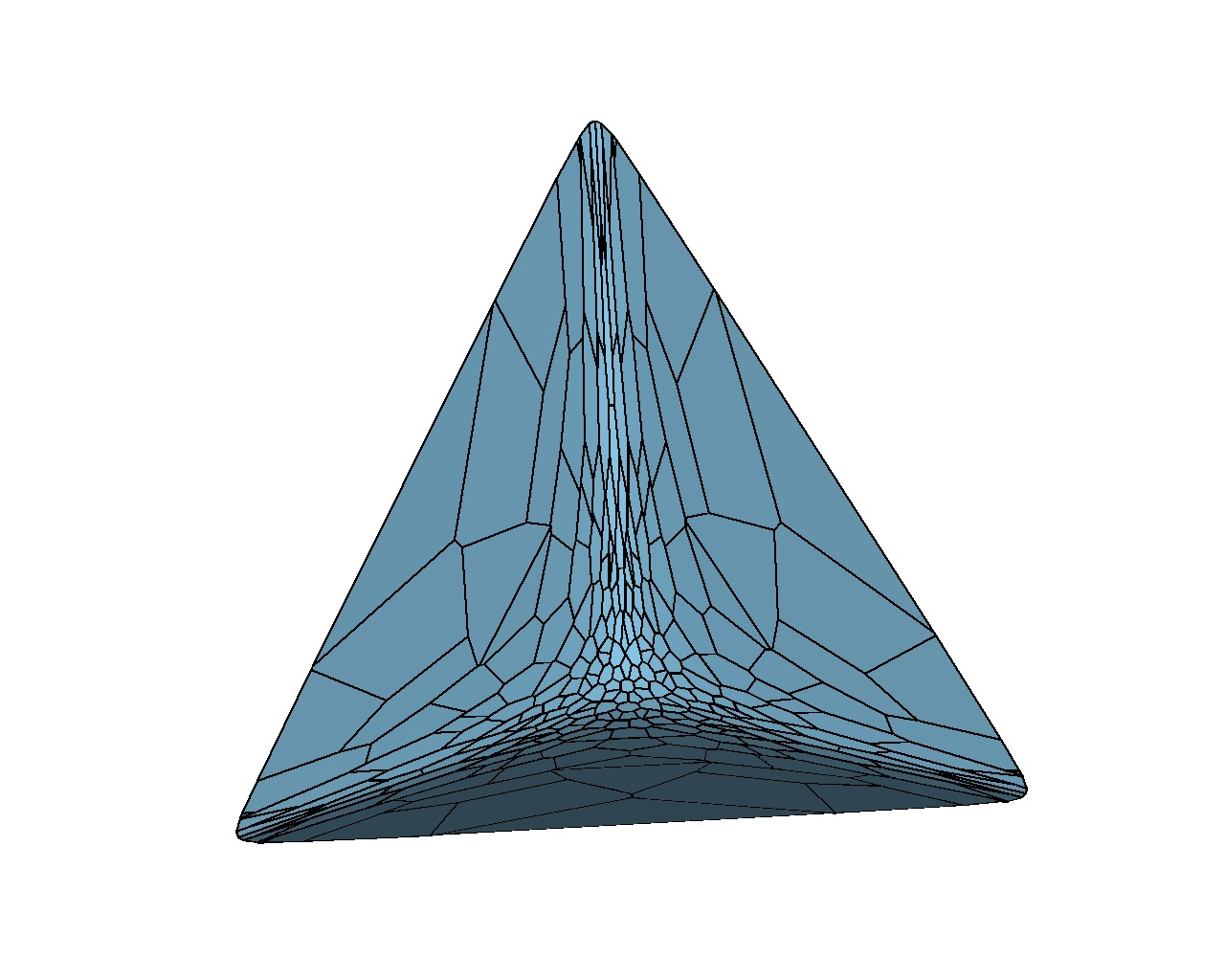

Now, let us solve the same example using the dual variant of the algorithm. We use the same approximation error and use the optional break in line 16. Note that . The initial non-vertical supporting hyperplane of is found as . The vertices of the initial outer approximation are then and . Note that the current outer approximation is , while the current inner approximation is , where denotes the ‘solution’ set at the end of iteration step . Figure 4 shows the approximations of the lower image after the first four iterations (). The computational data can be seen in Table 1.

After the fourth iteration the algorithm stops (). The algorithm calculated the vertices of the inner approximation of (see right picture in Figure 4 or left picture in Figure 5). An H-representation of the final outer approximation of is given by , see Section 4.3. Its vertices can be calculated by vertex enumeration, see left picture in Figure 5. The algorithm returns a finite weak -solution to (P) as follows:

If one uses the alternative version of the algorithm explained by Remark 4.15, then a finite weak -solution to (P) is found as

and the final inner and outer approximations of are given as in the right picture of Figure 5.

Example 5.2.

Consider the following problem with non-differentiable constraint function

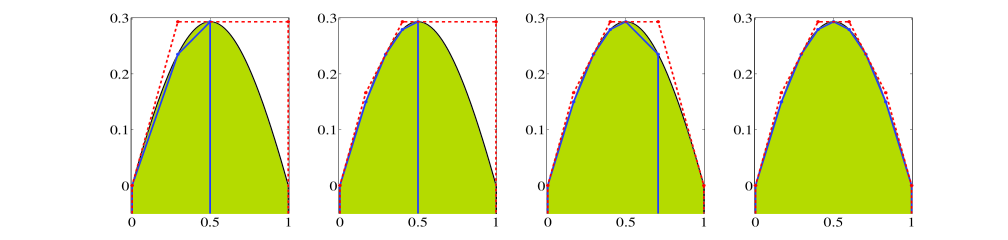

The ordering cone is , and we fix as before. This example is taken from [7], and it was used as an example which can not be solved by the algorithm provided in [7]. Since we do not assume differentiability in order to use the algorithms provided here, the example can be solved. Figure 6 shows the approximations of the upper and lower images generated by Algorithm 1, where the approximation error is taken as . Computational data regarding this example can be seen in Table 2.

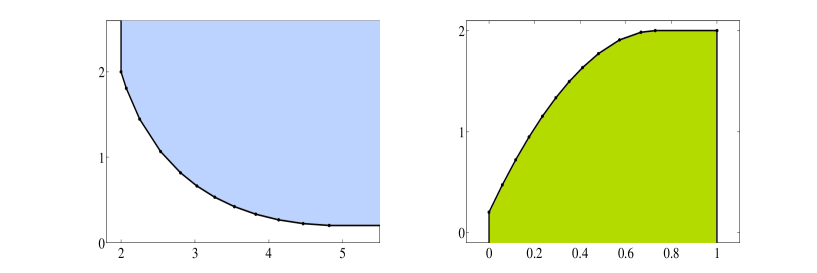

Example 5.3.

Consider the following problem

We fix , , and . Note that Assumptions 4.1 (b)-(d) hold, however the feasible region is not compact. Recall that one can still use the algorithms as long as the scalar problems have optimal solutions and in case the algorithms terminate, compare Remarks 3. and 4. in Section 4.3. We employ the convex optimization solver CVX, which detects whether the scalar problems are infeasible or unbounded, but not necessarily the case where a solution does not exist. If we apply Algorithm 2 to this example, for the unit vectors (), the solver does not detect that (P) does not have a solution and returns an approximate solution , where is very large. By numerical inaccuracy, we cannot ensure that the hyperplane according to Proposition 4.13 is non-vertical. This is the reason why the dual algorithm does not work for this example. However we can still use Algorithm 1. Figure 7 shows the outer approximations to the upper image generated by Algorithm 1 with approximation errors and . The graphics have been generated by JavaView111by Konrad Polthier, http://www.javaview.de. The numerical results can be seen in Table 3. This is an example where the algorithm proposed in [7] does not terminate for certain and (see [7]) due to a different measure for the approximation error.

| alg. / variant | opt. | vert. enum. | time (s) | |||||

|---|---|---|---|---|---|---|---|---|

| 1 / break | ||||||||

| 1 / no break | ||||||||

| 1 / break | ||||||||

| 1 / no break |

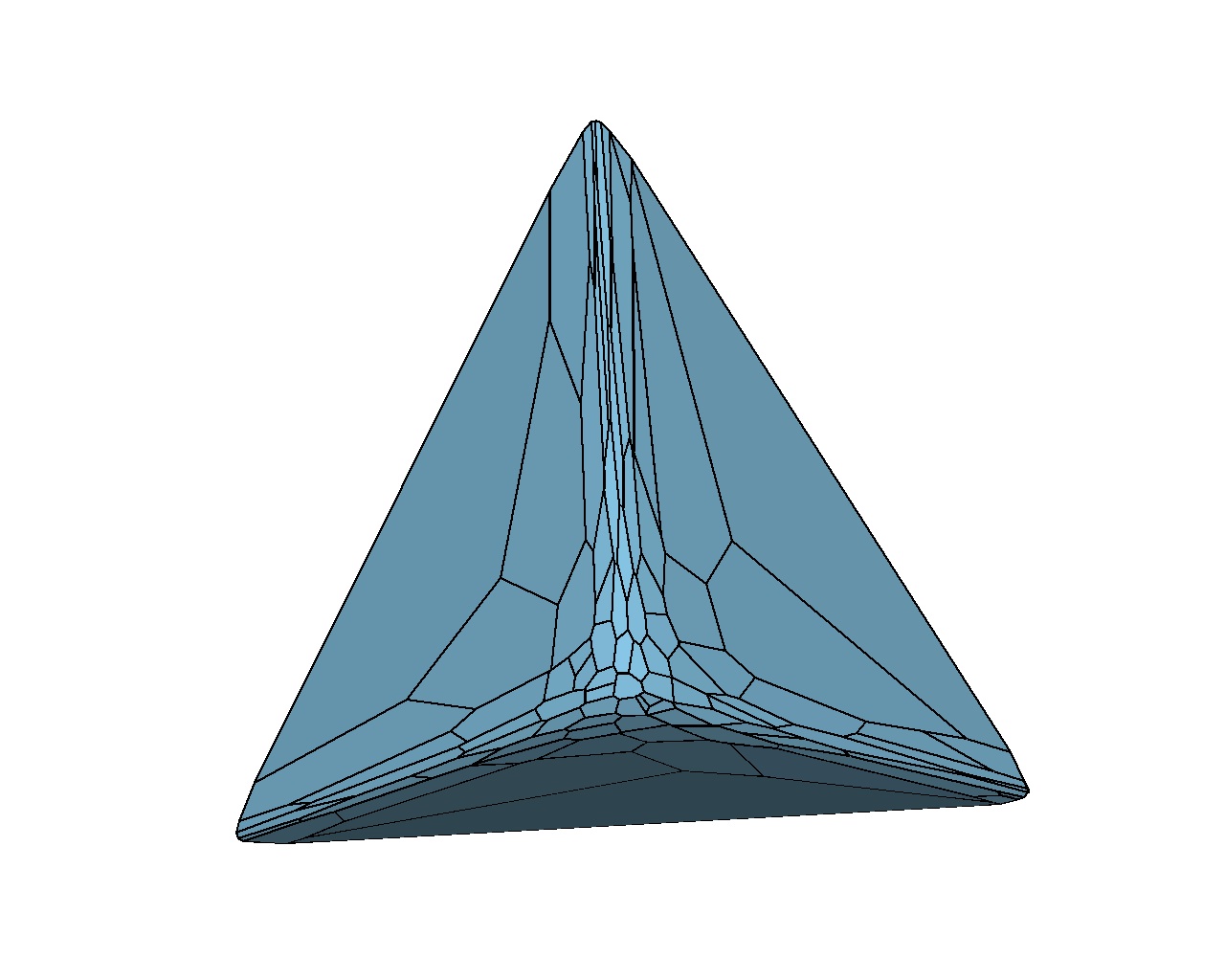

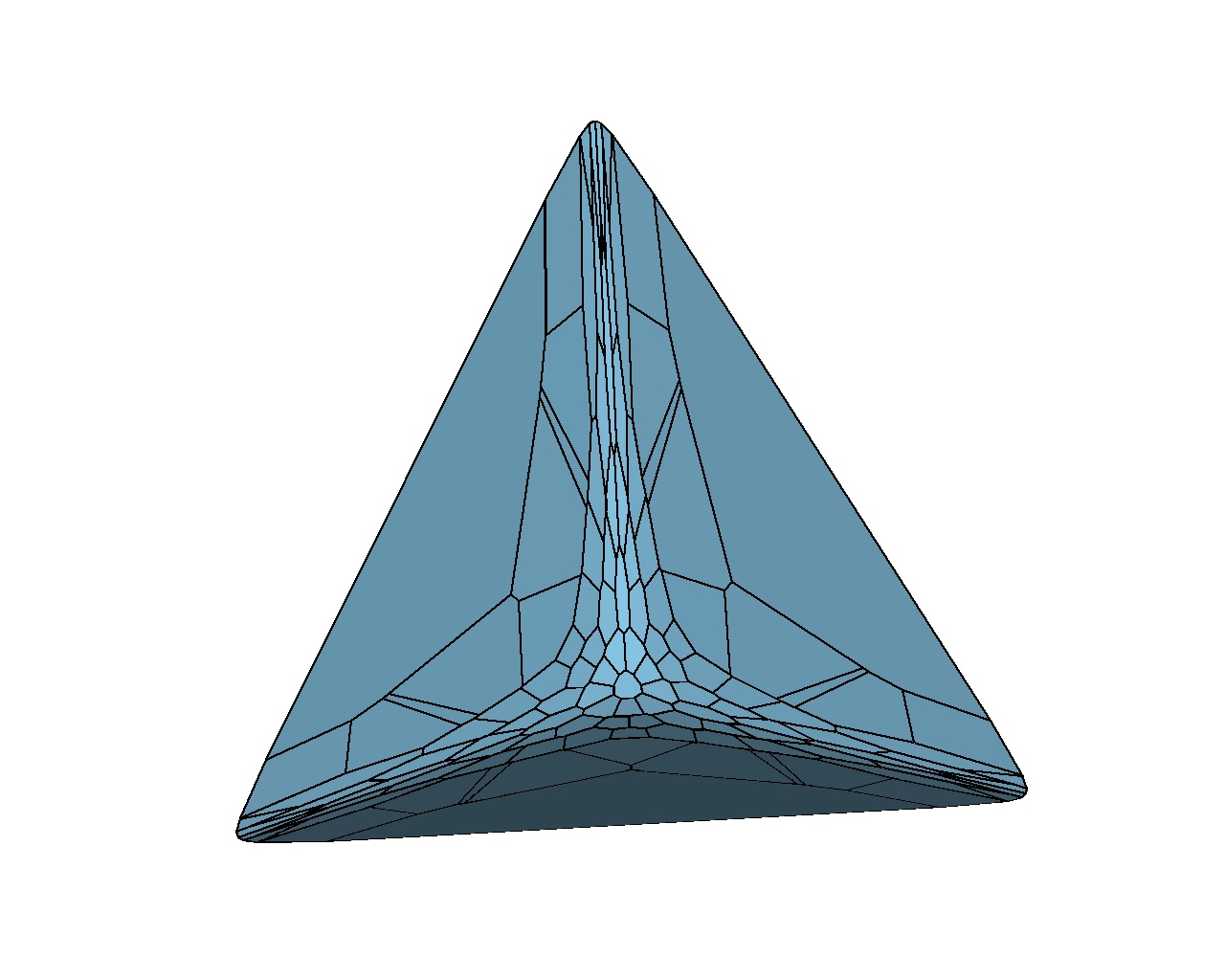

Example 5.4.

In this example we study the calculation of set-valued convex risk measures. It is known that polyhedral set-valued convex risk measures can be calculated by Benson’s algorithm for LVOPs (see [19, 12, 11]). Here, we show that (non-polyhedral) set-valued convex risk measures can be calculated approximately using the algorithms provided here. Consider a financial market consisting of assets, which can be traded at discrete time . Let be a finite probability space, where , such that , and . Assume that the market is defined by the adapted process of solvency cones, which represent the exchange rates and proportional transaction costs between the assets (see [17]). Note that is a polyhedral closed convex cone, with for , .

In this setting Ararat, Rudloff, and Hamel [1] consider set-valued shortfall risk measures on , the linear space of the equivalence classes of -measurable, -a.s. bounded, -dimensional random vectors. Let be a loss function such that is convex and increasing for . We consider here the one-period case only. It was shown that the market extension of the set-valued -shortfall risk measure is

where , , is a convex upper closed set, that is , and . It is shown in [1] that . For a given random vector , the set is the upper image of the following vector optimization problem

and thus can be approximated by the algorithms presented in this paper, whenever the set is polyhedral, say . Then, the constraint can be written as

As is upper closed we have , which implies that is convex. It is clear that the second and third set of constraints, and the objective function are linear. Thus, the problem is a CVOP with ordering cone . Similar to Example 5.3, Assumptions 4.1 (b)-(d) hold, however the feasible region is not compact as is not bounded. Remarks 3. and 4. in Section 4.3 explain the implications of that for the algorithms.

For a numerical example, set , , , and for . We fix , and , whose columns are the generating vectors of corresponding solvency cones and , . Let , and , where is the vector of ones. We calculate for being the payoff of an outperformance option. The vector-valued loss function is taken as , with .

We modeled the problem as a CVOP, where there are objectives, decision variables, and constraints. The ordering cone is with generating vectors, and we fix , , , and . We try both algorithms to solve the problem for different values of . It turns out that the solver fails to solve (P) for some of the vertices of the current outer approximation of the upper image. However, (P) can be solved for each , for the vertices of the outer approximations of the lower image. Thus, Algorithm 2 provides a finite weak -solution to (P), and a finite -solution to (D). Also, we only use the variant with ‘break’ as it turns out that it can solve the problem in less time compared to the variant without ‘break’. Table 4 shows some computational data of Algorithm 2.

References

- [1] Ç. Ararat, A. H. Hamel, and B. Rudloff. Set-valued shortfall and divergence risk measures. submitted, 2014.

- [2] H. P. Benson. An outer approximation algorithm for generating all efficient extreme points in the outcome set of a multiple objective linear programming problem. Journal of Global Optimization, 13:1–24, 1998.

- [3] D. Bremner, K. Fukuda, and A. Marzetta. Primal-dual methods for vertex and facet enumeration. Discrete Computational Geometry, 20(3):333–357, 1998.

- [4] L. Csirmaz. Using multiobjective optimization to map the entropy region of four random variables. preprint, 2013. http://eprints.renyi.hu/66/2/globopt.pdf.

- [5] Inc. CVX Research. CVX: Matlab software for disciplined convex programming, version 2.0 beta., September 2012.

- [6] M. Ehrgott, A. Löhne, and L. Shao. A dual variant of Benson’s outer approximation algorithm. Journal Global Optimization, 52(4):757–778, 2012.

- [7] M. Ehrgott, L. Shao, and A. Schöbel. An approximation algorithm for convex multi-objective programming problems. Journal of Global Optimization, 50(3):397–416, 2011.

- [8] M. Ehrgott and M. M. Wiecek. Multiobjective programming. In J. Figueira, S. Greco, and M. Ehrgott, editors, Multicriteria Decision Analysis: State of the Art Surveys, pages 667–722. Springer Science + Business Media, 2005.

- [9] M. C. Grant and S. P. Boyd. Graph implementations for nonsmooth convex programs. In V. Blondel, S. Boyd, and H. Kimura, editors, Recent Advances in Learning and Control, volume 371 of Lecture Notes in Control and Information Sciences, pages 95–110. Springer, London, 2008.

- [10] A. H. Hamel and A. Löhne. Lagrange duality in set optimization. Journal of Optimization Theory and Applications, 2013, DOI: 10.1007/s10957-013-0431-4.

- [11] A. H. Hamel, A. Löhne, and B. Rudloff. A Benson type algorithm for linear vector optimization and applications. Journal of Global Optimization, 2013, DOI: 10.1007/s10898-013-0098-2.

- [12] A. H. Hamel, B. Rudloff, and M. Yankova. Set-valued average value at risk and its computation. Mathematics and Financial Economics, 7(2):229–246, 2013.

- [13] F. Heyde. Geometric duality for convex vector optimization problems. Journal of Convex Analysis, 20(3):813–832, 2013.

- [14] F. Heyde and A. Löhne. Geometric duality in multiple objective linear programming. SIAM Journal of Optimization, 19(2):836–845, 2008.

- [15] F. Heyde and A. Löhne. Solution concepts in vector optimization: a fresh look at an old story. Optimization, 60(12):1421–1440, 2011.

- [16] J. Jahn. Vector Optimization - Theory, Applications, and Extensions. Springer, 2004.

- [17] Y. M. Kabanov. Hedging and liquidation under transaction costs in currency markets. Finance and Stochastics, 3:237–248, 1999.

- [18] A. Löhne. Vector Optimization with Infimum and Supremum. Springer, 2011.

- [19] A. Löhne and B. Rudloff. An algorithm for calculating the set of superhedging portfolios in markets with transaction costs. International Journal of Theoretical and Applied Finance, Forthcoming, 2013.

- [20] D. Luc. Theory of Vector Optimization, volume 319 of Lecture Notes in Economics and Mathematical Systems. Springer Verlag, 1989.

- [21] R. T. Rockafellar. Convex Analysis. Princeton University Press, 1970.

- [22] S. Ruzika and M. M. Wiecek. Approximation methods in multiobjective programming. Journal of Optimization Theory and Applications, 126(3):473–501, September 2005.

- [23] L. Shao and M. Ehrgott. Approximately solving multiobjective linear programmes in objective space and an application in radiotherapy treatment planning. Mathematical Methods of Operations Research, 68(2):257–276, 2008.

- [24] L. Shao and M. Ehrgott. Approximating the nondominated set of an MOLP by approximately solving its dual problem. Mathematical Methods of Operations Research, 68(3):469–492, 2008.