Distributed Energy Trading: The Multiple-Microgrid Case

Abstract

In this paper, a distributed convex optimization framework is developed for energy trading between islanded microgrids. More specifically, the problem consists of several islanded microgrids that exchange energy flows by means of an arbitrary topology. Due to scalability issues and in order to safeguard local information on cost functions, a subgradient-based cost minimization algorithm is proposed that converges to the optimal solution in a practical number of iterations and with a limited communication overhead. Furthermore, this approach allows for a very intuitive economics interpretation that explains the algorithm iterations in terms of “supply–demand model” and “market clearing.” Numerical results are given in terms of convergence rate of the algorithm and attained costs for different network topologies.

Index Terms:

Energy trading, smart grid, distributed convex optimizationI Introduction

Worldwide energy demand is expected to increase steadily over the incoming years, driven by energy demands from humans, industries and electrical vehicles: more precisely, it is expected that the growth will be in the order of 40% by year 2030. This demand is fueled by an increasingly energy-dependent lifestyle of humans, the emergence of electrical vehicles as the major source of transportation, and further automation of processes that will be facilitated by machines.

In today’s power grid, energy is produced in centralized and large energy plants (macrogrid energy generation); then, the energy is transported to the end client, often over very large distances and through complex energy transportation meshes. Such a complex structure has a reduced flexibility and will hardly adapt to the demand growth, thus increasing the probability of grid instabilities and outages. The implications are enormous as demonstrated by recent outages in Europe and North America that have caused losses of millions of Euros [1].

Given these problems at macro generation, it is of no surprise that a lot of efforts have been put into replacing or at least complementing macrogrid energy by means of local renewable energy sources. In this context, microgrids are emerging as a promising energy solution in which distributed (renewable) sources are serving local demand [2]. When local production cannot satisfy microgrid requests, energy is bought from the main utility. Microgrids are envisaged to provide a number of benefits: reliability in power delivery (e.g., by islanding), efficiency and sustainability by increasing the penetration of renewable sources, scalability and investment deferral, and the provision of ancillary services. From this list, the capability of islanding [3, 4, 5] deserves special attention. Islanding is one of the highlighted features of microgrids and refers to the ability to disconnect the microgrid loads from the main grid and energize them exclusively via local energy resources. Intended islanding will be executed in those situations where the main grid cannot support the aggregated demand and/or operators detect some major grid problem that may potentially degenerate into an outage. In these cases, the microgrid can provide enough energy to guarantee, at least, a basic electrical service. The connection to the main grid will be restored as soon as the entire system stabilizes again. Clearly, these are nontrivial functionalities that may cause instability. In this regard, the sequel of papers [6, 7] provide a recent survey on decentralized control techniques for microgrids.

In order to improve the capabilities of the Smart Grid, a typical approach is to consider the case where several microgrids exchange energy to one another even when the microgrids are islanded, that is disconnected from the main grid [8, 9]. In other words, there exist energy flows within a group of contiguous microgrids but not between the microgrids and the main grid. In this context, the optimal power flow problem has recently attracted considerable attention. For instance, in [10] the authors consider the power flow problem jointly with coordinated voltage control. Alternatively, the work in [11] focuses on unbalanced distribution networks and proposes a methodology to solve three-phase power flow problems based on a Newton-like descend method. Due to the fact that these centralized solutions may suffer from scalability [12, 11] and privacy issues, distributed approaches based on optimization tools have been proposed in [13, 14] and more recently in [15, 16, 17]. In general, the optimal power flow problem is nonconvex and, thus, an exact solution may be too complex to compute. For this reason, suboptimal approaches are often adopted. As an example, references [18, 16] show that semidefinite relaxation (see [19] for further details on this technique) can, in some cases, help to approximate the global optimal solution with high precision. Alternatively, [17] resorts to the so-called alternating direction method of multipliers (see [20] for further information) to solve the power flow problem in a distributed manner.

In this paper, conversely to the aforementioned works, we consider an abstract model that allows us to focus on the trading process rather than on the electrical operations of the grid. In terms of trading, the massive spread of distributed energy resources is expected to drive the transition from today’s oligopolistic market to a more open and flexible one [21]. This new picture of the market has triggered the interest on new energy trading mechanisms [22, 23, 24, 25, 26, 27, 28, 8, 29]. For instance, the authors in [22] consider a scenario where a set of geographically distributed energy storage units trade their stored energy with other elements of the grid. The authors formulate the problem as a noncooperative game that is shown to have at least one Nash equilibrium point. In the context of demand response, the work in [24] proposes an efficient energy management policy to control a cluster of demands. Interestingly, [23] considers demand-response capabilities as an asset to be offered within the market and, thus, they can be traded between the different agents (retailers, distribution system operators, aggregators, etc.). From a more general perspective, the problem of energy trading between microgrids (or, market agents) has been considered in [25, 26, 27, 28, 8, 29]. Whereas these works mainly focus on simulation studies and architectural issues, this paper attempts to provide a comprehensive analytical solution for the energy trading problem between microgrids that, besides its theoretical appeal, can be distributedly implemented without the need of a central coordinator. More specifically, our setting consists of microgrids in which: (i) each microgrid has an associated energy generation cost; (ii) there exists a cost imposed by the distribution network operator for transferring energy between adjacent microgrids; and (iii) each microgrid has an associated power demand that must be satisfied. Under these considerations, we aim to find the optimal amounts of energy to be exchanged by the microgrids in order to minimize the total operational cost of the system (energy production and transportation costs). Of course, a possible approach would be to solve the optimization problem by means of a central controller with global information of the system. However, such a centralized solution presents a number of drawbacks since microgrids might be operated by different utilities and information on production costs cannot be disclosed. Therefore, in order to safeguard critical information on local cost functions and make the system more scalable, we propose an algorithm based on dual decomposition that iteratively solves the problem in a distributed manner. Interestingly, each iteration of the resulting algorithm has a straightforward interpretation in economical terms, once the new operational variables we introduce are given the meaning of energy prices. First, each microgrid locally computes the amounts of energy it must produce, buy and sell to minimize its local cost according to the current energy prices. Then, after exchanging the microgrid bids, a regulation phase follows in which, in a distributed way, the energy prices are adjusted according to the law of demand. This two-step process iterates until a global agreement is reached about prices and transferred energies.

The remainder of this paper is organized as follows. In Section II we present the system model. Next, Section III shows how the distributed optimization framework provides a solution for the local subproblems and gives an interpretation from an economical point of view. Finally, in Sections IV and V, we present the numerical results and draw some conclusions.

II System Model

Consider a system composed of interconnected microgrids (Gs) operating in islanded mode. During each scheduling interval, each microgrid G- generates units of energy111For simplicity, we assume that all energies correspond to constant power generation/absorption/transfer over the scheduling interval. and consumes units of energy. Moreover, G- may be allowed to sell energy to G-, , and to buy energy from G-, . Then, energy equilibrium within the G requires

| (1) |

where the two -dimensional column vectors

| and | (2) |

gather all the energies bought and sold, respectively, by G-. Also, we have introduced the adjacency matrix : element is equal to one if there exists a connection from G- to G- and zero otherwise. Note that, generally, may be nonsymmetric, meaning that at least two Gs are allowed to exchange energy in one direction only. By convention, we fix . Also, MWh for all .

Next, let and be the costs of producing units of energy at G- and transferring units of energy on the G-–G- link, respectively. This transferring cost function may model several factors. For example, the distribution network operator, as the enabler of the energy transfer between Gs, may charge a tax for energy transactions. In addition, this transfer cost function may also account for line congestions by introducing soft constrains on the maximum capacity of the line (see Section II-A for further information).

Even though the solution below may be extended to the case where different links have different transfer cost functions, we assume that is common among all the links in order to avoid further complexity. As it will be clearer later, our approach is quite general and only requires that all cost functions (both production and transport) satisfy some mild convexity constraints, summarized in Section II-A.

Finally, we further assume that all Gs agree to cooperate with one another in order to minimize the total cost of the system. In other words, the energy quantities exchanged by interconnected Gs form the equilibrium point of the following minimization problem:

| (3) | ||||

| s. to | ||||

where is the -th column of the identity matrix and, with some abuse of notation, we wrote . Also, we used (1) to get rid of the variables . Note that problem (3) considers the Gs as parts of a common system (for instance, they are controlled by the same operator) and the aim is at minimizing the global cost, without focusing on the benefits/losses of each individual G. We will see later on, however, that the proposed distributed and iterative minimization algorithm opens to a wider-sense interpretation where achieving the global objective implies a cost reduction at every G.

II-A The cost functions

As mentioned before, the algorithm proposed hereafter works with any set of generation/transfer cost functions, as long as they all satisfy some mild convexity constraints. Specifically, it is required that and are positive valued, monotonically increasing, convex and twice differentiable. Even though these requirements may seem abstract and distant from real systems, one should take into account that the cost function of a common electrical generator (as, e.g., oil, coal, nuclear,…) is often modeled as a quadratic polynomial , where the coefficients , and depend on the generator type, see [30] and, especially [31]. Such a generation model clearly satisfies our assumptions and, without available counterexamples, we extended it to the transfer cost function .

It is worth commenting here that the assumptions on the cost functions also allow for a simple way to introduce upper bounds on the energy generated by the Gs or supported by the transfer connections. Indeed, one can introduce soft constraints by designing the cost function with a steep rise at the nominal maximum value (see also the first paragraph of Section IV, where we comment on the cost functions used for simulation). By doing so, the maximum generated/transferred energies are controlled directly by the cost functions, without the need for hard constraints (i.e., well specified inequalities such as ) that would increase the complexity of the minimization problem in (3). Note that this expedient translates, somehow, to a more flexible system: when needed, a G can produce more energy than the nominal maximum if it is willing to pay an (significant) extra cost. Indeed, this situation arises in practical systems when backup generators are activated.

III Iterative Distributed Minimization

III-A Decentralizing the problem

Problem (3) is known to have a unique minimum point since both the objective function and the constraints are strictly convex. However, dealing with unknowns can be very involved. Moreover, a centralized solution would require a control unit that is aware of all the system characteristics. This fact implies a considerable amount of data traffic to gather all the information and can miss some privacy requirements, since Gs may prefer to keep production costs and quantities private. To avoid these issues, we propose here a distributed iterative approach that reaches the minimum cost by decomposing the problem into local, reduced-complexity subproblems solved by the Gs with little information about the rest of the system.

III-A1 Identifying local subproblems

In order to decompose (3) into G subproblems, let us rewrite it in the following equivalent form

| (4) | ||||

| s. to | ||||

The idea is that, for each G, we first use the new variable to represent the energy sold by G- and only later we force it to be equal to all the energy bought by other Gs from G-, namely , the coupling constraint.

Due to the convexity properties of the primal problem (3) (or, equivalently, (4)), one can find the minimum cost by relaxing the coupling constraints and solving the dual problem

| (5) |

where with terms

| (6) | ||||

| s. to | ||||

In the last definition, which is a local minimization subproblem given the parameters , we introduced

| (7) |

that is the contribution of G- to the Lagrangian function relative to (4). The parameter vector gathers all the Lagrange multipliers corresponding to the coupling constraints , respectively and for all .

III-A2 Iterative dual problem solution

To solve the dual problem (5), we resort to the iterative subgradient method [32, Chapter 8], which basically finds a sequence that converges to the optimal point of the dual problem (5), namely . More specifically, for each point , each G minimizes its contribution to the Lagrangian function by solving the local subproblem (6) and determining the minimum point . Then, the Lagrange multipliers are updated according to

| (8) |

where is a positive step factor. Also, recall from (2) that the set of vectors can be readily derived knowing the set . Note that the vector is a subgradient of the dual concave function in , i.e. . Finally, (8) also says that can be updated at G- once the vector has been built with the inputs collected from the neighboring Gs.

III-A3 Interpretation—Market clearing

Algorithm 1 summarizes the distributed minimization procedure. One can readily notice that all necessary data is computed at the Gs, with no need for an external, centralized control unit. The information exchanged by the Gs is limited to the Lagrange multipliers and the demanded energies , computed at G- and communicated only to the corresponding G-. Both privacy and traffic limitations are hence satisfied.

As commented before, this algorithm allows for an interesting interpretation: each Lagrange multiplier may be understood as the price per energy unit requested by G- to sell energy to its neighbors. Then, the Lagrangian function (7) can be seen as the “net expenditure” (the opposite of the net income) for G-: each G pays for producing energy, for buying energy and for transporting the energy it buys. Conversely, the G is payed for the energy it sells. By solving problem (6) , G- is thus maximizing its benefit for some given selling () and buying () prices per energy unit. According to this view, the updating step (8) is clearing the market: prices should be modified until, globally, energy demand matches energy offer. Note that (8) is an example of the law of demand: if the energy offered by G- is less than all the energy demanded by the neighboring Gs from G-, that is , then the selling price must increase and .

III-B The G subproblem

In the previous section we have shown how the cost minimization problem (3) can be solved by means of successive iterations between the solution of local problems (6) and the update of the Lagrange multipliers according to (8). We will give now a closed-form solution to the local subproblem (6) to be solved by the generic G-.

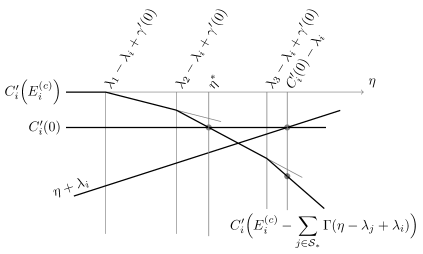

In order to keep notation as simple as possible, and without loss of generality, we assume that the Lagrange multipliers are ordered in increasing order, i.e. . Also, with some abuse of notation, we fix when : as far as G- is concerned, the fact that there is no connection from G- to G- is equivalent to assume that the price of the energy sold by G- is too high to be worth buying. Besides, we will make use of the functions and (the first derivatives of the cost functions and ) and of their inverse functions, respectively and . It is interesting to mention that, in economics, the derivative of a cost function is called the marginal cost (the cost of increasing infinitesimally the argument). To see this, consider for instance the generation cost function and assume that we increase production from to , with representing a small amount of energy. Then, the new generation cost can be approximated as

| (9) |

showing that the cost varies proportionally with and that the coefficient is . Note that can be either positive (more energy is produced for, e.g., selling purposes) or negative (because, e.g., some energy is bought from outside). Analogously, is the marginal transportation cost.

The solution to the minimization subproblem (6) at G- behaves according to six different cases. Each case is characterized by a specific relationship between the generation/transportation marginal costs and and the unitary selling/buying prices . We report next the mathematical definition of the six cases whereas, in Section III-C, some additional comments will help in grasping their electrical/economical meaning.

Case 1 (G- neither sells nor buys)

If and , then G- will decide to remain in a self-contained state and generate all and only the energy it consumes. Namely,

Case 2 (G- buys but neither generates nor sells)

Let us assume that and . Moreover, we can identify a partition of that satisfies the following assumptions:

-

•

it exists such that

-

for all ;

-

for all ;

-

is the unique positive solution to

-

-

•

either or and ;

-

•

for all , one has and

Then, G- buys all and only the energy it consumes, i.e. it neither generates nor sells any energy. More specifically

Case 3 (G- generates and buys but does not sell)

Let us assume that while and . Moreover, we can identify a partition of that satisfies the following assumptions:

-

•

it exists such that

-

for all ;

-

for all ;

-

is the unique positive solution to

-

-

•

either or and ;

-

•

either or and

Then, G- does not sell any energy. Furthermore, it buys some energy to supplement the local generator and feed all the loads. The exact amounts are as follows:

Case 4 (G- generates and sells but does not buy)

If and , then G- does not buy any energy. Conversely, it generates all the energy it needs plus some extra energy for the market. More specifically,

Case 5 (G- sells and buys but does not generate)

Assume that and . Also, let . Note that since, at least, . Then, G- does not generate any energy: it buys all the energy it consumes, plus some extra energy for the market, from all Gs in the set . The exact amounts are as follows:

Case 6 (G- sells, buys and generates)

Assume that , and

where we introduced the set . Then, the local generator is activated but G- also buys energy from all Gs in . After feeding all local loads with , some extra energy is left for selling in the market:

Proof:

The proof of these results is a cumbersome convex optimization exercise. From the Karush-Kuhn-Tucker conditions associated to (6), one must suppose all the different cases above and realize that the corresponding assumptions are necessary for each given case. Furthermore, one can also derive the exact values of all energy flows. Once all cases have been considered, a careful inspection shows that the derived necessary conditions form a partition of the hyperplane . Hence, the condition are also sufficient, along with necessary, and the proof is concluded. All the details are given in the appendix. ∎

As a final remark, note that we are assuming a positive load at the Gs, i.e. . The case where may be handled analogously and brings to similar results. More specifically, Cases 4, 5 and 6 extend directly because of continuity. Conversely, Cases 2 and 3 disappear and expand the domain of Case 1 to and .

III-C Interpretation and summary

It is interesting to note that the optimal solution provided in the previous section has a straightforward interpretation in economical terms. Recall that, at G-, the Lagrange multipliers can be interpreted as the unitary selling price () and the unitary buying prices from the other Gs (). Moreover, the derivatives and are the marginal generation cost and the marginal transportation cost, respectively, that is the linear variation on the cost due to an infinitesimal variation of the generated or transported energy, respectively.

Bearing this in mind, let us focus on Case 1. By means of (7) and (9), one readily realizes that G- is not interested in selling energy since the selling price is lower than the marginal production cost . Indeed, the income will be lower than the extra production cost, namely (the last inequality is due to the convexity of ). Similarly, buying is not profitable either since the minimum energy price is larger than the marginal benefit222When buying energy, the production cost reduces but the transportation cost increases. The marginal benefit with respect to —the G generates all and only the energy it consumes—is thus . . The conditions for Case 1 are hence justified. Analogous considerations hold for the other cases.

Another interesting point is that microgrids are always willing to trade since their local cost without trading, i.e. , will always be higher than their “net expenditure” in (7), where stands for the optimal point of (5). For the sake of brevity, we prove this result for Case 6 only, although the same reasoning holds true for the rest of cases. In Case 6, the “net expenditure” reads

where is now the minimum point of (6) for . Next, by means of the results of Case 6, one has and for all . Then, the equation above can be rewritten as follows:

with . Finally, since the cost functions are monotonically increasing and convex, it turns out that and , which leads to the desired result.

IV Numerical Results

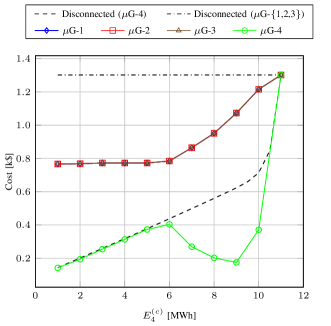

As for the numerical results, we have considered a system composed of four microgrids and, for simplicity, we have assumed the same generation cost function at all microgrids. More specifically, we have considered the U12 generator in [31], whose quadratic cost function has coefficients $, $/MWh and $/(MWh)2. Besides, as motivated in Section II-A, the original cost function has been multiplied by the function in order to include a soft constraint that accounts for the maximum energy generation MWh. Regarding the transfer cost function, we have modeled it as the cubic polynomial333 Note that this particular choice is arbitrary and this function may depend on physical parameters and the business model. However, similar results are expected with other setups. , with in MWh and in US dollars. Numerical results are given for the three topologies shown in Fig. 1: fully connected, ring and line.

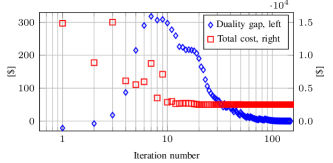

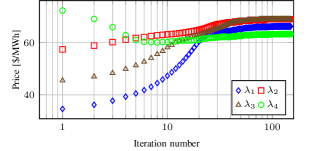

Fig. 2 assesses the convergence speed of the distributed minimization algorithm. The curves refer to a fully connected system where the microgrid loads are MWh. First, Fig. 2(a) shows the duality gap and the total cost of the system as a function of the iteration number. As we can observe, the algorithm converges (the duality gap is almost null) after a reasonable number of iterations. More interestingly, Fig. 2(b) shows the evolution of the selling prices. Note that the relationship between prices after convergence reflects the one between local loads: the more energy the G consumes locally, the higher its selling price is. While this is a natural consequence of the generation cost function being strictly increasing (if the local load is low, the G can generate extra energy for selling purposes at a lower cost), we can also see it as a manifestation of the law of demand. Indeed, the microgrid energy demand may be seen as composed by two terms, an internal one corresponding to the local loads and an external one from the other microgrids. The selling price will hence increase with the resulting total demand. Some more insights about how and how fast the algorithm converges can be found in [33]. There, only two microgrids are considered: such a simple case allows for a centralized closed-form solution and its direct comparison with the distributed approach.

Next, in order to get some more insight into the evolution of prices and energy flows, we consider a scenario where all local loads are held constant at 11 MWh (just above ), except for G-4, whose load varies from 1 to 11 MWh. In Figures 3(a), 4 and 5, for the four microgrids, we report the local cost after convergence , that is the minimum “net expenditure” (6), with the maximum point of (5). For benchmarking purposes, we have also depicted the costs at each microgrid in the disconnected case (i.e. when no trading is performed, the dashed lines). As shown in Section III-C, when using (7) as the local cost, we can observe that optimal trading always brings some benefit (cost reduction) to all microgrids.

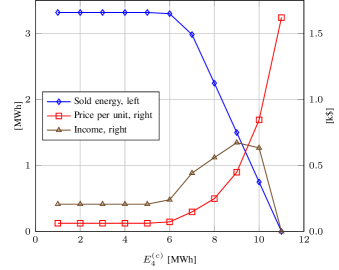

Let us now focus on the fully connected topology of Fig. 3. In Fig. 3(a) we see that the cost attained by G-4 after trading initially follows the cost of the disconnected microgrid. It is only when the local load grows above 6 MWh that the gain becomes noticeable, reaches its maximum for MWh and then decreases again until it becomes null at MWh. There, all Gs have the same internal demand and, for symmetry reasons, there is no energy exchange. The gain, indeed, is a result of the energy sold by G-4 to the other microgrids, whose amount, unit price and corresponding income is depicted in Fig. 3(b). At first sight, it may be disconcerting to see that the negligible gain obtained by G-4 for MWh is the result of selling a large amount of energy at a very low price (both almost constant for MWh). For MWh, however, the G sells less energy but the unit price increases fast enough to improve the gain (the “Income” curve): the best trade-off between the amount of energy sold by the G and its unit price is reached, as said before, for MWh. For larger values of , the high selling price cannot compensate for the decrease of sold energy and the income goes to zero.

To understand why this happens, let us consider G-4. After convergence, G-4 is defined by Case 4—generates and sells. Then, particularizing (7), the local costs at G-4 is

| (10) |

where we used the fact that we are assuming for . The optimal is given by the marginal cost, that is

| (11) |

Now, consider (10), (11) and recall that the cost function is the one with label “Disconnected (G-4)” in Fig. 3(a): for MWh approximately, the cost function is almost linear. Thus, the unit price (11) is nearly constant and so is the cost (10) as a function of for all and such that MWh. In other words, the G cost only depends on the consumed energy and not on the sold one since the income from selling some extra energy is canceled out by the extra cost needed to generate it. All these considerations are reflected by the curves in Figures 3(a) and 3(b) for MWh or, equivalently, MWh, since the total energy sold by G-4 in this regime is approximately 3 MWh.

Now, without loss of generality, let us focus on G-1. Note that, for symmetry reasons, G-1, G-2 and G-3 are all buying the same amount of energy from G-4 (namely, ) and they are not exchanging energy to one another. Intuitively, G-1 falls within Case 3—generates and buys—and its local cost is

The optimal price is given by (11) but, from G-1 perspective, can also be rewritten as

| (12) |

Let us neglect, for the moment, the transfer cost function . Also, recall that is again the one depicted in Fig. 3(a) with label “Disconnected (G-4)”. Since MWh, the production cost takes values above the curve elbow for all MWh, approximately. In this regime, the generation cost is very high and G-1 is certainly trying to buy energy to reduce its expenditure. For MWh, however, the generation cost takes values below the curve elbow and has an almost linear behavior (see also comments above). Then, it is not worth to buy more energy, since its price will cancel out the generation savings. The convex nature of the transfer cost function accentuates this trend. These considerations explain why MWh for all MWh.

For MWh, the four Gs work in the nonlinear part of the generation cost function. Matching the energy price at both the selling side (11) and the buying side (12) results in the trade-off of Fig. 3(b), which turns out to be quite fruitful for G-4. This fact compensates somehow for the little benefit (with respect to the benefits of the other Gs) experienced by G-4 at low values of .

Finally, let us recall that the purpose of the original problem (3) is to minimize the total cost of the system and not to maximize local benefits. This, together with the fact that we do not allow Gs to cheat, explains why G-4 always sells at a unit price given by the marginal cost and does not look for extra gains.

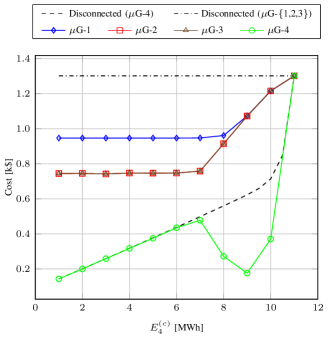

Even though the general ideas discussed above about the cost behaviors apply to all systems, connection topologies (see Fig. 1) other than the full connected one present some specific characteristics. For instance, Fig. 4 report the local cost for the four Gs in ring topology. We may see that G-2 and G-3 get some extra benefit from acting as intermediaries between G-4 and G-1. To be more precise, after the trading process, the local solutions at G- will fall within Case 6: energy is bought not only to satisfy internal needs but also to be resold to G-1. By doing so, G- can reduce their local cost substantially.

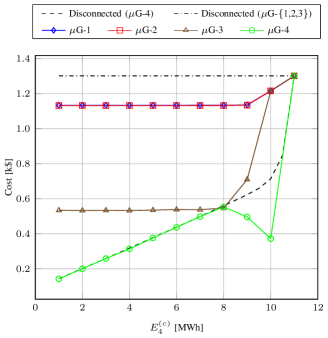

In Fig. 1(c) we depict another situation where topology heavily impacts on the costs. In this case, microgrids are connected by means of a line topology with G-4 at the end of the line. Therefore, G-3 can be regarded as the bottleneck of the system, since all the energy that goes from G-4 to G-{1,2} has to pass through it inevitably. As it can be observed in the figure, this situation benefits G-3.

V Conclusions

In this paper, we have addressed a problem in which several microgrids interact by exchanging energy in order to minimize the global operation cost, while still satisfying their local demands. In this context, we have proposed an iterative distributed algorithm that is scalable in the number of microgrids and keeps local cost functions and local consumption private. More specifically, each algorithm iteration consists of a local minimization step followed by a market clearing process. During the first step, each microgrid computes its local energy bid and reveals it to its potential sellers. Next, during the market clearing process, energy prices are adjusted according to the law of demand. As for the local optimization problem, it has been shown to have a closed form expression which lends itself to an economical interpretation. In particular, we have shown that no matter the local demand that a microgrid will be always willing to start the trading process since, eventually, its “net expenditure” will be lower than its local cost when operating on its own. Finally, numerical results have confirmed that the algorithm converges after a reasonable number of iterations and there certainly is a gain over nonconnected Gs which strongly depends on the energy demands and network topology.

Appendix A Solution to the Microgrid Problem

This appendix proves the solution to the G problem given in Section III-B. As explained before, we will suppose that the G best option is to operate in one of the six different states defined according to whether the G is (or is not) selling, buying and generating any energy, as described by the six cases of Section III-B. By doing so, one can compute all the energy values of interest and identify what constraints the prices must satisfy for the considered case to be feasible. After all cases have been considered, the six sets of necessary conditions should form a partition of the hyperplane. Indeed, this fact implies that each set of conditions is sufficient, along with necessary, for the corresponding G state and that the computed energy values are those minimizing the local cost function (7) for given prices .

Before delving into the different cases, some common preliminaries are needed. For the local problem (6) the Lagrangian function is as follows:

where we have introduced the Lagrange multipliers and . The KKT conditions hence write

| (13a) | |||

| (13b) | |||

| (13c) | |||

| (13d) | |||

| (13e) | |||

By recalling the definition of in Section II, the elements of the gradient in (13b) can be written in a much simpler form, namely

The derivation of the six possible solutions given in Section III-B is based on the analysis of the KKT conditions above, as explained hereafter.

A-A Proof of Case 1

Let us suppose that the solution of the minimization problem tells us that the G neither sells nor buys any energy, that is , and . If this was the case, then the KKT conditions (13) would write

The first condition implies

while the second condition yields

which are the two necessary conditions corresponding to Case 1.

A-B Proof of Case 2

We now look for the necessary conditions for Case 2, that is G- sells no energy (i.e. ) and buys energy from at least another G (i.e. ). Besides, G- generates no energy and . The KKT conditions (13) simplify to

| (14a) | |||||

| (14b) | |||||

| (14c) | |||||

| (14d) | |||||

| where we have introduced the sets | |||||

The first necessary condition is a straightforward consequence of (14a) and (14d). Next, for all , (14a) and (14b) imply

| (15) |

which means that

| (16) |

Similarly, because of (14a) and (14c), one has

By comparing the last two inequalities, one sees that for all , meaning that is certainly part of the set when this solution is correct.

From (15), and taking (16) into account, we can infer that

where is the inverse of , which exists because of the continuity and convexity assumptions on the cost function . Since we are supposing that the optimal working point satisfies , we see that shall satisfy the equality

| (17) |

Given that is an increasing function, and recalling (16), it can be easily shown that equation (17) in the variable has a unique solution, whose value allows us to compute the energies bought from neighbor G-, (compare with the statement of Case 2).

To derive the other necessary conditions for this case, let us focus on (17). Since is a non-negative function and , it follows:

Recalling that is the inverse of , this implies and, hence, is a necessary condition for Case 2.

Now, let , which is a subset of because of (16). Then, by comparison with (17),

where the second inequality is a consequence of being an increasing function. Also, we are letting , which is possible since for the considered . In particular, if then , as reported in Case 2. We will see later that this condition is important to identify the boundary between the solution regions of Case 2 and Case 5.

Consider now (14a) and (16), which give

and, in turn, a new necessary condition:

| (18) |

Moreover, (14a) and (17) yield

| (19) |

Substituting into (17), we can write the last necessary condition of Case 2, namely

| (20) |

Note that the left-hand side has a meaning according to (18). The last inequality may also be deduced from the graphical representation in Fig. 6.

A-C Proof of Case 3

We suppose again a solution where and for at least one . As opposed to the previous case, however, we also suppose that , i.e. G- produces some energy. With this solution, the Lagrange multiplier is zero and the KKT conditions become

| (21a) | |||||

| (21b) | |||||

| (21c) | |||||

| where, again, | |||||

Condition (21a) directly gives the first requirement for the case in hand, namely . Next, by combining (21a) and (21c), one has and, hence,

| (22) |

since . Similarly, (21a) and (21b) yield , which implies

| (23) |

since is an increasing function, and

| (24) |

where is the inverse of . Inequality (23) guarantees that is positive. Following, by injecting (24) into (21a), it turns out that must satisfy

| (25) |

It is straightforward to show that the last equation in admits a unique solution (see also the graphical representation in Fig. 7) that allows us to compute the energies bought from neighbor microgrids according to (24), as stated by Case 3. Also, knowing and recalling that is the inverse function of , (21a) allows us to compute the generated energy

Combining (25) with (23), we get for all and in particular for (see the statement of Case 3). We are particularly interested in since the corresponding microgrid will certainly belong to the set (and possibly be its only element) if this case is the solution to the minimization problem. This can be deduced by comparing (22) and (23).

Another necessary condition for this solution can be derived by noting that implies and, hence, . This bound requires and, together with (25), .

From (25) one further has . Then, again because of being increasing in ,

| (26) |

and, equivalently, , where we have introduced (see also Fig. 7). In particular, if then , which represents the complementary set of (20) in Case 2.

Finally, let . Then,

which is equivalent to . In particular, note that when and compare it with Case 6 below.

A-D Proof of Case 4

The next potential solution provides for all (G- does not buy any energy), and, obviously, (the G sells and generates some energy). According to the KKT conditions, we also have and

The first KKT condition can be satisfied only if (the first necessary condition for the current case). Moreover, combining both conditions, we get , which requires (the second necessary condition for the current case) in order to have .

The value taken by is obtained by inverting in the first condition above, namely . This also means .

A-E Proof of Case 5

We now analyze potential solutions of the type , for at least one index and . In other terms, the microgrid does not generate any energy but buys more than consumes and sells the surplus. In this case, the KKT conditions write

| (27a) | |||||

| (27b) | |||||

| (27c) | |||||

| where we have introduced the sets | |||||

Since , condition (27a) requires , the first necessary condition for the current case. Next, joining (27a) and (27c), we readily see that and

| (28) |

Similarly, (27a) and (27b) imply for all . By using the function , inverse of , the last equation allows computing the value of the energy bought from G-, namely , as we wanted to show. Note, however, that this is a meaningful expression only if for all . By comparing this last requirement with (28), we see that , which is the definition of the set as stated by Case 5.

Finally, the total sold energy is

Since we require , it must be , our last necessary condition (compare it with Case 2).

A-F Proof of Case 6

The last type of solution we have to deal with is characterized by , for at least one index and , i.e. G- generates, buys and sells certain positive amounts of energy. The KKT conditions become

| (29a) | |||||

| (29b) | |||||

| (29c) | |||||

| where we have introduced the sets | |||||

Condition (29a) directly implies (the first necessary condition for Case 6) because of the convexity assumptions on . Also, for all , the Lagrangian multipliers are given by (29a) and (29c), namely . This value is non-negative only if

| (30) |

On the other hand, (29a) and (29b) lead to for all . This identity allows us to express the quantity (the desired result), with the inverse of , provided that for all . This requirement, together with (30), results in the definition of for Case 6, namely .

To conclude, by means of the function , inverse of , (29a) is equivalent to or, also, , which are the required expressions of the total generated and sold energy, respectively. Note that this is a positive (and meaningful) quantity only if , the last necessary condition for Case 6 (compare also with Case 3).

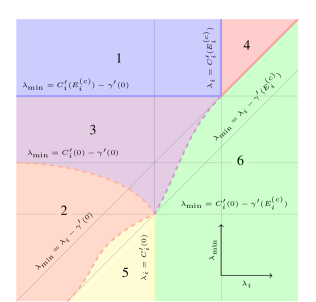

A-G Summary and remarks

So far, we have analyzed all the cases representing possible operating states for the microgrid. For each case we have found the corresponding values taken by the energy flows , and . Also, each case is characterized by a set of conditions that are necessary for the feasibility of the case itself. A close inspection of these conditions shows that they are mutually exclusive (see also the representation of Fig. 8). Thus, each set of conditions is also sufficient, together with necessary, for the respective solution case, meaning that the local minimization problem is univocally solved.

References

- [1] G. Andersson, P. Donalek, R. Farmer, N. Hatziargyriou, I. Kamwa, P. Kundur, N. Martins, J. Paserba, P. Pourbeik, J. Sanchez-Gasca, R. Schulz, A. Stankovic, C. Taylor, and V. Vittal, “Causes of the 2003 major grid blackouts in North America and Europe, and recommended means to improve system dynamic performance,” IEEE Trans. Power Syst., vol. 20, no. 4, pp. 1922–1928, 2005.

- [2] N. Hatziargyriou, H. Asano, R. Iravani, and C. Marnay, “Microgrids: An overview of ongoing research, development, and demonstration projects,” IEEE Power Energy Mag., vol. 5, no. 4, pp. 78–94, Jul./Aug. 2007.

- [3] I. Balaguer, Q. Lei, S. Yang, U. Supatti, and F. Z. Peng, “Control for grid-connected and intentional islanding operations of distributed power generation,” IEEE Trans. Ind. Electron., vol. 58, no. 1, pp. 147–157, Jan. 2011.

- [4] V. K. Sood, D. Fischer, J. M. Eklund, and T. Brown, “Developing a communication infrastructure for the smart grid,” in IEEE Electrical Power Energy Conference (EPEC), Oct. 2009, pp. 1–7.

- [5] F. Katiraei, R. Iravani, N. Hatziargyriou, and A. Dimeas, “Microgrids management,” IEEE Power Energy Mag., vol. 6, no. 3, pp. 54–65, May/Jun. 2008.

- [6] J. M. Guerrero, M. Chandorkar, T.-L. Lee, and P. C. Loh, “Advanced control architectures for intelligent microgrids - part I: Decentralized and hierarchical control,” IEEE Trans. Ind. Electron., vol. 60, no. 4, pp. 1254–1262, Apr. 2013.

- [7] J. M. Guerrero, P. C. Loh, T.-L. Lee, and M. Chandorkar, “Advanced control architectures for intelligent microgrids - part II: Power quality, energy storage, and AC/DC microgrids,” IEEE Trans. Ind. Electron., vol. 60, no. 4, pp. 1263–1270, Apr. 2013.

- [8] H. S. V. S. K. Nunna and S. Doolla, “Multiagent-based distributed-energy-resource management for intelligent microgrids,” IEEE Trans. Ind. Electron., vol. 60, no. 4, pp. 1678–1687, Apr. 2013.

- [9] M. Fathi and H. Bevrani, “Statistical cooperative power dispatching in interconnected microgrids,” IEEE Trans. Softw. Eng., vol. 4, no. 3, pp. 586–593, Jul. 2013.

- [10] L. F. Ochoa and G. P. Harrison, “Minimizing energy losses: Optimal accommodation and smart operation of renewable distributed generation,” IEEE Trans. Power Syst., vol. 26, no. 1, pp. 198–205, Feb. 2011.

- [11] S. Bruno, S. Lamonaca, G. Rotondo, U. Stecchi, and M. L. Scala, “Unbalanced three-phase optimal power flow for smart grids,” IEEE Trans. Ind. Electron., vol. 58, no. 10, pp. 4504–4513, Oct. 2011.

- [12] S. Paudyal, C. A. Cañizares, and K. Bhattacharya, “Three-phase distribution OPF in smart grids: Optimality versus computational burden,” in Innovative Smart Grid Technologies (ISGT Europe), 2011 2nd IEEE PES International Conference and Exhibition on, 2011, pp. 1–7.

- [13] B. H. Kim and R. Baldick, “Coarse-grained distributed optimal power flow,” IEEE Trans. Power Syst., vol. 12, no. 2, pp. 932–939, 1997.

- [14] R. Baldick, B. H. Kim, C. Chase, and Y. Luo, “A fast distributed implementation of optimal power flow,” IEEE Trans. Power Syst., vol. 14, no. 3, pp. 858–864, 1999.

- [15] M. Kraning, E. Chu, J. Lavaei, and S. Boyd, “Dynamic network energy management via proximal message passing,” Foundations and Trends in Optimization, vol. 1, no. 2, pp. 1–54, 2013.

- [16] E. Dall’Anese, H. Zhu, and G. B. Giannakis, “Distributed optimal power flow for smart microgrids,” IEEE Trans. Smart Grid, Accepted for publication.

- [17] T. Erseghe, “Distributed optimal power flow using ADMM,” IEEE Trans. Power Syst., to appear.

- [18] J. Lavaei and S. H. Low, “Zero duality gap in optimal power flow problem,” IEEE Trans. Power Syst., vol. 27, no. 1, pp. 92–107, 2012.

- [19] Z.-Q. Luo, W.-K. Ma, A. M.-C. So, Y. Ye, and S. Zhang, “Semidefinite relaxation of quadratic optimization problems,” IEEE Signal Process. Mag., vol. 27, no. 3, pp. 20–34, 2010.

- [20] S. Boyd, N. Parikh, E. Chu, B. Peleato, and J. Eckstein, “Distributed optimization and statistical learning via the alternating direction method of multipliers,” Foundations and Trends in Machine Learning, vol. 3, no. 1, pp. 1–122, 2010.

- [21] G. A. Pagani and M. Aiello, “Towards decentralization: A topological investigation of the medium and low voltage grids,” IEEE Trans. Smart Grid, vol. 2, no. 3, pp. 538–547, 2011.

- [22] Y. Wang, W. Saad, Z. Han, H. V. Poor, and T. Başar, “A game-theoretic approach to energy trading in the smart grid,” IEEE Trans. Smart Grid, vol. 5, no. 3, pp. 1439–1450, May 2014.

- [23] D. T. Nguyen, M. Negnevitsky, and M. de Groot, “Walrasian market clearing for demand response exchange,” IEEE Trans. Power Syst., vol. 27, no. 1, pp. 535–544, Feb. 2012.

- [24] M. Rahimiyan, L. Baringo, and A. J. Conejo, “Energy management of a cluster of interconnected price-responsive demands,” IEEE Trans. Power Syst., vol. 29, no. 2, pp. 645–655, Mar. 2014.

- [25] S. Kahrobaee, R. A. Rajabzadeh, L.-K. Soh, and S. Asgarpoor, “A multiagent modeling and investigation of smart homes with power generation, storage, and trading features,” IEEE Trans. Smart Grid, vol. 4, no. 2, pp. 659–668, Jun. 2013.

- [26] Z. Wang and L. Wang, “Adaptive negotiation agent for facilitating bi-directional energy trading between smart building and utility grid,” IEEE Trans. Smart Grid, vol. 4, no. 2, pp. 702–710, Jun. 2013.

- [27] A. L. Dimeas and N. D. Hatziargyriou, “Operation of a multiagent system for microgrid control,” IEEE Trans. Power Syst., vol. 20, no. 3, pp. 1447–1455, Aug. 2005.

- [28] H. S. V. S. K. Nunna and S. Doolla, “Demand response in smart distribution system with multiple microgrids,” IEEE Trans. Smart Grid, vol. 3, no. 4, pp. 1641–1649, Dec. 2012.

- [29] B. Ramachandran, S. K. Srivastava, C. S. Edrington, and D. A. Cartes, “An intelligent auction scheme for smart grid market using a hybrid immune algorithm,” IEEE Trans. Ind. Electron., vol. 58, no. 10, pp. 4603–4612, Oct. 2011.

- [30] A. Lenoir, “Modèles et algorithmes pour la planification de production à moyen terme en environnement incertain : Application de méthodes de décomposition proximales,” Ph.D. dissertation, Université Blaise Pascal – Clermont II, 2008.

- [31] (2008, Dec. 19) Three-phase, breaker-oriented IEEE 24-substation reliability test system: Generator data. School of Electrical and Computer Engineering at the Georgia Institute of Technology. [Online]. Available: http://pscal.ece.gatech.edu/testsys/generators.html

- [32] D. P. Bertsekas, Convex Analysis and Optimization. Nashua, NH, USA: Athena Scientific, 2003.

- [33] J. Matamoros, D. Gregoratti, and M. Dohler, “Microgrids energy trading in islanding mode,” in Proc. IEEE Third Int’l Conference on Smart Grid Communications (IEEE SmartGridComm 2012), Tainan City, Taiwan, Nov. 5–8, 2012.