American options with gradual exercise under proportional transaction costs

Abstract

American options in a multi-asset market model with proportional transaction costs are studied in the case when the holder of an option is able to exercise it gradually at a so-called mixed (randomised) stopping time. The introduction of gradual exercise leads to tighter bounds on the option price when compared to the case studied in the existing literature, where the standard assumption is that the option can only be exercised instantly at an ordinary stopping time. Algorithmic constructions for the bid and ask prices and the associated superhedging strategies and optimal mixed stoping times for an American option with gradual exercise are developed and implemented, and dual representations are established.

1 Introduction

This work on pricing American options under proportional transaction costs goes back to the seminal discovery by Chalasani & Jha (2001) that to hedge against a buyer who can exercise the option at any (ordinary) stopping time, the seller must in effect be protected against all mixed (randomised) stopping times. This was followed by Bouchard & Temam (2005), who established a non-constructive dual representation for the set of strategies superhedging the seller’s (though not the buyer’s) position in an American option under transaction costs. Efficient iterative algorithms for computing the upper and lower hedging prices of the option, the hedging strategies, optimal stopping times as well as dual representations for both the seller and the buyer of an American option under transaction costs were developed by Roux & Zastawniak (2009) in a model with two assets, and Roux & Zastawniak (2011) in a multi-asset model. All these approaches take it for granted that the buyer can only exercise the option instantly, at an ordinary stopping time of his choosing.

By contrast, in the present paper we allow the buyer the flexibility to exercise an American option gradually, rather than all at a single time instance. Though it would be difficult in practice to exercise a fraction of an option contract and to hold on to the reminder to exercise it later, the holder of a large portfolio of options may well choose to exercise the individual contracts on different dates if that proves beneficial. Does this ability to exercise gradually affect the pricing bounds, hedging strategies and optimal stopping times for the buyer and/or seller? Perhaps surprisingly, the answer to this question is yes, it does in the presence of transaction costs.

Gradual exercise turns out to be linked to another feature, referred to as deferred solvency, which will also be studied here. If a temporary loss of liquidity occurs in the market, as reflected by unusually large bid-ask spreads, agents may become insolvent. Being allowed to defer closing their positions until liquidity is restored might enable them to become solvent once again. This gives more leeway when constructing hedging strategies than the usual requirement that agents should remain solvent at all times.

Tien (2012) was the first to explore the consequences of gradual exercise and deferred solvency using a model with a single risky asset as a testing ground. In the present paper these ideas are developed in a systematic manner and extended to the much more general setting of the multi-asset market model with transaction costs due to Kabanov (1999); see also Kabanov & Stricker (2001) and Schachermayer (2004).

Pricing and hedging for the seller of an American option under transaction costs is a convex optimisation problem irrespective of whether instant or gradual exercise is permitted. However, this is not so for the buyer. In this case one has to tackle a non-convex optimisation problem for options that can only be exercised instantly. A very interesting consequence of gradual exercise is that pricing and hedging becomes a convex optimisation problem also for the buyer of an American option, making it possible to deploy convex duality methods. The convexity of the problem also makes it much easier to implement the pricing and hedging algorithms numerically. We will make use of this new opportunity in this paper.

The paper is organised as follows. Section 2 recalls the general setting of Kabanov’s multi-asset model with transaction costs. In Section 3 the hedging strategies for the buyer and seller and the corresponding option prices under gradual exercise are introduced and compared with the same notions under instant exercise. A toy example is set up to demonstrate that it is easier to hedge an option and that the bid-ask spread of the option prices can be narrower under gradual exercise as compared to instant exercise. In Section 4 the seller’s case is studied in detail. The notion of deferred solvency is first discussed and linked in Proposition 4.8 with the hedging problem for the seller of an American option with gradual exercise. The sets of seller’s hedging portfolios are then constructed and related to the ask price of the option under gradual exercise and to a construction of a seller’s hedging strategy realising the ask price; see Theorem 4.14. A dual representation of the seller’s price is established in Theorem 4.20. The toy example is revisited to illustrate the various constructions and results for the seller. Section 5 is devoted to the buyer’s case. Buyer’s hedging portfolios and strategies are constructed and used to compute the bid price of the option; see Theorem 5.7. Finally, the dual representation for the buyer is explored in Theorem 5.11. Once again, the toy example serves to illustrate the results. A numerical example with three assets can be found in Section 6. Some conclusions and possible further developments and ramifications are touched upon in Section 7. Technical information and proofs are collected in the Appendix.

2 Multi-currency model with proportional transaction costs

Let be a filtered probability space. We assume that is finite, , and for all . For each let be the collection of atoms of , called the nodes of the associated tree model. A node is said to be a successor of a node if . For each we denote the collection of successors of any given node by .

For each let be the collection of -measurable -valued random variables. We identify elements of with functions on whenever convenient.

We consider the discrete-time currency model introduced by Kabanov (1999) and developed further by Kabanov & Stricker (2001) and Schachermayer (2004) among others. The model contains assets or currencies. At each trading date and for each one unit of asset can be obtained by exchanging units of asset . We assume that the exchange rates are -measurable and for all and .

We say that a portfolio is can be exchanged into a portfolio at time whenever there are -measurable random variables , such that for all

| (2.1) |

where represents the number of units of asset received as a result of exchanging some units of asset .

The solvency cone is the set of portfolios that are solvent at time , i.e. the portfolios at time that can be exchanged into portfolios with non-negative holdings in all assets. It is straightforward to show that is the convex cone generated by the canonical basis of and the vectors for , and so is a polyhedral cone, hence closed. Note that contains all the non-negative elements of .

A trading strategy is a predictable -valued process with final value and initial endowment . For each the portfolio is held from time to time . Let be the set of trading strategies. We say that is a self-financing strategy whenever for all . Note that no implicitly assumed self-financing condition is included in the definition of .

A trading strategy is an arbitrage opportunity if it is self-financing, and there is a portfolio with non-negative holdings in all assets such that . This notion of arbitrage was considered by Schachermayer (2004), and its absence is formally different but equivalent to the weak no-arbitrage condition introduced by Kabanov & Stricker (2001).

Theorem 2.2 (Kabanov & Stricker (2001), Schachermayer (2004)).

The model admits no arbitrage opportunity if and only if there exists a probability measure equivalent to and an -valued -martingale such that

| (2.3) |

where is the polar of ; see (A.1) in the Appendix.

We denote by the set of pairs satisfying the conditions in Theorem 2.2, and by the set of pairs satisfying the conditions in Theorem 2.2 but with absolutely continuous with respect to (and not necessarily equivalent to) . We assume for the remainder of this paper that the model admits no arbitrage opportunities, i.e. .

Remark 2.4.

In place of a pair one can equivalently use the so-called consistent price process ; see Schachermayer (2004).

3 Instant versus gradual exercise

The payoff of an American option in the model with underlying currencies is, in general, an -valued adapted process . The seller of the American option is obliged to deliver, and the buyer is entitled to receive the portfolio of currencies at a stopping time chosen by the buyer. Here denotes the family of stopping times with values in . This is the usual setup in which the option is exercised instantly at a stopping time .

American options with the provision for instant exercise in the multi-currency model under proportional transaction costs have been studied by Bouchard & Temam (2005), who established a non-constructive characterisation of the superhedging strategies for the option seller only, and by Roux & Zastawniak (2011), who provided computationally efficient iterative constructions of the ask and bid option prices and the superhedging strategies for both the option seller and buyer.

In the present paper we relax the requirement that the option needs to be exercised instantly at a stopping time . Instead, we allow the buyer to exercise gradually at a mixed stopping time . (For the definition of mixed stopping times, see Appendix A.3.)

If the buyer chooses to exercise the option gradually according to a mixed stopping time , then the seller of the American option will be obliged to deliver, and the buyer will be entitled to receive the fraction of the portfolio of currencies at each time .

The question then arises whether or not it would be more beneficial for the buyer to exercise the option gradually rather than instantly? What will be the optimal mixed stopping time for the buyer? How should the seller hedge against gradual exercise? Are the ask (seller’s) and bid (buyer’s) option prices and hedging strategies affected by gradual exercise as compared to instant exercise?

3.1 Instant exercise

In the case of instant exercise the seller of an American option needs to hedge by means of a trading strategy against all ordinary stopping times chosen by the buyer. The trading strategy needs to be self-financing up to time and to allow the seller to remain solvent on delivering the portfolio at time , for any . Hence the family of seller’s superhedging strategies is defined as

and the ask price (seller’s price) of the option in currency is

This is the smallest amount in currency needed to superhedge a short position in .

On the other hand, the buyer of an American option can select both a stopping time and a trading strategy . The trading strategy needs to be self-financing up to time and to allow the buyer to remain solvent on receiving the portfolio at time . Thus, the family of buyer’s superhedging strategies is defined as

and the bid price (buyer’s price) of the option in currency is

This is the largest amount in currency that the buyer can raise using the option as surety.

For American options with instant exercise, iterative constructions of the ask and bid option prices and and the corresponding seller’s and buyer’s superhedging strategies from and were established by Roux & Zastawniak (2011).

3.2 Gradual exercise

When the buyer is allowed to exercise gradually, the seller needs to follow a suitable trading strategy to hedge his exposure. Since the seller can react to the buyer’s actions, this strategy may in general depend on the mixed stopping time followed by the buyer, and will be denoted by . In other words, we consider a function .

At each time the seller will be holding a portfolio and will be obliged to deliver a fraction of the payoff . He can then rebalance the remaining portfolio into in a self-financing manner, so that

| (3.1) |

The self-financing and superhedging conditions have merged into one. We call (3.1) the rebalancing condition.

When creating the portfolio at time , the seller can only use information available at that time. This includes , but the seller has no way of knowing the future values that will be chosen by the buyer. The trading strategies that can be adopted by the seller are therefore restricted to those satisfying the non-anticipation condition

| (3.2) |

In particular, the initial endowment of the trading strategy is the same for all . We denote this common value by .

We define the family of seller’s superhedging strategies against gradual exercise by

and the corresponding ask price (seller’s price) of the option in currency by

| (3.3) |

This is the smallest amount in currency that the seller needs to superhedge a short position in the American option when the buyer is allowed to exercise gradually.

On the other hand, the buyer is able to select both a mixed stopping time and a trading strategy , and will be taking delivery of a fraction of the payoff at each time . Because the choice of the mixed stopping time is up to the buyer, the trading strategy needs to be good just for the one chosen stopping time, and does not need to be considered as a function of , in contrast to the seller’s case. The rebalancing condition

| (3.4) |

needs to be satisfied.

Hence, the family of superhedging strategies for the buyer of an American option with gradual exercise is defined as

and the corresponding bid price (buyer’s price) of the option in currency is

| (3.5) |

This is the largest amount in currency that can be raised using the option as surety by a buyer who is able to exercise gradually.

Example 3.6.

We consider a toy example with two assets, a foreign currency (asset 1) and domestic currency (asset 2) in a two-step binomial tree model with the following bid/ask foreign currency prices in each of the four scenarios in :

|

|

Note there are only two nodes with a non-trivial bid/ask spread, namely the ‘up’ node and the ‘up-up’ node . The corresponding exchange rates are

In this model we consider an American option with the following payoff process :

|

|

In the case when the option can only be exercised instantly, using the algorithms of Roux & Zastawniak (2011) we can compute the bid and ask prices of the option in the domestic currency to be

Now consider given by

|

|

for any . Also consider and such that

|

|

We can verify that and . The existence of these strategies means that

This example demonstrates that the seller’s and buyer’s prices under gradual exercise may differ from their respective counterparts under instant exercise. It demonstrates the need to revisit and investigate the pricing and superhedging results in the case when the instant exercise provision is relaxed and replaced by gradual exercise.

4 Pricing and superhedging for the seller under gradual exercise

We have seen in Example 3.6 that the seller’s price may be higher than . The reason is that an option seller who follows a hedging strategy is required to be instantly solvent upon delivering the payoff at the stopping time when the buyer has chosen to exercise the option. Meanwhile, a seller who follows a strategy will be able to continue rebalancing the strategy up to the time horizon as long as a solvent position can be reached eventually. Being able to defer solvency in this fashion allows more flexibility for the seller, resulting in a lower seller’s price.

On the other hand, it might appear that a seller who hedges against gradual exercise (against mixed stopping times) would have a harder task to accomplish than someone who only needs to hedge against instant exercise (ordinary stopping times). However, this turns out not to be a factor affecting the seller’s price, as we shall see in Proposition 4.8.

4.1 Deferred solvency

These considerations indicate that the notion of solvency needs to be relaxed.

We say that a portfolio satisfies the deferred solvency condition at time if it can be exchanged into a solvent portfolio by time without any additional investment, i.e. if there is a sequence such that for all and

We call such a sequence a liquidation strategy starting from at time .

The set of portfolios satisfying the deferred solvency condition at time is a cone. We call it the deferred solvency cone and denote by .

Example 4.1.

In Example 3.6 the portfolio with in the domestic currency and in the foreign currency is insolvent at the ‘up’ node at time , that is, . It does, however, satisfy the deferred solvency condition at that node, i.e. . The large bid-ask spread at node indicates a temporary loss of liquidity. Although the portfolio is insolvent at that node, waiting until the market recovers from the loss of liquidity can restore solvency. The liquidation strategy is to hold the portfolio until time and to buy the foreign currency then.

The following result shows that the deferred solvency cones can be regarded as the sets of time superhedging portfolios for the seller of a European option with expiry time and zero payoff; see Roux & Zastawniak (2011).

Proposition 4.2.

The deferred solvency cones can be constructed by backward induction as follows:

| (4.3) | ||||

| (4.4) |

From (4.4) we can see that for any and for any

| (4.5) |

By backward induction, is given as an intersection and algebraic sum of a finite number of polyhedral cones, so it is a polyhedral cone. This also means the solvency cones can readily be computed using standard operations on polyhedral convex sets.

The next result shows that Theorem 2.2 can be formulated equivalently in terms of the deferred solvency cones instead of the solvency cones .

Proposition 4.6.

If is a probability measure and is an -valued -martingale, then satisfies (2.3) if and only if

| (4.7) |

where is the polar of .

4.2 Construction of seller’s price and superhedging strategy

We extend the family of seller’s superhedging strategies by allowing for deferred solvency:

The following proposition shows that the set of initial endowments that allow the seller to hedge against gradual exercise is the same as that allowing to hedge against instant exercise with deferred solvency.

Proposition 4.8.

For any American option

We now present an iterative construction of the set of initial endowments that allow superhedging for the seller under deferred solvency. By Proposition 4.8, this also gives the set of initial endowments that allow superhedging for the seller under gradual exercise.

Construction 4.9.

Construct adapted sequences , , , for by

| (4.10) | ||||

| and by backward induction on all | ||||

| (4.11) | ||||

| (4.12) | ||||

| (4.13) | ||||

It follows by backward induction that the sets

are convex and polyhedral for each and because the algebraic sum and the intersection of a finite number of convex polyhedral sets are convex and polyhedral, and

are convex polyhedral sets for each . Moreover, , , , are non-empty for each because the portfolio belongs to all of them when is large enough.

Theorem 4.14.

The set of initial endowments that superhedge the seller’s position in the American option under gradual exercise is equal to

| (4.15) |

and the ask (seller’s) price of the option in currency can be computed as

Moreover, a strategy can be constructed such that

We can conclude that the set of initial endowments superhedging the seller’s position, the option ask price , and a superhedging strategy realising the ask price can be computed by means of standard operations on convex polyhedral sets.

Example 4.16.

Working within the setting of Example 3.6, we can now apply the constructions described in the current section to compute the sets of superhedging portfolios for the seller. These are sets of portfolios satisfying the inequalities

|

|

From we obtain the ask price

We can also construct a superhedging strategy such that

It is the strategy specified in Example 3.6.

4.3 Dual representation of seller’s price

A dual representation of the seller’s price can be obtained with the aid of the support function of . For the definition of the support function of a convex set, see Appendix A.1. More generally, let , , , be the support functions of the sets , , , of Construction 4.9. The functions , , are polyhedral (Rockafellar 1996, Corollary 19.2.1), hence continuous. Proposition A.14 in Appendix A.4.2 lists a number of properties of support functions, which will prove useful in what follows.

Proposition 4.17.

The seller’s price of an American option with gradual exercise can be written as

for some mixed stopping time , a probability measure and an -valued adapted process such that

| (4.18) |

and for all . Such , and can be constructed by a recursive procedure.

The notation , and used in Proposition 4.17 is defined by (A.2), (A.7) and (A.8). The proof is provided in Appendix A.4.2.

For any denote by the set of pairs such that is a probability measure and is an -valued adapted process satisfying (4.18). Also define for

The lack of arbitrage opportunities and Proposition 4.6 ensure that

for all .

Remark 4.19.

The following result provides a representation of dual to the representation (3.3) in terms of superhedging strategies.

Theorem 4.20.

The ask price in currency of an American option with gradual exercise can be written as

Moreover, we can algorithmically construct , and such that

This theorem is proved in Appendix A.4.2.

Example 4.21.

5 Pricing and superhedging for the buyer under gradual exercise

The buyer of an American option is entitled to receive the payoff according to a mixed stopping time of his choosing. In other words, the buyer receives at each time . The family of superhedging strategies for the buyer and the bid price (buyer’s price) under gradual exercise are defined in Section 3.2. We turn to the task of computing the bid price and an optimal superhedging strategy for the buyer.

5.1 Construction of buyer’s price and superhedging strategy

We start by computing the set if initial endowments that allow superhedging for the buyer.

Construction 5.1.

Construct adapted sequences , , , for by

| (5.2) | ||||

| and by backward induction on all | ||||

| (5.3) | ||||

| (5.4) | ||||

| (5.5) | ||||

For each the convex hull in (5.5) is taken on each atom of , i.e. for all

The index indicates that the deferred solvency cones are used in this construction. The sets , , , are non-empty for each because the portfolio belongs to all of them when is large enough.

In contrast with Construction 4.6 of Roux & Zastawniak (2011), which was used the case of instant exercise at an ordinary stopping time, we have the convex hull of in (5.5) rather than the union of sets. This means that , , , are convex sets, unlike their counterparts in Construction 4.6 of Roux & Zastawniak (2011). This is important because, once it is established in the next proposition that the are polyhedral, it becomes possible to implement techniques from convex analysis to compute them.

Proposition 5.6.

The set in Construction 5.1 is polyhedral with recession cone for each .

The next result shows that Construction 5.1 produces the set of initial endowments that superhedges for the buyer, which in turn makes it possible to compute the option bid price and also to construct a strategy that realises this price. This is similar to Theorem 4.14 for the seller.

Theorem 5.7.

The set of initial endowments that superhedge the buyer’s position in the American option with gradual exercise is equal to

| (5.8) |

and the bid (buyer’s) price of the option in currency can be computed as

Moreover, a strategy can be constructed such that

The proof of this theorem is also in Appendix A.4.3.

Example 5.9.

Still within the setting of Example 3.6, we apply the constructions described in the current section to compute the sets of superhedging portfolios for the buyer. These are sets of portfolios satisfying the inequalities

|

|

From we obtain the ask price

We can also construct a superhedging strategy such that

It is the strategy specified in Example 3.6.

5.2 Dual representation of buyer’s price

Since the , , , are convex, it becomes possible to apply convex duality methods not just in the seller’s case but also in the buyer’s case. (This was impossible to do in Roux & Zastawniak (2011) for American options with instant exercise because of the lack of convexity in the buyer’s case.)

In particular, in a similar way as in the proof of Proposition 4.17, we can show that the bid price of an American option with payoff under gradual exercise can be expressed as

in terms of the support function of .

However, we follow a different approach to obtain a representation of the bid price dual to the representation (3.5) of by means of superhedging strategies. In Theorem 5.7 a mixed stopping time has already been constructed as part of a superhedging strategy such that . As a result, the bid price given by (3.5) can be written as

for this mixed stopping time . It turns out that the set on the right-hand side can be expressed by means of the family of superhedging strategies for the seller of a European option with expiry time and payoff as described in Appendix A.5, where is defined by (A.8).

Proposition 5.10.

For any American option and any mixed stopping time we have

This proposition is proved in Appendix A.4.3.

We are now in a position to state a representation of the bid price dual to (3.5), and to prove it with the aid of Proposition 5.10.

Theorem 5.11.

The buyer’s (bid) price of an American option in currency can be represented as

| (5.12) |

where is defined by (A.8). Moreover, we can algorithmically construct and such that

Example 5.13.

We revisit Example 3.6 one more time to construct a mixed stopping time and a pair such that

They are

|

|

6 Numerical example

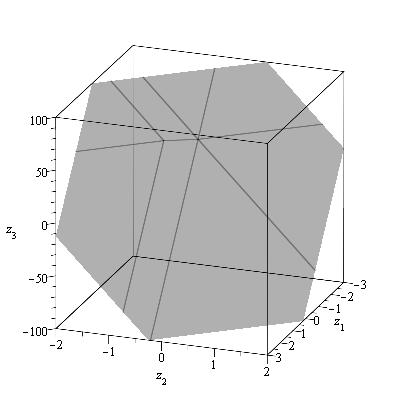

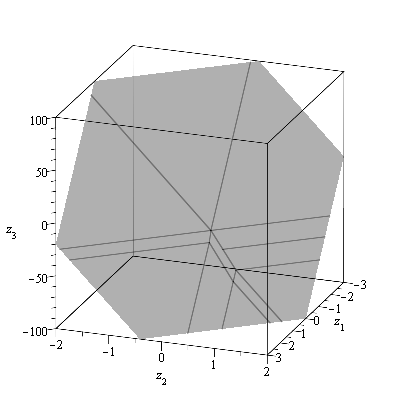

In this section we present a three-dimensional numerical example with a realistic flavour to illustrate Constructions 4.9 and 5.1. The numerical procedures below were implemented in Maple with the aid of the Convex package (Franz 2009).

Consider a model involving a domestic currency and two foreign currencies, with time horizon and with time steps. The friction-free nominal exchange rates between the domestic currency and the two foreign currencies follow the two-asset recombinant Korn & Müller (2009) model with Cholesky decomposition. That is, there are possibilities for the exchange rates at each time step , indexed by pairs with , and each non-terminal node with exchange rates has four successors, associated with exchange rates , , and . With defined for convenience, the exchange rates are given by

for and , where and are the initial exchange rates, and are the volatilities and is the correlation between the logarithmic growth of the exchange rates.

Assume that proportional transaction costs of are payable on all currency exchanges, except at time step , when is payable, modelling a temporary loss of liquidity. In other words, the matrix of exchange rates between each pair among the three currencies at each time step is

where

Consider an American put option with physical delivery and strike on a basket containing one unit of each of the foreign currencies. It offers the payoff

We allow for the possibility that the option may never be exercised by adding an extra time step to the model and setting the payoff to be at that time step. Constructions 4.9 and 5.1 give

where is the convex cone generated by the vectors

The sets and , which appear in Figure 1, yield the ask and bid prices

in each of the three currencies.

|

|

7 Conclusions and Outlook

In this paper we have explored American options with gradual exercise within Kabanov’s model (Kabanov 1999) of many assets under transaction costs, along with the related notion of deferred solvency, which helps to deal with a temporary loss of liquidity (large bid-ask spreads) in the market. We have demonstrated that gradual exercise (at a mixed stopping time chosen by the buyer) can reduce the ask (seller’s) price and increase the bid (buyer’s) price of the option compared with the case when the option can only be exercised instantly (at an ordinary stopping time).

In this context we have constructed and implemented algorithms to compute the ask and bid option prices, the buyer’s and seller’s optimal hedging portfolios and strategies, and their optimal mixed stopping times. We have studied dual representations for both the buyer and the seller of an American option with gradual exercise. The results have been illustrated by numerical examples.

Compared to options with instant exercise, a novel feature is that pricing and hedging an American option is a convex optimisation problem not just for the seller but also for the buyer of the option, making it possible to use convex duality in both cases. Ramifications to be explored further may include an extension of Bouchard and Temam’s representation of the strategies hedging the seller’s (short) position (Bouchard & Temam 2005) to the case of hedging the buyer’s (long) position in the option.

We also conjecture that it should be possible to adapt the constructions presented here so that linear vector optimisation methods can be used to price and hedge both the seller’s and buyer’s positions in an American option with gradual exercise, along similar lines as was done by Löhne & Rudloff (2011) for European options under transaction costs.

Appendix A Appendix

A.1 Some notation and facts from convex analysis

For any non-empty convex cone , denote by the polar of , i.e.

| (A.1) |

For any set define the cone generated by as

The recession cone of a non-empty convex set is defined as

It is a convex cone containing the origin (Rockafellar 1996, Theorem 8.1). If is a polyhedral cone, then (Rockafellar 1996, Corollary 8.3.2).

The convex hull of sets in is the smallest convex set in that contains , and is denoted by . The convex hull of convex functions is the function defined by

The effective domain of a convex function is defined as

The support function of a convex set is defined as

A.2 Compactly generated cones

For any set and define

| (A.2) |

We say that a cone is compactly -generated if is compact, non-empty and is generated by .

Lemma A.3.

If two cones and are compactly -generated and , then is compactly -generated and

| (A.4) |

Proof.

Equality (A.4) follows directly from (A.2). A vector is an element of if and only if and , if and only if and and , if and only if and , if and only if .

The set is compact since it is the intersection of two compact sets and . It remains to show that is non-empty and generates . To this end, fix any . As and are generated, respectively, by and , there exist , , and such that

As , we must have and . Moreover, since , we have

which in turn implies , completing the proof. ∎

In this paper we also make use of the following result by Roux & Zastawniak (2011, Lemma A.1).

Lemma A.5.

Fix any , and suppose that are non-empty closed convex sets in such that and is compactly -generated for all . Then

the cone is compactly -generated and

and for each there exist and with for all such that

A.3 Mixed stopping times

A mixed (or randomised) stopping time is a non-negative adapted process with values in such that

The family of mixed stopping times will be denoted by .

For any we put

| (A.6) |

Moreover, for any adapted process and for any we put

| (A.7) |

We also define evaluated at by

| (A.8) |

With each ordinary stopping time we associate the mixed stopping time defined as

| (A.9) |

A.4 Proofs and technical results

A.4.1 Deferred solvency

Proof of Proposition 4.2..

Proof of Proposition 4.6..

Conversely, suppose that is an -valued -martingale that satisfies (2.3). To show that it satisfies (4.7) we proceed by backward induction. By (4.3), we have . For any suppose that . As is a -martingale, we have for all that

For every and , observe from (4.5) that

Successive application of Corollaries 16.4.2 and 16.5.2 in Rockafellar (1996) then gives

| (A.10) |

Since by (2.3), it follows that , which concludes the inductive step. ∎

A.4.2 Seller’s case

Proof of Proposition 4.8..

We show first that for any there exists such that . If , then for each we have , i.e. there exists a liquidation strategy starting from at time . We also put for notational convenience. Moreover, for each we have , i.e. there exists a liquidation strategy starting from at time . For each define

where is defined by (A.6). The process belongs to and satisfies the non-anticipation condition (3.2). Moreover, for each

because and is a convex cone. Hence satisfies (3.1) in addition to (3.2), and so .

Conversely, fix any and put , where is defined by (A.9). Then for all we have and

Fix any . Then for each , and the non-anticipation property (3.2) of gives . Since , it means that

| (A.11) |

Moreover, for each we have , and so

| (A.12) |

We verify by backward induction that for each . Clearly, . Now suppose that for some . From (A.12) we can see that . Because is predictable, we have by (4.4), completing the backward induction argument. In particular, this means that . Together with (A.11) it gives for any . As a result, we have constructed such that . ∎

Proof of Theorem 4.14..

Suppose that . We construct a sequence of random variables by induction. First take . Now suppose that we have already constructed such that for some . From (4.13) we obtain , whence

by (4.10). We also obtain , and by (4.12) there exists a random variable such that . From (4.11) we have , which concludes the inductive step. Finally, we put . It follows that with . By Proposition 4.8, a strategy can be constructed such that .

Suppose now that . By Proposition 4.8, there is a such that . Clearly,

| (A.13) |

for all , and in particular . We now show by backward induction that for all . Suppose that for some . Since , this means by (4.11) that . The condition implies that . Property (A.13) then gives by (4.13), which completes the inductive step. We conclude that .

We have proved (4.15). It follows that

We know that is polyhedral, hence closed, so is also a closed set. It is non-empty and bounded below because for any large enough, and for any small enough. As a result, the infimum is attained. It means, in particular, that , so we know that a strategy can be constructed such that . ∎

The following result is similar to Lemma 5.5 in (Roux & Zastawniak 2011), but with the solvency cones replaced by the deferred solvency cones .

Proposition A.14.

-

For each the set is compactly -generated.

-

For all and we have

(A.15) (A.16) -

We have for all . For all and we have

(A.17) and for each there exist , and such that

-

For every and we have

and for each there exist and for all such that

Proof.

We first consider claim (2). As is a cone,

Note in particular that . For all and we have (Rockafellar 1996, p. 113)

which leads to (A.15). Equation (A.16) follows similarly from

Claims (1), (3) and (4) can be obtained by backward induction. We clearly have

and this set is compactly -generated because .

Now fix any and , and suppose that and that this set is compactly -generated. Since

Lemma A.5 can be applied to the sets for all . This justifies claim (4) for this and also that

is compactly -generated.

By Theorem 2.2 and Proposition 4.6, the lack of arbitrage opportunities implies that there is a pair such that and for each . Since is a martingale under , it follows that

and so . As and are compactly -generated, it follows from Lemma A.3 and (A.10) that is compactly -generated, which justifies claim (1) for this value of .

Proof of Proposition 4.17..

By Proposition A.14, is compactly -generated. Since is polyhedral, it is continuous on its effective domain and therefore attains a maximum on the non-empty compact set . From Theorem 4.14 it follows (Rockafellar 1996, Theorem 13.1) that

The following construction produces adapted processes , , and for , and for . We already know that the maximum of over the set is attained, i.e. there exists some such that

| (A.18) |

For any , suppose that is given, and fix any . Then by Proposition A.14(3), there exist , and such that

| (A.19) | ||||

| (A.20) |

By (A.16) and Proposition A.14(4), there exist and for all such that

| (A.21) | ||||

| (A.22) | ||||

This completes the inductive step. Also define for all

Define the probability measure on as

where denotes the element of that contains . It then follows from (A.21), (A.22) that for all

| (A.23) | ||||

| (A.24) |

The mixed stopping time is defined by setting and

It is straightforward to show by induction that for all . Moreover, since , we have

Observe also that

for all , where is defined by (A.6). It then follows from (A.19), (A.20) and (A.15) that for all

| (A.25) | ||||

| (A.26) |

We now show by backward induction that for all

| (A.27) |

At time the result is trivial because . Suppose now that (A.27) holds for some . Then, by the tower property of conditional expectation,

and, by (A.26), the predictability of , and (A.24),

This concludes the inductive step.

Proof of Theorem 4.20..

By Proposition 4.17, a stopping time and a pair can be constructed such that

To establish the reverse inequality we prove by backward induction that for any , and

| (A.29) |

When ,

since and . Now fix any , and suppose that

Then, by the tower property of conditional expectation, and since and , it follows that

which proves (A.29). The construction in the proof of Theorem 4.14 with initial portfolio yields a strategy . For any and we have , and therefore (A.29) with yields

It follows that

∎

A.4.3 Buyer’s case

Proof of Proposition 5.6..

As and are polyhedral cones, they are closed and convex. We have and . It follows that for all (Rockafellar 1996, Corollary 9.1.2).

The set is clearly polyhedral with recession cone . For we proceed by induction. Suppose that is polyhedral and its recession cone is . Then is polyhedral and its recession cone is (Rockafellar 1996, Corollary 8.3.3). Being polyhedral, is the convex hull of a finite set of points and directions, and its recession cone is the convex hull of the origin and the directions in .

The set is polyhedral (Rockafellar 1996, Corollary 19.3.2) and hence it is the convex hull of a finite set of points and directions. Since the cone can be written as the convex hull of the origin and a finite number of directions, it is possible to write as the convex hull of a finite set of points, all in , and a finite set of directions. These directions are exactly the directions in and , i.e. the directions in and . Thus the recession cone of is

since by (4.4). This means that the set is closed and its recession cone is (Rockafellar 1996, Corollary 9.8.1). Moreover, since and are polyhedral, it follows that is polyhedral (Rockafellar 1996, Theorem 19.6), which means that is polyhedral, concluding the inductive step. ∎

Proposition A.30.

If , then for all

Proof.

The proof is by backward induction. Since , from (3.4) we have

It immediately follows that on the set . On the set we have because is a cone, and therefore

Suppose now for some that

Because , this means that

Since by (3.4), it follows that

We consider the two possibilities separately.

-

•

On the set we have and therefore

so that

Since

it follows that on .

-

•

On the set we have

because by (4.4). There are two further possibilities.

-

–

On we have and therefore

-

–

On we have and therefore as claimed.

-

–

∎

Proof of Theorem 5.7..

In view of Proposition A.30, to verify (5.8) it is sufficient to show that for every there exists a pair such that . To this end, define and . Suppose by induction that for some we have constructed predictable sequences and such that and

| for all | |||||

| for all |

Because of (5.5), there exists an -measurable random variable such that and

Equations (5.2) and (5.4) then give

where

follows from the fact that is a convex cone. This means there exists a random variable

such that

Put . Then , which concludes the inductive step. Now define the mixed stopping time by

We also put . We have constructed and such that and

Finally, we construct such that and . By the definition of the deferred solvency cones , for each there is a liquidation strategy starting from at time . We put

which means that

for each , with , completing the proof of (5.8).

Next, if follows from (5.8) that

By Proposition 5.6, is polyhedral, hence closed. As a result, the set is also closed. It is non-empty and bounded above because for any large enough, and for any small enough. This means that the supremum is attained. It follows that , so we know that a strategy can be constructed such that . ∎

Proof of Proposition 5.10..

For any such that , put

for each , and . Then

for each , and

since , so with .

Conversely, for any we put

for each , and . Then

for each , and

It follows that and , completing the proof. ∎

Proof of Theorem 5.11..

Theorem 5.7 gives

The maximum is attained, so . The strategy constructed by the method in the proof of Theorem 5.7 from the initial portfolio therefore realises the supremum in (3.5). We write this supremum as a maximum,

and apply Proposition 5.10, which gives

where is the ask (seller’s) price in currency of a European option with expiry time and payoff as defined in Appendix A.5. We can now apply Lemma A.31 to write

For any , since is a martingale under , we have

This means that

proving (5.12). We know that realises the supremum in (3.5), and therefore the above maxima over are attained at . A pair such that

can be constructed by the method of Roux & Zastawniak (2011, Proposition 5.3) for the European option with payoff , completing the proof. ∎

A.5 European options

We recall a result for European options in the market model with assets under transaction costs. This is needed in the proof of the dual representation for the bid price of an American option.

A European option obliges the seller (writer) to deliver a portfolio at time . The set of strategies superhedging the seller’s position is given as

and the ask price (seller’s price) of such an option in currency is

The following result can be found in Roux & Zastawniak (2011, Section 4.3.1).

Lemma A.31.

The ask price in currency of a European option can be represented as

Moreover, a pair such that can be constructed algorithmically.

References

- (1)

- Bouchard & Temam (2005) Bouchard, B. & Temam, E. (2005), On the hedging of American options in discrete time markets with proportional transaction costs, Electronic Journal of Probability 10, 746–760.

- Chalasani & Jha (2001) Chalasani, P. & Jha, S. (2001), Randomized stopping times and American option pricing with transaction costs, Mathematical Finance 11(1), 33–77.

-

Franz (2009)

Franz, M. (2009), Convex – a Maple package for convex geometry.

http://www.math.uwo.ca/~mfranz/convex/ - Kabanov (1999) Kabanov, Y. M. (1999), Hedging and liquidation under transaction costs in currency markets, Finance and Stochastics 3, 237–248.

- Kabanov & Stricker (2001) Kabanov, Y. M. & Stricker, C. (2001), The Harrison-Pliska arbitrage pricing theorem under transaction costs, Journal of Mathematical Economics 35, 185–196.

- Korn & Müller (2009) Korn, R. & Müller, S. (2009), The decoupling approach to binomial pricing of multi-asset options, Journal of Computational Finance 12, 1–30.

-

Löhne & Rudloff (2011)

Löhne, A. & Rudloff, B. (2011), An algorithm for calculating the set of superhedging portfolios and

strategies in markets with transaction costs.

http://arxiv.org/abs/1107.5720v2 - Rockafellar (1996) Rockafellar, R. T. (1996), Convex Analysis, Princeton Landmarks in Mathematics and Physics, Princeton University Press.

- Roux & Zastawniak (2009) Roux, A. & Zastawniak, T. (2009), American options under proportional transaction costs: Pricing, hedging and stopping algorithms for long and short positions, Acta Applicandae Mathematicae 106, 199–228.

-

Roux & Zastawniak (2011)

Roux, A. & Zastawniak, T. (2011),

American and Bermudan options in currency markets under proportional

transaction costs.

http://arxiv.org/abs/1108.1910v2 - Schachermayer (2004) Schachermayer, W. (2004), The fundamental theorem of asset pricing under proportional transaction costs in finite discrete time, Mathematical Finance 14(1), 19–48.

- Tien (2012) Tien, C.-Y. (2012), Mixed Stopping Times and American Options under Transaction Costs, PhD thesis, University of York.