Optimal Stopping When the Absorbing Boundary is Following

After

Masahiko Egami

Graduate School of Economics,

Kyoto University, Sakyo-Ku, Kyoto, 606-8501, Japan

egami@econ.kyoto-u.ac.jphttp://www.econ.kyoto-u.ac.jp/~egami/ and Tadao Oryu

Graduate School of Economics,

Kyoto University, Sakyo-Ku, Kyoto, 606-8501, Japan

oryu.tadao.27r@st.kyoto-u.ac.jp

Abstract.

We consider a new type of optimal stopping problems where the absorbing boundary moves as the state process attains new maxima . More specifically, we set the absorbing boundary as where is a certain constant. This problem is naturally connected with excursions from zero of the reflected process . We examine this constrained optimization with the state variable as a spectrally negative Lévy process.

The problem is in nature a two-dimensional one. The threshold strategy given by the path of just is not in fact optimal. It turns out, however, that we can reduce the original problem to

an infinite number of one-dimensional optimal stopping problems, and we find explicit solutions.

This work is motivated by the bank’s profit maximization with the constraint that it maintain a certain level of leverage ratio. When the bank’s asset value severely deteriorates, the bank’s required capital requirement shall be violated. This situation corresponds to in our setting. This model may well describe a real-life situation where even a large bank can fail because the absorbing boundary is keeping up with the size of the bank.

First draft: September 3, 2012 ; this version: August 18, 2014.

TThis work is in part supported

by Grant-in-Aid for Scientific Research (B) No. 23330104 and No. 26285069, Japan Society for the Promotion of Science.

We thank the participants for their valuable comments in the workshop “Topics in Lévy and jump models” at Osaka University.

The literature about optimal stopping problems and their applications is immense. In an infinite horizon problem, with one-dimensional continuous diffusions as the state variable,

a full characterization of the value function and of optimal stopping rule is known and the methodology for solution has been established. See, for example, Dynkin [13], Alvarez [2], Dayanik and Karatzas [11].

For spectrally negative Lévy processes, or Lévy processes with only negative jumps, a number of authors have succeeded in extending the classical results by using the scale functions. We just name a few here : [5, 6] for stochastic games, [4, 19, 21] for the optimal dividend problem, [1, 3] for American and Russian options, and [16, 20] for credit risk. However, the solution techniques presented in each paper are more or less problem-specific and no characterization of the value function is yet known.

If the problem involves two state variables, then even for continuous diffusions, very few things are known in the literature.

We study a new type of optimal stopping problems. We let be a spectrally negative Lévy process and denote by the reflected process

where . We then consider an optimal stopping problem for both and in which the absorbing boundary is defined by with as a positive constant. This means that while grows and keeps attaining new maxima, the absorbing boundary is accompanying with . Hence an excursion from , if greater than , would bring to ruin. This situation is seen in the real world; for example, several large financial institutions failed in the last crisis in 2007-2008. One of the reasons is that, while becoming large banks, they maintain high leverage and accordingly, the banks are not so far way from the bankruptcy threshold. Instead, the bankruptcy threshold keeps up with the size of the banks. That is, despite the size of the bank, the risk of bankruptcy is not so much mitigated. This paper is motivated by this phenomenon. See Section 4 for details. While we take the example of banking, one can come up with other applications of this type, as long as the absorbing boundary is determined in relation to the state process’ running maxima. For instance, a gambler may have a policy that he stops betting when his wealth goes below a certain level from that day’s running maxima .

An excursion theory for spectrally negative Lévy processes has been developed recently. See Bertoin [7] as a general reference. More specifically, an exit problem of the reflected process was studied by Avram et al. [3], Pistorius [25][26] and Doney [12].

In the above cited papers on optimal stopping problems, the optimal strategy is usually obtained by so-called “threshold strategy”. That is, the player should stop and receive rewards on the first occasion when the state process enters

a stopping region. In Lévy and other jump models, the authors first find the optimal threshold level and then prove its optimality by verifying the ‘quasi-variational inequalities’. See Øksendal and Sulem [22]. Since the problem at hand involves two dimensions; one is and the other is , finding and proving the overall optimal strategy may be challenging (as mentioned, no characterization in two-dimensional problems has been found). Recent developments on two-dimensional optimal stopping problems (involving and ) include Ott [23] and Guo and Zervos [17]. In the former paper, the author solves problems including a capped version of the Shepp-Shiryaev problem [27], and the latter paper is another contribution that extends [27].

In our particular situation, by looking at excursions that occur at each level of , we reduce the problem to an infinite number of one-dimensional optimal stopping problems. We shall then find an explicit form of the solution, thanks to the results by Pistorius [26]. It turns out that the optimal stopping region can be shown in a diagram created by various values of and (e.g., Figure 6).

The rest of the paper is organized as follows. In Section

2, we formulate a mathematical model with a review of some important facts of spectrally negative Lévy processes, and then

find an optimal threshold level in Section 3. We shall take the example of a bank’s optimization in Section 4 and provide an explicit calculation.

2. Mathematical Model

Let the spectrally negative Levy process represent the state variable defined on the probability space

, where is the set of all possible realization of the

stochastic economy, and is a probability measure defined on . We denote by

the filtration with respect to which is adapted and with the usual

conditions being satisfied. The Laplace exponent of is given by

where , , and is a measure concentrated on satisfying

. It is well-known that is zero at the origin, convex on

and has a right-continuous inverse:

The running maximum process is defined by

. In addition, we write for the reflected process defined by ,

and let be the stopping time defined by

the time of ruin. The payoff is composed of three parts; the running income to be received continuously until stopped or absorbed, the terminal reward part

to be received when the process is stopped, and the penalty part incurred when the process is absorbed.

We consider the following optimal stopping problem and the value function associated with initial values and ;

where and is the expectation operator corresponding to , is the constant discount rate and is the set of all -adapted stopping times. The running income function

is a measurable function that satisfies

The reward function and the penalty function are assumed to be measurable. Our main purpose is to calculate and to find the stopping time which attains the supremum.

For each Borel measurable function , we define a stopping time by

(2.2)

and define a set of stopping times by

In other words, is the first time the excursion from level, say , becomes greater than some value .

When is constant, for example, on , we write

In particular, if , then .

Next we let be the set of stopping times defined by

Note that if , then . The following lemma shows that it suffices to consider stopping times .

Lemma 2.1.

Let us define by

Then for any , we can find a such that .

Proof.

Set functions and by for some and on . Then it is clear from the definition that if and only if , and on . Hence the right hand side of

(2) for and are equal to each other. Hence the lemma is proved.

∎

2.1. Note on the Optimal Strategy

We will reduce the original problem (2) to an infinite number of one-dimensional optimal stopping problem and discuss the optimality of the

proposed strategy (2.2). Let us denote by the -potential of where

From the strong Markov property of , we have

Hence the value function can be written as

where

(2.4)

Since has nothing to do with the choice of , we concentrate on .

By the dynamic programming principle, we can write as

(2.5)

for any stopping time . See, for example, Pham [24] page 97. Now we set in (2.5).

For each level from which an excursion occurs, the value does not change during the excursion.

Hence, during the first excursion interval from , and for any , and (2.5) can be written as the following one-dimensional problem for the state process ;

Now we can look at only the process and find .

In relation to (2.1), we consider the following one-dimensional optimal stopping problem as for and its value function ;

(2.7)

where is a constant. Then the following lemma provides a sufficient condition for a threshold strategy to be optimal

for (2.7). See also Theorem 2.2 in Øksendal and Sulem [22] for this type of verification theorem. Note that holds when , and can be obtained by our solution method offered in Section 3.

Lemma 2.2.

Fix some . If there exist and a function such that

(i)

(ii)

(iii)

(iv)

then for every and the -stopping time gives supremum in (2.7).

Note that

Proof.

First we prove for every . The Itô’s rule (see e.g. Cont and Tankov[10] page 277) gives us

where we denote by the Poisson random measure associated with . Since the process does not leave the interval , the integrals with respect to the Brownian motion and the compensated jump measure (i.e., the last term) are martingales. Therefore, by taking expectations, we have

By the assumption

we have

(2.9)

Now, for any stopping time , by using (i)-(iv),

(2.10)

Taking the supremum over the set , we have

On the other hand, if we substitute for in (2.1)-(2.10), then all the inequalities are satisfied as

equalities thanks to the assumptions (i)-(iv). Therefore, for every .

∎

To use Lemma 2.2, one usually constructs a candidate and proves the required inequalities (ii) and (iii). However, for the optimal stopping

problems in spectrally negative Lévy models, this procedure is nontrivial and problem-specific, depending on various data such as functions and process .

It is because no general results about the optimality of threshold strategy have been proven. Accordingly, in this paper, having thus far characterized our two-dimensional problem (2) as a set of one-dimensional optimal stopping problems (2.1), we shall focus on and contribute to obtaining, in the general setting, an explicit form of solution (3.9) under threshold

strategies. Note that, for our problem, optimality of (3.9) for (2.1) (and hence for (2)) is given by verifying the conditions in Lemma 2.2 with .

Recall that, in the linear diffusion case, a full characterization of the value function and of optimal stopping

rule are known and the methodology for solution has been established;

an optimal stopping rule is given by the threshold strategy in a very general setup.

See Dayanik and Karatzas [11]; Propositions 5.7 and 5.14. See also Pham [24]; Section 5.2.3. Hence at

least, if has no jump (that is, is Brownian motion with

drift), the solution we derive is an optimal strategy for the function

(2).

2.2. Scale functions

We review some mathematically important facts before solving the problem. Associated with every spectrally negative Lévy process, there exists a (-)scale function

that is continuous, strictly increasing on and on . It is

uniquely determined by

Fix and define

(2.11)

then we have

(2.12)

and

(2.13)

where

Here we have on . We also have

(2.14)

In particular, is continuously differentiable on if does not have atoms and is twice-differentiable on if ; see, e.g., Chan et al.[9]. Throughout this paper, we assume the former:

Assumption 2.1.

We assume that does not have atoms.

Fix . The scale function increases exponentially;

(2.15)

There exists a (scaled) version of the scale function that satisfies

(2.16)

and

Moreover is increasing, and as is clear from

(2.15),

(2.17)

Regarding its behavior in the neighborhood of zero, it is known that

(2.20)

where , and

(2.24)

see Lemmas 4.3-4.4 of Kyprianou and Surya

[20].

For a comprehensive account of the scale function, see

[7, 8, 18, 20]. See [15, 28] for numerical methods for computing the

scale function.

3. Explicit Solution

Now we look to an explicit solution of for . Let us introduce the probability measure such that the

Radon-Nikodym derivative between and is defined by

Under , has the Laplace exponent defined by

Note that since , drifts to for .

Let be the scale function of under , that is, has the Laplace transform

In addition, we define the process of the height of the excursion as

and otherwise, where .

Then is a Poisson point process, and we denote its

characteristic measure on by .

It is known that there is a relation between and

:

(3.1)

where is some positive constant. See Bertoin [7] page 195 for the explanation of this identity.

Then we have . Since ,

the optimal threshold should satisfy

From this equation, we obtain

where the last equality is obtained by L’Hôpital’s rule, and hence is the value which gives supremum to .

∎

Remark 3.2.

is the value for the strategy with and for every ; that is, this amount is obtained when we stop if goes below in the excursion at level and use optimal strategy for the higher level .

3.2. When

Finally, let us consider the case of . In this case,

can be represented in terms of as follows:

Set . Then, from (2.12), the first term

in (3.2) can be written by

For the second term, we use Theorem 1 and 2 in Pistorius[26] again to obtain, for

For the third term, we have, in the same way as above,

for .

Now by combining all these terms, we can

write for ,

(3.9a)

where is the maximizer of the map on . Note that and is given by (3.6) (or (3.5)).

For the stopping regions, it becomes from (3.2)

(3.9b)

(3.9c)

4. Bank’s Optimization under Capital Requirements

In this section, we solve an example. Imagine that a bank’s total

asset value is represented by . We set that the leverage

ratio, defined as (Debt)/(Total Asset), cannot exceed . For

example, if the bank has the initial asset of with

, it has total asset of financed by debt and

equity . We can think of this ratio as the maximum leverage

ratio that is allowed by the banking regulations. We assume that

the bank increases its asset base as long as where is the

running maximum of and that the bank’s leverage ratio is

maintained at . Hence if the asset value appreciates to ,

then this would provide the bank with more lending opportunity since

the equity value is now . With this new equity level, the bank

increases its leverage up to , that is, total asset increasing

to financed by debt and equity . Note that

and the debt level is . Now

if the bank’s asset deteriorates due to defaults in the lending

portfolio, we would have . In other words, there appears an

excursion from the level of . Since the asset level has

been pegged at , the bank’s equity would be wiped out when

. That is, when and the process is absorbed.

This model well describes a real situation where even a large bank

can fail easily as we have experienced several times, the recent and

magnified shock being the global financial crisis in 2007-2008. After

becoming a large bank, it may still have an incentive to increase

assets, seeking for profits. The danger of becoming insolvent is

still if the bank continues to use leverage ratio of

. The absorbing boundary is always coming after.

Moreover, note that this model can incorporate the regulatory

requirements that the bank, when experiencing asset deterioration,

need to sell the assets in order to reduce the leverage.111We

are thankful to Nan Chen for pointing out this requirement. For

example, assume that when the bank loses one dollar of asset, the

bank loses its equity by and reduces its debt by

, where . Then, at the time the equity is

wiped out, we have

that is, the process is absorbed when the excursion reaches .

Note that an application of this setting to bank regulations is studied in Egami and Oryu [14].

where is a standard Brownian

motion, is a Poisson process with intensity , and are independent identically distributed random

variables whose distributions are exponential with parameter

under . Note that if we put , then is a Brownian motion with drift.

The reward functions are set by ,

, and , so that the problem is

.

In this case, the Laplace exponent

of is given by

has three solutions , , and (in decreasing order) and -scale function of is represented with these values;

In the Brownian motion case, has only two solutions and , and the third term above vanishes.

For the existence of , we need some restriction on the parameters. can be calculated by

Hence the condition we need is , and then

4.1. Brownian motion

First, we consider a Brownian motion with drift by using parameters , , , ,

and . Note that the value of has no effects on the problem when .

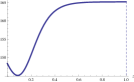

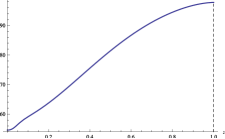

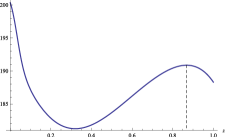

Panels (i), (ii), and (iii) in Figure 1 are the

graphs of with ,

and , respectively. As shown in Proposition

3.2, the maximum value in each graph corresponds to

for various values of , and are the

maximizers.

(i) s=5

(ii) s=5.2141

(iii) s=5.3

Figure 1. Graphs of for various values of .

In the case (i) , we have the boundary solution . This

means that, in the excursion which occurs at level , it is

optimal to stop when goes below . Since we set

here, if creeps over the level , we can obtain the terminal

reward. The case (ii) is a special point in some sense. Unlike

the case , there are two solutions and

. If we choose the former strategy , this

means, when reaches level for the first time, we stop

it immediately and gain the terminal reward. If we choose the latter

one , that means we should stop when goes below .

In the case (iii), there is the boundary solution .

That is, when reaches level for the first time, we should

exit immediately and gain the terminal reward.

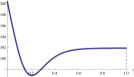

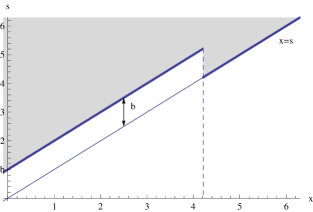

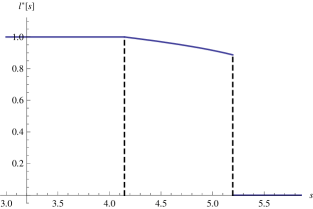

These arguments are summarized in Figure 2 that

illustrates an optimal strategy over the whole region of . The dashed line is drawn at , which indicates the

turning points of strategies. For , constantly takes

the value of . In this region, it is optimal to stop when the height

of the excursion is . For , constantly takes on .

In this region, our strategy reduces to the classical threshold strategy

by observing the path of process . That is, stop at the first passage time of level

by the process .

Figure 2. Graph of an optimal strategy .

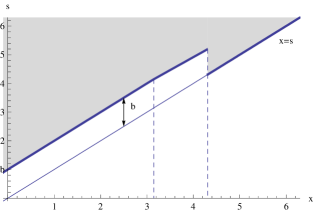

Figure 3. Graph of an optimal strategy on -plane. The shaded area is optimal stopping region.

4.2. Brownian motion with exponential jumps

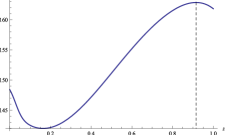

Next, to see the effects of jumps on the threshold strategy, we set , , , , , and .

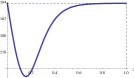

Panels (i), (ii), (iii), and (iv) in Figure 4 are the

graphs of with and , respectively. Note that the number in

(2.20) is 0.05 which is equal to the drift of the Brownian motion in Section 4.1.

(i) s=4

(ii) s=5

(iii) s=5.1963

(iv) s=5.3

Figure 4. Graphs of for various values of .

In the case (i) , we have the boundary solution . This

means that, in the excursion which occurs at level , it is

optimal to stop when goes below . Since we set

here, if creeps over the level , we can obtain the terminal

reward. Instead, if jumps over the level , we

should pay the penalty (but we set this as here) and cannot gain

the terminal reward. In the case (ii) , there is the internal

solution . Therefore, in the excursion which

occurs at level , it is optimal to stop immediately that

goes below . Since , if creeps over the

level or jumps onto in the area between and , we

can obtain the terminal reward. But if jumps across

the level , we cannot obtain the terminal reward.

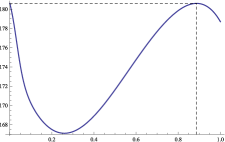

Figure 5. Graph of an optimal strategy .

Figure 6. Graph of an optimal strategy on -plane. The shaded area is optimal stopping region.

The case (iii) is a turning point of strategy like the case (ii)

in Figure 1. There are two solutions and

. If we choose the former strategy , this

means, when reaches level for the first time, we stop

it immediately and gain the terminal reward. If we choose the latter

one , that means we should behave like the case

(ii). In the case (iv), there is the boundary solution .

That is, when reaches level for the first time, we should

exit immediately and gain the terminal reward.

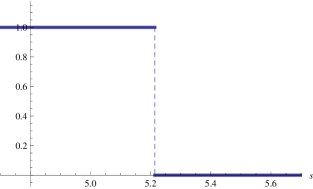

These arguments are summarized in Figure 5 that

illustrates an optimal strategy over the whole region of . Two dashed lines are drawn at and ,

which indicate the turning points of the strategies. For ,

constantly takes the value of . In this region, it is optimal

to stop when the height of the excursion is . When lies

between and , has the form of concave curve

started at . In this region, one should stop once the height of

excursion is greater than or equal to . Note that this region does not show up in the Brownian motion case.

Finally, for

, constantly takes on . In this region, our

strategy reduces to the classical threshold strategy by observing

the path of process . That is, stop at the first passage time of level

by the process .

Before concluding this section, let us make some comparisons of the two cases. In the jump case, we have two levels and

that mark the change points of strategy, while we have only one point in the no jump case. At the level of , the bank should stop the process during the excursion, a strategy that does not exist in the no jump case. It is due to the existence of jumps which could bring the process suddenly to the ruin. We have , which again shows that jumps make the bank more cautious; with it should not expect to reach a level as high as even with the large .

References

[1]

L. Alili and A. E. Kyprianou.

Some remarks on first passage of Lévy processes, the American

put and smooth pasting.

Ann. Appl. Probab., 15:2062–2080, 2004.

[2]

L. H. R. Alvarez.

On the properties of r-excessive mappings for a class of diffusions.

Ann. Appl. Probab., 13 (4):1517–1533, 2003.

[3]

F. Avram, A. E. Kyprianou, and M. R. Pistorius.

Exit problems for spectrally negative Lévy processes and

applications to (Canadized) Russion options.

Ann. Appl. Probab., 14:215–235, 2004.

[4]

F. Avram, Z. Palmowski, and M. R. Pistorius.

On the optimal dividend problem for a spectrally negative Lévy

process.

Ann. Appl. Probab., 17(1):156–180, 2007.

[5]

E. Baurdoux and A. E. Kyprianou.

The McKean stochastic game driven by a spectrally negative

Lévy process.

Electron. J. Probab., 13:no. 8, 173–197, 2008.

[6]

E. Baurdoux and A. E. Kyprianou.

The Shepp-Shiryaev stochastic game driven by a spectrally

negative Lévy process.

Theory Probab. Appl., 53, 2009.

[7]

J. Bertoin.

Lévy processes, volume 121 of Cambridge Tracts in

Mathematics.

Cambridge University Press, Cambridge, 1996.

[8]

J. Bertoin.

Exponential decay and ergodicity of completely asymmetric Lévy

processes in a finite interval.

Ann. Appl. Probab., 7(1):156–169, 1997.

[9]

T. Chan, A.E. Kyprianou, and M. Savov.

Smoothness of scale functions for spectrally negative Lévy

processes.

Probab. Theory Relat. Fields, to appear.

[10]

R. Cont and P. Tankov.

Financial modelling with jump processes.

Chapman Hall/CRC, Boca Raton, 2004.

[11]

S. Dayanik and I. Karatzas.

On the optimal stopping problem for one-dimensional diffusions.

Stochastic Process. Appl., 107 (2):173–212, 2003.

[12]

R. A. Doney.

Some excursion calculations for spectrally one-sided Lévy

processes.

In Séminaire de Probabilités XXXVIII, volume 1857 of

Lecture Notes in Math., pages 5–15. Springer, Berlin, 2005.

[13]

E. Dynkin.

Markov processes, Volume II.

Springer Verlag, Berlin, 1965.

[14]

M. Egami and T. Oryu.

An excursion theoretic approach to regulator’s bank reorganization problem.

Operations Research, to appear in 2015.

[15]

M. Egami and K. Yamazaki.

Phase-type fitting of scale functions for spectrally negative

Lévy processes.

Journal of Computational and Applied Mathematics, 264: 1-22, 2014.

[16]

M. Egami and K. Yamazaki.

Precautional measures for credit risk management in jump models.

Stochastics, 85:111-143, 2013.

[17]

X. Guo and M. Zervos.

options.

Stock. Proc. Appl., 120(7):1033-1059, 2010.

[18]

A. E. Kyprianou.

Introductory lectures on fluctuations of Lévy processes with

applications.

Universitext. Springer-Verlag, Berlin, 2006.

[19]

A. E. Kyprianou and Z. Palmowski.

Distributional study of de Finetti’s dividend problem for a general

Lévy insurance risk process.

J. Appl. Probab., 44(2):428–448, 2007.

[20]

A. E. Kyprianou and B. A. Surya.

Principles of smooth and continuous fit in the determination of

endogenous bankruptcy levels.

Finance Stoch., 11(1):131–152, 2007.

[21]

R. L. Loeffen.

On optimality of the barrier strategy in de Finetti’s dividend

problem for spectrally negative Lévy processes.

Ann. Appl. Probab., 18(5):1669–1680, 2008.

[22]

B. Øksendal and A. Sulem.

Applied Stochastic Control of Jump Diffusions.

Springer, New York, 2005.

[23]

C. Ott

Optimal stopping problems for the maximum process with upper and lower caps

Ann. Appl. Probab., 23(6): 2327–2356, 2013.

[24]

H. Pham.

Continuous-time Stochastic Control and Optimization with Financial Applications, volume 61 of Stochastic Modeling and Applied Probability.

Springer, Berlin Heidelberg, 2009.

[25]

M. R. Pistorius.

On exit and ergodicity of the spectrally one-sided Lévy process

reflected at its infimum.

J. Theoretical Probab., 17(1):183–220, 2004.

[26]M. R. Pistorius.

An excursion-theoretical approach to some boundary crossing problems and the Skorokhod embedding for reflected Lévy processes.

In Séminaire de Probabilités XL, volume 1899 of

Lecture Notes in Math., pages 278–307. Springer, Berlin, 2007.

[27]

L. Shepp and A. N. Shiraev

The Russian option: Reduced regret.

Ann. Appl. Probab., 3(3): 631–640, 1993.

[28]

B. A. Surya.

Evaluating scale functions of spectrally negative Lévy processes.

J. Appl. Probab., 45(1):135–149, 2008.