Spectral methods for network community detection and graph partitioning

Abstract

We consider three distinct and well studied problems concerning network structure: community detection by modularity maximization, community detection by statistical inference, and normalized-cut graph partitioning. Each of these problems can be tackled using spectral algorithms that make use of the eigenvectors of matrix representations of the network. We show that with certain choices of the free parameters appearing in these spectral algorithms the algorithms for all three problems are, in fact, identical, and hence that, at least within the spectral approximations used here, there is no difference between the modularity- and inference-based community detection methods, or between either and graph partitioning.

I Introduction

Networked systems, such as social, biological, and technological networks, have been the subject of much recent research activity Newman03d ; Boccaletti06 . Along with many studies focusing on local properties of networks, such as clustering WS98 , degree distributions BA99b ; ASBS00 , and correlations PVV01 ; Newman02f , are studies that examine large-scale properties like path lengths WS98 , percolation CEBH00 ; CNSW00 , or hierarchy RB03 ; CMN08 . Among large-scale network properties, however, the one attracting by far the most attention has been community structure Fortunato10 . Many networks are found to possess communities or modules, groups of nodes within which connections are relatively dense and between which they are sparser. Communities are of fundamental interest in networked systems because of their functional implications—communities in a social network, for instance, may indicate factions, interest groups, or social divisions; communities in a metabolic network might correspond to functional units, cycles, or circuits that perform certain tasks.

The detection of communities in network data is also of interest from an algorithmic point of view. It is a remarkably challenging and subtle task for which a large number of approaches have been proposed. In this paper we examine two of the most widely used, the modularity maximization method Newman04a and the method of statistical inference by maximum likelihood SN97b ; ABFX08 . In both of these approaches the community detection problem is mapped to one of optimizing a given objective function (either modularity or likelihood) over possible divisions of a network into groups, but the resulting optimization problem is, in general, a computationally hard one Brandes07 , so one typically employs one of a range of polynomial-time heuristics to find approximate optima, such as Markov chain Monte Carlo SN97b ; GSA04 ; MAD05 , extremal optimization DA05 , or greedy algorithms CNM04 .

In this paper we study one of the most elegant classes of heuristics for network optimization problems, the spectral algorithms, inherently global methods based on the eigenvectors of matrix representations of network structure. We show that both the maximum modularity and maximum likelihood methods for community detection can be formulated as spectral algorithms that rely on the eigenvectors of the so-called normalized Laplacian matrix. We also describe a standard spectral algorithm for a third network problem, the well-known problem of normalized-cut graph partitioning. Our primary finding is that the spectral algorithms for all three of these problems are identical. At least within the spectral approach taken here, there is no difference between the detection of community structure using the methods of maximum modularity and maximum likelihood, or between either and normalized-cut graph partitioning. The latter equivalence is of particular interest because graph partitioning has been studied in depth for several decades and a broad range of results both applied and theoretical have been established, some of which can now be applied to the community detection problem as well.

The outline of this paper is as follows. In Sections II, III and IV we derive in turn our spectral algorithms for the maximum modularity, maximum likelihood, and normalized-cut partitioning problems, which, as we have said, turn out all to be the same. In Section V we give a selection of applications of the method to example networks, including both computer-generated benchmark networks and real-world networks, demonstrating its efficacy in community detection. In Section VI we give our conclusions.

II Modularity maximization

In its most basic form, the problem of community detection in networks is one of dividing the vertices of a given network into nonoverlapping groups such that connections within groups are relatively dense while those between groups are sparse. As it stands, this definition is imprecise and leaves room for interpretation, and there have, as a result, been a large number of different methods proposed for solving the problem Fortunato10 . Of these, however, probably the most widely used is the method of modularity maximization, in which the objective function known as modularity is optimized over possible divisions of the network Newman04a . The modularity for a given division of a network is defined to be the fraction of edges within groups minus the expected fraction of such edges in a randomized null model of the network. Various null models have been used, but the most common by far is the so-called configuration model MR95 ; NSW01 , a random graph model in which the degrees of vertices are fixed to match those of the observed network but edges are in other respects placed at random. The expected number of edges falling between two vertices and in the configuration model is equal to , where is the degree of vertex and is the total number of edges in the observed network. The actual number of edges observed to fall between the same two vertices is equal to the element of the adjacency matrix , so that the actual-minus-expected edge count for the vertex pair is . Giving integer labels to the groups in the proposed network division and denoting by the label of the group to which vertex belongs, the modularity is then equal to

| (1) |

where is the Kronecker delta. The leading constant is purely conventional; it has no effect on the position of the modularity maximum.

The modularity can be calculated for divisions of a network into any number of groups, but for the purposes of this paper we will focus on the simplest case of division into just two groups, which is probably the most widely studied case.

Consider, then, a network of vertices and edges, which is to be divided into two groups of any size so as to maximize the modularity, Eq. (1). The modularity can be conveniently rewritten in terms of a set of “Ising spin” variables , one for each vertex, having values

| (2) |

Then and

| (3) |

We define the quantity

| (4) |

to be an element of a symmetric matrix , called the modularity matrix Newman06b . The modularity matrix has the crucial property that the sums of all its rows and columns are zero:

| (5) |

where we have made use of and . Thus Eq. (3) can be written as

| (6) |

the second term in the brackets vanishing because of (5).

The matrix elements are fixed once the network is given, while the spins represent the division of the network into groups. Our task is to maximize over the possible choices of the —the values of that achieve the maximum indicate the optimal division of the network into communities. This is still a difficult computational task, known to be NP-complete in general Brandes07 , so the maximization is usually performed using approximate heuristics. In this paper we consider a spectral optimization strategy, similar in spirit to the spectral method proposed previously in Newman06b , but differing from it in one crucial detail.

Maximization of (6) is difficult because the variables are discrete-valued. The problem can be made much easier by relaxing the discreteness and allowing the to take any real values. This is an approximation—we will be solving a somewhat different problem from the one we really want to solve—but in practice it often gives good results. When we relax the , however, we must still impose at least a minimal constraint on them to prevent them from becoming arbitrarily large, which would make large but only in a trivial way that yields no information about community structure. Most commonly one applies a constraint of the form , which limits any individual to the range and fixes the mean-square value at 1.

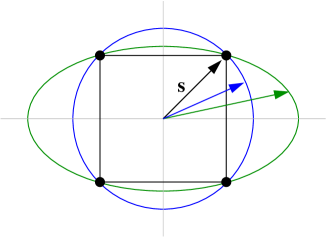

In the language of spin models, this would be called a “spherical model” BK52 . One can think of it in geometric terms, as shown in Fig. 1. If we consider the variables to be the elements of an -element vector , then the allowed values in the original “unrelaxed” problem restrict the vector to the corners of an -dimensional hypercube centered on the origin, while the relaxed values of the spherical model fall on the bounding hypersphere of radius that touches the hypercube at each of its corners. Thus the relaxed values include all the allowed values in the original problem, but also include many other values as well.

While this spherical relaxation is the commonest approach to the spectral method, it is only one of an infinite number of possible relaxations, differing from one another in the details of the constraint used to prevent the values of the from diverging. For instance, rather than relaxing onto the bounding hypersphere, we can relax onto any hyperellipsoid that touches the hypercube at all of its corners. In other words, we can choose a constraint of the form for any set of nonnegative constants . It is trivially the case that this constraint is satisfied by the unrelaxed values . The standard hypersphere corresponds to for all , but in this paper we will find it convenient to make a different choice, leading to a spectral modularity optimization algorithm that is different in some important respects from previous algorithms. We set equal to , the observed degrees of the vertices, so that our constraint takes the form

| (7) |

where is again the number of edges in the network and we have made use of .

Although the original unrelaxed modularity maximization problem is a hard one to solve, this relaxed problem is much easier. It can be solved exactly by simple differentiation. Applying the constraint (7) with a Lagrange multiplier , the maximum is given by

| (8) |

Performing the derivatives and rearranging, we find that

| (9) |

or, in matrix notation,

| (10) |

where is the diagonal matrix with elements equal to the vertex degrees . In other words is a solution of a generalized eigenvector equation, with being the eigenvalue.

To determine which eigenvector we should take, we multiply Eq. (9) by and sum over , making use of (6) and (7), to get an expression for the modularity:

| (11) |

To achieve the highest value of the modularity, therefore, we should choose to be the highest (most positive) eigenvalue of the generalized eigenvector equation (10).

Since all rows of the modularity matrix sum to zero, it follows that Eq. (10) always has a solution with eigenvalue . This solution, with all , corresponds to putting all vertices in group 1 and none in group 2, i.e., not dividing the network at all. This tells us that if is the highest eigenvalue then the best modularity is achieved by not dividing the network at all—the calculation is telling us that there is no good division of the network into groups, so we should leave it undivided. In our previous work we called such networks “indivisible.”

If, however, there is even a single strictly positive eigenvalue, then there will exist some nontrivial solution vector that achieves a higher modularity than the undivided network. Most, though not all, networks do have such a strictly positive eigenvalue, and we will assume this to be the case here.

The solution above can be simplified further. Using the definition (4) of the modularity matrix, we can rewrite Eq. (9) as

| (12) |

or in matrix notation as

| (13) |

where is the vector with elements and . Noting that and , we now multiply Eq. (13) throughout by to get , which implies either that the largest eigenvalue is zero or that

| (14) |

Since we are assuming there exists a nontrivial eigenvalue , we know that and hence (14) applies, which in turn means that Eq. (13) simplifies to

| (15) |

Thus our solution vector is also a solution of this generalized eigenvector equation, involving only the standard adjacency matrix. Again we should choose the largest allowed value of . Now, however, the most positive eigenvalue is disallowed—it is straightforward to see that the uniform vector is an eigenvector and by the Perron-Frobenius theorem it must have the most positive eigenvalue, since it has all elements positive. But this choice of eigenvector fails to satisfy Eq. (14) and hence is forbidden, in which case the best we can do is choose the eigenvector corresponding to the second most positive eigenvalue (which can easily be shown to satisfy (14), as indeed do all the remaining eigenvectors). This eigenvector is precisely equal to the leading eigenvector of Eq. (10), and hence either (10) or (15) will give us the solution we seek.

This is an exact solution of our relaxed modularity maximization problem. To get a solution to the original unrelaxed problem, in which is constrained to take only the values , the normal approach is simply to round the to the nearest allowed value . In practice, this just means that positive elements get rounded to and negative elements to . Thus our final algorithm is a simple one: we calculate the eigenvector of Eq. (15) corresponding to the second-highest eigenvalue, then divide the vertices of our network into two groups according to the signs of the elements of this vector. This is an approximation. It is not guaranteed to give an exact solution to the unrelaxed problem, but in many cases it does a good job, as we will later see.

As a practical matter, the solution of the generalized eigenvector equation (15) is most straightforwardly achieved by defining a rescaled vector , where is the diagonal matrix with diagonal elements equal to . Substituting into Eq. (15) and rearranging, we then find that

| (16) |

The matrix is symmetric, and thus is an ordinary eigenvector of a symmetric matrix, with elements having the same signs as those of , and with the same eigenvalue. The spectral algorithm is thus a simple matter of calculating the eigenvector for the second-highest eigenvalue of this symmetric matrix and then dividing the vertices according to the signs of its elements. For sparse networks this can be done efficiently using sparse matrix methods such as the Lanczos method.

The matrix

| (17) |

is sometimes called the normalized Laplacian of the network and we will use that terminology here. (The normalized Laplacian is sometimes defined as , where is the identity, but the two matrices differ only in a trivial transformation of their eigenvalues and the eigenvectors are the same for both.)

III Statistical inference

We now turn to a second method for community detection in networks, the method of statistical inference using stochastic block models. This method has attracted attention in recent years for the excellent results it returns and because of the solid mathematical foundations on which it rests, which have allowed researchers to prove rigorously a range of results about its expected performance. Indeed the method is provably optimal for certain classes of networks, in the sense that no other method will classify more vertices into their correct groups on average DKMZ11a ; ACBL13 .

The simplest form of the method is based on the standard stochastic block model SN97b , sometimes also called the planted partition model CK01 , a random graph model of a network containing community structure. The model does not itself constitute a method for community detection. Instead it provides a way of generating synthetic networks. To perform community detection, one fits the model to observed network data using a maximum likelihood method in much the same way as one might fit a straight line through a set of points to estimate their slope.

While formally elegant, however, this method has been found to work poorly in practice. The standard stochastic block model generates networks whose vertices have a Poisson degree distribution, quite unlike the degree distributions of most real-life networks, which means that the model is not, typically, a good fit to observed networks for any values of its parameters. The situation is akin to fitting a straight line through an inherently curved set of points—even the best fit will be a poor one because all fits are poor.

We can get around this problem by employing a slightly more sophisticated model, the degree-corrected block model KN11a , which incorporates additional parameters that allow the model to fit non-Poisson degree distributions, improving the fit to real-world data to the point where the degree-corrected model appears to give good community inference in practical situations.

The problem of fitting the degree-corrected block model to network data by likelihood maximization is, like the modularity maximization problem, a computationally difficult one in general, but it too can be tackled using approximate spectral methods, as we now describe. Indeed, as we will see, the spectral algorithm for the degree-corrected model is ultimately identical to the one we derived for the maximum modularity problem in the previous section.

In the degree-corrected block model vertices are divided into groups and edges placed between them independently at random with probabilities that depend on the desired degrees of the vertices and on their group membership. Let again denote the label of the group to which vertex belongs. Then between each pair of vertices we place a Poisson-distributed number of edges with mean equal to , where is the desired degree of vertex and is a set of parameters whose values control the relative probabilities of connections within and between groups.

If is again an element of the adjacency matrix of the observed network, equal to the number of edges between vertices and , then the probability, or likelihood, that this network was generated by the degree-corrected stochastic block model is

| (18) |

where the desired degrees are equal to the actual degrees of the vertices in the observed network. Thus the likelihood of observing the network that we did in fact observe, assuming it was generated by this model, depends on the assignment of the vertices to the groups. For some assignments the network would be highly unlikely to have occurred; for others it is more likely. In the maximum likelihood approach, we assume that the best assignment of vertices to groups is the one that maximizes the likelihood. This again turns the community detection problem into an optimization problem which, although hard to solve exactly, often has good approximate solutions that can be found with relative ease.

Typically, in fact, we maximize not the likelihood itself but its logarithm , which has its maximum in the same place:

| (19) |

where we have switched to a sum over all and compensated with the leading factor of , and we have assumed that the number of edges between any pair of vertices is either one or zero so that for all .

As in Section II, we will concentrate on the simplest case of a network with just two groups, and in addition we will assume (as most other authors also have) that there are just two different values for the model parameters: for pairs of vertices that fall in the same group and for pairs in different groups, with for traditional community structure (so-called assortative structure). Introducing indicator variables to denote group membership as we did in Section II, we note that

| (20) | ||||

| (21) |

Substituting these expressions into Eq. (19), we then find that

| (22) |

where is a positive constant given by

| (23) |

and we have dropped unimportant additive and multiplicative constants, which have no effect on the position of the likelihood maximum.

Our goal is now to maximize Eq. (22) with respect to the variables , but there is a problem: in most cases we don’t know the values of the parameters and and hence we don’t know either. Let us, however, suppose for the moment that we do know and see where it leads us. Equation (22) is closely similar in form to the modularity of Eq. (6), the only differences being a trivial leading constant, and the substitution of in the place of when compared to the modularity matrix of Eq. (4). The similarities are sufficiently strong that we can use the same spectral approach to maximize (22) as we did for the modularity, and it turns out to give the same answer. We relax the variables , allowing them to take any real values subject only to the elliptical constraint of Eq. (7), then introduce a Lagrange multiplier and differentiate to get

| (24) |

or, in matrix notation,

| (25) |

where is the diagonal matrix of degrees as previously. Thus the solution to our relaxed maximization problem is an eigenvector of the matrix and, by the same argument as before, we should choose the leading eigenvector.

Multiplying (25) on the left by and making use of and , we get

| (26) |

which implies either that or that . We are not at liberty, however, to choose any of the quantities , , or , and hence cannot in general satisfy the latter condition. Hence we must have and Eq. (25) simplifies to

| (27) |

which is identical to Eq. (15) for the maximum modularity problem. Note that the constant has dropped out of the equation, so the fact that its value is unknown is, after all, not a problem.

From this point onward, the argument is the same as for the maximum modularity problem and leads to the same result, that the optimal division of the network is given by the signs of the elements of the eigenvector of the normalized Laplacian matrix of Eq. (17) corresponding to the second most positive eigenvalue.

Thus, within the spectral approximation used here, the maximum modularity and maximum likelihood methods for community detection are functionally identical and give identical results.

IV Graph partitioning

We now turn to the third of the three problems mentioned in the introduction, the problem of normalized-cut graph partitioning, which, when tackled using the spectral method, we will show to be identical to the community detection problems of the previous sections. In a previous paper Newman13a we noted a mapping between maximum-likelihood community detection and the slightly different problem of minimum-cut partitioning, although that mapping requires an extra computational step not required by the mapping presented here. Connections between graph partitioning and modularity maximization have also been noted previously YD10 ; Bolla11 , although only for modified forms of the modularity and not for the standard modularity studied in this paper.

Traditional graph partitioning is the problem of dividing a network into a given number of parts of given sizes such that the cut size —the number of edges running between parts—is minimized. In the most commonly studied case the parts are taken to be of equal size. In many situations, however, one is willing to tolerate a little inequality of sizes if it allows for a better cut. Focusing once more on the case of division into two parts, a standard way to achieve this kind of tolerance is to minimize not the cut size but the ratio cut , where is again the cut size and and are the sizes of the two groups. The minimization is now performed with no constraint on the group sizes, but since is maximized when , the minimization still favors equally-sized groups, but it balances this favoritism against a desire for small cut size, and the compromise seems to work well in many practical situations.

Another variant on the same idea, which is particularly effective for networks that have broad degree distributions, as do many real-world networks, is minimization of the normalized cut , where and are the sums of the degrees of the vertices in the two groups. This choice favors divisions of the network where the groups contain equal numbers of edges, rather than equal numbers of vertices, which is desirable in certain applications. It is on this normalized-cut partitioning problem that we focus in this section.

The normalized-cut problem, like the other problems we have studied, is hard to solve exactly, but good approximate solutions can be found using spectral methods. The spectral approach given here is a standard one and is not new to this paper—see, for example, Zhang and Jordan ZJ08 . As before, we define index variables to denote the group membership of each vertex, but rather than the values we used previously, we define

| (28) |

where and are again the sums of the degrees of the vertices in each group. Note that this means that the values denoting the two groups change when the composition of the groups changes.

With this choice for the , and using our previous notations and for the vector and diagonal matrix of degrees respectively, we have

| (29) |

and

| (30) |

where is the number of edges in the network as before and the notation indicates that vertex is a member of group 1.

Note also that

| (31) |

meaning this quantity is nonzero only if belongs to group 1. Similarly

| (32) |

Using these results, we have

| (33) |

where, as before, is the cut size between the two groups. But the quantity on the left can also be written in matrix form as

| (34) |

where we have made use of , , and Eq. (29).

Combining Eqs. (33) and (34), we now have a matrix expression for the normalized cut:

| (35) |

Thus minimizing the normalized cut is equivalent to maximizing over choices of satisfying (28).

This hard optimization problem is once more made easier by relaxation. We relax the requirement that the take the values in Eq. (28), allowing them to take any real values subject only to the constraints (29) and (30). The relaxed problem can then be solved straightforwardly by introducing Lagrange multipliers for the two constraints and differentiating, which gives

| (36) |

Multiplying on the left by and making use of gives

| (37) |

which implies that because of Eq. (29), and hence we find once again that is a solution of the generalized eigenvector equation

| (38) |

Using Eqs. (30) and (35), the optimal value of the normalized cut is then

| (39) |

which is minimized by choosing as large as possible. The leading eigenvalue, however, is ruled out, since its eigenvector fails to satisfy Eq. (29), so once again our solution of the relaxed problem is given by the eigenvector corresponding to the second largest eigenvalue of Eq. (38) (which does satisfy (29), as do all the other eigenvectors).

Reversing the relaxation process is a little more complicated in this case than in the previous cases we have studied, because the discrete values of that we are rounding to, given by Eq. (28), are not constant, but depend on the composition of the groups themselves. In principle, the most correct way to do it is to go through every possible division of the elements of the leading eigenvector, of which there are , and find the one that gives the smallest value of the normalized cut. In practice, however, since we are looking for solutions with roughly equal group sizes, the values of and are also roughly equal, meaning that the discrete values of are approximately , and we can usually get good solutions by rounding to these values, which is equivalent to dividing vertices according to the signs of the vector elements. As we show in the next section, the divisions returned by the method are typically insensitive to the precise threshold value at which we divide the vector elements, so the results do not depend strongly on the rounding strategy chosen.

With this choice, which is the most common one, the algorithm becomes the same as the algorithms we have given for community detection, either by modularity maximization or the method of maximum likelihood.

V Examples

We have shown that three different problems—two-way community detection by maximum modularity and maximum likelihood, and normalized-cut bisection of a graph—can all be solved using the same spectral algorithm. We compute the leading eigenvector of the normalized Laplacian matrix, Eq. (17), and divide vertices according to the signs of the vector elements. In this section we give some example applications of the algorithm to both computer-generated and real-world networks.

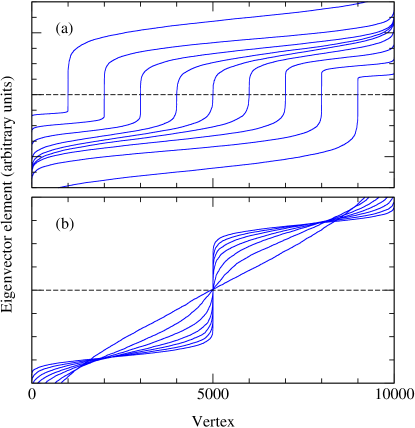

Figure 2 shows results from the application of the method to networks generated using the stochastic block model of Section III, which in addition to its use in community inference is also widely used as a benchmark test for community detection methods CK01 ; GN02 . Panel (a) of the figure shows a series of curves representing the elements of the second eigenvector of Eq. (15) in increasing order for single networks with two communities of varying sizes. The horizontal dashed line indicates the point at which the values of the elements pass zero—vertices on one side of this line are placed in the first group and vertices on the other side are placed in the second. Each curve passes briskly through zero at a point close to the sizes of the two groups planted in the network—the size of the first group in this test was 1000, 2000, 3000, and so on for each successive curve. This shows that the algorithm is capable of the accurate unsupervised detection of groups of a wide range of different sizes. Moreover it shows that detection is robust against fluctuations—because the line is close to vertical as it passes zero, the division of the network is insensitive to changes in the cut point. If the dashed line were moved up or down, even by quite a large amount, very few vertices would change group membership. This observation provides some justification for our contention at the end of Section IV that the exact choice of the cut point is unimportant.

Panel (b) of the figure shows similar curves for stochastic block model networks with two equally sized groups (which is the most challenging case) but varying strength of community structure. When the structure is strongest the curves show a pronounced step at the half-way point, indicating robust detection of the equally sized communities, but the step becomes progressively smaller as the planted structure gets weaker, and eventually disappears completely, so that the curve becomes featureless. The point at which the step disappears coincides with the “detectability threshold” below which it is believed that all algorithms (including this one) must fail to detect community structure RL08 ; DKMZ11a ; HRN12 ; NN12 ; MNS12 .

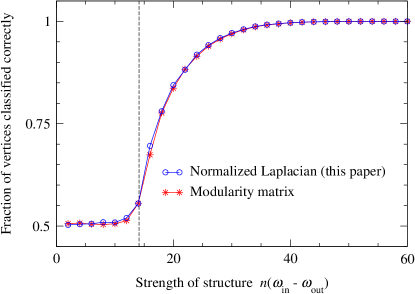

Figure 3 further quantifies the algorithm’s success at detecting community structure in block model networks. The figure shows the fraction of vertices classified into the correct groups for the same situation as in Fig. 2b—block model networks with and two equally sized groups, but varying strength of community structure. For most of the parameter range spanned by the figure the algorithm does a good job of putting vertices in the right groups. The vertical dashed line in the figure shows the position of the detectability threshold, below which we expect the algorithm (and indeed all algorithms) to return results no better than a random guess (which means 50% of vertices classified correctly). As we can see, the algorithm does better than random all the way down to the transition point (if only by a small margin in the region close to the threshold), which agrees with previous theoretical results finding that other spectral algorithms do the same NN12 . Also shown in Fig. 3 are results for tests on the same networks of the more standard spectral community detection method of Newman06b , in which one examines the leading eigenvector of the modularity matrix. As the figure shows, the performance of the two algorithms, at least in this test, is essentially identical.

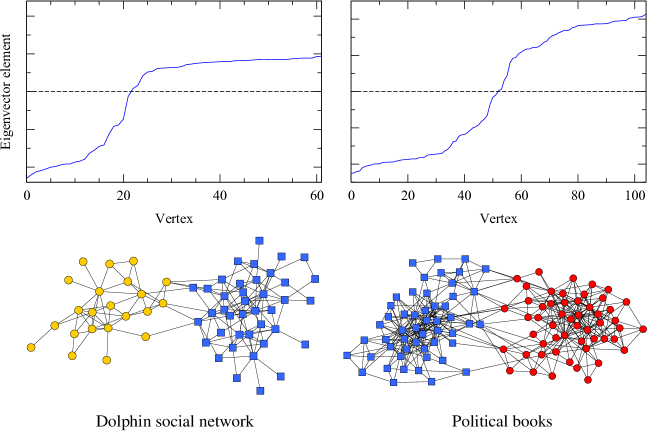

Figure 4 shows example applications to two well-studied real-world networks, the dolphin social network of Lusseau et al. Lusseau03a and the political book network of Krebs Newman06b , both of which are believed to break clearly into two communities. The top two panels in the figure show the equivalent of the curves in Fig. 2—values of the elements of the second eigenvector in increasing order. Each shows a clear step where it crosses the zero line (dashed lines in the plots) and the groups generated by dividing the vertices at this point are shown in the lower panels. In both cases the groups correspond closely to the accepted ground truth for these networks.

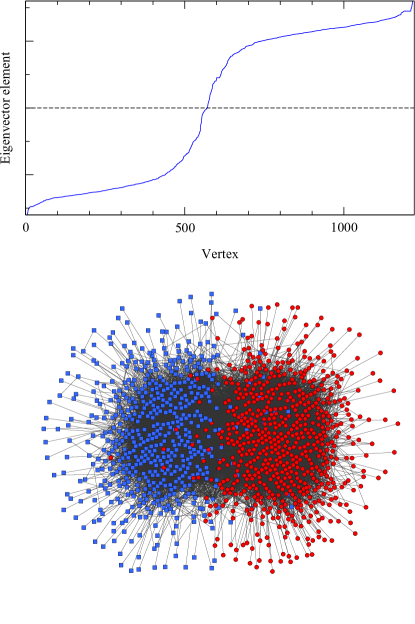

A further interesting example is given in Fig. 5, which shows an application of the method to a network of US political weblogs compiled by Adamic and Glance AG05 . Again this network is believed to divide strongly into two communities (along lines of political outlook), and the algorithm finds the accepted division to a good approximation. In this case, however, the division was found by examining the third eigenvector of the normalized Laplacian, not the second, as the developments of this paper would suggest. An examination of the second eigenvector reveals that it is entirely uncorrelated with the community structure in the network, instead being strongly localized around a few of the highest-degree vertices in the network—very large vector elements for these few hub vertices and small and apparently random elements for all other vertices. It is known that very high-degree vertices in networks can give rise to high-lying, localized eigenvectors NN13 , by mechanisms quite different from those that produce the eigenvectors containing community structure, and the two types of high-lying eigenvectors may compete to be the highest in the overall spectrum. The network of political blogs has a particularly broad distribution of vertex degrees, with some degrees far above the network mean, which in this case is apparently enough to create an additional eigenvector with eigenvalue above that of the vector containing the community structure. Nonetheless, the community structure is still there, clearly present in the third eigenvector. In practice, this means that application of the algorithm may not be quite as simple as our derivations suggest: it may require some finesse to extract useful community structure, particularly in the case of networks with very high-degree hubs. Anecdotally, based on our experiments, we believe that the replacement of the second eigenvector with a localized vector related to network hubs may occur more frequently in the algorithm described in this paper than it does in more conventional algorithms based on the eigenvectors of the modularity matrix Newman06b , but this at present is merely conjecture.

VI Conclusions

In this paper we have given spectral algorithms for the solution of three distinct network problems: community detection by modularity maximization, community detection by likelihood maximization using the degree-corrected block model, and normalized-cut graph partitioning. As we have shown, the algorithms for all three of these problems turn out to be the same, so that there is no difference, at least within the spectral formulation we use, between these three problems, although the algorithm described is different from standard spectral algorithms for modularity maximization described in the previous literature. We have given results from applications of the algorithm to a range of computer-generated and real-world networks, and it appears to perform well in practice.

One clear possibility for extension of the calculations outlined here is their generalization to the case of networks containing more than two groups or communities. The fundamental techniques needed for such a generalization are known ZJ08 ; RN13 —one replaces the index variables of Eq. (2) with vectors pointing to the corners of a (possibly irregular) simplex and the objective function (modularity, likelihood, or normalized cut) with the trace of a quadratic form involving the appropriate matrix. At present, however, a good all-purpose approach for community detection using such methods has yet to be found, and so the generalization to more than two communities must be considered an open problem.

Acknowledgements.

This work was funded in part by the National Science Foundation under grant DMS–1107796 and by the Air Force Office of Scientific Research (AFOSR) and the Defense Advanced Research Projects Agency (DARPA) under grant FA9550–12–1–0432.References

- (1) M. E. J. Newman, The structure and function of complex networks. SIAM Review 45, 167–256 (2003).

- (2) S. Boccaletti, V. Latora, Y. Moreno, M. Chavez, and D.-U. Hwang, Complex networks: Structure and dynamics. Physics Reports 424, 175–308 (2006).

- (3) D. J. Watts and S. H. Strogatz, Collective dynamics of ‘small-world’ networks. Nature 393, 440–442 (1998).

- (4) A.-L. Barabási and R. Albert, Emergence of scaling in random networks. Science 286, 509–512 (1999).

- (5) L. A. N. Amaral, A. Scala, M. Barthélémy, and H. E. Stanley, Classes of small-world networks. Proc. Natl. Acad. Sci. USA 97, 11149–11152 (2000).

- (6) R. Pastor-Satorras, A. Vázquez, and A. Vespignani, Dynamical and correlation properties of the Internet. Phys. Rev. Lett. 87, 258701 (2001).

- (7) M. E. J. Newman, Assortative mixing in networks. Phys. Rev. Lett. 89, 208701 (2002).

- (8) R. Cohen, K. Erez, D. ben-Avraham, and S. Havlin, Resilience of the Internet to random breakdowns. Phys. Rev. Lett. 85, 4626–4628 (2000).

- (9) D. S. Callaway, M. E. J. Newman, S. H. Strogatz, and D. J. Watts, Network robustness and fragility: Percolation on random graphs. Phys. Rev. Lett. 85, 5468–5471 (2000).

- (10) E. Ravasz and A.-L. Barabási, Hierarchical organization in complex networks. Phys. Rev. E 67, 026112 (2003).

- (11) A. Clauset, C. Moore, and M. E. J. Newman, Hierarchical structure and the prediction of missing links in networks. Nature 453, 98–101 (2008).

- (12) S. Fortunato, Community detection in graphs. Phys. Rep. 486, 75–174 (2010).

- (13) M. E. J. Newman, Fast algorithm for detecting community structure in networks. Phys. Rev. E 69, 066133 (2004).

- (14) T. A. B. Snijders and K. Nowicki, Estimation and prediction for stochastic blockmodels for graphs with latent block structure. Journal of Classification 14, 75–100 (1997).

- (15) E. M. Airoldi, D. M. Blei, S. E. Fienberg, and E. P. Xing, Mixed membership stochastic blockmodels. Journal of Machine Learning Research 9, 1981–2014 (2008).

- (16) U. Brandes, D. Delling, M. Gaertler, R. Görke, M. Hoefer, Z. Nikoloski, and D. Wagner, On finding graph clusterings with maximum modularity. In Proceedings of the 33rd International Workshop on Graph-Theoretic Concepts in Computer Science, number 4769 in Lecture Notes in Computer Science, Springer, Berlin (2007).

- (17) R. Guimerà, M. Sales-Pardo, and L. A. N. Amaral, Modularity from fluctuations in random graphs and complex networks. Phys. Rev. E 70, 025101 (2004).

- (18) A. Medus, G. Acuña, and C. O. Dorso, Detection of community structures in networks via global optimization. Physica A 358, 593–604 (2005).

- (19) J. Duch and A. Arenas, Community detection in complex networks using extremal optimization. Phys. Rev. E 72, 027104 (2005).

- (20) A. Clauset, M. E. J. Newman, and C. Moore, Finding community structure in very large networks. Phys. Rev. E 70, 066111 (2004).

- (21) M. Molloy and B. Reed, A critical point for random graphs with a given degree sequence. Random Structures and Algorithms 6, 161–179 (1995).

- (22) M. E. J. Newman, S. H. Strogatz, and D. J. Watts, Random graphs with arbitrary degree distributions and their applications. Phys. Rev. E 64, 026118 (2001).

- (23) M. E. J. Newman, Modularity and community structure in networks. Proc. Natl. Acad. Sci. USA 103, 8577–8582 (2006).

- (24) T. H. Berlin and M. Kac, The spherical model of a ferromagnet. Physical Review 86, 821–835 (1952).

- (25) A. Decelle, F. Krzakala, C. Moore, and L. Zdeborová, Inference and phase transitions in the detection of modules in sparse networks. Phys. Rev. Lett. 107, 065701 (2011).

- (26) A. A. Amini, A. Chen, P. J. Bickel, and E. Levina, Pseudo-likelihood methods for community detection in large sparse networks. Preprint arxiv:1207.2340 (2013).

- (27) A. Condon and R. M. Karp, Algorithms for graph partitioning on the planted partition model. Random Structures and Algorithms 18, 116–140 (2001).

- (28) B. Karrer and M. E. J. Newman, Stochastic blockmodels and community structure in networks. Phys. Rev. E 83, 016107 (2011).

- (29) M. E. J. Newman, Community detection and graph partitioning. Preprint arxiv:1305.4974 (2013).

- (30) L. Yu and C. Ding, Network community discovery: Solving modularity clustering via normalized cut. In Proceedings of the Eighth Workshop on Mining and Learning with Graphs, pp. 34–36, Association of Computing Machinery, New York (2010).

- (31) M. Bolla, Penalized versions of the Newman–Girvan modularity and their relation to normalized cuts and k-means clustering. Phys. Rev. E 84, 016108 (2011).

- (32) Z. Zhang and M. I. Jordan, Multiway spectral clustering: A margin-based perspective. Statistical Science 23, 383–403 (2008).

- (33) M. Girvan and M. E. J. Newman, Community structure in social and biological networks. Proc. Natl. Acad. Sci. USA 99, 7821–7826 (2002).

- (34) J. Reichardt and M. Leone, (Un)detectable cluster structure in sparse networks. Phys. Rev. Lett. 101, 078701 (2008).

- (35) D. Hu, P. Ronhovde, and Z. Nussinov, Phase transitions in random Potts systems and the community detection problem: Spin-glass type and dynamic perspectives. Phil. Mag. 92, 406–445 (2012).

- (36) R. R. Nadakuditi and M. E. J. Newman, Graph spectra and the detectability of community structure in networks. Phys. Rev. Lett. 108, 188701 (2012).

- (37) E. Mossel, J. Neeman, and A. Sly, Stochastic block models and reconstruction. Preprint arxiv:1202.1499 (2012).

- (38) D. Lusseau, K. Schneider, O. J. Boisseau, P. Haase, E. Slooten, and S. M. Dawson, The bottlenose dolphin community of Doubtful Sound features a large proportion of long-lasting associations. Can geographic isolation explain this unique trait? Behavioral Ecology and Sociobiology 54, 396–405 (2003).

- (39) L. A. Adamic and N. Glance, The political blogosphere and the 2004 US election. In Proceedings of the WWW-2005 Workshop on the Weblogging Ecosystem (2005).

- (40) R. R. Nadakuditi and M. E. J. Newman, Spectra of random graphs with arbitrary expected degrees. Phys. Rev. E 87, 012803 (2013).

- (41) M. A. Riolo and M. E. J. Newman, First-principles multiway spectral partitioning of graphs. Preprint arXiv:1209.5969 (2013).