A pricing measure to explain the risk premium in power markets

Abstract.

In electricity markets, it is sensible to use a two-factor model with mean reversion for spot prices. One of the factors is an Ornstein-Uhlenbeck (OU) process driven by a Brownian motion and accounts for the small variations. The other factor is an OU process driven by a pure jump Lévy process and models the characteristic spikes observed in such markets. When it comes to pricing, a popular choice of pricing measure is given by the Esscher transform that preserves the probabilistic structure of the driving Lévy processes, while changing the levels of mean reversion. Using this choice one can generate stochastic risk premiums (in geometric spot models) but with (deterministically) changing sign. In this paper we introduce a pricing change of measure, which is an extension of the Esscher transform. With this new change of measure we also can slow down the speed of mean reversion and generate stochastic risk premiums with stochastic non constant sign, even in arithmetic spot models. In particular, we can generate risk profiles with positive values in the short end of the forward curve and negative values in the long end. Finally, our pricing measure allows us to have a stationary spot dynamics while still having randomly fluctuating forward prices for contracts far from maturity.

1. Introduction

In modelling and analysis of forward and futures prices in commodity markets, the risk premium plays an important role. It is defined as the difference between the forward price and the expected commodity spot price at delivery, and the classical theory predicts a negative risk premium. The economical argument for this is that producers of the commodity is willing to pay a premium for hedging their production (see Geman [9] for a discussion, as well as a list of references).

Geman and Vasicek [10] argued that in power markets, the consumers may hedge the price risk using forward contracts which are close to delivery, and thus creating a positive premium. Power is a non-storable commodity, and as such may experience rather large price variations over short time (sometimes referred to as spikes). One might observe a risk premium which may be positive in the short end of the forward market, and negative in the long end where the producers are hedging their power generation. A theoretical and empirical foundation for this is provided in, for example, Bessembinder and Lemon [5] and Benth, Cartea and Kiesel [3].

When deriving the forward price, one specifies a pricing probability and computes the forward price as the conditional expected spot at delivery. In the power market, this pricing probability is not necessarily a so-called equivalent martingale measure, or a risk neutral probability (see Bingham and Kiesel [6]), as the spot is not tradeable in the usual sense. Thus, a pricing probability can a priori be any equivalent measure, and in effect is an indirect specification of the risk premium. In this paper we suggest a new class of pricing measures which gives a stochastically varying risk premium.

We will focus our considerations on the power market, where typically a spot price model may take the form as a two-factor mean reversion dynamics. Lucia and Schwartz [20] considered two-factor models for the electricity spot price dynamics in the Nordic power market NordPool. Both arithmetic and geometric models where suggested, that is, either directly modelling the spot price by a two-factor dynamics, or assuming such a model for the logarithmic spot prices. Their models were based on Brownian motion and, as such, not able to capture the extreme variations in the power spot markets. Cartea and Figueroa [7] used a compound Poisson process to model spikes, that is, extreme price jumps which are quickly reverted back to ”normal levels”. Benth, Šaltytė Benth and Koekebakker [2] give a general account on multi-factor models based on Ornstein-Uhlenbeck processes driven by both Brownian motion and Lévy processes. Empirical studies suggest a stationary power spot price dynamics after explaining deterministic seasonal variations (see e.g. Barndorff-Nielsen, Benth and Veraart [1] for a study of spot prices at EEX, the German power exchange). We will in this paper focus on a two-factor model for the spot, where each factor is an Ornstein-Uhlenbeck process, driven by a Brownian motion and a jump process, respectively. The first factor models the ”normal variations” of the spot price, whereas the second accounts for sudden jumps (spikes) due to unexpected imbalances in supply and demand.

The standard approach in power markets is to specify a pricing measure which is preserving the Lévy property. This is called the Esscher transform (see Benth et al. [2]), and works for Lévy processes as the Girsanov transform with a constant parameter for Brownian motion. The effect of doing such a measure change is to adjust the mean reversion level, and it is known that the risk premium becomes deterministic and typically either positive or negative for all maturities along the forward curve.

We propose a class of measure changes which slows down the speed of mean reversion of the two factors. As it turns out, in conjunction with an Esscher transform as mentioned above, we can produce a stochastically varying risk premium, where potential positive premiums in the short end of the market can be traced back to sudden jumps in the spike factor being slowed down under the pricing measure. This result holds for arithmetic spot models, whereas the geometric ones are much harder to analyse under this change of probability. The class of probabilities preserves the Ornstein-Uhlenbeck structure of the factors, and as such may be interpreted as a dynamic structure preserving measure change. For the Lévy driven component, the Lévy property is lost in general, and we obtain a rather complex jump process with state-dependent (random) compensator measure.

We can explicitly describe the density process for our measure change. The theoretical contribution of this paper, besides the new insight on risk premium, is a proof that the density process is a true martingale process, indeed verifying that we have constructed a probability measure. This verification is not straightforward because the kernels used to define the density process, through stochastic exponentiation, are stochastic and unbounded. Hence, the usual criterion by Lépingle-Mémin [19] is difficult to apply and, furthermore, it does not provide sharp results. We follow the same line of reasoning as in a very recent paper by Klebaner and Lipster [18]. Although their result is more general than ours in some respects, it does not apply directly to our case because we need some additional integrability requirements. The proof is roughly as follows. First, we reduce the problem to show the uniform integrability of the sequence of random variables obtained by evaluating at the end of the trading period the localised density process. This sequence of random variables naturally induces a sequence of measure changes which, combined with an easy inequality for the logarithm function, allow us to get rid of the stochastic exponential in the expression to be bounded. Finally, we can reduce the problem to get an uniform bound for the second moment of the factors under these new probability measures.

Interestingly, as our pricing probability is reducing the speed of mean reversion, we might in the extreme situation ”turn off” the mean reversion completely (by reducing it to zero). For example, if we take the Brownian factor as the case, we can have a stationary dynamics of the ”normal variations” in the market, but when looking at the process under the pricing probability the factor can be non-stationary, that is, a drifted Brownian motion. A purely stationary dynamics for the spot will produce constant forward prices in the long end of the market, something which is not observed empirically. Hence, the inclusion of non-stationary factors are popular in modelling the spot-forward markets. In many studies of commodity spot and forward markets, one is considering a two-factor model with one non-stationary and one stationary component. The stationary part explains the short term variations, while the non-stationary is supposed to account for long-term price fluctuations in the spot (see Gibson and Schwartz [11] and Schwartz and Smith [23] for such models applied to oil markets). Indeed, the power spot models in Lucia and Schwartz [20] are of this type. It is hard to detect the long term factor in spot price data, and one is usually filtering it out from the forward prices using contracts far from delivery. Theoretically, such contracts should have a dynamics being proportional to the long term factor. Contrary to this approach, one may in view of our new results, suggest a stationary spot dynamics and introduce a pricing measure which turns one of the factors into a non-stationary dynamics. This would imply that one could directly fit a two-factor stationary spot model to power data, and next calibrate a measure change to account for the long term variations in the forward prices by turning off (or significantly slow down) the speed of mean reversion.

Our results are presented as follows: in the next section we introduce the basic assumptions and properties satisfied by the factors in our model. Then, in Section 3, we define the new change of measure and prove the main results regarding the uniform integrability of its density process. We deal with the Brownian and pure jump case separately. Finally, in Section 4, we recall the arithmetic and geometric spot price models. We compute the forward price processes induced by this change of measure and we discuss the risk premium profiles that can be obtained.

2. The mathematical set up

Suppose that is a complete filtered probability space, where is a fixed finite time horizon. On this probability space there are defined , a standard Wiener process, and a pure jump Lévy subordinator with finite expectation, that is a Lévy process with the following Lévy-Itô representation where is a Poisson random measure with Lévy measure satisfying We shall suppose that and are independent of each other. The following assumption is minimal, having in mind, on the one hand, that our change of measure extends the Esscher transform and, on the other hand, that we are going to consider a geometric spot price model.

Assumption 1.

We assume that

| (2.1) |

is strictly positive constant, which may be

Actually, to have the geometric model well defined we will need to assume later that Some remarks are in order.

Remark 2.1.

In the cumulant (or log moment generating) function is well defined and analytic. As , has moments of all orders. Also, is convex, which yields that and, hence, that is non decreasing. Finally, as a consequence of a.s., we have that is non negative.

Remark 2.2.

Thanks to the Lévy-Kintchine representation of we can express and its derivatives in terms of the Lévy measure We have that for

showing, in fact, that

Consider the OU processes

| (2.2) | ||||

| (2.3) |

with Note that, in equation is written as a sum of a finite variation process and a martingale. We may also rewrite equation as a sum of a finite variation part and pure jump martingale

where is the compensated version of . In the notation of Shiryaev [24], page 669, the predictable characteristic triplets (with respect to the pseudo truncation function ) of and are given by

and

respectively. In addition, applying Itô formula to and one can find the following explicit expressions for and

| (2.4) | ||||

| (2.5) |

where

Remark 2.3.

Using that the stochastic integral of a deterministic function is Gaussian, one easily gets that is a Gaussian process and with

3. The change of measure

We will consider a parametrized family of measure changes which will allow us to simultaneously modify the speed and the level of mean reversion in equations and . The density processes of these measure changes will be determined by the stochastic exponential of certain martingales. To this end consider the following families of kernels

| (3.1) | ||||

| (3.2) |

The parameters and will take values on the following sets where and is given by equation By Assumption and Remarks 2.1 and 2.2 these kernels are well defined.

Remark 3.1.

Under the assumption which is stronger than one can consider the set cl( and our results still hold by changing and by its left derivatives at the rigth end of

Example 3.2.

Typical examples of and are the following:

-

(1)

Bounded support: has a jump of size i.e. In this case and

-

(2)

Finite activity: is a compound Poisson process with exponential jumps, i.e., for some and In this case and

-

(3)

Infinite activity: is a tempered stable subordinator, i.e., for some and In this case also and

Next, for define the following family of Wiener and Poisson integrals

| (3.3) | ||||

| (3.4) |

associated to the kernels and respectively.

Remark 3.3.

Let be a semimartingale on and denote by the stochastic exponential of that is, the unique strong solution of

When is a local martingale, is also a local martingale. If is positive, then is also a supermartingale and In that case, one has that is a true martingale if and only If is a positive true martingale, it can be used as a density process to define a new probability measure equivalent to that is,

The desired family of measure changes is given by with

| (3.5) |

where we are implicitly assuming that is a strictly positive true martingale. Then, by Girsanov’s theorem for semimartingales (Thm. 1 and 3, p. 702 and 703 in Shiryaev [24]), the process and become

| (3.6) |

with

| (3.7) | ||||

| (3.8) | ||||

where is a -standard Wiener process and the -compensator measure of (and ) is

In conclusion, the semimartingale triplet for and under are given by and respectively.

Remark 3.4.

Under and still satisfy Langevin equations with different parameters, that is, the measure change preserves the structure of the equations. The process is not a Lévy process under , but it remains a semimartingale. Therefore, one can use Itô formula again to obtain the following explicit expressions for and

| (3.9) | ||||

| (3.10) | ||||

where

Remark 3.5.

Looking at equations and , one can see how the values of the parameters and change the drift. Setting we keep fixed the level to which the process reverts and change the speed of mean reversion by changing . If we fix the speed of mean reversion and change the level by changing By choosing , say, we observe that in (3.9) becomes (using a limit consideration in the second term)

| (3.11) |

Hence, is a drifted Brownian motion and we have a non-stationary dynamics under the pricing measure with this choice of . Obviously, we can choose and obtain similarly a non-stationary dynamics for the jump component as well, however, this will not be driven by a Lévy process under .

The previous reasonings rely crucially on the assumption that is a probability measure. Hence, we have to find sufficient conditions on the Lévy process and the possible values of the parameters and that ensure to be a true martingale with strictly positive values. As the quadratic co-variation between and is identically zero, by Yor’s formula (equation II.8.19 in [14]) we can write

| (3.12) |

and, as the stochastic exponential of a continuous process is always positive, we just need to ensure the positivity of Assume that is positive, then remark 3.3 yields that is a true martingale if and only if Using the independence of and and the identity we get

showing that is a martingale if and only if and are also martingales. Hence, we can write

where and

The previous reasonings allow us to reduce the proof that is a probability measure equivalent to , to prove that is martingale (or ) and is a martingale with strictly positive values (or ). The literature on this topic is huge, see for instance Kazamaki [17], Novikov [21], Lépingle and Mémin [19] and Kallsen and Shiryaev [16]. The main difficulty when trying to use the classical criteria is that our kernels depend on the processes and which are unbounded. To prove that is a martingale one could use a localized version of Novikov’s criterion. However, this approach would entail to show that the expectation of the exponential of the integral of a stochastic iterated integral of order two is finite. Although these computations seem feasible, they are definitely very stodgy. On the other hand, the most widely used sufficient criterion for martingales with jumps is the Lépingle-Mémin criterion. This criterion is very general but the conditions obtained are far from optimal. Using this criterion we are only able to prove the result by requiring the Lévy process to have bounded jumps.

In a very recent paper, assuming some structure on the processes, Klebaner and Lipster [18] give a fairly general criterion which seems easier to apply than those of Novikov and Lépingle-Mémin. Although we can not apply directly their criteria, at least not in the pure jump case, we can reason similarly to prove the desired result for and

Finally, note that these results can be extended, in a straightforward manner, to any finite number of Langevin equations driven by Brownian motions and Lévy processes, independent of each other. In the following two subsections, we will drop the subindices in the parameters and

3.1. Brownian driven OU-process

We first show that the process is a martingale under .

Proposition 3.6.

Let and . Then, , defined by is a square integrable martingale under .

Proof.

We have to show that We get

By remark 2.3 and the properties of the Gaussian distribution, one has

because and are continuous functions on ∎

Theorem 3.7.

Let and . Then is a martingale under

Proof.

As is a martingale with continuous paths, we have that is a positive local martingale. By remark 3.3, it suffices to prove that Note that the sequence of stopping times is a reducing sequence for That is, converges a.s. to and, for every fixed, the stopped process is a (bounded) martingale on . Therefore, and if we show that

| (3.13) |

we will have finished. To show is equivalent to show the uniform integrability of the sequence of random variable that is, to show

It is not difficult to prove that if is a non-negative function such that and

then is uniformly integrable. We consider the test function Hence, it suffices to prove that

| (3.14) |

Note that we can use the sequence of martingales on given by to define a sequence of probability measures with Radon-Nykodim densities given by In addition, one has that

| (3.15) | ||||

where On the other hand, from we have the trivial bound Combining the last bound with the change of measure given by we get that

| (3.16) |

implies that holds. Applying Girsanov’s Theorem, we can write

where is a -Brownian motion. Therefore, it suffices to prove that

| (3.17) |

because this imply that is a -martingale with zero expectation and, in passing, that holds. Now we proceed as in the proof of Proposition 3.6. We have that

but now the term with is more delicate to treat. Using Remark 2.3, we know that conditioned to is Gaussian, but we do not know the distribution of and, hence, a direct computation of is not possible. However, we have that

where we have used that the function for and that

Hence, we have shown and the result follows. ∎

3.2. Lévy driven OU-processes

First we will prove that is a square integrable martingale.

Proposition 3.8.

Let . Then defined by , is a square integrable martingale under

Proof.

According to Ikeda-Watanabe [13], p. 59-63, we have to check that We can write

By the mean value theorem in integral form we have that Hence, as

Therefore, the result follows by showing that We have that

∎

Note that the stochastic exponential satisfies the following SDE

and it can be represented explicitly as

| (3.18) | ||||

Hence, a necessary and sufficient condition for the positivity of is that up to an evanescent set. Moreover, by the definition of and we have that

| (3.19) |

which yields the condition

| (3.20) |

Remark 3.9.

As we assume that is a subordinator and and , we have that , condition is automatically satisfied and is strictly positive.

Theorem 3.10.

Let and Then is a martingale under .

Proof.

As is a martingale on , we have that is a local martingale on Hence, there exists a sequence of increasing stopping times such that - and the stopped processes are martingales on . By Remark 3.3 and the same reasonings as in the proof of Theorem 3.7, to show that is a martingale is equivalent to show that and this is equivalent to prove that the sequence is uniformly integrable. A sufficient condition for the uniform integrability of is given by

| (3.21) |

By equation , we get

because the function for Hence, we can write

| (3.22) |

where we have used that for any stopping time the process is a -martingale with zero expectation. In addition, we have used that fixed, and

because is a reducing sequence for the local martingale One can reason as in the proof of Proposition 3.8 to show that the terms and in equation are finite. Note that thus, it just remains to prove that

to finish the proof. As is a strictly positive martingale, by Remark 3.9, we can define the probability measure by setting and, hence, it suffices to prove that Using Girsanov’s Theorem with the process can be written as

where

and is the compensated version of the random measure with -compensator given by Hence,

On the one hand,

On the other hand,

To sum up, where

and applying Gronwall’s lemma to the function we get that

| (3.23) |

Finally, using Fubini-Tonelli and inequality we obtain

and the proof is finished. ∎

Remark 3.11.

If has finite activity, that is then one can use the kernel

and the Poisson integral

to define the change of measure. The results in Proposition 3.8 and Theorem 3.10, below, also hold. Note that the change of measure with does not work for the infinite activity case. This is because, in the analogous proofs of the statements in Proposition 3.8 and Theorem 3.10 using the change of measure induced by it appears the integral which is divergent if

4. Study of the risk premium

We are interested in applying the previous probability measure change to study the risk premium in electricity markets. As we discussed in the Introduction, there are two reasonable models for the spot price in this market: the arithmetic and the exponential model. We define the arithmetic spot price model by

| (4.1) |

and the geometric spot price model by

| (4.2) |

where is a fixed time horizon. The processes and are assumed to be deterministic and they account for the seasonalities observed in the spot prices.

One of the particularities of electricity markets is that power is a non storable asset and for that reason is not a directly tradeable asset. This entails that one can not derive the forward price of electricity from the classical buy-and-hold hedging arguments. Using a risk-neutral pricing argument (see Benth, Šaltytė Benth and Koekebakker [2]), under the assumption of deterministic interest rates, the forward price, with time of delivery at time is given by where is any probability measure equivalent to the historical measure and is the market information up to time . In what follows we will use the probability measure discussed in the previous sections. However, in electricity markets, the delivery of the underlying takes place over a period of time where We call such contracts swap contracts and we will denote their price at time by

We can use the stochastic Fubini theorem to relate the price of forwards and swaps

The risk premium for forward prices is defined by the following expression and for swap prices by

| (4.3) |

In order to compute the previous quantities we need to know the dynamics of (that is, of and ) under and under Explicit expressions for and under are given in equations and respectively. In the rest of the paper, defined in and the explicit expressions for and under are given in Remark equations and respectively.

Remark 4.1.

We will use the subindices and to denote the arithmetic and the geometric spot models, respectively. That is, we will use the notation and

Remark 4.2.

In the discussion to follow, we are interested in finding values of the parameters such that some empirical features of the observed risk premium profiles are reproduced by our pricing measure. In particular, we show that is possible to have the sign of the risk premium changing stochastically from positive values on the short end of the market to negative values on the long end. This is proved for forward contracts in, both, the arithmetic and geometric model. Equation just tell us that the risk premium for swaps becomes the average of the risk premium for forwards with fixed-delivery. Hence, we can obtain stochastic sign change also for these, depending on the length of delivery. Worth noticing is that contracts in the short end have short delivery (a day, or a week), while in the long end have month/quarter/year delivery. Average for negative is negative, for the long end, and average over short period, dominantly positive, gives positive, in the short end.

4.1. Arithmetic spot price model

We assume in this section that the spot price is given by the dynamics (4.1) for , , with the maturity time of the forward contract satisfying Using equations and and the basic properties of the conditional expectation we get

Note that we have also used that and have independent increments under to write conditional expectations as expectations. If we assume that then

This last expression for is considerably simpler and depends explicitly on the spot price at time which is directly observable in the market.

To find a similar expression for we need the following lemma.

Lemma 4.3.

We have that is a -martingale on

Proof.

We have to prove that One has that

and because The proof that is finite follows the same lines as the last part of Theorem 3.10. Using the semimartingale representation of equation we obtain that there exist constants and such that Applying Gronwall’s Lemma we get that and the result follows. ∎

Remark 4.4.

We need the previous lemma because Girsanov’s Theorem just ensures that

| (4.4) |

is a -local martingale. We want to be a -martingale because then it follows trivially that

Note that we can not reduce the previous conditional expectation (unless which coincides with the Esscher change of measure) to an expectation because the compensator of depends on and, therefore, does not has independent increments.

Using the basic properties of the conditional expectation, Remark 4.4 and equations and we get

Therefore, we have proved the following result.

Proposition 4.5.

The forward price in the arithmetic spot model (4.1) is given by

In Lucia and Schwartz [20] a two-factor model (among others) is proposed as the dynamics for power spot prices in the Nordic electricity market NordPool. Following the model of Schwartz and Smith [23], they consider a non-stationary long term variation factor together with a stationary short term variation factor. In our context, one could let the mean reversion in be zero, to obtain a non-stationary factor as a drifted Brownian motion under the pricing measure . After doing a measure transform with , we can price forwards as in Proposition 4.5 to find

When becomes large, i.e. when we are far out on the forward curve, we see that

| (4.5) |

Thus, the forward curve moves stochastically as the non-stationary factor . If one, on the other hand, let be stationary, we find that the forward price in Proposition 4.5 will behave for large time to maturities as

The forward prices becomes constant after subtracting the seasonal function, with no stochastic movements. This is not what is observed for forward data in the market. However, following the empirical study in Barndorff-Nielsen, Benth and Veraart [1], electricity spot prices on the German power exchange EEX are stationary. One way to have a stationary spot dynamics, and still maintain forward prices which moves randomly in the long end, is to apply our measure change to slow down the mean reversion in one or more factors of the (stationary) spot. In the extreme case, we can let , and obtain a non-stationary factor under the pricing measure, in which case we obtain the same long term asymptotic behaviour as in the generalization of the Lucia and Schwartz model (4.5). In conclusion, our pricing measure allows for a stationary spot dynamics and a forward price dynamics which is not constant in the long end.

Let us return back to the risk premium, which in view of Prop. 4.5 becomes:

Proposition 4.6.

The risk premium for the forward price in the arithmetic spot model is given by

We analyse different cases for the risk premium in the next subsection.

4.1.1. Discussion on the risk premium

The first remarkable property of this measure change is that, as long as the parameter the risk premium is stochastic. This might be a desirable feature in view of the discussion in the Introduction where we referred to the economical and empirical evidence in Geman and Vasicek [10], Bessembinder and Lemon [5] and Benth, Cartea and Kiesel [3]. Note that when our measure change coincides with the Esscher transform (see Benth, Šaltytė Benth and Koekebakker [2]). In the Esscher case, the risk premium has a deterministic evolution given by

| (4.6) |

an already known result, see Benth and Sgarra [4].

Another interesting feature of the empirical risk premium is that its sign might change from positive to negative when the time to maturity increases. Hence, we are interested in theoretical models that allow to reproduce such empirical property. From now on we shall rewrite the expressions for the risk premium in terms of the time to maturity and, slightly abusing the notation, we will write instead of We fix the parameters of the model under the historical measure i.e., and and study the possible sign of in terms of the change of measure parameters, i.e., and and the time to maturity Note that the present time just enters into the picture through the stochastic components and We are going to assume This assumption is justified, from a modeling point of view, because we want the processes and to revert toward zero. In this way, the seasonality function accounts completely for the mean price level. On the other hand it is also reasonable to expect that which means that the component accounting for the jumps reverts the fastest (e.g., being the factor modelling the spikes). The factor is referred to as the base component, modelling the normal price variations when the market is not under particular stress. The expression for given in Proposition 4.6 allows for a quite rich behaviour. We are going to study the cases and the general case separately. Moreover, in order to graphically illustrate the discussion we plot the risk premium profiles obtained assuming that the subordinator is a compound Poisson process with jump intensity and exponential jump sizes with mean That is, will have the Lévy measure given in Example 3.2. We shall measure the time to maturity in days and plot for roughly one year. We fix the values of the following parameters

The speed of mean reversion for the base component yields a half-life of seven days, while the one for the spikes yields a half-life of two days (see e.g., Benth, Saltyte Benth and Koekebakker [2] for the concept of half-life). The values for and give jumps with mean and frequency of spikes a month.

The following lemma will help us in the discussion to follow.

Lemma 4.7.

If and we have that the risk premium satisfies

| (4.7) | ||||

where

is a non-negative function. Moreover,

| (4.8) | ||||

| (4.9) |

Proof.

It follows trivially from Proposition 4.6 and the assumptions on the coefficients and ∎

Remark 4.8.

The previous Lemma shows that the risk premium vanishes with rate given by equation at the short end of the forward curve, when converges to zero, and approaches the value given in equation at long end of the forward curve, when tends to infinity. It follows that the sign of in the short end of the forward curve will be positive if is positive and negative if is negative. Hence, a sufficient condition to obtain the empirically observed risk premium profiles (with positive values in the short end and negative values in the long end of the forward curve) is to choose the values of the parameters and such that the following two conditions are simultaneously satisfied

We also recall here that, according to Remark 2.2, is positive, increasing function, so the sign of is equal to the sign of Moreover, it is easy to see that

-

•

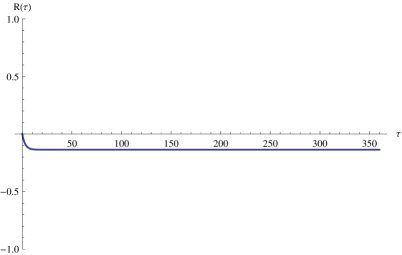

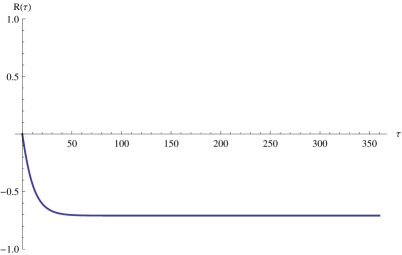

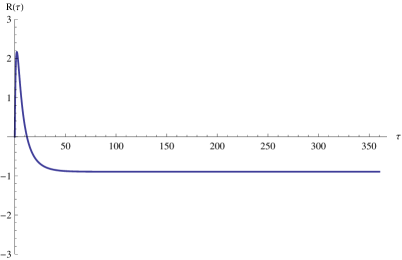

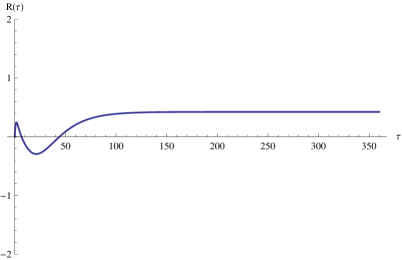

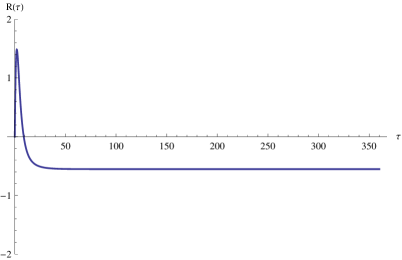

Changing the level of mean reversion (Esscher transform), Setting the probability measure only changes the level of mean reversion (which is assumed to be zero under the historical measure ). On the other hand, the risk premium is deterministic and cannot change with changing market conditions. From equation we get that if we set which means that we just change the level of the regular factor the sign of is the same for any time to maturity and it is equal to the sign of see Figures 1(a) and 1(b). The situation is similar if we set then the sign of is constant over the time to maturity end equal to the sign of that is to the sign of see Figures 1(c) and 1(d).

(a)

(b)

(c)

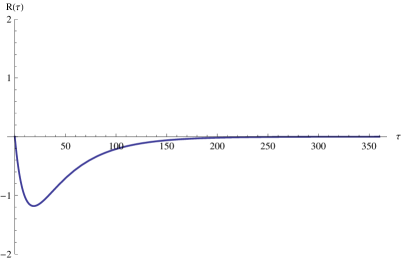

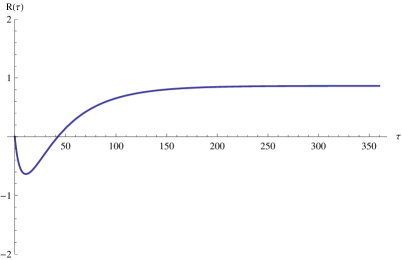

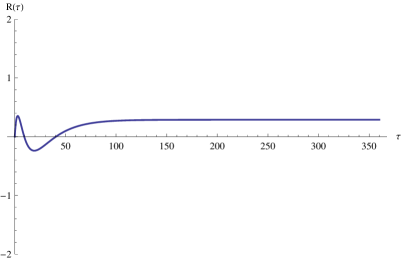

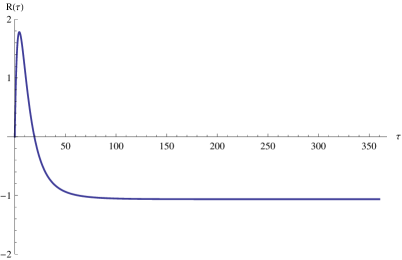

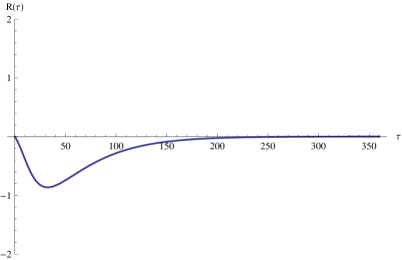

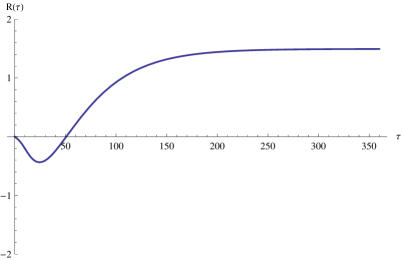

(d) Figure 2. Risk premium profiles when is a compound Poisson process with exponentially distributed jumps. Esscher transform: case Arithmetic spot price model When both and are different from zero the situation is more interesting, the sign of may change depending on the time to maturity. By Remark 4.8 it suffices to choose and satisfying

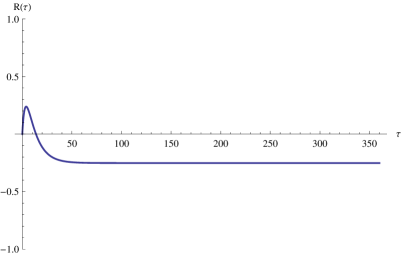

(4.10) (4.11) (these exist because and is increasing) to get that for close to zero and for large enough, see Figure 2(a). This corresponds to the situation of a premium induced from consumers’ hedging pressure on short-term contracts and long term hedging of producers. We can also choose values for and such that equations 4.10 and 4.11 are satisfied but with inverted inequalities. In this way, we can get that for close to zero and for large enough, see Figure 2(b). Risk premium profiles with constant sign can also be generated, see Figures 2(c) and 2(d).

-

•

Changing the speed of mean reversion, Setting the probability measure only changes speed of mean reversion. Note that in this case the risk premium is stochastic and it changes with market conditions. By Lemma 4.7 we have that the risk premium is given by

and

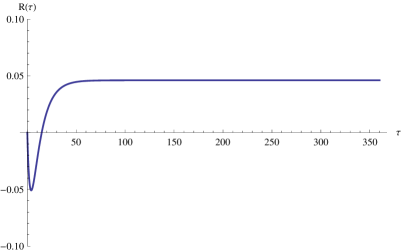

Hence the risk premium will approach to a non negative value in the long end of the market. In the short end, it can be both positive or negative and stochastically varying with and but will always contribute to a positive sign. Actually, as the function is non-negative and is strictly positive, the only negative contribution to comes from the term due to the base component . Hence, if or then will be positive for all times to maturity. Some of the possible risk profiles that can be obtained are plotted in Figure 3.

(a)

(b)

(c)

(d) Figure 3. Risk premium profiles when is a compound Poisson process with exponentially distributed jumps. Case Arithmetic spot price model

(a) Figure 4. Risk premium profiles when is a compound Poisson process with exponentially distributed jumps. Arithmetic spot price model -

•

Changing the level and speed of mean reversion simultaneously: The general case is quite complex to analyse. As we are more interested in how the change of measure influence the component , responsible for the spikes in the prices, we are going to assume that This means that may change the level of mean reversion of the regular component but not the speed at which this component reverts to that level. The first implication of this assumption is that the possible stochastic component in due to vanish. This simplifies the analysis as this term could be positive or negative. By Lemma 4.7 we get that

and

(4.12) (4.13) Note that we can make equation negative by simply choosing

(4.14) On the other hand, to make equation positive, we have to choose satisfying

(4.15) Equations and are compatible if the following inequality is satisfied

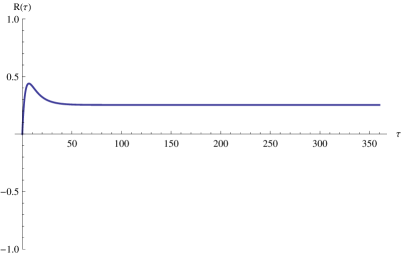

(4.16) For any which yields (and ), we have that there exists such that if equation is satisfied. Actually, the larger the value of the larger the value of . If is close to then is close to This just says that if the speed of mean reversion of the spikes component is large (in absolute value and relatively to the speed of mean reversion of the base component) one can choose close to one. Even in the case that , equation is satisfied by choosing small enough. To sum up, we can create a measure that can have a positive premium in the short end of the forward market due to sudden positive spikes in the price (that is, increases), whereas in the long end of the market these spikes are not influential and we have a negative premium, see Figure 4.

4.2. Geometric spot price model

We assume in this section that the spot price follows the geometric model for , and with the maturity of the forward contract being . In our setting, the geometric model is harder to deal with than the arithmetic one. The results obtained are fair less explicit and some additional integrability conditions on are required. A first, natural, additional assumption on is that the constant appearing in Assumption 1 to be bigger than This condition is reasonable to expect because it just states that for all , and if we want to be finite it seems a minimal assumption. Note, however that this is not entirely obvious because the process has a mean reversion structure that does not have. On the other hand, the complex probabilistic structure of the spike factor under the new probability measure makes the computations much more difficult. Still, it is possible to compute the risk premium analytically in some cases. In general, one has to rely on numerical techniques.

In what follows, we shall compute the conditional expectations involved under (note that when ). First, we show that the problem can be reduced to the study of the spike component Due to the independence of and we have that

which is finite if and only and As is a Gaussian random variable it has finite exponential moments. To determine whether is finite or not is not as straightforward. Let us assume, for now, that it is finite. Then, it makes sense to compute the following conditional expectation

Using , the fact that is independent of and basic properties of the conditional expectation we get that

Hence, we have reduced the problem to the study of

Let us start with the Esscher case with and We have that

where we have used that the compensator of under is (note that is a Lévy measure) and Proposition 3.6 in Cont and Tankov [8]. Of course, the previous result holds as long as the integral in the exponential is finite. A sufficient condition for the integrability of follows from

As to have yields the condition

Note that for to be strictly positive and, therefore, include the case , we need to have This, of course, is a restriction on the structure of the jumps. For instance, if is a compound Poisson process with exponentially distributed jump sizes, Example 3.2 (Case 2), we have that the jump sizes must have a mean less than one. Note also that, if then

Using expression and repeating the previous arguments we obtain

Hence we have proved the following result:

Proposition 4.9.

In the Esscher case for the spike component , i.e., , and assuming the forward price in the geometric spot model is given by

and the risk premium for the forward price is given by

where is also understood under the assumption

Corollary 4.10.

Setting in Proposition 4.9 we get

The previous result is as far as one can go using ”basic” martingale techniques. In the general case, in order to find conditions under which , and also to compute it is convenient to look at as an affine -semimartingale process with state space . In the sequel we follow the notation in Kallsen and Muhle-Karbe [15], but taking into account that in our case the Lévy characteristics do not depend on the time parameter. The Lévy-Kintchine triplets of are

which, according to Definition 2.4 in Kallsen and Muhle-Karbe [15], are (strongly) admissible. Note that, as the triplets do not depend on we can choose any truncation function. Moreover, as is a special -semimartingale, we choose the (pseudo) truncation function Associated to the previous Lévy-Kintchine triplets we have the following Lévy exponents

We have the following result.

Theorem 4.11.

Let . Assume that satisfy the ODE

| (4.17) |

and that the integrability condition

| (4.18) |

holds. Then, we have that the forward price in the geometric spot model is given by

and the risk premium for the forward price is given by

Proof.

We apply Theorem 5.1 in Kallsen and Muhle-Karbe [15]. Note that making the change of variable the ODE is reduced to the one appearing in items 2. and 3. of Theorem 5.1. The integrability assumption implies conditions 1. and 5., in Theorem 5.1, and condition 4. is trivially satisfied because is deterministic. Hence, the conclusion of that theorem, with holds and we get

| (4.19) |

The result now follows easily. ∎

Remark 4.12.

Equation is called a generalised Riccati equation in the literature. Note that the equation for is trivially solved, once we know by

Hence, the problem is really reduced to study the equation for

Remark 4.13.

The Esscher case can be obtained from Theorem 4.11, as and

solve

As the integrability condition is satisfied because

In general, one cannot find explicit solutions for the non-linear differential equation in Theorem 4.11 and has to rely on numerical techniques. However, the main problem that we find is that the maximal domain of definition of and may be a proper subset of in particular when is close to . As we are particularly interested in the solution of for large , we shall give a general sufficient criterion for global (defined for any ) existence and uniqueness of the solution of . The next theorem classifies the behaviour of the solutions of .

Theorem 4.14.

Assume that For any the system of ODEs (4.17) with and

admits a unique local solution and . In addition, let be the unique strictly positive solution of the following equation

| (4.20) |

The behaviour of and is characterised as follows:

-

(1)

If then and are globally defined, satisfy

and

(4.21) (4.22) -

(2)

If then and

-

(3)

If , then the maximal domain of definition of and is where

In addition,

where the previous integral is non negative and may be finite or infinite.

Proof.

We have to study the vector field

Consider

and, for any define

On the other hand, for one has that

and

Moreover, note that

Hence, the vector field is well defined (i.e., finite) and locally Lipschitz in As the initial condition for is , it is natural to require that and this is precisely the role of Then, by Picard-Lindelöf Theorem, see Theorem 3.1, pag. 18, in Hale [12], we have local existence and uniqueness for and In addition, we have that and, hence, we have local existence and uniqueness for solutions of with As we have that is the unique global solution of equation starting at 0. As a consequence, it is sufficient to study the vector field for because any solution of equation with cannot cross to the negative real line without contradicting the uniqueness result at The unicity of trivially follows from that of The next step is to study the zeros of We have to solve the non-linear equation

| (4.23) |

Note that equation has the trivial solution As the first and second derivatives of are

we have that there exists a unique for and such that equation is satisfied. Moreover for and for When converges to On the other hand, when converges to zero. Therefore, we have three possible cases to discuss

-

•

Case If then will monotonically converge to and, by uniqueness of solutions, it will take an infinite amount of time to reach Hence, will be a globally defined bounded solution. The exponential rate of convergence of to zero, equation 4.21, follows by applying Hôpital’s rule to

It follows that will be also globally defined and, as for by monotone convergence

To show that the previous integral is actually finite, it suffices to prove that converges to zero faster than for some when tends to infinity. We have that

and

By Hôpital’s rule and equation

and we can conclude that equation holds.

-

•

Case If then will be the unique global solution and

-

•

Case If then will increase monotonically to because the vector field is strictly positive in . Separating variables an integrating the equation for with we get that the maximal domain of definition of is with

To show that is actually finite we have to distinguish between the case and If then is bounded in and the integral is obviously finite. If we have to ensure that converges to zero fast enough when tends to infinity. Note that, by monotone convergence, one has that

For any we have that

which yields that the integral defining is finite. According to Remark 4.12, we have that

(4.24) which may be finite or infinite depending, of course, on how fast diverges to infinity when approaches to

∎

As it does not seem possible to give simple conditions for the finiteness (or not) of the integral and it is not relevant in the discussion to follow, we do not proceed further in the analysis.

Remark 4.15.

If then and

Obviously and

Note that

If we have that

for which yields that and monotonically diverges to infinity.

Although the previous result characterizes the behaviour of the solution of the ODE for different values of in terms of usually one cannot find analytically and, given equation must be solved numerically to know whether the solution associated to equation is bounded or not. Hence, the following corollary of Theorem 4.14 may be helpful in practice.

Corollary 4.16.

Under the hypothesis of Theorem 4.14 and for fixed, a sufficient condition for is that

| (4.25) |

Proof.

Assume fixed. According to the discussion in the proof of Theorem 4.14, for any and there exists a unique root of the vector field defined by equation and such that if and if Now, note that

is such that If one has that

which yields that the unique root of the vector field must be strictly greater than one and, therefore, we are in the case (1) of Theorem 4.14. ∎

Next, we present two examples where we apply the previous results.

Example 4.17.

We start by the simplest possible case. Assume that the Lévy measure is that is, the Lévy process has only jumps of size In this case and, hence, We have that and Therefore,

First, we have to solve

| (4.26) | ||||

and then integrate from to Although equation can be solved analytically, its solution is given in implicit form and a numerical method is easier to use. In this example, equation reads

| (4.27) |

which can only be solved numerically. Heuristically, if is close to one the solution of the previous equation must be close to zero and, hence, the solution diverges to Applying Corollary 4.16 we can guarantee that converges to zero if

Example 4.18.

Assume that the Lévy measure is that is, is a compound Poisson process with intensity and exponentially distributed jumps with mean In this case and, hence, We have that and Therefore,

Hence, we have to solve

and then integrate from to As in the previous example, there is an analytic solution to this equation in implicit form, but it is easier to use a numerical method. In this example, equation reads

which has roots

We are just interested in the root note that The inequality yields

| (4.28) |

Hence, for any and satisfying we can ensure global existence and boundedness of and .

4.2.1. Discussion on the risk premium

For the study of the sign change we are going to abuse the notation, as in the arithmetic spot price model, and we will denote where is the time to maturity. We also fix the parameters of the model under the historical measure i.e., and and study the possible sign of in terms of the change of measure parameters, i.e., and and the time to maturity As in the arithmetic model, the present time just enters into the picture through the stochastic components and We are also going to assume Analogously to the arithmetic case, in this way the seasonality function accounts completely for the mean price level. We also assume that which means that the component accounting for the jumps reverts the fastest. Finally, in the sequel, we are going to assume that we are in the Case 1 of Theorem 4.14, i.e., the values are such that and and are globally defined and the exponential affine formula holds.

The following lemma will help us in the discussion to follow.

Lemma 4.19.

If and we have that the sign of the risk premium will be the same as the sign of

| (4.29) | ||||

where is the (non-negative) function defined in Lemma 4.7. Moreover,

| (4.30) | ||||

| (4.31) | ||||

Proof.

The result follows easily from Theorem 4.11 and the following computations with and . We have that

and

In Theorem 4.14, it is proved that converges to when tends to infinity and

Hence, using the definitions of and the fact that and we get

∎

The sign of is more complex to analyse than the sign of the risk premium in the arithmetic model. In the Esscher case the computations can be done quite explicitly. In the general case we shall make use of Lemma 4.19 to prove that one can generate the empirically observed risk premium profile. Moreover, some additional information on can be deduced from classical results on comparison of solutions of ODEs. In order to graphically illustrate the discussion we plot the risk premium profiles obtained assuming that the subordinator is a compound Poisson process with jump intensity and exponential jump sizes with mean That is, will have the Lévy measure given in Example We shall measure the time to maturity in days and plot for roughly one year. We fix the values of the following parameters

The speed of mean reversion for the base component yields a half-life of seven days, while the one for the spikes yields a half-life of two days. The value for yields an annualised volatility of . The values for and give jumps with mean and frequency of spikes a month.

-

•

Changing the level of mean reversion (Esscher transform), Setting the probability measure only changes the level of mean reversion (which is assumed to be zero under the historical measure ). Moreover, as is deterministic when we have that the randomness in comes into the picture through in particular through the levels of the driving factors and By Proposition 4.9 we have that

and the sign of is the same as the sign of

which is equal to in Lemma 4.19.

(a)

(b)

(c)

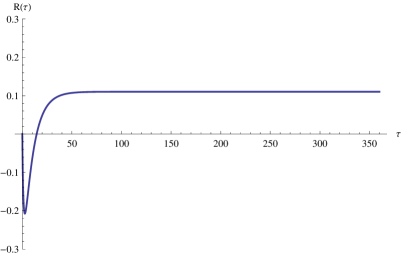

(d) Figure 5. Risk premium profiles when is a compound Poisson process with exponentially distributed jumps. Esscher transform: case Geometric spot model If then the sign of is the same as the sign of and it is constant over all times to maturity Similarly, if the sign is the same as the sign of and it is also constant. If both and are different from zero we can get risk premium profiles with non constant sign. By Lemma 4.19, we have that

Hence, if we want the sign of to be positive when is close to zero we have to impose

(4.32) For large times to maturity, Lemma 4.19 yields

Using Fubini’s theorem we get that

where is the exponential integral function and is the Euler-Mascheroni constant. Hence, if we want to be negative when is large we have to impose

(4.33) Note that and for all and Therefore, for all one has that

(4.34) Combining equations , and we can conclude that it is possible to choose and such that when the time to maturity is close to zero and when the time to maturity is large.

-

•

Changing the speed of mean reversion, Setting the probability measure only changes the speed of mean reversion. By Lemma 4.19 we have that the sign of will coincide with the sign of

and

(a)

(b)

(c)

(d) Figure 6. Risk premium profiles when is a compound Poisson process with exponentially distributed jumps. Case Geometric spot price model where and are strictly positive. Hence the risk premium will approach to a non negative value in the long end of the market. In the short end, it can be both positive or negative and stochastically varying with and but will always contribute to a positive sign. For any the sign of will be the sign of that can be positive or negative. As the function is positive, the term is always positive. To analyse the sign of note that

and Hence, applying a comparison theorem for ODEs, see Theorem 6.1, pag.31, in Hale [12], we have that for all and, as is always positive, the term is also always positive. Finally, as

is an strictly increasing function and we get that

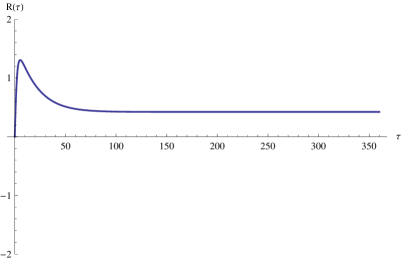

Hence, if or then will be positive for all times to maturity. Some of the possible risk profiles that can be obtained are plotted in Figure 6.

-

•

Changing the level and speed of mean reversion simultaneously: We proceed as in the arithmetic case. As we are more interested in how the change of measure influence the component , responsible for the spikes in the prices, we are going to assume that This means that may change the level of mean reversion of the regular component but not the speed at which this component reverts to that level. According to Lemma 4.19 we have that the sign of will coincide with the sign of

and

(4.35) (4.36)

(a) Figure 7. Risk premium profiles when is a compound Poisson process with exponentially distributed jumps. Geometric spot model Note that we can make equation negative by simply choosing

(4.37) On the other hand, to make equation positive, we have to choose satisfying

(4.38) Equations and are compatible if the following equation is satisfied

(4.39) As and we have that

and

As converges to zero exponentially fast, see equation , we have that

Actually, as we can use a comparison theorem for ODEs to obtain that

which yields

Hence,

and if we can find for some and such that then equation will be satisfied. Note that the larger the value of the easier to find such and Even in the case that by choosing close to zero and large enough we can get This shows that we can create a change of measure generating the empirically observed risk premium profile, see Figure 7.

References

- [1] Barndorff-Nielsen, O.E., Benth, F.E., and Veraart, A. (2010). Modelling energy spot prices by volatility modulated Levy-driven Volterra processes. Bernoulli 19 (3), pp. 803–845.

- [2] Benth, F.E., Šaltytė Benth, J. and Koekebakker, S. (2008). Stochastic Modelling of Electricity and Related Markets. World Scientific.

- [3] Benth, F.E., Cartea, A., and Kiesel, R. (2008). Pricing forward contracts in power markets by the certainty equivalence principle: explaining the sign of the market risk premium. Journal of Banking and Finance, 32(10), pp. 2006–2021.

- [4] Benth, F.E. and Sgarra, C. (2012). The Risk Premium and the Esscher Transform in Power Markets. Stochastic Analysis and Applications 30, pp. 20–43.

- [5] Bessembinder, H., and Lemon, M.L. (2002). Equilibrium pricing and optimal hedging in electricity forward markets. Journal of Finance, 57, pp. 1347–1382.

- [6] Bingham, N., and Kiesel, R. (1998). Risk-Neutral Valuation. Pricing and Hedging of Financial Derivatives. Springer-Verlag.

- [7] Cartea, A., and Figueroa, M.G. (2005). Pricing in electricity markets: a mean reverting jump diffusion model with seasonality. Applied Mathematical Finance, 12(3), pp. 313–335.

- [8] Cont, R. and Tankov, P. (2004). Financial Modelling with Jump Processes. Chapman & Hall/CRC

- [9] Geman, H. (2005). Commodities and Commodity Derivatives. Wiley-Finance.

- [10] Geman, H., and Vasicek, O. (2001). Forwards and futures on non storable commodities: the case of electricity. RISK, August.

- [11] Gibson, R., and Schwartz, E.S. (1990). Stochastic convenience yield and the pricing of oil contingent claims. Journal of Finance, 45, pp. 959–976.

- [12] Hale, J. (1969). Ordinary Differential Equations, Pure and Applied Mathematics, Vol. XXI. Wiley-Interscience.

- [13] Ikeda, N. and Watanabe, S. (1981). Stochastic Differential Equations and Diffusion Processes, North-Holland.

- [14] Jacod, J. and Shiryaev, A.N. (2003). Limit Theorems for Stochastic Processes, Springer.

- [15] Kallsen, J. and Muhle-Karbe J. (2010). Exponentially affine martingales, affine measure changes and exponential moments of affine processes. Stochastic Processes and their Applications 120, pp. 163–181.

- [16] Kallsen, J. and Shiryaev, A. (2002). The cumulant process and Esscher’s change of measure. Finance & Stochastics 6, pp. 397–428.

- [17] Kazamaki, N. (1977). On a problem of Girsanov. Tôhoku Math. J. 29 (4), pp. 597–600.

- [18] Klebaner, F. and Lipster, R. (2011). When a stochastic exponential is a true martingale. Extension of a method of Beneŝ. arXiv:1112.0430v1.

- [19] Lepingle, D. and Mémin, J. (1978). Sur l’intégrabilité uniforme des martingales exponentielles, Z. Wahrscheinlichkeitstheorie verw. Gebiete 42, pp. 175–203.

- [20] Lucia, J., and Schwartz, E.S. (2002). Electricity prices and power derivatives: evidence from the Nordic power exchange. Review of Derivatives Research, 5(1), pp. 5–50.

- [21] Novikov, A. (1980). On conditions for uniform integrability of continuous non-negative martingales. Theory of Probability and its Applications 24, pp. 820–824.

- [22] Sato, K. (1999). Lévy Processes and Infinitely Divisible Distributions. Cambridge Studies in Advanced Mathematics.

- [23] Schwartz, E.S., and Smith, J.E. (2000). Short-term variations and long-term dynamics in commodity prices. Management Science, 46(7), pp. 893–911.

- [24] Shiryaev, A. N. (1999). Essentials of Stochastic Finance, World Scientific.