Efficient variational inference for generalized

linear mixed models with large datasets

Abstract

The article develops a hybrid Variational Bayes algorithm that combines the mean-field and fixed-form Variational Bayes methods. The new estimation algorithm can be used to approximate any posterior without relying on conjugate priors. We propose a divide and recombine strategy for the analysis of large datasets, which partitions a large dataset into smaller pieces and then combines the variational distributions that have been learnt in parallel on each separate piece using the hybrid Variational Bayes algorithm. We also describe an efficient model selection strategy using cross validation, which is trivial to implement as a by-product of the parallel run. The proposed method is applied to fitting generalized linear mixed models. The computational efficiency of the parallel and hybrid Variational Bayes algorithm is demonstrated on several simulated and real datasets.

Keywords. Parallelization, Mean-field Variational Bayes, Fixed-form Variational Bayes.

1 Introduction

Variational Bayes (VB) methods are increasingly used in machine learning and statistics as a computationally efficient alternative to Markov Chain Monte Carlo simulation for approximating posterior distributions in Bayesian inference. See, for example, Bishop, (2006); Ormerod and Wand, (2010). VB algorithms can be categorized into two main groups: the mean-field Variational Bayes (MFVB) algorithm (Attias,, 1999; Waterhouse et al.,, 1996; Ghahramani and Beal,, 2001) and the fixed-form Variational Bayes (FFVB) algorithm (Honkela et al.,, 2010; Salimans and Knowles,, 2013). The MFVB algorithm provides an efficient and convenient iterative scheme for updating the variational parameters, but in its exact form it requires conjugate priors and therefore rules out some interesting models. The FFVB algorithm assumes a fixed functional form for the variational distribution and employs some optimization approaches such as stochastic gradient descent search for estimating the variational parameters. This article develops a VB algorithm that combines these two algorithms in which the stochastic search FFVB method of Salimans and Knowles, (2013) (see Section 3) is used within a MFVB procedure for updating variational distribution factors that do not have a conjugate form. The convergence of the whole updating procedure is formally justified. Related work by Waterhouse et al., (1996) and Wang and Blei, (2013) used the Laplace approximation for updating non-conjugate variational factors, and Knowles and Minka, (2011) introduced the non-conjugate variational message passing framework for variational Bayes with approximations in the exponential family when the lower bound can be approxmiated in some way. Braun and McAuliffe, (2010) and Wang and Blei, (2013) also consider approximating the lower bound in non-conjugate models using the delta method. Tan and Nott, 2013a extend the stochastic variational inference approach of Hoffman et al., (2013) by combining non-conjugate variational message passing with algorithms from stochastic optimization which work with mini-batches of data, and apply the idea to non-conjugate generalized linear mixed models. We refer to the suggested algorithm we develop as the fixed-form within mean-field Variational Bayes algorithm, or the hybrid Variational Bayes algorithm. The new algorithm can be used to conveniently and efficiently approximate any posterior without relying on the conjugacy assumption.

The second contribution of this article is to propose a divide and recombine strategy (Guha et al.,, 2012) for the analysis of large datasets based on exponential family variational Bayes posterior approximations. The idea is to partition a large dataset into smaller pieces and learn the variational distribution in parallel on each separate piece using the hybrid Variational Bayes algorithm. The resulting variational distributions then are recombined to construct the final approximation of the posterior. The recombination is particularly easy for posterior approximations in the exponential family. The methodology proposed in our article is closely related to the methodology proposed independently in a recent preprint by Broderick et al., (2013). The main difference is that they develop the methodology in an online setting in which the data pieces arrive sequentially in time, while we describe the method in a static setting in which the whole dataset has already been collected. Furthermore, we show how to use the parallel divide and recombine strategy for model selection using cross validation. We also study empirically the effect of the number of data pieces and recommend a good number to use in practice.

As a main application of the parallel and hybrid Variational Bayes algorithm, we derive a detailed algorithm for fitting generalized linear mixed models (GLMMs). GLMMs are often considered difficult to estimate because of the presence of random effects and lack of conjugate priors. VB schemes for GLMMs are considered previously by Rijmen and Vomlel, (2008); Ormerod and Wand, (2012) and Tan and Nott, 2013b , and are shown to have attractive computation and accuracy trade-offs. The computational efficiency and accuracy of the proposed method is demonstrated on several simulated and real datasets.

The rest of the paper is organized as follows. Section 2 provides the background to VB methods and presents the hybrid VB algorithm. Section 3 reviews the fixed-form VB method of Salimans and Knowles, (2013) that we use for updating the non-conjugate variational factors within the mean-field VB algorithm. Section 4 presents the parallel implementation idea for handling large datasets. The detailed parallel and hybrid Variational Bayes algorithm for fitting GLMMs is presented in Section 5, and Section 6 reports a simulation study and real data examples.

2 Some Variational Bayes theory

Let be a vector of parameters, the prior and the data. Variational Bayes (VB) approximates the posterior by a more easily accessible distribution , which minimizes the Kullback-Leibler divergence

| (1) |

We have

where

| (2) |

As , for every , is therefore often called the lower bound, and minimizing is therefore equivalent to maximizing .

Often factorized approximations to the posterior are considered in variational Bayes. We explain the idea for a factorization with 2 blocks. Assume that and is factorized as

| (3) |

We further assume that and where and are variational parameters that need to be estimated. Then

where is a constant depending only on and

Let

| (4) |

then

| (5) |

Similarly, let

| (6) |

with

hence

| (7) |

Let and as in (4) and in (6), we have

| (8) |

This leads to an iterative scheme for updating and (8) ensures the improvement of the lower bound over the iterations. Because the lower bound is bounded from above, the convergence of the iterative scheme is ensured under some mild conditions. The above argument can be easily extended to the general case in which is factorized into blocks .

Variational Bayes approximation is now reduced to solving an optimization problem in form of (4). In many cases, a conjugate prior can be selected such that belongs to a recognizable density family, then the optimal VB posterior that maximizes the integral on the right hand side of (4) is , i.e.

| (9) |

and is determined accordingly. In such cases, the resulting iterative procedure is often referred to as the mean-field Variational Bayes (MFVB) algorithm, or the Variational Bayes EM-like algorithm. The MFVB is computationally convenient but it is not applicable to some interesting models because of the requirement of conjugate priors.

If does not belong to a recognizable density family, some optimization technique is needed to solve (4). Note that (4) has exactly the same form as the original VB problem that attempts to maximize in (2). We can first select a functional form for the variational distribution and then estimate the unknown parameters accordingly. Such a method is known in the literature as the fixed-form Variational Bayes (FFVB) algorithm. If the variational distribution is assumed to belong to the exponential family with unknown parameters , Salimans and Knowles, (2013) propose a stochastic approximation method for solving for . The details of this method are presented in next section. It is obvious that we can use a FFVB algorithm within a MFVB procedure to solve for (4) and the convergence of the whole procedure is still guaranteed. Interestingly, this procedure is similar in spirit to the popular Metropolis-Hastings within Gibbs sampling in Markov Chain Monte Carlo simulation.

3 Fixed-form Variational Bayes method of Salimans and Knowles

Suppose we have data , a likelihood where is an unknown parameter, and a prior distribution for . Salimans and Knowles, (2013) approximate the posterior by a density (with respect to some base measure which for simplicity we assume is the Lebesgue measure below) which is in the exponential family

where is a vector of natural parameters, denotes a vector of sufficient statistics for the given exponential family and is a normalization term. The is chosen by minimizing the Kullback-Leibler divergence

Differentiating with respect to , and using the result for exponential families that

| (10) |

which can be obtained by differentiating the normalization condition with respect to , we have

Using (10), the first term on the right hand side above disappears leaving

where in obtaining the last line we have again made use of (10). Hence if

| (11) |

This is a fixed point iteration that holds for the optimal value of . Note that differs only by a constant not depending on from so (11) can be written

| (12) |

For minimization of this suggests an iterative scheme where at iteration the parameters are updated to

| (13) |

Salimans and Knowles, (2013) observe that this iterative scheme doesn’t necessarily converge. Instead, inspired by stochastic gradient descent algorithms (Robbins and Monro,, 1951) they choose to estimate and by a weighted average over iterates in a Monte Carlo approximation to a pre-conditioned gradient descent algorithm which is guaranteed to converge if a certain step size parameter in their algorithm is small enough. They argue for Monte Carlo estimation of both and using the same Monte Carlo samples. This results in the approximation of the right hand side of (13) taking the form of a linear regression of the log target distribution on the sufficient statistics of the approximating family. The number of iterations for which their algorithm is run is decided upon in advance, a constant step size of is chosen for all iterations and averaging is over the last iterations in forming the estimates of the covariance matrices to calculate an estimate of . Theoretical support for these choices in the context of stochastic gradient descent algorithms is given by Nemirovski et al., (2009). See Salimans and Knowles, (2013) for further discussion of why stochastic estimation of the covariance matrices rather than averaging over the parameters in a more conventional stochastic gradient algorithm is beneficial.

Salimans and Knowles, (2013) show using properties of the exponential family that

| (14) |

and

| (15) |

and then consider Monte Carlo approximations to the expectations on the right hand side of (14) and of (15) based on a random draw where and is some random seed. If is smooth, the Monte Carlo approximations are smooth functions of , and these approximations can be differentiated in (14) and (15). In the case of an approximating distribution which is multivariate normal, and working in a direct parameterization in terms of the mean and covariance matrix, results due to Minka, (2001) and Opper and Archambeau, (2009) are used for evaluating the gradients in (14) and (15) to simplify the approximations while making use of first and second derivative information of the target posterior (Salimans and Knowles,, 2013, Section 4.4 and Appendix C). This results in a highly efficient algorithm.

We will be concerned with a certain modification of their algorithm for Gaussian but where there is independence between blocks of the parameters. Suppose is decomposed into blocks and that the variational posterior factorizes as

with each factor , , being multivariate normal. Here denotes the natural parameter for the th factor, we write and for the corresponding mean and covariance matrix and write for the vector of sufficient statistics in the th normal factor. Because of the independence, the optimality condition (12) simplifies to

and we can use the ideas of Salimans and Knowles, (2013) to estimate the covariance matrices on the right hand side of this expression. The result is the following slight modification of their Algorithm 2. In the description below , , , are vectors of the same length as and and are square matrices with dimension the length of . We assume below that is even so that is an integer and set .

Algorithm 1:

-

•

Initialize , .

-

•

Initialize , and , .

-

•

Initialize , and , .

-

•

For do

-

–

Generate a draw from

-

–

For do

-

*

Set and

-

*

Calculate the gradient and Hessian of with respect to evaluated at .

-

*

Set , , .

-

*

If then set , , .

-

*

-

–

-

•

Set , for .

On termination of the algorithm , are the estimated mean and covariance matrix in the normal term .

4 Parallel implementation for large datasets

Suppose the data are partitioned into pieces, . Suppose also that we have learnt a variational posterior distribution for each piece, approximating . We assume that

| (16) |

where is the natural parameter for which has been assumed to have an exponential family form, and . We will also assume that

i.e. the blocks are conditionally independent given . Then the posterior distribution is

Hence given our approximation of , is approximately proportional to

The reasoning used here is the same as that used in the Bayesian committee machine (Tresp,, 2000) although Tresp focused more on applications to Gaussian process regression. A similar strategy was independently proposed in a recent preprint by Broderick et al., (2013), who assume that the data pieces arrive sequentially in time.

Recall that has the factorization (16) so that if the prior also factorizes

where , with natural parameters , has the same exponential family form as , then the marginal posterior for is approximately proportional to

| (17) |

This approximation to is an exponential family distribution of the same form as each of the factors with natural parameter . Hence we can learn the approximations independently in parallel for different chunks of the data and then combine these posteriors to get an approximation to the full posterior.

If the factors are all normal, with corresponding to mean and covariance matrix and if has mean and covariance matrix , then the approximation to is normal, with mean

and covariance matrix

A similar way of combining normal approximations of posterior distributions in mixed models has been considered by Huang and Gelman (2005). If is Wishart, , and if is Wishart, , then is approximated as Wishart,

4.1 Model selection with cross-validation

The way of combining approximations learnt independently on different pieces of the data makes model choice by cross-validation trivial to implement. Let one of the pieces ,…, be a future dataset , and the rest is used as the training data . Let be the model that is being considered. A common measure of the performance of the model is the log predictive density scores (LPDS) defined as (Good,, 1952)

where we assume that , i.e. conditional on and the future observations are independent of the observed, and is the posterior of the model parameter conditional on the training data . The posterior can be replaced by its VB estimate and then can be approximated by Monte Carlo samples drawn from . A simpler method is to estimate the integral by with an estimator of the posterior mean of which can be obtained by using the mean of the VB approximation . We use this plug-in method in this paper and define the -fold cross-validated LPDS as

| (18) |

Computing (18) is trivial with parallel implementation and the main advantage is that no extra time is needed to refit the model on each training dataset. From (17), the variational distribution of the parameter block conditional on dataset is proportional to

from which the estimator is easily computed accordingly. Recall that is the VB approximation to the marginal posterior of the th block , based on the th data piece, and .

5 Application to generalized linear mixed models

Consider a generalized linear mixed model in which given random effects there are vectors of responses , , where the are conditionally independently distributed with a distribution in an exponential family with density or probability function

where is a canonical parameter which is monotonically related to the conditional mean through a link function , , is a -vector of fixed effect parameters, is a scale parameter which we assume known (for example, in the binomial and Poisson families ), and and are known functions. Here for simplicity we are considering the case of a canonical link function, i.e. . The vector is modeled as , where is an design matrix for the fixed effects and is an matrix of random effects (where is the dimension of ). Let and

The likelihood can be written as

where is understood componentwise and . The random effects are independently distributed as , therefore with a block diagonal matrix .

We consider Bayesian inference, with a normal prior for , say, where and are known hyperparameters. The prior for is a Wishart where again and are known hyperparameters. We set , , and with a large , 1000 say.

We write for the vector of all the unknown parameters and random effects, and assume a factorized form for the variational posterior

where is normal with mean and covariance matrix , and is Wishart . It is important to note that treating and as a single block rather than as two independent blocks has a big influence on the statistical inferences because of strong posterior dependence between the fixed and random effects.

By combining the VB theory in Section 1 and Algorithm 2 of Section 3, we have the following mean-field fixed-form VB algorithm for fitting GLMM.

Algorithm 2

-

1.

Initialize .

-

2.

Update and as follows

-

•

Initialize , and .

-

•

Initialize , and .

-

•

For do

-

–

Generate and compute .

-

–

Set and .

-

–

Compute the gradient

and Hessian

-

–

Set , , .

-

–

If then set , , ,

-

–

-

•

Set , .

-

•

-

3.

Update , .

-

4.

Repeat Steps 2-3 until convergence.

In the above algorithm with , and are mean and covariance of computed accordingly from and . The and therefore are block, high-dimensional and sparse matrices whose lower right blocks are block diagonal. Techniques of handling such sparse matrices should be used to reduce the computing time. Specially, we should compute the inverse of in blocks. In our experience, the algorithm often converges very quickly, after a few iterations. A common stopping rule is to stop iterations when the lower bound is not improved any further. However, computing the lower bound in the GLMM context often involves an analytically intractable integral. Alternatively, we can stop iterations if the difference of the variational parameters between two successive iterations is smaller than a small threshold. In our implementation, the algorithm is terminated if either times the difference between two successive iterations is smaller than ( is the total number of the parameters) or the number of iterations exceeds 50. The number of iterations within each fixed-form update is set to 100 after some experimentation but this can be varied depending on the computational budget or even adaptively increased as we near convergence.

In the GLMMs context, the data consist of observations on subjects . To carry out the parallel implementation for large datasets, we randomly partition the whole dataset of subjects into pieces such that each piece has subjects (see Section 6.1), . The variational distribution is learnt separately and in parallel on each piece using Algorithm 2, and then recombined as in Section 4.

5.1 Model selection for GLMMs

Given the response vector , assume that a GLMM has been specified, then model selection in GLMMs consists of selecting fixed effect covariates and random effect covariates among a set of potential covariates. Assume that we have fitted a GLMM and denote the estimated parameter by . The log predictive score of a future dataset with response vector , fixed effect design matrix and random effect design matrix is

where and , , correspondingly. The integrals above can be estimated by the Laplace method. The -fold cross-validated LPDS is then computed as in (18). The model that has the biggest LPDS will be selected.

It is obvious that this model selection strategy can be used for selecting GLMMs themselves as well as the link functions. A drawback of this model selection method is that it is not suitable for cases in which the number of candidate covariates is large because the total number of candidate models is huge and searching over the model space is very time demanding.

6 Examples

The proposed hybrid VB algorithm is written in Matlab and run on an Intel Core 16 i7 3.2GHz desktop. The parallel implementation is supported by the Matlab Parallel Toolbox with 4 local workers.

The performance of the suggested VB method is compared to a MCMC simulation method. If the likelihood is estimated unbiasedly, then the Metropolis-Hastings algorithm with the likelihood replaced by its unbiased estimator is still able to sample exactly from the posterior. See, for example, Andrieu and Roberts, (2009) and Flury and Shephard, (2011). The likelihood in the GLMM context is a product of integrals over the random effects. Each integral is estimated using importance sampling, which uses samples and the Laplace approximation for selecting the importance proposal density. Note that each likelihood estimation is also run in parallel using the parfor loop in the Parallel Toolbox. To handle the positive definiteness constraint on the inverse covariance , we use the Leonard and Hsu transformation (Leonard and Hsu,, 1992) , where is an unconstrained symmetric matrix, to reparameterize by the lower-triangle elements of , which is an one-to-one transformation between and . We then use the adaptive random walk Metropolis-Hastings algorithm in Haario et al., (2001) to sample from the posterior . Each MCMC chain consists of 20000 iterates with another 20000 iterates as burn-in.

Alternative MCMC methods for estimating GLMMs such as Gibbs sampling (Zeger and Karim,, 1991) can be faster than the MCMC scheme implemented in this paper. However, the Metropolis-Hastings sampling scheme with the random effects integrated out using importance sampling can avoid mixing problems that one would have with Gibbs sampling due to strong coupling of the fixed and random effects. Gibbs sampling and similar MCMC methods for GLMMs are in general not parallelizable and therefore cumbersome in cases of a very large . It should be noted that it is often difficult to compare the CPU times between different algorithms which depend heavily on the programming language being used and the optimality of the algorithms implemented for the characteristics of the particular example considered. However, we believe the results reported here are indicative of the speed up obtained with our variational Bayes methods.

6.1 Simulations

6.1.1 A simulation study of parallel implementation

This simulation example studies the effect of the divide and recombine strategy and its parallel implementation. We consider the following logistic model with a random intercept

| (19) | |||||

with , and .

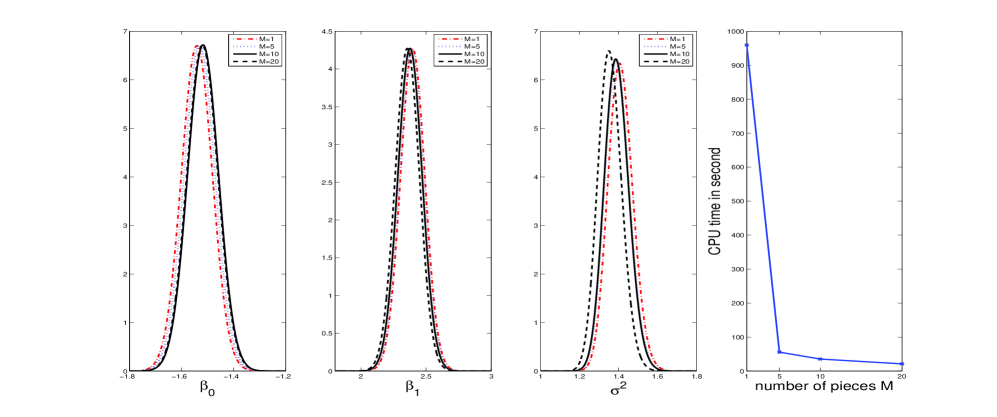

We first generate a dataset from (19) and run the proposed parallel VB method for four different values of the number of pieces: (i.e. no partitions of the data are performed), , and . All the partitions are done randomly. The first three panels of Figure 1 plot the variational densities for , and obtained by the four parallel VB runs, which show that the estimates are close to each other, in the sense that differences in the estimates are small relative to the estimated posterior standard deviations. The last panel plots the CPU times taken, which shows that running the divide and recombine strategy in parallel gains much efficiency in computing time.

In order to have a more formal comparison of these four parallel VB runs, we generate 50 independent datasets from model (19) and compute the mean squared errors of the estimates of the fixed effects () and the mean squared errors of the estimates of the random effect variance (). Table 1 summarizes these performance measures and the CPU times averaged over the 50 replications. The results show that the parallel VB run with , which has 200 subjects on each data piece, produces accurate estimates while having a reasonable running time. Our further exploration (results not shown) suggests that we should set to a value such that each data piece has roughly 200 subjects in order to have a good tradeoff between computing time and accuracy. However, obviously a good choice for the size of each piece depends on factors such as the dimension of the parameter space. In practice looking at whether the results change as we divide up the data less finely might be a good data driven diagnostic of whether subset sizes are too small.

All the VB runs in the following examples are run in parallel with such that each data piece has roughly 200 subjects.

| CPU (second) | |||

|---|---|---|---|

| 1 | 0.048 | 0.057 | 995.9 |

| 5 | 0.048 | 0.055 | 56.7 |

| 10 | 0.050 | 0.061 | 36.1 |

| 20 | 0.056 | 0.071 | 21.6 |

6.1.2 Model selection

We now study the performance of the model selection procedure discussed in Section 5.1. We generate datasets from the logistic random intercept model (19) and also generate covariates and randomly from the set . We have created a model selection problem in which the set of potential covariates for the fixed effects is and for the random effects is . It is reasonable to always include a fixed intercept and a random intercept in a GLMM, therefore there are a total of 8 candidate models to consider. We consider two values of , and , each is used to generate 100 datasets from the true model (19). The performance is measured by the correctly fitted rate (CFR) defined as the proportion of the 100 replications in which the true model is selected. The CFR is 80% for and 100% for , which shows that the model selection strategy performs well. The CPU time, averaged over the replications, taken to run the whole model selection procedure is 3.54 and 5.86 minutes for and , respectively. This CPU time is spent on fitting the 8 candidates models and computing the cross-validated LPDS.

6.1.3 A comparison to MCMC

This simulation study compares the performance of the proposed parallel and hybrid VB algorithm to MCMC. Datasets are generated from a Poisson mixed model with a random intercept

We set , and with generated from the uniform distribution on .

The performance is measured by (i) mean squared errors of the estimates of the fixed effects () and of the estimates of the variance of the random effect (); (ii) CPU time in minutes. Table 2 reports the simulation result, averaged over 10 replications, for four different sizes of data ranging from small data () to large data (). We do not run the MCMC simulation in the case and because it is very time consuming. In the case , it takes approximately 1.1 seconds to run each likelihood estimation in parallel, thus it would take approximately 733 minutes to run one MCMC chain in the setting of this example. Table 2 shows that the performance of the VB and MCMC is very similar in terms of mean squared errors, however the VB is much more computationally efficient.

| Method | CPU (minute) | |||

|---|---|---|---|---|

| 50 | VB | 0.155 | 0.025 | 0.07 |

| MCMC | 0.155 | 0.057 | 18.8 | |

| 200 | VB | 0.058 | 0.016 | 0.41 |

| MCMC | 0.059 | 0.016 | 33.4 | |

| 5000 | VB | 0.012 | 0.007 | 7.4 |

| MCMC | - | - | - | |

| 10000 | VB | 0.011 | 0.004 | 14.5 |

| MCMC | - | - | - |

6.2 Drug longitudinal data

The anti-epileptic drug longitudinal dataset (see, e.g., Fitzmaurice et al.,, 2011, p.346) consists of seizures counts on epileptic patients over 5 time-intervals of treatment. The objective is to study the effects of the anti-epileptic drug on the patients. Following Fitzmaurice et al., (2011), we consider a mixed effects Poisson regression model but with a random intercept

, and is an offset, and . The offset if and for , , if patient is in the placebo group and if in the treatment group.

The CPU time taken to run the VB and MCMC in this example is 0.14 and 17.7 minutes, respectively. Figure 2 plots the VB estimates (dashed line) and MCMC estimates (solid line) of the marginal posterior densities and . All the MCMC density estimates in this paper are carried out using the kernel density estimation based on the built-in Matlab function ksdensity. The figure shows that the VB estimates are very close to the MCMC estimates in this example.

6.3 Six city data

The six cities data in Fitzmaurice and Laird (1993) consists of binary responses which indicates the wheezing status (1 if wheezing, 0 if not wheezing) of the th child at time-point , and . Covariates are the age of the child at time-point , centered at 9 years, and the maternal smoking status (0 or 1). We consider the following logistic regression model with a random intercept

Figure 3 plots the VB estimates (dashed line) and MCMC estimates (solid line) of the marginal posterior densities and . The CPU time taken to run the VB and MCMC in this example is 0.56 and 52.8 minutes, respectively. The figure shows that the VB estimates of the posterior means are again close to the MCMC estimates. The VB is about 94 times more computationally efficient than the MCMC implementation considered.

6.4 Skin cancer data

A clinical trial is conducted to test the effectiveness of beta-carotene in preventing non-melanoma skin cancer (Greenberg et al.,, 1989). Patients were randomly assigned to a control or treatment group and biopsied once a year to ascertain the number of new skin cancers since the last examination. The response is a count of the number of new skin cancers in year for the th subject. Covariates include age, skin (1 if skin has burns and 0 otherwise), gender, exposure (a count of the number of previous skin cancers), year of follow-up and treatment (1 if the subject is in the treatment group and 0 otherwise). There are subjects with complete covariate information.

Donohue et al., (2011) consider 5 different Poisson mixed models with different inclusion of covariates whose including status is given in Table 3. Using the model selection strategy described in Section 5.1, we compute the cross-validated LPDS whose values are shown in Table 3, which suggest that Model 1 should be chosen. By using an AIC-type model selection criterion, Donohue et al., (2011) show that the first three models cannot be distinguished and, on parsimony grounds, they select Model 1.

| Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | |

| Fixed intercept | Y | Y | Y | Y | Y |

| Age | Y | Y | Y | Y | Y |

| Skin | Y | Y | Y | Y | Y |

| Gender | Y | Y | Y | Y | Y |

| Exposure | Y | Y | Y | Y | Y |

| Year | N | Y | Y | Y | Y |

| N | N | Y | N | Y | |

| Random intercept | Y | Y | Y | Y | Y |

| Random slope (Year) | N | N | N | Y | Y |

| LPDS |

For comparison, after selecting Model 1, we also use MCMC to estimate this model, which is

where , , .

Figure 4 plots the VB estimates (dashed line) and MCMC estimates (solid line) of the marginal posterior densities and . The CPU time taken to run the VB and MCMC is 1.45 and 130 minutes, respectively. The VB and MCMC estimates of the fixed effects are pretty similar. The VB is about 90 times more computationally efficient than the MCMC.

7 Conclusion

We have developed a hybrid VB algorithm that uses a flexible and accurate fixed-form VB algorithm within a mean-field VB updating procedure for approximate Bayesian inference, which is similar in spirit to the Metropolis-Hastings within Gibbs sampling method in MCMC simulation. If the variational distribution is factorized into a product and an exponential form is specified for factors that do not have a conjugate form, then the new algorithm can be used to approximate any posterior distributions without relying on conjugate priors. We have also developed a divide and recombine strategy for handling large datasets, and a method for model selection as a by-product. The proposed VB method is applied to fitting GLMMs and is demonstrated by several simulated and real data examples.

Acknowledgment

The research of Minh-Ngoc Tran and Robert Kohn was partially supported by Australian Research Council grant DP0667069.

References

- Andrieu and Roberts, (2009) Andrieu, C. and Roberts, G. (2009). The pseudo-marginal approach for efficient Monte Carlo computations. The Annals of Statistics, 37:697–725.

- Attias, (1999) Attias, H. (1999). Inferring parameters and structure of latent variable models by variational Bayes. In Proceedings of the 15th Conference on Uncertainty in Artificial Intelligence, pages 21–30.

- Bishop, (2006) Bishop, C. (2006). Pattern Recognition and Machine Learning. New York: Springer.

- Braun and McAuliffe, (2010) Braun, M. and McAuliffe, J. (2010). Variational inference for large-scale models of discrete choice. Journal of the American Statistical Association, 105(489):324–335.

- Broderick et al., (2013) Broderick, T., Boyd, N., Wibisono, A., Wilson, A., and Jordan, M. I. (2013). Streaming variational Bayes. Technical report, University of California, Berkeley. Available at http://arxiv.org/pdf/1307.6769v1.pdf.

- Donohue et al., (2011) Donohue, M. C., Overholser, R., Xu, R., and Vaida, F. (2011). Conditional Akaike information under generalized linear and proportional hazards mixed models. Biometrika, 98:685–700.

- Fitzmaurice et al., (2011) Fitzmaurice, G. M., Laird, N. M., and Ware, J. H. (2011). Applied Longitudinal Analysis. John Wiley & Sons, Ltd, New Jersey, 2nd edition.

- Flury and Shephard, (2011) Flury, T. and Shephard, N. (2011). Bayesian inference based only on simulated likelihood: Particle filter analysis of dynamic economic models. Econometric Theory, 1:1–24.

- Ghahramani and Beal, (2001) Ghahramani, Z. and Beal, M. (2001). Propagation algorithms for variational Bayesian learning. In Leen, T., Dietterich, T., and Tresp, V., editors, Neural Information Processing Systems, volume 13, pages 507–513. MIT Press.

- Good, (1952) Good, I. J. (1952). Rational decisions. Journal of the Royal Statistical Society B, 14:107–114.

- Greenberg et al., (1989) Greenberg, E., Baron, J., Stevens, M., Stukel, T., Mandel, J., Spencer, S., Elias, P., Lowe, N., Nierenberg, D., G., B., and Vance, J. (1989). The skin cancer prevention study: design of a clinical trial of beta-carotene among persons at high risk for nonmelanoma skin cancer. Controlled Clinical Trials, 10:153–166.

- Guha et al., (2012) Guha, S., Hafen, R., Rounds, J., Xia, J., Li, J., Xi, B., and Cleveland, W. S. (2012). Large complex data: divide and recombine (d&r) with rhipe. Stat, 1:53–67.

- Haario et al., (2001) Haario, H., Saksman, E., and Tamminen, J. (2001). An adaptive Metropolis algorithm. Bernoulli, 7:223–242.

- Hoffman et al., (2013) Hoffman, M. D., Blei, D. M., Wang, C., and Paisley, J. (2013). Stochastic variational inference. Journal of Machine Learning Research, 14:1303–1347.

- Honkela et al., (2010) Honkela, A., Raiko, T., Kuusela, M., Tornio, M., and Karhunen, J. (2010). Approximate Riemannian conjugate gradient learning for fixed-form variational Bayes. Journal of Machine Learning Research, 11:3235–3268.

- Knowles and Minka, (2011) Knowles, D. A. and Minka, T. (2011). Non-conjugate variational message passing for multinomial and binary regression. In Shawe-Taylor, J., Zemel, R., Bartlett, P., Pereira, F., and Weinberger, K., editors, Advances in Neural Information Processing Systems 24, pages 1701–1709.

- Leonard and Hsu, (1992) Leonard, T. and Hsu, J. S. J. (1992). Bayesian inference for a covariance matrix. The Annals of Statistics, 20(4):1669–1696.

- Minka, (2001) Minka, T. (2001). A family of algorithms for approximate Bayesian inference. PhD thesis, MIT.

- Nemirovski et al., (2009) Nemirovski, A., Juditsky, A., Lan, G., and Shapiro, A. (2009). Robust stochastic approximation approach to stochastic programming. SIAM Journal on Optimization, 19:1574–1609.

- Opper and Archambeau, (2009) Opper, M. and Archambeau, C. (2009). The variational Gaussian approximation revisited. Neural Computation, 21:786–792.

- Ormerod and Wand, (2012) Ormerod, J. and Wand, M. (2012). Gaussian variational approximate inference for generalized linear mixed models. J. Comput. Graph. Stat., 21:2–17.

- Ormerod and Wand, (2010) Ormerod, J. T. and Wand, M. (2010). Explaining variational approximations. American Statistician, 64:140–153.

- Rijmen and Vomlel, (2008) Rijmen, F. and Vomlel, J. (2008). Assessing the performance of variational methods for mixed logistic regression models. J. Stat. Comput. Simul., 78:765–779.

- Robbins and Monro, (1951) Robbins, H. and Monro, S. (1951). A stochastic approximation method. Annals of Mathematical Statistics, 22:400–407.

- Salimans and Knowles, (2013) Salimans, T. and Knowles, D. A. (2013). Fixed-form variational posterior approximation through stochastic linear regression. Technical report, Erasmus University Rotterdam. Available at http://arxiv.org/abs/1206.6679.

- (26) Tan, L. S. L. and Nott, D. J. (2013a). A stochastic variational framework for fitting and diagnosting generalized linear mixed models. Technical report, National University of Singapore. Available at http://arxiv.org/pdf/1208.4949v2.pdf.

- (27) Tan, L. S. L. and Nott, D. J. (2013b). Variational inference for generalized linear mixed models using partially noncentered parametrizations. Statistical Science, 28:168–188.

- Tresp, (2000) Tresp, V. (2000). A Bayesian committee machine. Neural Computation, 12:2719–2741.

- Wang and Blei, (2013) Wang, C. and Blei, D. M. (2013). Variational inference in nonconjugate models. Journal of Machine Learning Research, 14:1005–1031.

- Waterhouse et al., (1996) Waterhouse, S., MacKay, D., and Robinson, T. (1996). Bayesian methods for mixtures of experts. In Touretzky, M. C. M. D. S. and Hasselmo, M. E., editors, Advances in Neural Information Processing Systems, pages 351–357. MIT Press.

- Zeger and Karim, (1991) Zeger, S. L. and Karim, M. R. (1991). Generalized linear models with random effects: A Gibbs sampling approach. Journal of the American Statistical Association, 86:79–86.